Key Insights

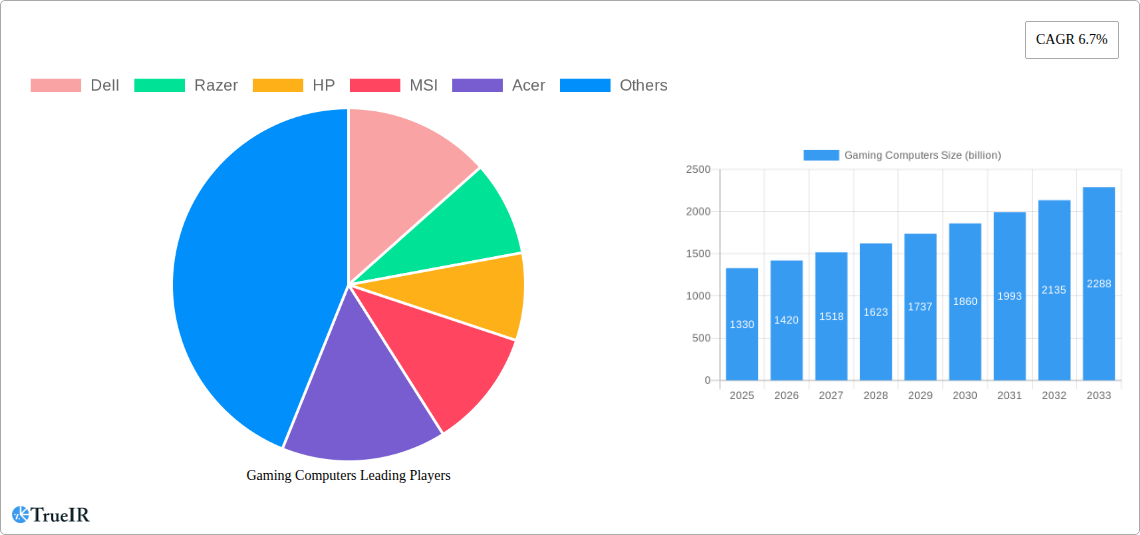

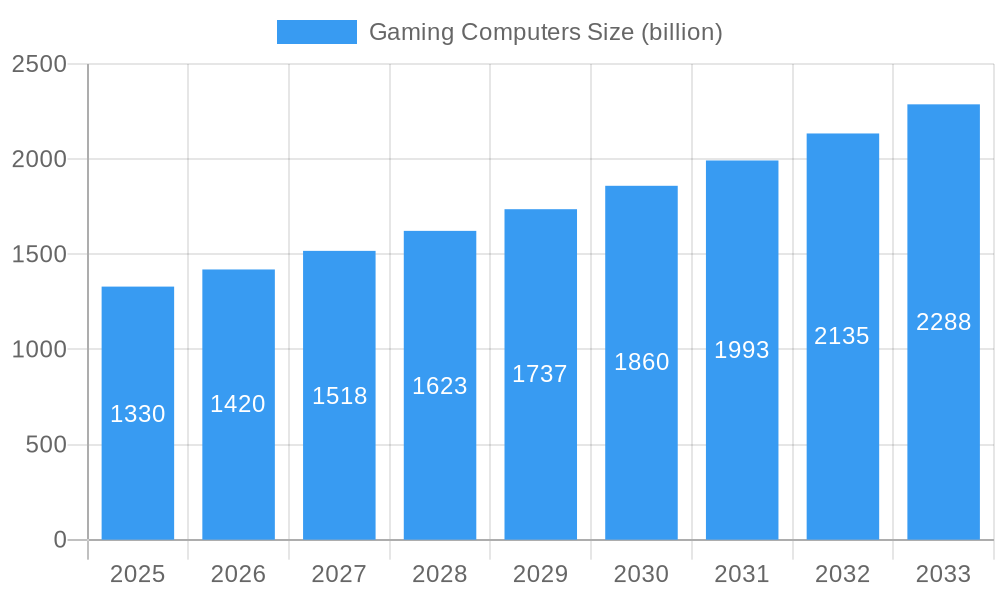

The global Gaming Computers market is poised for substantial growth, projected to reach an estimated $1.33 billion in 2025 and expand at a robust Compound Annual Growth Rate (CAGR) of 6.7% through 2033. This expansion is primarily fueled by the ever-increasing popularity of esports, the continuous evolution of game graphics and gameplay, and a growing global gaming community. The demand for high-performance hardware, capable of handling demanding AAA titles and immersive virtual reality experiences, is a significant driver. Furthermore, the increasing disposable income in emerging economies and the accessibility of gaming as a form of entertainment and social interaction are contributing to market penetration. Manufacturers are investing heavily in research and development to introduce innovative features, such as advanced cooling systems, customizable aesthetics, and AI-powered performance optimization, to cater to the sophisticated needs of modern gamers.

Gaming Computers Market Size (In Billion)

The market is segmented into Household and Commercial Use applications, with both segments showing promising growth trajectories. Within types, Gaming Desktops continue to command a significant share due to their raw power and upgradeability, while Gaming Laptops are witnessing rapid adoption owing to their portability and convenience, enabling gamers to enjoy high-fidelity experiences anytime, anywhere. Key players like Dell, Razer, HP, MSI, Acer, Asus, and Lenovo are intensely competing, driving innovation and offering a diverse range of products across different price points. Emerging trends such as the integration of cloud gaming technologies, the development of more powerful mobile gaming hardware, and the increasing focus on sustainable manufacturing practices are expected to shape the future landscape of the gaming computer industry. Despite the robust growth, potential supply chain disruptions and the high cost of premium components could present minor challenges.

Gaming Computers Company Market Share

Here is a dynamic, SEO-optimized report description for the Gaming Computers market, designed for immediate use and enhanced search visibility.

Gaming Computers Market Structure & Competitive Landscape

The global Gaming Computers market exhibits a dynamic and evolving structure, characterized by intense competition among a diverse range of players, from established multinational corporations to specialized boutique manufacturers. Market concentration is moderate, with the top five companies (Dell, Razer, HP, MSI, Acer, Asus, Lenovo, Samsung, Origin PC, Gigabyte Technology, EVGA, Eluktronics) collectively holding a significant, yet not fully dominant, share. Innovation serves as a primary driver, fueled by rapid advancements in processor technology (Intel), graphics processing units (Nvidia, AMD), display technology, and peripheral integration. Regulatory impacts are minimal, primarily revolving around import/export tariffs and consumer protection laws. Product substitutes, such as cloud gaming services, pose a growing but still nascent threat to dedicated hardware sales. End-user segmentation reveals a strong leaning towards the Household segment, driven by the pervasive growth of e-sports and home entertainment, though Commercial Use in gaming cafes and professional esports training facilities is a burgeoning niche. Merger and acquisition (M&A) trends are notable, with an estimated xx billion in M&A volumes over the historical period 2019-2024, indicating a consolidation phase and strategic realignments as companies seek to expand their product portfolios and market reach. The concentration ratio in key sub-segments is estimated at xx% for the top players.

Gaming Computers Market Trends & Opportunities

The Gaming Computers market is experiencing robust growth, projected to reach a valuation of over $100 billion by 2025, with a Compound Annual Growth Rate (CAGR) of approximately 15% projected through 2033. This expansion is driven by a confluence of significant technological shifts and evolving consumer preferences. The continuous innovation in high-performance components, including next-generation CPUs from Intel and advanced GPUs, is enabling more immersive and graphically demanding gaming experiences. The market penetration rate for gaming laptops has steadily increased, driven by their portability and increasingly powerful capabilities, now rivaling some desktop configurations. Similarly, the demand for high-refresh-rate displays and faster storage solutions continues to grow, pushing the boundaries of what's possible in home entertainment. Consumer preferences are increasingly shifting towards personalized and aesthetically customizable gaming rigs, leading to a rise in RGB lighting integration and modular component designs. The burgeoning e-sports industry is a monumental catalyst, creating a massive demand for top-tier gaming hardware that can support professional-level play. This surge in competitive gaming fuels the need for ultra-responsive peripherals, high-fidelity audio, and powerful systems capable of streaming and broadcasting simultaneously. The rise of virtual reality (VR) and augmented reality (AR) gaming further amplifies this demand, requiring even more potent processing power and specialized hardware. The integration of AI in gaming, both for in-game experiences and system optimization, is another significant trend that will shape future hardware requirements. Opportunities lie in the development of more affordable yet powerful entry-level gaming systems, catering to a wider demographic. Furthermore, the expansion of gaming communities and the growth of content creators on platforms like Twitch and YouTube necessitate powerful machines for streaming and video editing, presenting a significant avenue for market expansion. The increasing adoption of gaming computers for non-gaming applications, such as content creation, graphic design, and even scientific research, also broadens the market's appeal and revenue streams. The global market size for gaming computers was estimated at $60 billion in 2024 and is projected to reach $150 billion by 2033.

Dominant Markets & Segments in Gaming Computers

The Gaming Computers market is predominantly driven by the Household application segment, which accounts for an estimated 85% of global market revenue. This dominance is underpinned by the widespread accessibility of gaming as a form of entertainment, amplified by the exponential growth of e-sports and the increasing penetration of high-speed internet globally. The **Gaming Laptops** segment has emerged as a particularly strong growth area within this application, driven by evolving consumer lifestyles that prioritize flexibility and portability without compromising on performance. In 2025, the global market size for gaming computers is expected to be $100 billion.

Key Growth Drivers in the Household Segment:

- E-sports Phenomenon: The explosive popularity of professional e-sports tournaments and streaming platforms has created a strong demand for high-performance gaming hardware among both aspiring professionals and enthusiastic fans. Global e-sports viewership is projected to surpass 1 billion by 2027, significantly impacting hardware sales.

- Technological Advancements: Continuous innovation in CPUs, GPUs, and display technologies from industry giants like Intel and NVIDIA provides compelling upgrade cycles and attracts consumers seeking the latest immersive gaming experiences.

- Increasing Disposable Income: In many developed and emerging economies, rising disposable incomes allow a larger portion of the population to invest in premium gaming equipment.

- PC Gaming Revival: A resurgence in the popularity of PC gaming, fueled by a vast library of diverse titles and community engagement, further bolsters demand for dedicated gaming computers.

Gaming Computers Product Analysis

Product innovations in the Gaming Computers market are primarily centered on enhancing performance, visual fidelity, and user experience. Key advancements include the integration of multi-core processors like Intel's latest generations, powerful GPUs capable of real-time ray tracing, and ultra-fast NVMe SSDs for rapid load times. Gaming laptops are increasingly featuring high-refresh-rate OLED displays and advanced cooling systems to maintain peak performance. Competitive advantages are derived from a combination of raw processing power, optimized thermal management, sleek design aesthetics, and the integration of proprietary software for system control and customization. The increasing demand for immersive experiences, driven by VR and AAA titles, continues to push the boundaries of what gaming computers can deliver.

Key Drivers, Barriers & Challenges in Gaming Computers

Key Drivers:

The Gaming Computers market is propelled by several key factors. Technological advancements, particularly in CPU and GPU development by companies like Intel, are crucial, enabling more powerful and immersive gaming experiences. The burgeoning global e-sports industry acts as a significant economic driver, creating a sustained demand for high-performance hardware. Growing disposable incomes in emerging economies also contribute to market expansion by making gaming computers more accessible to a wider consumer base. Furthermore, government initiatives and investments in digital infrastructure in various regions are fostering a more conducive environment for the gaming industry.

Barriers & Challenges:

Despite robust growth, the market faces several challenges. Supply chain disruptions, exacerbated by geopolitical factors and component shortages, can lead to production delays and increased costs. Regulatory hurdles, such as import tariffs and varying consumer protection laws across different regions, can impact pricing and market access. Intense competitive pressure among established players and the emergence of new entrants also pose a challenge, often leading to price wars and pressure on profit margins. The high cost of premium gaming hardware can also be a barrier to entry for some consumer segments, limiting market penetration in price-sensitive regions.

Growth Drivers in the Gaming Computers Market

The Gaming Computers market is fueled by continuous technological innovation, with companies like Intel consistently releasing more powerful processors that enhance gaming performance and enable higher graphical fidelity. The rapid growth of the e-sports industry is a paramount driver, creating a global demand for top-tier gaming hardware from both aspiring professionals and passionate fans. As disposable incomes rise in emerging markets, gaming computers become more accessible, expanding the consumer base. Furthermore, the increasing prevalence of high-speed internet infrastructure globally facilitates online multiplayer gaming and streaming, further boosting hardware demand.

Challenges Impacting Gaming Computers Growth

The Gaming Computers market confronts significant challenges that can impede growth. Persistent global supply chain disruptions, particularly concerning critical components, lead to production delays and increased manufacturing costs. Navigating complex and diverse regulatory landscapes across different countries, including import duties and varying consumer protection laws, can create market access barriers and impact pricing strategies. Intense competition among numerous established and emerging brands often results in price wars, putting pressure on profit margins. Additionally, the high initial investment required for premium gaming computers can be a significant deterrent for price-sensitive consumers, limiting market penetration in certain demographics.

Key Players Shaping the Gaming Computers Market

- Dell

- Razer

- HP

- MSI

- Acer

- Asus

- Lenovo

- Samsung

- Origin PC

- Gigabyte Technology

- EVGA

- Eluktronics

- Intel

Significant Gaming Computers Industry Milestones

- 2019: Launch of NVIDIA GeForce RTX 30 Series GPUs, significantly enhancing real-time ray tracing capabilities.

- 2020: Release of AMD Ryzen 5000 series processors, offering substantial performance gains for gaming desktops.

- 2021: Increased demand for gaming laptops due to remote work and hybrid learning trends.

- 2022: Growth in custom PC building and the rise of boutique gaming PC manufacturers.

- 2023: Continued advancements in display technology, with wider adoption of 144Hz and higher refresh rates.

- 2024: Intel's introduction of new generation processors catering to mainstream and enthusiast gaming segments.

Future Outlook for Gaming Computers Market

The future outlook for the Gaming Computers market is exceptionally bright, driven by sustained technological innovation and the ever-expanding global gaming ecosystem. Key growth catalysts include the continued evolution of virtual and augmented reality technologies, which will demand more powerful and specialized hardware. The increasing sophistication of AI in gaming, both for in-game intelligence and system optimization, will also spur hardware upgrades. Furthermore, the persistent growth of e-sports and the creator economy will ensure a consistent demand for high-performance gaming machines. Strategic opportunities lie in the development of more energy-efficient yet powerful components, the expansion of customizable and modular PC designs, and the penetration of gaming hardware into emerging markets. The market potential remains substantial, with ongoing advancements promising to deliver even more immersive and integrated gaming experiences in the coming years.

Gaming Computers Segmentation

-

1. Application

- 1.1. Household

- 1.2. Commercial Use

-

2. Types

- 2.1. Gaming Desktops

- 2.2. Gaming Laptops

Gaming Computers Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

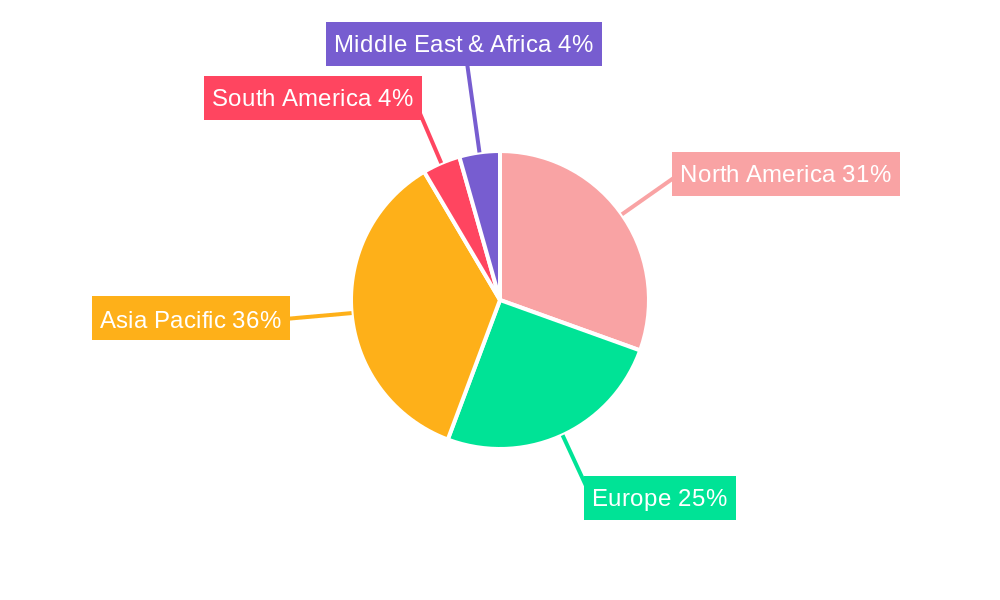

Gaming Computers Regional Market Share

Geographic Coverage of Gaming Computers

Gaming Computers REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Household

- 5.1.2. Commercial Use

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Gaming Desktops

- 5.2.2. Gaming Laptops

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Gaming Computers Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Household

- 6.1.2. Commercial Use

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Gaming Desktops

- 6.2.2. Gaming Laptops

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Gaming Computers Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Household

- 7.1.2. Commercial Use

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Gaming Desktops

- 7.2.2. Gaming Laptops

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Gaming Computers Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Household

- 8.1.2. Commercial Use

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Gaming Desktops

- 8.2.2. Gaming Laptops

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Gaming Computers Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Household

- 9.1.2. Commercial Use

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Gaming Desktops

- 9.2.2. Gaming Laptops

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Gaming Computers Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Household

- 10.1.2. Commercial Use

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Gaming Desktops

- 10.2.2. Gaming Laptops

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Gaming Computers Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Household

- 11.1.2. Commercial Use

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Gaming Desktops

- 11.2.2. Gaming Laptops

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Dell

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Razer

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 HP

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 MSI

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Acer

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Asus

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Lenovo

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Samsung

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Origin PC

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Gigabyte Technology

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 EVGA

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Eluktronics

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Intel

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.1 Dell

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Gaming Computers Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Gaming Computers Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Gaming Computers Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Gaming Computers Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Gaming Computers Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Gaming Computers Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Gaming Computers Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Gaming Computers Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Gaming Computers Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Gaming Computers Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Gaming Computers Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Gaming Computers Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Gaming Computers Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Gaming Computers Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Gaming Computers Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Gaming Computers Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Gaming Computers Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Gaming Computers Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Gaming Computers Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Gaming Computers Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Gaming Computers Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Gaming Computers Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Gaming Computers Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Gaming Computers Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Gaming Computers Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Gaming Computers Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Gaming Computers Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Gaming Computers Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Gaming Computers Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Gaming Computers Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Gaming Computers Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Gaming Computers Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Gaming Computers Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Gaming Computers Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Gaming Computers Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Gaming Computers Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Gaming Computers Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Gaming Computers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Gaming Computers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Gaming Computers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Gaming Computers Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Gaming Computers Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Gaming Computers Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Gaming Computers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Gaming Computers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Gaming Computers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Gaming Computers Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Gaming Computers Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Gaming Computers Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Gaming Computers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Gaming Computers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Gaming Computers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Gaming Computers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Gaming Computers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Gaming Computers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Gaming Computers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Gaming Computers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Gaming Computers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Gaming Computers Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Gaming Computers Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Gaming Computers Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Gaming Computers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Gaming Computers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Gaming Computers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Gaming Computers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Gaming Computers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Gaming Computers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Gaming Computers Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Gaming Computers Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Gaming Computers Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Gaming Computers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Gaming Computers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Gaming Computers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Gaming Computers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Gaming Computers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Gaming Computers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Gaming Computers Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Gaming Computers?

The projected CAGR is approximately 6.7%.

2. Which companies are prominent players in the Gaming Computers?

Key companies in the market include Dell, Razer, HP, MSI, Acer, Asus, Lenovo, Samsung, Origin PC, Gigabyte Technology, EVGA, Eluktronics, Intel.

3. What are the main segments of the Gaming Computers?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.33 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Gaming Computers," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Gaming Computers report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Gaming Computers?

To stay informed about further developments, trends, and reports in the Gaming Computers, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence