Key Insights

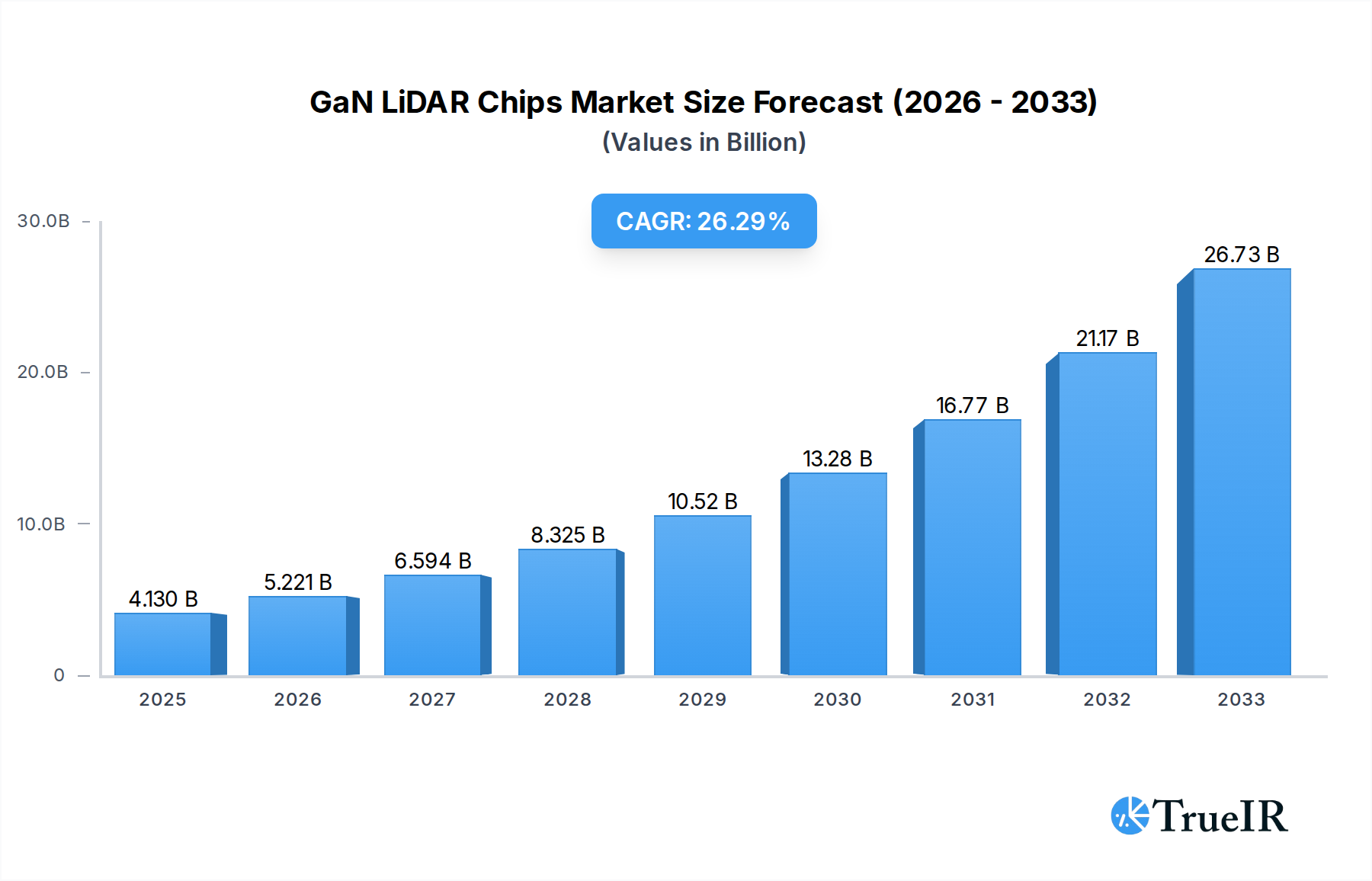

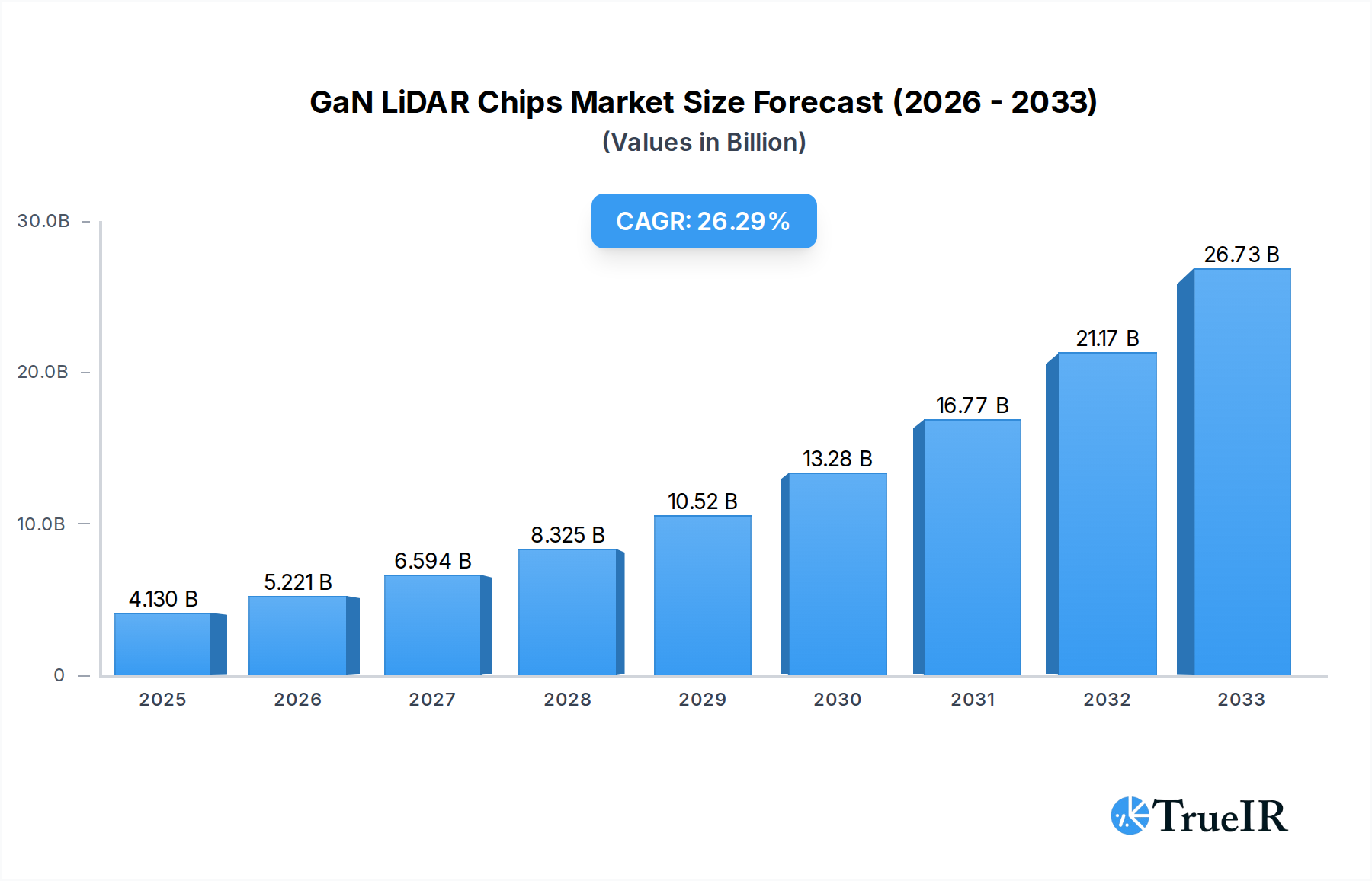

The GaN LiDAR Chips market is poised for remarkable expansion, projected to reach $4.13 billion by 2025. This surge is driven by the burgeoning demand for advanced sensing technologies across a multitude of industries, most notably in autonomous vehicles, robotics, and drones. Gallium Nitride (GaN) technology offers significant advantages over traditional silicon-based solutions, including higher power efficiency, improved performance at higher frequencies, and miniaturization capabilities, making GaN LiDAR chips ideal for these rapidly evolving applications. The substantial CAGR of 26.3% underscores the intense innovation and investment occurring within this sector. This growth trajectory is fueled by the continuous development of more sophisticated LiDAR systems that require smaller, more powerful, and more energy-efficient components. The increasing adoption of Level 3 and Level 4 autonomous driving systems, coupled with the expanding use of robots in logistics, manufacturing, and even consumer electronics, are directly translating into a heightened demand for these cutting-edge LiDAR chips.

GaN LiDAR Chips Market Size (In Billion)

The market's robust growth is further propelled by key trends such as the miniaturization of LiDAR sensors for integration into smaller devices and the development of solid-state LiDAR chips, which offer enhanced reliability and lower manufacturing costs compared to mechanical counterparts. While the adoption of GaN LiDAR chips faces some restraints, primarily related to the initial high cost of manufacturing and the need for further standardization within the industry, these challenges are being steadily addressed through ongoing research and development efforts and economies of scale. The competitive landscape is characterized by the presence of major players like Efficient Power Conversion, Texas Instruments, OSRAM Opto Semiconductors, and Innoscience, all actively engaged in developing and commercializing advanced GaN-based LiDAR solutions. These companies are investing heavily in R&D to enhance performance, reduce costs, and expand the application scope of GaN LiDAR chips, ensuring sustained innovation and market penetration across diverse segments including robots, autonomous vehicles, drones, and other emerging applications.

GaN LiDAR Chips Company Market Share

GaN LiDAR Chips Market Structure & Competitive Landscape

The GaN LiDAR chips market is characterized by a rapidly evolving structure, driven by intense innovation and a growing demand for advanced sensing solutions across multiple industries. Market concentration is moderate, with a few key players holding significant stakes, but the landscape is continually being reshaped by emerging technologies and strategic partnerships. Innovation drivers are primarily centered around increasing LiDAR performance metrics such as range, resolution, and power efficiency, with Gallium Nitride (GaN) technology proving instrumental in achieving these advancements. Regulatory impacts are beginning to be felt, particularly in the automotive sector, with increasing safety mandates pushing for wider LiDAR adoption. Product substitutes, though present in the form of radar and ultrasonic sensors, are finding it increasingly difficult to match the precision and comprehensive data provided by LiDAR, especially in complex environments. End-user segmentation reveals a strong demand from the autonomous vehicle sector, followed closely by robotics and drones. Mergers and acquisitions (M&A) are expected to play a crucial role in consolidating market share and fostering further innovation, with an estimated volume of over 10 M&A activities anticipated throughout the study period. Efficient Power Conversion, Texas Instruments, OSRAM Opto Semiconductors, and Innoscience are at the forefront of this dynamic market, actively pursuing technological leadership and strategic collaborations.

GaN LiDAR Chips Market Trends & Opportunities

The global GaN LiDAR chips market is projected for monumental growth, witnessing an impressive Compound Annual Growth Rate (CAGR) of over 25% throughout the forecast period of 2025–2033. This surge is primarily fueled by the transformative potential of Gallium Nitride (GaN) technology in enhancing LiDAR system capabilities. GaN's superior electron mobility and thermal conductivity enable smaller, more power-efficient, and higher-performance LiDAR chips, directly addressing the critical needs of emerging applications. The market size is expected to expand from an estimated base year value of $1.5 billion in 2025 to exceed $10 billion by 2033, underscoring a significant market penetration rate in key sectors.

Technological shifts are predominantly leaning towards solid-state LiDAR designs, which offer greater reliability, reduced cost, and smaller form factors compared to their mechanical counterparts. This transition is a major opportunity for GaN-based solutions, as they are inherently well-suited for solid-state architectures, including Flash LiDAR and MEMS LiDAR. Consumer preferences, particularly in the automotive industry, are increasingly prioritizing enhanced safety features and advanced driver-assistance systems (ADAS), directly driving demand for sophisticated sensing technologies like LiDAR. The continued advancement in autonomous driving capabilities, from Level 3 to Level 5 autonomy, will necessitate a widespread deployment of LiDAR sensors, making it an indispensable component for future mobility.

The competitive dynamics are intensifying as established semiconductor giants and specialized LiDAR technology developers vie for market dominance. Significant investment in research and development by companies like Efficient Power Conversion, Texas Instruments, OSRAM Opto Semiconductors, and Innoscience is leading to rapid product advancements and the introduction of next-generation GaN LiDAR chips. These innovations are not only improving performance metrics like range and resolution but also reducing the overall cost of LiDAR systems, making them more accessible for mass-market adoption. The growing ecosystem of LiDAR component suppliers and system integrators further contributes to market expansion, creating opportunities for specialized niche players and fostering collaborative innovation. The broader integration of LiDAR into diverse applications beyond automotive, such as industrial automation, smart city infrastructure, and advanced robotics, is opening up new revenue streams and market segments, further solidifying the positive growth trajectory of the GaN LiDAR chips market.

Dominant Markets & Segments in GaN LiDAR Chips

The Autonomous Vehicles segment is unequivocally the dominant force shaping the GaN LiDAR chips market, with its market share projected to remain consistently above 45% throughout the forecast period. This dominance stems from the critical role LiDAR plays in enabling advanced driver-assistance systems (ADAS) and fully autonomous driving functionalities. The increasing stringency of automotive safety regulations and the competitive race among automakers to deploy Level 3 and higher autonomous capabilities are significant growth drivers. Furthermore, the development of sophisticated infrastructure for autonomous mobility, including dedicated lanes and smart traffic management systems, indirectly bolsters the demand for robust LiDAR solutions.

Within the Types of LiDAR chips, Solid-state LiDAR Chips are experiencing exponential growth, expected to capture over 70% of the market by 2033. This shift is propelled by their inherent advantages in reliability, cost-effectiveness, and miniaturization, making them ideal for mass-market automotive applications. GaN technology is a key enabler of these solid-state designs, facilitating the development of compact and high-performance solutions.

Robotics represents another significant and rapidly expanding segment, with an anticipated CAGR of over 28%. The increasing adoption of robots in manufacturing, logistics, and warehousing, coupled with the growing demand for autonomous mobile robots (AMRs) and collaborative robots, are primary growth drivers. Enhanced environmental perception and navigation capabilities provided by LiDAR are crucial for improving the efficiency and safety of robotic operations.

The Drone segment, while currently smaller in market share compared to automotive and robotics, is poised for substantial growth with a CAGR exceeding 30%. The expanding applications of drones in aerial surveying, inspection, delivery, and security are directly fueling the demand for advanced sensing technologies. GaN LiDAR chips offer the necessary lightweight, power-efficient, and high-resolution sensing required for next-generation drone platforms.

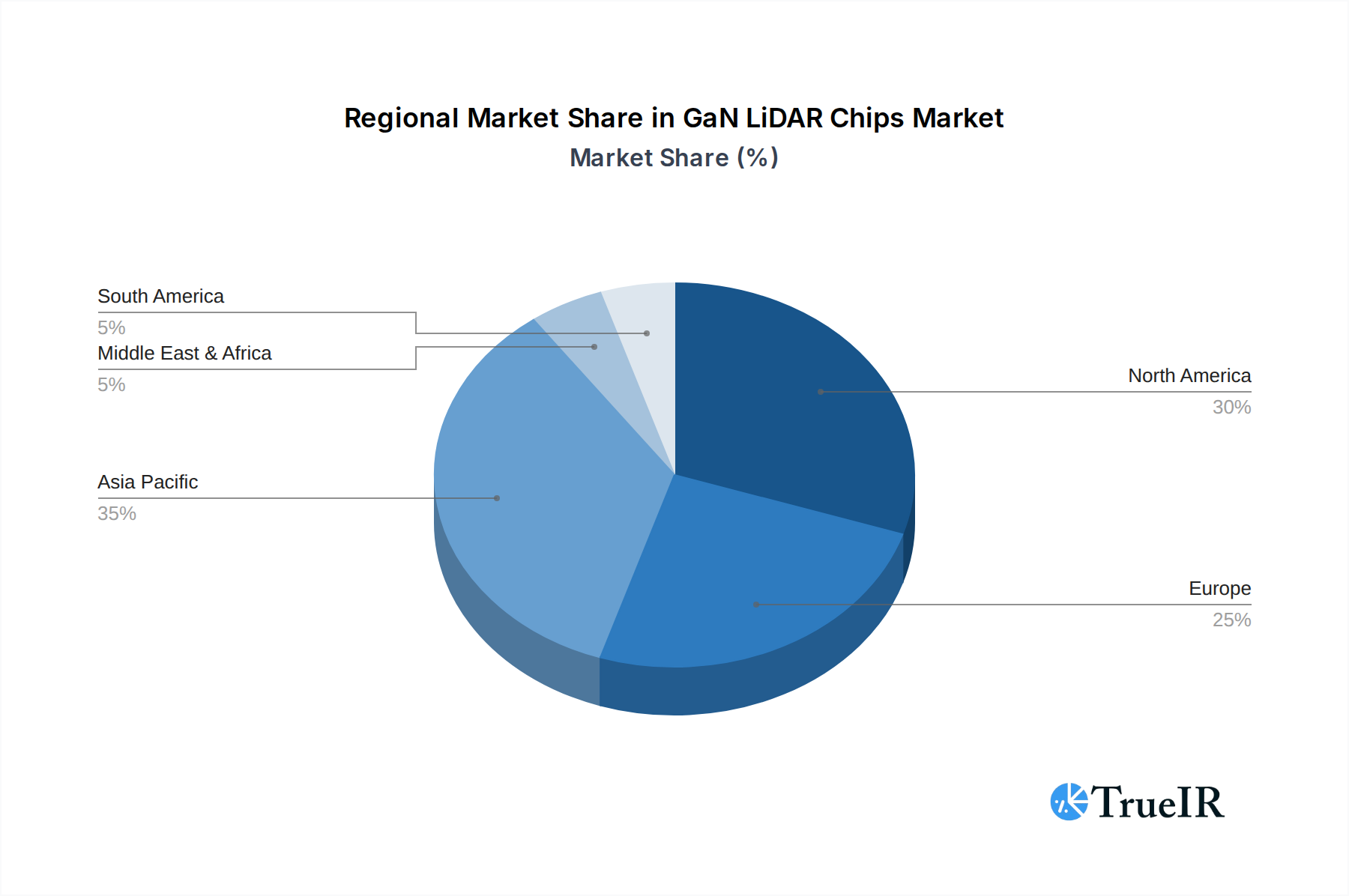

Geographically, North America is expected to lead the market, driven by its advanced automotive industry, significant investments in autonomous vehicle development, and strong government support for technological innovation. Stringent safety standards and a proactive approach to adopting new mobility solutions contribute to its dominant position. Europe follows closely, fueled by similar automotive advancements and a growing emphasis on smart city initiatives and industrial automation. Asia Pacific, particularly China, is emerging as a crucial growth engine due to its massive automotive market, rapid industrialization, and government-backed initiatives in AI and robotics.

GaN LiDAR Chips Product Analysis

GaN LiDAR chips represent a paradigm shift in sensing technology, offering unparalleled performance for applications demanding high accuracy and reliability. These chips leverage the inherent advantages of Gallium Nitride, including its high breakdown voltage, high electron mobility, and excellent thermal conductivity. This enables the creation of smaller, more power-efficient, and robust LiDAR systems. Product innovations are focused on enhancing range, resolution, and field-of-view while simultaneously reducing power consumption and cost. The competitive advantage lies in the ability to integrate sophisticated functionalities onto a single chip, facilitating the widespread adoption of solid-state LiDAR solutions for autonomous vehicles, robotics, and drones.

Key Drivers, Barriers & Challenges in GaN LiDAR Chips

Key Drivers, Barriers & Challenges in GaN LiDAR Chips

Key Drivers: The GaN LiDAR chips market is propelled by several key drivers. The escalating demand for advanced driver-assistance systems (ADAS) and autonomous driving capabilities in the automotive sector is paramount, with stringent safety regulations mandating sophisticated perception systems. The burgeoning robotics industry, from industrial automation to logistics, requires precise navigation and environmental understanding. Furthermore, the expanding applications of drones in diverse fields like delivery, surveillance, and inspection are creating significant market pull. Technological advancements in GaN material science and fabrication processes are continuously improving performance metrics and reducing costs, making LiDAR more accessible.

Challenges Impacting GaN LiDAR Chips Growth: Despite the promising outlook, the GaN LiDAR chips market faces several challenges. The high initial cost of LiDAR systems, although decreasing, remains a barrier to mass adoption in some segments. Complex regulatory frameworks and standardization issues, particularly for autonomous vehicles, can slow down market penetration. Supply chain complexities and the availability of raw materials for GaN chip manufacturing can impact production volumes and lead times. Intense competition among established and emerging players necessitates continuous innovation and strategic pricing, while the development of reliable and cost-effective manufacturing processes at scale remains a critical hurdle.

Growth Drivers in the GaN LiDAR Chips Market

The growth of the GaN LiDAR chips market is significantly driven by the relentless pursuit of enhanced safety and autonomy in the automotive industry, pushing for wider deployment of LiDAR in ADAS and self-driving vehicles. The increasing adoption of robotics in various sectors, from manufacturing to logistics, relies heavily on accurate spatial perception provided by LiDAR for efficient navigation and task execution. Expanding drone applications in aerial mapping, delivery, and security are also creating substantial demand for lightweight and powerful sensing solutions. Technological advancements in GaN materials, leading to higher performance and lower costs, are crucial catalysts, enabling more compact and power-efficient LiDAR systems.

Challenges Impacting GaN LiDAR Chips Growth

Challenges impacting GaN LiDAR chips growth include the high upfront cost of LiDAR systems, which, despite ongoing reductions, can still be a deterrent for certain applications and consumer markets. Regulatory hurdles and the slow pace of standardization for autonomous driving technologies can create uncertainty and delay widespread adoption. Supply chain constraints, including the availability of specialized raw materials and advanced manufacturing capabilities for GaN components, can affect production scalability and lead times. Moreover, intense competition and the need for continuous innovation to maintain a competitive edge present ongoing strategic challenges for market players.

Key Players Shaping the GaN LiDAR Chips Market

Efficient Power Conversion Texas Instruments OSRAM Opto Semiconductors Innoscience Velodyne Lidar Luminar Technologies Innoviz Technologies Aeva Technologies Waymo Ouster

Significant GaN LiDAR Chips Industry Milestones

- 2020: Efficient Power Conversion announces a breakthrough in GaN technology for LiDAR applications, enabling higher power density and performance.

- 2021: Texas Instruments introduces a new family of GaN-based LiDAR ICs designed for automotive and industrial applications.

- 2022: OSRAM Opto Semiconductors expands its portfolio of high-performance laser diodes for LiDAR systems, leveraging advanced semiconductor materials.

- 2022: Innoscience showcases its next-generation GaN power transistors, crucial for the efficient operation of high-power LiDAR systems.

- 2023: Luminar Technologies partners with a major automotive OEM to integrate its LiDAR technology into production vehicles, signaling increased industry adoption.

- 2023: Velodyne Lidar unveils its new Puck V3 sensor, offering improved range and resolution for a variety of applications.

- 2024: Aeva Technologies announces significant advancements in its Frequency Modulated Continuous Wave (FMCW) LiDAR technology, promising enhanced object detection capabilities.

- 2024: Waymo begins widespread testing of its fifth-generation autonomous driving system, heavily reliant on its advanced LiDAR sensor suite.

- 2024: Regulatory bodies in key automotive markets begin to release draft standards for LiDAR performance and safety, influencing product development.

- 2025: Anticipated launch of the first mass-produced vehicles featuring integrated GaN-based solid-state LiDAR systems.

Future Outlook for GaN LiDAR Chips Market

The future outlook for the GaN LiDAR chips market is exceptionally bright, driven by an accelerating integration into mainstream automotive applications and the proliferation of LiDAR in robotics, drones, and industrial automation. Strategic opportunities lie in the continued miniaturization and cost reduction of GaN LiDAR solutions, making them accessible for a wider array of consumer electronics and IoT devices. Advancements in AI and machine learning algorithms for LiDAR data processing will unlock new functionalities and enhance the overall utility of these sensing systems. The market potential is vast, with GaN LiDAR poised to become an indispensable component in creating safer, more intelligent, and autonomous environments across diverse industries.

GaN LiDAR Chips Segmentation

-

1. Application

- 1.1. Robot

- 1.2. Autonomous Vehicles

- 1.3. Drone

- 1.4. Others

-

2. Types

- 2.1. Mechanical Lidar Chips

- 2.2. Solid-state Lidar Chips

GaN LiDAR Chips Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

GaN LiDAR Chips Regional Market Share

Geographic Coverage of GaN LiDAR Chips

GaN LiDAR Chips REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 26.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Robot

- 5.1.2. Autonomous Vehicles

- 5.1.3. Drone

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Mechanical Lidar Chips

- 5.2.2. Solid-state Lidar Chips

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global GaN LiDAR Chips Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Robot

- 6.1.2. Autonomous Vehicles

- 6.1.3. Drone

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Mechanical Lidar Chips

- 6.2.2. Solid-state Lidar Chips

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America GaN LiDAR Chips Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Robot

- 7.1.2. Autonomous Vehicles

- 7.1.3. Drone

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Mechanical Lidar Chips

- 7.2.2. Solid-state Lidar Chips

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America GaN LiDAR Chips Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Robot

- 8.1.2. Autonomous Vehicles

- 8.1.3. Drone

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Mechanical Lidar Chips

- 8.2.2. Solid-state Lidar Chips

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe GaN LiDAR Chips Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Robot

- 9.1.2. Autonomous Vehicles

- 9.1.3. Drone

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Mechanical Lidar Chips

- 9.2.2. Solid-state Lidar Chips

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa GaN LiDAR Chips Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Robot

- 10.1.2. Autonomous Vehicles

- 10.1.3. Drone

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Mechanical Lidar Chips

- 10.2.2. Solid-state Lidar Chips

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific GaN LiDAR Chips Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Robot

- 11.1.2. Autonomous Vehicles

- 11.1.3. Drone

- 11.1.4. Others

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Mechanical Lidar Chips

- 11.2.2. Solid-state Lidar Chips

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Efficient Power Conversion

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Texas Instruments

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 OSRAM Opto Semiconductors

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Innoscience

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.1 Efficient Power Conversion

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global GaN LiDAR Chips Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America GaN LiDAR Chips Revenue (billion), by Application 2025 & 2033

- Figure 3: North America GaN LiDAR Chips Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America GaN LiDAR Chips Revenue (billion), by Types 2025 & 2033

- Figure 5: North America GaN LiDAR Chips Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America GaN LiDAR Chips Revenue (billion), by Country 2025 & 2033

- Figure 7: North America GaN LiDAR Chips Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America GaN LiDAR Chips Revenue (billion), by Application 2025 & 2033

- Figure 9: South America GaN LiDAR Chips Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America GaN LiDAR Chips Revenue (billion), by Types 2025 & 2033

- Figure 11: South America GaN LiDAR Chips Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America GaN LiDAR Chips Revenue (billion), by Country 2025 & 2033

- Figure 13: South America GaN LiDAR Chips Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe GaN LiDAR Chips Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe GaN LiDAR Chips Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe GaN LiDAR Chips Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe GaN LiDAR Chips Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe GaN LiDAR Chips Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe GaN LiDAR Chips Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa GaN LiDAR Chips Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa GaN LiDAR Chips Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa GaN LiDAR Chips Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa GaN LiDAR Chips Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa GaN LiDAR Chips Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa GaN LiDAR Chips Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific GaN LiDAR Chips Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific GaN LiDAR Chips Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific GaN LiDAR Chips Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific GaN LiDAR Chips Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific GaN LiDAR Chips Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific GaN LiDAR Chips Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global GaN LiDAR Chips Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global GaN LiDAR Chips Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global GaN LiDAR Chips Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global GaN LiDAR Chips Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global GaN LiDAR Chips Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global GaN LiDAR Chips Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States GaN LiDAR Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada GaN LiDAR Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico GaN LiDAR Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global GaN LiDAR Chips Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global GaN LiDAR Chips Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global GaN LiDAR Chips Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil GaN LiDAR Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina GaN LiDAR Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America GaN LiDAR Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global GaN LiDAR Chips Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global GaN LiDAR Chips Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global GaN LiDAR Chips Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom GaN LiDAR Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany GaN LiDAR Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France GaN LiDAR Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy GaN LiDAR Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain GaN LiDAR Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia GaN LiDAR Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux GaN LiDAR Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics GaN LiDAR Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe GaN LiDAR Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global GaN LiDAR Chips Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global GaN LiDAR Chips Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global GaN LiDAR Chips Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey GaN LiDAR Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel GaN LiDAR Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC GaN LiDAR Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa GaN LiDAR Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa GaN LiDAR Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa GaN LiDAR Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global GaN LiDAR Chips Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global GaN LiDAR Chips Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global GaN LiDAR Chips Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China GaN LiDAR Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India GaN LiDAR Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan GaN LiDAR Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea GaN LiDAR Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN GaN LiDAR Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania GaN LiDAR Chips Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific GaN LiDAR Chips Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the GaN LiDAR Chips?

The projected CAGR is approximately 26.3%.

2. Which companies are prominent players in the GaN LiDAR Chips?

Key companies in the market include Efficient Power Conversion, Texas Instruments, OSRAM Opto Semiconductors, Innoscience.

3. What are the main segments of the GaN LiDAR Chips?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 4.13 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "GaN LiDAR Chips," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the GaN LiDAR Chips report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the GaN LiDAR Chips?

To stay informed about further developments, trends, and reports in the GaN LiDAR Chips, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence