Key Insights

The High Performance Plastics for Semiconductor Equipment market is projected to reach $5.7 billion by 2025, exhibiting a Compound Annual Growth Rate (CAGR) of 11.13% from 2025 to 2033. This significant expansion is driven by the increasing demand for advanced semiconductor devices in consumer electronics, automotive, and telecommunications. The ongoing trends in miniaturization, enhanced processing power, and energy efficiency necessitate specialized materials capable of withstanding extreme manufacturing conditions. High-performance plastics are crucial for semiconductor fabrication processes, including vacuum chambers and wet processing, due to their superior chemical resistance, thermal stability, low outgassing, and mechanical strength. The complexity of wafer fabrication and stringent purity demands are spurring innovation in advanced polymer solutions.

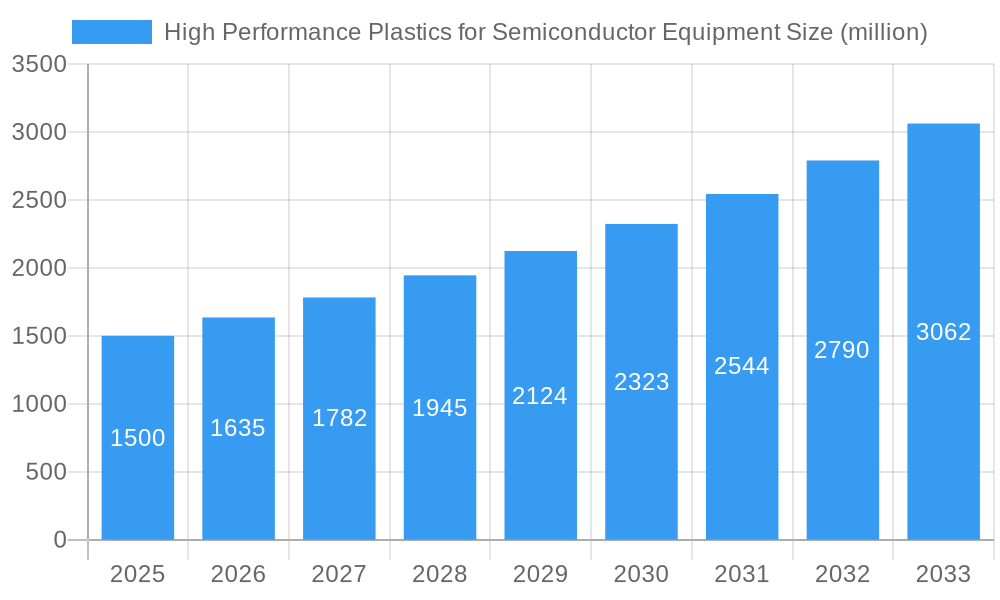

High Performance Plastics for Semiconductor Equipment Market Size (In Billion)

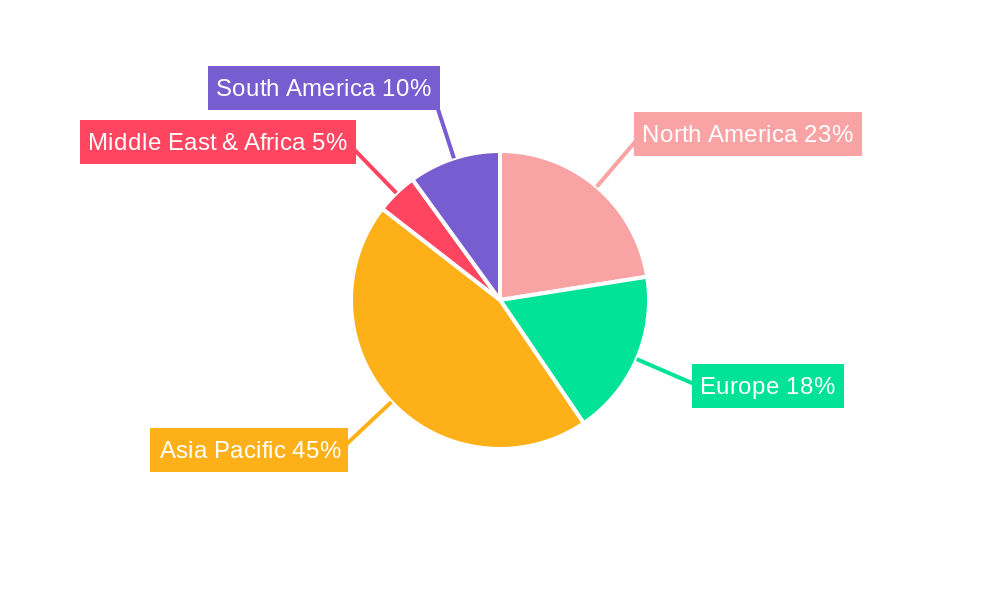

Key market drivers include substantial capital expenditure in the semiconductor industry, continuous advancements in chip manufacturing technology, and the widespread adoption of Industry 4.0 solutions. The expansion of 5G infrastructure and the proliferation of Artificial Intelligence (AI) applications further elevate the demand for these specialized plastics. Potential restraints include the high cost of certain advanced polymers and rigorous material qualification processes. However, ongoing research and development by leading companies are focused on delivering cost-effective, high-performance solutions. The market is segmented by application, with Vacuum Chamber and Wet Process segments showing strong demand. Asia Pacific, led by China and South Korea, is anticipated to lead the market due to its extensive semiconductor manufacturing capabilities, followed by North America and Europe.

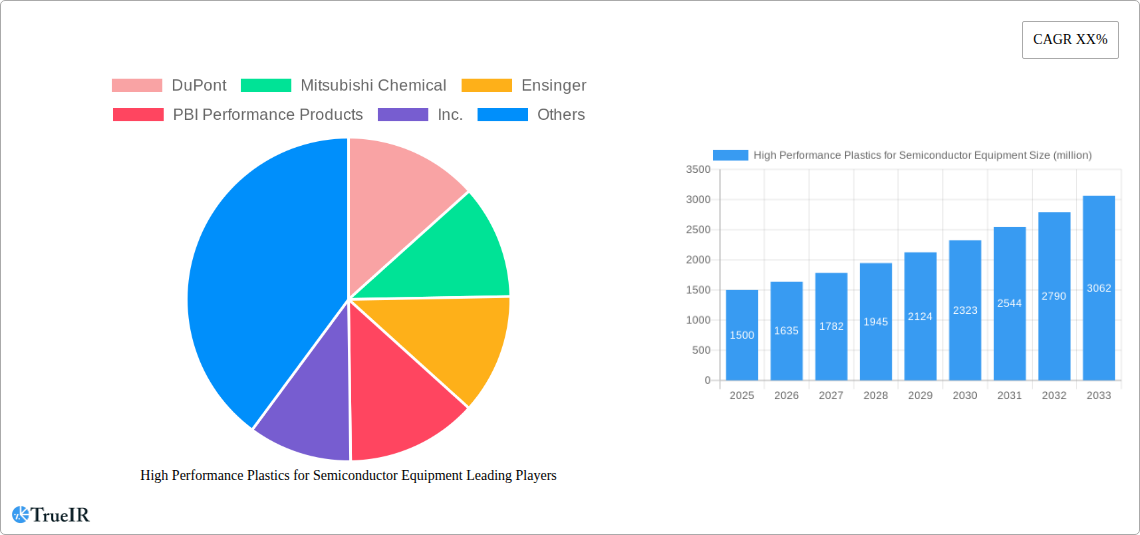

High Performance Plastics for Semiconductor Equipment Company Market Share

High Performance Plastics for Semiconductor Equipment: Market Insights, Trends, and Forecasts (2019–2033)

Report Description:

Unlock comprehensive insights into the rapidly evolving High Performance Plastics for Semiconductor Equipment market. This in-depth report, covering the study period of 2019–2033 with a base year of 2025, delivers critical data and analysis for stakeholders navigating this high-growth sector. Explore market structure, competitive landscape, dominant trends, and future opportunities shaping the semiconductor manufacturing equipment industry. We delve into the specific applications of these advanced materials, including vacuum chamber components (etch, vapor deposition, ion implant), wet process applications (cleaning, PVD, wet etch, ECD), dry environments & ESD protection, CMP (retainer rings), vacuum pumps, valves, and wafer handling systems.

The report meticulously analyzes the market penetration of key plastic types such as PPS, PEEK, PI (Polyimide/PAI), PC, PTFE, PBI, PEI, and other advanced polymers. Through quantitative and qualitative analysis, understand market concentration, innovation drivers, regulatory impacts, product substitutes, end-user segmentation, and M&A trends. Leverage data-driven forecasts and trend analysis, including compound annual growth rates (CAGR), to inform strategic decision-making. This report is essential for semiconductor material suppliers, equipment manufacturers, process engineers, and investment analysts seeking to capitalize on the growth of semiconductor manufacturing and the increasing demand for high-performance materials.

High Performance Plastics for Semiconductor Equipment Market Structure & Competitive Landscape

The High Performance Plastics for Semiconductor Equipment market exhibits a moderately concentrated structure, with a significant portion of the market share held by a few established global players. Innovation serves as a primary driver, with companies continuously investing in research and development to create novel materials with enhanced properties like superior thermal stability, chemical resistance, and mechanical strength, crucial for the demanding semiconductor fabrication environment. Regulatory impacts, particularly concerning environmental standards and material certifications for cleanroom applications, influence product development and market entry strategies. Product substitutes, such as advanced ceramics and specialized metals, exist, but high-performance plastics often offer a compelling balance of cost-effectiveness, processability, and performance for specific applications. End-user segmentation is critical, with distinct material requirements for applications ranging from vacuum environments to corrosive wet chemical processing. Mergers and acquisitions (M&A) are an emerging trend, as larger players seek to consolidate their market position, acquire new technologies, or expand their product portfolios. For instance, an estimated 10-15 significant M&A deals, with an aggregate transaction value in the hundreds of millions of dollars, have been observed over the historical period. Concentration ratios for the top five players are estimated to be around 50-60%.

High Performance Plastics for Semiconductor Equipment Market Trends & Opportunities

The global High Performance Plastics for Semiconductor Equipment market is experiencing robust growth, projected to reach an estimated market size of over $30 million by the end of the forecast period in 2033. This expansion is fundamentally driven by the insatiable global demand for advanced semiconductors, fueling continuous expansion and upgrades within the semiconductor manufacturing industry. The fifth generation wireless (5G) technology rollout, the proliferation of artificial intelligence (AI) and machine learning (ML) applications, and the increasing sophistication of consumer electronics and automotive electronics are all significant contributors to this sustained demand. These trends necessitate the development and deployment of next-generation semiconductor fabrication equipment, which, in turn, requires materials capable of withstanding increasingly stringent process conditions, including higher temperatures, more aggressive chemical environments, and ultra-high vacuum (UHV) requirements.

Technological shifts are paramount, with a growing emphasis on plastics that offer superior purity, reduced outgassing, and enhanced tribological properties. For instance, PEEK (Polyether Ether Ketone) and PI (Polyimide/PAI) are gaining prominence due to their exceptional thermal resistance and chemical inertness, making them ideal for critical components in wafer handling systems and vacuum chambers. The development of specialized grades of PPS (Polyphenylene Sulfide) with enhanced purity for etch and deposition processes is another notable trend. Consumer preferences, though indirect, are pushing the boundaries of semiconductor performance, demanding smaller, more powerful, and energy-efficient chips. This translates directly to the equipment manufacturers' need for advanced materials that enable higher precision and yield. Competitive dynamics are intensifying, with key players focusing on material innovation, customization for specific applications, and strategic partnerships to secure their market position. The market penetration rate of high-performance plastics in semiconductor equipment applications has grown from approximately 40% in 2019 to an estimated 65% by 2025, indicating a significant shift away from traditional materials. The compound annual growth rate (CAGR) for the market is projected to be around 7-9% during the forecast period. Opportunities lie in the development of novel composite materials, sustainable plastic solutions, and enhanced surface treatments to further improve performance and reduce manufacturing costs for semiconductor equipment. The increasing complexity of semiconductor nodes (e.g., sub-5nm) will further drive the need for materials with unparalleled purity and resistance to process-induced contamination.

Dominant Markets & Segments in High Performance Plastics for Semiconductor Equipment

The High Performance Plastics for Semiconductor Equipment market is experiencing dominance across several key segments, driven by distinct application needs and material advantages.

Application Segments:

- Vacuum Chamber (Etch, Vapor Deposition & Ion Implant): This segment is a significant growth driver due to the stringent requirements for ultra-high purity, low outgassing, and excellent chemical resistance in these critical process steps. Materials like PEEK and PI (Polyimide/PAI) are extensively used for components such as liners, baffles, and wafer chucks, where contamination control is paramount. The ongoing advancements in wafer processing technology, including atomic layer deposition (ALD) and advanced etching techniques, necessitate the use of plastics that can withstand corrosive plasmas and high temperatures without degradation. The market for this segment is projected to exceed $15 million by 2033.

- Key Growth Drivers: Increasing complexity of semiconductor nodes, demand for higher wafer throughput, and stricter purity standards in advanced fabrication.

- Wet Process (Clean, PVD, Wet Etch, ECD): This segment is characterized by exposure to a wide range of aggressive chemicals, including acids, bases, and solvents. High-performance plastics offer superior chemical inertness and resistance to swelling or degradation compared to traditional materials. PTFE and PPS are widely adopted for components like pump parts, valve seats, and tubing. The growth in electroplating (ECD) for advanced interconnects further fuels demand for specialized plastics in this area.

- Key Growth Drivers: Expansion of wet cleaning processes for defect reduction, growing demand for PVD and ECD in advanced packaging, and the need for corrosion-resistant materials.

- Vacuum Pumps, Valves & Wafer Handling: These segments require materials with excellent wear resistance, low friction, and dimensional stability under vacuum and varying temperatures. PEEK, PI (Polyimide/PAI), and PPS are utilized for seals, bearings, gears, and end-effectors in wafer robots. The drive for higher automation and precision in wafer handling systems directly impacts the demand for these durable and reliable plastics.

- Key Growth Drivers: Increased automation in semiconductor fabs, demand for precision wafer manipulation, and the need for long-life components in vacuum systems.

- CMP (Retainer Ring): Chemical Mechanical Planarization (CMP) applications demand materials with excellent wear resistance and precise dimensional control. PEEK and PI (Polyimide/PAI) are often used for retainer rings due to their ability to maintain shape and provide consistent polishing pressure.

- Key Growth Drivers: Advancements in CMP slurries and pads, increasing demand for ultra-flat wafer surfaces, and the need for materials that minimize slurry adhesion.

- Dry Environment & ESD: For applications requiring static discharge protection and operation in dry environments, specialized grades of plastics with inherent ESD properties and low moisture absorption are crucial.

- Key Growth Drivers: Increasing density of semiconductor components, reduced feature sizes leading to higher susceptibility to ESD, and the need for non-conductive materials in sensitive areas.

Types of High Performance Plastics:

- PEEK (Polyether Ether Ketone): Dominant in applications requiring high temperature resistance, excellent mechanical strength, and chemical inertness. Its use in vacuum chambers and wafer handling is substantial.

- Key Growth Drivers: Superior balance of properties for demanding applications, growing adoption in advanced wafer processing equipment.

- PI (Polyimide/PAI): Offers exceptional thermal stability and good mechanical properties, making it suitable for high-temperature vacuum applications and components subject to wear.

- Key Growth Drivers: High-temperature performance, radiation resistance, and dimensional stability in extreme environments.

- PPS (Polyphenylene Sulfide): Known for its excellent chemical resistance and good thermal properties, it is widely used in wet process equipment and components exposed to corrosive chemicals.

- Key Growth Drivers: Broad chemical resistance profile, cost-effectiveness for high-volume applications in wet processing.

- PTFE (Polytetrafluoroethylene): Exhibits outstanding chemical inertness and very low friction, making it ideal for seals, gaskets, and components in highly corrosive environments.

- Key Growth Drivers: Unmatched chemical resistance and non-stick properties for critical sealing applications.

- PEI (Polyetherimide): Offers a good combination of mechanical strength, thermal stability, and chemical resistance, finding applications in various equipment parts.

- Key Growth Drivers: Versatility and good performance-to-cost ratio for a range of semiconductor equipment components.

The Asia-Pacific region, particularly Taiwan, South Korea, and China, is the dominant geographical market due to the concentration of major semiconductor manufacturing facilities and the rapid expansion of their domestic semiconductor industries. Policies supporting domestic semiconductor production and investments in advanced manufacturing infrastructure in these regions are significant growth catalysts. The market size for this region is estimated to be over $20 million by 2033.

High Performance Plastics for Semiconductor Equipment Product Analysis

Key product innovations in high-performance plastics for semiconductor equipment focus on enhancing purity, reducing outgassing, and improving resistance to aggressive process chemistries and plasmas. Materials like PEEK and PI are being engineered with ultra-low levels of metallic impurities and particulate generation, critical for sub-5nm chip fabrication. Advanced grades of PPS now offer superior chemical stability in fluorine-based plasma environments. Victrex's PEEK 450CA30, for example, provides enhanced wear resistance and thermal stability for wafer handling applications. DuPont's advanced fluoropolymers are critical for corrosion-resistant components in wet etch systems. These product advancements translate into competitive advantages by enabling higher yields, reduced equipment downtime, and longer service life for critical semiconductor manufacturing tools.

Key Drivers, Barriers & Challenges in High Performance Plastics for Semiconductor Equipment

Key Drivers:

The High Performance Plastics for Semiconductor Equipment market is propelled by several interconnected factors. The relentless demand for more powerful and efficient semiconductors, driven by AI, 5G, and IoT, necessitates continuous innovation in fabrication equipment, which in turn fuels the need for advanced materials. Technological advancements in material science, such as the development of higher purity grades and composites, directly enhance the performance and reliability of semiconductor manufacturing processes. Furthermore, supportive government policies in key manufacturing regions, promoting domestic semiconductor production and R&D, create a favorable ecosystem for growth. For instance, the US CHIPS Act and similar initiatives in Europe and Asia are spurring significant investment in semiconductor infrastructure.

Barriers & Challenges:

Despite the positive outlook, the market faces significant challenges. Stringent regulatory requirements and industry certifications for cleanroom environments demand extensive testing and validation, leading to longer product development cycles and higher costs. Supply chain disruptions, as evidenced by recent global events, can impact the availability and pricing of raw materials. Competitive pressures from both established players and emerging material suppliers necessitate continuous innovation and cost optimization. The high initial investment required for developing and qualifying new high-performance plastic grades can also be a barrier for smaller companies. For example, the qualification process for a new material can take over 1-2 years and cost upwards of $1-5 million.

Growth Drivers in the High Performance Plastics for Semiconductor Equipment Market

The primary growth drivers for High Performance Plastics in Semiconductor Equipment are the escalating demand for advanced semiconductors powering technologies like AI, 5G, and IoT. This demand spurs investment in new and upgraded semiconductor fabrication facilities, directly translating to a need for higher-performance materials in manufacturing equipment. Technological innovation in material science, leading to plastics with superior purity, chemical resistance, and thermal stability, enables the fabrication of smaller and more complex chip architectures. Furthermore, government initiatives and subsidies aimed at bolstering domestic semiconductor manufacturing capabilities worldwide create a robust market environment. For example, significant government funding for R&D in advanced materials for semiconductor applications is a key catalyst.

Challenges Impacting High Performance Plastics for Semiconductor Equipment Growth

Challenges impacting growth include the stringent qualification and certification processes required for semiconductor applications, which can be time-consuming and costly, often taking years and millions of dollars. Supply chain vulnerabilities, particularly for specialized raw materials, can lead to production delays and price volatility. Intense competition among established and new material suppliers necessitates continuous innovation and cost management. The high upfront investment in R&D and manufacturing capabilities for advanced plastics can also be a barrier. Moreover, the need for continuous material development to keep pace with shrinking semiconductor nodes and evolving process technologies presents an ongoing challenge.

Key Players Shaping the High Performance Plastics for Semiconductor Equipment Market

- DuPont

- Mitsubishi Chemical

- Ensinger

- PBI Performance Products, Inc.

- SABIC

- Victrex

- Solvay

- Evonik Industries

- 3M

- Chemours

- CDI Products

Significant High Performance Plastics for Semiconductor Equipment Industry Milestones

- 2019: Increased adoption of PEEK in advanced wafer handling systems due to its superior wear resistance.

- 2020: Development of ultra-high purity PPS grades for next-generation etch equipment.

- 2021: Growing demand for PI (Polyimide/PAI) in high-temperature vacuum applications driven by advanced deposition techniques.

- 2022: Enhanced focus on sustainable sourcing and recycling of high-performance plastics within the semiconductor supply chain.

- 2023: Introduction of novel composite materials for enhanced structural integrity and thermal management in semiconductor equipment.

- 2024: Significant investments by major players in R&D for materials enabling sub-3nm semiconductor fabrication processes.

Future Outlook for High Performance Plastics for Semiconductor Equipment Market

The future outlook for High Performance Plastics in Semiconductor Equipment is exceptionally promising, driven by the sustained global demand for semiconductors and the relentless pace of technological innovation. The ongoing transition to advanced semiconductor nodes (e.g., sub-3nm) will amplify the need for ultra-pure, highly resilient materials capable of withstanding extreme process conditions. Strategic opportunities lie in the development of advanced composites, bio-based or recycled high-performance plastics that align with sustainability goals, and materials with enhanced properties for emerging applications like advanced packaging and specialized semiconductor devices. The market is poised for continued growth, with an estimated CAGR of 7-9% over the next decade, as equipment manufacturers increasingly rely on these advanced polymers to push the boundaries of semiconductor technology.

High Performance Plastics for Semiconductor Equipment Segmentation

-

1. Application

- 1.1. Vacuum Chamber (Etch, Vapor Deposition & Ion Implant)

- 1.2. Wet Process (Clean, PVD, Wet Etch, ECD)

- 1.3. Dry Environment & ESD

- 1.4. CMP (Retainer Ring)

- 1.5. Vacuum Pumps, Valves & Wafer Handling

- 1.6. Others

-

2. Types

- 2.1. PPS

- 2.2. PEEK

- 2.3. PI (Polyimide/PAI)

- 2.4. PC

- 2.5. PTFE

- 2.6. PBI

- 2.7. PEI

- 2.8. Others

High Performance Plastics for Semiconductor Equipment Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

High Performance Plastics for Semiconductor Equipment Regional Market Share

Geographic Coverage of High Performance Plastics for Semiconductor Equipment

High Performance Plastics for Semiconductor Equipment REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.13% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Vacuum Chamber (Etch, Vapor Deposition & Ion Implant)

- 5.1.2. Wet Process (Clean, PVD, Wet Etch, ECD)

- 5.1.3. Dry Environment & ESD

- 5.1.4. CMP (Retainer Ring)

- 5.1.5. Vacuum Pumps, Valves & Wafer Handling

- 5.1.6. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. PPS

- 5.2.2. PEEK

- 5.2.3. PI (Polyimide/PAI)

- 5.2.4. PC

- 5.2.5. PTFE

- 5.2.6. PBI

- 5.2.7. PEI

- 5.2.8. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global High Performance Plastics for Semiconductor Equipment Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Vacuum Chamber (Etch, Vapor Deposition & Ion Implant)

- 6.1.2. Wet Process (Clean, PVD, Wet Etch, ECD)

- 6.1.3. Dry Environment & ESD

- 6.1.4. CMP (Retainer Ring)

- 6.1.5. Vacuum Pumps, Valves & Wafer Handling

- 6.1.6. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. PPS

- 6.2.2. PEEK

- 6.2.3. PI (Polyimide/PAI)

- 6.2.4. PC

- 6.2.5. PTFE

- 6.2.6. PBI

- 6.2.7. PEI

- 6.2.8. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America High Performance Plastics for Semiconductor Equipment Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Vacuum Chamber (Etch, Vapor Deposition & Ion Implant)

- 7.1.2. Wet Process (Clean, PVD, Wet Etch, ECD)

- 7.1.3. Dry Environment & ESD

- 7.1.4. CMP (Retainer Ring)

- 7.1.5. Vacuum Pumps, Valves & Wafer Handling

- 7.1.6. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. PPS

- 7.2.2. PEEK

- 7.2.3. PI (Polyimide/PAI)

- 7.2.4. PC

- 7.2.5. PTFE

- 7.2.6. PBI

- 7.2.7. PEI

- 7.2.8. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America High Performance Plastics for Semiconductor Equipment Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Vacuum Chamber (Etch, Vapor Deposition & Ion Implant)

- 8.1.2. Wet Process (Clean, PVD, Wet Etch, ECD)

- 8.1.3. Dry Environment & ESD

- 8.1.4. CMP (Retainer Ring)

- 8.1.5. Vacuum Pumps, Valves & Wafer Handling

- 8.1.6. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. PPS

- 8.2.2. PEEK

- 8.2.3. PI (Polyimide/PAI)

- 8.2.4. PC

- 8.2.5. PTFE

- 8.2.6. PBI

- 8.2.7. PEI

- 8.2.8. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe High Performance Plastics for Semiconductor Equipment Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Vacuum Chamber (Etch, Vapor Deposition & Ion Implant)

- 9.1.2. Wet Process (Clean, PVD, Wet Etch, ECD)

- 9.1.3. Dry Environment & ESD

- 9.1.4. CMP (Retainer Ring)

- 9.1.5. Vacuum Pumps, Valves & Wafer Handling

- 9.1.6. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. PPS

- 9.2.2. PEEK

- 9.2.3. PI (Polyimide/PAI)

- 9.2.4. PC

- 9.2.5. PTFE

- 9.2.6. PBI

- 9.2.7. PEI

- 9.2.8. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa High Performance Plastics for Semiconductor Equipment Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Vacuum Chamber (Etch, Vapor Deposition & Ion Implant)

- 10.1.2. Wet Process (Clean, PVD, Wet Etch, ECD)

- 10.1.3. Dry Environment & ESD

- 10.1.4. CMP (Retainer Ring)

- 10.1.5. Vacuum Pumps, Valves & Wafer Handling

- 10.1.6. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. PPS

- 10.2.2. PEEK

- 10.2.3. PI (Polyimide/PAI)

- 10.2.4. PC

- 10.2.5. PTFE

- 10.2.6. PBI

- 10.2.7. PEI

- 10.2.8. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific High Performance Plastics for Semiconductor Equipment Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Vacuum Chamber (Etch, Vapor Deposition & Ion Implant)

- 11.1.2. Wet Process (Clean, PVD, Wet Etch, ECD)

- 11.1.3. Dry Environment & ESD

- 11.1.4. CMP (Retainer Ring)

- 11.1.5. Vacuum Pumps, Valves & Wafer Handling

- 11.1.6. Others

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. PPS

- 11.2.2. PEEK

- 11.2.3. PI (Polyimide/PAI)

- 11.2.4. PC

- 11.2.5. PTFE

- 11.2.6. PBI

- 11.2.7. PEI

- 11.2.8. Others

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 DuPont

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Mitsubishi Chemical

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Ensinger

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 PBI Performance Products

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Inc.

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 SABIC

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Victrex

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Solvay

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Evonik Industries

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 3M

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Chemours

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 CDI Products

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.1 DuPont

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global High Performance Plastics for Semiconductor Equipment Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America High Performance Plastics for Semiconductor Equipment Revenue (billion), by Application 2025 & 2033

- Figure 3: North America High Performance Plastics for Semiconductor Equipment Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America High Performance Plastics for Semiconductor Equipment Revenue (billion), by Types 2025 & 2033

- Figure 5: North America High Performance Plastics for Semiconductor Equipment Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America High Performance Plastics for Semiconductor Equipment Revenue (billion), by Country 2025 & 2033

- Figure 7: North America High Performance Plastics for Semiconductor Equipment Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America High Performance Plastics for Semiconductor Equipment Revenue (billion), by Application 2025 & 2033

- Figure 9: South America High Performance Plastics for Semiconductor Equipment Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America High Performance Plastics for Semiconductor Equipment Revenue (billion), by Types 2025 & 2033

- Figure 11: South America High Performance Plastics for Semiconductor Equipment Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America High Performance Plastics for Semiconductor Equipment Revenue (billion), by Country 2025 & 2033

- Figure 13: South America High Performance Plastics for Semiconductor Equipment Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe High Performance Plastics for Semiconductor Equipment Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe High Performance Plastics for Semiconductor Equipment Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe High Performance Plastics for Semiconductor Equipment Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe High Performance Plastics for Semiconductor Equipment Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe High Performance Plastics for Semiconductor Equipment Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe High Performance Plastics for Semiconductor Equipment Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa High Performance Plastics for Semiconductor Equipment Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa High Performance Plastics for Semiconductor Equipment Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa High Performance Plastics for Semiconductor Equipment Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa High Performance Plastics for Semiconductor Equipment Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa High Performance Plastics for Semiconductor Equipment Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa High Performance Plastics for Semiconductor Equipment Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific High Performance Plastics for Semiconductor Equipment Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific High Performance Plastics for Semiconductor Equipment Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific High Performance Plastics for Semiconductor Equipment Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific High Performance Plastics for Semiconductor Equipment Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific High Performance Plastics for Semiconductor Equipment Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific High Performance Plastics for Semiconductor Equipment Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global High Performance Plastics for Semiconductor Equipment Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global High Performance Plastics for Semiconductor Equipment Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global High Performance Plastics for Semiconductor Equipment Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global High Performance Plastics for Semiconductor Equipment Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global High Performance Plastics for Semiconductor Equipment Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global High Performance Plastics for Semiconductor Equipment Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States High Performance Plastics for Semiconductor Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada High Performance Plastics for Semiconductor Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico High Performance Plastics for Semiconductor Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global High Performance Plastics for Semiconductor Equipment Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global High Performance Plastics for Semiconductor Equipment Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global High Performance Plastics for Semiconductor Equipment Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil High Performance Plastics for Semiconductor Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina High Performance Plastics for Semiconductor Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America High Performance Plastics for Semiconductor Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global High Performance Plastics for Semiconductor Equipment Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global High Performance Plastics for Semiconductor Equipment Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global High Performance Plastics for Semiconductor Equipment Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom High Performance Plastics for Semiconductor Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany High Performance Plastics for Semiconductor Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France High Performance Plastics for Semiconductor Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy High Performance Plastics for Semiconductor Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain High Performance Plastics for Semiconductor Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia High Performance Plastics for Semiconductor Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux High Performance Plastics for Semiconductor Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics High Performance Plastics for Semiconductor Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe High Performance Plastics for Semiconductor Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global High Performance Plastics for Semiconductor Equipment Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global High Performance Plastics for Semiconductor Equipment Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global High Performance Plastics for Semiconductor Equipment Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey High Performance Plastics for Semiconductor Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel High Performance Plastics for Semiconductor Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC High Performance Plastics for Semiconductor Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa High Performance Plastics for Semiconductor Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa High Performance Plastics for Semiconductor Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa High Performance Plastics for Semiconductor Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global High Performance Plastics for Semiconductor Equipment Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global High Performance Plastics for Semiconductor Equipment Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global High Performance Plastics for Semiconductor Equipment Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China High Performance Plastics for Semiconductor Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India High Performance Plastics for Semiconductor Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan High Performance Plastics for Semiconductor Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea High Performance Plastics for Semiconductor Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN High Performance Plastics for Semiconductor Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania High Performance Plastics for Semiconductor Equipment Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific High Performance Plastics for Semiconductor Equipment Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the High Performance Plastics for Semiconductor Equipment?

The projected CAGR is approximately 11.13%.

2. Which companies are prominent players in the High Performance Plastics for Semiconductor Equipment?

Key companies in the market include DuPont, Mitsubishi Chemical, Ensinger, PBI Performance Products, Inc., SABIC, Victrex, Solvay, Evonik Industries, 3M, Chemours, CDI Products.

3. What are the main segments of the High Performance Plastics for Semiconductor Equipment?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 5.7 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4350.00, USD 6525.00, and USD 8700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "High Performance Plastics for Semiconductor Equipment," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the High Performance Plastics for Semiconductor Equipment report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the High Performance Plastics for Semiconductor Equipment?

To stay informed about further developments, trends, and reports in the High Performance Plastics for Semiconductor Equipment, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence