Key Insights

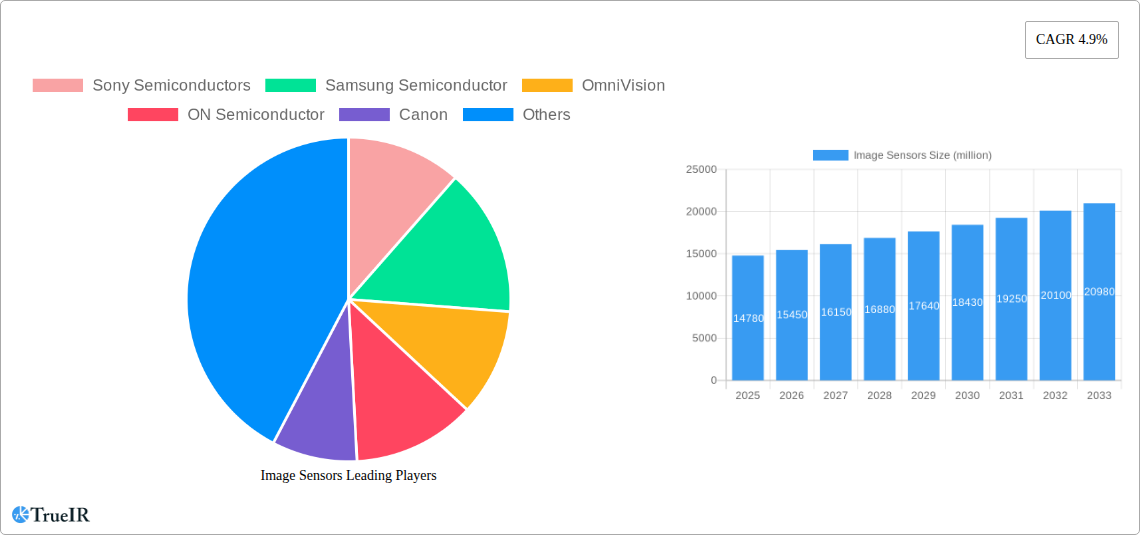

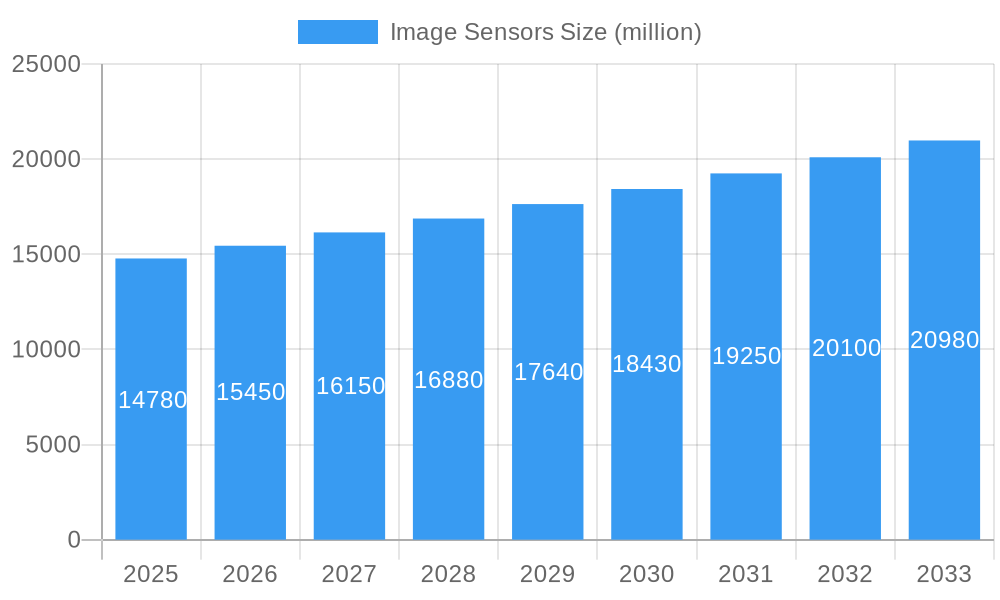

The global image sensor market is poised for substantial growth, projected to reach $22,260 million by 2033, exhibiting a robust Compound Annual Growth Rate (CAGR) of 4.9% from 2019 to 2033. This expansion is primarily driven by the escalating demand across a diverse range of applications, with consumer electronics leading the charge. The pervasive integration of advanced imaging capabilities in smartphones, digital cameras, drones, and wearable devices fuels this segment's dominance. Furthermore, the burgeoning medical electronics sector, propelled by innovations in diagnostic imaging, surgical tools, and telehealth, represents a significant growth avenue. Avionics and industrial applications, demanding high-resolution and reliable imaging for navigation, inspection, and automation, also contribute to the market's upward trajectory. The market is predominantly characterized by the widespread adoption of CMOS image sensors due to their superior performance, lower power consumption, and cost-effectiveness compared to CCD sensors, though CCDs continue to hold niche applications.

Image Sensors Market Size (In Billion)

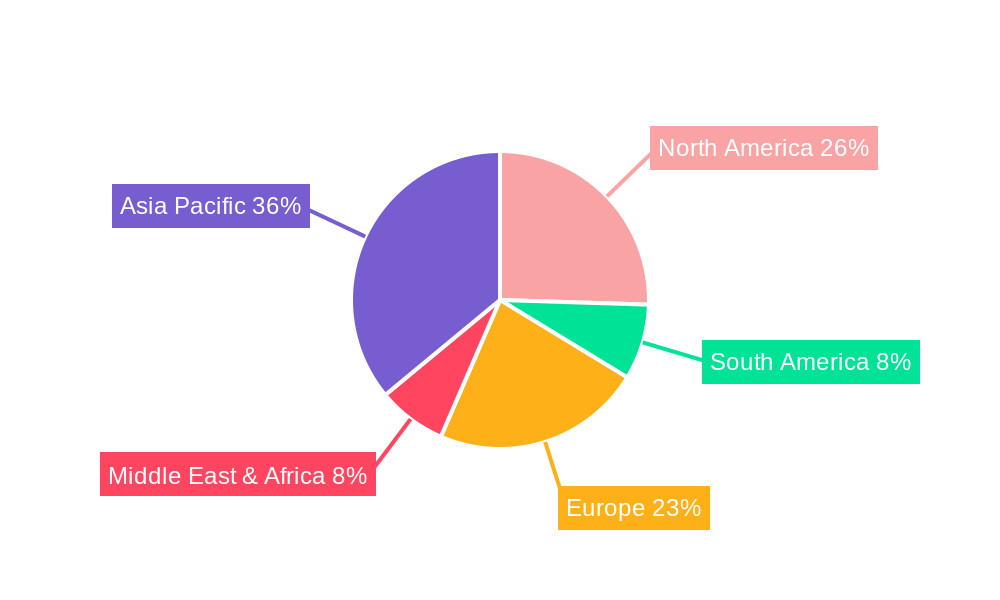

The market's growth trajectory is supported by several key trends, including the continuous miniaturization of image sensors, enabling their incorporation into increasingly compact devices, and the advancement of sensor technologies for enhanced low-light performance, higher dynamic range, and faster frame rates. The rise of artificial intelligence and machine learning is further accelerating demand for sophisticated image sensors capable of processing complex visual data for applications like autonomous driving and advanced surveillance. Geographically, the Asia Pacific region, spearheaded by China and Japan, is expected to remain the largest and fastest-growing market, owing to its significant manufacturing capabilities and a rapidly expanding consumer base for electronic devices. North America and Europe also present substantial market opportunities, driven by technological innovation and the adoption of advanced imaging solutions in various sectors. Emerging economies are anticipated to witness increasing penetration of image sensors as affordability and technological accessibility improve.

Image Sensors Company Market Share

This in-depth report provides a dynamic and SEO-optimized analysis of the global Image Sensors market, a crucial component driving innovation across numerous industries. Leveraging high-volume keywords such as CMOS Image Sensor, CCD Image Sensor, Consumer Electronics, Medical Electronics, Automotive Image Sensors, and Industrial Image Sensors, this study is designed to enhance search rankings and engage a broad spectrum of industry professionals, researchers, and investors. The report covers a comprehensive study period from 2019 to 2033, with a base year of 2025, an estimated year also of 2025, and a forecast period extending from 2025 to 2033. The historical period analyzed is 2019–2024.

Image Sensors Market Structure & Competitive Landscape

The Image Sensors market exhibits a moderately concentrated structure, with leading players such as Sony Semiconductors, Samsung Semiconductor, and OmniVision commanding significant market share. Innovation serves as a primary driver, fueled by relentless R&D in areas like higher resolution, improved low-light performance, and enhanced frame rates. Regulatory impacts, particularly concerning data privacy and industry-specific standards (e.g., automotive safety regulations), are increasingly influencing product development and market access. Product substitutes, while limited in high-performance niches, include traditional cameras and alternative sensing technologies that may fulfill specific, less demanding applications. End-user segmentation reveals a strong reliance on the Consumer Electronics sector, followed by growing demand from Medical Electronics and Industry. Mergers and acquisitions (M&A) remain a strategic tool for companies to expand their product portfolios, gain technological advantages, and consolidate market presence, with approximately 15-20 significant M&A activities recorded annually over the historical period. Key players like ON Semiconductor and Canon are actively involved in strategic partnerships and acquisitions to bolster their competitive edge in this rapidly evolving landscape.

Image Sensors Market Trends & Opportunities

The global Image Sensors market is projected to experience robust growth, with an estimated market size expected to reach over $25,000 million by 2025 and a projected compound annual growth rate (CAGR) of approximately 9.5% during the forecast period (2025–2033). This expansion is driven by several intersecting trends. Firstly, the insatiable demand for higher-quality imaging in Consumer Electronics, including smartphones, digital cameras, and wearable devices, continues to be a dominant force. Consumers are increasingly seeking advanced features like enhanced low-light capabilities, faster autofocus, and superior video recording resolutions, pushing manufacturers to innovate continuously. Secondly, the rapid advancements in Artificial Intelligence (AI) and Machine Learning (ML) are creating new opportunities for image sensors. The ability of sensors to capture detailed visual data is fundamental to the training and deployment of AI algorithms in applications ranging from autonomous vehicles to smart city infrastructure and advanced medical diagnostics.

The Medical Electronics sector is a rapidly growing segment, driven by the need for higher resolution and more sensitive sensors in diagnostic imaging equipment, surgical robotics, and telemedicine solutions. The precision and reliability offered by modern image sensors are critical for improving patient outcomes and enabling minimally invasive procedures. Similarly, the Industry segment, encompassing industrial automation, quality control, and machine vision, is witnessing substantial growth. The implementation of Industry 4.0 principles and the increasing adoption of smart manufacturing processes necessitate sophisticated imaging systems for real-time monitoring, defect detection, and robotic guidance. The Automotive Image Sensors market is poised for exceptional growth, propelled by the increasing integration of advanced driver-assistance systems (ADAS) and the ongoing development of autonomous driving technologies. These systems rely heavily on multiple image sensors to perceive the environment, detect obstacles, and ensure road safety.

Technological shifts are characterized by the continued dominance of CMOS Image Sensors, which offer advantages in terms of speed, power efficiency, and cost-effectiveness compared to older CCD technologies. Ongoing research and development are focused on enhancing pixel density, dynamic range, and spectral sensitivity, opening up new application frontiers. The competitive dynamics are intense, with established players constantly striving to differentiate through technological prowess, strategic partnerships, and vertical integration. Emerging markets and new application areas, such as augmented reality (AR) and virtual reality (VR) devices, also present significant growth opportunities for image sensor manufacturers. The increasing penetration of image-sensing technologies into everyday life, from smart home devices to advanced security systems, underscores the pervasive influence and vast potential of the image sensor market.

Dominant Markets & Segments in Image Sensors

The Image Sensors market is characterized by the overwhelming dominance of the Consumer Electronics application segment, which accounts for over 60% of the global market value. Within this segment, smartphones are the largest single end-use, driven by the continuous demand for higher resolution, improved low-light performance, and advanced computational photography features. Key growth drivers in this segment include the increasing global smartphone penetration rate, the upgrade cycle of mobile devices, and the integration of multi-camera systems for enhanced imaging capabilities. The CMOS Image Sensor type holds a commanding position, estimated to capture over 90% of the market due to its superior speed, power efficiency, and cost-effectiveness compared to CCD sensors.

The Asia-Pacific region stands as the largest and fastest-growing geographical market, propelled by the concentration of major consumer electronics manufacturing hubs in countries like China, South Korea, and Taiwan. The region's strong domestic demand, coupled with its role as a global manufacturing powerhouse, significantly contributes to its market leadership. China, in particular, is a pivotal market, driven by its large consumer base and substantial investments in domestic semiconductor manufacturing and technological innovation.

The Medical Electronics segment is exhibiting strong growth, driven by an increasing demand for advanced diagnostic imaging technologies, such as MRI, CT scans, and digital radiography, where high-resolution and high-sensitivity image sensors are critical. The development of minimally invasive surgical procedures and the expansion of telemedicine further fuel the adoption of sophisticated imaging solutions. Key growth drivers include an aging global population, rising healthcare expenditures, and technological advancements in medical imaging.

The Industry segment, encompassing industrial automation, quality inspection, and machine vision, is also a significant growth area. The adoption of Industry 4.0 principles and the drive for greater efficiency and precision in manufacturing processes necessitate advanced imaging capabilities for real-time monitoring, defect detection, and robotic guidance. Growth in this segment is supported by increased automation investments and the demand for enhanced product quality.

The Avionics segment, while smaller in volume, is characterized by high-value applications, driven by the need for robust and reliable imaging systems for navigation, surveillance, and pilot assistance. The increasing complexity of modern aircraft and the growing emphasis on safety are key drivers in this sector.

Image Sensors Product Analysis

Product innovation in the Image Sensors market is primarily focused on enhancing resolution, improving low-light performance, increasing dynamic range, and reducing power consumption. CMOS sensors continue to lead, with advancements in stacked sensor technology and backside illumination (BSI) significantly boosting light-gathering capabilities and reducing noise. These innovations directly translate into superior image quality for consumer devices, more accurate diagnostics in medical applications, and enhanced object recognition in industrial and automotive settings. Competitive advantages are being forged through the development of specialized sensors with integrated functionalities like autofocus mechanisms, signal processing capabilities, and advanced color filters, enabling manufacturers to offer compelling solutions for niche markets and demanding applications.

Key Drivers, Barriers & Challenges in Image Sensors

Key Drivers, Barriers & Challenges in Image Sensors

Key Drivers: The Image Sensors market is propelled by several key drivers. Technologically, the relentless pursuit of higher resolution, better low-light sensitivity, and faster frame rates in cameras for smartphones, automotive applications, and medical imaging is paramount. Economically, the growing demand for advanced consumer electronics, the expansion of AI and machine learning adoption requiring sophisticated visual data, and increasing healthcare expenditures are significant catalysts. Policy-driven factors, such as government initiatives promoting smart manufacturing and the automotive industry's push for enhanced safety features, further bolster market growth.

Barriers & Challenges: Despite the positive outlook, the Image Sensors market faces several challenges. Supply chain disruptions, particularly concerning the availability of critical raw materials and semiconductor manufacturing capacity, can lead to production delays and increased costs. Regulatory hurdles, including evolving data privacy laws and stringent industry-specific certifications (e.g., for medical devices), can impact product development timelines and market entry. Competitive pressures from established players and emerging entrants, along with the significant R&D investment required for continuous innovation, present ongoing challenges. The increasing complexity of sensor designs and manufacturing processes also contributes to higher production costs and potential yield issues.

Growth Drivers in the Image Sensors Market

The Image Sensors market is experiencing significant growth, primarily driven by technological advancements and burgeoning demand across multiple sectors. The continuous evolution of smartphone photography, with consumers expecting increasingly sophisticated features like superior night mode and high-resolution video, remains a core growth catalyst. The rapid adoption of Artificial Intelligence (AI) and Machine Learning (ML) fuels demand for image sensors that can capture rich visual data for applications such as facial recognition, object detection, and autonomous navigation. Furthermore, the automotive industry's transition towards advanced driver-assistance systems (ADAS) and autonomous driving relies heavily on a suite of high-performance image sensors for environmental perception, directly contributing to market expansion. The growing healthcare sector's reliance on advanced medical imaging equipment for diagnostics and treatment also presents a significant growth opportunity.

Challenges Impacting Image Sensors Growth

The Image Sensors market faces several significant challenges that can impact its growth trajectory. Supply chain vulnerabilities, particularly the reliance on a limited number of foundries for advanced semiconductor manufacturing, can lead to production bottlenecks and price fluctuations. Regulatory complexities, such as evolving data privacy laws like GDPR and CCPA, require careful consideration in sensor design and data handling, especially for consumer-facing applications. Intense competitive pressure among key players necessitates substantial and continuous investment in research and development to maintain market share and innovate, which can be a significant barrier for smaller companies. Furthermore, the increasing cost of advanced manufacturing processes and the pressure to deliver increasingly sophisticated features at competitive price points pose ongoing economic challenges.

Key Players Shaping the Image Sensors Market

The Image Sensors market is shaped by a confluence of innovative companies, including:

- Sony Semiconductors

- Samsung Semiconductor

- OmniVision

- ON Semiconductor

- Canon

- Panasonic

- SK Hynix

- STMicroelectronics

- Teledyne Technologies

- Hamamatsu

- Infineon Technologies

- CMOSIS

Significant Image Sensors Industry Milestones

- 2019: Introduction of larger pixel sizes and enhanced computational photography features in flagship smartphones.

- 2020: Significant advancements in automotive image sensor technology for improved ADAS performance.

- 2021: Increased focus on wafer-level optics integration for miniaturized camera modules.

- 2022: Growing adoption of stacked CMOS sensor architectures for higher frame rates and improved signal processing.

- 2023: Emergence of event-based sensors for specialized AI and robotics applications.

- 2024: Continued R&D on sensor technologies for AR/VR devices and advanced medical imaging.

Future Outlook for Image Sensors Market

The future outlook for the Image Sensors market is exceptionally promising, driven by ongoing technological innovation and the expanding scope of applications. The increasing integration of image sensors in AI-powered devices, autonomous systems, and advanced medical diagnostics will continue to fuel market expansion. Strategic opportunities lie in developing specialized sensors for emerging technologies like augmented reality (AR), virtual reality (VR), and the Internet of Things (IoT). Continued advancements in CMOS technology, focusing on higher resolution, greater dynamic range, and enhanced low-light capabilities, will solidify its dominance. The market is poised for sustained growth, driven by the fundamental human desire for improved visual perception and the ever-increasing role of visual data in shaping our technological future.

Image Sensors Segmentation

-

1. Application

- 1.1. Consumer Electronics

- 1.2. Medical Electronics

- 1.3. Avionics

- 1.4. Industry

- 1.5. Others

-

2. Type

- 2.1. CMOS Image Sensor

- 2.2. CCD Image Sensor

- 2.3. Other

Image Sensors Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Image Sensors Regional Market Share

Geographic Coverage of Image Sensors

Image Sensors REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Consumer Electronics

- 5.1.2. Medical Electronics

- 5.1.3. Avionics

- 5.1.4. Industry

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. CMOS Image Sensor

- 5.2.2. CCD Image Sensor

- 5.2.3. Other

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Image Sensors Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Consumer Electronics

- 6.1.2. Medical Electronics

- 6.1.3. Avionics

- 6.1.4. Industry

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. CMOS Image Sensor

- 6.2.2. CCD Image Sensor

- 6.2.3. Other

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Image Sensors Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Consumer Electronics

- 7.1.2. Medical Electronics

- 7.1.3. Avionics

- 7.1.4. Industry

- 7.1.5. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. CMOS Image Sensor

- 7.2.2. CCD Image Sensor

- 7.2.3. Other

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Image Sensors Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Consumer Electronics

- 8.1.2. Medical Electronics

- 8.1.3. Avionics

- 8.1.4. Industry

- 8.1.5. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. CMOS Image Sensor

- 8.2.2. CCD Image Sensor

- 8.2.3. Other

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Image Sensors Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Consumer Electronics

- 9.1.2. Medical Electronics

- 9.1.3. Avionics

- 9.1.4. Industry

- 9.1.5. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. CMOS Image Sensor

- 9.2.2. CCD Image Sensor

- 9.2.3. Other

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Image Sensors Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Consumer Electronics

- 10.1.2. Medical Electronics

- 10.1.3. Avionics

- 10.1.4. Industry

- 10.1.5. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. CMOS Image Sensor

- 10.2.2. CCD Image Sensor

- 10.2.3. Other

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Image Sensors Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Consumer Electronics

- 11.1.2. Medical Electronics

- 11.1.3. Avionics

- 11.1.4. Industry

- 11.1.5. Others

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. CMOS Image Sensor

- 11.2.2. CCD Image Sensor

- 11.2.3. Other

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Sony Semiconductors

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Samsung Semiconductor

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 OmniVision

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 ON Semiconductor

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Canon

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Panasonic

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 SK Hynix

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 STMicroelectronics

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Teledyne Technologies

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Hamamatsu

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Infineon Technologies

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 CMOSIS

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.1 Sony Semiconductors

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Image Sensors Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Image Sensors Revenue (million), by Application 2025 & 2033

- Figure 3: North America Image Sensors Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Image Sensors Revenue (million), by Type 2025 & 2033

- Figure 5: North America Image Sensors Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Image Sensors Revenue (million), by Country 2025 & 2033

- Figure 7: North America Image Sensors Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Image Sensors Revenue (million), by Application 2025 & 2033

- Figure 9: South America Image Sensors Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Image Sensors Revenue (million), by Type 2025 & 2033

- Figure 11: South America Image Sensors Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Image Sensors Revenue (million), by Country 2025 & 2033

- Figure 13: South America Image Sensors Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Image Sensors Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Image Sensors Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Image Sensors Revenue (million), by Type 2025 & 2033

- Figure 17: Europe Image Sensors Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Image Sensors Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Image Sensors Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Image Sensors Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Image Sensors Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Image Sensors Revenue (million), by Type 2025 & 2033

- Figure 23: Middle East & Africa Image Sensors Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Image Sensors Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Image Sensors Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Image Sensors Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Image Sensors Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Image Sensors Revenue (million), by Type 2025 & 2033

- Figure 29: Asia Pacific Image Sensors Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Image Sensors Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Image Sensors Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Image Sensors Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Image Sensors Revenue million Forecast, by Type 2020 & 2033

- Table 3: Global Image Sensors Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Image Sensors Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Image Sensors Revenue million Forecast, by Type 2020 & 2033

- Table 6: Global Image Sensors Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Image Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Image Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Image Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Image Sensors Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Image Sensors Revenue million Forecast, by Type 2020 & 2033

- Table 12: Global Image Sensors Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Image Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Image Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Image Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Image Sensors Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Image Sensors Revenue million Forecast, by Type 2020 & 2033

- Table 18: Global Image Sensors Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Image Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Image Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Image Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Image Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Image Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Image Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Image Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Image Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Image Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Image Sensors Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Image Sensors Revenue million Forecast, by Type 2020 & 2033

- Table 30: Global Image Sensors Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Image Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Image Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Image Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Image Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Image Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Image Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Image Sensors Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Image Sensors Revenue million Forecast, by Type 2020 & 2033

- Table 39: Global Image Sensors Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Image Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Image Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Image Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Image Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Image Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Image Sensors Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Image Sensors Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Image Sensors?

The projected CAGR is approximately 4.9%.

2. Which companies are prominent players in the Image Sensors?

Key companies in the market include Sony Semiconductors, Samsung Semiconductor, OmniVision, ON Semiconductor, Canon, Panasonic, SK Hynix, STMicroelectronics, Teledyne Technologies, Hamamatsu, Infineon Technologies, CMOSIS.

3. What are the main segments of the Image Sensors?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 22260 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 5900.00, USD 8850.00, and USD 11800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Image Sensors," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Image Sensors report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Image Sensors?

To stay informed about further developments, trends, and reports in the Image Sensors, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence