Key Insights

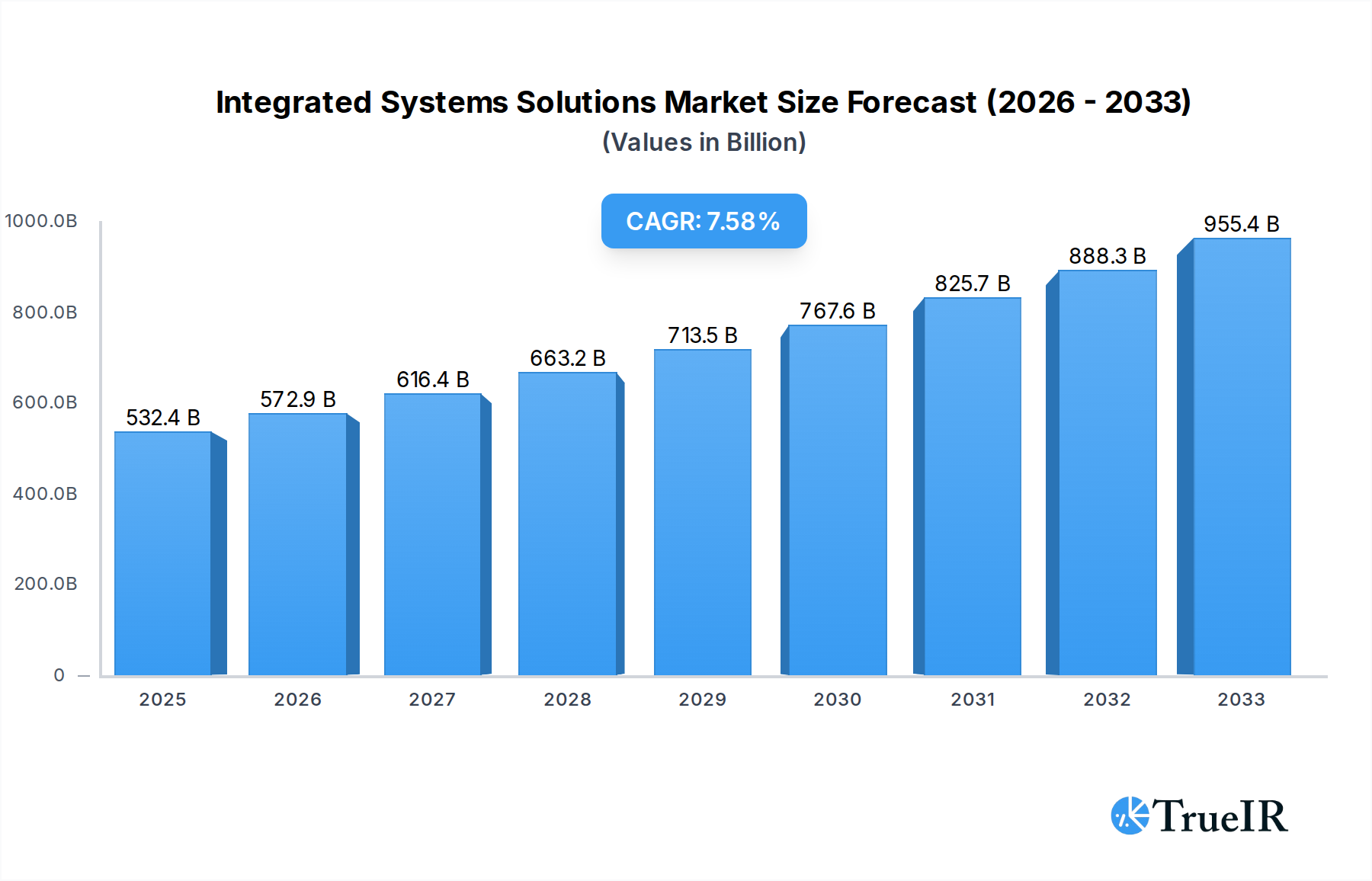

The global Integrated Systems Solutions market is poised for significant expansion, driven by the escalating demand for streamlined IT infrastructure and enhanced operational efficiency across enterprises worldwide. Valued at an impressive 532.42 billion in 2025, the market is projected to grow at a robust Compound Annual Growth Rate (CAGR) of 7.6% from 2025 to 2033. This robust growth is primarily fueled by accelerated digital transformation initiatives, the pervasive adoption of hybrid cloud strategies, and the imperative for organizations to manage increasing data volumes with greater agility and reduced complexity. Integrated systems, encompassing Hyperconverged Integrated Systems (HCIS), Integrated Stack Systems (ISS), and Integrated Infrastructure Systems (IIS), offer a unified approach to computing, storage, and networking, simplifying deployment and management while enhancing performance. Key market drivers also include the need for cost optimization through consolidated hardware and software, improved scalability, and reduced IT operational overheads, making these solutions indispensable for modern enterprises seeking to stay competitive and innovative.

Integrated Systems Solutions Market Size (In Billion)

The market landscape for Integrated Systems Solutions is continuously evolving, marked by several transformative trends and strategic innovations. A dominant trend is the rapid adoption of Hyperconverged Integrated Systems (HCIS), which are increasingly favored for their flexibility, ease of deployment, and scalability, particularly in supporting virtualized and cloud-native workloads. The move towards cloud-based integrated systems is gaining traction, offering organizations greater elasticity and OpEx models, although on-premises solutions continue to be critical for specific regulatory and performance requirements. Furthermore, the integration of advanced analytics, artificial intelligence (AI), and machine learning (ML) capabilities within these platforms is enabling predictive maintenance, automated resource management, and enhanced security. While challenges such as high initial capital expenditure and potential vendor lock-in exist, the long-term benefits of simplified IT environments, improved data center efficiency, and accelerated time-to-market for new services continue to propel the Integrated Systems Solutions market forward, with key players like Dell, IBM, Hewlett Packard, and Oracle leading innovation.

Integrated Systems Solutions Company Market Share

This comprehensive report offers unparalleled insights into the Integrated Systems Solutions market, a critical component of modern enterprise IT infrastructure. Leveraging high-volume keywords such as Integrated Systems Market, Hyperconverged Infrastructure, Cloud-based IT Solutions, Data Center Solutions, Enterprise Storage, Server Infrastructure, Digital Transformation, and IT Modernization, this analysis is meticulously crafted to rank high in search results and provide immediate value to industry stakeholders, investors, and technology leaders. Discover the forces driving a market projected to reach trillions in value, underpinned by innovations from global giants and agile disruptors. This report requires no further modification and presents all values in "billion."

Integrated Systems Solutions Market Structure & Competitive Landscape

The global Integrated Systems Solutions market exhibits a dynamic structure, characterized by intense competition and rapid innovation. Market concentration remains moderate, with the top five players collectively holding an estimated 45 billion to 55 billion percent of the total market share in 2025, driven by extensive product portfolios and established customer bases. Innovation drivers are primarily focused on enhancing system automation, optimizing performance for AI/ML workloads, and improving hybrid cloud integration. Regulatory impacts, particularly concerning data privacy and security compliance, are increasingly shaping product development and deployment strategies, necessitating robust security features within integrated offerings. Product substitutes, such as standalone server, storage, and networking components, continue to exist but are steadily losing ground to the compelling value proposition of pre-validated, optimized integrated systems.

End-user segmentation reveals a significant demand from large enterprises, which account for over 60 billion percent of total revenue, primarily for mission-critical applications and large-scale digital transformation initiatives. Small and medium-sized businesses (SMBs) are rapidly adopting integrated systems, especially hyperconverged solutions, due to their ease of deployment and simplified management, growing at an estimated CAGR of 15 billion percent from 2025 to 2033. Mergers and acquisitions (M&A) activities have been robust in the historical period (2019–2024), with a total M&A volume exceeding 250 billion dollars, as major players consolidate their market position and expand their technological capabilities. Notable acquisitions include strategic moves by Dell EMC to bolster its hyperconverged portfolio and Oracle's continuous integration of cloud-native capabilities. This competitive environment fosters continuous improvement and a race towards more intelligent, autonomous IT infrastructure solutions.

- Market Concentration (2025): Top 5 players account for 45 billion – 55 billion percent of market share.

- M&A Volume (2019–2024): Exceeded 250 billion dollars.

- End-User Segmentation: Large enterprises comprise over 60 billion percent of revenue; SMBs growing at 15 billion percent CAGR.

- Key Innovation Drivers: AI/ML optimization, hybrid cloud integration, automation.

- Regulatory Influences: Data privacy (GDPR, CCPA), cybersecurity standards.

Integrated Systems Solutions Market Trends & Opportunities

The Integrated Systems Solutions market is experiencing significant growth, projected to expand from an estimated market size of 150 billion dollars in 2025 to over 400 billion dollars by 2033, demonstrating a robust Compound Annual Growth Rate (CAGR) of 13.5 billion percent during the forecast period. This upward trajectory is fundamentally driven by accelerated digital transformation initiatives across all industries and the imperative for organizations to streamline their IT operations. Technological shifts are profoundly influencing the market, with a pronounced move towards software-defined architectures, AI-driven automation, and edge computing capabilities embedded within integrated systems. The proliferation of hybrid and multi-cloud strategies is also a key trend, with enterprises demanding integrated solutions that seamlessly bridge on-premises infrastructure with various public cloud environments.

Consumer preferences are increasingly leaning towards "as-a-service" consumption models, leading to a rise in integrated systems offered through subscription-based services, reducing upfront capital expenditure and providing greater operational flexibility. This shift is fueling the adoption of cloud-based integrated solutions, which are expected to achieve a market penetration rate of 40 billion percent among enterprise workloads by 2033. Competitive dynamics are evolving rapidly, with traditional hardware vendors like Dell EMC, Hewlett Packard Enterprise, and IBM intensely competing with software-defined infrastructure specialists like Nutanix (xx) and VMware (xx), as well as cloud providers integrating their offerings with on-premises solutions. The market is also witnessing the emergence of specialized solutions tailored for specific workloads, such as integrated systems optimized for big data analytics, high-performance computing (HPC), and virtual desktop infrastructure (VDI), creating diverse opportunities for vendors. The push for greater energy efficiency and sustainability in data centers is another emerging trend, compelling manufacturers to innovate with more environmentally conscious designs. This confluence of technological advancement, changing consumption models, and evolving competitive landscapes creates a fertile ground for sustained growth and innovation in the Integrated Systems Solutions market.

Dominant Markets & Segments in Integrated Systems Solutions

Within the Integrated Systems Solutions market, the Hyperconverged Integrated System (HCIS) segment is projected to hold the dominant market share throughout the forecast period (2025–2033), largely fueled by its inherent simplicity, scalability, and cost-effectiveness. HCIS is estimated to account for over 55 billion percent of the total market revenue in 2025, with its market share further expanding to nearly 65 billion percent by 2033. This dominance is significantly driven by the widespread enterprise adoption of virtualization, coupled with the need for agile and easily deployable IT infrastructure that can scale on demand. The on-premises deployment type, while facing strong competition from cloud-based models, still holds a substantial portion, particularly for highly sensitive data, compliance requirements, and applications demanding ultra-low latency. However, the Cloud-based segment is demonstrating the most explosive growth, with a projected CAGR of 18 billion percent, as organizations increasingly leverage public and hybrid cloud environments for greater operational flexibility and reduced infrastructure management overhead.

- Leading Segment (Application): Hyperconverged Integrated System (HCIS)

- Market Share (2025): Over 55 billion percent.

- Projected Market Share (2033): Nearly 65 billion percent.

- Key Growth Drivers:

- Infrastructure Simplification: HCIS reduces data center complexity by converging compute, storage, and networking into a single platform.

- Scalability: Easy 'pay-as-you-grow' expansion, adding nodes as needed.

- Cost Efficiency: Lower total cost of ownership (TCO) through reduced power, cooling, and management efforts.

- Agility & Speed: Faster deployment of new applications and services, crucial for digital transformation.

- Virtualization & Cloud Integration: Seamless integration with virtualized environments and hybrid cloud strategies.

- Remote & Edge Deployments: Ideal for distributed environments due to smaller footprint and simplified management.

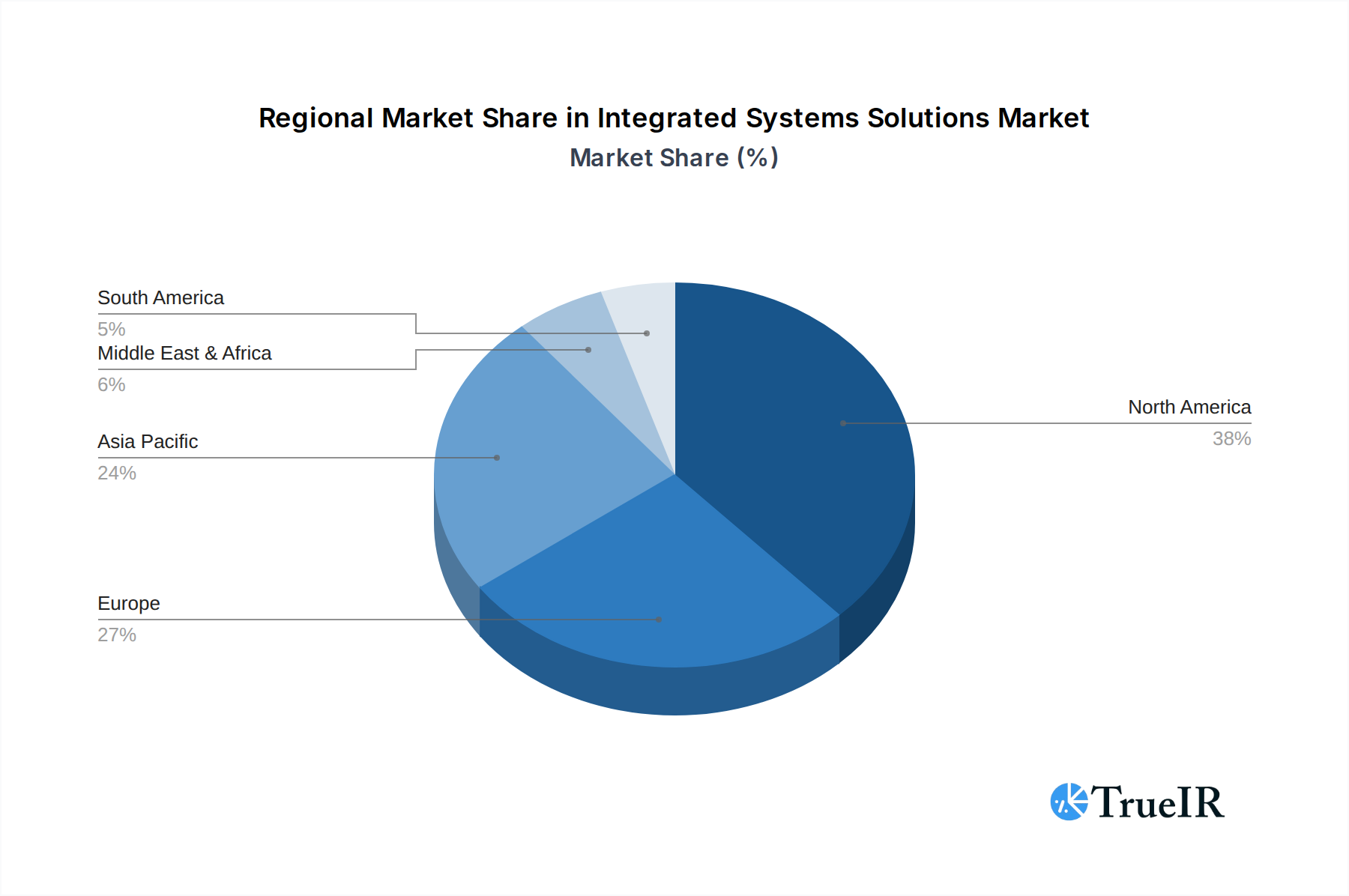

Geographically, North America is expected to remain the dominant region, accounting for an estimated 38 billion percent of the global market in 2025, driven by early adoption of advanced technologies, substantial investments in data center infrastructure, and a high concentration of key market players and end-use industries. The presence of major technology hubs and a mature IT ecosystem contribute significantly to this region's leadership. However, the Asia Pacific region is rapidly emerging as a high-growth market, propelled by accelerating digitalization, significant government initiatives supporting IT infrastructure development, and a burgeoning enterprise sector, particularly in countries like China, India, and Japan. The demand for integrated systems in Europe is also robust, fueled by stringent data residency regulations which often necessitate on-premises or regionally-based cloud solutions.

Integrated Systems Solutions Product Analysis

Product innovations in Integrated Systems Solutions are rapidly advancing, focusing on intelligent automation, AI-driven infrastructure management, and enhanced cybersecurity features. Solutions from leaders like Dell EMC, NetApp, and IBM now incorporate predictive analytics for performance optimization and self-healing capabilities, minimizing human intervention. Hyperconverged solutions from Diamanti and Maxta are specifically designed for containerized workloads and Kubernetes integration, offering superior performance and simplified orchestration for cloud-native applications. Cloud-based integrated systems are gaining traction, providing businesses with scalable, pay-as-you-go infrastructure without the burden of hardware management, while on-premises solutions continue to prioritize security, control, and ultra-low latency for critical workloads. The competitive advantage lies in delivering complete, validated stacks that offer seamless deployment, simplified operations, and superior performance right out of the box, perfectly fitting the market demand for agile and efficient IT.

Key Drivers, Barriers & Challenges in Integrated Systems Solutions

The Integrated Systems Solutions market is primarily propelled by the relentless drive for digital transformation and operational efficiency. Technological advancements in virtualization, cloud computing, and AI/ML are enabling more intelligent and autonomous systems, reducing IT complexity. Economically, integrated solutions offer a compelling total cost of ownership (TCO) reduction by consolidating hardware, simplifying management, and lowering energy consumption. Policy-driven factors, such as government initiatives promoting digital infrastructure and smart city projects, further stimulate market demand. For example, the increasing adoption of 5G infrastructure globally necessitates edge computing solutions, which are often delivered via integrated systems, driving billions in new market opportunities.

However, the market faces significant challenges, including the high initial investment cost of some advanced integrated systems, which can be a barrier for smaller enterprises. Regulatory hurdles, particularly regarding data governance, compliance, and cross-border data flows, add complexity to deployment, especially for multinational corporations. Supply chain issues, exacerbated by global events, can lead to component shortages and increased lead times, impacting product availability and pricing. Furthermore, intense competitive pressures from both established IT giants and agile startups force continuous innovation and aggressive pricing, potentially squeezing profit margins. Organizations also grapple with the challenge of integrating new integrated systems with legacy infrastructure, often requiring specialized expertise.

Growth Drivers in the Integrated Systems Solutions Market

The Integrated Systems Solutions market is fundamentally driven by the accelerating demand for simplified and agile IT infrastructure in an era of rapid digital transformation. Technologically, the maturation of virtualization, software-defined everything (SDX), and advanced analytics is enabling more efficient and powerful integrated solutions. The proliferation of hybrid and multi-cloud strategies mandates solutions that can seamlessly extend from on-premises to various cloud environments, a core offering of integrated systems. Economically, businesses are increasingly valuing the lower operational expenses and improved resource utilization that integrated platforms provide over traditional, siloed IT components. Policy-driven factors, such as global initiatives encouraging data center modernization and investments in critical infrastructure, further stimulate market expansion. The sheer volume of data generated by billions of IoT devices worldwide also fuels the need for integrated systems capable of processing and storing this information efficiently at the edge.

Challenges Impacting Integrated Systems Solutions Growth

Despite robust growth, the Integrated Systems Solutions market confronts several barriers and restraints that impact its full potential. The significant upfront capital expenditure required for certain high-end integrated systems remains a deterrent for budget-constrained organizations, particularly when compared to piecemeal component purchases, potentially costing enterprises billions in initial outlay. Regulatory complexities surrounding data privacy (e.g., GDPR, CCPA) and industry-specific compliance standards (e.g., HIPAA) necessitate intricate security and governance features, adding to development costs and deployment timelines. Global supply chain issues, including semiconductor shortages and logistics disruptions, have historically led to increased lead times and price volatility, impacting product availability and project schedules, estimated to have caused billions in delayed revenue across the IT sector. Moreover, the steep learning curve associated with managing highly integrated, complex solutions, coupled with a shortage of skilled IT professionals, presents an operational challenge for many adopters.

Key Players Shaping the Integrated Systems Solutions Market

- Dell

- Datrium

- Oracle

- Dell EMC

- NetApp

- Hewlett Packard

- BMC Software

- IBM

- Riverbed

- Hitachi Vantara

- Supermicro

- Diamanti

- Lenovo

- Gridstore

- Maxta

- NEC

- StorMagic

Significant Integrated Systems Solutions Industry Milestones

- 2019: Dell EMC launches its PowerFlex family, significantly expanding its software-defined storage and HCI portfolio, enabling greater flexibility and scalability for enterprise data centers.

- 2020: IBM introduces new hybrid cloud solutions built on integrated systems, emphasizing containerization and AI-driven automation for enterprise workloads, aiming to capture billions in market share.

- 2021: Oracle strengthens its Exadata Cloud@Customer offerings, blending on-premises integrated systems with cloud services, demonstrating a strong push towards hybrid cloud adoption for mission-critical databases.

- 2022: Hewlett Packard Enterprise (HPE) announces new GreenLake as-a-service offerings for its integrated systems, allowing customers to consume IT infrastructure on a utility basis, transforming capital expenditure to operational expenditure.

- 2023: Diamanti releases an updated product line focused specifically on bare-metal container platforms, addressing the growing demand for high-performance Kubernetes infrastructure, leading to billions in new investment.

- 2024: NetApp expands its integrated data management solutions, focusing on unified data services across hybrid and multi-cloud environments, ensuring seamless data mobility and protection across diverse integrated systems.

Future Outlook for Integrated Systems Solutions Market

The future of the Integrated Systems Solutions market is exceptionally bright, poised for continued exponential growth driven by a confluence of powerful catalysts. The ongoing global pursuit of digital transformation will continue to be the primary engine, pushing enterprises to adopt more agile, scalable, and simplified IT infrastructure. Strategic opportunities lie in the continuous evolution towards autonomous operations, where integrated systems will leverage advanced AI and machine learning to self-manage, self-optimize, and self-heal, significantly reducing human intervention and operational costs by billions. The expansion of edge computing and the widespread adoption of 5G will create massive demand for compact, powerful integrated systems deployed closer to data sources. Furthermore, the increasing focus on sustainability will drive innovation in energy-efficient designs and resource optimization. The market potential remains vast, with integrated systems becoming the foundational backbone for next-generation applications and services across every industry, promising a multi-trillion dollar opportunity for market players.

Integrated Systems Solutions Segmentation

-

1. Application

- 1.1. Integrated Stack System (ISS)

- 1.2. Integrated Infrastructure System (IIS)

- 1.3. Hyperconverged Integrated System (HCIS)

-

2. Types

- 2.1. Cloud-based

- 2.2. On-premises

Integrated Systems Solutions Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Integrated Systems Solutions Regional Market Share

Geographic Coverage of Integrated Systems Solutions

Integrated Systems Solutions REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Integrated Stack System (ISS)

- 5.1.2. Integrated Infrastructure System (IIS)

- 5.1.3. Hyperconverged Integrated System (HCIS)

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Cloud-based

- 5.2.2. On-premises

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Integrated Systems Solutions Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Integrated Stack System (ISS)

- 6.1.2. Integrated Infrastructure System (IIS)

- 6.1.3. Hyperconverged Integrated System (HCIS)

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Cloud-based

- 6.2.2. On-premises

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Integrated Systems Solutions Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Integrated Stack System (ISS)

- 7.1.2. Integrated Infrastructure System (IIS)

- 7.1.3. Hyperconverged Integrated System (HCIS)

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Cloud-based

- 7.2.2. On-premises

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Integrated Systems Solutions Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Integrated Stack System (ISS)

- 8.1.2. Integrated Infrastructure System (IIS)

- 8.1.3. Hyperconverged Integrated System (HCIS)

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Cloud-based

- 8.2.2. On-premises

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Integrated Systems Solutions Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Integrated Stack System (ISS)

- 9.1.2. Integrated Infrastructure System (IIS)

- 9.1.3. Hyperconverged Integrated System (HCIS)

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Cloud-based

- 9.2.2. On-premises

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Integrated Systems Solutions Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Integrated Stack System (ISS)

- 10.1.2. Integrated Infrastructure System (IIS)

- 10.1.3. Hyperconverged Integrated System (HCIS)

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Cloud-based

- 10.2.2. On-premises

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Integrated Systems Solutions Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Integrated Stack System (ISS)

- 11.1.2. Integrated Infrastructure System (IIS)

- 11.1.3. Hyperconverged Integrated System (HCIS)

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Cloud-based

- 11.2.2. On-premises

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Dell

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Datrium

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Oracle

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Dell EMC

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 NetApp

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Hewlett Packard

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 BMC Software

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 IBM

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Riverbed

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Hitachi Vantara

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Supermicro

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Diamanti

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Lenovo

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Gridstore

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Maxta

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 NEC

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 StorMagic

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.1 Dell

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Integrated Systems Solutions Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Integrated Systems Solutions Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Integrated Systems Solutions Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Integrated Systems Solutions Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Integrated Systems Solutions Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Integrated Systems Solutions Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Integrated Systems Solutions Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Integrated Systems Solutions Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Integrated Systems Solutions Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Integrated Systems Solutions Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Integrated Systems Solutions Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Integrated Systems Solutions Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Integrated Systems Solutions Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Integrated Systems Solutions Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Integrated Systems Solutions Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Integrated Systems Solutions Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Integrated Systems Solutions Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Integrated Systems Solutions Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Integrated Systems Solutions Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Integrated Systems Solutions Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Integrated Systems Solutions Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Integrated Systems Solutions Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Integrated Systems Solutions Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Integrated Systems Solutions Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Integrated Systems Solutions Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Integrated Systems Solutions Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Integrated Systems Solutions Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Integrated Systems Solutions Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Integrated Systems Solutions Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Integrated Systems Solutions Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Integrated Systems Solutions Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Integrated Systems Solutions Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Integrated Systems Solutions Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Integrated Systems Solutions Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Integrated Systems Solutions Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Integrated Systems Solutions Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Integrated Systems Solutions Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Integrated Systems Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Integrated Systems Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Integrated Systems Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Integrated Systems Solutions Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Integrated Systems Solutions Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Integrated Systems Solutions Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Integrated Systems Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Integrated Systems Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Integrated Systems Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Integrated Systems Solutions Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Integrated Systems Solutions Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Integrated Systems Solutions Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Integrated Systems Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Integrated Systems Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Integrated Systems Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Integrated Systems Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Integrated Systems Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Integrated Systems Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Integrated Systems Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Integrated Systems Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Integrated Systems Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Integrated Systems Solutions Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Integrated Systems Solutions Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Integrated Systems Solutions Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Integrated Systems Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Integrated Systems Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Integrated Systems Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Integrated Systems Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Integrated Systems Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Integrated Systems Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Integrated Systems Solutions Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Integrated Systems Solutions Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Integrated Systems Solutions Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Integrated Systems Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Integrated Systems Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Integrated Systems Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Integrated Systems Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Integrated Systems Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Integrated Systems Solutions Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Integrated Systems Solutions Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Integrated Systems Solutions?

The projected CAGR is approximately 7.6%.

2. Which companies are prominent players in the Integrated Systems Solutions?

Key companies in the market include Dell, Datrium, Oracle, Dell EMC, NetApp, Hewlett Packard, BMC Software, IBM, Riverbed, Hitachi Vantara, Supermicro, Diamanti, Lenovo, Gridstore, Maxta, NEC, StorMagic.

3. What are the main segments of the Integrated Systems Solutions?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 532.42 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Integrated Systems Solutions," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Integrated Systems Solutions report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Integrated Systems Solutions?

To stay informed about further developments, trends, and reports in the Integrated Systems Solutions, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence