Key Insights

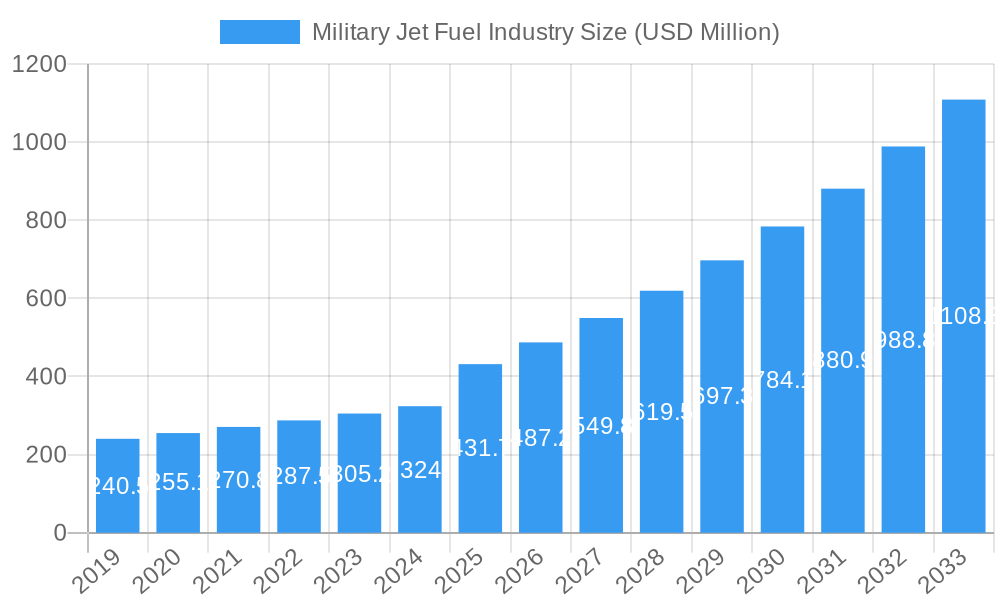

The global Military Jet Fuel market is poised for significant expansion, projected to reach USD 431.7 billion by 2025. This robust growth is driven by increasing geopolitical tensions and the continuous modernization of air forces worldwide. Nations are investing heavily in advanced fighter jets, bombers, and reconnaissance aircraft, necessitating a consistent and substantial supply of specialized jet fuels. The market is experiencing a CAGR of 12.8%, reflecting a strong demand trajectory fueled by an escalating need for high-performance aviation fuels that can withstand extreme operating conditions. Key drivers include the development of new military aviation platforms requiring fuels with enhanced energy density and thermal stability, coupled with a growing emphasis on ensuring energy security and operational readiness within defense sectors. The expansion of military exercises and strategic deployments further bolsters the demand for reliable and efficient jet fuel supply chains.

Military Jet Fuel Industry Market Size (In Million)

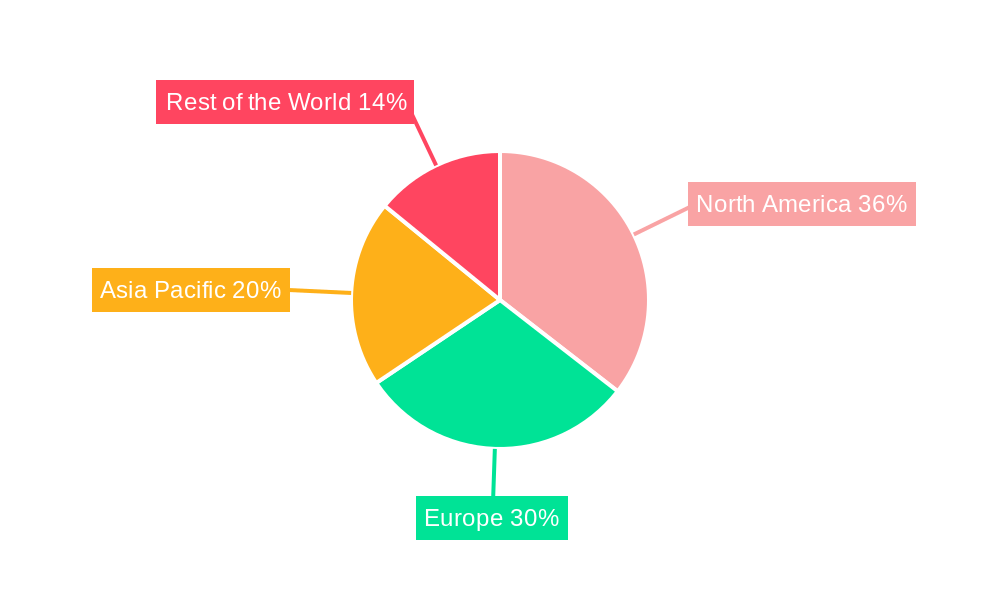

The market is segmented into Air Turbine Fuel and Renewable Aviation Fuel, with a growing focus on sustainable solutions to reduce the environmental footprint of military aviation. While traditional Air Turbine Fuel remains dominant, the integration of Renewable Aviation Fuel presents a significant long-term growth opportunity, driven by environmental regulations and the pursuit of energy independence. Key players such as Honeywell International Inc., Shell PLC, Exxonmobil Corporation, and BP PLC are actively investing in research and development to enhance fuel efficiency and explore sustainable fuel alternatives. Geographically, North America and Europe are expected to lead the market due to substantial defense budgets and the presence of advanced military aviation infrastructure. However, the Asia Pacific region, with its rapidly growing economies and increasing defense spending, is anticipated to exhibit the fastest growth rate in the coming years, driven by strategic military expansions and modernization programs.

Military Jet Fuel Industry Company Market Share

This comprehensive market research report offers an in-depth analysis of the global Military Jet Fuel market, projected to reach billions by 2033. Spanning the historical period from 2019 to 2024 and a robust forecast period from 2025 to 2033, with 2025 as the base and estimated year, this report is an indispensable resource for stakeholders seeking to understand market dynamics, capitalize on emerging opportunities, and mitigate potential challenges. We delve into key segments like Air Turbine Fuel and Renewable Aviation Fuel, analyze critical industry developments, and highlight the strategic moves of major players.

Military Jet Fuel Industry Market Structure & Competitive Landscape

The Military Jet Fuel market is characterized by a moderately concentrated structure, with a few multinational energy corporations and specialized fuel providers dominating global supply chains. Innovation drivers are primarily focused on enhancing fuel efficiency, reducing environmental impact through the adoption of sustainable aviation fuels, and ensuring supply chain resilience in volatile geopolitical landscapes. Regulatory impacts, including stringent environmental standards and defense procurement policies, significantly shape market entry and product development. Product substitutes, while limited in military applications due to strict performance requirements, are indirectly influenced by advancements in alternative propulsion technologies. End-user segmentation, based on military branches and specific aircraft types, dictates regional demand patterns and product specifications. Mergers and acquisitions (M&A) trends, valued in the billions, reflect a strategic consolidation to enhance market share, secure feedstock access, and expand technological capabilities. For instance, recent M&A activities are estimated to be in the range of billions of dollars annually, indicating intense competition and a drive for vertical integration. Concentration ratios (CR4) are estimated to be around xx%, underscoring the influence of key players.

Military Jet Fuel Industry Market Trends & Opportunities

The Military Jet Fuel market is poised for substantial growth, with an anticipated Compound Annual Growth Rate (CAGR) of xx% from 2025 to 2033, driving its valuation into the billions. This expansion is fueled by increasing global defense expenditures, modernization programs for air forces worldwide, and a growing emphasis on the strategic importance of secure and reliable fuel supplies. Technological shifts are a significant trend, with a strong push towards developing and scaling up renewable aviation fuels (RAFs) for military applications. This includes advanced biofuels and synthetic fuels designed to meet stringent military specifications while reducing carbon footprints. Consumer preferences, in this context, are dictated by operational requirements, cost-effectiveness, and increasingly, environmental sustainability mandates from governmental bodies. Competitive dynamics are intensifying, with established players investing heavily in R&D for sustainable alternatives and fortified supply chains to mitigate geopolitical risks. Market penetration rates for advanced fuels are projected to increase from xx% in 2025 to xx% by 2033, presenting substantial opportunities for early adopters and innovators. The market size is expected to grow from an estimated billions in 2025 to billions by 2033. The increasing deployment of advanced fighter jets and unmanned aerial vehicles (UAVs) further accentuates the demand for high-performance jet fuels. Furthermore, the strategic imperative for energy independence and diversification within defense sectors globally is creating a fertile ground for both conventional and alternative fuel suppliers.

Dominant Markets & Segments in Military Jet Fuel Industry

The dominant market segment within the Military Jet Fuel industry is undoubtedly Air Turbine Fuel, driven by the extensive use of conventional jet fuels across all branches of military aviation, including fighter jets, bombers, transport aircraft, and helicopters. The global market for Air Turbine Fuel is estimated to be valued at billions in 2025, representing the lion's share of the overall military jet fuel market. Key growth drivers for this segment include ongoing military modernization programs in major economies, increased operational tempo of air forces, and the sheer volume of aircraft requiring sustained fuel supply for training and deployment. Infrastructure plays a crucial role, with established refueling networks at military bases worldwide underpinning demand. Policies related to defense procurement and strategic reserves also contribute to the steady demand for Air Turbine Fuel.

Conversely, Renewable Aviation Fuel is the rapidly emerging segment, albeit with a smaller current market share, estimated at billions in 2025. However, it exhibits a significantly higher growth potential. Key growth drivers for RAF include stringent government mandates for decarbonization, the desire to reduce reliance on fossil fuels, and advancements in sustainable fuel production technologies. Policies promoting the use of sustainable aviation fuels (SAFs), coupled with investments in bio-refineries and synthetic fuel production, are critical. The competitive advantage for RAF lies in its environmental benefits and its potential to enhance energy security by diversifying feedstock. While infrastructure development for RAF is still in its nascent stages compared to conventional fuels, strategic partnerships and government incentives are accelerating its adoption. The projected CAGR for RAF is expected to be xx%, significantly higher than that of Air Turbine Fuel, indicating a substantial shift towards more sustainable military aviation in the long term.

Military Jet Fuel Industry Product Analysis

Military jet fuels, primarily Air Turbine Fuel (e.g., JP-8, JP-5) and increasingly, Renewable Aviation Fuel (RAF), are engineered for extreme performance under diverse operational conditions. Innovations focus on improving energy density, thermal stability, and cold-weather operability. Competitive advantages stem from the ability to meet stringent military specifications, ensuring aircraft safety and mission readiness. Advanced formulations are also addressing reduced emissions and improved lubricity. The market is witnessing a rise in specialized RAF blends designed to offer comparable or superior performance to conventional fuels, supporting the military's decarbonization goals without compromising operational effectiveness.

Key Drivers, Barriers & Challenges in Military Jet Fuel Industry

Key Drivers:

- Escalating Global Defense Budgets: Increased geopolitical tensions and modernization efforts by global defense forces are driving higher demand for military aviation fuels, estimated to add billions to the market.

- Technological Advancements in Aircraft: The introduction of next-generation fighter jets and drones necessitates advanced fuel formulations with higher energy density and stability.

- Push for Energy Security and Independence: Nations are prioritizing secure and diversified fuel sources to reduce reliance on volatile global markets.

- Environmental Regulations and Sustainability Goals: Growing pressure to reduce the carbon footprint of military operations is accelerating the adoption of Renewable Aviation Fuels (RAFs).

Key Barriers & Challenges:

- High Cost of Renewable Aviation Fuel Production: The current cost of producing RAF is significantly higher than conventional jet fuels, impacting widespread adoption, with cost premiums estimated at xx%.

- Limited Infrastructure for RAF: The absence of robust and widespread infrastructure for the production, distribution, and storage of RAF poses a significant hurdle.

- Stringent Military Specifications and Qualification Processes: Gaining military approval for new fuel formulations, especially RAF, is a lengthy and rigorous process, often taking years and costing millions.

- Geopolitical Instability and Supply Chain Disruptions: Conflicts and trade tensions can severely impact the availability and pricing of raw materials for both conventional and renewable fuels, with potential economic impacts in the billions.

- Competition from Alternative Energy Sources: While not yet direct substitutes for high-performance jet engines, long-term advancements in electric or hydrogen propulsion could eventually influence fuel demand.

Growth Drivers in the Military Jet Fuel Industry Market

Key growth drivers in the Military Jet Fuel market include robust government investments in defense modernization programs, projected to exceed billions annually. Technological advancements in aircraft design, demanding higher-performance fuels, are another significant catalyst. The global imperative for energy security and reduced carbon emissions is compelling defense ministries to explore and adopt Renewable Aviation Fuels (RAFs), creating new market opportunities estimated at billions of dollars. Policy support, including mandates and incentives for sustainable fuel development, is crucial for driving this transition.

Challenges Impacting Military Jet Fuel Industry Growth

Challenges impacting Military Jet Fuel industry growth are multifaceted. The substantial cost premium associated with Renewable Aviation Fuels (RAFs) remains a significant barrier, with production costs often xx% higher than conventional fuels. Developing the necessary infrastructure for RAF production and distribution requires massive capital investment, estimated in the billions. Furthermore, the rigorous and time-consuming qualification processes for new fuel types within military organizations present a hurdle to rapid adoption. Supply chain vulnerabilities, exacerbated by geopolitical instability, can lead to price volatility and supply disruptions.

Key Players Shaping the Military Jet Fuel Industry Market

- Honeywell International Inc

- Shell PLC

- Exxonmobil Corporation

- Totalenergies SE

- Chevron Corporation

- GS Caltex Corporation

- BP PLC

- Repsol SA

Significant Military Jet Fuel Industry Industry Milestones

- July 2023: Viva Energy Refining Pty Ltd (Viva Energy) secured a significant contract with the Department of Defense to supply aviation, marine, and ground fuel to the Australian Defense Force (ADF). This Fuel Supply Contract, with an initial six-year term extendable to 12 years, highlights the ongoing demand for reliable fuel sources and includes plans to resume production of F-44 (Avcat) or JP-5 at the Geelong Refinery, a critical military-grade aviation turbine fuel.

- March 2023: The United States imposed sanctions on two individuals and six entities connected to Myanmar's military regime, significantly impacting the jet fuel supply for the country's armed forces. Three of the sanctioned entities were directly involved in the import, storage, and distribution of aviation fuel for Myanmar's military, illustrating the geopolitical leverage and supply chain vulnerabilities in the sector.

Future Outlook for Military Jet Fuel Industry Market

The future outlook for the Military Jet Fuel market is characterized by a dual trajectory of sustained demand for conventional fuels and accelerated growth in Renewable Aviation Fuels (RAFs). Strategic investments by major players in R&D for advanced biofuels and synthetic fuels, coupled with increasing government mandates for sustainability, are expected to propel the RAF market into the billions of dollars range. The focus will be on developing cost-effective production methods, expanding infrastructure, and ensuring these sustainable alternatives meet stringent military performance requirements. Diversification of supply chains and enhanced resilience against geopolitical disruptions will remain paramount. Opportunities lie in innovation for high-performance sustainable fuels, advanced logistics solutions, and strategic partnerships to navigate regulatory landscapes and capitalize on evolving defense needs, projected to reshape the global market worth billions.

Military Jet Fuel Industry Segmentation

-

1. Fuel Type

- 1.1. Air Turbine Fuel

- 1.2. Renewable Avaition Fuel

Military Jet Fuel Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Rest of North America

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. Italy

- 2.4. France

- 2.5. Russia

- 2.6. Rest of North America

-

3. Asia Pacific

- 3.1. China

- 3.2. India

- 3.3. Japan

- 3.4. South Korea

- 3.5. Rest of Asia Pacific

-

4. Rest of the World

- 4.1. Saudi Arabia

- 4.2. United Arab Emirates

- 4.3. South Africa

- 4.4. Algeria

Military Jet Fuel Industry Regional Market Share

Geographic Coverage of Military Jet Fuel Industry

Military Jet Fuel Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 14.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Fuel Type

- 5.1.1. Air Turbine Fuel

- 5.1.2. Renewable Avaition Fuel

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. Europe

- 5.2.3. Asia Pacific

- 5.2.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Fuel Type

- 6. Global Military Jet Fuel Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Fuel Type

- 6.1.1. Air Turbine Fuel

- 6.1.2. Renewable Avaition Fuel

- 6.1. Market Analysis, Insights and Forecast - by Fuel Type

- 7. North America Military Jet Fuel Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Fuel Type

- 7.1.1. Air Turbine Fuel

- 7.1.2. Renewable Avaition Fuel

- 7.1. Market Analysis, Insights and Forecast - by Fuel Type

- 8. Europe Military Jet Fuel Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Fuel Type

- 8.1.1. Air Turbine Fuel

- 8.1.2. Renewable Avaition Fuel

- 8.1. Market Analysis, Insights and Forecast - by Fuel Type

- 9. Asia Pacific Military Jet Fuel Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Fuel Type

- 9.1.1. Air Turbine Fuel

- 9.1.2. Renewable Avaition Fuel

- 9.1. Market Analysis, Insights and Forecast - by Fuel Type

- 10. Rest of the World Military Jet Fuel Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Fuel Type

- 10.1.1. Air Turbine Fuel

- 10.1.2. Renewable Avaition Fuel

- 10.1. Market Analysis, Insights and Forecast - by Fuel Type

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Honeywell International Inc

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 Shell PLC

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 Exxonmobil Corporation

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Totalenergies SE

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 Chevron Corporation

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 GS Caltex Corporation

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 BP PLC

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Repsol SA

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.1 Honeywell International Inc

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global Military Jet Fuel Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Global Military Jet Fuel Industry Volume Breakdown (Litre, %) by Region 2025 & 2033

- Figure 3: North America Military Jet Fuel Industry Revenue (billion), by Fuel Type 2025 & 2033

- Figure 4: North America Military Jet Fuel Industry Volume (Litre), by Fuel Type 2025 & 2033

- Figure 5: North America Military Jet Fuel Industry Revenue Share (%), by Fuel Type 2025 & 2033

- Figure 6: North America Military Jet Fuel Industry Volume Share (%), by Fuel Type 2025 & 2033

- Figure 7: North America Military Jet Fuel Industry Revenue (billion), by Country 2025 & 2033

- Figure 8: North America Military Jet Fuel Industry Volume (Litre), by Country 2025 & 2033

- Figure 9: North America Military Jet Fuel Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: North America Military Jet Fuel Industry Volume Share (%), by Country 2025 & 2033

- Figure 11: Europe Military Jet Fuel Industry Revenue (billion), by Fuel Type 2025 & 2033

- Figure 12: Europe Military Jet Fuel Industry Volume (Litre), by Fuel Type 2025 & 2033

- Figure 13: Europe Military Jet Fuel Industry Revenue Share (%), by Fuel Type 2025 & 2033

- Figure 14: Europe Military Jet Fuel Industry Volume Share (%), by Fuel Type 2025 & 2033

- Figure 15: Europe Military Jet Fuel Industry Revenue (billion), by Country 2025 & 2033

- Figure 16: Europe Military Jet Fuel Industry Volume (Litre), by Country 2025 & 2033

- Figure 17: Europe Military Jet Fuel Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Europe Military Jet Fuel Industry Volume Share (%), by Country 2025 & 2033

- Figure 19: Asia Pacific Military Jet Fuel Industry Revenue (billion), by Fuel Type 2025 & 2033

- Figure 20: Asia Pacific Military Jet Fuel Industry Volume (Litre), by Fuel Type 2025 & 2033

- Figure 21: Asia Pacific Military Jet Fuel Industry Revenue Share (%), by Fuel Type 2025 & 2033

- Figure 22: Asia Pacific Military Jet Fuel Industry Volume Share (%), by Fuel Type 2025 & 2033

- Figure 23: Asia Pacific Military Jet Fuel Industry Revenue (billion), by Country 2025 & 2033

- Figure 24: Asia Pacific Military Jet Fuel Industry Volume (Litre), by Country 2025 & 2033

- Figure 25: Asia Pacific Military Jet Fuel Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Military Jet Fuel Industry Volume Share (%), by Country 2025 & 2033

- Figure 27: Rest of the World Military Jet Fuel Industry Revenue (billion), by Fuel Type 2025 & 2033

- Figure 28: Rest of the World Military Jet Fuel Industry Volume (Litre), by Fuel Type 2025 & 2033

- Figure 29: Rest of the World Military Jet Fuel Industry Revenue Share (%), by Fuel Type 2025 & 2033

- Figure 30: Rest of the World Military Jet Fuel Industry Volume Share (%), by Fuel Type 2025 & 2033

- Figure 31: Rest of the World Military Jet Fuel Industry Revenue (billion), by Country 2025 & 2033

- Figure 32: Rest of the World Military Jet Fuel Industry Volume (Litre), by Country 2025 & 2033

- Figure 33: Rest of the World Military Jet Fuel Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Rest of the World Military Jet Fuel Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Military Jet Fuel Industry Revenue billion Forecast, by Fuel Type 2020 & 2033

- Table 2: Global Military Jet Fuel Industry Volume Litre Forecast, by Fuel Type 2020 & 2033

- Table 3: Global Military Jet Fuel Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Military Jet Fuel Industry Volume Litre Forecast, by Region 2020 & 2033

- Table 5: Global Military Jet Fuel Industry Revenue billion Forecast, by Fuel Type 2020 & 2033

- Table 6: Global Military Jet Fuel Industry Volume Litre Forecast, by Fuel Type 2020 & 2033

- Table 7: Global Military Jet Fuel Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 8: Global Military Jet Fuel Industry Volume Litre Forecast, by Country 2020 & 2033

- Table 9: United States Military Jet Fuel Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: United States Military Jet Fuel Industry Volume (Litre) Forecast, by Application 2020 & 2033

- Table 11: Canada Military Jet Fuel Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Canada Military Jet Fuel Industry Volume (Litre) Forecast, by Application 2020 & 2033

- Table 13: Rest of North America Military Jet Fuel Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Rest of North America Military Jet Fuel Industry Volume (Litre) Forecast, by Application 2020 & 2033

- Table 15: Global Military Jet Fuel Industry Revenue billion Forecast, by Fuel Type 2020 & 2033

- Table 16: Global Military Jet Fuel Industry Volume Litre Forecast, by Fuel Type 2020 & 2033

- Table 17: Global Military Jet Fuel Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 18: Global Military Jet Fuel Industry Volume Litre Forecast, by Country 2020 & 2033

- Table 19: Germany Military Jet Fuel Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Military Jet Fuel Industry Volume (Litre) Forecast, by Application 2020 & 2033

- Table 21: United Kingdom Military Jet Fuel Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: United Kingdom Military Jet Fuel Industry Volume (Litre) Forecast, by Application 2020 & 2033

- Table 23: Italy Military Jet Fuel Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Italy Military Jet Fuel Industry Volume (Litre) Forecast, by Application 2020 & 2033

- Table 25: France Military Jet Fuel Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: France Military Jet Fuel Industry Volume (Litre) Forecast, by Application 2020 & 2033

- Table 27: Russia Military Jet Fuel Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Russia Military Jet Fuel Industry Volume (Litre) Forecast, by Application 2020 & 2033

- Table 29: Rest of North America Military Jet Fuel Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Rest of North America Military Jet Fuel Industry Volume (Litre) Forecast, by Application 2020 & 2033

- Table 31: Global Military Jet Fuel Industry Revenue billion Forecast, by Fuel Type 2020 & 2033

- Table 32: Global Military Jet Fuel Industry Volume Litre Forecast, by Fuel Type 2020 & 2033

- Table 33: Global Military Jet Fuel Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 34: Global Military Jet Fuel Industry Volume Litre Forecast, by Country 2020 & 2033

- Table 35: China Military Jet Fuel Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: China Military Jet Fuel Industry Volume (Litre) Forecast, by Application 2020 & 2033

- Table 37: India Military Jet Fuel Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: India Military Jet Fuel Industry Volume (Litre) Forecast, by Application 2020 & 2033

- Table 39: Japan Military Jet Fuel Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Japan Military Jet Fuel Industry Volume (Litre) Forecast, by Application 2020 & 2033

- Table 41: South Korea Military Jet Fuel Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: South Korea Military Jet Fuel Industry Volume (Litre) Forecast, by Application 2020 & 2033

- Table 43: Rest of Asia Pacific Military Jet Fuel Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: Rest of Asia Pacific Military Jet Fuel Industry Volume (Litre) Forecast, by Application 2020 & 2033

- Table 45: Global Military Jet Fuel Industry Revenue billion Forecast, by Fuel Type 2020 & 2033

- Table 46: Global Military Jet Fuel Industry Volume Litre Forecast, by Fuel Type 2020 & 2033

- Table 47: Global Military Jet Fuel Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 48: Global Military Jet Fuel Industry Volume Litre Forecast, by Country 2020 & 2033

- Table 49: Saudi Arabia Military Jet Fuel Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 50: Saudi Arabia Military Jet Fuel Industry Volume (Litre) Forecast, by Application 2020 & 2033

- Table 51: United Arab Emirates Military Jet Fuel Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 52: United Arab Emirates Military Jet Fuel Industry Volume (Litre) Forecast, by Application 2020 & 2033

- Table 53: South Africa Military Jet Fuel Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 54: South Africa Military Jet Fuel Industry Volume (Litre) Forecast, by Application 2020 & 2033

- Table 55: Algeria Military Jet Fuel Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 56: Algeria Military Jet Fuel Industry Volume (Litre) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Military Jet Fuel Industry?

The projected CAGR is approximately 14.3%.

2. Which companies are prominent players in the Military Jet Fuel Industry?

Key companies in the market include Honeywell International Inc, Shell PLC, Exxonmobil Corporation, Totalenergies SE, Chevron Corporation, GS Caltex Corporation, BP PLC, Repsol SA.

3. What are the main segments of the Military Jet Fuel Industry?

The market segments include Fuel Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 11.3 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Modernization and Upgrades of Existing Military Aircraft Fleets4.; Increasing Defense Budgets.

6. What are the notable trends driving market growth?

Renewable Aviation Fuel to be the Fastest Growing Market.

7. Are there any restraints impacting market growth?

4.; Shift Toward Unmanned Aircraft.

8. Can you provide examples of recent developments in the market?

July 2023: Viva Energy Refining Pty Ltd (Viva Energy) secured a contract with the Department of Defense to supply aviation, marine, and ground fuel to the Australian Defense Force (ADF). The Fuel Supply Contract is for an initial six-year term which may be extended to 12 years. As part of the deal and an essential Australian Industry Capability activity, Viva Energy is expected to resume production at Geelong Refinery of F-44 (Avcat) or JP-5, a military specification aviation turbine fuel used on aircraft carriers.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in Litre.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Military Jet Fuel Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Military Jet Fuel Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Military Jet Fuel Industry?

To stay informed about further developments, trends, and reports in the Military Jet Fuel Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence