Key Insights

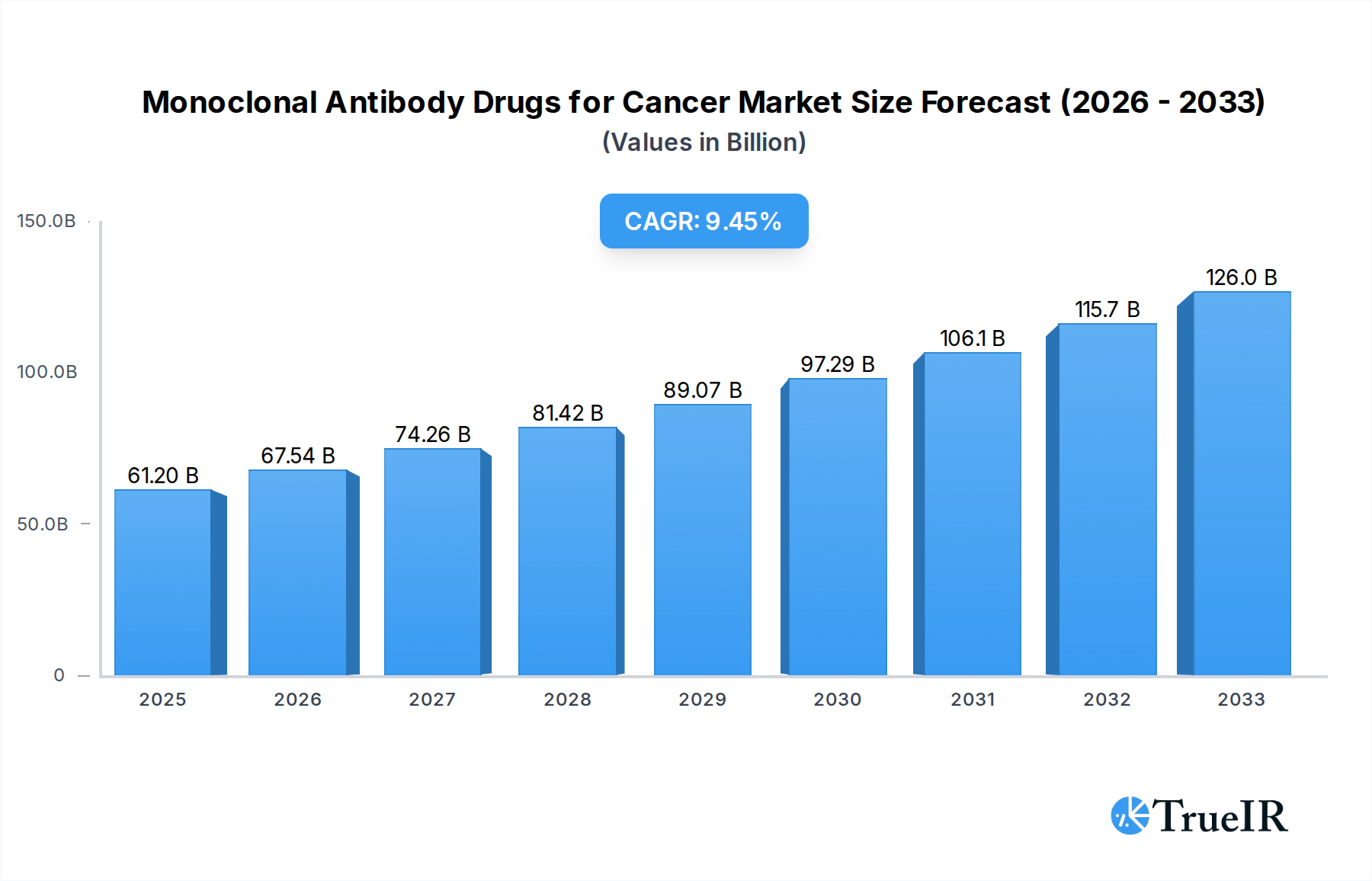

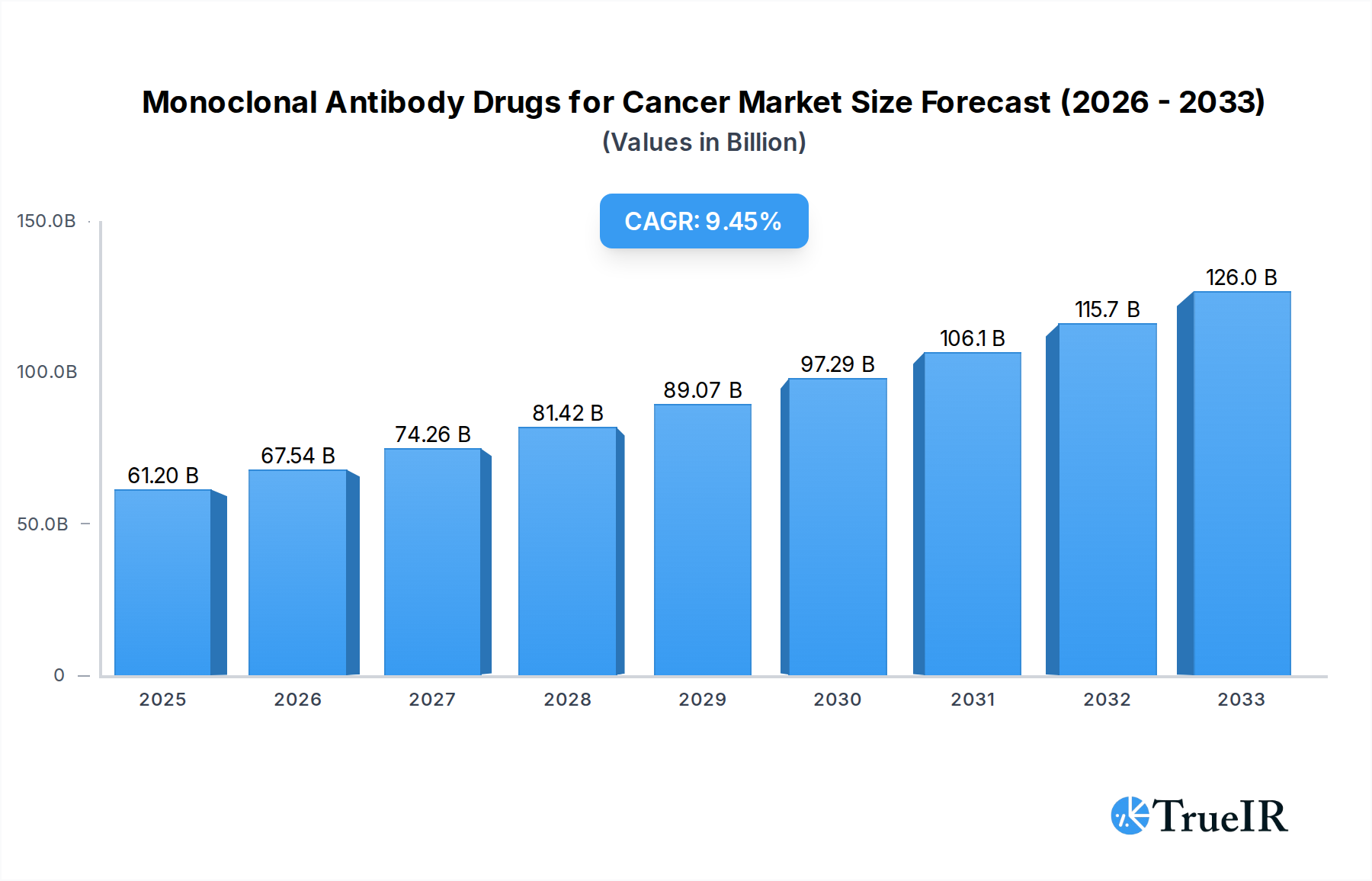

The global market for Monoclonal Antibody Drugs for Cancer is poised for significant expansion, projected to reach $61.2 billion in 2025. This robust growth is driven by a confluence of factors including advancements in precision medicine, a rising incidence of various cancers, and increasing investments in research and development by leading pharmaceutical giants. The market is expected to exhibit a compound annual growth rate (CAGR) of 10.4% from 2025 to 2033, indicating a sustained upward trajectory. Key therapeutic areas like Lung Cancer, Breast Cancer, and Prostate Cancer are leading the charge, with ongoing clinical trials and approvals of novel antibody-based therapies bolstering market performance. The development of innovative antibody types, such as humanized and chimeric antibodies, offers improved efficacy and reduced immunogenicity, further fueling market demand.

Monoclonal Antibody Drugs for Cancer Market Size (In Billion)

The competitive landscape is characterized by the presence of major players like Johnson & Johnson, Novartis, Gilead Sciences, and Roche, who are actively involved in developing and commercializing cutting-edge monoclonal antibody treatments. Emerging markets, particularly in the Asia Pacific region, are presenting new opportunities for growth due to increasing healthcare expenditure and a growing focus on advanced cancer therapies. While the market benefits from strong drivers, potential restraints such as high drug development costs and stringent regulatory approvals need to be carefully navigated by market participants. Nevertheless, the continuous innovation in antibody engineering and the expanding pipeline of targeted therapies suggest a highly promising future for monoclonal antibody drugs in the fight against cancer.

Monoclonal Antibody Drugs for Cancer Company Market Share

Monoclonal Antibody Drugs for Cancer: A Comprehensive Market Analysis (2019-2033)

This in-depth report provides a dynamic, SEO-optimized analysis of the Monoclonal Antibody Drugs for Cancer market, leveraging high-volume keywords to enhance search rankings and engage industry professionals. Covering the study period from 2019 to 2033, with a base year of 2025 and a forecast period extending to 2033, this report offers crucial insights into market dynamics, competitive landscapes, and future trajectories for stakeholders seeking to capitalize on this rapidly evolving sector.

Monoclonal Antibody Drugs for Cancer Market Structure & Competitive Landscape

The global monoclonal antibody drugs for cancer market is characterized by a dynamic and increasingly concentrated competitive landscape. Leading players like Johnson & Johnson, Novartis, Gilead Sciences, Roche, Bristol-Myers Squibb, Amgen, AstraZeneca, Merck & Co, Takeda, Merck KGaA, Seagen, Eli Lilly, Ono Pharmaceutical, Pfizer, Regeneron, Innovent, and Hengrui Medicine are driving innovation and market share. The industry concentration is significant, with the top 5 companies holding an estimated 70% of the market share in 2025. Innovation drivers are primarily focused on enhancing drug efficacy, reducing side effects through targeted therapy, and developing novel immunotherapies. Regulatory impacts are substantial, with stringent approval processes for new drug applications (NDAs) and ongoing post-market surveillance influencing market entry and expansion. Product substitutes, while evolving, are currently limited, with small molecule inhibitors and traditional chemotherapy representing the primary alternatives, albeit with distinct treatment profiles and efficacy. End-user segmentation, predominantly hospitals and specialized cancer treatment centers, plays a crucial role in drug distribution and adoption. Mergers and acquisitions (M&A) trends are evident, with an estimated 15 significant M&A deals projected between 2021 and 2025, collectively valued at over $50 billion, aimed at consolidating portfolios and acquiring cutting-edge technologies.

Monoclonal Antibody Drugs for Cancer Market Trends & Opportunities

The global market for monoclonal antibody drugs for cancer is experiencing robust growth, projected to reach a valuation of approximately $150 billion by 2025 and expand to over $300 billion by 2033. This significant expansion is underpinned by a Compound Annual Growth Rate (CAGR) of approximately 12% during the forecast period. Technological shifts are paramount, with a continuous drive towards precision medicine and personalized treatment approaches. The development of bispecific antibodies, antibody-drug conjugates (ADCs), and next-generation immunotherapies is revolutionizing cancer treatment by offering enhanced specificity and reduced systemic toxicity. Consumer preferences are increasingly aligned with treatments that offer improved quality of life and superior efficacy, driving demand for these advanced biologic therapies. Competitive dynamics are characterized by intense research and development (R&D) efforts, strategic partnerships, and a race to secure intellectual property. Market penetration rates for monoclonal antibodies are steadily increasing across various cancer types, moving beyond established indications to address more complex and previously untreatable malignancies. The growing prevalence of cancer globally, coupled with advancements in diagnostic technologies that enable earlier and more accurate cancer detection, further fuels market expansion. The integration of artificial intelligence (AI) and machine learning (ML) in drug discovery and development is accelerating the identification of novel targets and the optimization of antibody design, promising to further streamline the R&D pipeline and reduce time-to-market for new therapeutic agents. The expanding healthcare infrastructure in emerging economies and increasing patient affordability for advanced therapies also present significant opportunities for market growth. Furthermore, the ongoing research into the tumor microenvironment and immune checkpoints is unlocking new therapeutic avenues, leading to the development of combination therapies that leverage the synergistic effects of multiple monoclonal antibodies or combine them with other treatment modalities.

Dominant Markets & Segments in Monoclonal Antibody Drugs for Cancer

The Lung Cancer segment stands as the dominant application within the monoclonal antibody drugs for cancer market, projected to account for over 30% of the market share in 2025. This dominance is driven by the high incidence and mortality rates associated with lung cancer globally, as well as the significant advancements in immunotherapy and targeted therapies specifically developed for this disease. Key growth drivers in this segment include robust clinical trial data demonstrating improved survival rates and patient outcomes, favorable reimbursement policies for advanced cancer treatments, and continuous pipeline development by major pharmaceutical companies.

Within the Types of monoclonal antibodies, Humanized Antibodies are expected to lead the market, capturing an estimated 50% of the market share in 2025. This is attributed to their reduced immunogenicity compared to mouse-derived or chimeric antibodies, leading to better patient tolerance and longer treatment durations. The ongoing refinement of humanization techniques and the successful clinical translation of numerous humanized antibody drugs have solidified their position.

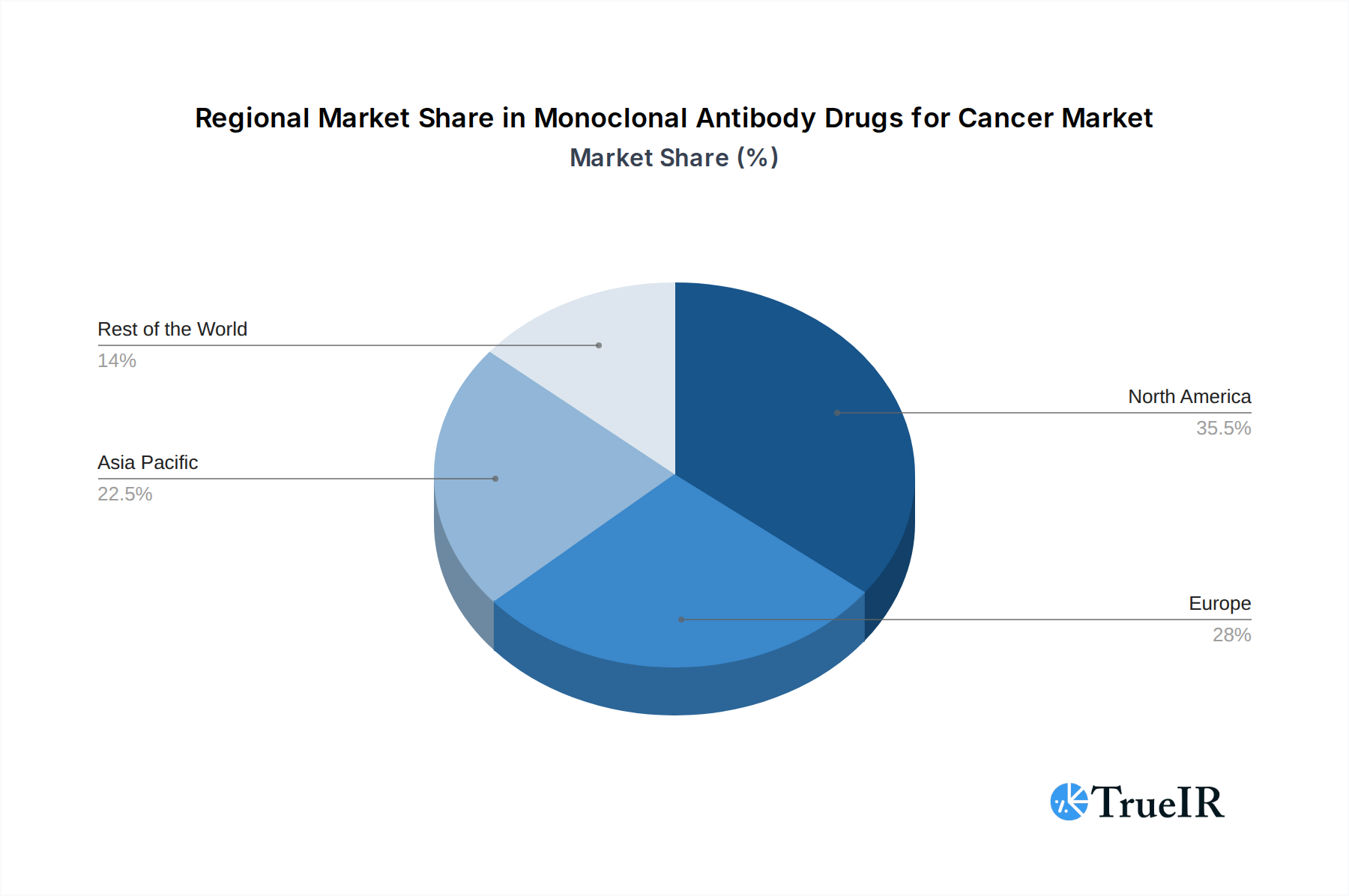

Geographically, North America is the leading market for monoclonal antibody drugs for cancer, driven by a well-established healthcare system, high healthcare expenditure, early adoption of innovative therapies, and a strong presence of leading pharmaceutical companies engaged in extensive R&D. The United States, in particular, represents a significant portion of this market, fueled by robust clinical research infrastructure and a favorable regulatory environment for drug approvals.

The Breast Cancer segment is another major contributor to market growth, driven by high prevalence, ongoing research into novel therapeutic targets, and the availability of effective monoclonal antibody treatments that improve both survival and quality of life. The Blood-related Cancer segment, including hematological malignancies like leukemia and lymphoma, also exhibits strong growth due to the success of targeted therapies and immunotherapies in these specific cancer types.

Monoclonal Antibody Drugs for Cancer Product Analysis

Product innovation in monoclonal antibody drugs for cancer is rapidly advancing, focusing on enhanced specificity, reduced off-target effects, and novel mechanisms of action. Antibody-drug conjugates (ADCs), combining the targeting ability of monoclonal antibodies with the cytotoxic payload of chemotherapy, are offering highly potent and localized cancer cell destruction. Bispecific antibodies, capable of binding to two different antigens simultaneously, are revolutionizing immunotherapy by bridging immune cells to cancer cells or by simultaneously targeting multiple oncogenic pathways. These advancements translate into significant competitive advantages, including improved treatment efficacy, reduced side effects, and the potential to overcome drug resistance.

Key Drivers, Barriers & Challenges in Monoclonal Antibody Drugs for Cancer

The monoclonal antibody drugs for cancer market is propelled by several key drivers. Technological advancements, particularly in genetic engineering and antibody engineering, are enabling the development of more potent and targeted therapies. The increasing global cancer incidence and mortality rates create a continuous demand for innovative treatment options. Supportive government initiatives and favorable reimbursement policies in many regions incentivize the development and adoption of these advanced therapies.

However, significant barriers and challenges exist. The high cost of research, development, and manufacturing for monoclonal antibodies presents a major hurdle, leading to expensive treatments that can strain healthcare systems and limit patient access. Complex and lengthy regulatory approval processes, though essential for patient safety, can delay market entry. Supply chain complexities, especially for biologics requiring specialized storage and transportation, pose logistical challenges. Intense competition among key players can lead to pricing pressures and the need for continuous innovation to maintain market share.

Growth Drivers in the Monoclonal Antibody Drugs for Cancer Market

Key growth drivers in the monoclonal antibody drugs for cancer market include the accelerating pace of technological innovation, such as the refinement of antibody-drug conjugates (ADCs) and bispecific antibodies, offering enhanced precision and efficacy. The growing global cancer burden, particularly in aging populations, creates a substantial and expanding patient pool requiring advanced treatment modalities. Favorable regulatory landscapes in developed nations, coupled with increasing healthcare expenditure and evolving reimbursement policies, are facilitating market access and patient affordability for these high-value therapies. The expanding understanding of cancer biology and the tumor microenvironment is continuously uncovering novel therapeutic targets, fueling pipeline development and market expansion.

Challenges Impacting Monoclonal Antibody Drugs for Cancer Growth

Challenges impacting the growth of the monoclonal antibody drugs for cancer market are multifaceted. The substantial cost associated with the research, development, and manufacturing of these complex biologics leads to high drug prices, creating significant financial burdens on patients and healthcare systems, and potentially limiting accessibility in resource-constrained regions. Stringent and protracted regulatory approval pathways, while critical for ensuring patient safety, can significantly delay the commercialization of new therapies and lead to substantial investment risks. The intricate and sensitive nature of the biologics supply chain, requiring specialized cold chain logistics and stringent quality control measures, presents ongoing operational and logistical hurdles. Furthermore, intense competition among major pharmaceutical companies necessitates continuous innovation and significant investment in R&D to maintain a competitive edge and secure market share, often leading to patent expirative cliffs for blockbuster drugs and the need for robust pipeline diversification.

Key Players Shaping the Monoclonal Antibody Drugs for Cancer Market

- Johnson & Johnson

- Novartis

- Gilead Sciences

- Roche

- Bristol-Myers Squibb

- Amgen

- AstraZeneca

- Merck & Co

- Takeda

- Merck KGaA

- Seagen

- Eli Lilly

- Ono Pharmaceutical

- Pfizer

- Regeneron

- Innovent

- Hengrui Medicine

Significant Monoclonal Antibody Drugs for Cancer Industry Milestones

- 2019: Approval of [Specific Drug Name] for [Specific Cancer Type] marking a significant advancement in targeted therapy.

- 2020: Roche's strong pipeline development and key regulatory approvals in [Specific Cancer Type] bolstered its market leadership.

- 2021: Bristol-Myers Squibb's strategic acquisition of [Acquired Company Name] for $XX billion to strengthen its immuno-oncology portfolio.

- 2022: Pfizer's significant investment in antibody-drug conjugate (ADC) research and development, aiming to capture a larger share of the oncology market.

- 2023: Gilead Sciences' progress in clinical trials for novel monoclonal antibodies targeting [Specific Cancer Type] showing promising results.

- 2024: Seagen's continued success with its ADC portfolio, leading to increased market penetration for [Specific Drug Name].

Future Outlook for Monoclonal Antibody Drugs for Cancer Market

The future outlook for the monoclonal antibody drugs for cancer market is exceptionally bright, driven by continued innovation in personalized medicine and immunotherapies. The increasing integration of AI and machine learning in drug discovery will accelerate the development of novel targets and more efficacious antibodies. Expansion into new therapeutic areas and combination therapies will further broaden the market reach. Strategic partnerships and collaborations between pharmaceutical companies, academic institutions, and technology providers will be crucial for overcoming R&D challenges and accelerating market entry. The growing demand for targeted treatments that minimize side effects and improve patient outcomes will continue to fuel significant growth, positioning monoclonal antibodies as a cornerstone of future cancer treatment paradigms.

Monoclonal Antibody Drugs for Cancer Segmentation

-

1. Application

- 1.1. Lung Cancer

- 1.2. Breast Cancer

- 1.3. Prostate Cancer

- 1.4. Blood-related Cancer

- 1.5. Other

-

2. Types

- 2.1. Mouse-derived Antibodies

- 2.2. Chimeric Antibodies

- 2.3. Humanized Antibodies

Monoclonal Antibody Drugs for Cancer Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Monoclonal Antibody Drugs for Cancer Regional Market Share

Geographic Coverage of Monoclonal Antibody Drugs for Cancer

Monoclonal Antibody Drugs for Cancer REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Lung Cancer

- 5.1.2. Breast Cancer

- 5.1.3. Prostate Cancer

- 5.1.4. Blood-related Cancer

- 5.1.5. Other

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Mouse-derived Antibodies

- 5.2.2. Chimeric Antibodies

- 5.2.3. Humanized Antibodies

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Monoclonal Antibody Drugs for Cancer Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Lung Cancer

- 6.1.2. Breast Cancer

- 6.1.3. Prostate Cancer

- 6.1.4. Blood-related Cancer

- 6.1.5. Other

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Mouse-derived Antibodies

- 6.2.2. Chimeric Antibodies

- 6.2.3. Humanized Antibodies

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Monoclonal Antibody Drugs for Cancer Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Lung Cancer

- 7.1.2. Breast Cancer

- 7.1.3. Prostate Cancer

- 7.1.4. Blood-related Cancer

- 7.1.5. Other

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Mouse-derived Antibodies

- 7.2.2. Chimeric Antibodies

- 7.2.3. Humanized Antibodies

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Monoclonal Antibody Drugs for Cancer Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Lung Cancer

- 8.1.2. Breast Cancer

- 8.1.3. Prostate Cancer

- 8.1.4. Blood-related Cancer

- 8.1.5. Other

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Mouse-derived Antibodies

- 8.2.2. Chimeric Antibodies

- 8.2.3. Humanized Antibodies

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Monoclonal Antibody Drugs for Cancer Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Lung Cancer

- 9.1.2. Breast Cancer

- 9.1.3. Prostate Cancer

- 9.1.4. Blood-related Cancer

- 9.1.5. Other

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Mouse-derived Antibodies

- 9.2.2. Chimeric Antibodies

- 9.2.3. Humanized Antibodies

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Monoclonal Antibody Drugs for Cancer Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Lung Cancer

- 10.1.2. Breast Cancer

- 10.1.3. Prostate Cancer

- 10.1.4. Blood-related Cancer

- 10.1.5. Other

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Mouse-derived Antibodies

- 10.2.2. Chimeric Antibodies

- 10.2.3. Humanized Antibodies

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Monoclonal Antibody Drugs for Cancer Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Lung Cancer

- 11.1.2. Breast Cancer

- 11.1.3. Prostate Cancer

- 11.1.4. Blood-related Cancer

- 11.1.5. Other

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Mouse-derived Antibodies

- 11.2.2. Chimeric Antibodies

- 11.2.3. Humanized Antibodies

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Johnson & Johnson

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Novartis

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Gilead Sciences

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Roche

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Bristol-Myers Squibb

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Amgen

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 AstraZeneca

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Merck & Co

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Takeda

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Merck KGaA

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Seagen

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Eli Lilly

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Ono Pharmaceutical

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Pfizer

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Regeneron

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 Innovent

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 Hengrui Medicine

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.1 Johnson & Johnson

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Monoclonal Antibody Drugs for Cancer Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Monoclonal Antibody Drugs for Cancer Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Monoclonal Antibody Drugs for Cancer Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Monoclonal Antibody Drugs for Cancer Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Monoclonal Antibody Drugs for Cancer Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Monoclonal Antibody Drugs for Cancer Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Monoclonal Antibody Drugs for Cancer Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Monoclonal Antibody Drugs for Cancer Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Monoclonal Antibody Drugs for Cancer Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Monoclonal Antibody Drugs for Cancer Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Monoclonal Antibody Drugs for Cancer Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Monoclonal Antibody Drugs for Cancer Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Monoclonal Antibody Drugs for Cancer Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Monoclonal Antibody Drugs for Cancer Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Monoclonal Antibody Drugs for Cancer Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Monoclonal Antibody Drugs for Cancer Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Monoclonal Antibody Drugs for Cancer Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Monoclonal Antibody Drugs for Cancer Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Monoclonal Antibody Drugs for Cancer Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Monoclonal Antibody Drugs for Cancer Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Monoclonal Antibody Drugs for Cancer Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Monoclonal Antibody Drugs for Cancer Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Monoclonal Antibody Drugs for Cancer Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Monoclonal Antibody Drugs for Cancer Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Monoclonal Antibody Drugs for Cancer Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Monoclonal Antibody Drugs for Cancer Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Monoclonal Antibody Drugs for Cancer Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Monoclonal Antibody Drugs for Cancer Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Monoclonal Antibody Drugs for Cancer Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Monoclonal Antibody Drugs for Cancer Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Monoclonal Antibody Drugs for Cancer Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Monoclonal Antibody Drugs for Cancer Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Monoclonal Antibody Drugs for Cancer Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Monoclonal Antibody Drugs for Cancer Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Monoclonal Antibody Drugs for Cancer Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Monoclonal Antibody Drugs for Cancer Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Monoclonal Antibody Drugs for Cancer Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Monoclonal Antibody Drugs for Cancer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Monoclonal Antibody Drugs for Cancer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Monoclonal Antibody Drugs for Cancer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Monoclonal Antibody Drugs for Cancer Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Monoclonal Antibody Drugs for Cancer Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Monoclonal Antibody Drugs for Cancer Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Monoclonal Antibody Drugs for Cancer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Monoclonal Antibody Drugs for Cancer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Monoclonal Antibody Drugs for Cancer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Monoclonal Antibody Drugs for Cancer Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Monoclonal Antibody Drugs for Cancer Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Monoclonal Antibody Drugs for Cancer Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Monoclonal Antibody Drugs for Cancer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Monoclonal Antibody Drugs for Cancer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Monoclonal Antibody Drugs for Cancer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Monoclonal Antibody Drugs for Cancer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Monoclonal Antibody Drugs for Cancer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Monoclonal Antibody Drugs for Cancer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Monoclonal Antibody Drugs for Cancer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Monoclonal Antibody Drugs for Cancer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Monoclonal Antibody Drugs for Cancer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Monoclonal Antibody Drugs for Cancer Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Monoclonal Antibody Drugs for Cancer Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Monoclonal Antibody Drugs for Cancer Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Monoclonal Antibody Drugs for Cancer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Monoclonal Antibody Drugs for Cancer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Monoclonal Antibody Drugs for Cancer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Monoclonal Antibody Drugs for Cancer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Monoclonal Antibody Drugs for Cancer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Monoclonal Antibody Drugs for Cancer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Monoclonal Antibody Drugs for Cancer Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Monoclonal Antibody Drugs for Cancer Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Monoclonal Antibody Drugs for Cancer Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Monoclonal Antibody Drugs for Cancer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Monoclonal Antibody Drugs for Cancer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Monoclonal Antibody Drugs for Cancer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Monoclonal Antibody Drugs for Cancer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Monoclonal Antibody Drugs for Cancer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Monoclonal Antibody Drugs for Cancer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Monoclonal Antibody Drugs for Cancer Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Monoclonal Antibody Drugs for Cancer?

The projected CAGR is approximately 10.4%.

2. Which companies are prominent players in the Monoclonal Antibody Drugs for Cancer?

Key companies in the market include Johnson & Johnson, Novartis, Gilead Sciences, Roche, Bristol-Myers Squibb, Amgen, AstraZeneca, Merck & Co, Takeda, Merck KGaA, Seagen, Eli Lilly, Ono Pharmaceutical, Pfizer, Regeneron, Innovent, Hengrui Medicine.

3. What are the main segments of the Monoclonal Antibody Drugs for Cancer?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3350.00, USD 5025.00, and USD 6700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Monoclonal Antibody Drugs for Cancer," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Monoclonal Antibody Drugs for Cancer report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Monoclonal Antibody Drugs for Cancer?

To stay informed about further developments, trends, and reports in the Monoclonal Antibody Drugs for Cancer, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence