Key Insights

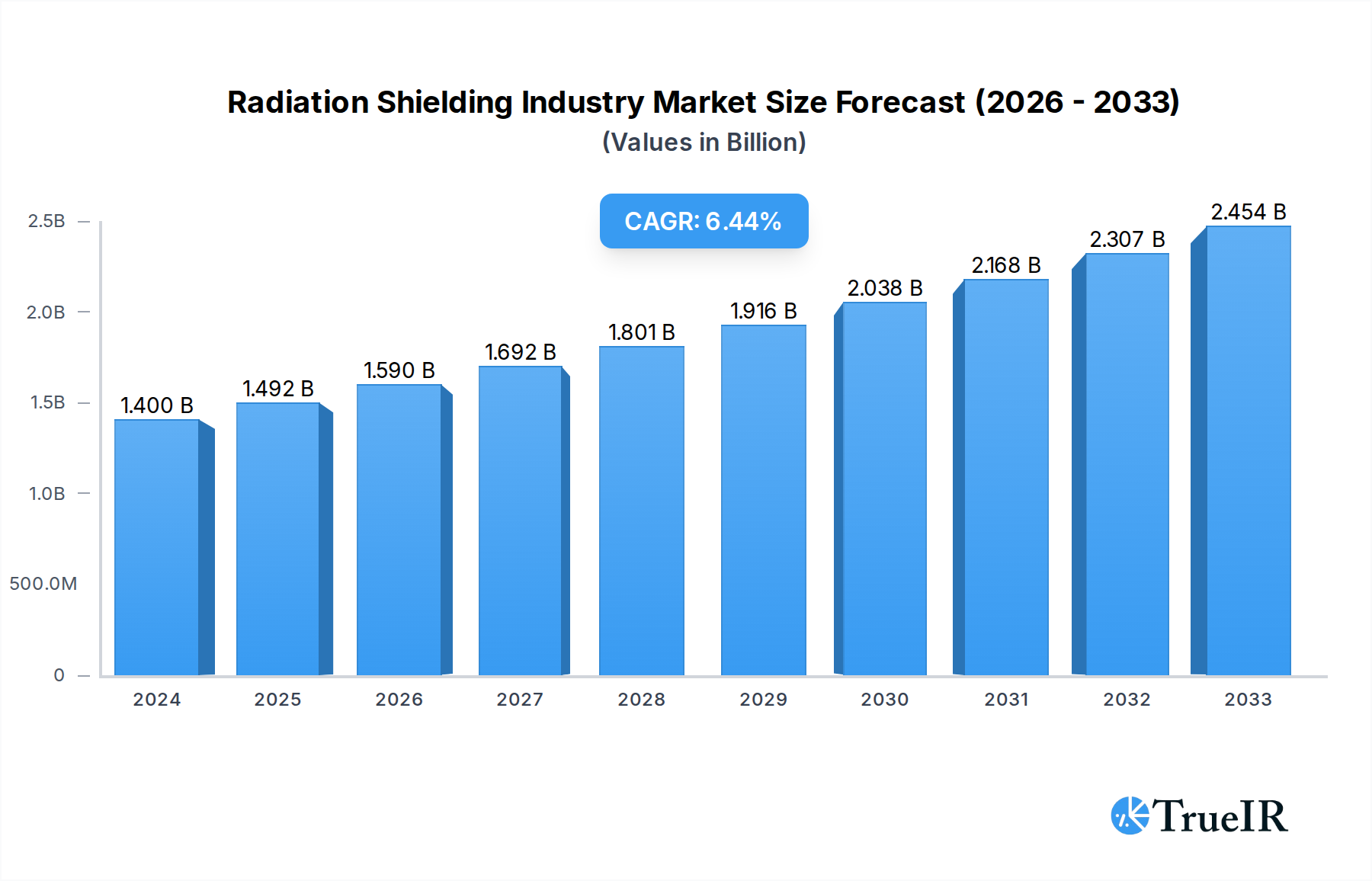

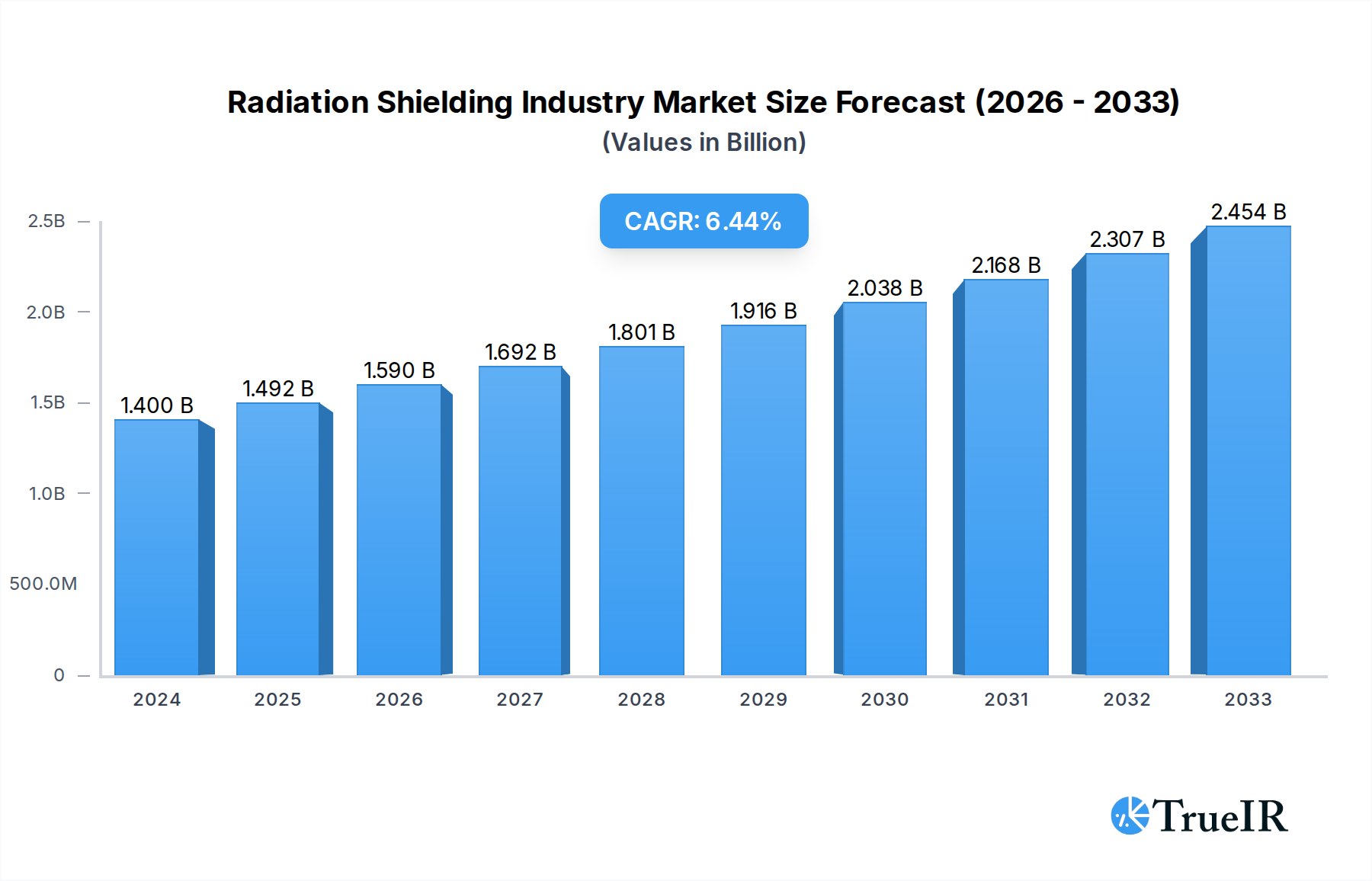

The global Radiation Shielding Market is poised for significant expansion, driven by the increasing adoption of advanced medical imaging and radiation therapy techniques, alongside a growing awareness of radiation safety protocols in various industries. The market is projected to reach an estimated $1.4 billion in 2024, demonstrating a robust Compound Annual Growth Rate (CAGR) of 6.6% from 2019 to 2033. This growth is primarily fueled by the escalating demand for sophisticated radiation therapy solutions to combat cancer and the expanding use of diagnostic imaging technologies like CT scans and X-rays, which necessitate effective shielding to protect patients and healthcare professionals. Furthermore, stringent regulatory frameworks mandating radiation safety in nuclear power plants, research laboratories, and industrial settings are also acting as key growth catalysts. The market's expansion is further supported by ongoing technological advancements in materials science, leading to the development of more efficient, lightweight, and cost-effective shielding solutions.

Radiation Shielding Industry Market Size (In Billion)

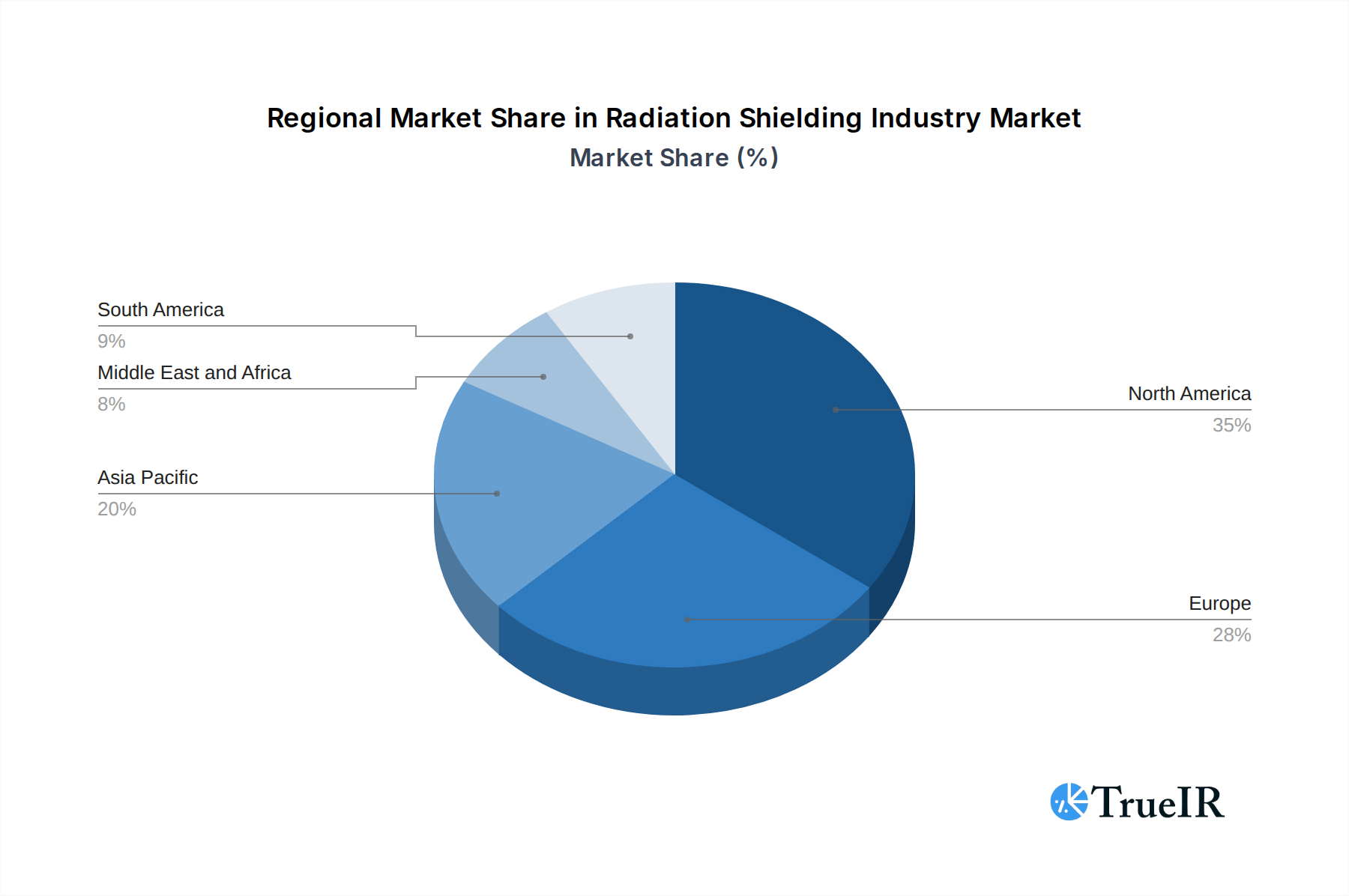

The Radiation Shielding Market is segmented into Radiation Therapy Shielding and Diagnostic Shielding, with hospitals and diagnostic centers representing the largest end-user segment. Research institutes and other end-users also contribute significantly to market demand. Geographically, North America currently leads the market due to its advanced healthcare infrastructure and high adoption rate of sophisticated medical technologies. However, the Asia Pacific region is expected to witness the fastest growth, propelled by increasing healthcare expenditure, a rising prevalence of chronic diseases, and government initiatives to improve healthcare access. Key players in the market, including Marshield, Amray Medical, and ESCO Technologies Inc., are focusing on product innovation and strategic collaborations to expand their market reach and cater to the evolving needs of the industry, ensuring a secure and protected environment for radiation-based applications.

Radiation Shielding Industry Company Market Share

Unveiling the Billion-Dollar Radiation Shielding Industry: A Comprehensive Market Analysis (2019-2033)

This in-depth report delves into the global Radiation Shielding Industry, a critical sector projected to reach billions in market value. Analyzing the period from 2019 to 2033, with a base year of 2025 and a forecast period extending from 2025 to 2033, this report provides unparalleled insights into market structure, trends, dominant segments, product innovations, key drivers, challenges, and the competitive landscape. Leveraging high-volume keywords such as "radiation shielding," "medical shielding," "nuclear shielding," "lead shielding," and "radiation protection solutions," this SEO-optimized analysis is designed to capture maximum search visibility and engage industry professionals.

Radiation Shielding Industry Market Structure & Competitive Landscape

The Radiation Shielding Industry exhibits a moderately concentrated market structure, with a few dominant players commanding a significant market share exceeding billions. Innovation remains a primary driver, fueled by advancements in material science and the increasing demand for advanced radiation protection in healthcare and industrial applications. Regulatory impacts, particularly stringent safety standards and government mandates for radiation safety, play a pivotal role in shaping market entry and product development, with compliance representing a substantial investment. Product substitutes, while present, often lack the efficacy and specific performance characteristics of dedicated radiation shielding materials. End-user segmentation highlights the critical role of healthcare facilities, which account for a substantial portion of the market value, estimated to be in the billions. Mergers and acquisitions (M&A) activity has been moderate, driven by consolidation strategies and the pursuit of synergistic capabilities, with transaction volumes in the past few years reaching into the billions. Key companies like ESCO Technologies Inc., Gaven Industries Inc., and Marshield are key contributors to the competitive dynamics.

- Market Concentration: Moderately concentrated with key players holding significant market share.

- Innovation Drivers: Material science advancements, demand for enhanced safety, and technological integration.

- Regulatory Impacts: Stringent safety standards, government mandates, and compliance costs are significant factors.

- Product Substitutes: Limited effectiveness compared to specialized shielding solutions.

- End-User Segmentation: Hospitals and Diagnostic Centers are the dominant end-users, followed by Research Institutes.

- M&A Trends: Moderate activity focused on consolidation and capability enhancement.

Radiation Shielding Industry Market Trends & Opportunities

The global Radiation Shielding Industry is experiencing robust growth, with market size projections reaching billions by the end of the forecast period in 2033. This expansion is driven by a confluence of factors including an increasing global emphasis on radiation safety across diverse applications, from medical imaging and radiotherapy to nuclear power and industrial radiography. Technological shifts are a significant trend, with a move towards lighter, more efficient, and specialized shielding materials that offer superior attenuation properties while minimizing weight and bulk. The demand for customized solutions tailored to specific radiation sources and exposure levels is also on the rise, presenting substantial opportunities for manufacturers. Consumer preferences are increasingly influenced by safety regulations and the proven effectiveness of advanced shielding technologies, leading to a higher adoption rate of premium products. Competitive dynamics are characterized by a blend of established players and emerging innovators, all vying for market share through product differentiation, strategic partnerships, and a focus on meeting evolving industry standards. The continuous need for upgradation of existing facilities and the construction of new ones equipped with state-of-the-art radiation protection systems further bolster market penetration rates, which are expected to see a Compound Annual Growth Rate (CAGR) in the high single digits. The market is ripe with opportunities for companies that can offer integrated solutions, combining advanced materials with installation and maintenance services, and those that can cater to niche markets with specialized shielding requirements. The increasing prevalence of diagnostic imaging procedures worldwide, coupled with the expanding applications of radiation therapy for cancer treatment, are fundamental growth catalysts. Furthermore, the growing interest in advanced research involving particle accelerators and other high-energy radiation sources necessitates sophisticated shielding solutions, opening up new avenues for market players. The global market size is projected to surpass billions by 2033.

Dominant Markets & Segments in Radiation Shielding Industry

The Radiation Shielding Industry's dominance is clearly evident in specific geographical regions and application segments, driven by robust healthcare infrastructure, favorable government policies, and high levels of investment in research and development.

Leading Region: North America, particularly the United States, currently holds a dominant position, driven by its advanced healthcare system, significant investment in medical technology, and stringent regulatory framework for radiation safety. The region’s substantial number of hospitals, diagnostic centers, and leading research institutions create a perpetual demand for high-performance radiation shielding solutions.

Dominant Solution Segment: Radiation Therapy Shielding stands as the leading segment within the industry. This is primarily due to the escalating global incidence of cancer and the consequent widespread adoption of radiotherapy as a primary treatment modality. The continuous advancements in radiotherapy equipment, such as linear accelerators and proton therapy systems, necessitate the implementation of sophisticated and highly effective shielding solutions to protect medical personnel and patients from harmful radiation. The market for radiation therapy shielding is estimated to be in the billions.

Dominant End User: Hospitals and Diagnostic Centers collectively represent the most significant end-user segment. The sheer volume of diagnostic imaging procedures (e.g., X-rays, CT scans, PET scans) and radiation therapy treatments conducted within these facilities creates an insatiable demand for a wide array of radiation shielding products. Investment in upgrading existing facilities and building new ones with enhanced safety features further solidifies this segment's dominance. The market value from this segment alone is projected to reach billions.

Key Growth Drivers:

- Infrastructure Development: Expansion and modernization of healthcare facilities globally, particularly in emerging economies, require substantial investment in radiation shielding.

- Increasing Cancer Incidence: The rising global burden of cancer drives the demand for radiotherapy, a key application for radiation shielding.

- Technological Advancements in Medical Imaging: New and advanced imaging technologies often require specialized shielding solutions.

- Stringent Regulatory Frameworks: Government regulations emphasizing radiation safety mandate the use of effective shielding.

- Growth in Nuclear Medicine: Increased utilization of radioisotopes for diagnostic and therapeutic purposes fuels demand for specialized shielding.

- Research and Development Investments: Growing investments in scientific research involving radiation sources necessitate advanced shielding.

Radiation Shielding Industry Product Analysis

The Radiation Shielding Industry is characterized by a constant stream of product innovations aimed at enhancing efficacy, safety, and user convenience. Key advancements include the development of lighter and more flexible shielding materials, such as advanced polymer composites and specialized metal alloys, offering superior attenuation with reduced weight and improved handling. The application spectrum is broad, encompassing everything from lead-lined walls and doors for diagnostic imaging rooms to portable shielding solutions for interventional radiology and specialized containment for high-energy physics research. Competitive advantages are increasingly derived from the ability to offer customized solutions, seamless integration into existing infrastructure, and compliance with evolving international safety standards. The market is witnessing a growing demand for integrated shielding systems that combine passive and active protection measures.

Key Drivers, Barriers & Challenges in Radiation Shielding Industry

Key Drivers:

- Increasing Healthcare Spending: Global healthcare expenditures are rising, leading to greater investment in medical equipment and facilities, including radiation shielding.

- Technological Advancements: Innovations in radiation detection and treatment technologies necessitate corresponding advancements in shielding solutions.

- Stringent Safety Regulations: Growing awareness and enforcement of radiation safety standards drive demand for compliant shielding products.

- Growth in Nuclear Power: Expansion and maintenance of nuclear power plants require significant radiation shielding for safety.

- Industrial Applications: Increased use of radiography and other radiation-based techniques in industries like oil & gas and manufacturing.

Key Barriers & Challenges:

- High Cost of Materials and Manufacturing: Specialized materials and precision manufacturing can lead to high product costs, impacting affordability, especially for smaller institutions.

- Regulatory Hurdles and Compliance: Navigating complex and evolving international safety regulations can be time-consuming and costly.

- Supply Chain Disruptions: Reliance on specific raw materials and global supply chains can lead to vulnerabilities, impacting production and delivery timelines.

- Competition from Substitute Materials: While not always as effective, alternative materials can sometimes present a cost-competitive challenge.

- Skilled Labor Shortage: A lack of skilled technicians for installation and maintenance can pose a challenge.

Growth Drivers in the Radiation Shielding Industry Market

The Radiation Shielding Industry is propelled by several key factors. Technologically, the continuous development of advanced materials like composite shielding and specialized polymers is creating more effective and user-friendly solutions. Economically, the burgeoning global healthcare sector, with its increasing demand for advanced diagnostic and therapeutic radiation equipment, is a primary growth catalyst. Policy-driven factors, such as stricter governmental regulations mandating higher radiation safety standards, further incentivize the adoption of robust shielding solutions. For instance, the increasing focus on patient and occupational safety in radiotherapy centers directly fuels the demand for enhanced shielding systems, contributing significantly to market growth, projected to reach billions.

Challenges Impacting Radiation Shielding Industry Growth

Despite its robust growth potential, the Radiation Shielding Industry faces several challenges. Regulatory complexities and the constant need for adaptation to evolving international standards can create significant compliance burdens for manufacturers. Supply chain issues, particularly concerning the sourcing of critical raw materials like lead and specialized isotopes, can lead to production delays and increased costs. Competitive pressures from both established players and new entrants, especially those offering lower-cost alternatives, can impact profit margins. Furthermore, the skilled labor shortage for the specialized installation and maintenance of radiation shielding systems presents an ongoing operational challenge, potentially limiting the pace of market expansion.

Key Players Shaping the Radiation Shielding Industry Market

- Gaven Industries Inc.

- Marshield

- Amray Medical

- Radiation Protection Products Inc.

- ESCO Technologies Inc.

- Nelco Inc.

- Global Partners in Shielding Inc.

- Veritas Medical Solutions LLC

- A&L Shielding

- Ray-Bar Engineering Corp.

Significant Radiation Shielding Industry Industry Milestones

- April 2022: Radiaction Medical Ltd. received Food and Drug Administration 510(K) clearance to market its RadiationShield System in the United States, signaling a significant advancement in portable radiation shielding technology.

- March 2022: Rampart IC secured an exclusive distribution agreement with Japan Lifeline (JLL), expanding its reach into the Japanese market and highlighting the growing international demand for advanced, adjustable radiation attenuation devices like the Rampart M1128, offering 1mm lead equivalency for enhanced physician protection.

Future Outlook for Radiation Shielding Industry Market

The future outlook for the Radiation Shielding Industry is exceptionally bright, with sustained growth anticipated over the forecast period. Key growth catalysts include the ongoing expansion of healthcare infrastructure globally, particularly in emerging markets, coupled with the increasing adoption of advanced medical imaging and radiotherapy techniques. Continued investment in nuclear energy safety and the expanding use of radiation in industrial processes will further bolster demand. Opportunities lie in the development of smart, integrated shielding solutions, the incorporation of sustainable materials, and the provision of comprehensive service packages including installation, maintenance, and disposal. The industry is poised for significant innovation, driven by the relentless pursuit of enhanced safety and efficiency, with the global market expected to continue its upward trajectory, surpassing billions.

Radiation Shielding Industry Segmentation

-

1. Solution

- 1.1. Radiation Therapy Shielding

- 1.2. Diagnostic Shielding

-

2. End User

- 2.1. Hospitals and Diagnostic Centers

- 2.2. Research Institutes

- 2.3. Other End Users

Radiation Shielding Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Radiation Shielding Industry Regional Market Share

Geographic Coverage of Radiation Shielding Industry

Radiation Shielding Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Solution

- 5.1.1. Radiation Therapy Shielding

- 5.1.2. Diagnostic Shielding

- 5.2. Market Analysis, Insights and Forecast - by End User

- 5.2.1. Hospitals and Diagnostic Centers

- 5.2.2. Research Institutes

- 5.2.3. Other End Users

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Middle East and Africa

- 5.3.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Solution

- 6. Global Radiation Shielding Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Solution

- 6.1.1. Radiation Therapy Shielding

- 6.1.2. Diagnostic Shielding

- 6.2. Market Analysis, Insights and Forecast - by End User

- 6.2.1. Hospitals and Diagnostic Centers

- 6.2.2. Research Institutes

- 6.2.3. Other End Users

- 6.1. Market Analysis, Insights and Forecast - by Solution

- 7. North America Radiation Shielding Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Solution

- 7.1.1. Radiation Therapy Shielding

- 7.1.2. Diagnostic Shielding

- 7.2. Market Analysis, Insights and Forecast - by End User

- 7.2.1. Hospitals and Diagnostic Centers

- 7.2.2. Research Institutes

- 7.2.3. Other End Users

- 7.1. Market Analysis, Insights and Forecast - by Solution

- 8. Europe Radiation Shielding Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Solution

- 8.1.1. Radiation Therapy Shielding

- 8.1.2. Diagnostic Shielding

- 8.2. Market Analysis, Insights and Forecast - by End User

- 8.2.1. Hospitals and Diagnostic Centers

- 8.2.2. Research Institutes

- 8.2.3. Other End Users

- 8.1. Market Analysis, Insights and Forecast - by Solution

- 9. Asia Pacific Radiation Shielding Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Solution

- 9.1.1. Radiation Therapy Shielding

- 9.1.2. Diagnostic Shielding

- 9.2. Market Analysis, Insights and Forecast - by End User

- 9.2.1. Hospitals and Diagnostic Centers

- 9.2.2. Research Institutes

- 9.2.3. Other End Users

- 9.1. Market Analysis, Insights and Forecast - by Solution

- 10. Middle East and Africa Radiation Shielding Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Solution

- 10.1.1. Radiation Therapy Shielding

- 10.1.2. Diagnostic Shielding

- 10.2. Market Analysis, Insights and Forecast - by End User

- 10.2.1. Hospitals and Diagnostic Centers

- 10.2.2. Research Institutes

- 10.2.3. Other End Users

- 10.1. Market Analysis, Insights and Forecast - by Solution

- 11. South America Radiation Shielding Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Solution

- 11.1.1. Radiation Therapy Shielding

- 11.1.2. Diagnostic Shielding

- 11.2. Market Analysis, Insights and Forecast - by End User

- 11.2.1. Hospitals and Diagnostic Centers

- 11.2.2. Research Institutes

- 11.2.3. Other End Users

- 11.1. Market Analysis, Insights and Forecast - by Solution

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Gaven Industries Inc

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Marshield

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Amray Medical

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Radiation Protection Products Inc

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 ESCO Technologies Inc

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Nelco Inc

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Global Partners in Shielding Inc

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Veritas Medical Solutions LLC*List Not Exhaustive

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 A&L Shielding

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Ray-Bar Engineering Corp

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Gaven Industries Inc

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Radiation Shielding Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Radiation Shielding Industry Revenue (billion), by Solution 2025 & 2033

- Figure 3: North America Radiation Shielding Industry Revenue Share (%), by Solution 2025 & 2033

- Figure 4: North America Radiation Shielding Industry Revenue (billion), by End User 2025 & 2033

- Figure 5: North America Radiation Shielding Industry Revenue Share (%), by End User 2025 & 2033

- Figure 6: North America Radiation Shielding Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Radiation Shielding Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Europe Radiation Shielding Industry Revenue (billion), by Solution 2025 & 2033

- Figure 9: Europe Radiation Shielding Industry Revenue Share (%), by Solution 2025 & 2033

- Figure 10: Europe Radiation Shielding Industry Revenue (billion), by End User 2025 & 2033

- Figure 11: Europe Radiation Shielding Industry Revenue Share (%), by End User 2025 & 2033

- Figure 12: Europe Radiation Shielding Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: Europe Radiation Shielding Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Radiation Shielding Industry Revenue (billion), by Solution 2025 & 2033

- Figure 15: Asia Pacific Radiation Shielding Industry Revenue Share (%), by Solution 2025 & 2033

- Figure 16: Asia Pacific Radiation Shielding Industry Revenue (billion), by End User 2025 & 2033

- Figure 17: Asia Pacific Radiation Shielding Industry Revenue Share (%), by End User 2025 & 2033

- Figure 18: Asia Pacific Radiation Shielding Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Asia Pacific Radiation Shielding Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East and Africa Radiation Shielding Industry Revenue (billion), by Solution 2025 & 2033

- Figure 21: Middle East and Africa Radiation Shielding Industry Revenue Share (%), by Solution 2025 & 2033

- Figure 22: Middle East and Africa Radiation Shielding Industry Revenue (billion), by End User 2025 & 2033

- Figure 23: Middle East and Africa Radiation Shielding Industry Revenue Share (%), by End User 2025 & 2033

- Figure 24: Middle East and Africa Radiation Shielding Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East and Africa Radiation Shielding Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Radiation Shielding Industry Revenue (billion), by Solution 2025 & 2033

- Figure 27: South America Radiation Shielding Industry Revenue Share (%), by Solution 2025 & 2033

- Figure 28: South America Radiation Shielding Industry Revenue (billion), by End User 2025 & 2033

- Figure 29: South America Radiation Shielding Industry Revenue Share (%), by End User 2025 & 2033

- Figure 30: South America Radiation Shielding Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: South America Radiation Shielding Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Radiation Shielding Industry Revenue billion Forecast, by Solution 2020 & 2033

- Table 2: Global Radiation Shielding Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 3: Global Radiation Shielding Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Radiation Shielding Industry Revenue billion Forecast, by Solution 2020 & 2033

- Table 5: Global Radiation Shielding Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 6: Global Radiation Shielding Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Radiation Shielding Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Radiation Shielding Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Radiation Shielding Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Radiation Shielding Industry Revenue billion Forecast, by Solution 2020 & 2033

- Table 11: Global Radiation Shielding Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 12: Global Radiation Shielding Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Germany Radiation Shielding Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: United Kingdom Radiation Shielding Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: France Radiation Shielding Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Italy Radiation Shielding Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Spain Radiation Shielding Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Rest of Europe Radiation Shielding Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: Global Radiation Shielding Industry Revenue billion Forecast, by Solution 2020 & 2033

- Table 20: Global Radiation Shielding Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 21: Global Radiation Shielding Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 22: China Radiation Shielding Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Japan Radiation Shielding Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: India Radiation Shielding Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Australia Radiation Shielding Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: South Korea Radiation Shielding Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Asia Pacific Radiation Shielding Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Radiation Shielding Industry Revenue billion Forecast, by Solution 2020 & 2033

- Table 29: Global Radiation Shielding Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 30: Global Radiation Shielding Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 31: GCC Radiation Shielding Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: South Africa Radiation Shielding Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: Rest of Middle East and Africa Radiation Shielding Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: Global Radiation Shielding Industry Revenue billion Forecast, by Solution 2020 & 2033

- Table 35: Global Radiation Shielding Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 36: Global Radiation Shielding Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 37: Brazil Radiation Shielding Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: Argentina Radiation Shielding Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 39: Rest of South America Radiation Shielding Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Radiation Shielding Industry?

The projected CAGR is approximately 6.6%.

2. Which companies are prominent players in the Radiation Shielding Industry?

Key companies in the market include Gaven Industries Inc, Marshield, Amray Medical, Radiation Protection Products Inc, ESCO Technologies Inc, Nelco Inc, Global Partners in Shielding Inc, Veritas Medical Solutions LLC*List Not Exhaustive, A&L Shielding, Ray-Bar Engineering Corp.

3. What are the main segments of the Radiation Shielding Industry?

The market segments include Solution, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.4 billion as of 2022.

5. What are some drivers contributing to market growth?

Increasing Usage of Nuclear Medicine and Radiation Therapy for Diagnosis and Treatment; Rising Burden of Chronic Diseases; Growing Safety Awareness Among People Working in Radiation-prone Environments.

6. What are the notable trends driving market growth?

Diagnostic Shielding Holds Significant Share in the Global Medical Radiation Shielding Market.

7. Are there any restraints impacting market growth?

Lack of Awareness Among Healthcare Professionals; High Cost of Radiation Shielding.

8. Can you provide examples of recent developments in the market?

In April 2022, Radiaction Medical Ltd. received Food and Drug Administration 510(K) clearance to market its RadiationShield System in the United States.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Radiation Shielding Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Radiation Shielding Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Radiation Shielding Industry?

To stay informed about further developments, trends, and reports in the Radiation Shielding Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence