Key Insights

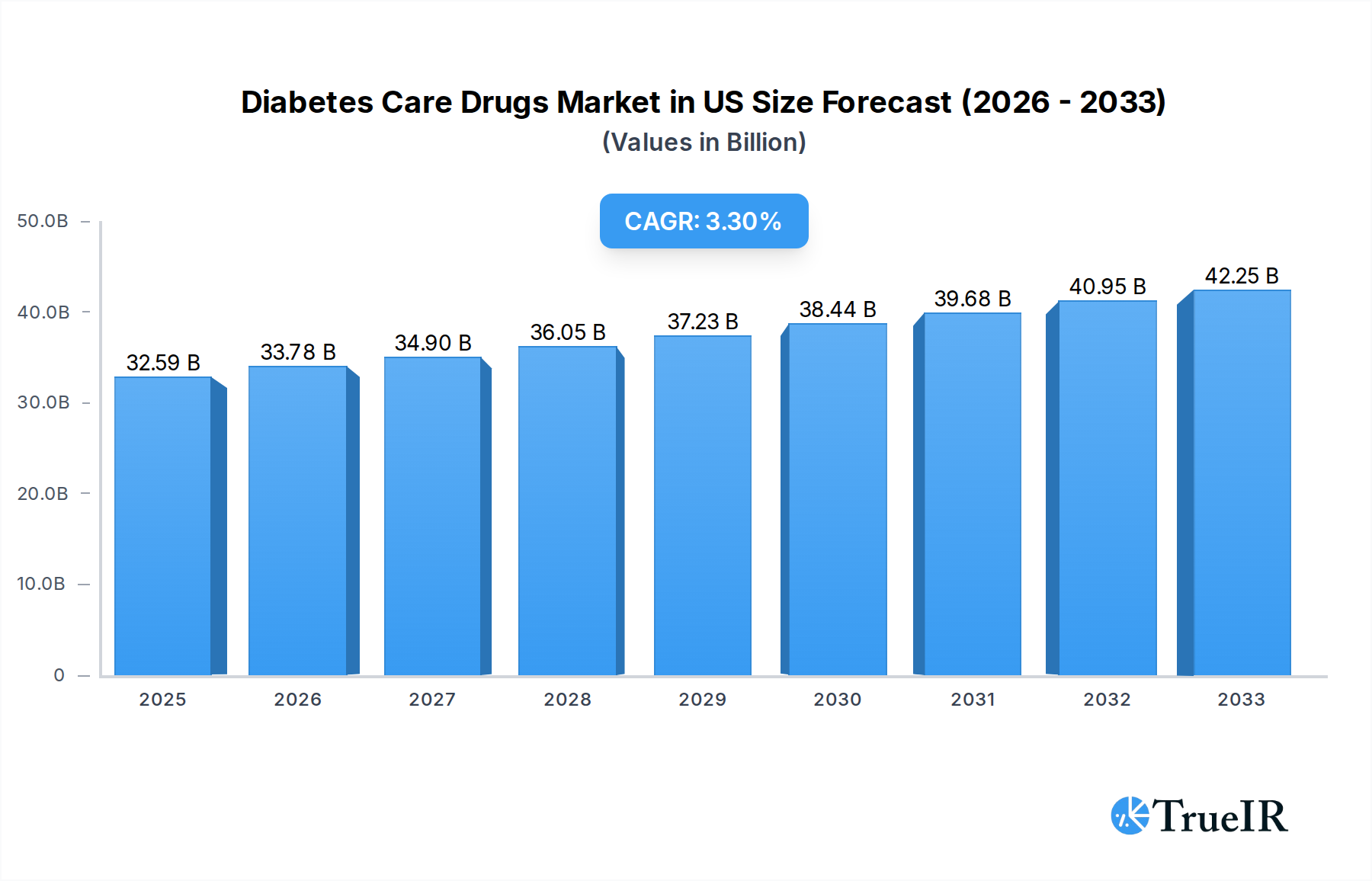

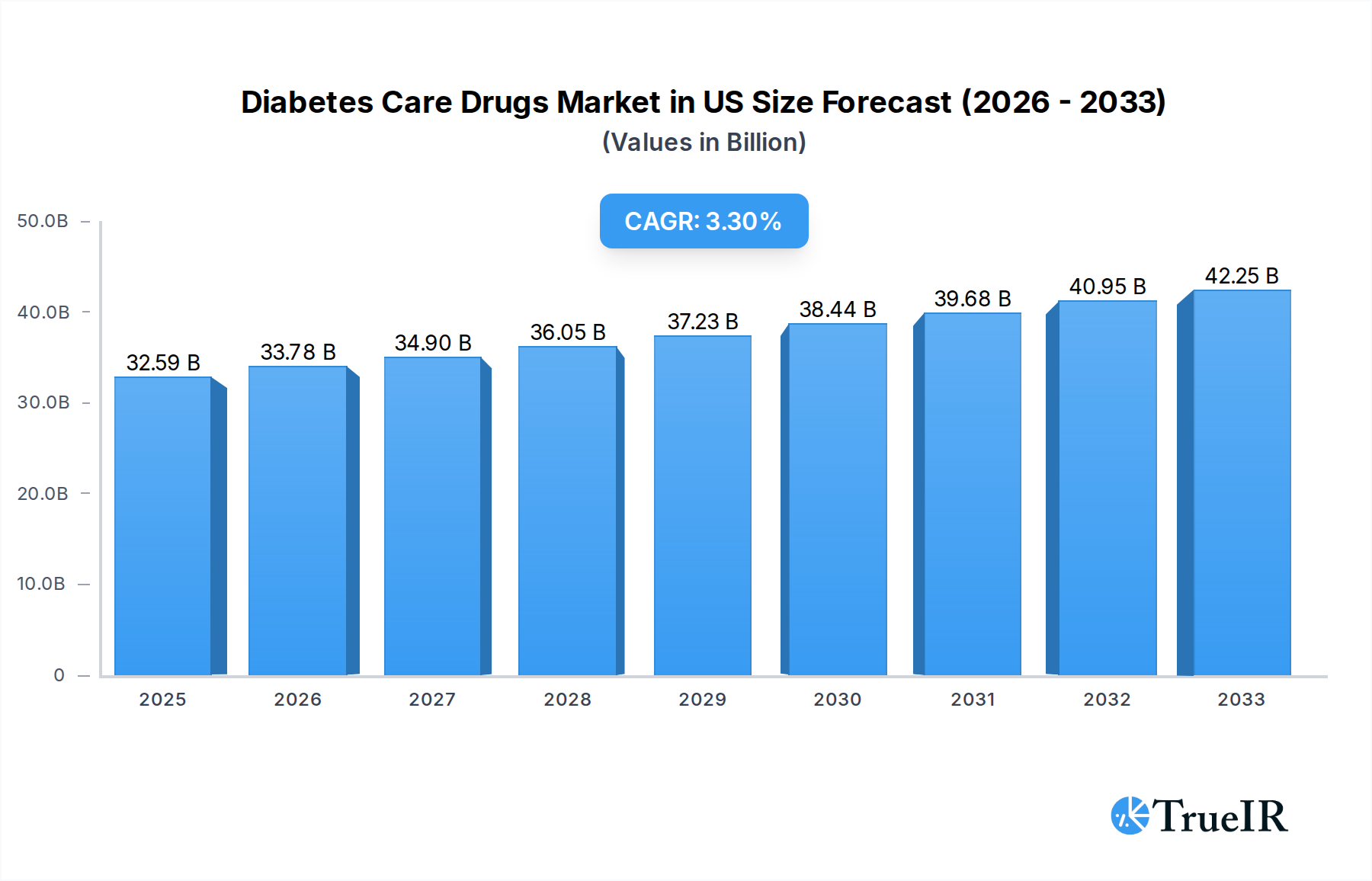

The global Diabetes Care Drugs Market is projected to reach an estimated $32.59 billion by 2025, with a projected Compound Annual Growth Rate (CAGR) of 3.70% from 2025 to 2033. This robust growth is fueled by a confluence of factors including the increasing prevalence of diabetes worldwide, driven by sedentary lifestyles, aging populations, and rising obesity rates. Technological advancements in drug development, leading to more effective and patient-friendly treatment options such as advanced insulins and non-insulin injectable drugs, are also significant growth catalysts. Furthermore, a growing awareness about diabetes management and the availability of comprehensive treatment regimens contribute to market expansion. The market is segmented across various therapeutic classes, including oral anti-diabetic drugs, insulins, combination therapies, and non-insulin injectable drugs, catering to both Type 1 and Type 2 diabetes indications. The increasing adoption of these advanced therapies, coupled with supportive healthcare policies and rising disposable incomes in developing economies, are expected to further propel the market forward.

Diabetes Care Drugs Market in US Market Size (In Billion)

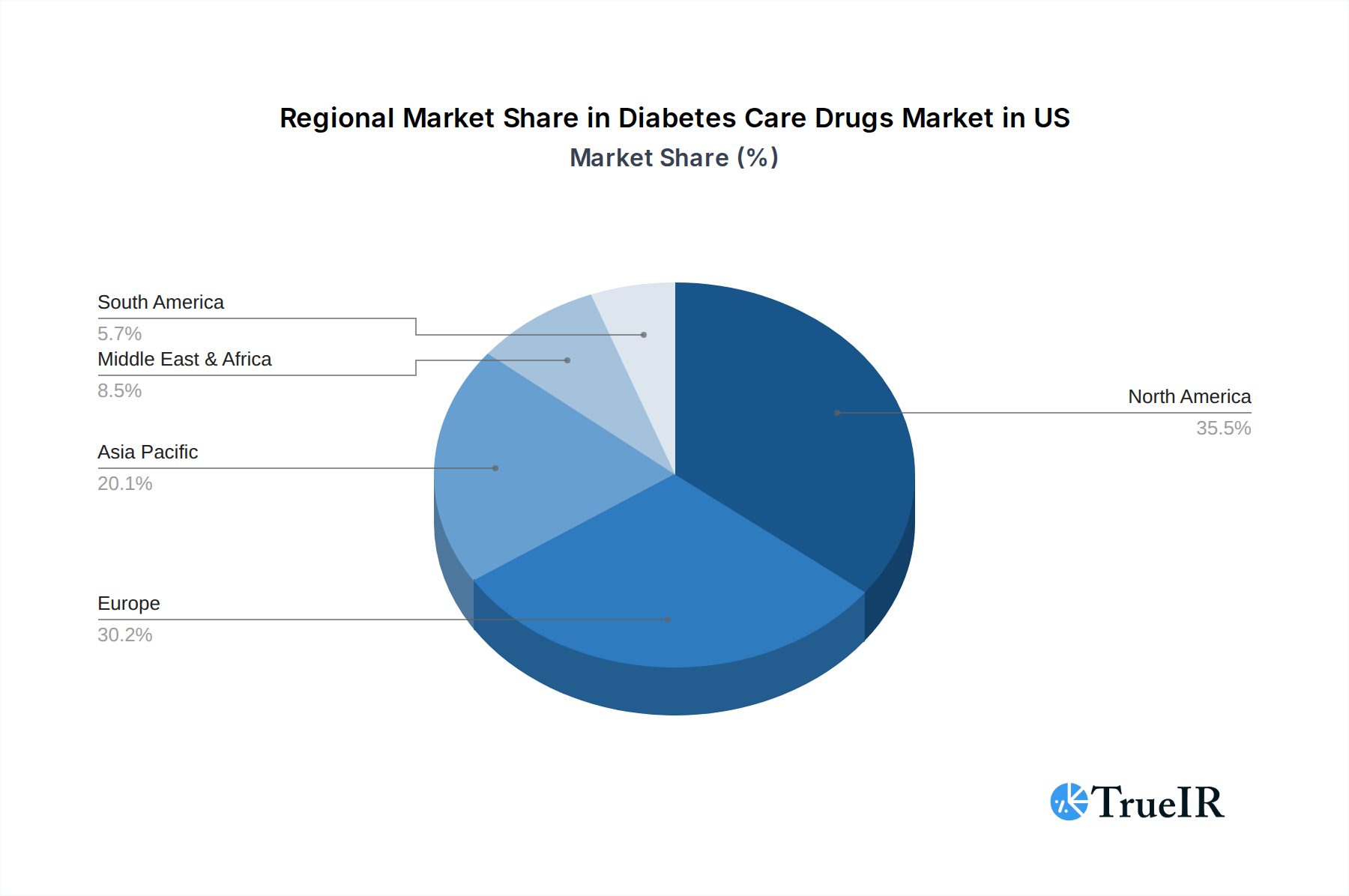

The dynamics of the Diabetes Care Drugs Market are shaped by both drivers and restraints, with continuous innovation playing a pivotal role. Key drivers include the escalating burden of diabetes, particularly Type 2 diabetes, owing to lifestyle changes, and the expanding pipeline of novel drug candidates offering improved efficacy and safety profiles. The growing demand for combination therapies, which offer synergistic benefits and better glycemic control, is also a significant trend. However, challenges such as the high cost of some advanced diabetes medications, patent expiries leading to generic competition, and stringent regulatory hurdles for new drug approvals present potential restraints. The distribution landscape is diverse, encompassing retail pharmacies, hospital pharmacies, and the rapidly growing online pharmacy segment, offering increased accessibility to patients. Geographically, North America and Europe currently dominate the market, but the Asia Pacific region is anticipated to witness the fastest growth due to its large and growing diabetic population and improving healthcare infrastructure.

Diabetes Care Drugs Market in US Company Market Share

Here's a comprehensive, SEO-optimized report description for the Diabetes Care Drugs Market in the US, designed for immediate use without further modification:

Report Title: US Diabetes Care Drugs Market: Comprehensive Analysis & Future Outlook (2019-2033) - Industry Trends, Opportunities, and Key Players

Report Description:

Uncover critical insights into the dynamic US Diabetes Care Drugs Market, a vital sector projected for significant expansion. This in-depth report provides a granular analysis of market size, segmentation, competitive landscape, and future trajectories from 2019 to 2033. Focusing on high-volume keywords like "diabetes drugs US," "type 2 diabetes treatment," "insulin market," and "oral anti-diabetic drugs," this report is engineered to rank prominently in search results and attract key stakeholders. Dive deep into market trends, technological innovations, regulatory impacts, and the strategies of leading pharmaceutical giants including Merck And Co, Pfizer, Takeda, Janssen Pharmaceuticals, Eli Lilly, Novartis, Sanofi, AstraZeneca, Bristol Myers Squibb, Novo Nordisk, Boehringer Ingelheim, and Astellas. Essential for investors, manufacturers, researchers, and policymakers navigating the evolving diabetes care landscape.

US Diabetes Care Drugs Market Market Structure & Competitive Landscape

The US diabetes care drugs market is characterized by a moderately concentrated structure, with a few major pharmaceutical companies holding significant market share. Innovation remains a key driver, fueled by ongoing research into novel therapeutic targets and drug delivery systems, aiming to improve glycemic control and reduce the burden of diabetes complications. Regulatory impacts are substantial, with the FDA's stringent approval processes shaping product development and market entry. However, the availability of numerous therapeutic classes, including oral anti-diabetics, insulins, combination therapies, and non-insulin injectables, offers a wide array of product substitutes, fostering competition. End-user segmentation, primarily driven by the prevalence of type 1 and type 2 diabetes, dictates market demand. Mergers and acquisitions (M&A) activity, while not exceptionally high, plays a role in market consolidation and portfolio expansion. For instance, the acquisition of smaller biotech firms with promising diabetes technologies by larger players is a recurring trend, aiming to bolster R&D pipelines and market presence. The market concentration ratio is estimated to be around 60-65% among the top five players. M&A volumes have averaged between 2-3 significant deals per year over the historical period.

US Diabetes Care Drugs Market Market Trends & Opportunities

The US diabetes care drugs market is experiencing robust growth, driven by an escalating prevalence of diabetes, an aging population, and advancements in therapeutic innovation. The market size is projected to reach an estimated $XX Billion by 2025, with a projected Compound Annual Growth Rate (CAGR) of approximately 5-7% during the forecast period of 2025-2033. Technological shifts are profoundly impacting the market, with a growing emphasis on personalized medicine, biosimil insulins, and novel drug classes like GLP-1 receptor agonists and SGLT2 inhibitors. These innovations are not only improving patient outcomes but also expanding treatment options beyond traditional metformin and insulin therapies. Consumer preferences are evolving, with patients increasingly seeking convenient, less invasive, and more effective treatment regimens that minimize side effects and improve quality of life. This has led to a surge in demand for oral anti-diabetic drugs and non-insulin injectable therapies. Competitive dynamics are intense, with key players continuously investing in R&D to develop next-generation therapies and expand their market reach. Opportunities lie in addressing the unmet needs of specific patient populations, such as those with brittle diabetes or advanced complications, and in developing cost-effective treatment solutions to improve market penetration in underserved communities. The increasing focus on preventative care and early intervention also presents a significant avenue for growth, with opportunities for combination therapies and combination products that offer synergistic benefits. Furthermore, the burgeoning market for digital health solutions integrated with diabetes management drugs, such as connected insulin pens and glucose monitoring systems, is creating new avenues for market expansion and enhanced patient engagement.

Dominant Markets & Segments in US Diabetes Care Drugs Market

The dominant market segment within the US diabetes care drugs landscape is overwhelmingly Type 2 diabetes, owing to its significantly higher prevalence compared to Type 1 diabetes. This indication accounts for an estimated 85-90% of the total diabetes patient population in the US, thus driving the largest share of the drug market. Within the product segments, Oral Anti-diabetic drugs currently hold a substantial market share, driven by their convenience, accessibility, and efficacy in managing early-stage Type 2 diabetes. However, Insulins remain a critical therapeutic class, indispensable for many Type 1 diabetes patients and an increasing number of Type 2 diabetes patients with advanced disease progression. Non-insulin injectable drugs, particularly GLP-1 receptor agonists, are experiencing rapid growth due to their dual benefits of glycemic control and weight management, making them highly attractive for the large segment of overweight and obese individuals with Type 2 diabetes. Combination therapies are also gaining traction, offering improved glycemic control and patient convenience by combining multiple active ingredients in a single dosage form.

Regarding distribution channels, Retail pharmacies represent the largest segment, benefiting from widespread accessibility and the convenience of prescription fulfillment for a vast outpatient population. Hospital pharmacies play a crucial role in managing inpatient diabetes care and dispensing specialized or high-cost medications. The Online pharmacies segment is experiencing significant growth, propelled by the increasing adoption of e-commerce for healthcare products and the convenience it offers to patients, especially during periods of restricted movement. Key growth drivers for these dominant segments include:

- High Prevalence of Type 2 Diabetes: The escalating epidemic of obesity and sedentary lifestyles continues to fuel the incidence of Type 2 diabetes.

- Aging Population: Older adults are at a higher risk of developing diabetes and its complications, increasing the demand for diabetes medications.

- Technological Advancements in Drug Formulations: Development of novel oral anti-diabetic drugs with improved efficacy and reduced side effects.

- Growing Demand for Weight Management Solutions: The success of GLP-1 agonists in promoting weight loss has significantly boosted their market share.

- Increased Healthcare Expenditure and Insurance Coverage: Greater access to healthcare services and prescription drug coverage enables more patients to afford and access diabetes medications.

- Patient Preference for Convenience: The popularity of oral medications and convenient injectable formulations caters to patient demand for easier administration.

US Diabetes Care Drugs Market Product Analysis

Product innovation in the US diabetes care drugs market is characterized by a relentless pursuit of enhanced efficacy, improved safety profiles, and greater patient convenience. Key advancements include the development of next-generation oral anti-diabetic agents with novel mechanisms of action, such as dual and triple agonists, and innovative insulin formulations offering longer durations of action and reduced injection frequencies. The competitive advantage lies in drugs that demonstrate significant cardiovascular or renal benefits, beyond glycemic control, addressing the broader comorbidity landscape of diabetes. Furthermore, the integration of digital technologies with drug delivery systems, such as smart insulin pens and connected glucose monitors, is creating a synergistic advantage by improving treatment adherence and providing real-time data for better disease management.

Key Drivers, Barriers & Challenges in US Diabetes Care Drugs Market

Key Drivers: The US diabetes care drugs market is propelled by several critical drivers. Technologically, the continuous development of novel drug classes like GLP-1 receptor agonists and SGLT2 inhibitors, offering benefits beyond glycemic control such as weight loss and cardiovascular protection, is a significant growth catalyst. Economically, the increasing healthcare expenditure and improved insurance coverage for diabetes medications enable wider patient access. Policy-driven factors, including government initiatives to improve diabetes care outcomes and incentives for pharmaceutical research and development, further fuel market expansion. For instance, recent FDA approvals for new diabetes medications and expanded indications for existing ones directly stimulate market growth.

Barriers & Challenges: Despite the growth, the market faces significant challenges. Regulatory hurdles, including lengthy and costly drug approval processes, can delay market entry for innovative therapies. Supply chain issues, such as manufacturing complexities for biologics and potential drug shortages, can disrupt product availability. Competitive pressures are intense, with multiple players vying for market share, leading to pricing pressures and the need for continuous differentiation. The high cost of some novel diabetes medications also poses a barrier to access for a significant portion of the patient population, leading to concerns about affordability and equitable care. For example, the estimated annual cost of advanced diabetes therapies can range from $5,000 to $15,000 per patient, creating a significant economic burden.

Growth Drivers in the US Diabetes Care Drugs Market

The growth drivers in the US diabetes care drugs market are multifaceted, encompassing technological, economic, and regulatory factors. Technologically, the ongoing innovation in drug discovery has led to the introduction of highly effective classes like GLP-1 receptor agonists and SGLT2 inhibitors, which offer not only glycemic control but also crucial benefits for cardiovascular and renal health, appealing to a growing segment of patients with co-existing conditions. Economically, rising disposable incomes and an expanding health insurance coverage base in the US translate to increased affordability and access to a wider range of diabetes medications, including newer, more advanced therapies. Regulatory support, through expedited approval pathways for innovative treatments and government focus on chronic disease management, also plays a pivotal role in accelerating market penetration and incentivizing pharmaceutical investment.

Challenges Impacting US Diabetes Care Drugs Market Growth

The growth of the US diabetes care drugs market is impacted by several significant barriers and restraints. Regulatory complexities, including stringent clinical trial requirements and post-market surveillance obligations, can prolong the time-to-market for new drugs and increase development costs. Supply chain vulnerabilities, such as the reliance on specialized manufacturing processes for biologics and potential disruptions from global events, can lead to drug shortages and impact patient treatment continuity. Intense competitive pressures from a large number of established and emerging players often lead to price erosion and necessitate substantial investment in marketing and brand differentiation. Furthermore, the escalating cost of diabetes medications, particularly novel therapies, remains a critical challenge, limiting access for many patients and prompting calls for greater affordability and value-based pricing models, potentially impacting market expansion if not adequately addressed.

Key Players Shaping the US Diabetes Care Drugs Market

- Merck And Co

- Pfizer

- Takeda

- Janssen Pharmaceuticals

- Eli Lilly

- Novartis

- Sanofi

- AstraZeneca

- Bristol Myers Squibb

- Novo Nordisk

- Boehringer Ingelheim

- Astellas

Significant US Diabetes Care Drugs Market Industry Milestones

- June 2023: Lantidra, the first allogeneic pancreatic islet cellular therapy, received FDA approval. This groundbreaking treatment for type 1 diabetes, derived from deceased donor pancreatic cells, targets adults struggling with severe hypoglycemia despite intensive management, marking a significant advancement in cell-based diabetes therapy.

- June 2023: The FDA authorized the use of Jardiance (empagliflozin) and Synjardy (empagliflozin and metformin hydrochloride) for children aged 10 and older with type 2 diabetes, in conjunction with diet and exercise. This approval signifies the introduction of a new class of oral medications for pediatric type 2 diabetes management, expanding treatment options for younger populations.

Future Outlook for US Diabetes Care Drugs Market

The future outlook for the US diabetes care drugs market is exceptionally promising, driven by a confluence of factors poised to catalyze substantial growth. Continued advancements in pharmaceutical research and development will unveil novel therapeutic targets and more effective drug formulations, including next-generation oral agents and long-acting injectables with enhanced safety and efficacy profiles. The increasing recognition of diabetes as a systemic disease, with significant cardiovascular and renal implications, will fuel demand for drugs offering comprehensive benefits beyond glycemic control. Furthermore, the integration of digital health technologies, such as AI-powered treatment platforms and wearable devices, will revolutionize patient monitoring and treatment adherence, creating a more personalized and effective diabetes management ecosystem. Strategic opportunities lie in addressing unmet clinical needs, such as developing cures or more effective preventative measures for diabetes, and in expanding access to innovative treatments for underserved populations. The market is anticipated to witness continued expansion, driven by these innovations and a persistent societal focus on improving the lives of individuals living with diabetes.

Diabetes Care Drugs Market in US Segmentation

-

1. Type

- 1.1. Oral Anti-diabetic drugs

- 1.2. Insulins

- 1.3. Combination therapies

- 1.4. Non-insulin injectable drugs

-

2. Indication

- 2.1. Type 1 diabetes

- 2.2. Type 2 diabetes

-

3. Distribution Channel

- 3.1. Retail pharmacies

- 3.2. Hospital pharmacies

- 3.3. Online pharmacies

Diabetes Care Drugs Market in US Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Diabetes Care Drugs Market in US Regional Market Share

Geographic Coverage of Diabetes Care Drugs Market in US

Diabetes Care Drugs Market in US REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.70% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Oral Anti-diabetic drugs

- 5.1.2. Insulins

- 5.1.3. Combination therapies

- 5.1.4. Non-insulin injectable drugs

- 5.2. Market Analysis, Insights and Forecast - by Indication

- 5.2.1. Type 1 diabetes

- 5.2.2. Type 2 diabetes

- 5.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.3.1. Retail pharmacies

- 5.3.2. Hospital pharmacies

- 5.3.3. Online pharmacies

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. South America

- 5.4.3. Europe

- 5.4.4. Middle East & Africa

- 5.4.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Diabetes Care Drugs Market in US Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Oral Anti-diabetic drugs

- 6.1.2. Insulins

- 6.1.3. Combination therapies

- 6.1.4. Non-insulin injectable drugs

- 6.2. Market Analysis, Insights and Forecast - by Indication

- 6.2.1. Type 1 diabetes

- 6.2.2. Type 2 diabetes

- 6.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.3.1. Retail pharmacies

- 6.3.2. Hospital pharmacies

- 6.3.3. Online pharmacies

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. North America Diabetes Care Drugs Market in US Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Oral Anti-diabetic drugs

- 7.1.2. Insulins

- 7.1.3. Combination therapies

- 7.1.4. Non-insulin injectable drugs

- 7.2. Market Analysis, Insights and Forecast - by Indication

- 7.2.1. Type 1 diabetes

- 7.2.2. Type 2 diabetes

- 7.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.3.1. Retail pharmacies

- 7.3.2. Hospital pharmacies

- 7.3.3. Online pharmacies

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. South America Diabetes Care Drugs Market in US Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Oral Anti-diabetic drugs

- 8.1.2. Insulins

- 8.1.3. Combination therapies

- 8.1.4. Non-insulin injectable drugs

- 8.2. Market Analysis, Insights and Forecast - by Indication

- 8.2.1. Type 1 diabetes

- 8.2.2. Type 2 diabetes

- 8.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 8.3.1. Retail pharmacies

- 8.3.2. Hospital pharmacies

- 8.3.3. Online pharmacies

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Europe Diabetes Care Drugs Market in US Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Oral Anti-diabetic drugs

- 9.1.2. Insulins

- 9.1.3. Combination therapies

- 9.1.4. Non-insulin injectable drugs

- 9.2. Market Analysis, Insights and Forecast - by Indication

- 9.2.1. Type 1 diabetes

- 9.2.2. Type 2 diabetes

- 9.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 9.3.1. Retail pharmacies

- 9.3.2. Hospital pharmacies

- 9.3.3. Online pharmacies

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Middle East & Africa Diabetes Care Drugs Market in US Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Oral Anti-diabetic drugs

- 10.1.2. Insulins

- 10.1.3. Combination therapies

- 10.1.4. Non-insulin injectable drugs

- 10.2. Market Analysis, Insights and Forecast - by Indication

- 10.2.1. Type 1 diabetes

- 10.2.2. Type 2 diabetes

- 10.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 10.3.1. Retail pharmacies

- 10.3.2. Hospital pharmacies

- 10.3.3. Online pharmacies

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Asia Pacific Diabetes Care Drugs Market in US Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Oral Anti-diabetic drugs

- 11.1.2. Insulins

- 11.1.3. Combination therapies

- 11.1.4. Non-insulin injectable drugs

- 11.2. Market Analysis, Insights and Forecast - by Indication

- 11.2.1. Type 1 diabetes

- 11.2.2. Type 2 diabetes

- 11.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 11.3.1. Retail pharmacies

- 11.3.2. Hospital pharmacies

- 11.3.3. Online pharmacies

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Merck And Co

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Pfizer

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Takeda

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Janssen Pharmaceuticals

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Eli Lilly

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Novartis

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Sanofi

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 AstraZeneca

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Bristol Myers Squibb

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Novo Nordisk

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Boehringer Ingelheim

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Astellas

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.1 Merck And Co

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Diabetes Care Drugs Market in US Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Diabetes Care Drugs Market in US Share (%) by Company 2025

List of Tables

- Table 1: Diabetes Care Drugs Market in US Revenue Million Forecast, by Type 2020 & 2033

- Table 2: Diabetes Care Drugs Market in US Volume K Unit Forecast, by Type 2020 & 2033

- Table 3: Diabetes Care Drugs Market in US Revenue Million Forecast, by Indication 2020 & 2033

- Table 4: Diabetes Care Drugs Market in US Volume K Unit Forecast, by Indication 2020 & 2033

- Table 5: Diabetes Care Drugs Market in US Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 6: Diabetes Care Drugs Market in US Volume K Unit Forecast, by Distribution Channel 2020 & 2033

- Table 7: Diabetes Care Drugs Market in US Revenue Million Forecast, by Region 2020 & 2033

- Table 8: Diabetes Care Drugs Market in US Volume K Unit Forecast, by Region 2020 & 2033

- Table 9: Diabetes Care Drugs Market in US Revenue Million Forecast, by Type 2020 & 2033

- Table 10: Diabetes Care Drugs Market in US Volume K Unit Forecast, by Type 2020 & 2033

- Table 11: Diabetes Care Drugs Market in US Revenue Million Forecast, by Indication 2020 & 2033

- Table 12: Diabetes Care Drugs Market in US Volume K Unit Forecast, by Indication 2020 & 2033

- Table 13: Diabetes Care Drugs Market in US Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 14: Diabetes Care Drugs Market in US Volume K Unit Forecast, by Distribution Channel 2020 & 2033

- Table 15: Diabetes Care Drugs Market in US Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Diabetes Care Drugs Market in US Volume K Unit Forecast, by Country 2020 & 2033

- Table 17: United States Diabetes Care Drugs Market in US Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: United States Diabetes Care Drugs Market in US Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 19: Canada Diabetes Care Drugs Market in US Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Canada Diabetes Care Drugs Market in US Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 21: Mexico Diabetes Care Drugs Market in US Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Mexico Diabetes Care Drugs Market in US Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 23: Diabetes Care Drugs Market in US Revenue Million Forecast, by Type 2020 & 2033

- Table 24: Diabetes Care Drugs Market in US Volume K Unit Forecast, by Type 2020 & 2033

- Table 25: Diabetes Care Drugs Market in US Revenue Million Forecast, by Indication 2020 & 2033

- Table 26: Diabetes Care Drugs Market in US Volume K Unit Forecast, by Indication 2020 & 2033

- Table 27: Diabetes Care Drugs Market in US Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 28: Diabetes Care Drugs Market in US Volume K Unit Forecast, by Distribution Channel 2020 & 2033

- Table 29: Diabetes Care Drugs Market in US Revenue Million Forecast, by Country 2020 & 2033

- Table 30: Diabetes Care Drugs Market in US Volume K Unit Forecast, by Country 2020 & 2033

- Table 31: Brazil Diabetes Care Drugs Market in US Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Brazil Diabetes Care Drugs Market in US Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 33: Argentina Diabetes Care Drugs Market in US Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: Argentina Diabetes Care Drugs Market in US Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 35: Rest of South America Diabetes Care Drugs Market in US Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: Rest of South America Diabetes Care Drugs Market in US Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 37: Diabetes Care Drugs Market in US Revenue Million Forecast, by Type 2020 & 2033

- Table 38: Diabetes Care Drugs Market in US Volume K Unit Forecast, by Type 2020 & 2033

- Table 39: Diabetes Care Drugs Market in US Revenue Million Forecast, by Indication 2020 & 2033

- Table 40: Diabetes Care Drugs Market in US Volume K Unit Forecast, by Indication 2020 & 2033

- Table 41: Diabetes Care Drugs Market in US Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 42: Diabetes Care Drugs Market in US Volume K Unit Forecast, by Distribution Channel 2020 & 2033

- Table 43: Diabetes Care Drugs Market in US Revenue Million Forecast, by Country 2020 & 2033

- Table 44: Diabetes Care Drugs Market in US Volume K Unit Forecast, by Country 2020 & 2033

- Table 45: United Kingdom Diabetes Care Drugs Market in US Revenue (Million) Forecast, by Application 2020 & 2033

- Table 46: United Kingdom Diabetes Care Drugs Market in US Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 47: Germany Diabetes Care Drugs Market in US Revenue (Million) Forecast, by Application 2020 & 2033

- Table 48: Germany Diabetes Care Drugs Market in US Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 49: France Diabetes Care Drugs Market in US Revenue (Million) Forecast, by Application 2020 & 2033

- Table 50: France Diabetes Care Drugs Market in US Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 51: Italy Diabetes Care Drugs Market in US Revenue (Million) Forecast, by Application 2020 & 2033

- Table 52: Italy Diabetes Care Drugs Market in US Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 53: Spain Diabetes Care Drugs Market in US Revenue (Million) Forecast, by Application 2020 & 2033

- Table 54: Spain Diabetes Care Drugs Market in US Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 55: Russia Diabetes Care Drugs Market in US Revenue (Million) Forecast, by Application 2020 & 2033

- Table 56: Russia Diabetes Care Drugs Market in US Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 57: Benelux Diabetes Care Drugs Market in US Revenue (Million) Forecast, by Application 2020 & 2033

- Table 58: Benelux Diabetes Care Drugs Market in US Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 59: Nordics Diabetes Care Drugs Market in US Revenue (Million) Forecast, by Application 2020 & 2033

- Table 60: Nordics Diabetes Care Drugs Market in US Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 61: Rest of Europe Diabetes Care Drugs Market in US Revenue (Million) Forecast, by Application 2020 & 2033

- Table 62: Rest of Europe Diabetes Care Drugs Market in US Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 63: Diabetes Care Drugs Market in US Revenue Million Forecast, by Type 2020 & 2033

- Table 64: Diabetes Care Drugs Market in US Volume K Unit Forecast, by Type 2020 & 2033

- Table 65: Diabetes Care Drugs Market in US Revenue Million Forecast, by Indication 2020 & 2033

- Table 66: Diabetes Care Drugs Market in US Volume K Unit Forecast, by Indication 2020 & 2033

- Table 67: Diabetes Care Drugs Market in US Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 68: Diabetes Care Drugs Market in US Volume K Unit Forecast, by Distribution Channel 2020 & 2033

- Table 69: Diabetes Care Drugs Market in US Revenue Million Forecast, by Country 2020 & 2033

- Table 70: Diabetes Care Drugs Market in US Volume K Unit Forecast, by Country 2020 & 2033

- Table 71: Turkey Diabetes Care Drugs Market in US Revenue (Million) Forecast, by Application 2020 & 2033

- Table 72: Turkey Diabetes Care Drugs Market in US Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 73: Israel Diabetes Care Drugs Market in US Revenue (Million) Forecast, by Application 2020 & 2033

- Table 74: Israel Diabetes Care Drugs Market in US Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 75: GCC Diabetes Care Drugs Market in US Revenue (Million) Forecast, by Application 2020 & 2033

- Table 76: GCC Diabetes Care Drugs Market in US Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 77: North Africa Diabetes Care Drugs Market in US Revenue (Million) Forecast, by Application 2020 & 2033

- Table 78: North Africa Diabetes Care Drugs Market in US Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 79: South Africa Diabetes Care Drugs Market in US Revenue (Million) Forecast, by Application 2020 & 2033

- Table 80: South Africa Diabetes Care Drugs Market in US Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 81: Rest of Middle East & Africa Diabetes Care Drugs Market in US Revenue (Million) Forecast, by Application 2020 & 2033

- Table 82: Rest of Middle East & Africa Diabetes Care Drugs Market in US Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 83: Diabetes Care Drugs Market in US Revenue Million Forecast, by Type 2020 & 2033

- Table 84: Diabetes Care Drugs Market in US Volume K Unit Forecast, by Type 2020 & 2033

- Table 85: Diabetes Care Drugs Market in US Revenue Million Forecast, by Indication 2020 & 2033

- Table 86: Diabetes Care Drugs Market in US Volume K Unit Forecast, by Indication 2020 & 2033

- Table 87: Diabetes Care Drugs Market in US Revenue Million Forecast, by Distribution Channel 2020 & 2033

- Table 88: Diabetes Care Drugs Market in US Volume K Unit Forecast, by Distribution Channel 2020 & 2033

- Table 89: Diabetes Care Drugs Market in US Revenue Million Forecast, by Country 2020 & 2033

- Table 90: Diabetes Care Drugs Market in US Volume K Unit Forecast, by Country 2020 & 2033

- Table 91: China Diabetes Care Drugs Market in US Revenue (Million) Forecast, by Application 2020 & 2033

- Table 92: China Diabetes Care Drugs Market in US Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 93: India Diabetes Care Drugs Market in US Revenue (Million) Forecast, by Application 2020 & 2033

- Table 94: India Diabetes Care Drugs Market in US Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 95: Japan Diabetes Care Drugs Market in US Revenue (Million) Forecast, by Application 2020 & 2033

- Table 96: Japan Diabetes Care Drugs Market in US Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 97: South Korea Diabetes Care Drugs Market in US Revenue (Million) Forecast, by Application 2020 & 2033

- Table 98: South Korea Diabetes Care Drugs Market in US Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 99: ASEAN Diabetes Care Drugs Market in US Revenue (Million) Forecast, by Application 2020 & 2033

- Table 100: ASEAN Diabetes Care Drugs Market in US Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 101: Oceania Diabetes Care Drugs Market in US Revenue (Million) Forecast, by Application 2020 & 2033

- Table 102: Oceania Diabetes Care Drugs Market in US Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 103: Rest of Asia Pacific Diabetes Care Drugs Market in US Revenue (Million) Forecast, by Application 2020 & 2033

- Table 104: Rest of Asia Pacific Diabetes Care Drugs Market in US Volume (K Unit) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Diabetes Care Drugs Market in US?

The projected CAGR is approximately 3.70%.

2. Which companies are prominent players in the Diabetes Care Drugs Market in US?

Key companies in the market include Merck And Co, Pfizer, Takeda, Janssen Pharmaceuticals, Eli Lilly, Novartis, Sanofi, AstraZeneca, Bristol Myers Squibb, Novo Nordisk, Boehringer Ingelheim, Astellas.

3. What are the main segments of the Diabetes Care Drugs Market in US?

The market segments include Type, Indication, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 32.59 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Geriatric Population and Changing Dietary Habits; High Prevalence of Irritable bowel syndrome with constipation (IBS-C) and Opioid-induced constipation (OIC) and Chronic Constipation; Development of Latest Drugs and Treatment Procedures.

6. What are the notable trends driving market growth?

Oral-Anti Diabetes Drugs Segment is Having the Highest Market Share in Current Year.

7. Are there any restraints impacting market growth?

Increasing Dependence on Majority of Over-the-Counter (OTC) Drugs; Lack of Awareness and Reluctance Among Patients due to Adverse Effects of Opioid-Induced Constipation (OIC) Drugs.

8. Can you provide examples of recent developments in the market?

June 2023: The initial allogeneic pancreatic islet cellular therapy, Lantidra, has been sanctioned by the U.S. Food and Drug Administration. This treatment, derived from deceased donor pancreatic cells, is specifically designed for individuals with type 1 diabetes. Lantidra is intended for adults who struggle to achieve target glycated hemoglobin levels due to frequent severe hypoglycemia episodes, despite undergoing intensive diabetes management and education.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Diabetes Care Drugs Market in US," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Diabetes Care Drugs Market in US report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Diabetes Care Drugs Market in US?

To stay informed about further developments, trends, and reports in the Diabetes Care Drugs Market in US, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence