Key Insights

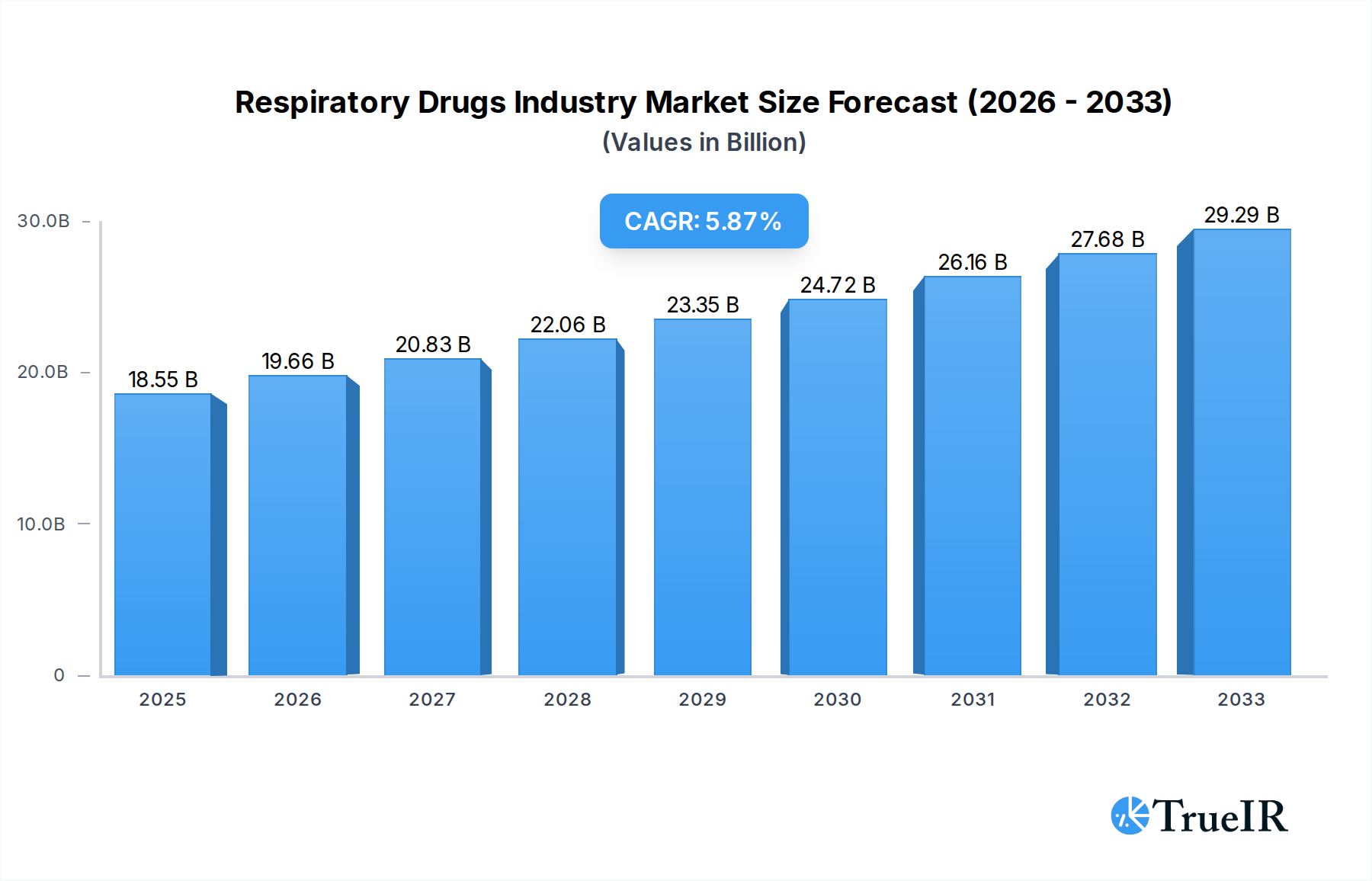

The global Respiratory Drugs market is poised for robust growth, projected to reach USD 18.55 billion in 2025 with a compound annual growth rate (CAGR) of 5.8% from 2025 to 2033. This expansion is driven by a confluence of factors, including the increasing prevalence of chronic respiratory diseases such as asthma and COPD, rising air pollution levels, and a growing aging population more susceptible to respiratory ailments. The market's dynamism is further fueled by advancements in drug development, leading to the introduction of more targeted and effective therapies like monoclonal antibodies and combination drugs. These innovations are crucial in managing complex respiratory conditions and improving patient outcomes. Furthermore, a heightened awareness and diagnosis of allergic rhinitis and pulmonary arterial hypertension are also contributing to market expansion. Pharmaceutical companies are heavily investing in research and development, anticipating a surge in demand for innovative treatment solutions.

Respiratory Drugs Industry Market Size (In Billion)

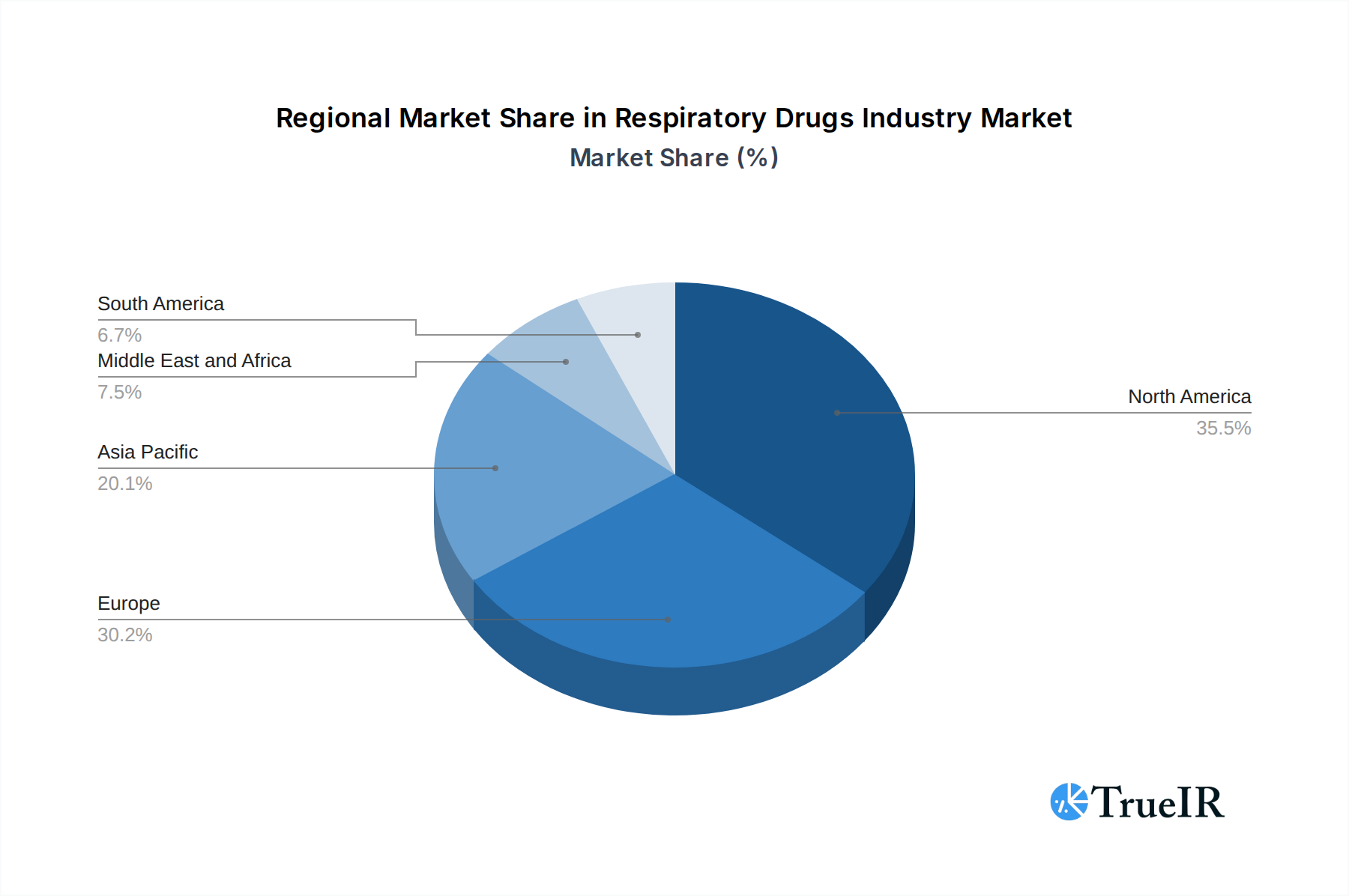

The market's segmentation reveals a diverse landscape. Within drug classes, Beta-2 Agonists, Oral and Inhaled Corticosteroids, and Combination Drugs are expected to command significant shares due to their established efficacy in managing common respiratory conditions. Asthma and COPD remain the primary indications driving market demand, underscoring the persistent burden of these diseases globally. The distribution channels also reflect varied accessibility, with hospital pharmacies playing a crucial role in dispensing specialized treatments, while retail pharmacies cater to a broader patient base for chronic management. Key players like Sanofi SA, Teva Pharmaceutical Industries Ltd, Regeneron Pharmaceuticals Inc, Merck & Co Inc, F Hoffmann-La Roche Ltd, AstraZeneca PLC, and GlaxoSmithKline PLC are at the forefront, competing through product innovation, strategic collaborations, and expanding their global reach. Geographically, North America and Europe are anticipated to maintain their leadership positions, driven by high healthcare expenditure and advanced healthcare infrastructure, while the Asia Pacific region presents significant growth opportunities due to increasing healthcare access and a burgeoning patient population.

Respiratory Drugs Industry Company Market Share

Comprehensive Respiratory Drugs Industry Market Report: Trends, Opportunities, and Competitive Landscape (2019–2033)

This in-depth market analysis provides a granular view of the global Respiratory Drugs Industry, covering a study period from 2019 to 2033, with a base and estimated year of 2025. The report meticulously examines market dynamics, key players, and future projections, offering critical insights for stakeholders within the pharmaceutical and healthcare sectors. With a projected market size reaching billions by 2033, this report is essential for understanding the evolving landscape of respiratory therapeutics.

Respiratory Drugs Industry Market Structure & Competitive Landscape

The Respiratory Drugs Industry is characterized by a moderately concentrated market structure, driven by significant R&D investments and stringent regulatory frameworks. Innovation remains a primary differentiator, with companies actively pursuing novel drug delivery systems and targeted therapies to address unmet medical needs in chronic respiratory diseases like Asthma and COPD. The presence of established pharmaceutical giants and emerging biotechs fosters a dynamic competitive environment. Market growth is further influenced by increasing healthcare expenditure globally, a growing prevalence of respiratory conditions, and strategic mergers and acquisitions aimed at expanding product portfolios and market reach. Substitutes, while present in the form of lifestyle interventions and supportive care, are largely outpaced by the efficacy of pharmacological treatments. End-user segmentation reveals a strong reliance on hospital pharmacies for critical care and specialized treatments, while retail pharmacies cater to chronic disease management. M&A activities are expected to remain robust, with an estimated volume of xx billion in deal value, as larger players seek to acquire innovative technologies and diversify their offerings.

- Market Concentration: Moderate, with key players holding substantial market share.

- Innovation Drivers: Novel drug targets, advanced drug delivery, personalized medicine.

- Regulatory Impacts: Strict approval processes by agencies like FDA and EMA.

- Product Substitutes: Lifestyle modifications, physiotherapy (limited impact on severe conditions).

- End-User Segmentation: Hospital Pharmacies (specialized/critical care), Retail Pharmacies (chronic management).

- M&A Trends: Strategic acquisitions for pipeline expansion and market consolidation.

Respiratory Drugs Industry Market Trends & Opportunities

The global Respiratory Drugs Industry is poised for significant expansion, projected to witness a Compound Annual Growth Rate (CAGR) of xx% between 2025 and 2033, pushing market valuation into the hundreds of billions. This growth is underpinned by a confluence of escalating prevalence of respiratory ailments such as Asthma and COPD, an aging global population susceptible to these conditions, and a rising awareness regarding advanced treatment options. Technological advancements are at the forefront, with a burgeoning interest in biologics and monoclonal antibodies offering targeted therapies with improved efficacy and reduced side effects for severe respiratory diseases. The shift towards precision medicine and patient-centric care is also shaping market trends, encouraging the development of personalized treatment regimens. Furthermore, increasing healthcare infrastructure development in emerging economies is creating new market opportunities for pharmaceutical companies. Consumer preferences are increasingly leaning towards convenient and effective drug delivery systems, such as inhalers and nebulizers, driving innovation in this space. The competitive landscape is intensifying, with key players continuously investing in R&D to develop next-generation therapeutics and secure intellectual property. Opportunities abound for companies that can innovate in areas of unmet medical needs, such as Idiopathic Pulmonary Fibrosis (IPF) and severe exacerbations of COPD. The report will delve into the detailed market size growth projections, anticipated technological shifts, evolving consumer preferences, and the intricate competitive dynamics that will define the respiratory therapeutics market in the coming decade. Market penetration rates for advanced therapies are expected to rise as affordability and accessibility improve.

Dominant Markets & Segments in Respiratory Drugs Industry

The global Respiratory Drugs Industry showcases distinct regional dominance and segment leadership. North America currently holds the largest market share, driven by high healthcare spending, advanced medical infrastructure, and a high prevalence of respiratory conditions, particularly Asthma and COPD. The United States, in particular, stands out due to its robust pharmaceutical R&D ecosystem and a significant patient population. In terms of drug classes, Oral and Inhaled Corticosteroids and Beta-2 Agonists represent the largest segments, forming the backbone of treatment for common respiratory diseases. These drug classes benefit from a long history of clinical use, established efficacy, and widespread availability.

- Leading Region: North America, followed by Europe and Asia Pacific.

- Key Country: United States, Germany, Japan.

- Dominant Drug Class: Oral and Inhaled Corticosteroids, Beta-2 Agonists.

- Growth Drivers: Established efficacy, broad patient applicability, well-understood safety profiles.

- Market Dominance: High prescription rates for Asthma and COPD management.

- Dominant Indication: Asthma and COPD (Chronic Obstructive Pulmonary Disease).

- Growth Drivers: Increasing prevalence due to lifestyle factors and air pollution, aging population.

- Market Dominance: These conditions represent the largest patient burden and drive demand for continuous treatment.

- Dominant Distribution Channel: Retail Pharmacies.

- Growth Drivers: Convenient access for chronic disease management, patient preference for self-administration.

- Market Dominance: Facilitates ongoing supply of maintenance medications for millions of patients worldwide.

The Asthma and COPD indications are the primary revenue generators within the respiratory drugs market, owing to their chronic nature and widespread incidence. The market for Monoclonal Antibodies is experiencing rapid growth, fueled by their success in treating severe and complex respiratory conditions that are often refractory to traditional therapies, such as severe asthma. Combination Drugs are also gaining traction, offering enhanced patient compliance and therapeutic benefits by combining multiple active ingredients in a single dosage form, particularly for COPD management. Emerging markets in the Asia Pacific region are projected to witness the fastest growth, driven by improving healthcare access, increasing disposable incomes, and a rising burden of respiratory diseases.

Respiratory Drugs Industry Product Analysis

Product innovation in the Respiratory Drugs Industry is centered on developing more effective, safer, and convenient therapeutic options. Recent advancements include the introduction of novel biologics targeting specific inflammatory pathways in severe asthma and the development of long-acting bronchodilators and inhaled corticosteroids for improved COPD management. The focus is on precision medicine, tailoring treatments to individual patient profiles and disease severity. New drug delivery systems, such as smart inhalers and nebulizers, are enhancing patient adherence and treatment outcomes. Competitive advantages are being gained through superior efficacy, reduced side effect profiles, and innovative formulations that simplify dosing regimens.

Key Drivers, Barriers & Challenges in Respiratory Drugs Industry

The Respiratory Drugs Industry is propelled by several key drivers, including the escalating global prevalence of chronic respiratory diseases, a growing aging population, and significant advancements in pharmaceutical research and development. Technological innovations in drug discovery and delivery systems are crucial enablers. Economic factors like increasing healthcare expenditure and government initiatives supporting public health also contribute to market expansion.

Key challenges impacting the industry include stringent regulatory hurdles and lengthy approval processes for new drugs. Supply chain complexities and disruptions can affect the availability of raw materials and finished products. Intense competition among established players and the threat of generic drug entry also pose significant restraints. The high cost of novel therapies can also limit market access in certain regions.

Growth Drivers in the Respiratory Drugs Industry Market

The growth of the Respiratory Drugs Industry is primarily driven by the increasing incidence of chronic respiratory diseases like Asthma and COPD, exacerbated by environmental factors and lifestyle changes. Technological advancements in drug discovery, leading to the development of targeted therapies such as biologics and personalized medicine, are significant growth catalysts. Economic factors, including rising healthcare spending and improved access to treatment in emerging markets, further fuel market expansion. Supportive government policies and initiatives aimed at managing respiratory health also play a crucial role.

Challenges Impacting Respiratory Drugs Industry Growth

Despite robust growth prospects, the Respiratory Drugs Industry faces several challenges. Stringent regulatory requirements and the complex, time-consuming approval pathways for new drugs represent significant hurdles. Supply chain vulnerabilities, including the sourcing of active pharmaceutical ingredients and manufacturing complexities, can lead to disruptions. Intense competition from both branded and generic manufacturers exerts downward pressure on pricing. Furthermore, the high cost of innovative biologic therapies can limit patient access, particularly in resource-constrained regions, thereby impacting overall market penetration.

Key Players Shaping the Respiratory Drugs Industry Market

- Sanofi SA

- Teva Pharmaceutical Industries Ltd

- Regeneron Pharmaceuticals Inc

- Merck & Co Inc

- F Hoffmann-La Roche Ltd

- AstraZeneca PLC

- Circassia Pharmaceuticals Plc

- Sumitomo Dainippon Pharma Co Ltd

- Grifols S A

- Boehringer Ingelheim

- GlaxoSmithKline PLC

- Pfizer Inc

Significant Respiratory Drugs Industry Industry Milestones

- April 2022: Penn Medicine discovered a new type of cell, respiratory airway secretory cells (RASCs), deep within human lungs that exhibit stem-cell-like properties crucial for alveoli regeneration. This discovery suggests a potential new avenue for treating COPD by correcting disrupted regenerative functions.

- December 2021: AstraZeneca integrated a novel target for Idiopathic Pulmonary Fibrosis (IPF) into its drug development pipeline, identified using BenevolentAI's platform. This marks the second significant target identified through their collaboration, underscoring advancements in IPF and chronic kidney disease (CKD) treatment research.

Future Outlook for Respiratory Drugs Industry Market

The future outlook for the Respiratory Drugs Industry remains exceptionally positive, driven by ongoing innovation and an increasing global need for effective respiratory therapeutics. The market is expected to witness sustained growth propelled by the development of novel biologics, advanced combination therapies, and personalized treatment approaches for complex respiratory conditions. Emerging markets will present substantial growth opportunities as healthcare infrastructure and access to medicines improve. The continued focus on R&D, coupled with strategic collaborations and potential regulatory streamlining, will shape a dynamic and expanding market landscape, promising improved patient outcomes and significant commercial potential for industry stakeholders.

Respiratory Drugs Industry Segmentation

-

1. Drug Class

- 1.1. Beta-2 Agonists

- 1.2. Anti-cholinergic Agents

- 1.3. Oral and Inhaled Corticosteroids

- 1.4. Anti-leukotrienes

- 1.5. Antihistamines

- 1.6. Monoclonal Antibodies

- 1.7. Combination Drugs

- 1.8. Others

-

2. Indication

- 2.1. Asthma

- 2.2. COPD (Chronic Obstructive Pulmonary Disease)

- 2.3. Allergic Rhinitis

- 2.4. Pulmonary Arterial Hypertension

- 2.5. Cystic Fibrosis

- 2.6. Others

-

3. Distribution Channel

- 3.1. Hospital Pharmacies

- 3.2. Retail Pharmacies

- 3.3. Others

Respiratory Drugs Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Respiratory Drugs Industry Regional Market Share

Geographic Coverage of Respiratory Drugs Industry

Respiratory Drugs Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Drug Class

- 5.1.1. Beta-2 Agonists

- 5.1.2. Anti-cholinergic Agents

- 5.1.3. Oral and Inhaled Corticosteroids

- 5.1.4. Anti-leukotrienes

- 5.1.5. Antihistamines

- 5.1.6. Monoclonal Antibodies

- 5.1.7. Combination Drugs

- 5.1.8. Others

- 5.2. Market Analysis, Insights and Forecast - by Indication

- 5.2.1. Asthma

- 5.2.2. COPD (Chronic Obstructive Pulmonary Disease)

- 5.2.3. Allergic Rhinitis

- 5.2.4. Pulmonary Arterial Hypertension

- 5.2.5. Cystic Fibrosis

- 5.2.6. Others

- 5.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.3.1. Hospital Pharmacies

- 5.3.2. Retail Pharmacies

- 5.3.3. Others

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Middle East and Africa

- 5.4.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Drug Class

- 6. Global Respiratory Drugs Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Drug Class

- 6.1.1. Beta-2 Agonists

- 6.1.2. Anti-cholinergic Agents

- 6.1.3. Oral and Inhaled Corticosteroids

- 6.1.4. Anti-leukotrienes

- 6.1.5. Antihistamines

- 6.1.6. Monoclonal Antibodies

- 6.1.7. Combination Drugs

- 6.1.8. Others

- 6.2. Market Analysis, Insights and Forecast - by Indication

- 6.2.1. Asthma

- 6.2.2. COPD (Chronic Obstructive Pulmonary Disease)

- 6.2.3. Allergic Rhinitis

- 6.2.4. Pulmonary Arterial Hypertension

- 6.2.5. Cystic Fibrosis

- 6.2.6. Others

- 6.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 6.3.1. Hospital Pharmacies

- 6.3.2. Retail Pharmacies

- 6.3.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Drug Class

- 7. North America Respiratory Drugs Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Drug Class

- 7.1.1. Beta-2 Agonists

- 7.1.2. Anti-cholinergic Agents

- 7.1.3. Oral and Inhaled Corticosteroids

- 7.1.4. Anti-leukotrienes

- 7.1.5. Antihistamines

- 7.1.6. Monoclonal Antibodies

- 7.1.7. Combination Drugs

- 7.1.8. Others

- 7.2. Market Analysis, Insights and Forecast - by Indication

- 7.2.1. Asthma

- 7.2.2. COPD (Chronic Obstructive Pulmonary Disease)

- 7.2.3. Allergic Rhinitis

- 7.2.4. Pulmonary Arterial Hypertension

- 7.2.5. Cystic Fibrosis

- 7.2.6. Others

- 7.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 7.3.1. Hospital Pharmacies

- 7.3.2. Retail Pharmacies

- 7.3.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Drug Class

- 8. Europe Respiratory Drugs Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Drug Class

- 8.1.1. Beta-2 Agonists

- 8.1.2. Anti-cholinergic Agents

- 8.1.3. Oral and Inhaled Corticosteroids

- 8.1.4. Anti-leukotrienes

- 8.1.5. Antihistamines

- 8.1.6. Monoclonal Antibodies

- 8.1.7. Combination Drugs

- 8.1.8. Others

- 8.2. Market Analysis, Insights and Forecast - by Indication

- 8.2.1. Asthma

- 8.2.2. COPD (Chronic Obstructive Pulmonary Disease)

- 8.2.3. Allergic Rhinitis

- 8.2.4. Pulmonary Arterial Hypertension

- 8.2.5. Cystic Fibrosis

- 8.2.6. Others

- 8.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 8.3.1. Hospital Pharmacies

- 8.3.2. Retail Pharmacies

- 8.3.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Drug Class

- 9. Asia Pacific Respiratory Drugs Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Drug Class

- 9.1.1. Beta-2 Agonists

- 9.1.2. Anti-cholinergic Agents

- 9.1.3. Oral and Inhaled Corticosteroids

- 9.1.4. Anti-leukotrienes

- 9.1.5. Antihistamines

- 9.1.6. Monoclonal Antibodies

- 9.1.7. Combination Drugs

- 9.1.8. Others

- 9.2. Market Analysis, Insights and Forecast - by Indication

- 9.2.1. Asthma

- 9.2.2. COPD (Chronic Obstructive Pulmonary Disease)

- 9.2.3. Allergic Rhinitis

- 9.2.4. Pulmonary Arterial Hypertension

- 9.2.5. Cystic Fibrosis

- 9.2.6. Others

- 9.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 9.3.1. Hospital Pharmacies

- 9.3.2. Retail Pharmacies

- 9.3.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Drug Class

- 10. Middle East and Africa Respiratory Drugs Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Drug Class

- 10.1.1. Beta-2 Agonists

- 10.1.2. Anti-cholinergic Agents

- 10.1.3. Oral and Inhaled Corticosteroids

- 10.1.4. Anti-leukotrienes

- 10.1.5. Antihistamines

- 10.1.6. Monoclonal Antibodies

- 10.1.7. Combination Drugs

- 10.1.8. Others

- 10.2. Market Analysis, Insights and Forecast - by Indication

- 10.2.1. Asthma

- 10.2.2. COPD (Chronic Obstructive Pulmonary Disease)

- 10.2.3. Allergic Rhinitis

- 10.2.4. Pulmonary Arterial Hypertension

- 10.2.5. Cystic Fibrosis

- 10.2.6. Others

- 10.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 10.3.1. Hospital Pharmacies

- 10.3.2. Retail Pharmacies

- 10.3.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Drug Class

- 11. South America Respiratory Drugs Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Drug Class

- 11.1.1. Beta-2 Agonists

- 11.1.2. Anti-cholinergic Agents

- 11.1.3. Oral and Inhaled Corticosteroids

- 11.1.4. Anti-leukotrienes

- 11.1.5. Antihistamines

- 11.1.6. Monoclonal Antibodies

- 11.1.7. Combination Drugs

- 11.1.8. Others

- 11.2. Market Analysis, Insights and Forecast - by Indication

- 11.2.1. Asthma

- 11.2.2. COPD (Chronic Obstructive Pulmonary Disease)

- 11.2.3. Allergic Rhinitis

- 11.2.4. Pulmonary Arterial Hypertension

- 11.2.5. Cystic Fibrosis

- 11.2.6. Others

- 11.3. Market Analysis, Insights and Forecast - by Distribution Channel

- 11.3.1. Hospital Pharmacies

- 11.3.2. Retail Pharmacies

- 11.3.3. Others

- 11.1. Market Analysis, Insights and Forecast - by Drug Class

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Sanofi SA

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Teva Pharmaceutical Industries Ltd

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Regeneron Pharmaceuticals Inc

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Merck & Co Inc

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 F Hoffmann-La Roche Ltd

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 AstraZeneca PLC

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Circassia Pharmaceuticals Plc

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Sumitomo Dainippon Pharma Co Ltd

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Grifols S A

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Boehringer Ingelheim

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 GlaxoSmithKline PLC

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Pfizer Inc

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.1 Sanofi SA

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Respiratory Drugs Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Global Respiratory Drugs Industry Volume Breakdown (K Unit, %) by Region 2025 & 2033

- Figure 3: North America Respiratory Drugs Industry Revenue (billion), by Drug Class 2025 & 2033

- Figure 4: North America Respiratory Drugs Industry Volume (K Unit), by Drug Class 2025 & 2033

- Figure 5: North America Respiratory Drugs Industry Revenue Share (%), by Drug Class 2025 & 2033

- Figure 6: North America Respiratory Drugs Industry Volume Share (%), by Drug Class 2025 & 2033

- Figure 7: North America Respiratory Drugs Industry Revenue (billion), by Indication 2025 & 2033

- Figure 8: North America Respiratory Drugs Industry Volume (K Unit), by Indication 2025 & 2033

- Figure 9: North America Respiratory Drugs Industry Revenue Share (%), by Indication 2025 & 2033

- Figure 10: North America Respiratory Drugs Industry Volume Share (%), by Indication 2025 & 2033

- Figure 11: North America Respiratory Drugs Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 12: North America Respiratory Drugs Industry Volume (K Unit), by Distribution Channel 2025 & 2033

- Figure 13: North America Respiratory Drugs Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 14: North America Respiratory Drugs Industry Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 15: North America Respiratory Drugs Industry Revenue (billion), by Country 2025 & 2033

- Figure 16: North America Respiratory Drugs Industry Volume (K Unit), by Country 2025 & 2033

- Figure 17: North America Respiratory Drugs Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: North America Respiratory Drugs Industry Volume Share (%), by Country 2025 & 2033

- Figure 19: Europe Respiratory Drugs Industry Revenue (billion), by Drug Class 2025 & 2033

- Figure 20: Europe Respiratory Drugs Industry Volume (K Unit), by Drug Class 2025 & 2033

- Figure 21: Europe Respiratory Drugs Industry Revenue Share (%), by Drug Class 2025 & 2033

- Figure 22: Europe Respiratory Drugs Industry Volume Share (%), by Drug Class 2025 & 2033

- Figure 23: Europe Respiratory Drugs Industry Revenue (billion), by Indication 2025 & 2033

- Figure 24: Europe Respiratory Drugs Industry Volume (K Unit), by Indication 2025 & 2033

- Figure 25: Europe Respiratory Drugs Industry Revenue Share (%), by Indication 2025 & 2033

- Figure 26: Europe Respiratory Drugs Industry Volume Share (%), by Indication 2025 & 2033

- Figure 27: Europe Respiratory Drugs Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 28: Europe Respiratory Drugs Industry Volume (K Unit), by Distribution Channel 2025 & 2033

- Figure 29: Europe Respiratory Drugs Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 30: Europe Respiratory Drugs Industry Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 31: Europe Respiratory Drugs Industry Revenue (billion), by Country 2025 & 2033

- Figure 32: Europe Respiratory Drugs Industry Volume (K Unit), by Country 2025 & 2033

- Figure 33: Europe Respiratory Drugs Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Europe Respiratory Drugs Industry Volume Share (%), by Country 2025 & 2033

- Figure 35: Asia Pacific Respiratory Drugs Industry Revenue (billion), by Drug Class 2025 & 2033

- Figure 36: Asia Pacific Respiratory Drugs Industry Volume (K Unit), by Drug Class 2025 & 2033

- Figure 37: Asia Pacific Respiratory Drugs Industry Revenue Share (%), by Drug Class 2025 & 2033

- Figure 38: Asia Pacific Respiratory Drugs Industry Volume Share (%), by Drug Class 2025 & 2033

- Figure 39: Asia Pacific Respiratory Drugs Industry Revenue (billion), by Indication 2025 & 2033

- Figure 40: Asia Pacific Respiratory Drugs Industry Volume (K Unit), by Indication 2025 & 2033

- Figure 41: Asia Pacific Respiratory Drugs Industry Revenue Share (%), by Indication 2025 & 2033

- Figure 42: Asia Pacific Respiratory Drugs Industry Volume Share (%), by Indication 2025 & 2033

- Figure 43: Asia Pacific Respiratory Drugs Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 44: Asia Pacific Respiratory Drugs Industry Volume (K Unit), by Distribution Channel 2025 & 2033

- Figure 45: Asia Pacific Respiratory Drugs Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 46: Asia Pacific Respiratory Drugs Industry Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 47: Asia Pacific Respiratory Drugs Industry Revenue (billion), by Country 2025 & 2033

- Figure 48: Asia Pacific Respiratory Drugs Industry Volume (K Unit), by Country 2025 & 2033

- Figure 49: Asia Pacific Respiratory Drugs Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: Asia Pacific Respiratory Drugs Industry Volume Share (%), by Country 2025 & 2033

- Figure 51: Middle East and Africa Respiratory Drugs Industry Revenue (billion), by Drug Class 2025 & 2033

- Figure 52: Middle East and Africa Respiratory Drugs Industry Volume (K Unit), by Drug Class 2025 & 2033

- Figure 53: Middle East and Africa Respiratory Drugs Industry Revenue Share (%), by Drug Class 2025 & 2033

- Figure 54: Middle East and Africa Respiratory Drugs Industry Volume Share (%), by Drug Class 2025 & 2033

- Figure 55: Middle East and Africa Respiratory Drugs Industry Revenue (billion), by Indication 2025 & 2033

- Figure 56: Middle East and Africa Respiratory Drugs Industry Volume (K Unit), by Indication 2025 & 2033

- Figure 57: Middle East and Africa Respiratory Drugs Industry Revenue Share (%), by Indication 2025 & 2033

- Figure 58: Middle East and Africa Respiratory Drugs Industry Volume Share (%), by Indication 2025 & 2033

- Figure 59: Middle East and Africa Respiratory Drugs Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 60: Middle East and Africa Respiratory Drugs Industry Volume (K Unit), by Distribution Channel 2025 & 2033

- Figure 61: Middle East and Africa Respiratory Drugs Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 62: Middle East and Africa Respiratory Drugs Industry Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 63: Middle East and Africa Respiratory Drugs Industry Revenue (billion), by Country 2025 & 2033

- Figure 64: Middle East and Africa Respiratory Drugs Industry Volume (K Unit), by Country 2025 & 2033

- Figure 65: Middle East and Africa Respiratory Drugs Industry Revenue Share (%), by Country 2025 & 2033

- Figure 66: Middle East and Africa Respiratory Drugs Industry Volume Share (%), by Country 2025 & 2033

- Figure 67: South America Respiratory Drugs Industry Revenue (billion), by Drug Class 2025 & 2033

- Figure 68: South America Respiratory Drugs Industry Volume (K Unit), by Drug Class 2025 & 2033

- Figure 69: South America Respiratory Drugs Industry Revenue Share (%), by Drug Class 2025 & 2033

- Figure 70: South America Respiratory Drugs Industry Volume Share (%), by Drug Class 2025 & 2033

- Figure 71: South America Respiratory Drugs Industry Revenue (billion), by Indication 2025 & 2033

- Figure 72: South America Respiratory Drugs Industry Volume (K Unit), by Indication 2025 & 2033

- Figure 73: South America Respiratory Drugs Industry Revenue Share (%), by Indication 2025 & 2033

- Figure 74: South America Respiratory Drugs Industry Volume Share (%), by Indication 2025 & 2033

- Figure 75: South America Respiratory Drugs Industry Revenue (billion), by Distribution Channel 2025 & 2033

- Figure 76: South America Respiratory Drugs Industry Volume (K Unit), by Distribution Channel 2025 & 2033

- Figure 77: South America Respiratory Drugs Industry Revenue Share (%), by Distribution Channel 2025 & 2033

- Figure 78: South America Respiratory Drugs Industry Volume Share (%), by Distribution Channel 2025 & 2033

- Figure 79: South America Respiratory Drugs Industry Revenue (billion), by Country 2025 & 2033

- Figure 80: South America Respiratory Drugs Industry Volume (K Unit), by Country 2025 & 2033

- Figure 81: South America Respiratory Drugs Industry Revenue Share (%), by Country 2025 & 2033

- Figure 82: South America Respiratory Drugs Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Respiratory Drugs Industry Revenue billion Forecast, by Drug Class 2020 & 2033

- Table 2: Global Respiratory Drugs Industry Volume K Unit Forecast, by Drug Class 2020 & 2033

- Table 3: Global Respiratory Drugs Industry Revenue billion Forecast, by Indication 2020 & 2033

- Table 4: Global Respiratory Drugs Industry Volume K Unit Forecast, by Indication 2020 & 2033

- Table 5: Global Respiratory Drugs Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 6: Global Respiratory Drugs Industry Volume K Unit Forecast, by Distribution Channel 2020 & 2033

- Table 7: Global Respiratory Drugs Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 8: Global Respiratory Drugs Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 9: Global Respiratory Drugs Industry Revenue billion Forecast, by Drug Class 2020 & 2033

- Table 10: Global Respiratory Drugs Industry Volume K Unit Forecast, by Drug Class 2020 & 2033

- Table 11: Global Respiratory Drugs Industry Revenue billion Forecast, by Indication 2020 & 2033

- Table 12: Global Respiratory Drugs Industry Volume K Unit Forecast, by Indication 2020 & 2033

- Table 13: Global Respiratory Drugs Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 14: Global Respiratory Drugs Industry Volume K Unit Forecast, by Distribution Channel 2020 & 2033

- Table 15: Global Respiratory Drugs Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: Global Respiratory Drugs Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 17: United States Respiratory Drugs Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: United States Respiratory Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 19: Canada Respiratory Drugs Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Canada Respiratory Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 21: Mexico Respiratory Drugs Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Mexico Respiratory Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 23: Global Respiratory Drugs Industry Revenue billion Forecast, by Drug Class 2020 & 2033

- Table 24: Global Respiratory Drugs Industry Volume K Unit Forecast, by Drug Class 2020 & 2033

- Table 25: Global Respiratory Drugs Industry Revenue billion Forecast, by Indication 2020 & 2033

- Table 26: Global Respiratory Drugs Industry Volume K Unit Forecast, by Indication 2020 & 2033

- Table 27: Global Respiratory Drugs Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 28: Global Respiratory Drugs Industry Volume K Unit Forecast, by Distribution Channel 2020 & 2033

- Table 29: Global Respiratory Drugs Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 30: Global Respiratory Drugs Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 31: Germany Respiratory Drugs Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Germany Respiratory Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 33: United Kingdom Respiratory Drugs Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: United Kingdom Respiratory Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 35: France Respiratory Drugs Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: France Respiratory Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 37: Italy Respiratory Drugs Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: Italy Respiratory Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 39: Spain Respiratory Drugs Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Spain Respiratory Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 41: Rest of Europe Respiratory Drugs Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Rest of Europe Respiratory Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 43: Global Respiratory Drugs Industry Revenue billion Forecast, by Drug Class 2020 & 2033

- Table 44: Global Respiratory Drugs Industry Volume K Unit Forecast, by Drug Class 2020 & 2033

- Table 45: Global Respiratory Drugs Industry Revenue billion Forecast, by Indication 2020 & 2033

- Table 46: Global Respiratory Drugs Industry Volume K Unit Forecast, by Indication 2020 & 2033

- Table 47: Global Respiratory Drugs Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 48: Global Respiratory Drugs Industry Volume K Unit Forecast, by Distribution Channel 2020 & 2033

- Table 49: Global Respiratory Drugs Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 50: Global Respiratory Drugs Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 51: China Respiratory Drugs Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 52: China Respiratory Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 53: Japan Respiratory Drugs Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 54: Japan Respiratory Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 55: India Respiratory Drugs Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 56: India Respiratory Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 57: Australia Respiratory Drugs Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 58: Australia Respiratory Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 59: South Korea Respiratory Drugs Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 60: South Korea Respiratory Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 61: Rest of Asia Pacific Respiratory Drugs Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 62: Rest of Asia Pacific Respiratory Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 63: Global Respiratory Drugs Industry Revenue billion Forecast, by Drug Class 2020 & 2033

- Table 64: Global Respiratory Drugs Industry Volume K Unit Forecast, by Drug Class 2020 & 2033

- Table 65: Global Respiratory Drugs Industry Revenue billion Forecast, by Indication 2020 & 2033

- Table 66: Global Respiratory Drugs Industry Volume K Unit Forecast, by Indication 2020 & 2033

- Table 67: Global Respiratory Drugs Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 68: Global Respiratory Drugs Industry Volume K Unit Forecast, by Distribution Channel 2020 & 2033

- Table 69: Global Respiratory Drugs Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 70: Global Respiratory Drugs Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 71: GCC Respiratory Drugs Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 72: GCC Respiratory Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 73: South Africa Respiratory Drugs Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 74: South Africa Respiratory Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 75: Rest of Middle East and Africa Respiratory Drugs Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 76: Rest of Middle East and Africa Respiratory Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 77: Global Respiratory Drugs Industry Revenue billion Forecast, by Drug Class 2020 & 2033

- Table 78: Global Respiratory Drugs Industry Volume K Unit Forecast, by Drug Class 2020 & 2033

- Table 79: Global Respiratory Drugs Industry Revenue billion Forecast, by Indication 2020 & 2033

- Table 80: Global Respiratory Drugs Industry Volume K Unit Forecast, by Indication 2020 & 2033

- Table 81: Global Respiratory Drugs Industry Revenue billion Forecast, by Distribution Channel 2020 & 2033

- Table 82: Global Respiratory Drugs Industry Volume K Unit Forecast, by Distribution Channel 2020 & 2033

- Table 83: Global Respiratory Drugs Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 84: Global Respiratory Drugs Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 85: Brazil Respiratory Drugs Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 86: Brazil Respiratory Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 87: Argentina Respiratory Drugs Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 88: Argentina Respiratory Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

- Table 89: Rest of South America Respiratory Drugs Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 90: Rest of South America Respiratory Drugs Industry Volume (K Unit) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Respiratory Drugs Industry?

The projected CAGR is approximately 5.8%.

2. Which companies are prominent players in the Respiratory Drugs Industry?

Key companies in the market include Sanofi SA, Teva Pharmaceutical Industries Ltd , Regeneron Pharmaceuticals Inc, Merck & Co Inc, F Hoffmann-La Roche Ltd, AstraZeneca PLC, Circassia Pharmaceuticals Plc, Sumitomo Dainippon Pharma Co Ltd, Grifols S A, Boehringer Ingelheim, GlaxoSmithKline PLC, Pfizer Inc.

3. What are the main segments of the Respiratory Drugs Industry?

The market segments include Drug Class, Indication, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 18.55 billion as of 2022.

5. What are some drivers contributing to market growth?

Rising Prevalence of Pulmonary Diseases; Increasing Burden of Geriatric Population.

6. What are the notable trends driving market growth?

Treatment for Chronic Obstructive Pulmonary Disease is Expected to Witness Growth Over the Forecast Period.

7. Are there any restraints impacting market growth?

Stringent Government Regulations for Product Approval; Side Effects Associated With Drugs.

8. Can you provide examples of recent developments in the market?

In April 2022, Penn Medicine discovered a new type of cell that resides deep within human lungs and may play a key role in human lung diseases. The researchers, analyzed human lung tissue to identify the new cells, which they called respiratory airway secretory cells (RASCs). The cells line tiny airway branches, deep in the lungs, near the alveoli structures where oxygen is exchanged for carbon dioxide. The scientists showed that Renal Allograft Compartment Syndrome (RASCs) have stem-cell-like properties enabling them to regenerate other cells that are essential for the normal functioning of alveoli. They also found evidence that cigarette smoking and the common smoking-related ailment called chronic obstructive pulmonary disease (COPD) can disrupt the regenerative functions of Renal Allograft Compartment Syndrome (RASCs)-hinting that correcting this disruption could be a good way to treat COPD.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Respiratory Drugs Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Respiratory Drugs Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Respiratory Drugs Industry?

To stay informed about further developments, trends, and reports in the Respiratory Drugs Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence