Key Insights

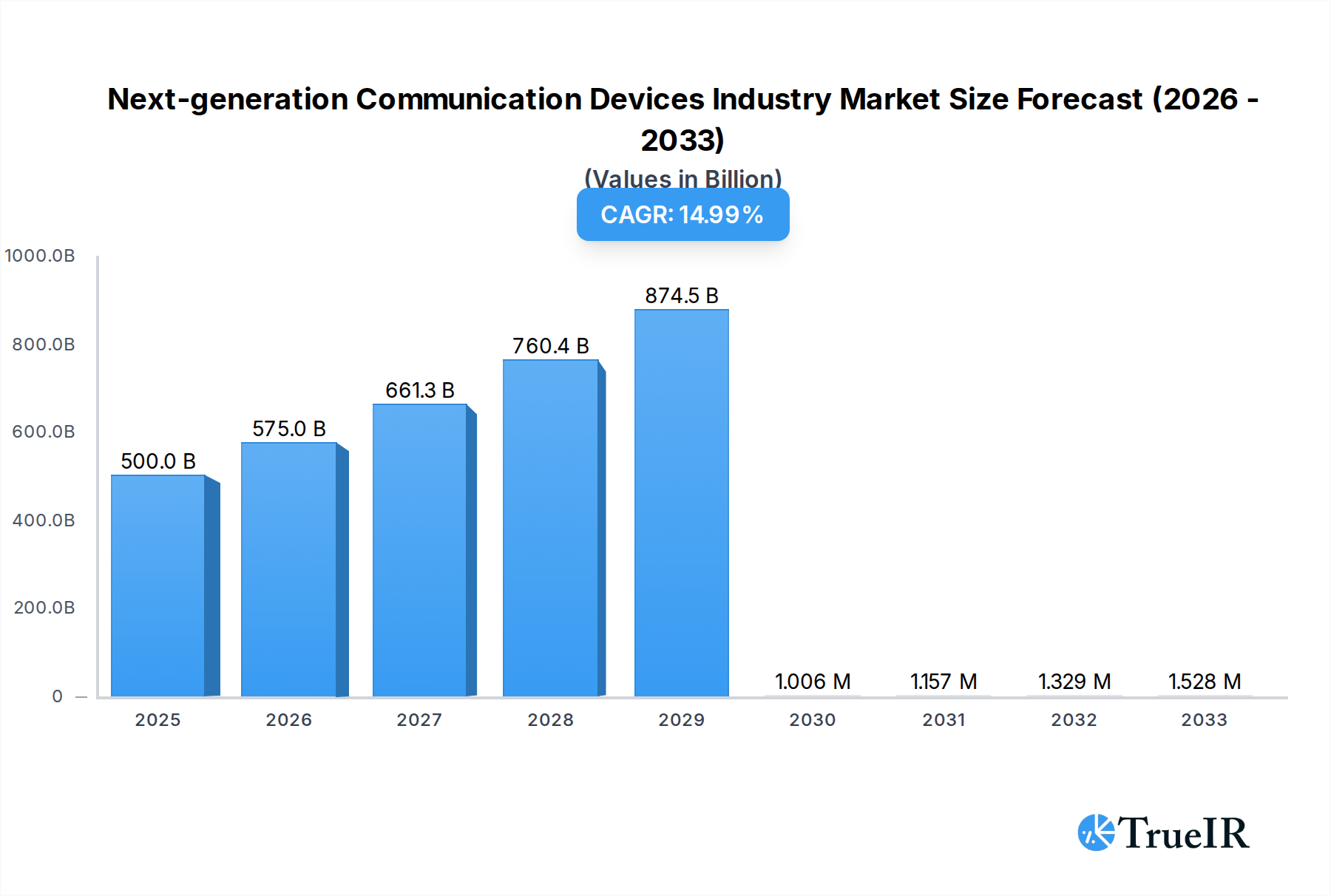

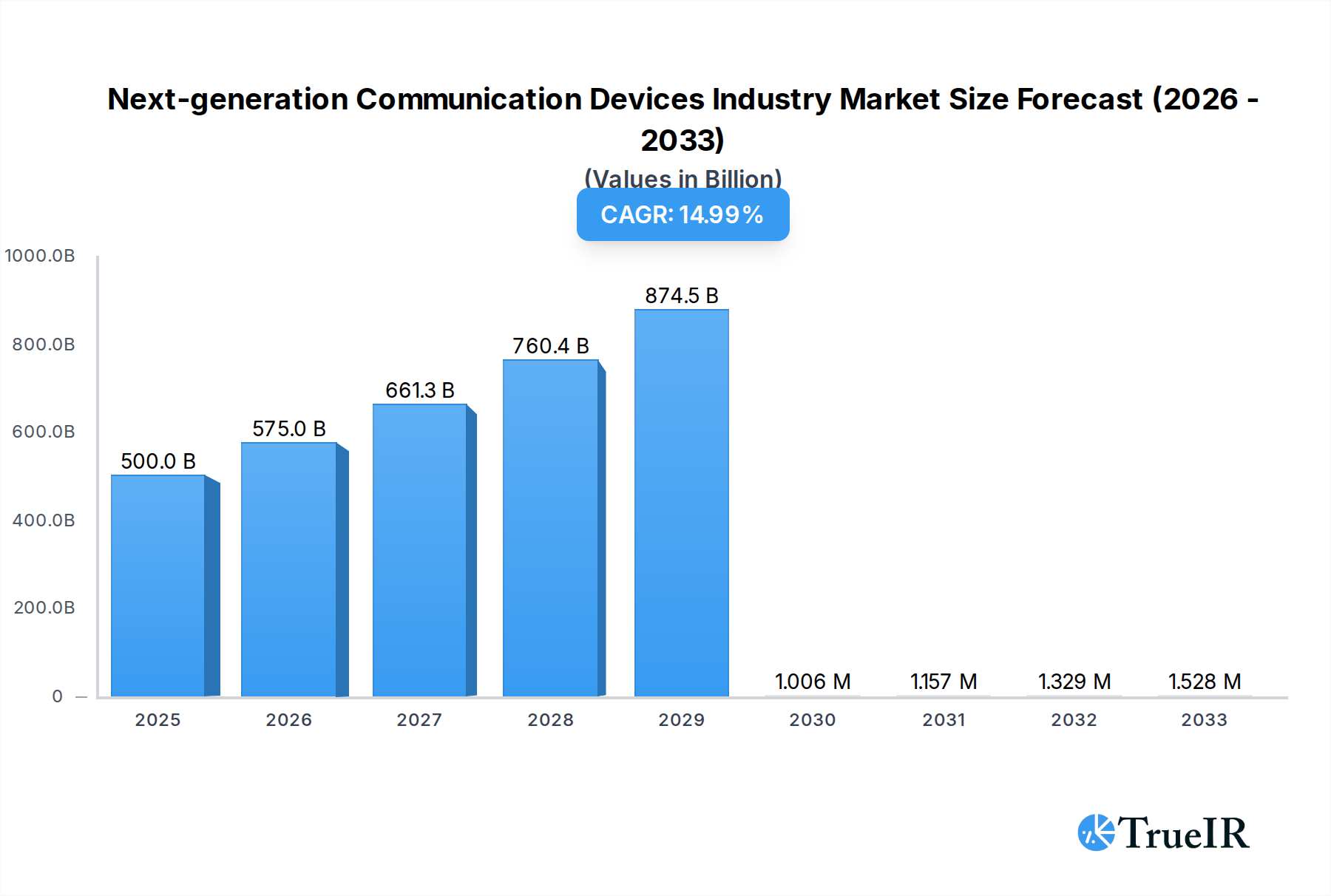

The Next-generation Communication Devices Industry is poised for substantial expansion, projecting a robust market size of USD 500 billion in 2025, with an anticipated Compound Annual Growth Rate (CAGR) of 15% through 2033. This dynamic growth is primarily fueled by the escalating demand for faster, more reliable, and secure communication solutions across diverse sectors. Key drivers include the rapid deployment of 5G networks, the emergence of innovative technologies like Visible Light Communication (VLC) / Li-Fi, and the increasing integration of Wireless Sensor Networks (WSN) for enhanced data collection and connectivity. These advancements are critical for supporting the growing volume of data traffic and the proliferation of connected devices, from smart factories to autonomous vehicles. The industry's trajectory is further bolstered by advancements in infrastructure and the development of specialized devices designed for high-performance communication.

Next-generation Communication Devices Industry Market Size (In Billion)

The market's expansion is further shaped by significant trends such as the increasing adoption of IoT devices, the growing need for low-latency communication in industries like gaming and virtual reality, and the imperative for enhanced cybersecurity in communication systems. While the potential for exponential growth is evident, certain restraints exist, including the high cost of infrastructure deployment for new technologies, regulatory hurdles in certain regions, and the ongoing challenge of ensuring widespread interoperability and standardization. Nevertheless, the industry is actively addressing these challenges through strategic investments, research and development, and collaborative efforts. Key end-user industries driving this growth include Manufacturing, where automation and real-time monitoring are paramount; Military and Defense, demanding secure and resilient communication; and Automotive, with the advent of connected and autonomous vehicles. Companies such as Honeywell, PureLiFi, Analog Devices, Ericsson, Cisco, Philips, and Qualcomm are at the forefront of developing and deploying these transformative communication devices.

Next-generation Communication Devices Industry Company Market Share

This comprehensive report delves into the dynamic Next-generation Communication Devices Industry, providing an in-depth analysis of market structure, trends, opportunities, and future outlook. With a study period spanning from 2019 to 2033, including a base year of 2025 and a forecast period from 2025 to 2033, this report offers invaluable insights for stakeholders navigating this rapidly evolving sector. Leveraging high-volume keywords and detailed market segmentation, this report is optimized for search engines and designed to engage industry professionals seeking a competitive edge.

Next-generation Communication Devices Industry Market Structure & Competitive Landscape

The Next-generation Communication Devices Industry exhibits a moderately consolidated market structure, with leading players investing heavily in research and development to drive innovation. Key innovation drivers include the escalating demand for faster data speeds, lower latency, and enhanced connectivity across diverse applications, from IoT deployments to advanced autonomous systems. Regulatory impacts, while varied across regions, are increasingly focused on spectrum allocation and cybersecurity standards, shaping market entry and product development strategies. Product substitutes, though emerging, are largely complementary rather than directly competitive at this stage, with advancements in 5G and Visible Light Communication (VLC)/Li-Fi offering unique advantages. End-user segmentation reveals significant growth in the Manufacturing and Military & Defense sectors, driven by the need for real-time data processing and secure communication channels. Mergers and Acquisitions (M&A) trends are on the rise, with strategic consolidations aimed at expanding technological portfolios and market reach. The estimated M&A volume for the forecast period is projected to exceed xx billion USD. Concentration ratios are estimated to be around xx% for the top five players in key segments.

Next-generation Communication Devices Industry Market Trends & Opportunities

The Next-generation Communication Devices Industry is poised for substantial expansion, driven by a confluence of technological advancements and burgeoning market demand. The global market size is projected to reach xx trillion USD by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of xx% from 2025. Technological shifts are a primary catalyst, with the widespread adoption of 5G technology forming the bedrock for new communication paradigms. This transition is not merely an upgrade; it unlocks a plethora of new applications and services, including enhanced mobile broadband, ultra-reliable low-latency communication, and massive machine-type communication. Visible Light Communication (VLC)/Li-Fi is emerging as a significant complementary technology, offering secure, high-speed, and interference-free wireless data transmission, particularly in sensitive environments like hospitals, aircraft cabins, and secure facilities. Wireless Sensor Networks (WSN) continue to evolve, becoming more sophisticated and integral to the Internet of Things (IoT) ecosystem, enabling data collection and analysis for smart cities, industrial automation, and environmental monitoring. Consumer preferences are increasingly leaning towards seamless, high-performance connectivity that supports immersive experiences, remote work, and a proliferation of connected devices. The competitive dynamics are intensifying, with a strategic focus on developing integrated solutions that combine multiple communication technologies to cater to diverse end-user needs. Market penetration rates for next-generation devices are expected to surge, as infrastructure investments accelerate and the benefits of enhanced connectivity become more tangible. The market is also witnessing a rise in specialized devices tailored for niche applications within sectors like automotive (V2X communication) and defense (secure, jam-resistant communication).

Dominant Markets & Segments in Next-generation Communication Devices Industry

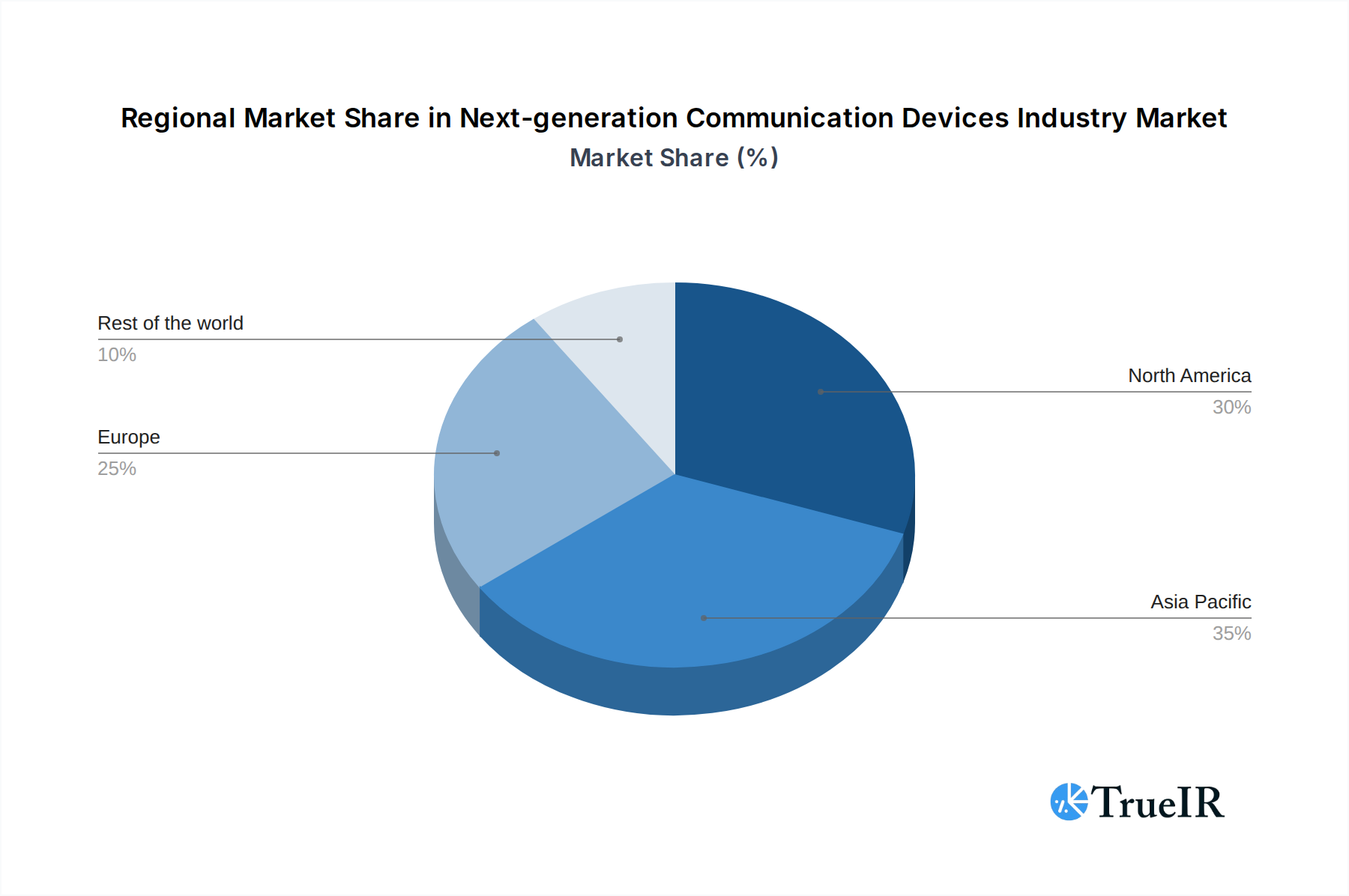

The Next-generation Communication Devices Industry is experiencing robust growth across multiple regions and segments. North America, led by the United States, and Asia-Pacific, spearheaded by China and South Korea, are emerging as dominant markets due to aggressive infrastructure development and high adoption rates of advanced technologies.

Technology Segments:

- 5G: This segment is the primary growth engine, fueled by massive government and private investments in 5G network deployment. Key growth drivers include:

- Ubiquitous High-Speed Connectivity: Enabling real-time data transfer for critical applications like autonomous vehicles and remote surgery.

- Enhanced Mobile Broadband (eMBB): Supporting the increasing demand for high-bandwidth services like 4K/8K video streaming and immersive gaming.

- Ultra-Reliable Low-Latency Communication (URLLC): Crucial for industrial automation, robotics, and mission-critical communications in defense.

- Massive Machine-Type Communication (mMTC): Facilitating the exponential growth of IoT devices.

- Visible Light Communication / Li-Fi: While still in its nascent stages compared to 5G, Li-Fi presents significant growth potential, especially in specific niches.

- Enhanced Security: Its inherent broadcast nature and inability to penetrate walls make it ideal for secure environments.

- Spectrum Efficiency: Utilizes existing lighting infrastructure, reducing the need for new spectrum allocation.

- High Data Rates: Offers comparable or even superior data speeds to some Wi-Fi standards.

- Interference-Free Operation: Valuable in environments sensitive to radio frequency interference.

- Wireless Sensor Networks (WSN): The expansion of the IoT landscape continues to drive WSN adoption.

- Industrial IoT (IIoT): Enabling smart manufacturing, predictive maintenance, and supply chain optimization.

- Smart Cities: Facilitating intelligent traffic management, environmental monitoring, and public safety.

- Healthcare Monitoring: Supporting remote patient care and real-time health tracking.

- Other Technologies: This includes advancements in satellite communication, quantum communication, and advanced Wi-Fi standards, catering to specialized needs and future connectivity solutions.

End User Industry Segments:

- Manufacturing: The adoption of Industry 4.0 principles is a major growth driver.

- Smart Factories: Real-time data acquisition and control for enhanced efficiency and automation.

- Predictive Maintenance: Minimizing downtime through sensor-based monitoring.

- Robotics and Automation: Enabling seamless communication between robots and control systems.

- Military and Defense: The demand for secure, reliable, and high-bandwidth communication is paramount.

- Situational Awareness: Real-time data sharing for enhanced battlefield intelligence.

- Secure Command and Control: Robust communication networks for mission-critical operations.

- Unmanned Systems: Reliable connectivity for drones, autonomous vehicles, and remote operations.

- Automotive: The advent of connected and autonomous vehicles is transforming this sector.

- Vehicle-to-Everything (V2X) Communication: Enhancing road safety, traffic flow, and infotainment.

- Over-the-Air (OTA) Updates: Enabling seamless software and firmware upgrades.

- In-Car Infotainment: Providing advanced entertainment and connectivity options.

- Other End Users Industries: This broad category encompasses telecommunications, healthcare, retail, and entertainment, all seeking to leverage next-generation communication for improved services and operational efficiencies.

Next-generation Communication Devices Industry Product Analysis

Product innovations in the Next-generation Communication Devices Industry are characterized by miniaturization, increased processing power, and enhanced energy efficiency. Devices are being designed with integrated multi-technology capabilities, supporting seamless transitions between 5G, Wi-Fi 6/7, and emerging standards. Applications range from advanced smartphones and wearables to industrial gateways, smart sensors, and sophisticated communication modules for vehicles and defense systems. Competitive advantages lie in superior data throughput, reduced latency, robust security features, and AI-driven network optimization.

Key Drivers, Barriers & Challenges in Next-generation Communication Devices Industry

Key Drivers:

- Technological Advancements: The relentless evolution of 5G, Li-Fi, and WSN technologies is a primary growth catalyst.

- Increasing Data Demand: The proliferation of data-intensive applications and the growth of the IoT ecosystem necessitate faster and more reliable communication.

- Government Initiatives & Investments: Global efforts to deploy 5G infrastructure and promote digital transformation are significant drivers.

- Demand for Enhanced Connectivity: Industries across the board are seeking improved connectivity for operational efficiency, automation, and new service delivery.

Barriers & Challenges:

- High Infrastructure Costs: The substantial investment required for deploying new communication networks, particularly 5G, poses a significant barrier.

- Regulatory Complexities: Navigating diverse spectrum regulations, cybersecurity mandates, and data privacy laws across different regions can be challenging.

- Supply Chain Disruptions: Global supply chain vulnerabilities, as evidenced by recent events, can impact the availability and cost of key components.

- Interoperability and Standardization: Ensuring seamless interoperability between different devices and technologies remains an ongoing challenge.

- Cybersecurity Threats: The increased connectivity opens up new avenues for cyberattacks, requiring robust security solutions.

Growth Drivers in the Next-generation Communication Devices Industry Market

The growth of the Next-generation Communication Devices Industry is propelled by several key factors. Technologically, the continued rollout and enhancement of 5G networks, coupled with the emerging potential of Li-Fi for specialized applications, are fundamental drivers. Economically, the increasing demand for high-speed, low-latency connectivity across industries like manufacturing, automotive, and defense is fueling investment. Government policies, including spectrum auctions and initiatives promoting digital transformation, are also playing a crucial role in accelerating market adoption. The expansion of the Internet of Things (IoT) ecosystem, with billions of devices requiring seamless communication, presents an unprecedented opportunity for growth.

Challenges Impacting Next-generation Communication Devices Industry Growth

Several challenges can impede the growth of the Next-generation Communication Devices Industry. Regulatory complexities surrounding spectrum allocation, international standards, and data privacy can create hurdles for widespread adoption and market entry. Supply chain issues, including component shortages and geopolitical uncertainties, can impact production and lead to increased costs. Competitive pressures are intensifying as established players and new entrants vie for market share, necessitating continuous innovation and cost-effectiveness. Furthermore, the significant capital expenditure required for network infrastructure upgrades presents a long-term challenge for many organizations.

Key Players Shaping the Next-generation Communication Devices Industry Market

- Honeywell International Inc

- Purelifi Ltd

- Analog Devices Inc

- Laser Light Global

- Telefonaktiebolaget LM Ericsson

- Cisco Systems Inc

- Panasonic Corp

- Netgear Inc

- Koninklijke Philips NV

- Huawei Technologies Co Ltd

- Qualcomm Technologies Inc

- Northrop Grumman Corporation

List Not Exhaustive

Significant Next-generation Communication Devices Industry Industry Milestones

- 2019: Initial widespread commercial deployments of 5G networks begin in select regions.

- 2020: Increased focus on R&D for Visible Light Communication (VLC)/Li-Fi due to its potential for secure and high-speed data transfer.

- 2021: Significant advancements in miniaturization and power efficiency for wireless sensor network (WSN) devices, enabling broader IoT applications.

- 2022: Major telecommunications equipment manufacturers announce partnerships to accelerate 5G Advanced and future 6G research.

- 2023: Growing adoption of Wi-Fi 6E and anticipation for Wi-Fi 7, further enhancing in-building wireless capabilities.

- 2024: Increased integration of AI and machine learning into communication devices for intelligent network management and enhanced user experience.

- 2025 (Estimated): Significant market penetration of 5G-enabled devices across consumer and enterprise segments.

- 2026-2030: Continued evolution of 5G capabilities, with early explorations and standardization efforts for 6G commencing. Expansion of Li-Fi into commercial and industrial use cases.

- 2031-2033: Emergence of early 6G technologies and widespread deployment of advanced WSN for hyper-connected environments.

Future Outlook for Next-generation Communication Devices Industry Market

The future outlook for the Next-generation Communication Devices Industry is exceptionally bright, driven by the continuous demand for hyper-connectivity and transformative technologies. Strategic opportunities lie in the further development and integration of 5G Advanced and the nascent stages of 6G, promising unprecedented data speeds, ultra-low latency, and enhanced network intelligence. The expansion of IoT ecosystems will continue to fuel the market for sophisticated wireless sensor networks. Furthermore, the increasing demand for secure and efficient data transmission will likely see Li-Fi carve out significant market share in specific enterprise and industrial applications. The market potential is vast, with ongoing innovation poised to enable revolutionary applications in areas such as extended reality (XR), fully autonomous systems, and pervasive digital integration across all facets of life.

Next-generation Communication Devices Industry Segmentation

-

1. Technology

- 1.1. 5G

- 1.2. Visible Light Communication / Li-Fi

- 1.3. Wireless Sensor Networks (WSN)

- 1.4. Other Technologies

-

2. End User Industry

- 2.1. Manufacturing

- 2.2. Military and Defense

- 2.3. Automotive

- 2.4. Other End Users Industries

Next-generation Communication Devices Industry Segmentation By Geography

- 1. North America

- 2. Asia Pacific

- 3. Europe

- 4. Rest of the world

Next-generation Communication Devices Industry Regional Market Share

Geographic Coverage of Next-generation Communication Devices Industry

Next-generation Communication Devices Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 20% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Technology

- 5.1.1. 5G

- 5.1.2. Visible Light Communication / Li-Fi

- 5.1.3. Wireless Sensor Networks (WSN)

- 5.1.4. Other Technologies

- 5.2. Market Analysis, Insights and Forecast - by End User Industry

- 5.2.1. Manufacturing

- 5.2.2. Military and Defense

- 5.2.3. Automotive

- 5.2.4. Other End Users Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Asia Pacific

- 5.3.3. Europe

- 5.3.4. Rest of the world

- 5.1. Market Analysis, Insights and Forecast - by Technology

- 6. Global Next-generation Communication Devices Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Technology

- 6.1.1. 5G

- 6.1.2. Visible Light Communication / Li-Fi

- 6.1.3. Wireless Sensor Networks (WSN)

- 6.1.4. Other Technologies

- 6.2. Market Analysis, Insights and Forecast - by End User Industry

- 6.2.1. Manufacturing

- 6.2.2. Military and Defense

- 6.2.3. Automotive

- 6.2.4. Other End Users Industries

- 6.1. Market Analysis, Insights and Forecast - by Technology

- 7. North America Next-generation Communication Devices Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Technology

- 7.1.1. 5G

- 7.1.2. Visible Light Communication / Li-Fi

- 7.1.3. Wireless Sensor Networks (WSN)

- 7.1.4. Other Technologies

- 7.2. Market Analysis, Insights and Forecast - by End User Industry

- 7.2.1. Manufacturing

- 7.2.2. Military and Defense

- 7.2.3. Automotive

- 7.2.4. Other End Users Industries

- 7.1. Market Analysis, Insights and Forecast - by Technology

- 8. Asia Pacific Next-generation Communication Devices Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Technology

- 8.1.1. 5G

- 8.1.2. Visible Light Communication / Li-Fi

- 8.1.3. Wireless Sensor Networks (WSN)

- 8.1.4. Other Technologies

- 8.2. Market Analysis, Insights and Forecast - by End User Industry

- 8.2.1. Manufacturing

- 8.2.2. Military and Defense

- 8.2.3. Automotive

- 8.2.4. Other End Users Industries

- 8.1. Market Analysis, Insights and Forecast - by Technology

- 9. Europe Next-generation Communication Devices Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Technology

- 9.1.1. 5G

- 9.1.2. Visible Light Communication / Li-Fi

- 9.1.3. Wireless Sensor Networks (WSN)

- 9.1.4. Other Technologies

- 9.2. Market Analysis, Insights and Forecast - by End User Industry

- 9.2.1. Manufacturing

- 9.2.2. Military and Defense

- 9.2.3. Automotive

- 9.2.4. Other End Users Industries

- 9.1. Market Analysis, Insights and Forecast - by Technology

- 10. Rest of the world Next-generation Communication Devices Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Technology

- 10.1.1. 5G

- 10.1.2. Visible Light Communication / Li-Fi

- 10.1.3. Wireless Sensor Networks (WSN)

- 10.1.4. Other Technologies

- 10.2. Market Analysis, Insights and Forecast - by End User Industry

- 10.2.1. Manufacturing

- 10.2.2. Military and Defense

- 10.2.3. Automotive

- 10.2.4. Other End Users Industries

- 10.1. Market Analysis, Insights and Forecast - by Technology

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Honeywell International Inc

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 Purelifi Ltd

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 Analong Devices Inc

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 Laser Light Global

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 Telefonaktiebolaget LM Ericsson

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 Cisco Systems Inc

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 Panasonic Corp

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Netgear Inc

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Koninklijke Philips NV

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.10 Huawei Technologies Co Ltd

- 11.1.10.1. Company Overview

- 11.1.10.2. Products

- 11.1.10.3. Company Financials

- 11.1.10.4. SWOT Analysis

- 11.1.11 Qualcomm Technologies Inc*List Not Exhaustive

- 11.1.11.1. Company Overview

- 11.1.11.2. Products

- 11.1.11.3. Company Financials

- 11.1.11.4. SWOT Analysis

- 11.1.12 Northrop Grumman Corporation

- 11.1.12.1. Company Overview

- 11.1.12.2. Products

- 11.1.12.3. Company Financials

- 11.1.12.4. SWOT Analysis

- 11.1.1 Honeywell International Inc

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Global Next-generation Communication Devices Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Next-generation Communication Devices Industry Revenue (billion), by Technology 2025 & 2033

- Figure 3: North America Next-generation Communication Devices Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 4: North America Next-generation Communication Devices Industry Revenue (billion), by End User Industry 2025 & 2033

- Figure 5: North America Next-generation Communication Devices Industry Revenue Share (%), by End User Industry 2025 & 2033

- Figure 6: North America Next-generation Communication Devices Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Next-generation Communication Devices Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: Asia Pacific Next-generation Communication Devices Industry Revenue (billion), by Technology 2025 & 2033

- Figure 9: Asia Pacific Next-generation Communication Devices Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 10: Asia Pacific Next-generation Communication Devices Industry Revenue (billion), by End User Industry 2025 & 2033

- Figure 11: Asia Pacific Next-generation Communication Devices Industry Revenue Share (%), by End User Industry 2025 & 2033

- Figure 12: Asia Pacific Next-generation Communication Devices Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: Asia Pacific Next-generation Communication Devices Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Next-generation Communication Devices Industry Revenue (billion), by Technology 2025 & 2033

- Figure 15: Europe Next-generation Communication Devices Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 16: Europe Next-generation Communication Devices Industry Revenue (billion), by End User Industry 2025 & 2033

- Figure 17: Europe Next-generation Communication Devices Industry Revenue Share (%), by End User Industry 2025 & 2033

- Figure 18: Europe Next-generation Communication Devices Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Next-generation Communication Devices Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Rest of the world Next-generation Communication Devices Industry Revenue (billion), by Technology 2025 & 2033

- Figure 21: Rest of the world Next-generation Communication Devices Industry Revenue Share (%), by Technology 2025 & 2033

- Figure 22: Rest of the world Next-generation Communication Devices Industry Revenue (billion), by End User Industry 2025 & 2033

- Figure 23: Rest of the world Next-generation Communication Devices Industry Revenue Share (%), by End User Industry 2025 & 2033

- Figure 24: Rest of the world Next-generation Communication Devices Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Rest of the world Next-generation Communication Devices Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Next-generation Communication Devices Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 2: Global Next-generation Communication Devices Industry Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 3: Global Next-generation Communication Devices Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Next-generation Communication Devices Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 5: Global Next-generation Communication Devices Industry Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 6: Global Next-generation Communication Devices Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: Global Next-generation Communication Devices Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 8: Global Next-generation Communication Devices Industry Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 9: Global Next-generation Communication Devices Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 10: Global Next-generation Communication Devices Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 11: Global Next-generation Communication Devices Industry Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 12: Global Next-generation Communication Devices Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Global Next-generation Communication Devices Industry Revenue billion Forecast, by Technology 2020 & 2033

- Table 14: Global Next-generation Communication Devices Industry Revenue billion Forecast, by End User Industry 2020 & 2033

- Table 15: Global Next-generation Communication Devices Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Next-generation Communication Devices Industry?

The projected CAGR is approximately 20%.

2. Which companies are prominent players in the Next-generation Communication Devices Industry?

Key companies in the market include Honeywell International Inc, Purelifi Ltd, Analong Devices Inc, Laser Light Global, Telefonaktiebolaget LM Ericsson, Cisco Systems Inc, Panasonic Corp, Netgear Inc, Koninklijke Philips NV, Huawei Technologies Co Ltd, Qualcomm Technologies Inc*List Not Exhaustive, Northrop Grumman Corporation.

3. What are the main segments of the Next-generation Communication Devices Industry?

The market segments include Technology, End User Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 21.7 billion as of 2022.

5. What are some drivers contributing to market growth?

; Rising Demand for High-speed Network; Growing Machine-to-Machine/IoT Connections.

6. What are the notable trends driving market growth?

5G Technology is Expected to Hold a Significant Share.

7. Are there any restraints impacting market growth?

; High Infrastructural and Development Cost.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Next-generation Communication Devices Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Next-generation Communication Devices Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Next-generation Communication Devices Industry?

To stay informed about further developments, trends, and reports in the Next-generation Communication Devices Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence