Key Insights

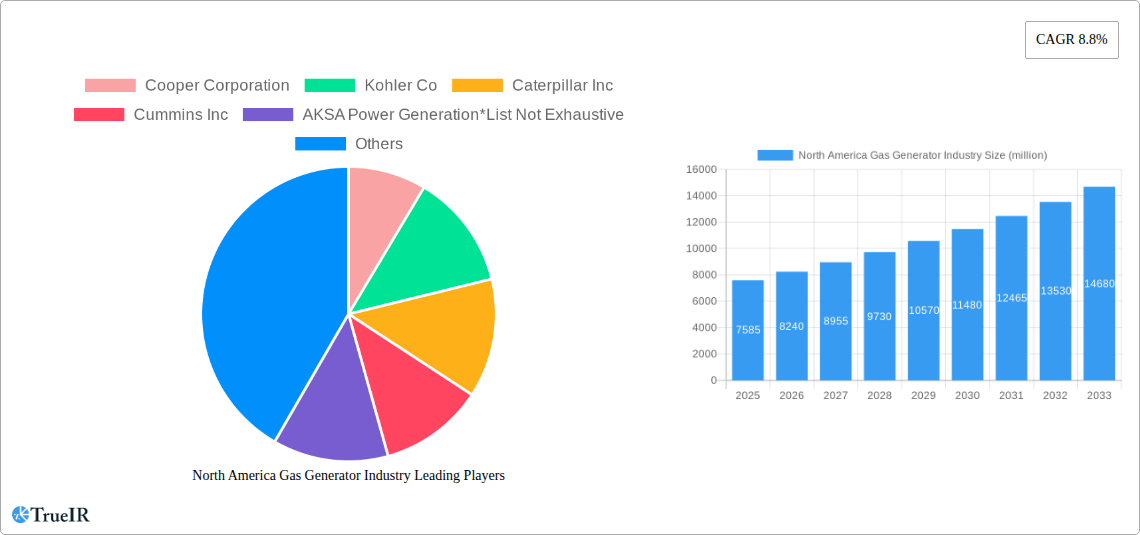

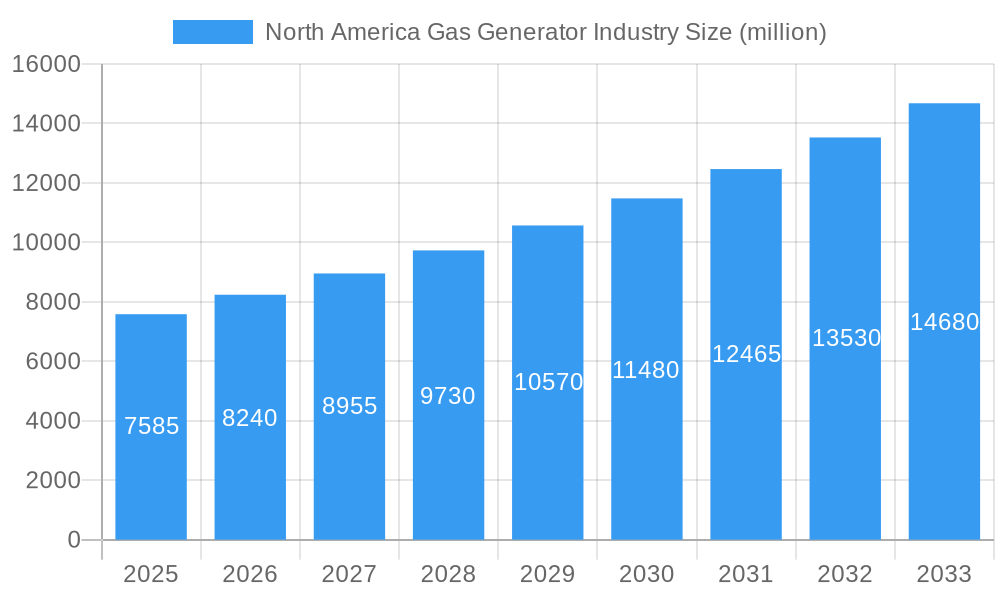

The North America Gas Generator Market is poised for significant expansion, projected to reach a market size of $7,585 million in 2025, with an impressive CAGR of 8.8% during the forecast period of 2025-2033. This robust growth is primarily fueled by increasing industrialization and commercial development across the region, necessitating reliable and efficient power backup solutions. The growing demand for continuous power supply in critical sectors such as manufacturing, healthcare, and data centers, coupled with the inherent benefits of natural gas generators – including lower emissions compared to diesel alternatives and cost-effectiveness in regions with accessible natural gas infrastructure – are key market drivers. Furthermore, the escalating frequency of extreme weather events, leading to power outages, is also a significant catalyst for the adoption of gas generators, especially for residential backup power.

North America Gas Generator Industry Market Size (In Billion)

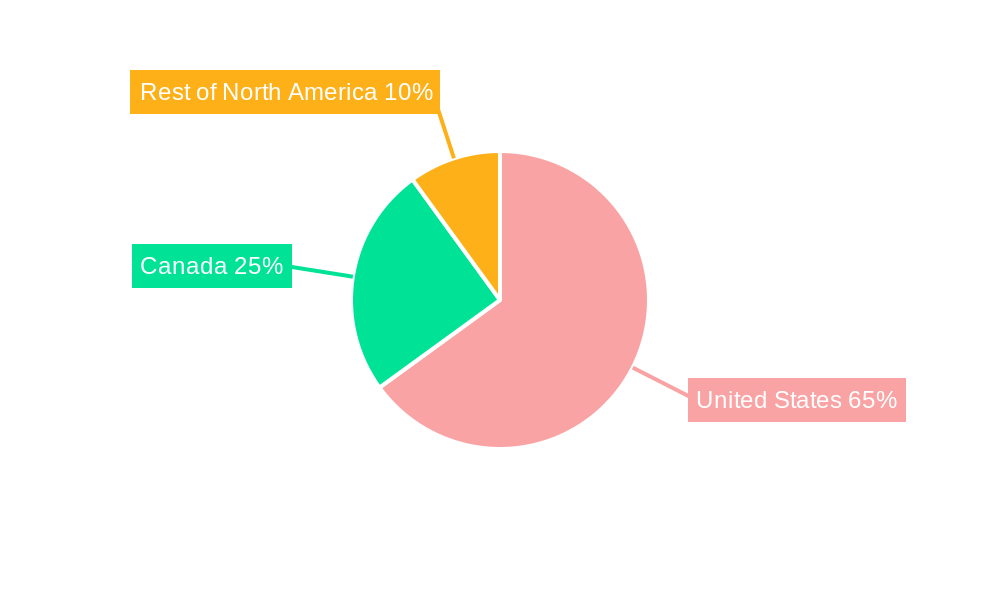

The market segmentation reveals a dynamic landscape, with the 75-375 kVA capacity segment likely to witness substantial demand due to its versatility for a wide range of industrial and commercial applications. Geographically, the United States will continue to dominate the market, driven by its advanced industrial base and extensive natural gas network. Canada and the Rest of North America are also expected to contribute significantly to the market's growth, as these regions increasingly invest in infrastructure development and seek stable power solutions. While the market benefits from strong demand drivers, potential restraints such as the initial high cost of installation for some advanced models and the fluctuating prices of natural gas could influence the pace of growth. However, ongoing technological advancements, focusing on improved efficiency and reduced emissions, are expected to mitigate these challenges and further propel the market forward.

North America Gas Generator Industry Company Market Share

This in-depth report provides a dynamic and SEO-optimized analysis of the North America Gas Generator Industry. Leveraging high-volume keywords such as "gas generator market," "natural gas generator," "power generation solutions," and "backup power," this report offers unparalleled insights into market structure, trends, opportunities, and competitive landscapes. Designed for industry professionals, investors, and stakeholders, this report delivers actionable intelligence for strategic decision-making. The study period spans from 2019 to 2033, with a base year of 2025 and a forecast period of 2025–2033, building upon a detailed historical analysis from 2019–2024.

North America Gas Generator Industry Market Structure & Competitive Landscape

The North America Gas Generator Industry is characterized by a moderate to high market concentration, with a few key players dominating significant market share. The innovation drivers are primarily focused on increasing efficiency, reducing emissions, and enhancing reliability for critical applications. Regulatory impacts are significant, with evolving EPA standards and state-specific mandates influencing technology adoption and product development. Product substitutes, including diesel generators and renewable energy storage solutions, present a competitive challenge, though natural gas generators offer distinct advantages in terms of fuel availability and cost-effectiveness in many regions.

End-user segmentation is robust, with the industrial and commercial sectors being major consumers, driven by the need for uninterrupted power supply. The residential segment, while smaller, is experiencing growth due to increasing awareness of backup power needs and the availability of more compact and efficient units.

Mergers and acquisitions (M&A) trends indicate a consolidation phase, with larger players acquiring smaller innovators to expand their product portfolios and market reach. The industry has witnessed an average of 2-3 significant M&A deals annually over the historical period, primarily driven by technological synergy and market penetration goals. Key companies actively shaping this landscape include Caterpillar Inc., Cummins Inc., Generac Holdings Inc., and Kohler Co., alongside specialized players like Cooper Corporation and AKSA Power Generation.

North America Gas Generator Industry Market Trends & Opportunities

The North America Gas Generator Industry is poised for significant growth, projected to expand from an estimated market size of approximately $20,000 million in the base year 2025 to an impressive $35,000 million by 2033. This translates to a Compound Annual Growth Rate (CAGR) of approximately 6.8% during the forecast period (2025–2033). This robust expansion is fueled by a confluence of factors, including the increasing demand for reliable backup power solutions across various sectors, particularly in the face of aging grid infrastructure and the growing frequency of extreme weather events. The shift towards natural gas as a cleaner and more readily available fuel source compared to diesel also plays a crucial role in driving market penetration.

Technological shifts are at the forefront of this growth. Manufacturers are investing heavily in developing advanced generator sets that offer enhanced fuel efficiency, lower emissions, and superior transient response capabilities. This includes the integration of smart technologies for remote monitoring, predictive maintenance, and seamless integration with existing power systems. The development of smaller, more compact, and quieter gas generators is also opening up new avenues in the residential and small commercial segments.

Consumer preferences are increasingly leaning towards solutions that offer not only reliability but also environmental responsibility. Natural gas generators, with their comparatively lower carbon footprint than diesel alternatives, are well-positioned to meet these evolving demands. Furthermore, the desire for energy independence and resilience against grid disruptions is a significant driver for both industrial and residential consumers.

The competitive dynamics are intensifying, with established players like Caterpillar Inc., Cummins Inc., and Generac Holdings Inc. facing competition from both global giants and specialized regional manufacturers such as Kohler Co., Cooper Corporation, and AKSA Power Generation. Innovation, pricing strategies, and robust after-sales service are becoming critical differentiators. The market penetration rate for gas generators, particularly in the industrial and commercial sectors, is expected to climb steadily, exceeding 70% by 2033 in key markets. Opportunities abound for companies that can offer tailored solutions, advanced technological integration, and competitive pricing.

Dominant Markets & Segments in North America Gas Generator Industry

The United States stands as the dominant market within the North America Gas Generator Industry, accounting for an estimated 75% of the total market revenue in the base year 2025. This dominance is driven by a robust industrial and commercial base, significant investments in infrastructure development, and a pronounced need for reliable backup power solutions. Canada represents the second-largest market, contributing approximately 20%, with increasing adoption in commercial and residential sectors. The Rest of North America, though smaller, presents nascent growth opportunities, particularly in Mexico, driven by industrial expansion.

Capacity: The Above 375 kVA segment is the largest contributor to market revenue, reflecting the substantial power requirements of industrial facilities, data centers, and large commercial complexes. This segment is expected to grow at a CAGR of approximately 7.2%. The 75-375 kVA segment follows closely, serving mid-sized commercial operations, healthcare facilities, and small industrial units, with a projected CAGR of 6.5%. The Less than 75 kVA segment, catering primarily to the residential market and small businesses, is anticipated to experience the fastest growth, with a CAGR of around 7.5%, driven by increased awareness of home backup power needs and the availability of more affordable and user-friendly models.

End User: The Industrial end-user segment is the most significant, driven by the critical need for uninterrupted power in manufacturing plants, oil and gas operations, and other heavy industries where downtime is exceptionally costly. This segment is projected to grow at a CAGR of 6.9%. The Commercial segment, encompassing retail, hospitality, data centers, and healthcare, is the second-largest and is experiencing steady growth (CAGR of 6.7%) due to business continuity requirements and increasing reliance on technology. The Residential segment, while smaller in absolute terms, is showing strong growth potential (CAGR of 7.5%), fueled by rising consumer demand for home standby generators in response to power outages and grid instability.

Geography: The United States will continue to lead the market, with key growth drivers including aging power infrastructure, stringent reliability standards in critical industries, and federal incentives for energy efficiency. Canada's growth will be propelled by its expanding natural resources sector and a growing emphasis on disaster preparedness. The Rest of North America, particularly Mexico, presents emerging opportunities driven by industrialization and foreign direct investment.

North America Gas Generator Industry Product Analysis

Product innovation in the North America Gas Generator Industry is sharply focused on enhancing efficiency, reducing emissions, and improving the transient response of natural gas generator sets. Manufacturers are developing advanced models with integrated smart technologies for remote diagnostics, predictive maintenance, and seamless grid synchronization. Key applications span critical infrastructure, data centers, industrial manufacturing, and residential backup power. The competitive advantage lies in offering reliable, cost-effective, and environmentally compliant solutions, with companies like Caterpillar Inc. and Cummins Inc. leading in technological advancements and product reliability.

Key Drivers, Barriers & Challenges in North America Gas Generator Industry

Key Drivers:

- Increasing demand for reliable backup power: Driven by grid instability, aging infrastructure, and extreme weather events.

- Natural gas availability and cost-effectiveness: Promotes adoption over other fuel sources.

- Technological advancements: Enhanced efficiency, lower emissions, and smart integration capabilities.

- Stringent emission regulations: Favoring cleaner natural gas options over diesel.

- Growth in data centers and critical infrastructure: Requiring continuous and dependable power.

Barriers & Challenges:

- Initial capital investment: Can be a significant barrier for smaller businesses and residential users.

- Natural gas infrastructure limitations: In some remote areas, accessibility to natural gas lines can be an issue.

- Competition from alternative energy sources: Including battery storage and renewable energy.

- Skilled labor shortage: For installation, maintenance, and repair of advanced generator systems.

- Supply chain disruptions: Affecting the availability of components and lead times.

Growth Drivers in the North America Gas Generator Industry Market

The North America Gas Generator Industry is propelled by several key growth drivers. Technological advancements in engine design and control systems are leading to more fuel-efficient and lower-emission units, making them attractive to environmentally conscious consumers and businesses. Economic factors, such as the declining cost of natural gas relative to other fossil fuels and increased industrial output, are creating a favorable environment for gas generator adoption. Furthermore, regulatory mandates promoting cleaner energy solutions and requiring backup power for critical facilities are acting as significant catalysts. For instance, the increasing focus on grid resilience post-major power outages is a substantial driver.

Challenges Impacting North America Gas Generator Industry Growth

Several challenges are impacting the growth of the North America Gas Generator Industry. Regulatory complexities, including varying emission standards and permitting processes across different jurisdictions, can create hurdles for manufacturers and end-users. Supply chain issues, such as component shortages and increased lead times for critical parts, can disrupt production and project timelines, impacting overall market responsiveness. Competitive pressures from established players and emerging technologies, including advanced battery energy storage systems, necessitate continuous innovation and competitive pricing strategies. The high upfront cost of some advanced gas generator systems can also be a restraint for market penetration, especially in price-sensitive segments.

Key Players Shaping the North America Gas Generator Industry Market

- Cooper Corporation

- Kohler Co

- Caterpillar Inc

- Cummins Inc

- AKSA Power Generation

- MTU America Inc

- General Electric Company

- Honda Power Equipment Mfg Inc

- Generac Holdings Inc

Significant North America Gas Generator Industry Industry Milestones

- Jan 2022: Caterpillar Inc. unveiled the Cat G3516 Fast Reaction generator set, adding a 1.5 MW power node to its array of natural-gas power solutions, emphasizing market-leading load acceptance, transient response, and EPA certification for mission-critical applications.

- Dec 2021: HIPOWER SYSTEMS, HIMOINSA's new North American production hub, began operations in its new 515,000-square-foot factory in Olathe, Kansas, equipped with cutting-edge technology for generator set production for the North American market.

Future Outlook for North America Gas Generator Industry Market

The future outlook for the North America Gas Generator Industry is highly promising, driven by sustained demand for reliable and cleaner power solutions. Continued investment in technological innovation, particularly in areas of enhanced fuel efficiency, emission reduction, and smart grid integration, will be a key growth catalyst. The expansion of natural gas infrastructure and supportive government policies aimed at energy resilience and environmental sustainability will further bolster market growth. Strategic opportunities lie in catering to the evolving needs of the industrial, commercial, and residential sectors, with a particular focus on providing customized, integrated, and sustainable power generation solutions. The market is expected to witness significant growth in the adoption of advanced natural gas generator technologies over the next decade.

North America Gas Generator Industry Segmentation

-

1. Capacity

- 1.1. Less than 75 kVA

- 1.2. 75-375 kVA

- 1.3. Above 375 kVA

-

2. End User

- 2.1. Industrial

- 2.2. Commercial

- 2.3. Residential

-

3. Geography

- 3.1. United States

- 3.2. Canada

- 3.3. Rest of North America

North America Gas Generator Industry Segmentation By Geography

- 1. United States

- 2. Canada

- 3. Rest of North America

North America Gas Generator Industry Regional Market Share

Geographic Coverage of North America Gas Generator Industry

North America Gas Generator Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Capacity

- 5.1.1. Less than 75 kVA

- 5.1.2. 75-375 kVA

- 5.1.3. Above 375 kVA

- 5.2. Market Analysis, Insights and Forecast - by End User

- 5.2.1. Industrial

- 5.2.2. Commercial

- 5.2.3. Residential

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. United States

- 5.3.2. Canada

- 5.3.3. Rest of North America

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. United States

- 5.4.2. Canada

- 5.4.3. Rest of North America

- 5.1. Market Analysis, Insights and Forecast - by Capacity

- 6. North America Gas Generator Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Capacity

- 6.1.1. Less than 75 kVA

- 6.1.2. 75-375 kVA

- 6.1.3. Above 375 kVA

- 6.2. Market Analysis, Insights and Forecast - by End User

- 6.2.1. Industrial

- 6.2.2. Commercial

- 6.2.3. Residential

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. United States

- 6.3.2. Canada

- 6.3.3. Rest of North America

- 6.1. Market Analysis, Insights and Forecast - by Capacity

- 7. United States North America Gas Generator Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Capacity

- 7.1.1. Less than 75 kVA

- 7.1.2. 75-375 kVA

- 7.1.3. Above 375 kVA

- 7.2. Market Analysis, Insights and Forecast - by End User

- 7.2.1. Industrial

- 7.2.2. Commercial

- 7.2.3. Residential

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. United States

- 7.3.2. Canada

- 7.3.3. Rest of North America

- 7.1. Market Analysis, Insights and Forecast - by Capacity

- 8. Canada North America Gas Generator Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Capacity

- 8.1.1. Less than 75 kVA

- 8.1.2. 75-375 kVA

- 8.1.3. Above 375 kVA

- 8.2. Market Analysis, Insights and Forecast - by End User

- 8.2.1. Industrial

- 8.2.2. Commercial

- 8.2.3. Residential

- 8.3. Market Analysis, Insights and Forecast - by Geography

- 8.3.1. United States

- 8.3.2. Canada

- 8.3.3. Rest of North America

- 8.1. Market Analysis, Insights and Forecast - by Capacity

- 9. Rest of North America North America Gas Generator Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Capacity

- 9.1.1. Less than 75 kVA

- 9.1.2. 75-375 kVA

- 9.1.3. Above 375 kVA

- 9.2. Market Analysis, Insights and Forecast - by End User

- 9.2.1. Industrial

- 9.2.2. Commercial

- 9.2.3. Residential

- 9.3. Market Analysis, Insights and Forecast - by Geography

- 9.3.1. United States

- 9.3.2. Canada

- 9.3.3. Rest of North America

- 9.1. Market Analysis, Insights and Forecast - by Capacity

- 10. Competitive Analysis

- 10.1. Company Profiles

- 10.1.1 Cooper Corporation

- 10.1.1.1. Company Overview

- 10.1.1.2. Products

- 10.1.1.3. Company Financials

- 10.1.1.4. SWOT Analysis

- 10.1.2 Kohler Co

- 10.1.2.1. Company Overview

- 10.1.2.2. Products

- 10.1.2.3. Company Financials

- 10.1.2.4. SWOT Analysis

- 10.1.3 Caterpillar Inc

- 10.1.3.1. Company Overview

- 10.1.3.2. Products

- 10.1.3.3. Company Financials

- 10.1.3.4. SWOT Analysis

- 10.1.4 Cummins Inc

- 10.1.4.1. Company Overview

- 10.1.4.2. Products

- 10.1.4.3. Company Financials

- 10.1.4.4. SWOT Analysis

- 10.1.5 AKSA Power Generation*List Not Exhaustive

- 10.1.5.1. Company Overview

- 10.1.5.2. Products

- 10.1.5.3. Company Financials

- 10.1.5.4. SWOT Analysis

- 10.1.6 MTU America Inc

- 10.1.6.1. Company Overview

- 10.1.6.2. Products

- 10.1.6.3. Company Financials

- 10.1.6.4. SWOT Analysis

- 10.1.7 General Electric Company

- 10.1.7.1. Company Overview

- 10.1.7.2. Products

- 10.1.7.3. Company Financials

- 10.1.7.4. SWOT Analysis

- 10.1.8 Honda Power Equipment Mfg Inc

- 10.1.8.1. Company Overview

- 10.1.8.2. Products

- 10.1.8.3. Company Financials

- 10.1.8.4. SWOT Analysis

- 10.1.9 Generac Holdings Inc

- 10.1.9.1. Company Overview

- 10.1.9.2. Products

- 10.1.9.3. Company Financials

- 10.1.9.4. SWOT Analysis

- 10.1.1 Cooper Corporation

- 10.2. Market Entropy

- 10.2.1 Company's Key Areas Served

- 10.2.2 Recent Developments

- 10.3. Company Market Share Analysis 2025

- 10.3.1 Top 5 Companies Market Share Analysis

- 10.3.2 Top 3 Companies Market Share Analysis

- 10.4. List of Potential Customers

- 11. Research Methodology

List of Figures

- Figure 1: North America Gas Generator Industry Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: North America Gas Generator Industry Share (%) by Company 2025

List of Tables

- Table 1: North America Gas Generator Industry Revenue million Forecast, by Capacity 2020 & 2033

- Table 2: North America Gas Generator Industry Volume K Unit Forecast, by Capacity 2020 & 2033

- Table 3: North America Gas Generator Industry Revenue million Forecast, by End User 2020 & 2033

- Table 4: North America Gas Generator Industry Volume K Unit Forecast, by End User 2020 & 2033

- Table 5: North America Gas Generator Industry Revenue million Forecast, by Geography 2020 & 2033

- Table 6: North America Gas Generator Industry Volume K Unit Forecast, by Geography 2020 & 2033

- Table 7: North America Gas Generator Industry Revenue million Forecast, by Region 2020 & 2033

- Table 8: North America Gas Generator Industry Volume K Unit Forecast, by Region 2020 & 2033

- Table 9: North America Gas Generator Industry Revenue million Forecast, by Capacity 2020 & 2033

- Table 10: North America Gas Generator Industry Volume K Unit Forecast, by Capacity 2020 & 2033

- Table 11: North America Gas Generator Industry Revenue million Forecast, by End User 2020 & 2033

- Table 12: North America Gas Generator Industry Volume K Unit Forecast, by End User 2020 & 2033

- Table 13: North America Gas Generator Industry Revenue million Forecast, by Geography 2020 & 2033

- Table 14: North America Gas Generator Industry Volume K Unit Forecast, by Geography 2020 & 2033

- Table 15: North America Gas Generator Industry Revenue million Forecast, by Country 2020 & 2033

- Table 16: North America Gas Generator Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 17: North America Gas Generator Industry Revenue million Forecast, by Capacity 2020 & 2033

- Table 18: North America Gas Generator Industry Volume K Unit Forecast, by Capacity 2020 & 2033

- Table 19: North America Gas Generator Industry Revenue million Forecast, by End User 2020 & 2033

- Table 20: North America Gas Generator Industry Volume K Unit Forecast, by End User 2020 & 2033

- Table 21: North America Gas Generator Industry Revenue million Forecast, by Geography 2020 & 2033

- Table 22: North America Gas Generator Industry Volume K Unit Forecast, by Geography 2020 & 2033

- Table 23: North America Gas Generator Industry Revenue million Forecast, by Country 2020 & 2033

- Table 24: North America Gas Generator Industry Volume K Unit Forecast, by Country 2020 & 2033

- Table 25: North America Gas Generator Industry Revenue million Forecast, by Capacity 2020 & 2033

- Table 26: North America Gas Generator Industry Volume K Unit Forecast, by Capacity 2020 & 2033

- Table 27: North America Gas Generator Industry Revenue million Forecast, by End User 2020 & 2033

- Table 28: North America Gas Generator Industry Volume K Unit Forecast, by End User 2020 & 2033

- Table 29: North America Gas Generator Industry Revenue million Forecast, by Geography 2020 & 2033

- Table 30: North America Gas Generator Industry Volume K Unit Forecast, by Geography 2020 & 2033

- Table 31: North America Gas Generator Industry Revenue million Forecast, by Country 2020 & 2033

- Table 32: North America Gas Generator Industry Volume K Unit Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Gas Generator Industry?

The projected CAGR is approximately 8.8%.

2. Which companies are prominent players in the North America Gas Generator Industry?

Key companies in the market include Cooper Corporation, Kohler Co, Caterpillar Inc, Cummins Inc, AKSA Power Generation*List Not Exhaustive, MTU America Inc, General Electric Company, Honda Power Equipment Mfg Inc, Generac Holdings Inc.

3. What are the main segments of the North America Gas Generator Industry?

The market segments include Capacity, End User, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 7585 million as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing Supply and Consumption of Gas-based Systems in Various End-user Industry4.; Implementation of stricter emission regulations worldwide.

6. What are the notable trends driving market growth?

Below 75 kVA Capacity Gas Generator to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Growing Inclination towards Renewable Sources.

8. Can you provide examples of recent developments in the market?

Jan 2022: Caterpillar Inc. unveiled the Cat G3516 Fast Reaction generator set, which adds a 1.5 MW power node to its increasing array of natural-gas power solutions that deliver market-leading load acceptance, transient response, and EPA certification for mission-critical applications.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Gas Generator Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Gas Generator Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Gas Generator Industry?

To stay informed about further developments, trends, and reports in the North America Gas Generator Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence