Key Insights

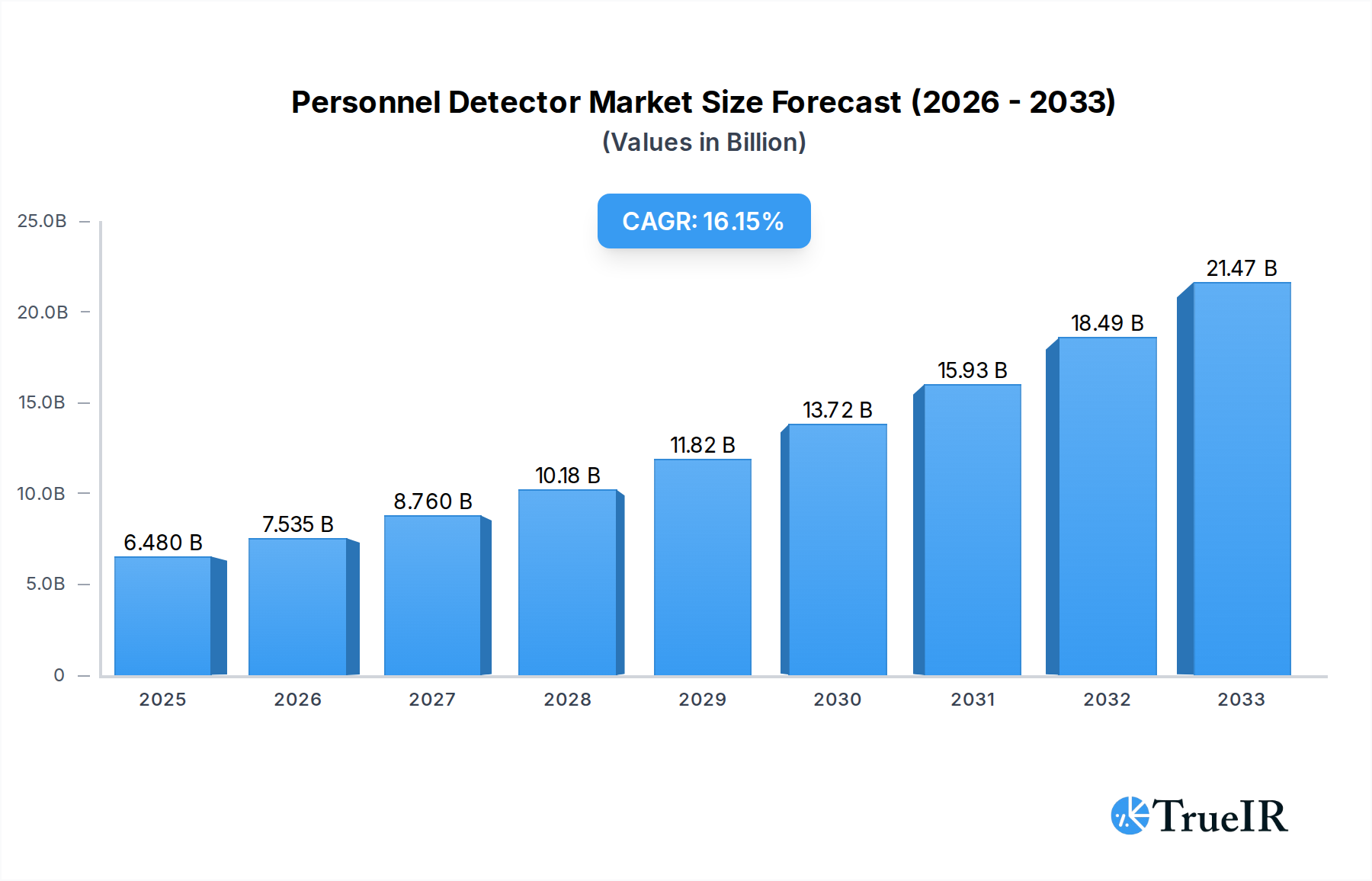

The global Personnel Detector market is poised for significant expansion, projected to reach an estimated USD 6.48 billion in 2025. This robust growth is fueled by an impressive CAGR of 16.13% from 2019 to 2033, indicating a dynamic and rapidly evolving industry. The increasing demand for enhanced safety and security across residential, commercial, and industrial sectors is a primary driver. Advancements in sensor technology, miniaturization, and the integration of AI and IoT are enabling more sophisticated and accurate personnel detection solutions. The proliferation of smart homes and smart buildings, coupled with stringent regulations mandating safety protocols, further propels market adoption. Furthermore, the growing awareness of energy efficiency, with personnel detectors contributing to automated lighting and HVAC control, adds another layer of impetus to market growth. The integration of wireless technologies is simplifying installation and reducing costs, making these systems more accessible to a wider range of applications.

Personnel Detector Market Size (In Billion)

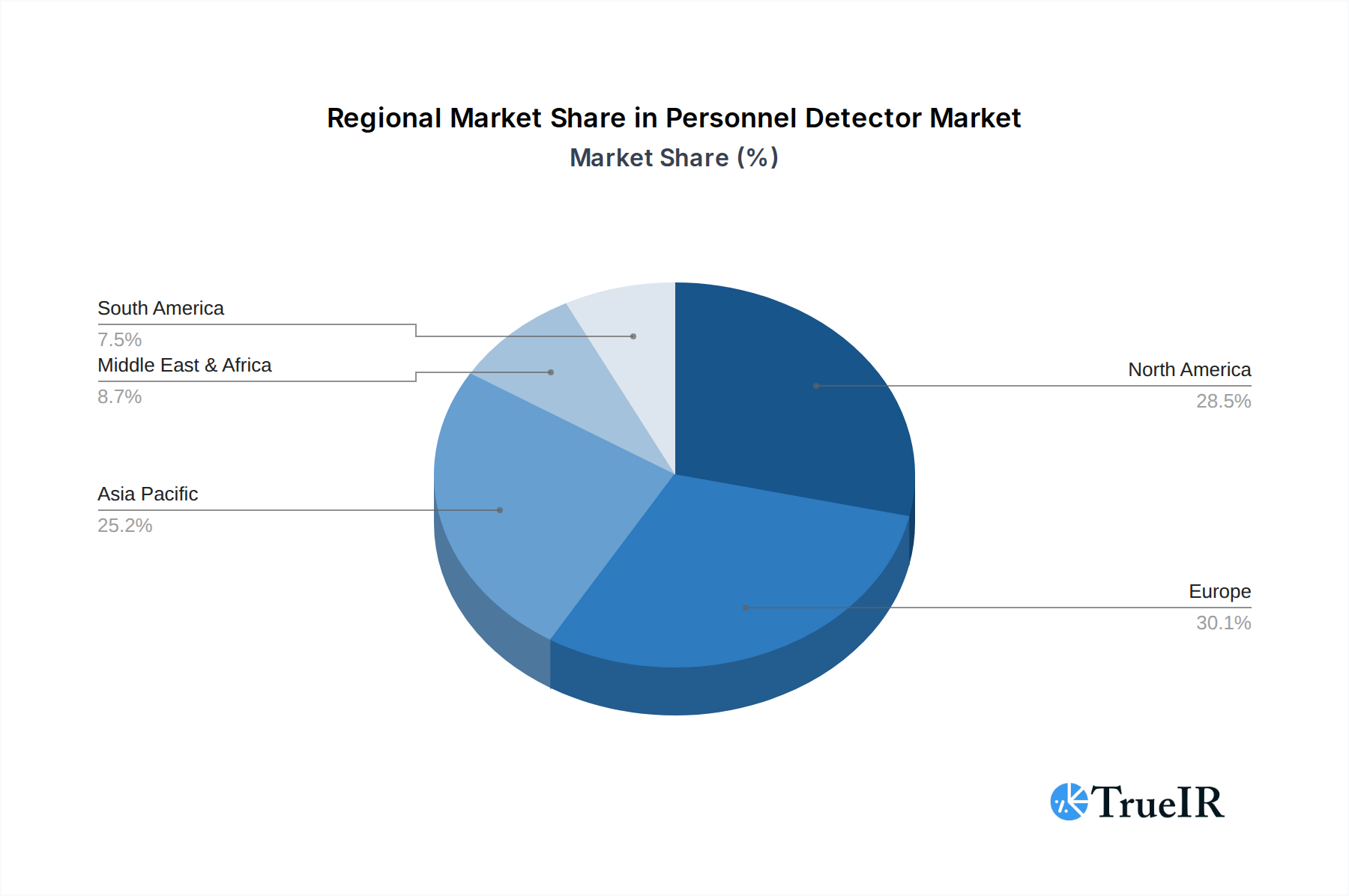

The market landscape is characterized by continuous innovation from key players such as Panasonic, Eaton, and Schneider Electric, who are investing heavily in research and development to introduce cutting-edge products. While the market enjoys strong growth, potential restraints include the initial cost of advanced systems in certain segments and concerns surrounding data privacy and cybersecurity. However, the overarching benefits of enhanced safety, operational efficiency, and energy savings are expected to outweigh these challenges. The market is segmented into wired and wireless types, with wireless solutions gaining traction due to their flexibility and ease of deployment. Geographically, the Asia Pacific region, driven by rapid urbanization and industrialization in countries like China and India, is expected to emerge as a significant growth hub, while North America and Europe will continue to represent mature and innovation-driven markets.

Personnel Detector Company Market Share

This in-depth report provides a dynamic, SEO-optimized analysis of the global Personnel Detector market, leveraging high-volume keywords to enhance search rankings and engage industry audiences. With a study period spanning from 2019 to 2033, a base year of 2025, and a forecast period from 2025 to 2033, this report offers unparalleled insights into market structure, trends, opportunities, dominant segments, product innovations, key drivers, challenges, and the competitive landscape.

Personnel Detector Market Structure & Competitive Landscape

The Personnel Detector market exhibits a moderately concentrated structure, with key players like Panasonic, Eaton, Schneider Electric, and Signify Holding dominating a significant portion of the global market share, estimated to be in the billions of dollars. Innovation drivers are primarily fueled by advancements in sensor technology, miniaturization, and integration with smart building systems, aiming to achieve enhanced accuracy and reduced false positives. Regulatory impacts are increasingly shaping market dynamics, with a growing emphasis on privacy concerns and data security protocols influencing product design and deployment strategies. Product substitutes, such as basic motion sensors and manual surveillance systems, exist but offer limited functionality compared to advanced personnel detectors. End-user segmentation reveals strong adoption in both residential and commercial applications, driven by the need for enhanced security and energy efficiency. The Industrial segment is also experiencing a notable surge due to stringent safety regulations and the demand for automated monitoring. Merger and acquisition (M&A) trends are anticipated to continue as larger players seek to consolidate market share and acquire innovative technologies, with an estimated volume of M&A activities reaching billions over the forecast period. Concentration ratios are expected to remain high among the top ten players, holding over 80% of the market value.

Personnel Detector Market Trends & Opportunities

The global Personnel Detector market is poised for substantial growth, projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 12.5% over the forecast period, reaching a market valuation in the tens of billions of dollars. This expansion is driven by a confluence of technological advancements, evolving consumer preferences, and an increasing demand for intelligent automation across various sectors. Technological shifts are characterized by the rapid development and adoption of AI-powered detection algorithms, advanced infrared sensors, and millimeter-wave radar technology, enabling more precise and sophisticated people counting, occupancy sensing, and presence detection. These innovations are significantly improving the accuracy and reliability of personnel detectors, reducing false alarms, and expanding their application scope. Consumer preferences are increasingly leaning towards smart home and smart building solutions that offer enhanced security, energy savings, and improved occupant comfort. Personnel detectors play a pivotal role in these ecosystems by enabling adaptive lighting, HVAC control, and access management, thereby contributing to a more efficient and responsive built environment. The market penetration rate for advanced personnel detectors in new construction is expected to reach over 60% by the end of the forecast period. Competitive dynamics are intensifying, with a growing emphasis on product differentiation through features such as enhanced privacy modes, seamless integration capabilities with IoT platforms, and specialized detection functionalities for specific environments. Strategic partnerships and collaborations between technology providers and system integrators are becoming crucial for expanding market reach and offering comprehensive solutions. The rise of the Internet of Things (IoT) ecosystem provides a fertile ground for growth, enabling personnel detectors to contribute to data-driven insights for building management and operational efficiency. Furthermore, the growing awareness and adoption of energy-saving initiatives are propelling the demand for occupancy-based control systems, where personnel detectors are indispensable. The market also presents significant opportunities in retrofitting existing buildings with advanced detection systems, particularly in commercial and industrial sectors aiming to upgrade their infrastructure for better safety and efficiency. The increasing focus on public safety and security in high-traffic areas further fuels the demand for robust and reliable personnel detection solutions. The evolution of AI and machine learning is enabling personnel detectors to not only detect presence but also to infer activity patterns, which can be invaluable for optimizing building operations and enhancing occupant experiences. The integration of personnel detectors with other smart building technologies, such as smart locks and alarm systems, is creating sophisticated security and automation solutions that are highly attractive to both residential and commercial clients. The market is also witnessing a trend towards wireless and easy-to-install solutions, catering to the growing DIY segment and simplifying deployment in diverse settings. The increasing prevalence of smart cities initiatives globally also provides a significant thrust for personnel detector adoption, as these devices are crucial for traffic management, public space monitoring, and resource optimization.

Dominant Markets & Segments in Personnel Detector

The Personnel Detector market is experiencing robust growth across its primary segments, with the Commercial application sector currently holding the largest market share, projected to contribute over 50% of the global market revenue, estimated in the tens of billions of dollars. This dominance is propelled by the escalating need for enhanced security, energy efficiency, and space utilization in office buildings, retail establishments, and hospitality venues. Key growth drivers within the commercial segment include stringent building codes mandating energy-efficient technologies, a rising demand for smart building solutions that optimize operational costs, and the imperative for advanced security systems to protect assets and personnel. The integration of personnel detectors with Building Management Systems (BMS) is a significant trend, enabling automated control of lighting, HVAC, and access systems based on real-time occupancy data, leading to substantial energy savings and improved occupant comfort. The Industrial application segment is also witnessing considerable expansion, driven by the implementation of stricter workplace safety regulations and the growing adoption of automation in manufacturing and logistics. Personnel detectors are crucial for monitoring hazardous zones, ensuring compliance with safety protocols, and optimizing workforce management. The Industrial sector's growth is further fueled by the demand for process optimization and predictive maintenance, where occupancy data can provide valuable insights. In the Residential segment, adoption is on an upward trajectory, fueled by the increasing consumer interest in smart home technologies, enhanced security, and energy-saving features. The availability of user-friendly, wireless personnel detectors is making them more accessible to homeowners. Regarding types, the Wireless segment is outpacing its Wired counterpart, expected to capture over 70% of the market share. Key growth drivers for wireless detectors include ease of installation, flexibility in deployment, and lower infrastructure costs. This is particularly advantageous for retrofitting existing buildings and for applications where wiring is impractical or cost-prohibitive. Wireless technologies like Wi-Fi, Bluetooth, and Zigbee are enabling seamless integration with smart home hubs and other IoT devices. However, the Wired segment continues to hold its ground in large-scale commercial and industrial installations where robust connectivity and higher bandwidth are critical. Key growth drivers for wired detectors include their reliability, security, and suitability for applications requiring continuous, high-integrity data transmission. Countries like the United States, China, and Germany are leading the market in terms of adoption, driven by strong economic growth, technological advancements, and supportive government initiatives. The Asia-Pacific region, in particular, is projected to witness the fastest growth due to rapid urbanization, increasing disposable incomes, and a burgeoning smart building sector. Infrastructure development and government policies promoting energy efficiency and smart city initiatives are creating a favorable environment for personnel detector adoption across all segments and regions.

Personnel Detector Product Analysis

Personnel detector product innovations are focused on enhancing accuracy, miniaturization, and seamless integration with smart ecosystems. Advanced AI-powered algorithms are enabling sophisticated presence detection, occupancy counting, and even activity pattern recognition, moving beyond simple motion sensing. Integration with IoT platforms and other smart building technologies allows for automated control of lighting, HVAC, and security systems, offering significant energy savings and improved occupant experiences. Competitive advantages lie in products offering superior detection accuracy, enhanced privacy features, ease of installation, and robust connectivity options.

Key Drivers, Barriers & Challenges in Personnel Detector

Key Drivers:

- Technological Advancements: Innovations in sensor technology (e.g., mmWave, AI-powered analytics) are enhancing accuracy and functionality.

- Energy Efficiency Mandates: Growing demand for smart building solutions to reduce energy consumption.

- Enhanced Security Needs: Increasing adoption for improved safety and surveillance in residential, commercial, and industrial settings.

- IoT Integration: The proliferation of connected devices fuels demand for intelligent sensors within smart ecosystems.

Barriers & Challenges:

- Privacy Concerns: Public apprehension regarding surveillance and data privacy can hinder widespread adoption.

- Installation Costs: While decreasing, the initial investment for advanced systems can be a barrier for some segments.

- Regulatory Complexities: Evolving regulations concerning data handling and privacy can create compliance challenges.

- Supply Chain Disruptions: Global component shortages and logistics issues can impact product availability and pricing.

Growth Drivers in the Personnel Detector Market

The growth drivers in the Personnel Detector market are multifaceted, propelled by technological innovation and evolving market demands. The increasing integration of Artificial Intelligence (AI) and Machine Learning (ML) into personnel detection systems is a significant catalyst, enabling more sophisticated analytics, improved accuracy, and enhanced privacy features. Government initiatives promoting energy efficiency and smart building technologies are creating substantial demand for occupancy sensing solutions, where personnel detectors play a crucial role in optimizing energy consumption for lighting and HVAC systems, leading to billions in potential energy savings. The burgeoning smart home and smart building market, driven by consumer desire for convenience, security, and automation, is a primary growth engine. Furthermore, the growing emphasis on workplace safety and security in commercial and industrial environments, coupled with the need for accurate people counting for space management and compliance, is driving adoption.

Challenges Impacting Personnel Detector Growth

Challenges impacting Personnel Detector growth are primarily centered around privacy concerns and the complexities of integration and adoption. Public apprehension regarding constant surveillance and the potential misuse of personal data can create a significant hurdle for widespread market penetration. While improving, the initial installation costs for advanced, interconnected systems can still be a deterrent for some segments of the market, particularly for smaller businesses or individual homeowners. Navigating the evolving regulatory landscape, especially concerning data privacy laws and their impact on sensor deployment and data handling, presents ongoing challenges for manufacturers and integrators. Furthermore, ensuring interoperability and seamless integration with a diverse range of existing building management systems and other smart devices can be complex, requiring significant development effort and standardization. Supply chain volatility and potential component shortages can also impact the availability and cost of personnel detector devices, posing a risk to consistent market growth.

Key Players Shaping the Personnel Detector Market

- Panasonic

- Eaton

- Schneider Electric

- Top Greener

- Sensio Lighting

- HPM (Legrand)

- Walnut Innovation

- Lutron Electronics

- Leviton Manufacturing

- GE Lighting (Savant)

- Sunricher

- ELEGRP

- RS Components & Controls

- Ecoamica Tech

- DS Electronics

- Sensinova

- Signify Holding

Significant Personnel Detector Industry Milestones

- 2019: Introduction of advanced AI-powered analytics for enhanced occupancy sensing.

- 2020: Increased adoption of wireless personnel detectors for easier smart home integration.

- 2021: Development of privacy-focused detection technologies addressing user concerns.

- 2022: Milestones in miniaturization, allowing for discreet integration into various fixtures.

- 2023: Enhanced interoperability with major smart home platforms and BMS.

- 2024: Emergence of millimeter-wave radar technology for highly accurate, non-intrusive detection.

Future Outlook for Personnel Detector Market

The future outlook for the Personnel Detector market is exceptionally bright, driven by continued technological innovation and expanding application horizons. Anticipate a surge in demand for AI-driven, privacy-enhanced solutions that offer granular insights into building occupancy and behavior. The integration of personnel detectors with the broader IoT ecosystem will deepen, enabling more intelligent and responsive smart buildings, contributing to billions in energy savings and operational efficiencies. Opportunities lie in specialized detectors for healthcare, retail analytics, and public safety applications, further diversifying the market. The ongoing trend towards wireless and easily deployable devices will accelerate adoption across residential and commercial sectors. Strategic collaborations and continuous product development will be key to navigating the evolving landscape and capitalizing on the significant market potential projected to reach tens of billions in valuation.

Personnel Detector Segmentation

-

1. Application

- 1.1. Residential

- 1.2. Commercial

- 1.3. Industrial

-

2. Types

- 2.1. Wired

- 2.2. Wireless

Personnel Detector Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Personnel Detector Regional Market Share

Geographic Coverage of Personnel Detector

Personnel Detector REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 16.13% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Personnel Detector Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Residential

- 5.1.2. Commercial

- 5.1.3. Industrial

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Wired

- 5.2.2. Wireless

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Personnel Detector Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Residential

- 6.1.2. Commercial

- 6.1.3. Industrial

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Wired

- 6.2.2. Wireless

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Personnel Detector Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Residential

- 7.1.2. Commercial

- 7.1.3. Industrial

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Wired

- 7.2.2. Wireless

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Personnel Detector Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Residential

- 8.1.2. Commercial

- 8.1.3. Industrial

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Wired

- 8.2.2. Wireless

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Personnel Detector Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Residential

- 9.1.2. Commercial

- 9.1.3. Industrial

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Wired

- 9.2.2. Wireless

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Personnel Detector Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Residential

- 10.1.2. Commercial

- 10.1.3. Industrial

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Wired

- 10.2.2. Wireless

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Panasonic

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Eaton

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Schneider Electric

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Top Greener

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Sensio Lighting

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 HPM (Legrand)

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Walnut Innovation

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Lutron Electronics

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Leviton Manufacturing

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 GE Lighting (Savant)

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Sunricher

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 ELEGRP

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 RS Components & Controls

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Ecoamica Tech

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 DS Electronics

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Sensinova

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Signify Holding

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.1 Panasonic

List of Figures

- Figure 1: Global Personnel Detector Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: Global Personnel Detector Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Personnel Detector Revenue (undefined), by Application 2025 & 2033

- Figure 4: North America Personnel Detector Volume (K), by Application 2025 & 2033

- Figure 5: North America Personnel Detector Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Personnel Detector Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Personnel Detector Revenue (undefined), by Types 2025 & 2033

- Figure 8: North America Personnel Detector Volume (K), by Types 2025 & 2033

- Figure 9: North America Personnel Detector Revenue Share (%), by Types 2025 & 2033

- Figure 10: North America Personnel Detector Volume Share (%), by Types 2025 & 2033

- Figure 11: North America Personnel Detector Revenue (undefined), by Country 2025 & 2033

- Figure 12: North America Personnel Detector Volume (K), by Country 2025 & 2033

- Figure 13: North America Personnel Detector Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Personnel Detector Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Personnel Detector Revenue (undefined), by Application 2025 & 2033

- Figure 16: South America Personnel Detector Volume (K), by Application 2025 & 2033

- Figure 17: South America Personnel Detector Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Personnel Detector Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Personnel Detector Revenue (undefined), by Types 2025 & 2033

- Figure 20: South America Personnel Detector Volume (K), by Types 2025 & 2033

- Figure 21: South America Personnel Detector Revenue Share (%), by Types 2025 & 2033

- Figure 22: South America Personnel Detector Volume Share (%), by Types 2025 & 2033

- Figure 23: South America Personnel Detector Revenue (undefined), by Country 2025 & 2033

- Figure 24: South America Personnel Detector Volume (K), by Country 2025 & 2033

- Figure 25: South America Personnel Detector Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Personnel Detector Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Personnel Detector Revenue (undefined), by Application 2025 & 2033

- Figure 28: Europe Personnel Detector Volume (K), by Application 2025 & 2033

- Figure 29: Europe Personnel Detector Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Personnel Detector Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Personnel Detector Revenue (undefined), by Types 2025 & 2033

- Figure 32: Europe Personnel Detector Volume (K), by Types 2025 & 2033

- Figure 33: Europe Personnel Detector Revenue Share (%), by Types 2025 & 2033

- Figure 34: Europe Personnel Detector Volume Share (%), by Types 2025 & 2033

- Figure 35: Europe Personnel Detector Revenue (undefined), by Country 2025 & 2033

- Figure 36: Europe Personnel Detector Volume (K), by Country 2025 & 2033

- Figure 37: Europe Personnel Detector Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Personnel Detector Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Personnel Detector Revenue (undefined), by Application 2025 & 2033

- Figure 40: Middle East & Africa Personnel Detector Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Personnel Detector Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Personnel Detector Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Personnel Detector Revenue (undefined), by Types 2025 & 2033

- Figure 44: Middle East & Africa Personnel Detector Volume (K), by Types 2025 & 2033

- Figure 45: Middle East & Africa Personnel Detector Revenue Share (%), by Types 2025 & 2033

- Figure 46: Middle East & Africa Personnel Detector Volume Share (%), by Types 2025 & 2033

- Figure 47: Middle East & Africa Personnel Detector Revenue (undefined), by Country 2025 & 2033

- Figure 48: Middle East & Africa Personnel Detector Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Personnel Detector Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Personnel Detector Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Personnel Detector Revenue (undefined), by Application 2025 & 2033

- Figure 52: Asia Pacific Personnel Detector Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Personnel Detector Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Personnel Detector Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Personnel Detector Revenue (undefined), by Types 2025 & 2033

- Figure 56: Asia Pacific Personnel Detector Volume (K), by Types 2025 & 2033

- Figure 57: Asia Pacific Personnel Detector Revenue Share (%), by Types 2025 & 2033

- Figure 58: Asia Pacific Personnel Detector Volume Share (%), by Types 2025 & 2033

- Figure 59: Asia Pacific Personnel Detector Revenue (undefined), by Country 2025 & 2033

- Figure 60: Asia Pacific Personnel Detector Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Personnel Detector Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Personnel Detector Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Personnel Detector Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Personnel Detector Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Personnel Detector Revenue undefined Forecast, by Types 2020 & 2033

- Table 4: Global Personnel Detector Volume K Forecast, by Types 2020 & 2033

- Table 5: Global Personnel Detector Revenue undefined Forecast, by Region 2020 & 2033

- Table 6: Global Personnel Detector Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Personnel Detector Revenue undefined Forecast, by Application 2020 & 2033

- Table 8: Global Personnel Detector Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Personnel Detector Revenue undefined Forecast, by Types 2020 & 2033

- Table 10: Global Personnel Detector Volume K Forecast, by Types 2020 & 2033

- Table 11: Global Personnel Detector Revenue undefined Forecast, by Country 2020 & 2033

- Table 12: Global Personnel Detector Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Personnel Detector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: United States Personnel Detector Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Personnel Detector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Canada Personnel Detector Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Personnel Detector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 18: Mexico Personnel Detector Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Personnel Detector Revenue undefined Forecast, by Application 2020 & 2033

- Table 20: Global Personnel Detector Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Personnel Detector Revenue undefined Forecast, by Types 2020 & 2033

- Table 22: Global Personnel Detector Volume K Forecast, by Types 2020 & 2033

- Table 23: Global Personnel Detector Revenue undefined Forecast, by Country 2020 & 2033

- Table 24: Global Personnel Detector Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Personnel Detector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Brazil Personnel Detector Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Personnel Detector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Argentina Personnel Detector Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Personnel Detector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Personnel Detector Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Personnel Detector Revenue undefined Forecast, by Application 2020 & 2033

- Table 32: Global Personnel Detector Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Personnel Detector Revenue undefined Forecast, by Types 2020 & 2033

- Table 34: Global Personnel Detector Volume K Forecast, by Types 2020 & 2033

- Table 35: Global Personnel Detector Revenue undefined Forecast, by Country 2020 & 2033

- Table 36: Global Personnel Detector Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Personnel Detector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Personnel Detector Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Personnel Detector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 40: Germany Personnel Detector Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Personnel Detector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: France Personnel Detector Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Personnel Detector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: Italy Personnel Detector Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Personnel Detector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Spain Personnel Detector Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Personnel Detector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 48: Russia Personnel Detector Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Personnel Detector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 50: Benelux Personnel Detector Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Personnel Detector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 52: Nordics Personnel Detector Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Personnel Detector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Personnel Detector Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Personnel Detector Revenue undefined Forecast, by Application 2020 & 2033

- Table 56: Global Personnel Detector Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Personnel Detector Revenue undefined Forecast, by Types 2020 & 2033

- Table 58: Global Personnel Detector Volume K Forecast, by Types 2020 & 2033

- Table 59: Global Personnel Detector Revenue undefined Forecast, by Country 2020 & 2033

- Table 60: Global Personnel Detector Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Personnel Detector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 62: Turkey Personnel Detector Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Personnel Detector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 64: Israel Personnel Detector Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Personnel Detector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 66: GCC Personnel Detector Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Personnel Detector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 68: North Africa Personnel Detector Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Personnel Detector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 70: South Africa Personnel Detector Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Personnel Detector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Personnel Detector Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Personnel Detector Revenue undefined Forecast, by Application 2020 & 2033

- Table 74: Global Personnel Detector Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Personnel Detector Revenue undefined Forecast, by Types 2020 & 2033

- Table 76: Global Personnel Detector Volume K Forecast, by Types 2020 & 2033

- Table 77: Global Personnel Detector Revenue undefined Forecast, by Country 2020 & 2033

- Table 78: Global Personnel Detector Volume K Forecast, by Country 2020 & 2033

- Table 79: China Personnel Detector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 80: China Personnel Detector Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Personnel Detector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 82: India Personnel Detector Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Personnel Detector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 84: Japan Personnel Detector Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Personnel Detector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 86: South Korea Personnel Detector Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Personnel Detector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Personnel Detector Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Personnel Detector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 90: Oceania Personnel Detector Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Personnel Detector Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Personnel Detector Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Personnel Detector?

The projected CAGR is approximately 16.13%.

2. Which companies are prominent players in the Personnel Detector?

Key companies in the market include Panasonic, Eaton, Schneider Electric, Top Greener, Sensio Lighting, HPM (Legrand), Walnut Innovation, Lutron Electronics, Leviton Manufacturing, GE Lighting (Savant), Sunricher, ELEGRP, RS Components & Controls, Ecoamica Tech, DS Electronics, Sensinova, Signify Holding.

3. What are the main segments of the Personnel Detector?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3350.00, USD 5025.00, and USD 6700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Personnel Detector," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Personnel Detector report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Personnel Detector?

To stay informed about further developments, trends, and reports in the Personnel Detector, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence