Key Insights

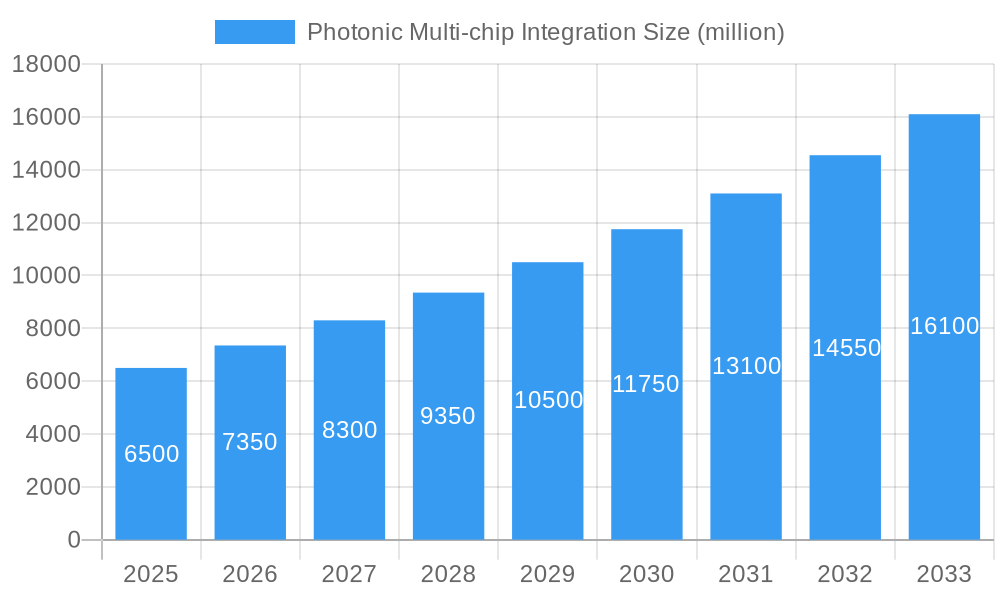

The Photonic Multi-chip Integration market is set for substantial expansion, with a projected market size of $15.47 billion by 2025, driven by a compelling Compound Annual Growth Rate (CAGR) of 20.1%. This robust growth is fueled by escalating demand for high-speed data transmission, crucial for telecommunications advancements and the expanding optical fiber communication sector. Photonic multi-chip integration addresses key industry needs for miniaturization, reduced power consumption, and enhanced performance, making it vital for next-generation optical networks. The proliferation of optical fiber sensors across industrial monitoring and healthcare, coupled with the transformative potential of quantum computing and advanced biomedical applications, are significant market accelerators. The market's ability to deliver greater functionality and efficiency in smaller form factors aligns directly with the technological trajectory of these high-growth industries, ensuring sustained momentum.

Photonic Multi-chip Integration Market Size (In Billion)

Key trends shaping the market include the development of advanced packaging techniques and the growing adoption of silicon photonics as a manufacturing platform. These advancements facilitate the creation of more complex and cost-effective photonic integrated circuits (PICs). Potential restraints, such as high initial R&D and manufacturing investment costs, alongside the requirement for skilled photonic design and fabrication expertise, may present challenges. However, the strategic importance of integrated photonic solutions in enabling future technological paradigms, particularly for 5G/6G infrastructure and advanced data centers, is expected to outweigh these limitations. Leading companies like Broadcom, Intel Corporation, and Infinera Corporation are investing heavily in innovation, indicating a competitive landscape focused on delivering cutting-edge solutions for Passive and Active Photonic Integrated Circuits.

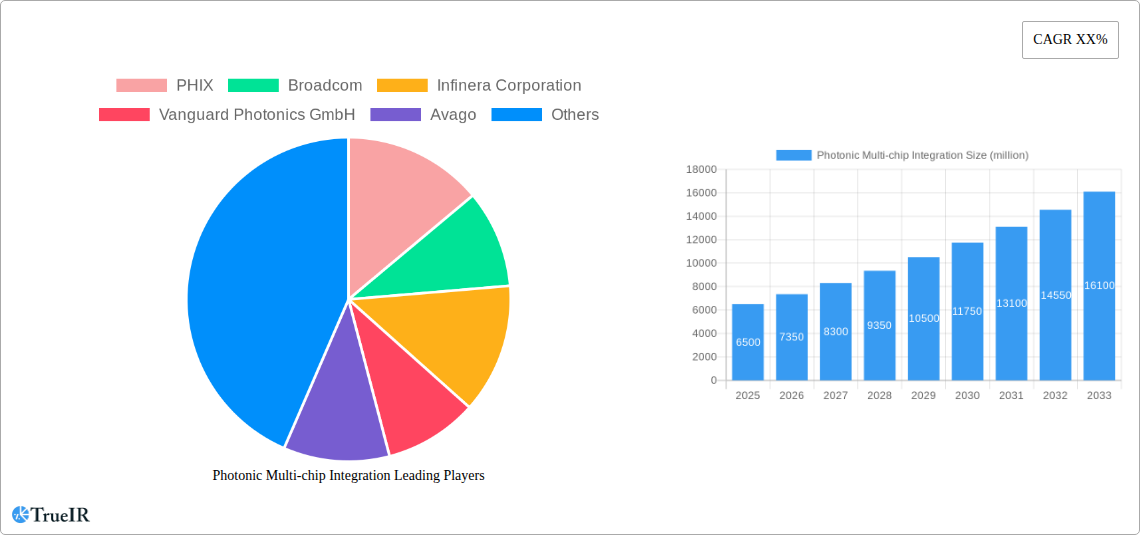

Photonic Multi-chip Integration Company Market Share

Discover the dynamic, SEO-optimized market outlook for Photonic Multi-chip Integration, featuring market size, growth forecasts, and key industry trends.

Photonic Multi-chip Integration Market Structure & Competitive Landscape

The Photonic Multi-chip Integration market is characterized by a moderate to high level of concentration, driven by significant R&D investments and the increasing demand for miniaturized, high-performance photonic components. Key innovation drivers include advancements in silicon photonics, heterogeneous integration techniques, and the development of novel light sources and detectors. Regulatory impacts are minimal at present, though industry standards for interoperability and performance are gradually emerging. Product substitutes, such as discrete optical components and electronic signal processing, are being increasingly challenged by the superior speed, bandwidth, and power efficiency offered by integrated photonic solutions. End-user segmentation is diverse, spanning telecommunications, data centers, sensing, and emerging quantum technologies. Mergers and acquisitions (M&A) are a notable trend, with an estimated xx million dollars in M&A volume over the historical period 2019-2024, reflecting the industry's consolidation and the pursuit of synergistic capabilities. Major players are actively acquiring smaller, specialized firms to enhance their product portfolios and gain market share. For instance, companies like Broadcom, Infinera Corporation, and Intel Corporation are strategically positioned through internal development and targeted acquisitions. The competitive landscape is shaped by a mix of established semiconductor giants and specialized photonics companies, all striving to capture the immense potential of this rapidly evolving technology.

Photonic Multi-chip Integration Market Trends & Opportunities

The Photonic Multi-chip Integration market is experiencing robust growth, projected to reach an estimated xx million dollars by the base year 2025, with a compelling Compound Annual Growth Rate (CAGR) of xx% during the forecast period 2025–2033. This expansion is fueled by a confluence of technological advancements and burgeoning application demands. The relentless need for higher bandwidth and lower latency in optical fiber communication networks, driven by cloud computing, big data analytics, and the proliferation of 5G and beyond, is a primary catalyst. The increasing adoption of passive photonic integrated circuits (PICs) for signal routing and modulation, alongside active PICs incorporating lasers and detectors for signal generation and reception, underscores a significant shift towards highly integrated solutions. Market penetration rates are rapidly increasing across various sectors, with optical fiber communication accounting for the largest share, estimated at xx million dollars in 2025. Opportunities are abundant in the development of next-generation transceivers, optical interconnects for high-performance computing, and compact sensing modules. Consumer preferences are increasingly leaning towards smaller, more power-efficient, and cost-effective photonic devices, directly benefiting the multi-chip integration approach. Competitive dynamics are intense, with companies like PHIX, NeoPhotonics, and LioniX continually pushing the boundaries of integration density and performance. The trend towards co-packaged optics, where photonic components are integrated directly with processors, represents a significant technological shift, promising to revolutionize data center architecture and unlock new levels of performance. Furthermore, the growing interest in quantum computing, where precise control of photons is paramount, presents a nascent but high-potential segment for advanced photonic integration. The biomedical sector is also emerging as a key application area, with integrated photonics enabling advancements in diagnostic tools, lab-on-a-chip devices, and optical coherence tomography. The pursuit of higher levels of integration, such as monolithic integration where possible, alongside advanced packaging techniques, will continue to define the market's trajectory.

Dominant Markets & Segments in Photonic Multi-chip Integration

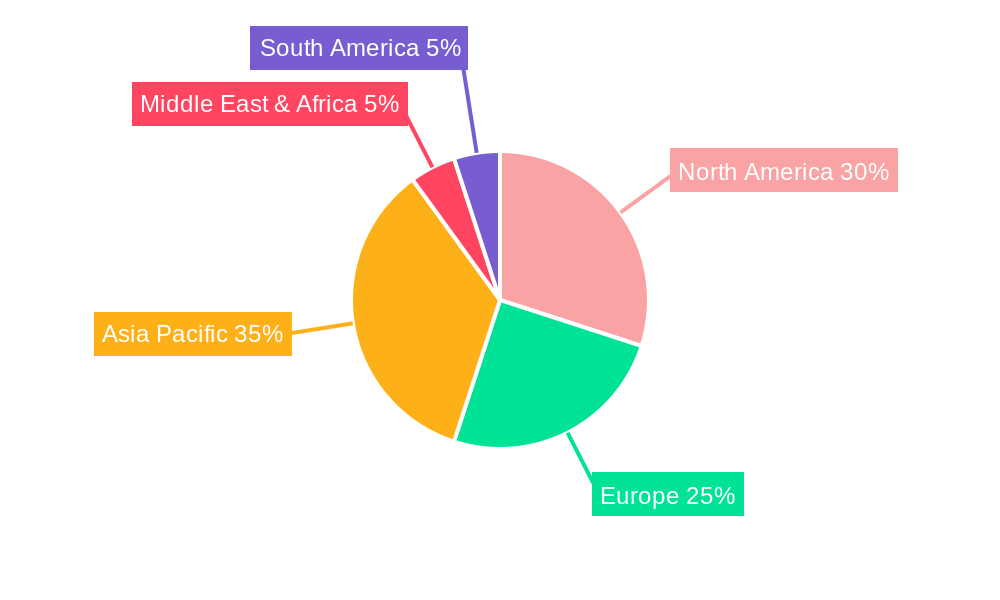

The Photonic Multi-chip Integration market is witnessing significant dominance by the Optical Fiber Communication segment, which is projected to account for xx million dollars in 2025 and is expected to be the primary growth engine throughout the forecast period. This dominance is attributed to the escalating demand for higher data transmission rates in telecommunications and data centers. The ongoing rollout of 5G infrastructure, expansion of fiber-to-the-home (FTTH) networks, and the insatiable appetite for bandwidth from cloud services and AI workloads are critical growth drivers. Government initiatives and policies promoting digital transformation and broadband expansion globally further bolster this segment. The Asia-Pacific region, particularly China and Japan, is identified as the leading geographical market, contributing an estimated xx million dollars in 2025. This leadership is driven by extensive investments in telecommunications infrastructure, a robust manufacturing base for electronic and photonic components, and a growing domestic demand for advanced communication technologies. Key growth drivers in this region include the widespread adoption of high-speed internet, the development of smart cities, and significant government support for R&D in advanced technologies.

In terms of Types, Active Photonic Integrated Circuits (PICs) are currently leading the market with an estimated valuation of xx million dollars in 2025. This is due to their crucial role in signal generation, amplification, and detection, which are essential for optical communication systems. However, the market is also seeing rapid growth in Passive Photonic Integrated Circuits (PICs), particularly in applications requiring complex signal routing, multiplexing, and demultiplexing. The synergy between passive and active components within a multi-chip integration framework is a key enabler for compact and cost-effective photonic modules.

Emerging segments like Quantum Computing and Biomedical applications, while smaller in current market size, represent significant future growth opportunities. Quantum computing relies heavily on precise photonic control and entanglement, making integrated photonic solutions indispensable. The biomedical sector is leveraging photonic integration for miniaturized diagnostic tools, advanced imaging, and lab-on-a-chip devices, offering non-invasive and highly sensitive detection capabilities. The United States and Europe are also significant markets, driven by strong research institutions, innovation hubs, and the presence of major technology companies like Intel Corporation and Broadcom, actively investing in R&D and new product development. The ongoing quest for higher integration levels, reduced power consumption, and lower manufacturing costs continues to drive market expansion across all segments and regions.

Photonic Multi-chip Integration Product Analysis

Photonic Multi-chip Integration is revolutionizing the landscape of optical components by enabling the miniaturization, enhanced performance, and cost reduction of complex photonic systems. Key product innovations revolve around the seamless integration of diverse photonic functionalities—including lasers, modulators, detectors, and waveguides—onto a single platform, often through advanced packaging techniques or heterogeneous integration. These advancements lead to smaller footprints, reduced power consumption, and significantly improved signal integrity compared to discrete optical solutions. Competitive advantages are derived from higher bandwidth densities, lower latency, and greater reliability. Applications span across high-speed optical fiber communication transceivers, optical sensors for industrial automation and healthcare, and critical components for emerging fields like quantum computing and advanced biomedical diagnostics. The focus on advanced materials and manufacturing processes, such as indium phosphide (InP) and silicon photonics, further enhances the performance and scalability of these integrated photonic products.

Key Drivers, Barriers & Challenges in Photonic Multi-chip Integration

Key Drivers: The Photonic Multi-chip Integration market is primarily propelled by the insatiable demand for higher bandwidth and lower latency in telecommunications and data centers, driven by the growth of cloud computing, AI, and 5G. Technological advancements in silicon photonics, heterogeneous integration, and advanced packaging are enabling smaller, more power-efficient, and cost-effective photonic devices. Economic factors, including the pursuit of reduced total cost of ownership in optical systems, are also significant drivers. Policy support for digital infrastructure development and research in emerging technologies like quantum computing further fuels market expansion.

Key Barriers & Challenges: Supply chain complexities and the specialized nature of photonic component manufacturing present significant challenges, potentially impacting lead times and costs. Regulatory hurdles related to interoperability standards and material sourcing can also influence market adoption. Intense competitive pressures from established players and emerging startups necessitate continuous innovation and cost optimization. The high upfront investment required for R&D and manufacturing infrastructure can act as a barrier to entry for smaller companies, contributing to market concentration. Overcoming these challenges is crucial for sustained growth.

Growth Drivers in the Photonic Multi-chip Integration Market

The Photonic Multi-chip Integration market is experiencing accelerated growth driven by several key factors. Technologically, the maturation of silicon photonics platforms and advanced heterogeneous integration techniques allows for the co-fabrication and packaging of multiple photonic functions, leading to unprecedented miniaturization and performance gains. Economically, the increasing demand for high-speed data transmission in telecommunications, data centers, and enterprise networks is creating a massive market opportunity. The push for power efficiency and lower operational costs in these high-bandwidth applications directly favors integrated solutions. Regulatory tailwinds, such as government initiatives supporting digital infrastructure expansion and the promotion of advanced manufacturing, also provide a conducive environment for market expansion.

Challenges Impacting Photonic Multi-chip Integration Growth

Several challenges can impact the growth trajectory of the Photonic Multi-chip Integration market. Supply chain vulnerabilities, particularly for specialized photonic materials and components, can lead to production bottlenecks and increased costs. Regulatory complexities surrounding intellectual property, standardization, and international trade policies may also create hurdles. Competitive pressures are intense, with a rapid pace of innovation requiring significant and continuous investment in research and development. Furthermore, the high capital expenditure associated with advanced photonic fabrication facilities can limit the accessibility for smaller players, potentially hindering broader market adoption and fostering market concentration.

Key Players Shaping the Photonic Multi-chip Integration Market

- PHIX

- Broadcom

- Infinera Corporation

- Vanguard Photonics GmbH

- Avago

- Intel Corporation

- NeoPhotonics

- Cisco

- ColorChip

- Finisar

- Ciena

- JDS Uniphase

- OneChip

- LioniX

Significant Photonic Multi-chip Integration Industry Milestones

- 2019: Advancements in silicon photonics fabrication enabling higher integration densities.

- 2020: Increased adoption of co-packaged optics for high-performance computing interconnects.

- 2021: Significant investment in R&D for photonic integrated circuits in quantum computing applications.

- 2022: Breakthroughs in heterogeneous integration of disparate photonic materials.

- 2023: Development of novel passive PICs for advanced optical sensing.

- 2024: Growing market traction for integrated photonic solutions in biomedical diagnostics.

- 2025 (Estimated): Widespread deployment of high-density photonic transceivers in 5G infrastructure.

- 2026-2033 (Projected): Continuous innovation leading to further miniaturization and cost reduction, enabling broader adoption across new application areas.

Future Outlook for Photonic Multi-chip Integration Market

The future outlook for the Photonic Multi-chip Integration market is exceptionally bright, driven by sustained demand for higher bandwidth, lower latency, and increased power efficiency across critical sectors. Strategic opportunities lie in the continued advancement of heterogeneous integration technologies, enabling the fusion of silicon photonics with other advanced materials like InP and III-V semiconductors. The burgeoning fields of quantum computing and advanced biomedical diagnostics present significant avenues for growth, where the precise control and manipulation of light are paramount. As miniaturization and cost reduction efforts intensify, photonic multi-chip integration is poised to become the de facto standard for optical interconnects and sensing, unlocking new frontiers in technology and innovation. The market is expected to witness further consolidation and collaborative efforts to accelerate product development and market penetration.

Photonic Multi-chip Integration Segmentation

-

1. Application

- 1.1. Optical Fiber Communication

- 1.2. Optical Fiber Sensor

- 1.3. Biomedical

- 1.4. Quantum Computing

-

2. Types

- 2.1. Passive Photonic Integrated Circuit

- 2.2. Active Photonic Integrated Circuit

Photonic Multi-chip Integration Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Photonic Multi-chip Integration Regional Market Share

Geographic Coverage of Photonic Multi-chip Integration

Photonic Multi-chip Integration REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 20.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Optical Fiber Communication

- 5.1.2. Optical Fiber Sensor

- 5.1.3. Biomedical

- 5.1.4. Quantum Computing

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Passive Photonic Integrated Circuit

- 5.2.2. Active Photonic Integrated Circuit

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Photonic Multi-chip Integration Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Optical Fiber Communication

- 6.1.2. Optical Fiber Sensor

- 6.1.3. Biomedical

- 6.1.4. Quantum Computing

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Passive Photonic Integrated Circuit

- 6.2.2. Active Photonic Integrated Circuit

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Photonic Multi-chip Integration Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Optical Fiber Communication

- 7.1.2. Optical Fiber Sensor

- 7.1.3. Biomedical

- 7.1.4. Quantum Computing

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Passive Photonic Integrated Circuit

- 7.2.2. Active Photonic Integrated Circuit

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Photonic Multi-chip Integration Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Optical Fiber Communication

- 8.1.2. Optical Fiber Sensor

- 8.1.3. Biomedical

- 8.1.4. Quantum Computing

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Passive Photonic Integrated Circuit

- 8.2.2. Active Photonic Integrated Circuit

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Photonic Multi-chip Integration Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Optical Fiber Communication

- 9.1.2. Optical Fiber Sensor

- 9.1.3. Biomedical

- 9.1.4. Quantum Computing

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Passive Photonic Integrated Circuit

- 9.2.2. Active Photonic Integrated Circuit

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Photonic Multi-chip Integration Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Optical Fiber Communication

- 10.1.2. Optical Fiber Sensor

- 10.1.3. Biomedical

- 10.1.4. Quantum Computing

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Passive Photonic Integrated Circuit

- 10.2.2. Active Photonic Integrated Circuit

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Photonic Multi-chip Integration Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Optical Fiber Communication

- 11.1.2. Optical Fiber Sensor

- 11.1.3. Biomedical

- 11.1.4. Quantum Computing

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Passive Photonic Integrated Circuit

- 11.2.2. Active Photonic Integrated Circuit

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 PHIX

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Broadcom

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Infinera Corporation

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Vanguard Photonics GmbH

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Avago

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Intel Corporation

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 NeoPhotonics

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Cisco

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 ColorChip

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Finisar

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Ciena

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 JDS Uniphase

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 OneChip

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 LioniX

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.1 PHIX

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Photonic Multi-chip Integration Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Global Photonic Multi-chip Integration Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Photonic Multi-chip Integration Revenue (billion), by Application 2025 & 2033

- Figure 4: North America Photonic Multi-chip Integration Volume (K), by Application 2025 & 2033

- Figure 5: North America Photonic Multi-chip Integration Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Photonic Multi-chip Integration Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Photonic Multi-chip Integration Revenue (billion), by Types 2025 & 2033

- Figure 8: North America Photonic Multi-chip Integration Volume (K), by Types 2025 & 2033

- Figure 9: North America Photonic Multi-chip Integration Revenue Share (%), by Types 2025 & 2033

- Figure 10: North America Photonic Multi-chip Integration Volume Share (%), by Types 2025 & 2033

- Figure 11: North America Photonic Multi-chip Integration Revenue (billion), by Country 2025 & 2033

- Figure 12: North America Photonic Multi-chip Integration Volume (K), by Country 2025 & 2033

- Figure 13: North America Photonic Multi-chip Integration Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Photonic Multi-chip Integration Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Photonic Multi-chip Integration Revenue (billion), by Application 2025 & 2033

- Figure 16: South America Photonic Multi-chip Integration Volume (K), by Application 2025 & 2033

- Figure 17: South America Photonic Multi-chip Integration Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Photonic Multi-chip Integration Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Photonic Multi-chip Integration Revenue (billion), by Types 2025 & 2033

- Figure 20: South America Photonic Multi-chip Integration Volume (K), by Types 2025 & 2033

- Figure 21: South America Photonic Multi-chip Integration Revenue Share (%), by Types 2025 & 2033

- Figure 22: South America Photonic Multi-chip Integration Volume Share (%), by Types 2025 & 2033

- Figure 23: South America Photonic Multi-chip Integration Revenue (billion), by Country 2025 & 2033

- Figure 24: South America Photonic Multi-chip Integration Volume (K), by Country 2025 & 2033

- Figure 25: South America Photonic Multi-chip Integration Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Photonic Multi-chip Integration Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Photonic Multi-chip Integration Revenue (billion), by Application 2025 & 2033

- Figure 28: Europe Photonic Multi-chip Integration Volume (K), by Application 2025 & 2033

- Figure 29: Europe Photonic Multi-chip Integration Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Photonic Multi-chip Integration Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Photonic Multi-chip Integration Revenue (billion), by Types 2025 & 2033

- Figure 32: Europe Photonic Multi-chip Integration Volume (K), by Types 2025 & 2033

- Figure 33: Europe Photonic Multi-chip Integration Revenue Share (%), by Types 2025 & 2033

- Figure 34: Europe Photonic Multi-chip Integration Volume Share (%), by Types 2025 & 2033

- Figure 35: Europe Photonic Multi-chip Integration Revenue (billion), by Country 2025 & 2033

- Figure 36: Europe Photonic Multi-chip Integration Volume (K), by Country 2025 & 2033

- Figure 37: Europe Photonic Multi-chip Integration Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Photonic Multi-chip Integration Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Photonic Multi-chip Integration Revenue (billion), by Application 2025 & 2033

- Figure 40: Middle East & Africa Photonic Multi-chip Integration Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Photonic Multi-chip Integration Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Photonic Multi-chip Integration Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Photonic Multi-chip Integration Revenue (billion), by Types 2025 & 2033

- Figure 44: Middle East & Africa Photonic Multi-chip Integration Volume (K), by Types 2025 & 2033

- Figure 45: Middle East & Africa Photonic Multi-chip Integration Revenue Share (%), by Types 2025 & 2033

- Figure 46: Middle East & Africa Photonic Multi-chip Integration Volume Share (%), by Types 2025 & 2033

- Figure 47: Middle East & Africa Photonic Multi-chip Integration Revenue (billion), by Country 2025 & 2033

- Figure 48: Middle East & Africa Photonic Multi-chip Integration Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Photonic Multi-chip Integration Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Photonic Multi-chip Integration Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Photonic Multi-chip Integration Revenue (billion), by Application 2025 & 2033

- Figure 52: Asia Pacific Photonic Multi-chip Integration Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Photonic Multi-chip Integration Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Photonic Multi-chip Integration Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Photonic Multi-chip Integration Revenue (billion), by Types 2025 & 2033

- Figure 56: Asia Pacific Photonic Multi-chip Integration Volume (K), by Types 2025 & 2033

- Figure 57: Asia Pacific Photonic Multi-chip Integration Revenue Share (%), by Types 2025 & 2033

- Figure 58: Asia Pacific Photonic Multi-chip Integration Volume Share (%), by Types 2025 & 2033

- Figure 59: Asia Pacific Photonic Multi-chip Integration Revenue (billion), by Country 2025 & 2033

- Figure 60: Asia Pacific Photonic Multi-chip Integration Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Photonic Multi-chip Integration Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Photonic Multi-chip Integration Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Photonic Multi-chip Integration Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Photonic Multi-chip Integration Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Photonic Multi-chip Integration Revenue billion Forecast, by Types 2020 & 2033

- Table 4: Global Photonic Multi-chip Integration Volume K Forecast, by Types 2020 & 2033

- Table 5: Global Photonic Multi-chip Integration Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Global Photonic Multi-chip Integration Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Photonic Multi-chip Integration Revenue billion Forecast, by Application 2020 & 2033

- Table 8: Global Photonic Multi-chip Integration Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Photonic Multi-chip Integration Revenue billion Forecast, by Types 2020 & 2033

- Table 10: Global Photonic Multi-chip Integration Volume K Forecast, by Types 2020 & 2033

- Table 11: Global Photonic Multi-chip Integration Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Global Photonic Multi-chip Integration Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Photonic Multi-chip Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: United States Photonic Multi-chip Integration Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Photonic Multi-chip Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Canada Photonic Multi-chip Integration Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Photonic Multi-chip Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Mexico Photonic Multi-chip Integration Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Photonic Multi-chip Integration Revenue billion Forecast, by Application 2020 & 2033

- Table 20: Global Photonic Multi-chip Integration Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Photonic Multi-chip Integration Revenue billion Forecast, by Types 2020 & 2033

- Table 22: Global Photonic Multi-chip Integration Volume K Forecast, by Types 2020 & 2033

- Table 23: Global Photonic Multi-chip Integration Revenue billion Forecast, by Country 2020 & 2033

- Table 24: Global Photonic Multi-chip Integration Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Photonic Multi-chip Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Brazil Photonic Multi-chip Integration Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Photonic Multi-chip Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Argentina Photonic Multi-chip Integration Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Photonic Multi-chip Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Photonic Multi-chip Integration Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Photonic Multi-chip Integration Revenue billion Forecast, by Application 2020 & 2033

- Table 32: Global Photonic Multi-chip Integration Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Photonic Multi-chip Integration Revenue billion Forecast, by Types 2020 & 2033

- Table 34: Global Photonic Multi-chip Integration Volume K Forecast, by Types 2020 & 2033

- Table 35: Global Photonic Multi-chip Integration Revenue billion Forecast, by Country 2020 & 2033

- Table 36: Global Photonic Multi-chip Integration Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Photonic Multi-chip Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Photonic Multi-chip Integration Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Photonic Multi-chip Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Germany Photonic Multi-chip Integration Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Photonic Multi-chip Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: France Photonic Multi-chip Integration Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Photonic Multi-chip Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: Italy Photonic Multi-chip Integration Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Photonic Multi-chip Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Spain Photonic Multi-chip Integration Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Photonic Multi-chip Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 48: Russia Photonic Multi-chip Integration Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Photonic Multi-chip Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 50: Benelux Photonic Multi-chip Integration Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Photonic Multi-chip Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 52: Nordics Photonic Multi-chip Integration Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Photonic Multi-chip Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Photonic Multi-chip Integration Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Photonic Multi-chip Integration Revenue billion Forecast, by Application 2020 & 2033

- Table 56: Global Photonic Multi-chip Integration Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Photonic Multi-chip Integration Revenue billion Forecast, by Types 2020 & 2033

- Table 58: Global Photonic Multi-chip Integration Volume K Forecast, by Types 2020 & 2033

- Table 59: Global Photonic Multi-chip Integration Revenue billion Forecast, by Country 2020 & 2033

- Table 60: Global Photonic Multi-chip Integration Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Photonic Multi-chip Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 62: Turkey Photonic Multi-chip Integration Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Photonic Multi-chip Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 64: Israel Photonic Multi-chip Integration Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Photonic Multi-chip Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 66: GCC Photonic Multi-chip Integration Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Photonic Multi-chip Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 68: North Africa Photonic Multi-chip Integration Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Photonic Multi-chip Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 70: South Africa Photonic Multi-chip Integration Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Photonic Multi-chip Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Photonic Multi-chip Integration Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Photonic Multi-chip Integration Revenue billion Forecast, by Application 2020 & 2033

- Table 74: Global Photonic Multi-chip Integration Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Photonic Multi-chip Integration Revenue billion Forecast, by Types 2020 & 2033

- Table 76: Global Photonic Multi-chip Integration Volume K Forecast, by Types 2020 & 2033

- Table 77: Global Photonic Multi-chip Integration Revenue billion Forecast, by Country 2020 & 2033

- Table 78: Global Photonic Multi-chip Integration Volume K Forecast, by Country 2020 & 2033

- Table 79: China Photonic Multi-chip Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 80: China Photonic Multi-chip Integration Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Photonic Multi-chip Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 82: India Photonic Multi-chip Integration Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Photonic Multi-chip Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 84: Japan Photonic Multi-chip Integration Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Photonic Multi-chip Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 86: South Korea Photonic Multi-chip Integration Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Photonic Multi-chip Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Photonic Multi-chip Integration Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Photonic Multi-chip Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 90: Oceania Photonic Multi-chip Integration Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Photonic Multi-chip Integration Revenue (billion) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Photonic Multi-chip Integration Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Photonic Multi-chip Integration?

The projected CAGR is approximately 20.1%.

2. Which companies are prominent players in the Photonic Multi-chip Integration?

Key companies in the market include PHIX, Broadcom, Infinera Corporation, Vanguard Photonics GmbH, Avago, Intel Corporation, NeoPhotonics, Cisco, ColorChip, Finisar, Ciena, JDS Uniphase, OneChip, LioniX.

3. What are the main segments of the Photonic Multi-chip Integration?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 15.47 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3350.00, USD 5025.00, and USD 6700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Photonic Multi-chip Integration," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Photonic Multi-chip Integration report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Photonic Multi-chip Integration?

To stay informed about further developments, trends, and reports in the Photonic Multi-chip Integration, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence