Key Insights

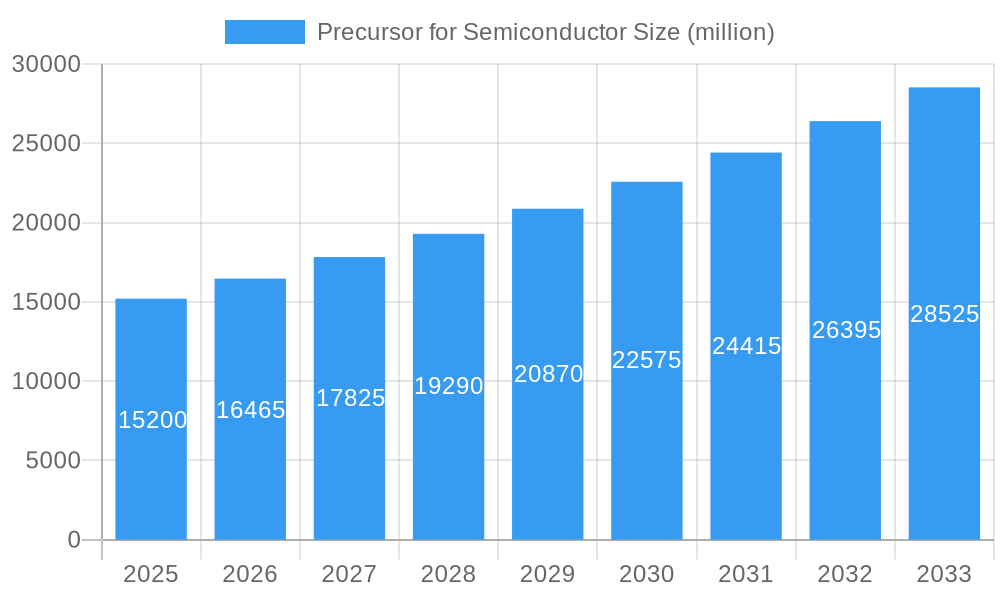

The global Precursor for Semiconductor market is poised for significant expansion, projected to reach an estimated USD 15,200 million by 2025 and grow at a Compound Annual Growth Rate (CAGR) of 8.5% through 2033. This robust growth is primarily fueled by the insatiable demand for advanced semiconductor devices across a multitude of industries, including consumer electronics, automotive, telecommunications, and artificial intelligence. The increasing complexity and miniaturization of integrated circuits necessitate the use of highly specialized and pure precursors for critical manufacturing processes such as Physical Vapor Deposition (PVD), Chemical Vapor Deposition (CVD), Atomic Layer Deposition (ALD), epitaxial growth, and etching. Emerging technologies like 5G deployment, the proliferation of IoT devices, and advancements in autonomous driving systems are directly contributing to this surging demand. Furthermore, the continuous innovation in semiconductor fabrication techniques, aiming for enhanced performance, efficiency, and reduced power consumption, requires the development and adoption of novel precursor materials with specific properties.

Precursor for Semiconductor Market Size (In Billion)

Several key drivers are propelling the precursor market forward. The relentless pursuit of smaller, faster, and more powerful chips by leading foundries and integrated device manufacturers (IDMs) is a primary catalyst. This trend directly translates to a higher requirement for high-purity precursors that enable finer feature sizes and improved device reliability. Geopolitical shifts and the emphasis on supply chain resilience are also influencing market dynamics, potentially leading to regionalization of production and increased investment in domestic precursor manufacturing capabilities. However, the market is not without its restraints. The stringent purity requirements and complex manufacturing processes for high-performance precursors can lead to high production costs, potentially impacting affordability. Moreover, the long qualification cycles for new precursor materials within the semiconductor industry can pose a challenge to rapid market adoption. Despite these hurdles, the overarching demand for cutting-edge semiconductor technology and the continuous evolution of fabrication processes suggest a bright future for the precursor market.

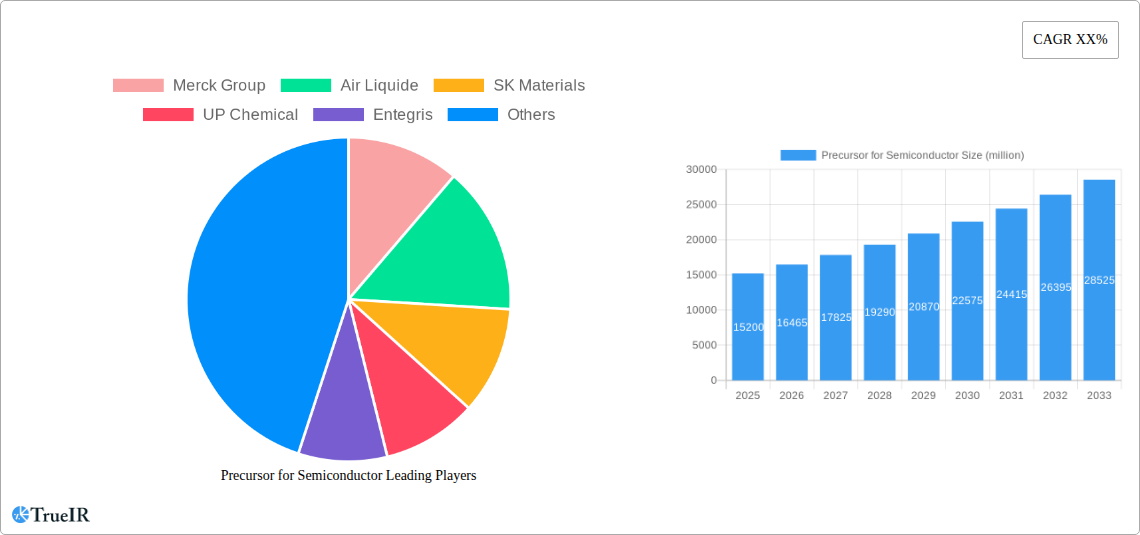

Precursor for Semiconductor Company Market Share

This comprehensive report delves into the dynamic global market for semiconductor precursors, essential chemical compounds critical for the fabrication of advanced microelectronic devices. Leveraging extensive data from 2019 to 2033, with a base year of 2025, this analysis provides in-depth insights into market structure, trends, dominant segments, and future outlook, equipping stakeholders with actionable intelligence for strategic decision-making.

Precursor for Semiconductor Market Structure & Competitive Landscape

The global precursor for semiconductor market exhibits a moderately concentrated structure, with a significant presence of both established multinational corporations and emerging specialized manufacturers. Key players like Merck Group, Air Liquide, SK Materials, UP Chemical, Entegris, ADEKA, Hansol Chemical, DuPont, SoulBrain Co Ltd, Nanmat, DNF Solutions, Natachem, Tanaka Kikinzoku, Botai Electronic Material, Gelest, Strem Chemicals, Anhui Adchem, EpiValence, FUJIFILM Corporation, Japan Advanced Chemicals, Wonik Materials, and others are actively shaping the competitive landscape. Innovation drivers, such as the relentless pursuit of miniaturization and enhanced performance in semiconductor chips, fuel continuous product development and the introduction of novel precursor chemistries. Regulatory impacts, particularly concerning environmental sustainability and material safety, are increasingly influencing manufacturing processes and product formulations. The threat of product substitutes, while present in certain niche applications, is largely mitigated by the highly specialized nature of precursor materials tailored for specific fabrication processes. End-user segmentation is primarily driven by the diverse applications within the semiconductor industry, including PVD/CVD/ALD, Epitaxial Growth, and Etching. Mergers and acquisitions (M&A) are significant trends, with companies strategically acquiring competitors or complementary technologies to expand their product portfolios, enhance market reach, and consolidate their positions. An estimated XX million in M&A activity was observed in the historical period, indicating a strong drive for consolidation. Concentration ratios in key segments are estimated to be in the range of XX% for the top five players, highlighting the influence of dominant entities while still allowing for niche player success.

Precursor for Semiconductor Market Trends & Opportunities

The precursor for semiconductor market is poised for substantial growth, driven by the insatiable demand for advanced electronic devices across a multitude of industries. The market is projected to reach an estimated value of XX million by 2033, exhibiting a robust Compound Annual Growth Rate (CAGR) of XX% during the forecast period of 2025–2033. This growth is underpinned by several compelling trends. Firstly, the relentless advancement in semiconductor technology, including the transition to smaller process nodes (e.g., 3nm and below), necessitates the development and adoption of highly pure and specialized precursors for PVD, CVD, and ALD processes. These processes are critical for depositing thin films with precise control over thickness and composition, enabling the creation of more powerful and energy-efficient chips.

Secondly, the burgeoning demand for 5G infrastructure, artificial intelligence (AI), the Internet of Things (IoT), and electric vehicles (EVs) are significant market penetrators, directly fueling the need for advanced semiconductors and, consequently, their constituent precursors. The expansion of data centers and the increasing complexity of consumer electronics also contribute to this upward trajectory.

Thirdly, there is a discernible shift towards precursors that offer improved performance characteristics, such as lower deposition temperatures, enhanced film quality, and reduced impurity levels. This is particularly evident in the demand for high-k and low-k precursors, crucial for gate dielectrics and inter-layer dielectrics, respectively, which are vital for improving transistor performance and reducing power consumption.

Technological shifts, including the development of novel precursor chemistries with enhanced precursor stability, safer handling properties, and reduced environmental impact, are also creating new opportunities. Companies are investing heavily in R&D to develop precursors that are compatible with next-generation fabrication techniques and materials, such as advanced packaging technologies and emerging memory solutions. The competitive dynamics are characterized by intense innovation, strategic partnerships, and a focus on vertical integration to ensure supply chain security and cost optimization. Opportunities also lie in the development of cost-effective precursor solutions for emerging markets and specialized applications.

Dominant Markets & Segments in Precursor for Semiconductor

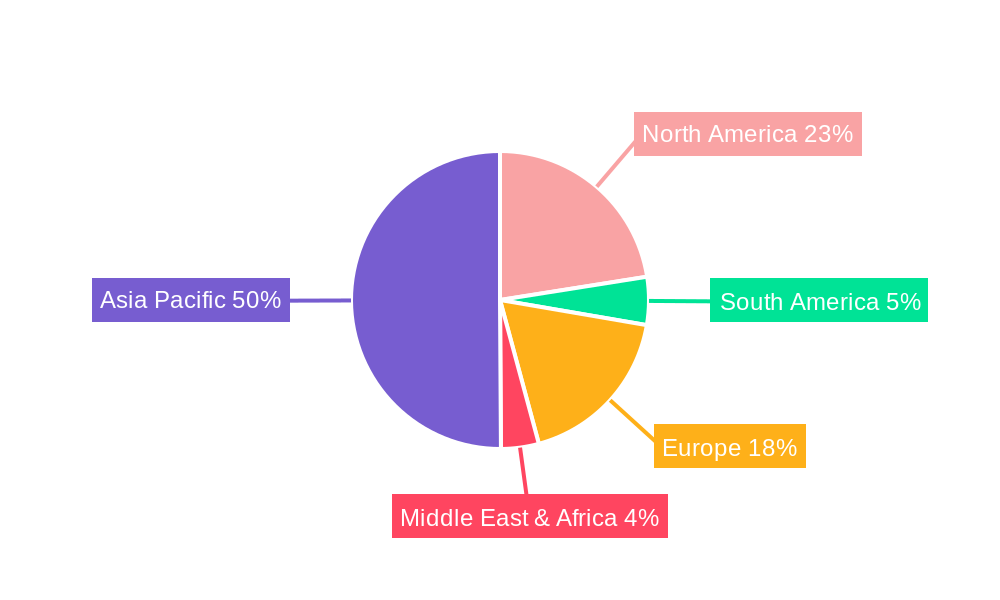

The global precursor for semiconductor market exhibits dominance across various geographical regions and product segments.

Dominant Region: Asia-Pacific is the leading market for semiconductor precursors, driven by its status as the global manufacturing hub for semiconductors. Countries like Taiwan, South Korea, China, and Japan are home to major foundries and integrated device manufacturers (IDMs) that consume vast quantities of precursors. The robust growth in these regions is attributed to:

- Infrastructure Investment: Significant government and private sector investments in advanced semiconductor manufacturing facilities and R&D centers.

- Policy Support: Favorable government policies and incentives aimed at bolstering domestic semiconductor production and technological self-sufficiency.

- Demand for Advanced Electronics: The massive consumer base in Asia drives demand for smartphones, computers, and other electronic devices, indirectly boosting precursor consumption.

Dominant Application Segment: The PVD/CVD/ALD segment is the largest and fastest-growing application area for semiconductor precursors. These techniques are fundamental to virtually all semiconductor fabrication processes, enabling the deposition of a wide array of materials with precise control.

- Enabling Miniaturization: PVD, CVD, and ALD are critical for depositing thin films of metals, dielectrics, and other materials required for creating smaller, more powerful transistors and integrated circuits.

- Material Diversity: These processes support the deposition of a wide range of materials, from conductive metals like copper and tungsten to insulating dielectrics like silicon dioxide and silicon nitride, and advanced high-k materials.

- Technological Advancement: Continuous innovation in PVD, CVD, and ALD processes necessitates the development of new and highly specialized precursors to meet the demands of next-generation semiconductor nodes.

Dominant Type Segment: Among the precursor types, Metal Precursors and High-k Precursors are experiencing significant growth.

- Metal Precursors: Essential for creating conductive pathways and interconnects in semiconductor devices, demand for high-purity metal precursors for copper, tungsten, and other metals remains strong.

- High-k Precursors: The transition to high-k gate dielectric materials in advanced transistors is a critical trend. These precursors enable the deposition of materials with higher dielectric constants, leading to reduced leakage current and improved device performance. Examples include precursors for Hafnium oxide (HfO2) and other advanced high-k materials.

- Silicon Precursors: Remain fundamental for various layers in semiconductor fabrication, including buffer layers and passivation.

- Low-k Precursors: Crucial for inter-layer dielectrics to reduce capacitance and signal delay, especially in high-speed applications.

The interplay of these dominant regions, applications, and precursor types creates a robust market environment with substantial opportunities for growth and innovation.

Precursor for Semiconductor Product Analysis

The precursor for semiconductor market is characterized by continuous product innovation focused on enhancing purity, performance, and process compatibility. Key advancements include the development of novel organometallic and inorganic precursors with improved thermal stability and lower decomposition temperatures, enabling lower-cost and more efficient deposition processes. For instance, the introduction of new metal-organic chemical vapor deposition (MOCVD) precursors has significantly improved the quality and yield of epitaxial growth for advanced compound semiconductors and silicon-germanium (SiGe) alloys. Furthermore, the development of ultra-high purity precursors with parts-per-trillion (ppt) impurity levels is critical for enabling sub-XX nm semiconductor manufacturing, where even trace contaminants can lead to device failure. Competitive advantages are derived from proprietary synthesis routes, advanced purification techniques, and strong intellectual property portfolios that ensure a consistent supply of high-performance precursors tailored for specific applications like PVD, CVD, ALD, and etching processes.

Key Drivers, Barriers & Challenges in Precursor for Semiconductor

Key Drivers: The semiconductor precursor market is propelled by several key factors. Technologically, the relentless drive towards smaller process nodes (e.g., 3nm and below) necessitates the development of highly specialized, ultra-pure precursors for PVD, CVD, and ALD applications. The increasing adoption of advanced materials like high-k dielectrics and novel interconnect metals is also a significant driver. Economically, the expanding global demand for consumer electronics, 5G infrastructure, AI, IoT devices, and electric vehicles directly translates to increased semiconductor production, thus boosting precursor consumption. Policy-driven factors, such as government initiatives to bolster domestic semiconductor manufacturing and R&D investments, further stimulate market growth.

Key Barriers & Challenges: The market faces several significant challenges and restraints. Supply chain issues, including the reliance on specific raw material sources and geopolitical vulnerabilities, can lead to price volatility and availability concerns. Regulatory hurdles related to chemical safety, environmental impact, and handling protocols for highly reactive precursors add complexity to manufacturing and logistics. Competitive pressures, particularly from established players with extensive R&D capabilities and economies of scale, can pose a barrier to entry for new companies. Furthermore, the high cost associated with developing and qualifying new precursor materials for semiconductor fabrication, often running into millions of dollars per qualification cycle, can be a significant restraint. The need for stringent quality control and consistency in precursor properties presents an ongoing operational challenge.

Growth Drivers in the Precursor for Semiconductor Market

The growth of the semiconductor precursor market is fundamentally driven by the insatiable global demand for more powerful, smaller, and energy-efficient electronic devices. The ongoing transition to advanced semiconductor manufacturing nodes, such as those below 5nm, is a primary technological driver, requiring highly specialized and ultra-pure precursors for PVD, CVD, and ALD processes. The proliferation of AI, 5G networks, IoT devices, and electric vehicles creates a multiplier effect on semiconductor demand, thereby stimulating the need for advanced precursors. Government initiatives worldwide to secure and expand domestic semiconductor manufacturing capabilities, coupled with significant R&D investments in novel materials and processes, also contribute substantially to market expansion.

Challenges Impacting Precursor for Semiconductor Growth

Several critical challenges impede the smooth growth of the semiconductor precursor market. Supply chain disruptions, including raw material sourcing complexities and geopolitical instabilities, can lead to price fluctuations and availability issues for key precursor components. Regulatory complexities surrounding the handling, transportation, and environmental impact of highly reactive and specialized precursor chemicals necessitate stringent compliance and can increase operational costs. Intense competitive pressures from established industry giants with significant R&D budgets and market share can create barriers to entry for smaller players. The high cost and lengthy qualification cycles for new precursor materials within the highly regulated semiconductor manufacturing ecosystem represent a significant financial and temporal hurdle for innovation.

Key Players Shaping the Precursor for Semiconductor Market

- Merck Group

- Air Liquide

- SK Materials

- UP Chemical

- Entegris

- ADEKA

- Hansol Chemical

- DuPont

- SoulBrain Co Ltd

- Nanmat

- DNF Solutions

- Natachem

- Tanaka Kikinzoku

- Botai Electronic Material

- Gelest

- Strem Chemicals

- Anhui Adchem

- EpiValence

- FUJIFILM Corporation

- Japan Advanced Chemicals

- Wonik Materials

Significant Precursor for Semiconductor Industry Milestones

- 2019: Launch of novel high-purity silicon precursors enabling advanced epitaxial growth for next-generation DRAM.

- 2020: Introduction of new metal-organic precursors for Atomic Layer Deposition (ALD) with improved conformality for 3D NAND fabrication.

- 2021: Merck Group expands its precursor manufacturing capacity to meet rising demand for advanced semiconductor materials.

- 2022: Entegris acquires a leading supplier of specialty chemicals and materials for the semiconductor industry, enhancing its portfolio.

- 2022: Air Liquide announces significant investments in research and development for advanced semiconductor precursors.

- 2023: SK Materials showcases innovative precursors for EUV lithography applications.

- 2023: FUJIFILM Corporation introduces a new generation of CVD precursors for high-performance logic devices.

- 2024: UP Chemical announces strategic partnerships to accelerate the development of novel precursors for emerging memory technologies.

Future Outlook for Precursor for Semiconductor Market

The future outlook for the precursor for semiconductor market remains exceptionally bright, driven by sustained technological advancements and escalating global demand for semiconductors. Strategic opportunities lie in the continuous development of ultra-high purity, low-cost precursors that enable next-generation semiconductor nodes (e.g., 2nm and below) and advanced packaging solutions. The growing importance of AI, autonomous driving, and the metaverse will further propel demand for specialized precursors. Companies that can demonstrate robust supply chain resilience, a strong commitment to sustainability, and agility in adapting to evolving fabrication processes will be well-positioned for significant growth. The market is expected to witness continued M&A activity as players seek to consolidate their market positions and expand their technological capabilities.

Precursor for Semiconductor Segmentation

-

1. Application

- 1.1. PVD/CVD/ALD

- 1.2. Epitaxial Growth and Etching, etc.

-

2. Types

- 2.1. Silicon Precursor

- 2.2. Metal Precursor

- 2.3. High-k Precursor

- 2.4. Low-k Precursor

Precursor for Semiconductor Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Precursor for Semiconductor Regional Market Share

Geographic Coverage of Precursor for Semiconductor

Precursor for Semiconductor REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of XX% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. PVD/CVD/ALD

- 5.1.2. Epitaxial Growth and Etching, etc.

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Silicon Precursor

- 5.2.2. Metal Precursor

- 5.2.3. High-k Precursor

- 5.2.4. Low-k Precursor

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Precursor for Semiconductor Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. PVD/CVD/ALD

- 6.1.2. Epitaxial Growth and Etching, etc.

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Silicon Precursor

- 6.2.2. Metal Precursor

- 6.2.3. High-k Precursor

- 6.2.4. Low-k Precursor

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Precursor for Semiconductor Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. PVD/CVD/ALD

- 7.1.2. Epitaxial Growth and Etching, etc.

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Silicon Precursor

- 7.2.2. Metal Precursor

- 7.2.3. High-k Precursor

- 7.2.4. Low-k Precursor

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Precursor for Semiconductor Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. PVD/CVD/ALD

- 8.1.2. Epitaxial Growth and Etching, etc.

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Silicon Precursor

- 8.2.2. Metal Precursor

- 8.2.3. High-k Precursor

- 8.2.4. Low-k Precursor

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Precursor for Semiconductor Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. PVD/CVD/ALD

- 9.1.2. Epitaxial Growth and Etching, etc.

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Silicon Precursor

- 9.2.2. Metal Precursor

- 9.2.3. High-k Precursor

- 9.2.4. Low-k Precursor

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Precursor for Semiconductor Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. PVD/CVD/ALD

- 10.1.2. Epitaxial Growth and Etching, etc.

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Silicon Precursor

- 10.2.2. Metal Precursor

- 10.2.3. High-k Precursor

- 10.2.4. Low-k Precursor

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Precursor for Semiconductor Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. PVD/CVD/ALD

- 11.1.2. Epitaxial Growth and Etching, etc.

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Silicon Precursor

- 11.2.2. Metal Precursor

- 11.2.3. High-k Precursor

- 11.2.4. Low-k Precursor

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Merck Group

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Air Liquide

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 SK Materials

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 UP Chemical

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Entegris

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 ADEKA

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Hansol Chemical

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 DuPont

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 SoulBrain Co Ltd

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Nanmat

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 DNF Solutions

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Natachem

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Tanaka Kikinzoku

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Botai Electronic Material

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Gelest

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 Strem Chemicals

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 Anhui Adchem

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.18 EpiValence

- 12.1.18.1. Company Overview

- 12.1.18.2. Products

- 12.1.18.3. Company Financials

- 12.1.18.4. SWOT Analysis

- 12.1.19 FUJIFILM Corporation

- 12.1.19.1. Company Overview

- 12.1.19.2. Products

- 12.1.19.3. Company Financials

- 12.1.19.4. SWOT Analysis

- 12.1.20 Japan Advanced Chemicals

- 12.1.20.1. Company Overview

- 12.1.20.2. Products

- 12.1.20.3. Company Financials

- 12.1.20.4. SWOT Analysis

- 12.1.21 Wonik Materials

- 12.1.21.1. Company Overview

- 12.1.21.2. Products

- 12.1.21.3. Company Financials

- 12.1.21.4. SWOT Analysis

- 12.1.1 Merck Group

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Precursor for Semiconductor Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Precursor for Semiconductor Revenue (million), by Application 2025 & 2033

- Figure 3: North America Precursor for Semiconductor Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Precursor for Semiconductor Revenue (million), by Types 2025 & 2033

- Figure 5: North America Precursor for Semiconductor Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Precursor for Semiconductor Revenue (million), by Country 2025 & 2033

- Figure 7: North America Precursor for Semiconductor Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Precursor for Semiconductor Revenue (million), by Application 2025 & 2033

- Figure 9: South America Precursor for Semiconductor Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Precursor for Semiconductor Revenue (million), by Types 2025 & 2033

- Figure 11: South America Precursor for Semiconductor Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Precursor for Semiconductor Revenue (million), by Country 2025 & 2033

- Figure 13: South America Precursor for Semiconductor Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Precursor for Semiconductor Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Precursor for Semiconductor Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Precursor for Semiconductor Revenue (million), by Types 2025 & 2033

- Figure 17: Europe Precursor for Semiconductor Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Precursor for Semiconductor Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Precursor for Semiconductor Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Precursor for Semiconductor Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Precursor for Semiconductor Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Precursor for Semiconductor Revenue (million), by Types 2025 & 2033

- Figure 23: Middle East & Africa Precursor for Semiconductor Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Precursor for Semiconductor Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Precursor for Semiconductor Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Precursor for Semiconductor Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Precursor for Semiconductor Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Precursor for Semiconductor Revenue (million), by Types 2025 & 2033

- Figure 29: Asia Pacific Precursor for Semiconductor Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Precursor for Semiconductor Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Precursor for Semiconductor Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Precursor for Semiconductor Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Precursor for Semiconductor Revenue million Forecast, by Types 2020 & 2033

- Table 3: Global Precursor for Semiconductor Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Precursor for Semiconductor Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Precursor for Semiconductor Revenue million Forecast, by Types 2020 & 2033

- Table 6: Global Precursor for Semiconductor Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Precursor for Semiconductor Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Precursor for Semiconductor Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Precursor for Semiconductor Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Precursor for Semiconductor Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Precursor for Semiconductor Revenue million Forecast, by Types 2020 & 2033

- Table 12: Global Precursor for Semiconductor Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Precursor for Semiconductor Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Precursor for Semiconductor Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Precursor for Semiconductor Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Precursor for Semiconductor Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Precursor for Semiconductor Revenue million Forecast, by Types 2020 & 2033

- Table 18: Global Precursor for Semiconductor Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Precursor for Semiconductor Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Precursor for Semiconductor Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Precursor for Semiconductor Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Precursor for Semiconductor Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Precursor for Semiconductor Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Precursor for Semiconductor Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Precursor for Semiconductor Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Precursor for Semiconductor Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Precursor for Semiconductor Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Precursor for Semiconductor Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Precursor for Semiconductor Revenue million Forecast, by Types 2020 & 2033

- Table 30: Global Precursor for Semiconductor Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Precursor for Semiconductor Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Precursor for Semiconductor Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Precursor for Semiconductor Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Precursor for Semiconductor Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Precursor for Semiconductor Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Precursor for Semiconductor Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Precursor for Semiconductor Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Precursor for Semiconductor Revenue million Forecast, by Types 2020 & 2033

- Table 39: Global Precursor for Semiconductor Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Precursor for Semiconductor Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Precursor for Semiconductor Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Precursor for Semiconductor Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Precursor for Semiconductor Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Precursor for Semiconductor Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Precursor for Semiconductor Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Precursor for Semiconductor Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Precursor for Semiconductor?

The projected CAGR is approximately XX%.

2. Which companies are prominent players in the Precursor for Semiconductor?

Key companies in the market include Merck Group, Air Liquide, SK Materials, UP Chemical, Entegris, ADEKA, Hansol Chemical, DuPont, SoulBrain Co Ltd, Nanmat, DNF Solutions, Natachem, Tanaka Kikinzoku, Botai Electronic Material, Gelest, Strem Chemicals, Anhui Adchem, EpiValence, FUJIFILM Corporation, Japan Advanced Chemicals, Wonik Materials.

3. What are the main segments of the Precursor for Semiconductor?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4350.00, USD 6525.00, and USD 8700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Precursor for Semiconductor," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Precursor for Semiconductor report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Precursor for Semiconductor?

To stay informed about further developments, trends, and reports in the Precursor for Semiconductor, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence