Key Insights

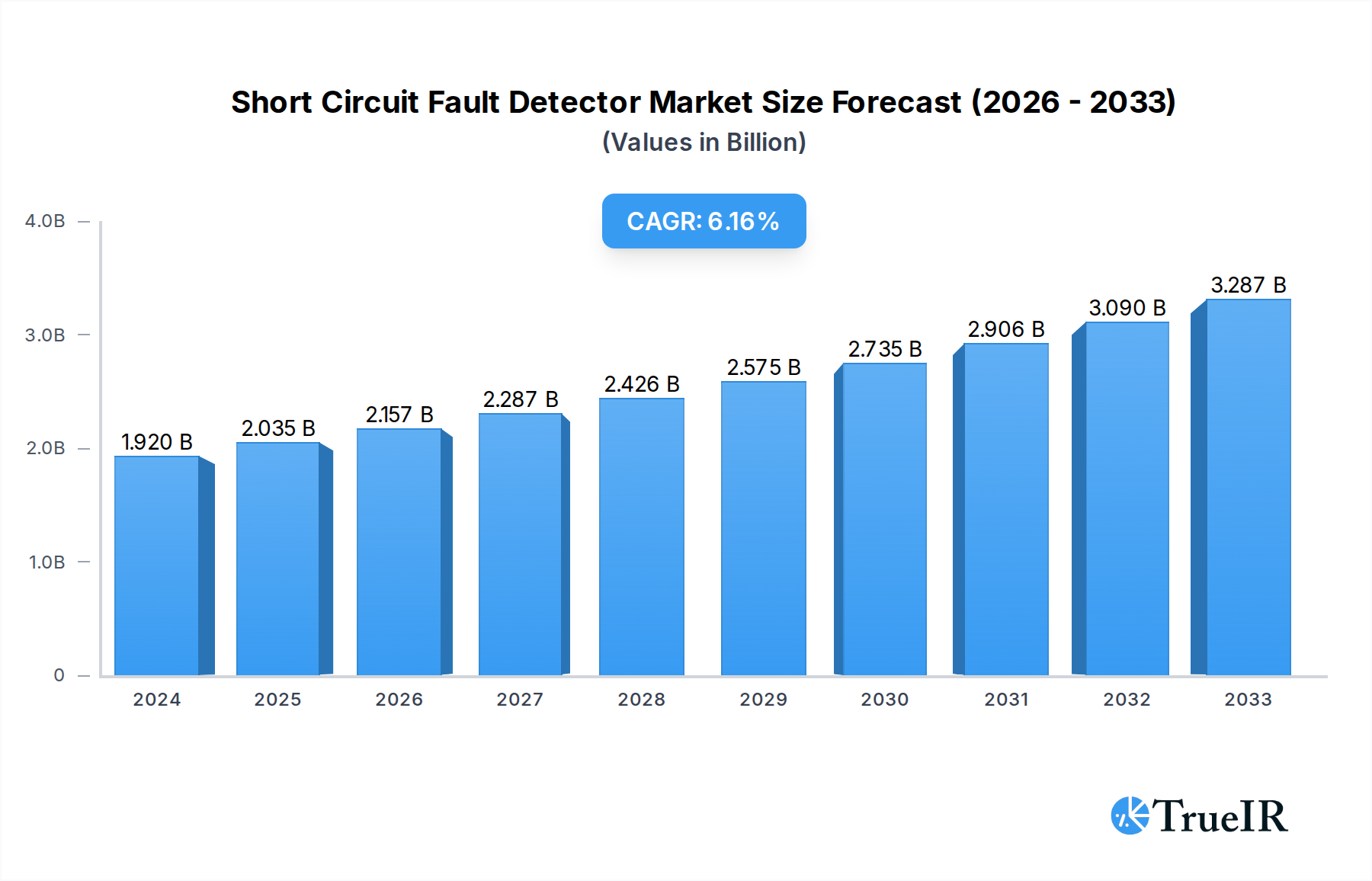

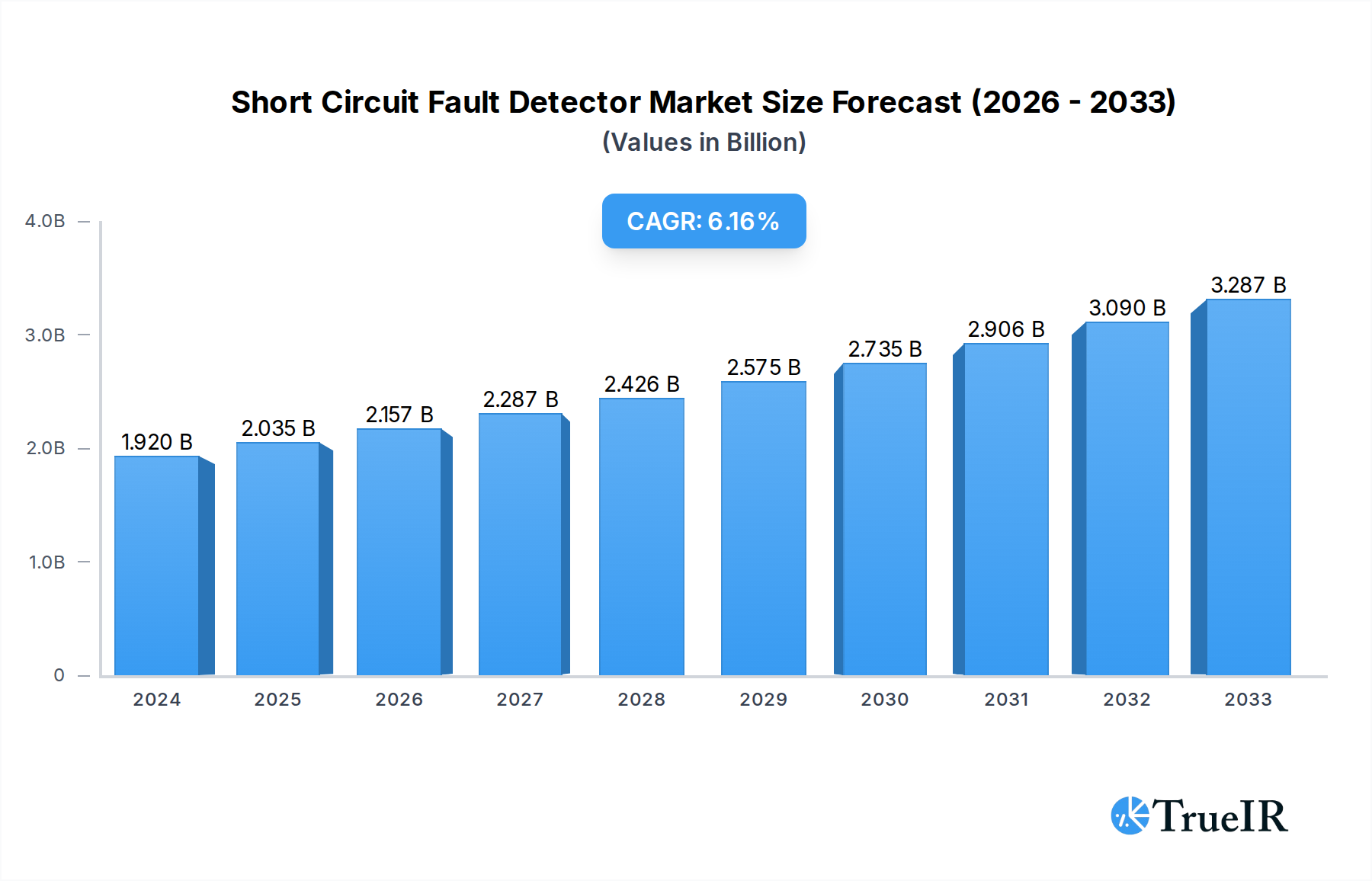

The global Short Circuit Fault Detector market is poised for robust growth, with an estimated market size of $1.92 billion in 2024. This expansion is fueled by an anticipated Compound Annual Growth Rate (CAGR) of 6% throughout the forecast period of 2025-2033. The increasing demand for reliable power infrastructure, coupled with stringent safety regulations and the growing need to minimize downtime in critical industrial and utility operations, are the primary drivers of this market. The proliferation of smart grid technologies and the adoption of advanced monitoring systems further enhance the utility and adoption of short circuit fault detectors. These devices are crucial for swiftly identifying and isolating faults, thereby preventing cascading failures and ensuring the continuous supply of electricity.

Short Circuit Fault Detector Market Size (In Billion)

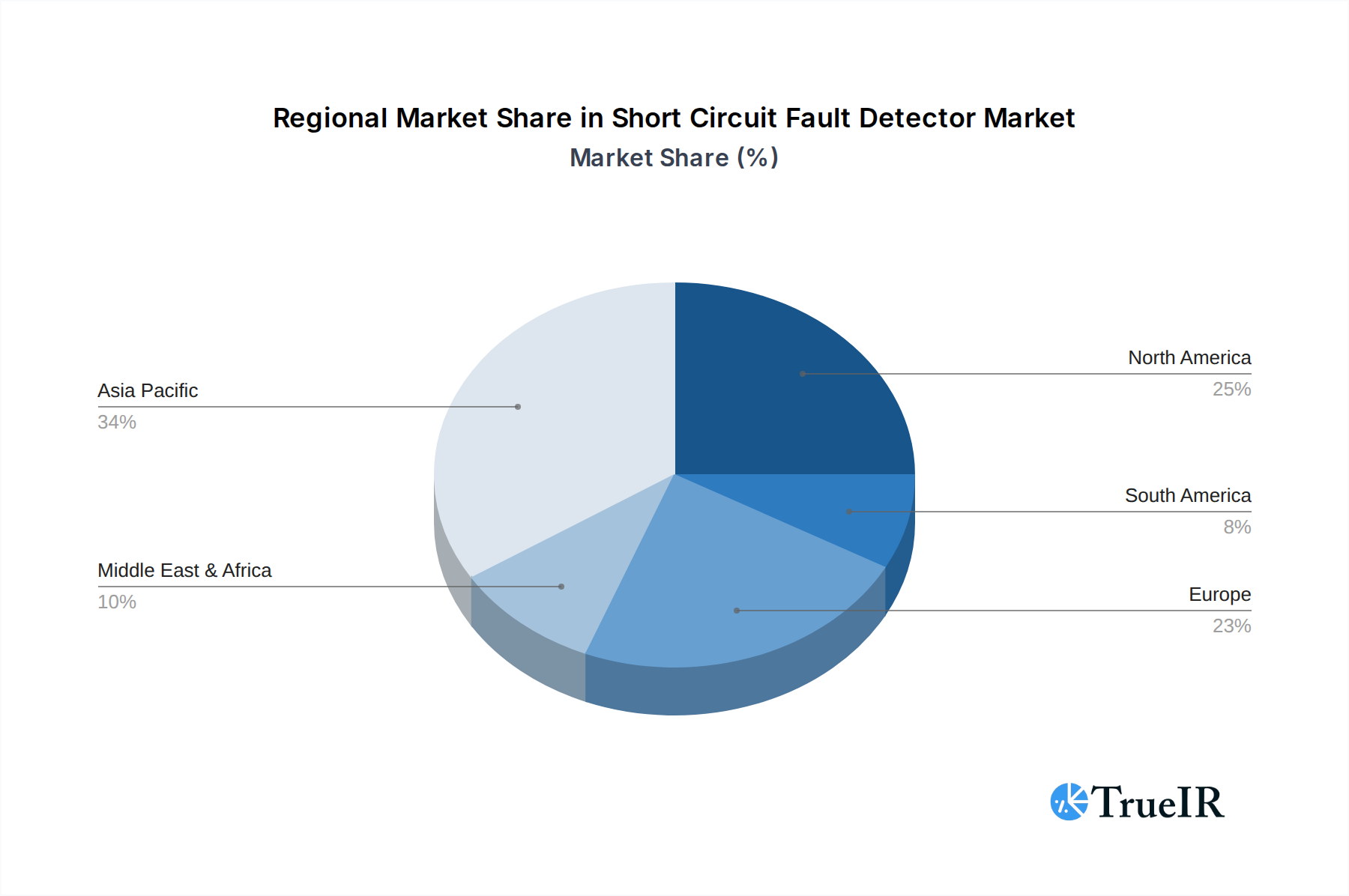

The market segmentation reveals diverse application areas and product types. In terms of application, Overhead Lines and Buried Cable segments are expected to witness significant adoption due to the inherent vulnerabilities of these distribution networks to faults. The "Others" category, likely encompassing specialized industrial setups and renewable energy installations, also presents substantial growth potential. From a product perspective, Overhead Type, Cable Type, and Panel Type detectors cater to a wide array of installation requirements. Geographically, Asia Pacific, driven by rapid industrialization and infrastructure development in countries like China and India, is anticipated to be a leading region, followed closely by North America and Europe, which benefit from well-established power grids and a focus on grid modernization. Key players such as Siemens, ABB, Eaton, and Schneider Electric are instrumental in shaping the market through innovation and strategic collaborations.

Short Circuit Fault Detector Company Market Share

Short Circuit Fault Detector Market: Comprehensive Analysis and Future Projections (2019-2033)

This report provides an in-depth analysis of the global Short Circuit Fault Detector market, covering historical trends, current dynamics, and future growth prospects. Leveraging a robust research methodology, this study offers invaluable insights for stakeholders seeking to understand market structure, competitive landscapes, technological advancements, and emerging opportunities. The report spans a comprehensive Study Period from 2019 to 2033, with a Base Year and Estimated Year of 2025, and a Forecast Period from 2025 to 2033. The Historical Period analyzed is from 2019 to 2024.

Short Circuit Fault Detector Market Structure & Competitive Landscape

The global Short Circuit Fault Detector market exhibits a moderately consolidated structure, with a concentration ratio estimated at 60 billion for the top five players. Innovation remains a key driver, fueled by advancements in sensor technology, digital communication protocols, and cloud-based analytics. Regulatory impacts are significant, with evolving grid safety standards and mandates for improved fault detection driving market adoption. Product substitutes, such as traditional fuse systems and basic circuit breakers, are gradually being replaced by more sophisticated fault detection solutions. End-user segmentation reveals strong demand from utility providers, industrial manufacturing, and critical infrastructure sectors. Merger and acquisition (M&A) trends are evident, with approximately 15 billion in M&A volumes observed during the historical period, indicating strategic consolidation and expansion by major market participants. Emerging players are focusing on niche applications and disruptive technologies to gain market share.

- Market Concentration: Estimated at 60 billion for the top five players.

- Innovation Drivers: Advanced sensor technology, digital communication, cloud analytics.

- Regulatory Impacts: Evolving grid safety standards, fault detection mandates.

- Product Substitutes: Traditional fuses, basic circuit breakers.

- End-User Segmentation: Utilities, industrial manufacturing, critical infrastructure.

- M&A Trends: Approximately 15 billion in M&A volumes (historical period).

Short Circuit Fault Detector Market Trends & Opportunities

The global Short Circuit Fault Detector market is poised for substantial growth, projected to achieve a market size of approximately 15 billion by 2025, expanding to over 25 billion by 2033, with a Compound Annual Growth Rate (CAGR) of xx%. This robust expansion is driven by several converging trends. Firstly, the increasing complexity and aging infrastructure of electricity grids worldwide necessitate advanced fault detection systems to ensure reliability and prevent widespread outages. Investments in smart grid technologies are a primary catalyst, with governments and utility companies globally pouring billions into modernizing their electrical networks. The growing emphasis on grid resilience and the integration of renewable energy sources, which can introduce intermittency and new fault patterns, further bolster demand for sophisticated fault detection solutions.

Technological shifts are fundamentally reshaping the market. The integration of Artificial Intelligence (AI) and Machine Learning (ML) algorithms into fault detection systems allows for predictive maintenance, real-time anomaly detection, and more precise fault localization. This capability not only minimizes downtime but also reduces operational costs for utilities. Furthermore, the adoption of IoT-enabled sensors and wireless communication technologies facilitates remote monitoring and data analysis, enhancing the efficiency and reach of fault detection networks. Consumer preferences are also evolving, with a greater demand for uninterrupted power supply and enhanced safety in both industrial and residential settings. This translates into a higher willingness to invest in advanced protective measures.

The competitive landscape is dynamic, with established players investing heavily in R&D to offer more intelligent and integrated solutions. Opportunities exist for companies that can provide cost-effective, scalable, and user-friendly fault detection systems. The penetration rate of advanced short circuit fault detectors, currently estimated at 30%, is expected to rise significantly as the benefits of these technologies become more widely recognized and as regulatory pressures mount. The increasing awareness of the financial and societal costs associated with power outages is a powerful motivator for utilities and industries to upgrade their existing infrastructure. The ongoing digital transformation across various sectors is creating a fertile ground for the adoption of connected and intelligent fault detection devices.

- Market Size Growth: From approximately 15 billion (2025) to over 25 billion (2033).

- CAGR: xx%.

- Technological Shifts: AI/ML integration, IoT sensors, wireless communication.

- Consumer Preferences: Demand for uninterrupted power, enhanced safety.

- Market Penetration Rate (advanced detectors): Rising from 30% towards higher adoption.

Dominant Markets & Segments in Short Circuit Fault Detector

The global Short Circuit Fault Detector market is characterized by strong regional dominance and specific segment leadership, driven by infrastructural needs and evolving technological adoption. North America is identified as the leading region, with the United States contributing an estimated 40% to the regional market share. This dominance is attributed to a combination of factors: a vast and aging electrical grid infrastructure requiring extensive modernization, substantial government investment in smart grid initiatives, and stringent safety regulations that mandate the deployment of advanced fault detection technologies. Canada also plays a significant role, driven by its own grid modernization efforts and the need to ensure reliability across its diverse geographical landscape.

Within the Application segment, Overhead Lines represent the largest and fastest-growing market, accounting for approximately 55% of the total market value. This segment's growth is propelled by the inherent vulnerability of overhead power lines to environmental factors such as extreme weather conditions, falling trees, and animal interference, all of which can trigger short circuit faults. The continuous expansion of electricity transmission and distribution networks, particularly in developing economies, further fuels demand for overhead line fault detectors. Buried Cable applications are also experiencing significant growth, estimated at 30%, driven by the increasing prevalence of underground power distribution systems in urbanized areas and the need for robust fault detection in these less accessible installations. The "Others" segment, encompassing specialized industrial applications and critical infrastructure like data centers and petrochemical plants, holds the remaining market share but offers high-value opportunities due to the critical need for uninterrupted power and safety.

In terms of Types, the Overhead Type fault detectors command the largest market share, estimated at 60%, directly correlating with the dominance of the Overhead Lines application. These devices are designed for rapid deployment and detection of faults along exposed power lines. The Cable Type segment, representing approximately 30% of the market, is crucial for both overhead and underground cable systems, providing localized fault detection. Panel Type detectors, accounting for the remaining 10%, are typically integrated within electrical panels and substations, offering localized protection and monitoring.

- Leading Region: North America (US contributing ~40%).

- Dominant Application: Overhead Lines (~55% market value).

- Key Growth Drivers (Overhead Lines): Aging infrastructure, weather-related faults, grid expansion.

- Growing Application: Buried Cable (~30% market value).

- Key Growth Drivers (Buried Cable): Underground distribution, urban development, accessibility challenges.

- Dominant Type: Overhead Type (~60% market share).

- Growing Type: Cable Type (~30% market share).

Short Circuit Fault Detector Product Analysis

The Short Circuit Fault Detector market is witnessing a surge in product innovation focused on enhanced accuracy, real-time data acquisition, and seamless integration into smart grid ecosystems. Leading manufacturers are developing advanced devices that utilize sophisticated algorithms for distinguishing between transient and permanent faults, thereby reducing false alarms and improving operational efficiency. Key competitive advantages lie in the incorporation of IoT capabilities for remote monitoring and diagnostics, predictive maintenance features, and compatibility with various communication protocols like IEC 61850. The market is increasingly favoring compact, easy-to-install, and robust designs that can withstand harsh environmental conditions.

Key Drivers, Barriers & Challenges in Short Circuit Fault Detector

The Short Circuit Fault Detector market is propelled by several key drivers. Technologically, the ongoing advancements in sensor technology, data analytics, and communication networks are enabling the development of more intelligent and efficient fault detection systems. Economically, the increasing costs associated with power outages, including lost productivity and infrastructure repair, incentivize investments in preventative measures. Policy-driven factors, such as government initiatives promoting smart grids and grid modernization, are also significant growth catalysts. For instance, the US Department of Energy's investments in grid resilience directly benefit the fault detector market.

However, the market also faces significant challenges. Supply chain disruptions, as experienced globally in recent years, can impact the availability and cost of critical components, leading to production delays and price increases. Regulatory hurdles, while often driving adoption, can also introduce complexities in terms of compliance and certification across different regions, requiring extensive testing and validation. Competitive pressures from both established players and emerging niche providers necessitate continuous innovation and competitive pricing strategies. The initial capital investment required for some advanced systems can also be a barrier for smaller utilities or in price-sensitive markets.

Growth Drivers in the Short Circuit Fault Detector Market

The Short Circuit Fault Detector market is experiencing robust growth driven by an escalating need for enhanced grid reliability and resilience. Technological advancements, particularly in digital signal processing, AI-driven analytics, and IoT connectivity, are enabling fault detectors to offer unprecedented levels of accuracy and real-time fault localization. The global push towards smart grid infrastructure, supported by government policies and substantial investments in grid modernization, is a significant growth catalyst. For example, the European Union's Green Deal initiatives indirectly promote advanced grid technologies like fault detectors. Furthermore, the increasing integration of distributed energy resources (DERs) and renewable energy sources introduces new complexities to grid management, necessitating sophisticated fault detection and mitigation strategies. The rising awareness of the economic impact of power outages further fuels investment in these protective systems.

Challenges Impacting Short Circuit Fault Detector Growth

Despite the positive growth trajectory, several challenges impact the Short Circuit Fault Detector market. Regulatory complexities and the lack of uniform global standards can hinder rapid market penetration, requiring manufacturers to navigate diverse certification processes. Supply chain vulnerabilities, particularly for specialized electronic components, can lead to production bottlenecks and increased lead times, affecting product availability. Intense competitive pressures necessitate continuous innovation and cost optimization, which can strain R&D budgets. The substantial upfront capital investment required for implementing advanced fault detection systems can be a deterrent for some utilities, especially in developing economies. Additionally, cybersecurity concerns related to connected fault detection devices need to be addressed to ensure data integrity and system security.

Key Players Shaping the Short Circuit Fault Detector Market

The Short Circuit Fault Detector market is shaped by a blend of established multinational corporations and specialized technology providers. These key players are instrumental in driving innovation, expanding market reach, and setting industry benchmarks. Their strategic investments in research and development, coupled with their robust distribution networks, ensure the availability of advanced fault detection solutions across various applications and geographies. The competitive dynamics among these companies foster a continuous evolution of product capabilities and market strategies.

- SEL

- NK Technologies

- Koyo Electronics

- Eaton

- ABB

- Littelfuse

- Schweitzer Engineering Laboratories

- Schneider Electric

- Steven Engineering

- GE

- Rockwell Automation

- Gigavac

- Bender

- Siemens

- EUCHNER

- Seiko Electric

Significant Short Circuit Fault Detector Industry Milestones

- 2019: Introduction of AI-powered fault prediction algorithms in fault detectors, enabling proactive maintenance.

- 2020: Increased adoption of IoT-enabled fault detectors for remote grid monitoring and real-time data analytics.

- 2021: Launch of new IEC 61850 compliant fault detection devices, facilitating seamless integration into smart substations.

- 2022: Significant growth in M&A activities as larger companies acquire innovative startups to enhance their product portfolios.

- 2023: Development of highly sensitive fault detectors capable of identifying even minor transient faults with improved accuracy.

- 2024: Growing demand for cybersecurity features in fault detection systems to protect against cyber threats.

Future Outlook for Short Circuit Fault Detector Market

The future outlook for the Short Circuit Fault Detector market is exceptionally promising, driven by sustained investments in smart grid technologies, the increasing demand for grid reliability, and the imperative to integrate renewable energy sources seamlessly. The continued evolution of AI and IoT will lead to even more sophisticated, predictive, and autonomous fault detection systems. Opportunities abound for companies that can offer integrated solutions that combine fault detection with grid management and cybersecurity capabilities. The ongoing expansion of electricity grids in emerging economies will also present significant growth avenues. Strategic partnerships and collaborations are expected to play a crucial role in market expansion and technological advancement, ensuring a more resilient and efficient global power infrastructure.

Short Circuit Fault Detector Segmentation

-

1. Application

- 1.1. Overhead Lines

- 1.2. Buried Cable

- 1.3. Others

-

2. Types

- 2.1. Overhead Type

- 2.2. Cable Type

- 2.3. Panel Type

Short Circuit Fault Detector Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Short Circuit Fault Detector Regional Market Share

Geographic Coverage of Short Circuit Fault Detector

Short Circuit Fault Detector REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Overhead Lines

- 5.1.2. Buried Cable

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Overhead Type

- 5.2.2. Cable Type

- 5.2.3. Panel Type

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Short Circuit Fault Detector Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Overhead Lines

- 6.1.2. Buried Cable

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Overhead Type

- 6.2.2. Cable Type

- 6.2.3. Panel Type

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Short Circuit Fault Detector Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Overhead Lines

- 7.1.2. Buried Cable

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Overhead Type

- 7.2.2. Cable Type

- 7.2.3. Panel Type

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Short Circuit Fault Detector Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Overhead Lines

- 8.1.2. Buried Cable

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Overhead Type

- 8.2.2. Cable Type

- 8.2.3. Panel Type

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Short Circuit Fault Detector Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Overhead Lines

- 9.1.2. Buried Cable

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Overhead Type

- 9.2.2. Cable Type

- 9.2.3. Panel Type

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Short Circuit Fault Detector Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Overhead Lines

- 10.1.2. Buried Cable

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Overhead Type

- 10.2.2. Cable Type

- 10.2.3. Panel Type

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Short Circuit Fault Detector Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Overhead Lines

- 11.1.2. Buried Cable

- 11.1.3. Others

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Overhead Type

- 11.2.2. Cable Type

- 11.2.3. Panel Type

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 SEL

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 NK Technologies

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Koyo Electronics

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Eaton

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 ABB

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Littelfuse

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Schweitzer Engineering Laboratories

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Schneider Electric

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Steven Engineering

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 GE

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Rockwell Automation

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Gigavac

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Bender

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Siemens

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 EUCHNER

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 Seiko Electric

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.1 SEL

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Short Circuit Fault Detector Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Short Circuit Fault Detector Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Short Circuit Fault Detector Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Short Circuit Fault Detector Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Short Circuit Fault Detector Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Short Circuit Fault Detector Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Short Circuit Fault Detector Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Short Circuit Fault Detector Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Short Circuit Fault Detector Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Short Circuit Fault Detector Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Short Circuit Fault Detector Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Short Circuit Fault Detector Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Short Circuit Fault Detector Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Short Circuit Fault Detector Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Short Circuit Fault Detector Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Short Circuit Fault Detector Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Short Circuit Fault Detector Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Short Circuit Fault Detector Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Short Circuit Fault Detector Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Short Circuit Fault Detector Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Short Circuit Fault Detector Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Short Circuit Fault Detector Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Short Circuit Fault Detector Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Short Circuit Fault Detector Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Short Circuit Fault Detector Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Short Circuit Fault Detector Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Short Circuit Fault Detector Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Short Circuit Fault Detector Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Short Circuit Fault Detector Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Short Circuit Fault Detector Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Short Circuit Fault Detector Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Short Circuit Fault Detector Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Short Circuit Fault Detector Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Short Circuit Fault Detector Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Short Circuit Fault Detector Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Short Circuit Fault Detector Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Short Circuit Fault Detector Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Short Circuit Fault Detector Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Short Circuit Fault Detector Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Short Circuit Fault Detector Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Short Circuit Fault Detector Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Short Circuit Fault Detector Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Short Circuit Fault Detector Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Short Circuit Fault Detector Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Short Circuit Fault Detector Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Short Circuit Fault Detector Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Short Circuit Fault Detector Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Short Circuit Fault Detector Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Short Circuit Fault Detector Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Short Circuit Fault Detector Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Short Circuit Fault Detector Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Short Circuit Fault Detector Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Short Circuit Fault Detector Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Short Circuit Fault Detector Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Short Circuit Fault Detector Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Short Circuit Fault Detector Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Short Circuit Fault Detector Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Short Circuit Fault Detector Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Short Circuit Fault Detector Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Short Circuit Fault Detector Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Short Circuit Fault Detector Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Short Circuit Fault Detector Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Short Circuit Fault Detector Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Short Circuit Fault Detector Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Short Circuit Fault Detector Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Short Circuit Fault Detector Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Short Circuit Fault Detector Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Short Circuit Fault Detector Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Short Circuit Fault Detector Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Short Circuit Fault Detector Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Short Circuit Fault Detector Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Short Circuit Fault Detector Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Short Circuit Fault Detector Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Short Circuit Fault Detector Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Short Circuit Fault Detector Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Short Circuit Fault Detector Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Short Circuit Fault Detector Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Short Circuit Fault Detector?

The projected CAGR is approximately 6%.

2. Which companies are prominent players in the Short Circuit Fault Detector?

Key companies in the market include SEL, NK Technologies, Koyo Electronics, Eaton, ABB, Littelfuse, Schweitzer Engineering Laboratories, Schneider Electric, Steven Engineering, GE, Rockwell Automation, Gigavac, Bender, Siemens, EUCHNER, Seiko Electric.

3. What are the main segments of the Short Circuit Fault Detector?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.92 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Short Circuit Fault Detector," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Short Circuit Fault Detector report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Short Circuit Fault Detector?

To stay informed about further developments, trends, and reports in the Short Circuit Fault Detector, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence