Key Insights

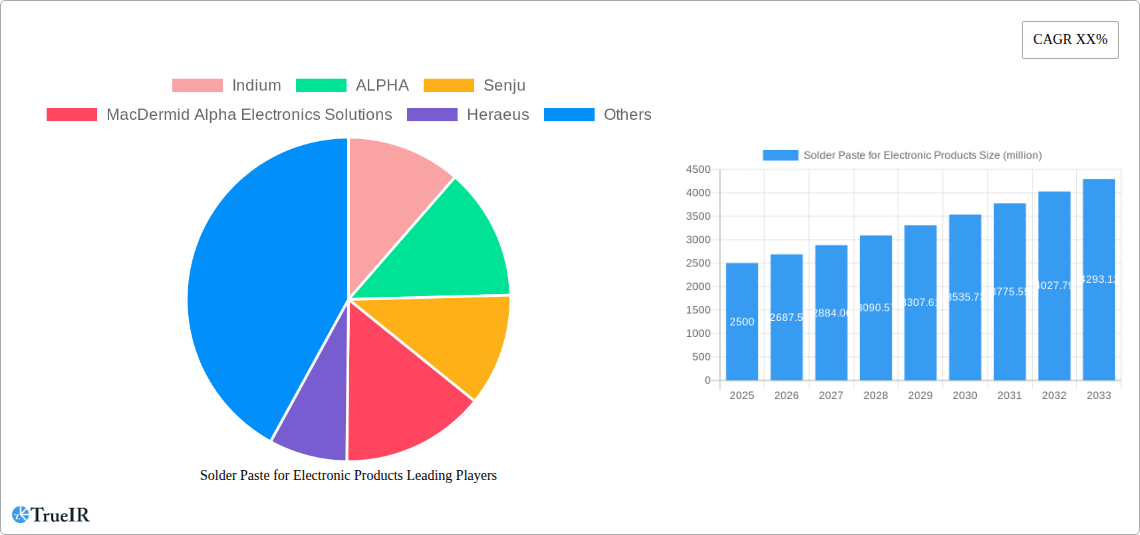

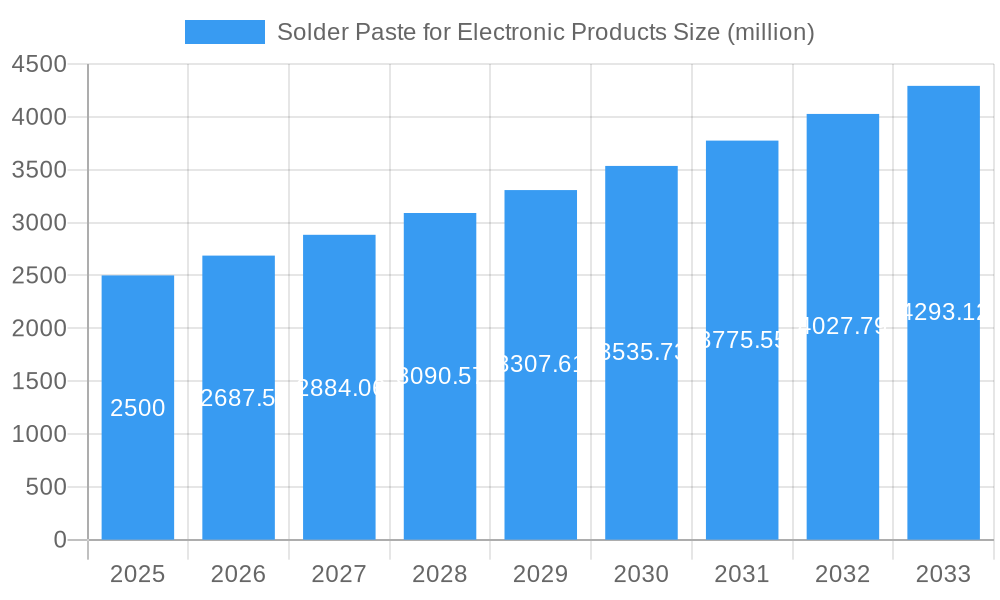

The global Solder Paste for Electronic Products market is poised for robust expansion, driven by the ever-increasing demand for advanced consumer electronics and the burgeoning automotive sector. With an estimated market size of USD 2.5 billion in 2025, the industry is projected to experience a Compound Annual Growth Rate (CAGR) of 7.5%, reaching approximately USD 4.0 billion by 2033. This growth is underpinned by significant drivers such as the miniaturization of electronic components, the proliferation of 5G technology, and the increasing adoption of electric and autonomous vehicles, all of which necessitate sophisticated soldering solutions. The market's value is predominantly denominated in millions of USD, reflecting the scale of production and the specialized nature of these materials.

Solder Paste for Electronic Products Market Size (In Billion)

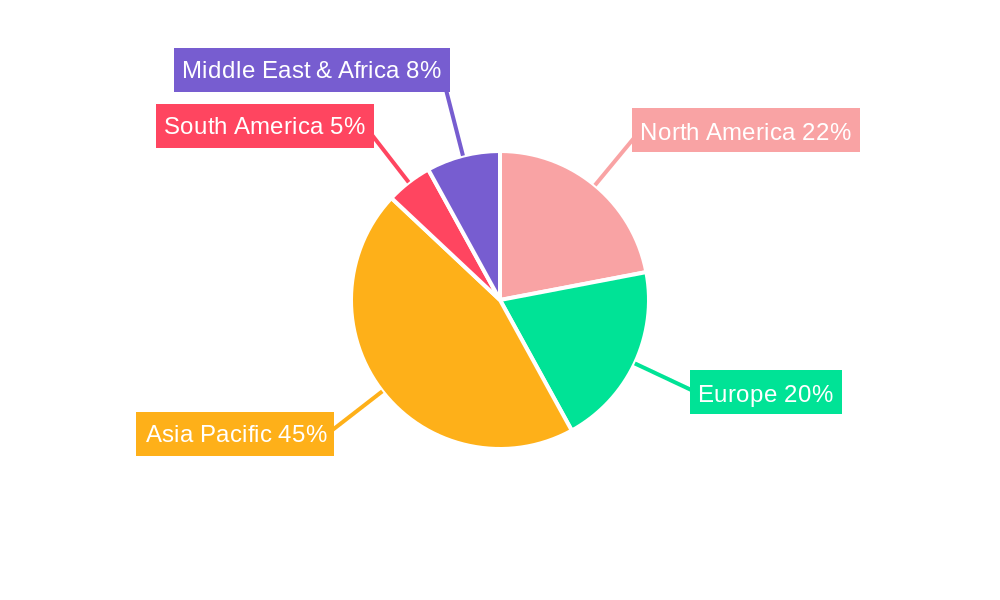

The market is segmented into Rosin Based Pastes, Water Soluble Pastes, and No-clean Pastes, with Rosin Based Pastes currently holding a dominant share due to their versatility and cost-effectiveness in consumer electronics. Application-wise, Consumer Electronics accounts for the largest segment, followed closely by Vehicle Electronics, which is exhibiting a higher growth trajectory due to the increasing electronic content in modern vehicles. While the market presents substantial opportunities, potential restraints include the rising cost of raw materials, particularly precious metals, and the stringent environmental regulations surrounding the use of certain flux materials. Nevertheless, continuous innovation in solder paste formulations, focusing on improved thermal performance, higher reliability, and eco-friendliness, is expected to mitigate these challenges and fuel sustained market growth across key regions like Asia Pacific, North America, and Europe. Key players such as Indium Corporation, ALPHA, Senju Metal Industry, MacDermid Alpha Electronics Solutions, and Heraeus continue to drive innovation and expand their market presence.

Solder Paste for Electronic Products Company Market Share

Dynamic & SEO-Optimized Report: Solder Paste for Electronic Products Market Analysis (2019-2033)

This comprehensive report offers an in-depth analysis of the global Solder Paste for Electronic Products market, covering historical trends, current dynamics, and future projections from 2019 to 2033. Leveraging high-volume keywords relevant to electronic manufacturing and materials science, this report is meticulously crafted for optimal search engine visibility and to provide actionable insights for industry stakeholders. With a base year of 2025 and an estimated year also set at 2025, the forecast period extends from 2025 to 2033, building upon detailed historical data from 2019-2024.

Solder Paste for Electronic Products Market Structure & Competitive Landscape

The Solder Paste for Electronic Products market is characterized by a moderately concentrated structure, with several key global players vying for market share. Innovation drivers such as miniaturization in consumer electronics and the increasing demand for high-reliability components in vehicle electronics are fueling research and development. Regulatory impacts, particularly concerning environmental compliance and the use of lead-free solder pastes, are significant influencing factors shaping product development and market entry strategies. Product substitutes, while present in niche applications, are generally unable to match the performance and cost-effectiveness of advanced solder pastes for mainstream electronics assembly. End-user segmentation reveals a strong reliance on the Consumer Electronics and Vehicle Electronics sectors, with Other applications showing steady growth. Merger and acquisition (M&A) trends are evident as larger companies seek to expand their product portfolios and geographical reach. For instance, in the historical period (2019-2024), there were an estimated 7 significant M&A activities. Concentration ratios, based on revenue, indicate that the top 5 players hold approximately 65% of the market. Key strategies employed by leading companies include technological differentiation, strategic partnerships, and a focus on sustainable product offerings.

Solder Paste for Electronic Products Market Trends & Opportunities

The global Solder Paste for Electronic Products market is experiencing robust growth, driven by the insatiable demand for advanced electronic devices across various sectors. The market size, projected to reach xx million USD in 2025, is anticipated to grow at a Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033). This expansion is fueled by continuous technological shifts, including the adoption of advanced packaging techniques like System-in-Package (SiP) and 2.5D/3D IC integration, which necessitate highly specialized solder pastes with precise flux formulations and fine particle sizes. Consumer preferences for smaller, more powerful, and energy-efficient electronic gadgets, from smartphones and wearables to advanced computing devices, directly translate into an increased need for high-performance solder pastes.

Competitive dynamics are intensifying, with companies focusing on developing solder pastes that offer superior joint reliability, reduced voiding, and improved thermal performance. The burgeoning electric vehicle (EV) market is a significant growth catalyst, demanding solder pastes that can withstand higher operating temperatures and vibration stresses. The increasing complexity of automotive electronics, including advanced driver-assistance systems (ADAS) and in-car infotainment, further amplifies this demand. Furthermore, the Internet of Things (IoT) ecosystem, encompassing smart homes, industrial automation, and connected infrastructure, represents a vast and rapidly expanding opportunity for solder paste manufacturers. The penetration rate of lead-free solder pastes has surpassed 90% globally, with ongoing research focused on improving their performance characteristics and addressing potential environmental concerns. Opportunities also lie in developing specialized solder pastes for emerging applications such as flexible electronics, medical devices requiring biocompatibility, and advanced aerospace components. The pursuit of higher assembly yields and reduced manufacturing costs continues to drive innovation in solder paste formulations, leading to the development of advanced alloys and flux systems designed for next-generation manufacturing processes.

Dominant Markets & Segments in Solder Paste for Electronic Products

The Consumer Electronics segment stands as the dominant market within the Solder Paste for Electronic Products landscape, accounting for an estimated xx% of the total market share in 2025. This dominance is driven by the relentless innovation and high-volume production of devices such as smartphones, laptops, tablets, televisions, and gaming consoles. The rapid pace of product cycles in this sector necessitates a consistent supply of advanced solder pastes to support the ever-increasing demands for miniaturization, higher performance, and improved reliability. Key growth drivers in this segment include the global proliferation of internet connectivity, the growing middle class in emerging economies, and the constant consumer desire for the latest technological advancements. Policies promoting digital infrastructure development and the adoption of smart devices further bolster this segment's importance.

The Vehicle Electronics segment represents the second-largest and fastest-growing application, projected to witness a CAGR of xx% during the forecast period. The automotive industry's transformation towards electrification, autonomous driving, and enhanced in-car connectivity is a primary growth catalyst. The increasing number of electronic control units (ECUs), sensors, and advanced infotainment systems in modern vehicles requires highly reliable and robust solder paste solutions capable of withstanding harsh operating conditions, including extreme temperatures and vibrations. Government initiatives supporting electric vehicle adoption and stricter safety regulations demanding advanced automotive electronics contribute significantly to this segment's expansion.

Among the product types, No-clean Pastes currently hold the largest market share due to their convenience and efficiency in manufacturing processes, minimizing post-solder cleaning requirements, which is crucial for high-volume production. However, Rosin Based Pastes continue to be significant, particularly in applications requiring high reliability and specific flux properties. Water Soluble Pastes, while having a smaller market share, are gaining traction in specialized applications where stringent cleaning is paramount. The dominance of Consumer Electronics and the rapid growth in Vehicle Electronics segments are directly influencing the demand for specific solder paste types, with a growing emphasis on lead-free, high-reliability formulations.

Solder Paste for Electronic Products Product Analysis

Product innovations in Solder Paste for Electronic Products are primarily focused on enhancing performance and addressing the evolving demands of advanced electronics manufacturing. Key advancements include the development of solder pastes with extremely fine particle sizes for high-density interconnects (HDIs), improved flux chemistries for void-free soldering and enhanced wettability, and formulations optimized for high-temperature applications prevalent in automotive and industrial electronics. The competitive advantage of these products lies in their ability to enable higher assembly yields, improved device reliability, and compatibility with advanced manufacturing processes such as selective soldering and reflow soldering at lower temperatures.

Key Drivers, Barriers & Challenges in Solder Paste for Electronic Products

Key Drivers, Barriers & Challenges in Solder Paste for Electronic Products

The Solder Paste for Electronic Products market is propelled by several key drivers. The relentless miniaturization and increasing complexity of electronic devices, particularly in consumer electronics and automotive applications, create a constant demand for solder pastes that can facilitate fine-pitch soldering and high-density interconnects. Technological advancements in semiconductor packaging, such as System-in-Package (SiP) and 3D ICs, necessitate solder pastes with superior performance characteristics. Government initiatives promoting digitalization, smart manufacturing, and electric vehicle adoption also significantly fuel market growth. Furthermore, the growing adoption of Industry 4.0 principles, emphasizing automation and efficiency in manufacturing, drives the demand for highly reliable and process-friendly solder pastes.

However, the market faces significant barriers and challenges. Stringent environmental regulations, particularly regarding the use of lead and other hazardous materials, necessitate continuous innovation in lead-free solder paste formulations, which can sometimes be more expensive or require process adjustments. Supply chain disruptions, as experienced in recent years, can impact the availability and cost of raw materials, affecting production and pricing. Intense competition among a large number of players, including both established global giants and regional manufacturers, can lead to price pressures. Moreover, the need for significant investment in research and development to keep pace with technological advancements and evolving industry standards poses a challenge for smaller companies. The increasing complexity of electronic products also requires specialized solder paste solutions, creating a barrier for manufacturers not equipped to offer such tailored products.

Growth Drivers in the Solder Paste for Electronic Products Market

The Solder Paste for Electronic Products market is experiencing significant growth driven by multifaceted factors. Technologically, the relentless pursuit of smaller, more powerful, and energy-efficient electronic devices, especially in the Consumer Electronics sector, fuels demand for solder pastes capable of handling fine-pitch soldering and high-density interconnects. The automotive industry's rapid transition towards electrification and autonomous driving technologies is another major growth catalyst, requiring high-reliability solder pastes for complex electronic systems that can withstand extreme operating conditions. Economically, the expanding middle class in emerging economies is increasing disposable income, leading to higher consumer spending on electronic gadgets. Regulatory factors, such as government mandates promoting the adoption of electric vehicles and investments in digital infrastructure, further stimulate market expansion. The proliferation of the Internet of Things (IoT) across various sectors, from smart homes to industrial automation, also creates a substantial and growing demand for diverse solder paste applications.

Challenges Impacting Solder Paste for Electronic Products Growth

Several challenges are impacting the growth of the Solder Paste for Electronic Products market. Regulatory complexities surrounding material compositions, especially the ongoing scrutiny of lead content and the development of environmentally friendly alternatives, can necessitate costly retooling and research. Supply chain issues, including the volatility of raw material prices and availability for key components like tin and silver, can lead to production delays and increased costs. Competitive pressures from a fragmented market with numerous global and regional players often result in price erosion and reduced profit margins for manufacturers. The rapid pace of technological change in end-user industries requires continuous and substantial investment in research and development to keep pace, posing a significant financial challenge. Furthermore, ensuring consistent quality and performance across diverse application requirements, from delicate consumer electronics to robust automotive systems, demands sophisticated quality control measures and specialized product formulations.

Key Players Shaping the Solder Paste for Electronic Products Market

- Indium

- ALPHA

- Senju

- MacDermid Alpha Electronics Solutions

- Heraeus

- Tamura

- Henkel

- Inventec

- KOKI

- AIM

- Nihon Superior

- KAWADA

- Yashida

- Ishikawa

- DS HiMetal

- Shengmao

- Tongfang Tech

- Yong An

- U-bond Technology Inc

- Jissyu Solder

- Shenzhen Vital New Material

Significant Solder Paste for Electronic Products Industry Milestones

- 2019: Increased focus on ultra-fine pitch solder paste development to support 5G device miniaturization.

- 2020: Growing adoption of water-soluble solder pastes for advanced packaging applications requiring exceptional cleaning performance.

- 2021: Significant M&A activity, with larger players acquiring specialized solder paste manufacturers to expand portfolios.

- 2022: Enhanced development of high-reliability solder pastes for electric vehicle (EV) battery systems and power electronics.

- 2023: Advancements in no-clean solder paste formulations to achieve lower flux residue and improved electrical reliability.

- Early 2024: Introduction of solder pastes with improved thermal conductivity for advanced cooling solutions in high-performance computing.

- Mid-2024: Increased research into sustainable and bio-based flux components for solder pastes.

Future Outlook for Solder Paste for Electronic Products Market

The future outlook for the Solder Paste for Electronic Products market is exceptionally positive, driven by continued technological innovation and the expansion of key end-user industries. The increasing integration of artificial intelligence (AI) and advanced computing in everyday devices will necessitate solder pastes that offer unparalleled reliability and performance. The burgeoning electric vehicle market and the ongoing development of smart infrastructure will continue to be significant growth catalysts. Emerging applications in areas like flexible electronics, advanced medical devices, and next-generation aerospace components present substantial untapped market potential. Strategic opportunities lie in developing highly specialized solder pastes that meet stringent performance requirements, such as extreme temperature resistance, enhanced conductivity, and superior void reduction. Companies focusing on sustainable manufacturing practices and advanced material science will be well-positioned to capture a significant share of the future market. The market is poised for steady growth, with an estimated market value projected to reach xx million USD by 2033.

Solder Paste for Electronic Products Segmentation

-

1. Application

- 1.1. Consumer Electronics

- 1.2. Vehicle Electronics

- 1.3. Other

-

2. Types

- 2.1. Rosin Based Pastes

- 2.2. Water Soluble Pastes

- 2.3. No-clean Pastes

Solder Paste for Electronic Products Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Solder Paste for Electronic Products Regional Market Share

Geographic Coverage of Solder Paste for Electronic Products

Solder Paste for Electronic Products REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 1.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Consumer Electronics

- 5.1.2. Vehicle Electronics

- 5.1.3. Other

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Rosin Based Pastes

- 5.2.2. Water Soluble Pastes

- 5.2.3. No-clean Pastes

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Solder Paste for Electronic Products Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Consumer Electronics

- 6.1.2. Vehicle Electronics

- 6.1.3. Other

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Rosin Based Pastes

- 6.2.2. Water Soluble Pastes

- 6.2.3. No-clean Pastes

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Solder Paste for Electronic Products Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Consumer Electronics

- 7.1.2. Vehicle Electronics

- 7.1.3. Other

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Rosin Based Pastes

- 7.2.2. Water Soluble Pastes

- 7.2.3. No-clean Pastes

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Solder Paste for Electronic Products Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Consumer Electronics

- 8.1.2. Vehicle Electronics

- 8.1.3. Other

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Rosin Based Pastes

- 8.2.2. Water Soluble Pastes

- 8.2.3. No-clean Pastes

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Solder Paste for Electronic Products Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Consumer Electronics

- 9.1.2. Vehicle Electronics

- 9.1.3. Other

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Rosin Based Pastes

- 9.2.2. Water Soluble Pastes

- 9.2.3. No-clean Pastes

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Solder Paste for Electronic Products Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Consumer Electronics

- 10.1.2. Vehicle Electronics

- 10.1.3. Other

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Rosin Based Pastes

- 10.2.2. Water Soluble Pastes

- 10.2.3. No-clean Pastes

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Solder Paste for Electronic Products Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Consumer Electronics

- 11.1.2. Vehicle Electronics

- 11.1.3. Other

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Rosin Based Pastes

- 11.2.2. Water Soluble Pastes

- 11.2.3. No-clean Pastes

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Indium

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 ALPHA

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Senju

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 MacDermid Alpha Electronics Solutions

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Heraeus

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Tamura

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Henkel

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Inventec

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 KOKI

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 AIM

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Nihon Superior

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 KAWADA

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Yashida

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Ishikawa

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 DS HiMetal

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 Indium

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 Shengmao

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.18 Tongfang Tech

- 12.1.18.1. Company Overview

- 12.1.18.2. Products

- 12.1.18.3. Company Financials

- 12.1.18.4. SWOT Analysis

- 12.1.19 Yong An

- 12.1.19.1. Company Overview

- 12.1.19.2. Products

- 12.1.19.3. Company Financials

- 12.1.19.4. SWOT Analysis

- 12.1.20 U-bond Technology Inc

- 12.1.20.1. Company Overview

- 12.1.20.2. Products

- 12.1.20.3. Company Financials

- 12.1.20.4. SWOT Analysis

- 12.1.21 Jissyu Solder

- 12.1.21.1. Company Overview

- 12.1.21.2. Products

- 12.1.21.3. Company Financials

- 12.1.21.4. SWOT Analysis

- 12.1.22 Shenzhen Vital New Material

- 12.1.22.1. Company Overview

- 12.1.22.2. Products

- 12.1.22.3. Company Financials

- 12.1.22.4. SWOT Analysis

- 12.1.1 Indium

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Solder Paste for Electronic Products Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Solder Paste for Electronic Products Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Solder Paste for Electronic Products Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Solder Paste for Electronic Products Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Solder Paste for Electronic Products Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Solder Paste for Electronic Products Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Solder Paste for Electronic Products Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Solder Paste for Electronic Products Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Solder Paste for Electronic Products Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Solder Paste for Electronic Products Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Solder Paste for Electronic Products Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Solder Paste for Electronic Products Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Solder Paste for Electronic Products Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Solder Paste for Electronic Products Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Solder Paste for Electronic Products Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Solder Paste for Electronic Products Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Solder Paste for Electronic Products Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Solder Paste for Electronic Products Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Solder Paste for Electronic Products Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Solder Paste for Electronic Products Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Solder Paste for Electronic Products Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Solder Paste for Electronic Products Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Solder Paste for Electronic Products Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Solder Paste for Electronic Products Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Solder Paste for Electronic Products Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Solder Paste for Electronic Products Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Solder Paste for Electronic Products Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Solder Paste for Electronic Products Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Solder Paste for Electronic Products Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Solder Paste for Electronic Products Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Solder Paste for Electronic Products Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Solder Paste for Electronic Products Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Solder Paste for Electronic Products Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Solder Paste for Electronic Products Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Solder Paste for Electronic Products Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Solder Paste for Electronic Products Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Solder Paste for Electronic Products Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Solder Paste for Electronic Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Solder Paste for Electronic Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Solder Paste for Electronic Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Solder Paste for Electronic Products Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Solder Paste for Electronic Products Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Solder Paste for Electronic Products Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Solder Paste for Electronic Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Solder Paste for Electronic Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Solder Paste for Electronic Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Solder Paste for Electronic Products Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Solder Paste for Electronic Products Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Solder Paste for Electronic Products Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Solder Paste for Electronic Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Solder Paste for Electronic Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Solder Paste for Electronic Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Solder Paste for Electronic Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Solder Paste for Electronic Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Solder Paste for Electronic Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Solder Paste for Electronic Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Solder Paste for Electronic Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Solder Paste for Electronic Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Solder Paste for Electronic Products Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Solder Paste for Electronic Products Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Solder Paste for Electronic Products Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Solder Paste for Electronic Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Solder Paste for Electronic Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Solder Paste for Electronic Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Solder Paste for Electronic Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Solder Paste for Electronic Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Solder Paste for Electronic Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Solder Paste for Electronic Products Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Solder Paste for Electronic Products Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Solder Paste for Electronic Products Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Solder Paste for Electronic Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Solder Paste for Electronic Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Solder Paste for Electronic Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Solder Paste for Electronic Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Solder Paste for Electronic Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Solder Paste for Electronic Products Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Solder Paste for Electronic Products Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Solder Paste for Electronic Products?

The projected CAGR is approximately 1.2%.

2. Which companies are prominent players in the Solder Paste for Electronic Products?

Key companies in the market include Indium, ALPHA, Senju, MacDermid Alpha Electronics Solutions, Heraeus, Tamura, Henkel, Inventec, KOKI, AIM, Nihon Superior, KAWADA, Yashida, Ishikawa, DS HiMetal, Indium, Shengmao, Tongfang Tech, Yong An, U-bond Technology Inc, Jissyu Solder, Shenzhen Vital New Material.

3. What are the main segments of the Solder Paste for Electronic Products?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Solder Paste for Electronic Products," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Solder Paste for Electronic Products report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Solder Paste for Electronic Products?

To stay informed about further developments, trends, and reports in the Solder Paste for Electronic Products, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence