Key Insights

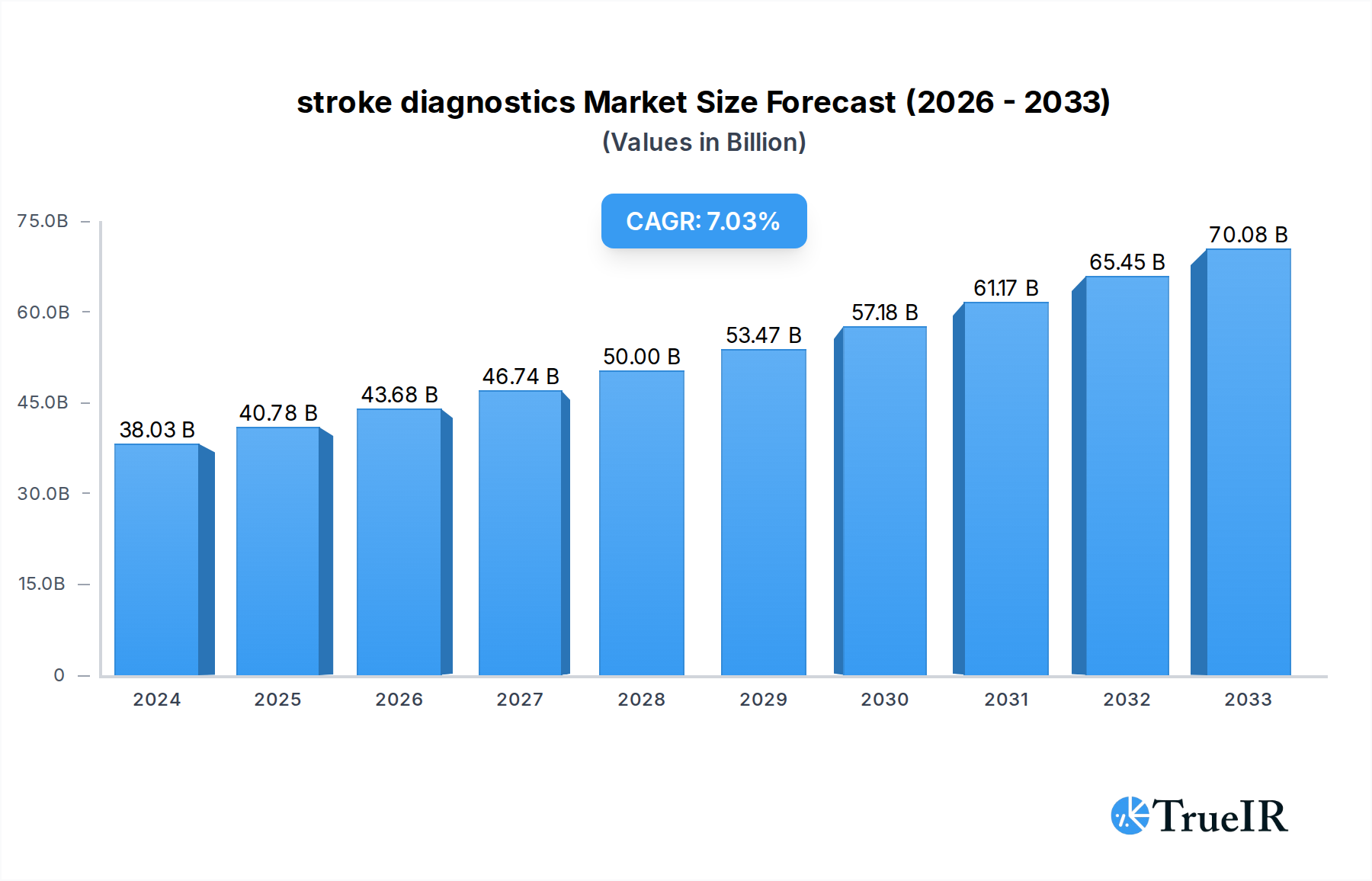

The global stroke diagnostics market is experiencing robust growth, projected to reach an estimated USD 38.03 billion in 2024 and expand at a compound annual growth rate (CAGR) of 7.2% from 2019 to 2033. This expansion is fueled by several key drivers including the increasing global prevalence of stroke, particularly among aging populations, and the growing awareness surrounding the critical importance of rapid diagnosis and intervention for improved patient outcomes. Advancements in imaging technologies, such as CT scans, MRI, and advanced AI-powered diagnostic software, are playing a pivotal role in enhancing diagnostic accuracy and speed. Furthermore, the rising adoption of minimally invasive diagnostic procedures and the increasing focus on early detection and prevention strategies are further propelling market growth. The market is segmented by application into Ischemic Stroke, Hemorrhagic Stroke, and Transient Ischemic Attack (TIA). Ischemic strokes, being the most common type, naturally represent a significant portion of the diagnostic market. The demand for effective diagnostics for all stroke types is amplified by the escalating burden of cerebrovascular diseases worldwide.

stroke diagnostics Market Size (In Billion)

Technological innovation is a dominant trend shaping the stroke diagnostics landscape. The integration of artificial intelligence (AI) and machine learning (ML) into diagnostic software is revolutionizing how stroke is identified, enabling faster analysis of medical images and providing critical decision support for clinicians. This is particularly impactful in reducing "door-to-needle" times for ischemic stroke treatment. The market is characterized by a dynamic competitive environment with major global players like Abbott Laboratories, Medtronic, and GE Healthcare, alongside emerging innovators focusing on novel diagnostic solutions. While the market presents substantial opportunities, certain restraints such as the high cost of advanced diagnostic equipment and the need for specialized training for healthcare professionals in underdeveloped regions could pose challenges. However, the continuous drive for more accessible and efficient diagnostic tools, coupled with strategic collaborations and R&D investments, is expected to overcome these hurdles, ensuring sustained market expansion throughout the forecast period.

stroke diagnostics Company Market Share

Revolutionizing Stroke Care: A Comprehensive Stroke Diagnostics Market Report (2019-2033)

This in-depth report provides unparalleled insights into the dynamic stroke diagnostics market, a critical segment of the global healthcare industry projected to experience substantial growth. Leveraging high-volume keywords such as "stroke diagnostics," "ischemic stroke detection," "hemorrhagic stroke diagnosis," "TIA assessment," "AI in stroke imaging," "neurological imaging technologies," and "acute stroke management," this analysis is designed to empower industry stakeholders, researchers, and investors. Spanning a study period from 2019 to 2033, with a base and estimated year of 2025, this report offers a forward-looking perspective on market evolution, technological advancements, and strategic opportunities in stroke diagnostics. The market is segmented by application (Ischemic Stroke, Hemorrhagic Stroke, Transient Ischemic Attack) and type (Software, Hardware), with a detailed examination of key players, industry developments, and future trends.

stroke diagnostics Market Structure & Competitive Landscape

The stroke diagnostics market exhibits a moderately concentrated structure, with several large, established global players dominating the landscape. Key innovation drivers include the relentless pursuit of faster, more accurate diagnostic tools, particularly in the critical time window following stroke onset. The integration of artificial intelligence (AI) and machine learning (ML) into imaging analysis and decision support software is a significant disruptor, enhancing diagnostic speed and precision. Regulatory impacts, while sometimes posing hurdles for novel technologies, also drive standardization and quality assurance, ultimately benefiting patient outcomes. Product substitutes, such as advancements in point-of-care diagnostics and less invasive monitoring techniques, are emerging but currently pose limited threats to the core advanced imaging and software solutions. End-user segmentation reveals a strong demand from hospitals, specialized stroke centers, and emergency medical services, all focused on rapid and effective stroke diagnosis. Merger and acquisition (M&A) activities have been robust, with an estimated XXX billion in M&A volume during the historical period, as companies seek to consolidate their market position, acquire cutting-edge technologies, and expand their product portfolios. Notable M&A activities are anticipated to continue shaping the competitive terrain, fostering consolidation and driving innovation.

stroke diagnostics Market Trends & Opportunities

The stroke diagnostics market is poised for exceptional growth, projected to reach a valuation of over XXX billion by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of approximately XX% from the base year 2025. This expansion is fueled by a confluence of factors including the increasing global incidence of stroke, a growing and aging population, and a heightened awareness of the importance of timely diagnosis and intervention for improved patient outcomes. Technological shifts are at the forefront of this market evolution. The integration of advanced neuroimaging techniques such as computed tomography angiography (CTA), magnetic resonance angiography (MRA), and diffusion-weighted MRI is becoming standard practice for stroke assessment. Furthermore, the rapid adoption of AI-powered diagnostic software is revolutionizing stroke interpretation, enabling faster and more accurate identification of stroke type, severity, and potential treatment pathways. Consumer preferences are shifting towards minimally invasive diagnostic procedures and solutions that offer real-time data and predictive analytics, empowering clinicians with actionable insights. Competitive dynamics are characterized by intense R&D investments and strategic partnerships aimed at developing next-generation diagnostic tools. The market penetration rate for advanced stroke diagnostic solutions is steadily increasing, particularly in developed economies, with emerging markets showing significant untapped potential. Opportunities abound for companies that can offer integrated solutions combining hardware and software, demonstrating clear clinical efficacy, and navigating the complex reimbursement landscape. The demand for portable and point-of-care diagnostic devices for pre-hospital assessment is also a growing trend.

Dominant Markets & Segments in stroke diagnostics

The Ischemic Stroke segment is currently the dominant application within the stroke diagnostics market, driven by its higher prevalence compared to hemorrhagic stroke. This dominance is further amplified by the critical need for rapid identification and reperfusion therapies, making every minute count in ischemic stroke management. Key growth drivers in this segment include advancements in imaging modalities like CT perfusion and advanced MRI sequences that can precisely delineate the ischemic penumbra, guiding time-sensitive treatment decisions. The widespread availability of advanced neuroimaging infrastructure in developed healthcare systems, coupled with supportive government policies promoting stroke care, significantly contributes to the dominance of ischemic stroke diagnostics.

The Software segment, particularly AI-powered diagnostic platforms, is experiencing exponential growth and is projected to significantly influence market dynamics. The ability of AI algorithms to analyze complex imaging data, identify subtle abnormalities, and provide decision support rapidly is transforming stroke diagnosis. Key growth drivers for software solutions include the increasing volume of imaging data generated, the need to reduce diagnostic turnaround times, and the potential for AI to democratize access to expert-level stroke interpretation. Furthermore, the development of cloud-based platforms is enabling seamless integration and data sharing, further accelerating adoption.

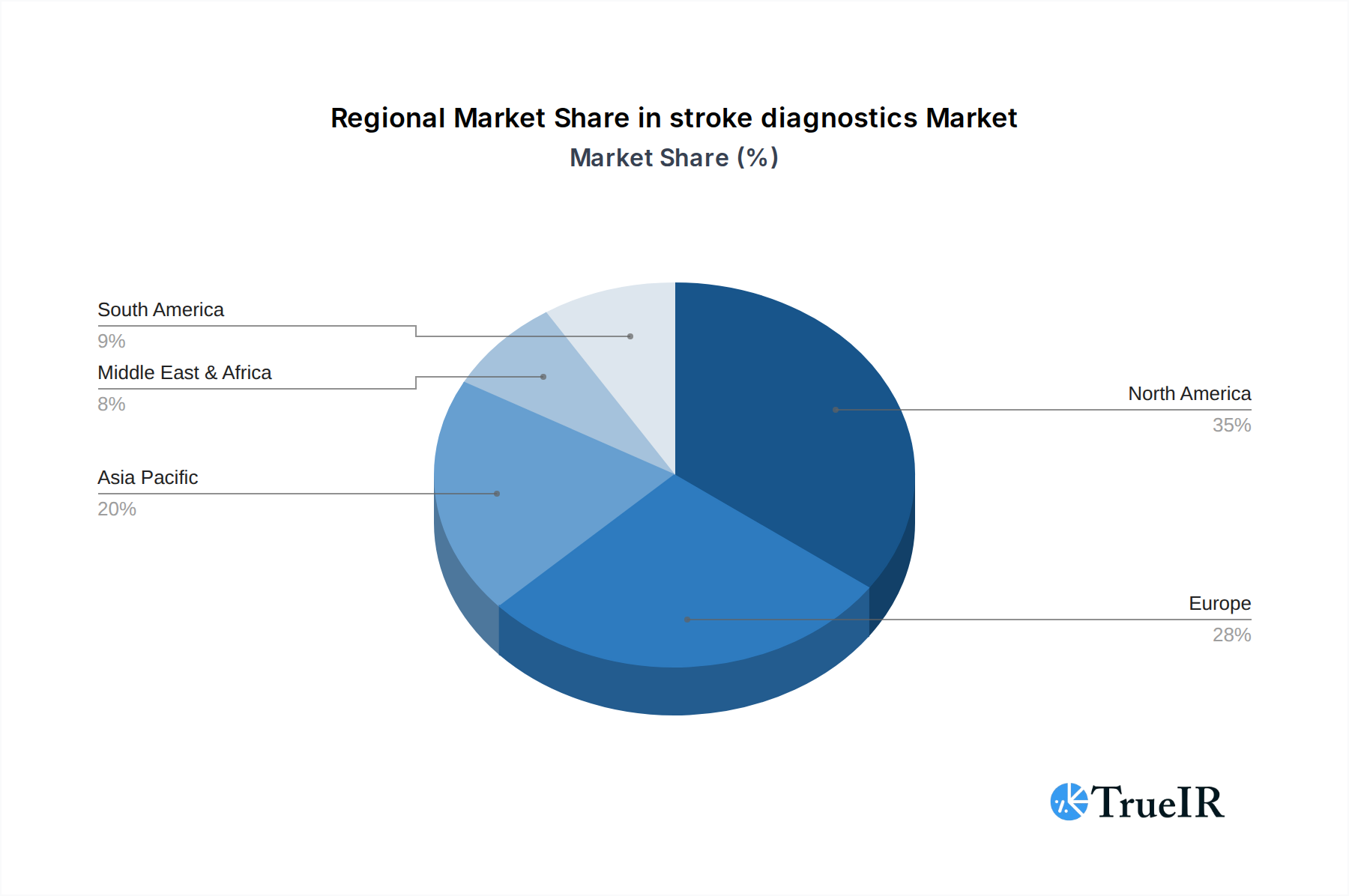

In terms of regional dominance, North America currently leads the stroke diagnostics market. This leadership is attributed to several factors:

- Advanced Healthcare Infrastructure: Extensive availability of sophisticated neuroimaging equipment and specialized stroke centers.

- High Stroke Incidence and Awareness: A large population susceptible to stroke and a high level of public and professional awareness regarding stroke prevention and treatment.

- Robust R&D Investment: Significant investment in research and development by both academic institutions and private companies, leading to early adoption of innovative technologies.

- Favorable Reimbursement Policies: Supportive reimbursement frameworks that facilitate the adoption of advanced diagnostic tools and procedures.

- Proactive Regulatory Environment: A regulatory landscape that, while stringent, generally encourages innovation and market access for beneficial medical technologies.

The dominance of these segments is underpinned by a continuous drive for greater diagnostic accuracy, faster turnaround times, and improved patient outcomes in the critical phase of stroke management.

stroke diagnostics Product Analysis

Product innovations in stroke diagnostics are primarily focused on enhancing speed, accuracy, and accessibility. AI-powered software solutions are revolutionizing image interpretation, enabling rapid identification of stroke type and severity. Advanced hardware, including high-resolution CT and MRI scanners with specialized stroke protocols, provides detailed anatomical and physiological information. Competitive advantages stem from integrated hardware-software solutions that offer seamless workflows, from imaging acquisition to automated reporting and clinical decision support. The development of portable and point-of-care devices is also a key trend, aiming to bring advanced diagnostics closer to the patient, even in pre-hospital settings.

Key Drivers, Barriers & Challenges in stroke diagnostics

Key Drivers:

- Technological Advancements: Continuous innovation in AI, imaging hardware, and software for faster and more accurate diagnosis.

- Increasing Stroke Incidence: A growing and aging global population leads to a higher prevalence of stroke.

- Growing Awareness: Enhanced public and medical professional awareness of the critical importance of rapid stroke diagnosis and intervention.

- Supportive Healthcare Policies: Government initiatives and healthcare reforms promoting stroke care and the adoption of advanced diagnostic technologies.

Barriers & Challenges:

- High Initial Investment: The substantial cost of advanced neuroimaging equipment and AI software can be a barrier, especially for smaller healthcare facilities.

- Regulatory Hurdles: The complex and time-consuming regulatory approval processes for new diagnostic technologies can slow market entry.

- Data Integration and Interoperability: Challenges in integrating data from various sources and ensuring seamless interoperability between different diagnostic systems.

- Shortage of Skilled Professionals: A lack of trained personnel to operate advanced equipment and interpret complex diagnostic data effectively.

- Reimbursement Landscape: Navigating evolving reimbursement policies and securing adequate coverage for advanced diagnostic procedures.

Growth Drivers in the stroke diagnostics Market

The stroke diagnostics market is propelled by a robust interplay of technological, economic, and regulatory factors. Technologically, the transformative impact of artificial intelligence in image analysis and workflow optimization is a paramount growth driver, enabling faster and more accurate identification of stroke types. Economically, increasing healthcare expenditure globally, coupled with a growing emphasis on preventative and acute care, fuels demand for advanced diagnostic solutions. Policy-driven initiatives aimed at improving stroke outcomes and reducing long-term disability also play a crucial role, encouraging the adoption of cutting-edge diagnostic tools and protocols.

Challenges Impacting stroke diagnostics Growth

Several challenges impact the growth trajectory of the stroke diagnostics market. Regulatory complexities, including stringent approval processes for novel AI algorithms and medical devices, can significantly extend time-to-market and increase development costs. Supply chain issues, particularly in the wake of global disruptions, can affect the availability and cost of critical hardware components for imaging systems. Furthermore, intense competitive pressures among established players and emerging innovators necessitate continuous R&D investment and strategic market positioning to maintain a competitive edge. The integration of new technologies into existing healthcare infrastructures also presents a logistical and financial challenge for many institutions.

Key Players Shaping the stroke diagnostics Market

- Abbott Laboratories Ltd.

- Medtronic(Covidien)

- General Electric Company(GE Healthcare)

- Hitachi,Ltd.

- Johnson & Johnson

- Penumbra,Inc.

- Koninklijke Philips N.V.

- Siemens(Siemens International GmbH)

- Stryker Corporation (Concentric Medical,Inc.)

- Canon Medical Systems Corporation

- Nihon Kohden Corporation

- Sense Neuro Diagnostics

- Forest Devices

- Brainomix

- Jan Medical

- RapidAI

- Viz.ai

Significant stroke diagnostics Industry Milestones

- 2019: Launch of AI-powered stroke imaging analysis software, significantly reducing diagnostic interpretation time.

- 2020: FDA clearance for a novel point-of-care device for rapid stroke detection in pre-hospital settings.

- 2021: Major acquisition of a leading AI stroke platform by a global medical technology company, consolidating market leadership.

- 2022: Introduction of advanced CT perfusion imaging techniques for more precise assessment of ischemic stroke.

- 2023: Significant increase in venture capital funding for AI-driven stroke diagnostics startups.

- 2024 (Q1-Q4): Continued integration of AI into MRI and CT workflows, leading to enhanced diagnostic accuracy for various stroke types.

- 2025 (Est.): Wider adoption of cloud-based stroke imaging platforms for improved data accessibility and collaboration.

Future Outlook for stroke diagnostics Market

The future outlook for the stroke diagnostics market is exceptionally promising, driven by ongoing technological advancements and an increasing global focus on stroke prevention and acute care. Strategic opportunities lie in the further development and integration of AI-powered solutions, the expansion of minimally invasive diagnostic techniques, and the penetration of emerging markets. The market is expected to witness a sustained CAGR of XX% in the forecast period, fueled by the increasing demand for rapid and accurate stroke diagnosis, leading to improved patient outcomes and reduced healthcare burdens. The development of integrated diagnostic and treatment platforms will further shape the market, offering a comprehensive approach to stroke management.

stroke diagnostics Segmentation

-

1. Application

- 1.1. Ischemic Stroke

- 1.2. Hemorrhagic Stroke

- 1.3. Transient Ischemic Attack

-

2. Types

- 2.1. Software

- 2.2. Hardware

stroke diagnostics Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

stroke diagnostics Regional Market Share

Geographic Coverage of stroke diagnostics

stroke diagnostics REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global stroke diagnostics Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Ischemic Stroke

- 5.1.2. Hemorrhagic Stroke

- 5.1.3. Transient Ischemic Attack

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Software

- 5.2.2. Hardware

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America stroke diagnostics Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Ischemic Stroke

- 6.1.2. Hemorrhagic Stroke

- 6.1.3. Transient Ischemic Attack

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Software

- 6.2.2. Hardware

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America stroke diagnostics Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Ischemic Stroke

- 7.1.2. Hemorrhagic Stroke

- 7.1.3. Transient Ischemic Attack

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Software

- 7.2.2. Hardware

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe stroke diagnostics Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Ischemic Stroke

- 8.1.2. Hemorrhagic Stroke

- 8.1.3. Transient Ischemic Attack

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Software

- 8.2.2. Hardware

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa stroke diagnostics Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Ischemic Stroke

- 9.1.2. Hemorrhagic Stroke

- 9.1.3. Transient Ischemic Attack

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Software

- 9.2.2. Hardware

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific stroke diagnostics Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Ischemic Stroke

- 10.1.2. Hemorrhagic Stroke

- 10.1.3. Transient Ischemic Attack

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Software

- 10.2.2. Hardware

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Abbott Laboratories Ltd.

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Medtronic(Covidien)

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 General Electric Company(GE Healthcare)

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Hitachi

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Ltd.

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Johnson & Johnson

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Penumbra

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Inc.

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Koninklijke Philips N.V.

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Siemens(Siemens International GmbH)

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Stryker Corporation (Concentric Medical

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Inc.)

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Canon Medical Systems Corporation

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Nihon Kohden Corporation

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Sense Neuro Diagnostics

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Forest Devices

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Brainomix

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Jan Medical

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 RapidAI

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Viz.ai

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.1 Abbott Laboratories Ltd.

List of Figures

- Figure 1: Global stroke diagnostics Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America stroke diagnostics Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America stroke diagnostics Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America stroke diagnostics Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America stroke diagnostics Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America stroke diagnostics Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America stroke diagnostics Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America stroke diagnostics Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America stroke diagnostics Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America stroke diagnostics Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America stroke diagnostics Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America stroke diagnostics Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America stroke diagnostics Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe stroke diagnostics Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe stroke diagnostics Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe stroke diagnostics Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe stroke diagnostics Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe stroke diagnostics Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe stroke diagnostics Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa stroke diagnostics Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa stroke diagnostics Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa stroke diagnostics Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa stroke diagnostics Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa stroke diagnostics Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa stroke diagnostics Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific stroke diagnostics Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific stroke diagnostics Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific stroke diagnostics Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific stroke diagnostics Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific stroke diagnostics Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific stroke diagnostics Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global stroke diagnostics Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global stroke diagnostics Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global stroke diagnostics Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global stroke diagnostics Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global stroke diagnostics Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global stroke diagnostics Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States stroke diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada stroke diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico stroke diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global stroke diagnostics Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global stroke diagnostics Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global stroke diagnostics Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil stroke diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina stroke diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America stroke diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global stroke diagnostics Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global stroke diagnostics Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global stroke diagnostics Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom stroke diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany stroke diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France stroke diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy stroke diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain stroke diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia stroke diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux stroke diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics stroke diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe stroke diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global stroke diagnostics Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global stroke diagnostics Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global stroke diagnostics Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey stroke diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel stroke diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC stroke diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa stroke diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa stroke diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa stroke diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global stroke diagnostics Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global stroke diagnostics Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global stroke diagnostics Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China stroke diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India stroke diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan stroke diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea stroke diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN stroke diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania stroke diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific stroke diagnostics Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the stroke diagnostics?

The projected CAGR is approximately 7.2%.

2. Which companies are prominent players in the stroke diagnostics?

Key companies in the market include Abbott Laboratories Ltd., Medtronic(Covidien), General Electric Company(GE Healthcare), Hitachi, Ltd., Johnson & Johnson, Penumbra, Inc., Koninklijke Philips N.V., Siemens(Siemens International GmbH), Stryker Corporation (Concentric Medical, Inc.), Canon Medical Systems Corporation, Nihon Kohden Corporation, Sense Neuro Diagnostics, Forest Devices, Brainomix, Jan Medical, RapidAI, Viz.ai.

3. What are the main segments of the stroke diagnostics?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4350.00, USD 6525.00, and USD 8700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "stroke diagnostics," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the stroke diagnostics report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the stroke diagnostics?

To stay informed about further developments, trends, and reports in the stroke diagnostics, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence