Key Insights

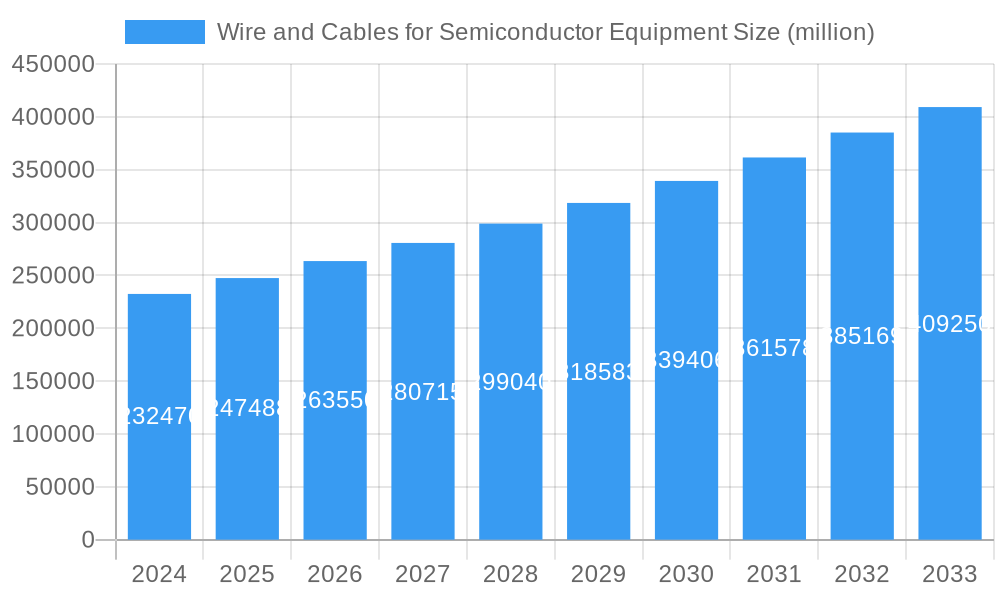

The global market for Wire and Cables for Semiconductor Equipment is poised for significant expansion, driven by the relentless demand for advanced semiconductors across a multitude of industries. Valued at approximately $232.47 billion in 2024, the market is projected to grow at a robust Compound Annual Growth Rate (CAGR) of 6.51% through 2033. This growth is fueled by the escalating complexity of semiconductor manufacturing processes, necessitating highly specialized and reliable cabling solutions for both front-end and back-end operations. The increasing investment in semiconductor fabrication plants (fabs) worldwide, coupled with the miniaturization and higher performance demands of electronic devices, are primary market drivers. Furthermore, the ongoing technological advancements in areas such as Artificial Intelligence (AI), 5G deployment, and the Internet of Things (IoT) are creating a continuous need for cutting-edge semiconductor components, thereby bolstering the demand for their associated wiring infrastructure.

Wire and Cables for Semiconductor Equipment Market Size (In Billion)

The market segmentation reveals a strong emphasis on both application and cable type. While Front-End Processes and Back-End Processes represent key application areas, the demand for specific cable constructions like Foil Shielded, Braid Shielded, and Foil+Braid Shielded types underscores the critical need for signal integrity and protection against electromagnetic interference (EMI) in sensitive semiconductor manufacturing environments. Restraints such as the high cost of specialized materials and the stringent quality control required in this sector are present, but the overarching trends of technological innovation and increased global semiconductor production capacity are expected to outweigh these challenges. Key players like TE Connectivity, Alpha Wire, and LEONI are actively involved in this competitive landscape, innovating and expanding their offerings to meet the evolving needs of semiconductor equipment manufacturers. The Asia Pacific region, particularly China and South Korea, is anticipated to remain a dominant force due to its extensive semiconductor manufacturing base.

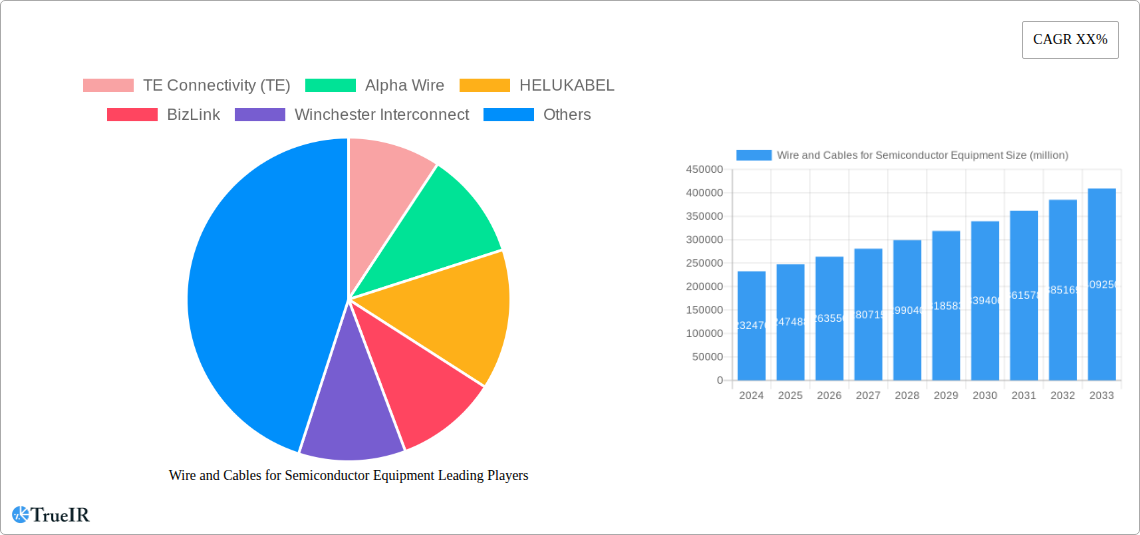

Wire and Cables for Semiconductor Equipment Company Market Share

This comprehensive report provides an in-depth analysis of the global Wire and Cables for Semiconductor Equipment Market, crucial for powering the next generation of microchips. Spanning from 2019 to 2033, with a base year of 2025, this study offers unparalleled insights into market dynamics, trends, opportunities, and competitive strategies. We delve into the critical role of high-performance semiconductor wiring, interconnect solutions, and advanced cable technologies in supporting front-end processes, back-end processes, and fab support equipment.

Wire and Cables for Semiconductor Equipment Market Structure & Competitive Landscape

The Wire and Cables for Semiconductor Equipment Market exhibits a moderately consolidated structure, with several key players holding significant market share, estimated at over 70% by the top 10 companies. Innovation remains a primary driver, fueled by the relentless demand for higher bandwidth, lower latency, and enhanced signal integrity in increasingly complex semiconductor manufacturing environments. Regulatory impacts, particularly concerning material compliance and environmental standards, influence product development and market entry. Product substitutes are limited, given the specialized nature of semiconductor applications, but advancements in alternative connection technologies are being closely monitored. End-user segmentation highlights the distinct needs of front-end processing equipment (e.g., lithography, etching) and back-end processing equipment (e.g., dicing, packaging), each requiring tailored cable solutions. Merger and acquisition (M&A) trends, valued at approximately 1.5 billion in the historical period (2019-2024), indicate strategic consolidation and expansion efforts by leading manufacturers to broaden their product portfolios and geographical reach.

- Innovation Drivers: Miniaturization of components, increasing data transfer speeds, stringent performance requirements for advanced nodes.

- Regulatory Impacts: RoHS, REACH, and other material compliance mandates.

- End-User Segmentation:

- Front-End Processes (e.g., wafer fabrication)

- Back-End Processes (e.g., assembly, testing)

- Fab Support Equipment (e.g., facility infrastructure)

- M&A Trends: Focus on acquiring specialized technologies and expanding market penetration.

Wire and Cables for Semiconductor Equipment Market Trends & Opportunities

The Wire and Cables for Semiconductor Equipment Market is poised for substantial growth, projected to reach a valuation exceeding 25 billion by the end of the forecast period. This expansion is driven by the exponential increase in semiconductor demand across diverse industries, including artificial intelligence (AI), automotive, telecommunications, and consumer electronics. Technological shifts are paramount, with a growing emphasis on high-frequency cables, miniaturized connectors, and materials with superior thermal and electrical properties to accommodate higher power densities and faster data rates in next-generation semiconductor manufacturing tools. Consumer preferences are increasingly aligned with higher performance and reliability, pushing manufacturers to develop cables that minimize signal loss and electromagnetic interference (EMI). Competitive dynamics are intensifying, characterized by ongoing product innovation, strategic partnerships, and a focus on vertical integration. The market penetration rate for advanced shielding technologies, such as foil + braid shielded cables, is expected to grow significantly. The Compound Annual Growth Rate (CAGR) for the forecast period (2025-2033) is estimated at an impressive 7.5%.

Opportunities abound for manufacturers capable of developing and supplying cutting-edge semiconductor wiring solutions. The continuous evolution of semiconductor fabrication processes, demanding ever-higher precision and speed, creates a constant need for specialized cabling. For instance, the drive towards smaller process nodes (e.g., sub-7nm) necessitates cables that can withstand extreme temperatures and chemical environments while maintaining signal integrity. Furthermore, the increasing complexity of testing and inspection equipment used in both front-end and back-end processes requires cables with exceptional durability and data transmission capabilities. The growth of advanced packaging technologies, such as 3D stacking, also presents new challenges and opportunities for cable manufacturers to provide flexible and high-density interconnects.

The push for automation and Industry 4.0 in semiconductor fabs further amplifies the demand for robust and reliable cabling. These smart factories rely on extensive sensor networks, robotic systems, and high-speed communication infrastructure, all of which are underpinned by advanced wire and cable solutions. The transition to unshielded, foil shielded, braid shielded, and foil + braid shielded cable types will continue, driven by the specific shielding requirements of different equipment and applications to mitigate noise and interference.

Geographically, regions investing heavily in semiconductor manufacturing capacity, such as Asia-Pacific and North America, represent the most significant growth markets. Government initiatives and incentives aimed at reshoring semiconductor production further bolster this trend. The increasing adoption of AI and machine learning is creating a surge in demand for high-performance computing chips, directly translating into a higher demand for the specialized equipment and thus, the wires and cables that power it.

Dominant Markets & Segments in Wire and Cables for Semiconductor Equipment

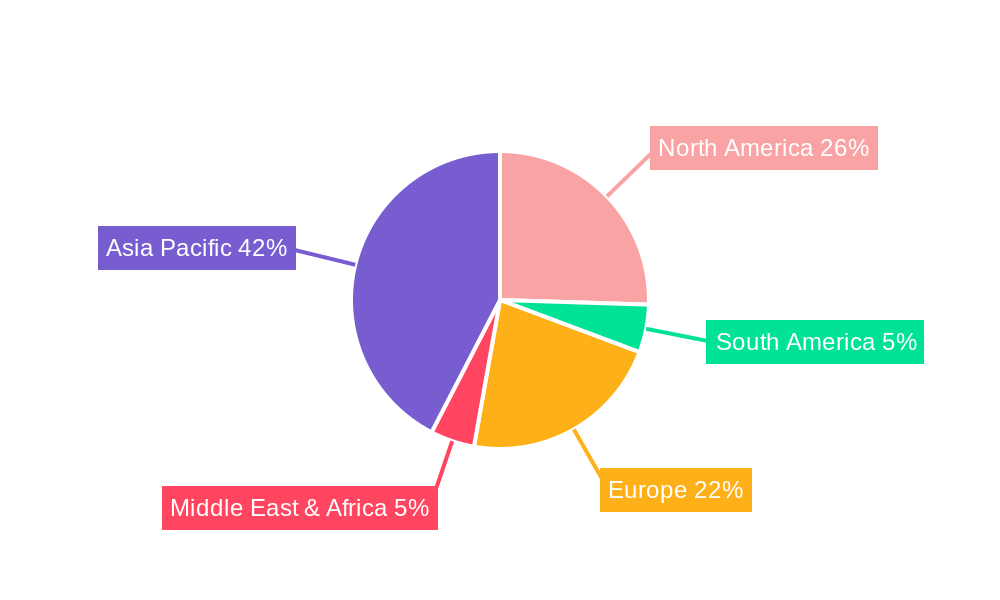

The Asia-Pacific region stands out as the dominant market for Wire and Cables for Semiconductor Equipment, primarily driven by the concentration of leading semiconductor manufacturing facilities in countries like Taiwan, South Korea, and China. This dominance is fueled by substantial infrastructure investments, supportive government policies aimed at fostering domestic semiconductor ecosystems, and the presence of major semiconductor foundries and assembly plants. Within this region, front-end processes represent the largest application segment, demanding high-purity, high-reliability cables that can withstand extreme temperatures, corrosive chemicals, and vacuum environments essential for wafer fabrication. The segment of foil + braid shielded cables is experiencing remarkable growth within front-end applications due to the critical need for maximum signal integrity and EMI/RFI protection in sensitive lithography and etching equipment.

The United States, particularly with its renewed focus on semiconductor manufacturing through legislative support, is emerging as a significant growth market. Investments in advanced research and development and the establishment of new fabrication plants are driving demand for specialized interconnects and high-performance cables.

In terms of cable types, foil + braid shielded cables are increasingly preferred across both front-end and back-end processes where noise immunity and signal integrity are paramount. This is critical for applications involving high-speed data transmission and sensitive control signals within semiconductor manufacturing equipment. However, braid shielded cables continue to hold a substantial market share due to their robust performance and cost-effectiveness in many applications. Foil shielded and unshielded cables cater to less demanding applications or specific environmental requirements. The overall market value for this segment is estimated to be in the billions, with front-end processes accounting for over 60 billion in historical spending (2019-2024).

- Leading Region: Asia-Pacific

- Key Countries: Taiwan, South Korea, China, United States

- Dominant Application Segment: Front-End Processes

- Fastest Growing Cable Type: Foil + Braid Shielded

- Key Growth Drivers:

- Expansion of wafer fabrication capacity.

- Government incentives for domestic semiconductor production.

- Technological advancements in semiconductor manufacturing equipment.

- Increasing demand for advanced chip technologies (AI, 5G).

Wire and Cables for Semiconductor Equipment Product Analysis

Product innovation in Wire and Cables for Semiconductor Equipment focuses on delivering superior performance, miniaturization, and enhanced reliability. Manufacturers are developing cables with improved dielectric properties, higher temperature resistance, and reduced signal loss for demanding applications like high-speed data transfer in wafer steppers and etching systems. Competitive advantages are derived from specialized materials, advanced shielding techniques, and custom connector solutions designed for specific equipment interfaces. Technological advancements are enabling smaller form factors for cables and connectors, crucial for dense equipment layouts, while maintaining robust signal integrity and data throughput.

Key Drivers, Barriers & Challenges in Wire and Cables for Semiconductor Equipment

Key Drivers: The Wire and Cables for Semiconductor Equipment Market is propelled by the insatiable global demand for semiconductors, driven by AI, 5G, IoT, and the automotive sector. Technological advancements in semiconductor manufacturing processes, requiring higher precision and faster data transmission, necessitate advanced cabling solutions. Government initiatives worldwide supporting domestic chip production and R&D further stimulate market growth.

Barriers & Challenges: Supply chain disruptions, particularly for specialized raw materials, and geopolitical tensions pose significant challenges. Stringent quality control and certification requirements for semiconductor-grade cables add to development costs and lead times. Intense competition among global players can lead to price pressures, impacting profit margins. The rapid pace of technological change requires continuous R&D investment to keep pace with evolving equipment needs.

Growth Drivers in the Wire and Cables for Semiconductor Equipment Market

The primary growth catalysts for the Wire and Cables for Semiconductor Equipment Market include the accelerating adoption of advanced technologies such as artificial intelligence (AI) and 5G, which are driving unprecedented demand for high-performance semiconductors. Furthermore, significant global investments in building new semiconductor fabrication plants and expanding existing ones, supported by favorable government policies and incentives in key regions, are directly increasing the need for specialized wiring and cabling infrastructure. The continuous innovation in semiconductor manufacturing processes, pushing towards smaller nodes and more complex architectures, mandates the development and deployment of cables with superior signal integrity, thermal management, and durability.

Challenges Impacting Wire and Cables for Semiconductor Equipment Growth

The Wire and Cables for Semiconductor Equipment Market faces several challenges that could impede its growth trajectory. Supply chain volatility, including shortages of critical raw materials and disruptions due to geopolitical events, can significantly impact production timelines and costs. The highly regulated nature of the semiconductor industry necessitates adherence to stringent quality, safety, and environmental standards, requiring substantial investment in compliance and certification. Intense global competition, characterized by multiple established players and new entrants, can lead to price wars and pressure on profit margins, especially for standard cable types. Moreover, the rapid evolution of semiconductor technology demands continuous and significant investment in research and development to innovate and meet the ever-increasing performance requirements of next-generation equipment.

Key Players Shaping the Wire and Cables for Semiconductor Equipment Market

- TE Connectivity (TE)

- Alpha Wire

- HELUKABEL

- BizLink

- Winchester Interconnect

- LEONI

- Oki Electric Industry

- MC Electronics

- Cicoil

- Teledyne

- Kowa Denzai Sha LTD

- CHUGOKU ELECTRIC WIRE & CABLE CO.,LTD.

- Prysmian

- Nexans

- LS Cable & System

- TF Kable

- W. L. Gore & Associates

- TOTOKU INC.

- SAB

- Daiichi Denzai (DID)

- NICHIGOH COMMUNICATION ELECTRIC WIRE CO.,LTD.

Significant Wire and Cables for Semiconductor Equipment Industry Milestones

- 2019: Introduction of new high-speed data transmission cables with improved shielding for advanced lithography equipment.

- 2020: TE Connectivity's acquisition of a specialized interconnect solutions provider, bolstering its semiconductor offerings.

- 2021: HELUKABEL launches a new series of high-temperature resistant cables for vacuum applications in wafer processing.

- 2022: BizLink expands its manufacturing capacity in Asia to meet growing demand for semiconductor wiring.

- 2023: W. L. Gore & Associates introduces advanced fluoropolymer-based cables offering superior chemical resistance and electrical performance.

- 2024: Nexans announces strategic partnerships to develop next-generation cabling for advanced packaging technologies.

Future Outlook for Wire and Cables for Semiconductor Equipment Market

The future outlook for the Wire and Cables for Semiconductor Equipment Market is exceptionally bright, driven by sustained global demand for advanced semiconductors. Strategic opportunities lie in developing ultra-high-speed, low-loss cables for AI accelerators, autonomous driving systems, and next-generation networking infrastructure. The increasing trend towards miniaturization in semiconductor devices will necessitate smaller, more flexible, and higher-density cabling solutions. Manufacturers focusing on material innovation, sustainable production, and customized solutions for specific equipment vendors are well-positioned for significant growth. The ongoing expansion of semiconductor manufacturing capacity globally, coupled with technological advancements, will continue to fuel demand for specialized wire and cable products, projecting robust market expansion throughout the forecast period.

Wire and Cables for Semiconductor Equipment Segmentation

-

1. Application

- 1.1. Front-End Processes

- 1.2. Back-End Processes

- 1.3. Fab Support Equipment

-

2. Types

- 2.1. Unshielded

- 2.2. Foil Shielded

- 2.3. Braid Shielded

- 2.4. Foil+ Braid Shielded

Wire and Cables for Semiconductor Equipment Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Wire and Cables for Semiconductor Equipment Regional Market Share

Geographic Coverage of Wire and Cables for Semiconductor Equipment

Wire and Cables for Semiconductor Equipment REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.51% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Front-End Processes

- 5.1.2. Back-End Processes

- 5.1.3. Fab Support Equipment

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Unshielded

- 5.2.2. Foil Shielded

- 5.2.3. Braid Shielded

- 5.2.4. Foil+ Braid Shielded

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Wire and Cables for Semiconductor Equipment Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Front-End Processes

- 6.1.2. Back-End Processes

- 6.1.3. Fab Support Equipment

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Unshielded

- 6.2.2. Foil Shielded

- 6.2.3. Braid Shielded

- 6.2.4. Foil+ Braid Shielded

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Wire and Cables for Semiconductor Equipment Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Front-End Processes

- 7.1.2. Back-End Processes

- 7.1.3. Fab Support Equipment

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Unshielded

- 7.2.2. Foil Shielded

- 7.2.3. Braid Shielded

- 7.2.4. Foil+ Braid Shielded

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Wire and Cables for Semiconductor Equipment Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Front-End Processes

- 8.1.2. Back-End Processes

- 8.1.3. Fab Support Equipment

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Unshielded

- 8.2.2. Foil Shielded

- 8.2.3. Braid Shielded

- 8.2.4. Foil+ Braid Shielded

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Wire and Cables for Semiconductor Equipment Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Front-End Processes

- 9.1.2. Back-End Processes

- 9.1.3. Fab Support Equipment

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Unshielded

- 9.2.2. Foil Shielded

- 9.2.3. Braid Shielded

- 9.2.4. Foil+ Braid Shielded

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Wire and Cables for Semiconductor Equipment Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Front-End Processes

- 10.1.2. Back-End Processes

- 10.1.3. Fab Support Equipment

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Unshielded

- 10.2.2. Foil Shielded

- 10.2.3. Braid Shielded

- 10.2.4. Foil+ Braid Shielded

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Wire and Cables for Semiconductor Equipment Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Front-End Processes

- 11.1.2. Back-End Processes

- 11.1.3. Fab Support Equipment

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Unshielded

- 11.2.2. Foil Shielded

- 11.2.3. Braid Shielded

- 11.2.4. Foil+ Braid Shielded

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 TE Connectivity (TE)

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Alpha Wire

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 HELUKABEL

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 BizLink

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Winchester Interconnect

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 LEONI

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Oki Electric Industry

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 MC Electronics

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Cicoil

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Teledyne

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Kowa Denzai Sha LTD

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 CHUGOKU ELECTRIC WIRE & CABLE CO.

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 LTD.

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Prysmian

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Nexans

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 LS Cable & System

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 TF Kable

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.18 W. L. Gore & Associates

- 12.1.18.1. Company Overview

- 12.1.18.2. Products

- 12.1.18.3. Company Financials

- 12.1.18.4. SWOT Analysis

- 12.1.19 TOTOKU INC.

- 12.1.19.1. Company Overview

- 12.1.19.2. Products

- 12.1.19.3. Company Financials

- 12.1.19.4. SWOT Analysis

- 12.1.20 SAB

- 12.1.20.1. Company Overview

- 12.1.20.2. Products

- 12.1.20.3. Company Financials

- 12.1.20.4. SWOT Analysis

- 12.1.21 Daiichi Denzai (DID)

- 12.1.21.1. Company Overview

- 12.1.21.2. Products

- 12.1.21.3. Company Financials

- 12.1.21.4. SWOT Analysis

- 12.1.22 NICHIGOH COMMUNICATION ELECTRIC WIRE CO.

- 12.1.22.1. Company Overview

- 12.1.22.2. Products

- 12.1.22.3. Company Financials

- 12.1.22.4. SWOT Analysis

- 12.1.23 LTD.

- 12.1.23.1. Company Overview

- 12.1.23.2. Products

- 12.1.23.3. Company Financials

- 12.1.23.4. SWOT Analysis

- 12.1.1 TE Connectivity (TE)

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Wire and Cables for Semiconductor Equipment Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Wire and Cables for Semiconductor Equipment Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Wire and Cables for Semiconductor Equipment Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Wire and Cables for Semiconductor Equipment Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Wire and Cables for Semiconductor Equipment Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Wire and Cables for Semiconductor Equipment Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Wire and Cables for Semiconductor Equipment Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Wire and Cables for Semiconductor Equipment Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Wire and Cables for Semiconductor Equipment Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Wire and Cables for Semiconductor Equipment Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Wire and Cables for Semiconductor Equipment Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Wire and Cables for Semiconductor Equipment Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Wire and Cables for Semiconductor Equipment Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Wire and Cables for Semiconductor Equipment Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Wire and Cables for Semiconductor Equipment Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Wire and Cables for Semiconductor Equipment Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Wire and Cables for Semiconductor Equipment Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Wire and Cables for Semiconductor Equipment Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Wire and Cables for Semiconductor Equipment Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Wire and Cables for Semiconductor Equipment Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Wire and Cables for Semiconductor Equipment Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Wire and Cables for Semiconductor Equipment Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Wire and Cables for Semiconductor Equipment Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Wire and Cables for Semiconductor Equipment Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Wire and Cables for Semiconductor Equipment Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Wire and Cables for Semiconductor Equipment Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Wire and Cables for Semiconductor Equipment Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Wire and Cables for Semiconductor Equipment Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Wire and Cables for Semiconductor Equipment Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Wire and Cables for Semiconductor Equipment Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Wire and Cables for Semiconductor Equipment Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Wire and Cables for Semiconductor Equipment Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Wire and Cables for Semiconductor Equipment Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Wire and Cables for Semiconductor Equipment Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Wire and Cables for Semiconductor Equipment Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Wire and Cables for Semiconductor Equipment Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Wire and Cables for Semiconductor Equipment Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Wire and Cables for Semiconductor Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Wire and Cables for Semiconductor Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Wire and Cables for Semiconductor Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Wire and Cables for Semiconductor Equipment Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Wire and Cables for Semiconductor Equipment Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Wire and Cables for Semiconductor Equipment Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Wire and Cables for Semiconductor Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Wire and Cables for Semiconductor Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Wire and Cables for Semiconductor Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Wire and Cables for Semiconductor Equipment Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Wire and Cables for Semiconductor Equipment Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Wire and Cables for Semiconductor Equipment Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Wire and Cables for Semiconductor Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Wire and Cables for Semiconductor Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Wire and Cables for Semiconductor Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Wire and Cables for Semiconductor Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Wire and Cables for Semiconductor Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Wire and Cables for Semiconductor Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Wire and Cables for Semiconductor Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Wire and Cables for Semiconductor Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Wire and Cables for Semiconductor Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Wire and Cables for Semiconductor Equipment Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Wire and Cables for Semiconductor Equipment Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Wire and Cables for Semiconductor Equipment Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Wire and Cables for Semiconductor Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Wire and Cables for Semiconductor Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Wire and Cables for Semiconductor Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Wire and Cables for Semiconductor Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Wire and Cables for Semiconductor Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Wire and Cables for Semiconductor Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Wire and Cables for Semiconductor Equipment Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Wire and Cables for Semiconductor Equipment Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Wire and Cables for Semiconductor Equipment Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Wire and Cables for Semiconductor Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Wire and Cables for Semiconductor Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Wire and Cables for Semiconductor Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Wire and Cables for Semiconductor Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Wire and Cables for Semiconductor Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Wire and Cables for Semiconductor Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Wire and Cables for Semiconductor Equipment Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Wire and Cables for Semiconductor Equipment?

The projected CAGR is approximately 6.51%.

2. Which companies are prominent players in the Wire and Cables for Semiconductor Equipment?

Key companies in the market include TE Connectivity (TE), Alpha Wire, HELUKABEL, BizLink, Winchester Interconnect, LEONI, Oki Electric Industry, MC Electronics, Cicoil, Teledyne, Kowa Denzai Sha LTD, CHUGOKU ELECTRIC WIRE & CABLE CO., LTD., Prysmian, Nexans, LS Cable & System, TF Kable, W. L. Gore & Associates, TOTOKU INC., SAB, Daiichi Denzai (DID), NICHIGOH COMMUNICATION ELECTRIC WIRE CO., LTD..

3. What are the main segments of the Wire and Cables for Semiconductor Equipment?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Wire and Cables for Semiconductor Equipment," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Wire and Cables for Semiconductor Equipment report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Wire and Cables for Semiconductor Equipment?

To stay informed about further developments, trends, and reports in the Wire and Cables for Semiconductor Equipment, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence