Key Insights

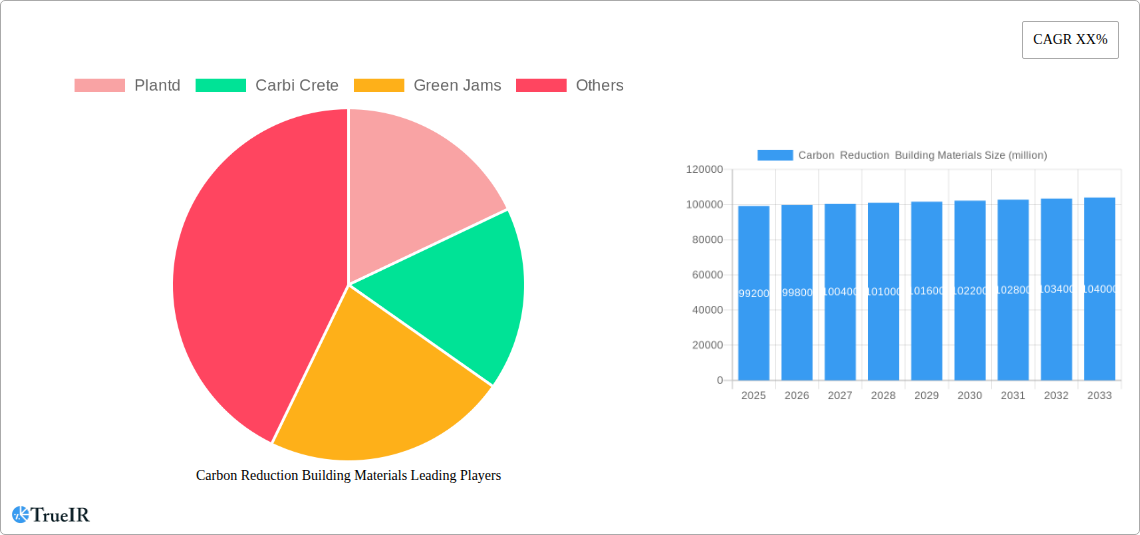

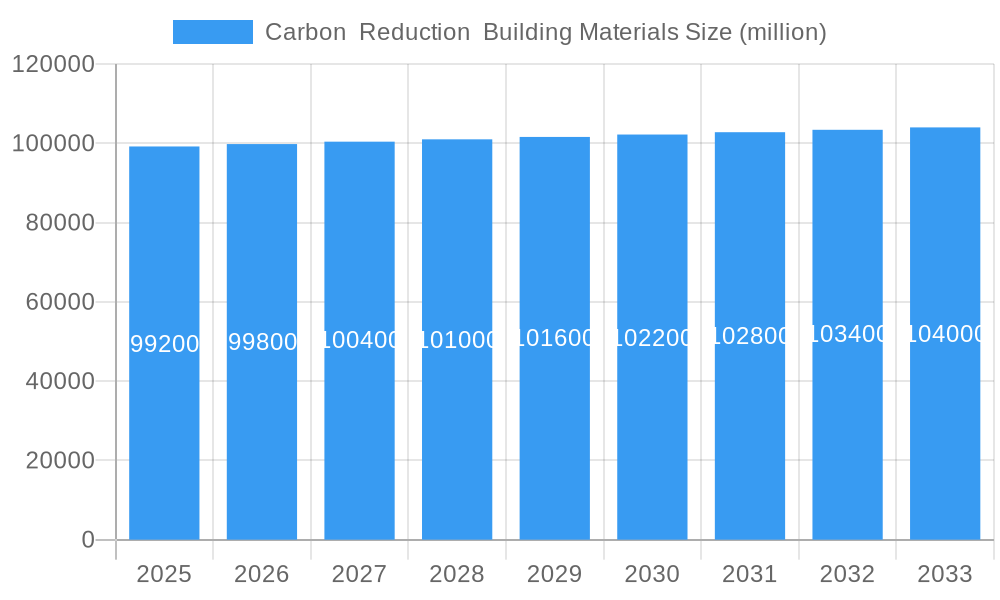

The global Carbon Reduction Building Materials market is poised for steady growth, projected to reach an estimated $99.2 billion in 2025. While the compound annual growth rate (CAGR) of 0.6% for the forecast period (2025-2033) suggests a measured expansion, this is driven by increasing regulatory pressures and a growing environmental consciousness within the construction sector. The market is being propelled by a clear demand for sustainable alternatives to traditional materials, with applications spanning industrial, civil, and public buildings. Key drivers include stringent government mandates aimed at reducing carbon footprints in construction, coupled with rising consumer and corporate awareness of the environmental impact of building practices. The development and adoption of innovative materials like low-carbon adobe brick, agricultural concrete, hempcrete, and structural wood are central to this market's evolution. These materials offer a compelling alternative by sequestering carbon, utilizing recycled content, or requiring less energy-intensive production processes, thereby addressing the urgent need for climate-resilient and eco-friendly construction solutions.

Carbon Reduction Building Materials Market Size (In Billion)

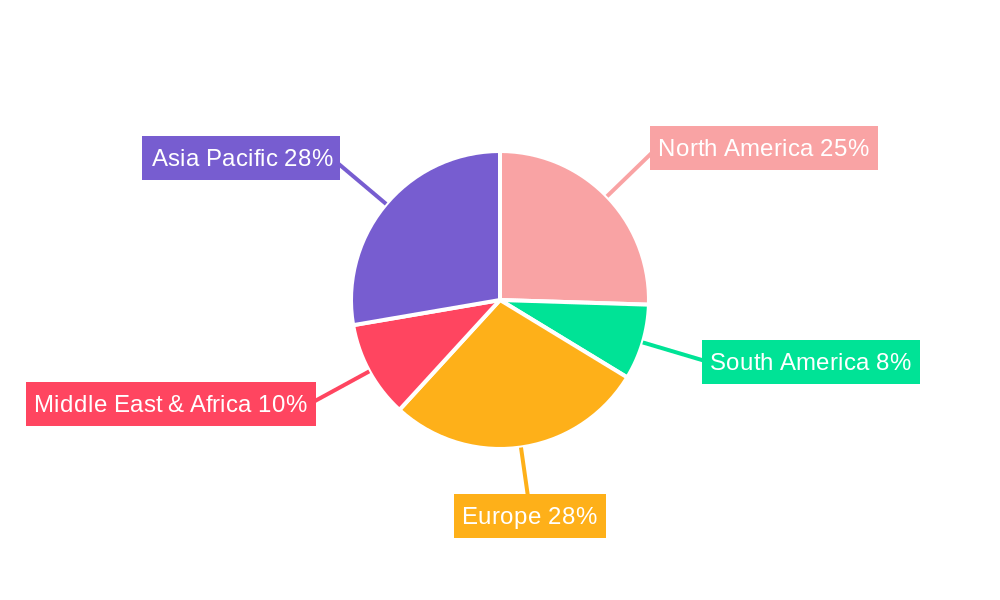

Despite the positive growth trajectory, certain restraints could temper the market's expansion. These may include higher initial costs associated with some novel carbon-reducing materials compared to conventional options, potential challenges in scaling up production to meet widespread demand, and the need for extensive education and training for architects, engineers, and construction workers to ensure proper implementation and optimal performance. Furthermore, existing building codes and standards may require updates to fully accommodate and encourage the widespread use of these emergent materials. Nevertheless, the overarching trend towards a circular economy and the global commitment to achieving net-zero emissions are powerful tailwinds. Regions like Asia Pacific, driven by rapid urbanization and significant investments in infrastructure, alongside Europe and North America, with their advanced regulatory frameworks and strong emphasis on sustainability, are expected to be key contributors to market expansion.

Carbon Reduction Building Materials Company Market Share

Carbon Reduction Building Materials Market Analysis: Unlocking Sustainable Construction Growth

This comprehensive report delves into the dynamic and rapidly evolving Carbon Reduction Building Materials market. Spanning a study period from 2019 to 2033, with a base and estimated year of 2025, and a forecast period of 2025–2033, this analysis provides deep insights into market structure, trends, opportunities, dominant segments, product innovations, key drivers, challenges, and the leading players shaping the future of sustainable construction. Leveraging high-volume keywords, this report is designed to enhance search rankings and engage industry professionals seeking to understand and capitalize on the burgeoning carbon-neutral building solutions market, with a projected market size in the billions.

Carbon Reduction Building Materials Market Structure & Competitive Landscape

The Carbon Reduction Building Materials market, with a projected global valuation in the billions of dollars, exhibits a dynamic and evolving competitive landscape. Market concentration varies significantly across regions and specific material types, with emerging players and established construction material manufacturers vying for market share. Innovation remains a primary driver, fueled by increasing environmental awareness and stringent regulatory frameworks pushing for sustainable alternatives. These regulatory impacts, including carbon pricing mechanisms and green building certifications, are compelling a significant shift in material adoption. Product substitutes are abundant, ranging from traditional materials with improved lifecycle assessments to entirely novel bio-based and recycled composites. End-user segmentation is also a critical factor, with distinct adoption rates and requirements across Industrial Building, Civil Buildings, and Public Building applications. Mergers and acquisitions (M&A) are on the rise as larger entities seek to integrate innovative sustainable material technologies and expand their product portfolios. M&A volumes are expected to reach several billion in the coming years, indicating a strong consolidation trend. The market's growth is also influenced by the increasing demand for transparency in material sourcing and production, leading to a greater emphasis on life cycle assessments and environmental product declarations.

Carbon Reduction Building Materials Market Trends & Opportunities

The global Carbon Reduction Building Materials market is poised for substantial expansion, driven by a confluence of escalating environmental concerns, supportive government policies, and growing consumer demand for sustainable living. The market size is projected to reach tens of billions by the end of the forecast period, reflecting a robust Compound Annual Growth Rate (CAGR) in the high single digits. Technological shifts are at the forefront of this growth, with continuous advancements in material science leading to the development of high-performance, low-carbon alternatives to conventional materials. This includes innovations in agricultural concrete, hempcrete, structural wood, and low-carbon adobe brick, each offering unique benefits in terms of embodied carbon reduction and performance. Consumer preferences are increasingly tilting towards eco-friendly construction solutions, not only due to environmental consciousness but also for long-term cost savings associated with energy efficiency and reduced maintenance. The competitive dynamics are intensifying, with both established construction material giants and agile startups introducing innovative products and strategies. Market penetration rates for these advanced materials are expected to accelerate, particularly in regions with aggressive climate targets and strong incentives for green building practices. Opportunities abound for companies that can offer scalable, cost-effective, and high-performing carbon reduction building materials across diverse applications, from residential and commercial to large-scale infrastructure projects. The development of circular economy principles within the building sector, focusing on material reuse and recycling, also presents a significant avenue for future growth and innovation. Furthermore, the integration of smart technologies for monitoring material performance and environmental impact throughout the building lifecycle will further enhance the appeal and adoption of carbon reduction building materials, creating a more resilient and sustainable built environment for generations to come.

Dominant Markets & Segments in Carbon Reduction Building Materials

The Carbon Reduction Building Materials market exhibits distinct dominance across various geographical regions and application segments, driven by a complex interplay of regulatory mandates, economic incentives, and infrastructure development needs. Among the applications, Industrial Building currently represents a significant market share, primarily due to the growing emphasis on reducing the embodied carbon footprint of large-scale manufacturing and logistics facilities. This is closely followed by Civil Buildings, which are experiencing a surge in demand for sustainable materials in residential and commercial construction projects, propelled by urbanisation and a rising awareness of the environmental impact of traditional building practices. Public Building projects, often subject to stringent green procurement policies, are also emerging as a key growth area. In terms of material types, Structural Wood is a dominant force, leveraging its renewable nature and carbon sequestration capabilities, with market expansion driven by advancements in engineered wood products. Agricultural Concrete, utilizing waste streams and industrial by-products, is gaining traction for its cost-effectiveness and reduced environmental impact, particularly in infrastructure projects. Hempcrete, known for its exceptional thermal insulation properties and low embodied energy, is experiencing rapid growth in the residential and commercial sectors, especially in regions with supportive building codes. Low Carbon Adobe Brick, while a more traditional material, is witnessing a resurgence due to its inherent sustainability and aesthetic appeal, finding applications in niche markets and historical restoration projects. Growth drivers for these segments include substantial government investments in green infrastructure, stringent building energy efficiency regulations, and public sector commitments to achieving net-zero emissions targets. The increasing availability of funding for sustainable construction projects further bolsters market penetration. The demand for materials that offer improved thermal performance, reduced lifecycle costs, and enhanced occupant well-being is a universal trend across all segments, accelerating the adoption of innovative carbon reduction solutions.

Carbon Reduction Building Materials Product Analysis

Innovations in Carbon Reduction Building Materials are transforming the construction industry by offering viable alternatives with significantly lower embodied carbon footprints. Products like advanced Structural Wood, engineered for enhanced strength and durability, are enabling the construction of taller and more complex structures with a reduced environmental impact. Agricultural Concrete formulations, incorporating supplementary cementitious materials and recycled aggregates, are providing cost-effective and eco-friendly solutions for foundations, pavements, and structural elements. Hempcrete, with its excellent insulative and breathable properties, is revolutionizing wall systems, contributing to energy efficiency and improved indoor air quality. Low Carbon Adobe Brick, modernized with sustainable binders and production techniques, offers a durable and aesthetically pleasing option for various construction needs. The competitive advantage of these products lies in their ability to meet stringent performance standards while actively sequestering carbon or utilizing waste materials, aligning with global sustainability goals and creating a healthier built environment.

Key Drivers, Barriers & Challenges in Carbon Reduction Building Materials

The Carbon Reduction Building Materials market is propelled by powerful drivers, including stringent global environmental regulations and carbon emission reduction targets, driving demand for sustainable alternatives. Technological advancements in material science and manufacturing processes are continually improving the performance and cost-effectiveness of low-carbon options. Economic incentives, such as tax credits and subsidies for green building, further encourage adoption. Policy-driven initiatives, like green public procurement, are also significant growth catalysts.

However, several barriers and challenges impede rapid market expansion. High upfront costs compared to conventional materials remain a significant restraint for some applications, although lifecycle cost analyses often reveal long-term savings. Supply chain complexities and the need for specialized knowledge and equipment for installation can also pose hurdles. Regulatory hurdles, including the need for updated building codes and standards to accommodate novel materials, are being addressed but still present challenges. Competitive pressures from established, cost-effective traditional materials necessitate continuous innovation and market education.

Growth Drivers in the Carbon Reduction Building Materials Market

The growth of the Carbon Reduction Building Materials market is primarily fueled by an increasing global commitment to sustainability and net-zero emission targets. Technological advancements are consistently yielding more efficient and cost-effective low-carbon materials, such as advanced bio-composites and recycled aggregate concrete. Supportive government policies, including carbon pricing, tax incentives for green construction, and stringent building energy codes, are creating a favorable regulatory environment. Economic drivers, such as rising energy costs and a growing awareness of the long-term cost benefits of sustainable buildings, are also contributing to market expansion. The demand for healthier and more resilient buildings further bolsters the adoption of natural and low-impact materials.

Challenges Impacting Carbon Reduction Building Materials Growth

Despite robust growth prospects, the Carbon Reduction Building Materials market faces several challenges. The perceived higher upfront cost of some sustainable materials compared to conventional alternatives remains a significant barrier for widespread adoption, particularly in price-sensitive markets. Regulatory complexities and the need for updated building codes and standards to fully embrace these innovative materials can slow down their integration. Supply chain issues, including the availability of raw materials and specialized manufacturing capabilities, can also present logistical hurdles. Furthermore, a lack of widespread awareness and understanding among builders, architects, and consumers about the benefits and performance of carbon reduction materials necessitates ongoing education and advocacy efforts.

Key Players Shaping the Carbon Reduction Building Materials Market

- Plantd

- Carbi Crete

- Green Jams

Significant Carbon Reduction Building Materials Industry Milestones

- 2019: Increased global focus on climate change and the Paris Agreement spurred research and development in low-carbon building materials.

- 2020: Launch of new bio-based insulation materials offering significant embodied carbon reductions.

- 2021: Growing investment in circular economy solutions for construction, promoting recycled content in building materials.

- 2022: Several governments introduced enhanced incentives and mandates for green building certifications, boosting demand for sustainable materials.

- 2023: Expansion of hempcrete adoption into larger commercial projects, demonstrating its structural capabilities.

- 2024: Advancements in agricultural concrete technology led to wider acceptance in infrastructure projects.

Future Outlook for Carbon Reduction Building Materials Market

The future outlook for the Carbon Reduction Building Materials market is exceptionally bright, driven by escalating global climate action and the urgent need to decarbonize the built environment. Anticipated growth catalysts include continued technological innovation leading to more affordable and high-performing materials, alongside increasingly stringent government regulations and carbon pricing mechanisms. Strategic opportunities lie in the expansion of material applications across industrial, civil, and public building sectors, as well as the development of integrated solutions that offer energy efficiency and improved occupant well-being. The market potential is vast, with a clear trajectory towards widespread adoption as the economic and environmental benefits of sustainable construction become increasingly undeniable, promising a substantial impact on the global construction industry and a significant contribution to climate change mitigation efforts, with market valuations projected to reach tens of billions in the coming years.

Carbon Reduction Building Materials Segmentation

-

1. Application

- 1.1. Industrial Building

- 1.2. Civil Buildings

- 1.3. Public Building

- 1.4. Others

-

2. Types

- 2.1. Low Carbon Adobe Brick

- 2.2. Agricultural Concrete

- 2.3. Hempcrete

- 2.4. Structural Wood

Carbon Reduction Building Materials Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Carbon Reduction Building Materials Regional Market Share

Geographic Coverage of Carbon Reduction Building Materials

Carbon Reduction Building Materials REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 14% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Carbon Reduction Building Materials Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Industrial Building

- 5.1.2. Civil Buildings

- 5.1.3. Public Building

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Low Carbon Adobe Brick

- 5.2.2. Agricultural Concrete

- 5.2.3. Hempcrete

- 5.2.4. Structural Wood

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Carbon Reduction Building Materials Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Industrial Building

- 6.1.2. Civil Buildings

- 6.1.3. Public Building

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Low Carbon Adobe Brick

- 6.2.2. Agricultural Concrete

- 6.2.3. Hempcrete

- 6.2.4. Structural Wood

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Carbon Reduction Building Materials Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Industrial Building

- 7.1.2. Civil Buildings

- 7.1.3. Public Building

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Low Carbon Adobe Brick

- 7.2.2. Agricultural Concrete

- 7.2.3. Hempcrete

- 7.2.4. Structural Wood

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Carbon Reduction Building Materials Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Industrial Building

- 8.1.2. Civil Buildings

- 8.1.3. Public Building

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Low Carbon Adobe Brick

- 8.2.2. Agricultural Concrete

- 8.2.3. Hempcrete

- 8.2.4. Structural Wood

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Carbon Reduction Building Materials Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Industrial Building

- 9.1.2. Civil Buildings

- 9.1.3. Public Building

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Low Carbon Adobe Brick

- 9.2.2. Agricultural Concrete

- 9.2.3. Hempcrete

- 9.2.4. Structural Wood

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Carbon Reduction Building Materials Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Industrial Building

- 10.1.2. Civil Buildings

- 10.1.3. Public Building

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Low Carbon Adobe Brick

- 10.2.2. Agricultural Concrete

- 10.2.3. Hempcrete

- 10.2.4. Structural Wood

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Plantd

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Carbi Crete

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Green Jams

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.1 Plantd

List of Figures

- Figure 1: Global Carbon Reduction Building Materials Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Carbon Reduction Building Materials Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Carbon Reduction Building Materials Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Carbon Reduction Building Materials Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Carbon Reduction Building Materials Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Carbon Reduction Building Materials Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Carbon Reduction Building Materials Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Carbon Reduction Building Materials Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Carbon Reduction Building Materials Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Carbon Reduction Building Materials Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Carbon Reduction Building Materials Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Carbon Reduction Building Materials Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Carbon Reduction Building Materials Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Carbon Reduction Building Materials Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Carbon Reduction Building Materials Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Carbon Reduction Building Materials Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Carbon Reduction Building Materials Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Carbon Reduction Building Materials Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Carbon Reduction Building Materials Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Carbon Reduction Building Materials Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Carbon Reduction Building Materials Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Carbon Reduction Building Materials Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Carbon Reduction Building Materials Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Carbon Reduction Building Materials Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Carbon Reduction Building Materials Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Carbon Reduction Building Materials Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Carbon Reduction Building Materials Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Carbon Reduction Building Materials Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Carbon Reduction Building Materials Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Carbon Reduction Building Materials Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Carbon Reduction Building Materials Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Carbon Reduction Building Materials Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Carbon Reduction Building Materials Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Carbon Reduction Building Materials Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Carbon Reduction Building Materials Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Carbon Reduction Building Materials Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Carbon Reduction Building Materials Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Carbon Reduction Building Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Carbon Reduction Building Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Carbon Reduction Building Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Carbon Reduction Building Materials Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Carbon Reduction Building Materials Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Carbon Reduction Building Materials Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Carbon Reduction Building Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Carbon Reduction Building Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Carbon Reduction Building Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Carbon Reduction Building Materials Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Carbon Reduction Building Materials Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Carbon Reduction Building Materials Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Carbon Reduction Building Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Carbon Reduction Building Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Carbon Reduction Building Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Carbon Reduction Building Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Carbon Reduction Building Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Carbon Reduction Building Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Carbon Reduction Building Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Carbon Reduction Building Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Carbon Reduction Building Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Carbon Reduction Building Materials Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Carbon Reduction Building Materials Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Carbon Reduction Building Materials Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Carbon Reduction Building Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Carbon Reduction Building Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Carbon Reduction Building Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Carbon Reduction Building Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Carbon Reduction Building Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Carbon Reduction Building Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Carbon Reduction Building Materials Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Carbon Reduction Building Materials Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Carbon Reduction Building Materials Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Carbon Reduction Building Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Carbon Reduction Building Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Carbon Reduction Building Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Carbon Reduction Building Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Carbon Reduction Building Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Carbon Reduction Building Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Carbon Reduction Building Materials Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Carbon Reduction Building Materials?

The projected CAGR is approximately 14%.

2. Which companies are prominent players in the Carbon Reduction Building Materials?

Key companies in the market include Plantd, Carbi Crete, Green Jams.

3. What are the main segments of the Carbon Reduction Building Materials?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Carbon Reduction Building Materials," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Carbon Reduction Building Materials report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Carbon Reduction Building Materials?

To stay informed about further developments, trends, and reports in the Carbon Reduction Building Materials, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence