Key Insights into the Medical Cold Plasma Market

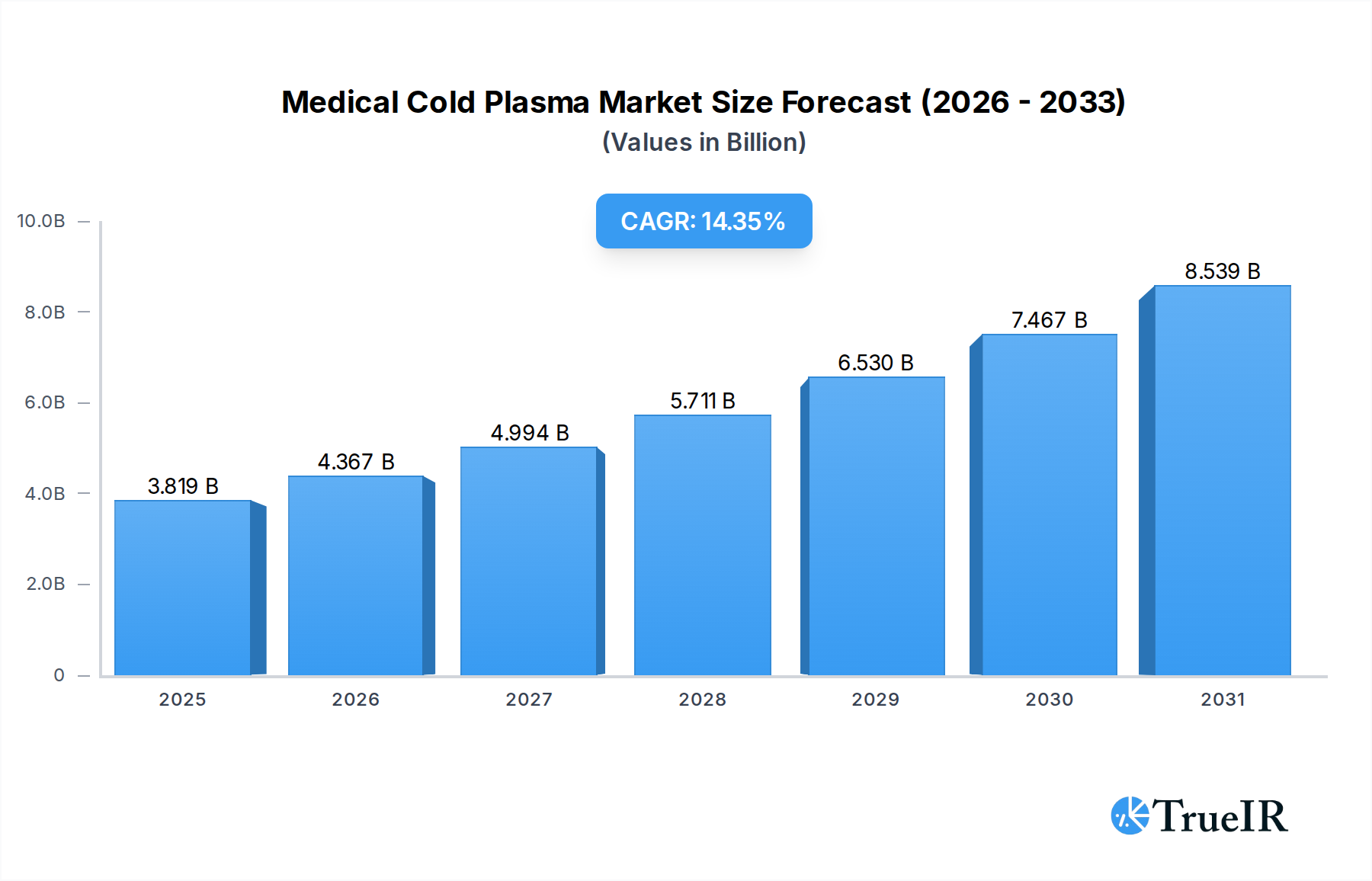

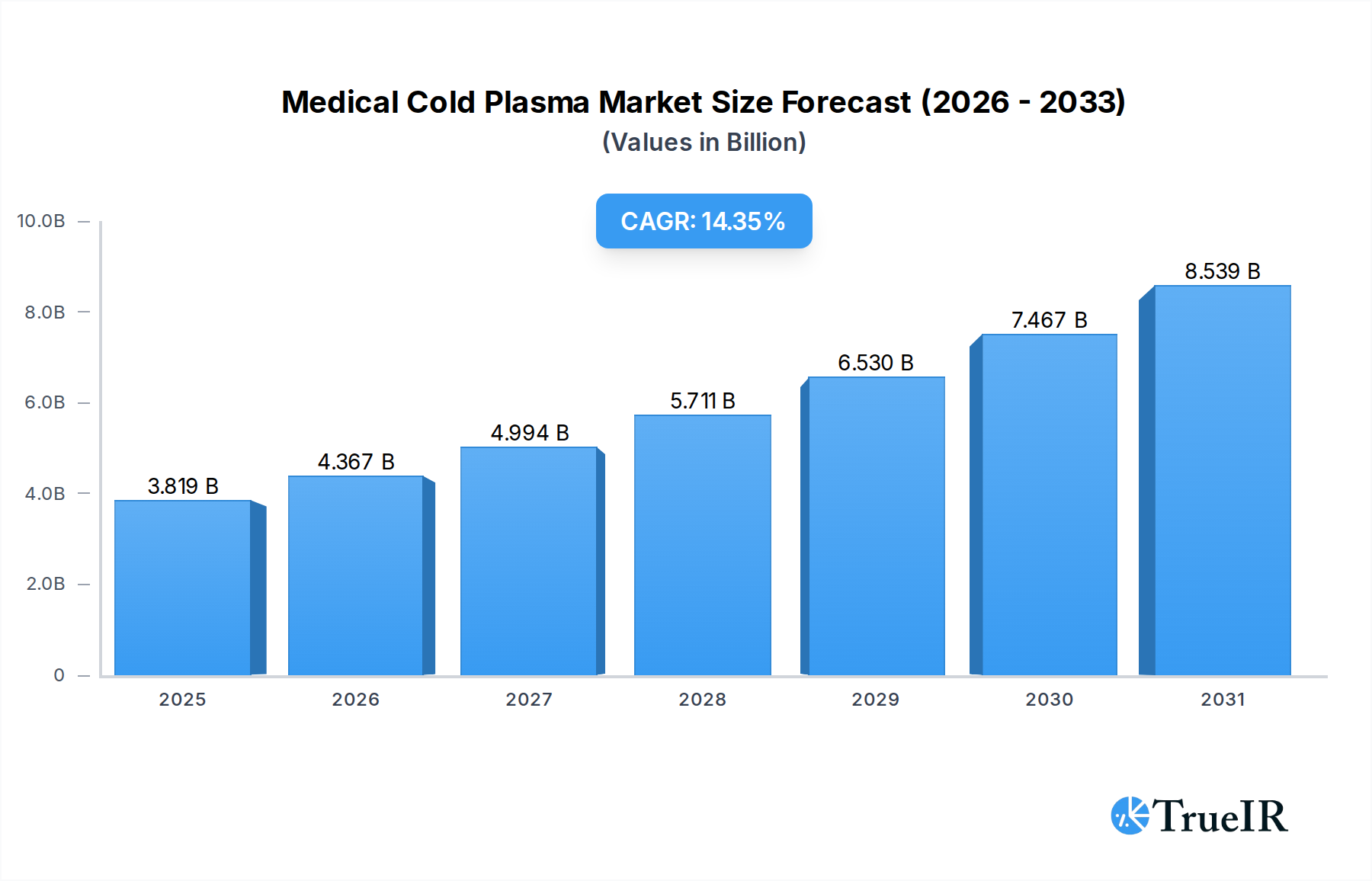

The Medical Cold Plasma Market is poised for substantial expansion, driven by its diverse applications in wound care, sterilization, and oncology. Valued at $3.34 billion in 2025, the market is projected to reach approximately $9.94 billion by 2033, demonstrating a robust Compound Annual Growth Rate (CAGR) of 14.35% over the forecast period. This significant growth trajectory is underpinned by several macro-economic and clinical tailwinds, including the rising global prevalence of chronic wounds, the urgent need for advanced infection control solutions amidst growing antimicrobial resistance, and increasing demand for minimally invasive medical procedures.

Medical Cold Plasma Market Size (In Billion)

Cold plasma technology, characterized by its ability to generate reactive species at low temperatures, offers distinct advantages, such as broad-spectrum antimicrobial efficacy, enhanced tissue regeneration, and minimal side effects, making it a compelling alternative to conventional therapies. The integration of cold plasma into various medical devices and therapeutic modalities is expanding, particularly within the Hospitals and Clinics Market. Innovations in device portability and enhanced treatment precision are further catalyzing market penetration. While regulatory challenges and the initial cost of devices present notable restraints, the compelling clinical outcomes and expanding evidence base are expected to outweigh these hurdles. The broader Plasma Technology Market is seeing significant investment, contributing to the advancements in medical applications. Geographically, North America and Europe currently hold significant market shares due to advanced healthcare infrastructures and high adoption rates, while the Asia Pacific region is anticipated to exhibit the fastest growth, propelled by increasing healthcare expenditure and a large patient demographic. The outlook for the Medical Cold Plasma Market remains highly optimistic, with continuous R&D leading to new applications and broader clinical acceptance, particularly as the demand for advanced, non-pharmacological treatment options escalates across the healthcare continuum.

Medical Cold Plasma Company Market Share

Wound Care & Dermatology Segment Dominance in Medical Cold Plasma Market

The Wound Care & Dermatology application segment currently holds the largest revenue share within the Medical Cold Plasma Market and is anticipated to maintain its dominant position throughout the forecast period. This supremacy is largely attributed to the alarmingly high prevalence of chronic wounds, such as diabetic foot ulcers, venous leg ulcers, and pressure ulcers, which affect millions globally and represent a significant burden on healthcare systems. Cold plasma’s unique properties, including its ability to effectively inactivate a wide range of microorganisms (bacteria, viruses, fungi, and spores), disrupt biofilms, and promote angiogenesis and tissue regeneration, make it an ideal therapeutic modality for complex wound management. Its non-thermal nature also ensures minimal damage to surrounding healthy tissue, enhancing patient comfort and recovery outcomes.

Key players like Neoplas med GmbH and Terraplasma Medical have established strong footholds in this segment, offering specialized devices designed for dermatological and wound healing applications. The effectiveness of cold plasma in addressing issues like antibiotic-resistant infections further solidifies its value proposition in wound care, which is particularly critical given the global challenge of antimicrobial resistance. While other application areas such as Oncology Treatment Market and Infection Control Market are experiencing rapid growth, the sheer volume of chronic wound cases and the proven clinical efficacy of cold plasma in this domain ensure its continued leadership. The market for Wound Care Devices Market is continuously evolving with new product developments, and cold plasma devices are increasingly being integrated as a standard of care. Despite potential competition from traditional and advanced wound care therapies, the demonstrated ability of cold plasma to accelerate healing, reduce infection rates, and improve quality of life for patients with difficult-to-treat wounds cements its leading role in the Medical Cold Plasma Market.

Key Market Drivers & Constraints in Medical Cold Plasma Market

The Medical Cold Plasma Market is influenced by a complex interplay of demand drivers and operational constraints, shaping its growth trajectory and market dynamics.

Drivers:

- Rising Incidence of Chronic Wounds and Infections: The global aging population and increasing prevalence of chronic diseases like diabetes contribute significantly to the burden of chronic wounds, which often require advanced treatment modalities. Approximately 2% of the population in developed countries suffers from chronic wounds, creating substantial demand for effective solutions. Cold plasma offers a novel approach to accelerate healing, reduce infection, and manage biofilms. Furthermore, the growing concern over healthcare-associated infections (HAIs) and surgical site infections (SSIs) is fueling the adoption of medical-grade sterilization technologies, where cold plasma demonstrates significant efficacy.

- Growing Threat of Antimicrobial Resistance (AMR): The diminishing effectiveness of conventional antibiotics due to AMR necessitates alternative antimicrobial strategies. Cold plasma, with its broad-spectrum antimicrobial properties against multi-drug resistant pathogens, provides a promising non-pharmacological solution. Reports from the World Health Organization (WHO) consistently highlight AMR as a global health crisis, driving research and adoption of technologies like cold plasma in the Infection Control Market. This critical need positions cold plasma as a vital tool in combating resistant infections across various medical settings.

Constraints:

- High Initial Cost of Devices and Evolving Reimbursement Landscape: The capital expenditure for Medical Cold Plasma Market devices can be substantial, with systems potentially costing upwards of $20,000 to $50,000 or more, which can be a barrier for budget-constrained hospitals and clinics. Additionally, the reimbursement landscape for cold plasma therapies is still evolving in many regions. Lack of standardized and comprehensive reimbursement codes can deter widespread adoption, as healthcare providers may face challenges in recouping treatment costs, thereby impacting the return on investment for new equipment.

- Stringent Regulatory Approvals and Lack of Standardized Protocols: Medical cold plasma devices are subject to rigorous regulatory scrutiny by bodies like the FDA in the U.S. and EMA in Europe. The long and costly approval processes, coupled with the requirement for extensive clinical evidence, prolong market entry. Moreover, the lack of universally standardized treatment protocols across different applications and device types can lead to variability in clinical outcomes and hinder broader clinical acceptance, demanding more robust and harmonized guidelines for consistent application.

Competitive Ecosystem of Medical Cold Plasma Market

The Medical Cold Plasma Market is characterized by the presence of several specialized companies alongside diversified medical technology players, all striving to innovate and expand the therapeutic applications of cold plasma. The competitive landscape is shaped by ongoing research, product development, and strategic partnerships aimed at broadening market reach and clinical utility.

- Apyx Medical Corporation: A key innovator in advanced energy-based surgical platforms, Apyx Medical Corporation is known for its J-Plasma®/Renuvion® technology, which leverages helium plasma for various dermatological and surgical applications, driving advancements in precision energy delivery.

- ADTEC Plasma Technology Co. Ltd.: A prominent player with a global footprint, ADTEC specializes in advanced plasma technology across multiple sectors, including medical applications, focusing on high-performance plasma sources and systems for research and clinical use.

- Neoplas med GmbH: This German company is a specialist in medical plasma technology, developing and distributing CE-marked cold atmospheric plasma devices for dermatological conditions and wound treatment, emphasizing clinical efficacy and patient safety.

- Terraplasma Medical: A pioneer in the field, Terraplasma Medical develops medical devices utilizing cold atmospheric plasma, with a strong focus on effective wound treatment and disinfection, and is known for its scientific backing and robust product pipeline.

- GD Medical: Primarily a distributor of innovative medical solutions, GD Medical often partners with technology leaders to bring advanced therapeutic and diagnostic products, including cold plasma systems, to healthcare providers.

- Olympus: A global leader in medical technology, Olympus offers a wide array of endoscopy, surgical, and diagnostic solutions. While not a primary cold plasma developer, its extensive market presence and R&D capabilities suggest potential future integration or partnerships in plasma-based therapies.

- PlasmaDerm: Focused on developing cold atmospheric plasma devices for medical use, PlasmaDerm emphasizes non-invasive treatments for skin diseases and wound healing, backed by scientific research and clinical studies.

- Adtec Healthcare: Building on general plasma technology expertise, Adtec Healthcare applies its knowledge to therapeutic plasma solutions for medical applications, including sterilization and tissue treatment.

- Nova Plasma: An emerging company dedicated to leveraging cold plasma technology for innovative medical treatments, focusing on developing new applications and improving existing plasma devices for broader clinical utility.

- Others: This category includes a dynamic group of smaller start-ups, academic spin-offs, and research institutions continually pushing the boundaries of cold plasma applications, often specializing in niche areas or developing next-generation plasma sources.

Recent Developments & Milestones in Medical Cold Plasma Market

The Medical Cold Plasma Market has witnessed several strategic advancements and innovations, reflecting the industry's commitment to expanding therapeutic applications and market accessibility.

- March 2025: Apyx Medical Corporation received an expanded indication for its J-Plasma® system from a major regulatory body in a key regional market, allowing its use for additional dermatological resurfacing procedures, broadening its clinical utility.

- November 2024: Neoplas med GmbH announced a significant strategic partnership with a consortium of leading European hospital groups, aiming for the broader adoption and integration of its plasmajet® system in chronic wound care clinics across the region.

- July 2024: Terraplasma Medical launched its innovative new portable atmospheric pressure cold plasma device, specifically designed for home healthcare settings, enhancing patient access to advanced wound treatment and post-operative care.

- February 2024: ADTEC Plasma Technology Co. Ltd. unveiled advancements in their high-efficiency plasma sterilization systems, targeting critical medical device reprocessing for sensitive instruments, thereby improving hospital infection control protocols.

- October 2023: Results from a large-scale, multi-center clinical trial were published, definitively demonstrating the superior efficacy of cold plasma in reducing bacterial load and promoting accelerated healing in chronic diabetic foot ulcers compared to standard care, significantly bolstering clinical confidence and investment interest in the sector.

Regional Market Breakdown for Medical Cold Plasma Market

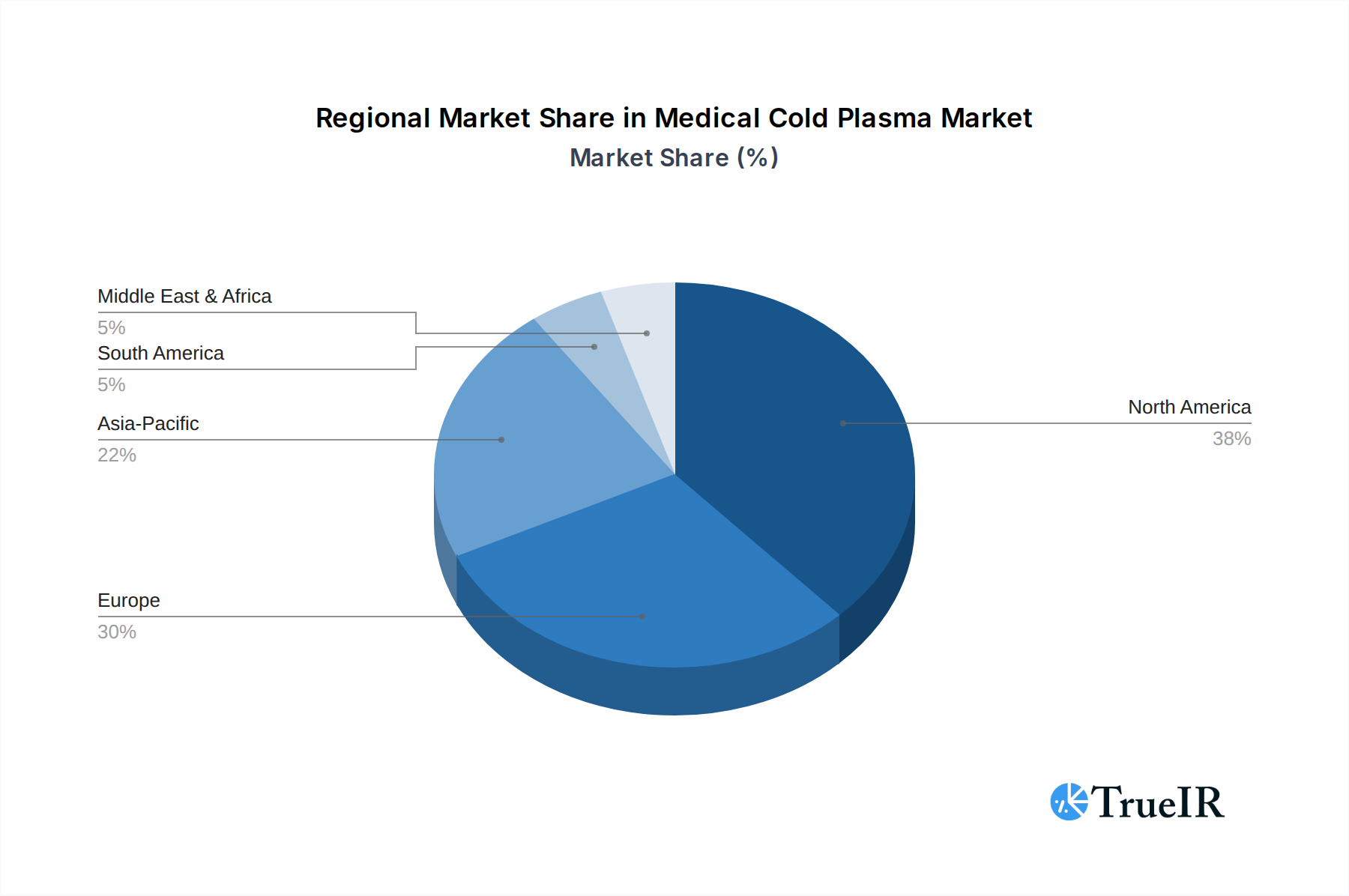

The Medical Cold Plasma Market exhibits distinct regional dynamics, influenced by healthcare infrastructure, regulatory environments, prevalence of target conditions, and technological adoption rates. These variations contribute to differing market shares and growth trajectories across key geographical segments.

North America currently leads the Medical Cold Plasma Market, holding an estimated 38-40% revenue share. This dominance is primarily driven by substantial healthcare expenditure, a well-established medical device industry, high awareness and rapid adoption of advanced technologies, and a significant burden of chronic diseases such as diabetes and associated chronic wounds. The region is projected to grow at a CAGR of approximately 13.5%, sustained by continuous R&D investment and favorable reimbursement policies. The United States, in particular, is a stronghold for innovation and market expansion.

Europe represents the second-largest market, accounting for an estimated 32-35% share. The region benefits from robust government support for research, a high geriatric population contributing to chronic wound incidence, and stringent regulatory standards that ensure high-quality medical devices. Countries like Germany, France, and the UK are at the forefront of cold plasma research and clinical integration. Europe is expected to record a healthy CAGR of around 14.0%, propelled by increasing clinical evidence and expanding application areas.

The Asia Pacific region is anticipated to be the fastest-growing market, projected at a formidable CAGR of approximately 16.5%. This rapid expansion is fueled by increasing healthcare spending, improving healthcare infrastructure, a vast and aging population leading to a higher prevalence of chronic diseases, and rising awareness of advanced treatment options. Countries like China, India, and Japan are emerging as significant growth engines due to their large patient pools and growing medical tourism sector. The rising demand for sophisticated healthcare solutions and the expanding Medical Devices Market are key demand drivers here.

Middle East & Africa (MEA) and South America collectively constitute a smaller, yet rapidly emerging, segment of the Medical Cold Plasma Market. While their current market shares are lower, both regions demonstrate significant growth potential. Improving economic conditions, increasing access to healthcare, and a rising focus on advanced medical technologies are stimulating market expansion. Investment in healthcare infrastructure and growing awareness of cold plasma's benefits are expected to drive robust growth in these developing markets over the forecast period.

Medical Cold Plasma Regional Market Share

Supply Chain & Raw Material Dynamics for Medical Cold Plasma Market

The supply chain for the Medical Cold Plasma Market is intricate, involving a range of specialized components and raw materials that are crucial for device manufacturing and operation. Upstream dependencies include high-purity noble gases, precision power supply components, and specialized electrodes, which together constitute the core functional elements of cold plasma systems. Noble gases such as argon and helium are essential for plasma generation, and their availability and price stability are critical. The Medical Electronics Market provides the sophisticated power supplies and control systems necessary for precise plasma delivery.

Sourcing risks are notable, particularly concerning the supply of noble gases, which can be susceptible to geopolitical events, industrial accidents affecting production facilities, and fluctuating global demand. For instance, price volatility in noble gases, like xenon, has historically impacted manufacturing costs in other high-tech industries, a risk that extends to the medical plasma sector. Specialized electrode materials and dielectric barrier discharge (DBD) components also require specific manufacturing processes, leading to a relatively concentrated supplier base. Any disruption to these specialized component manufacturers can lead to production delays and increased costs for device makers.

Historically, global supply chain disruptions, such as those experienced during the COVID-19 pandemic, have highlighted vulnerabilities in the sourcing of microchips and other electronic components vital for the control units of cold plasma devices. These disruptions have sometimes led to increased lead times and higher procurement costs. Manufacturers in the Medical Cold Plasma Market often adopt strategies like dual-sourcing, building inventory buffers, and engaging in long-term supply agreements to mitigate these risks. The overall trend indicates a need for robust supplier relationship management and careful monitoring of global commodity markets to ensure stable and cost-effective production.

Pricing Dynamics & Margin Pressure in Medical Cold Plasma Market

The pricing dynamics in the Medical Cold Plasma Market are complex, reflecting the interplay of high R&D costs, regulatory hurdles, manufacturing complexities, and market competition. Average Selling Prices (ASPs) for cold plasma devices tend to be at a premium compared to conventional therapies, ranging from several thousand to tens of thousands of dollars per system, depending on the device’s capabilities, portability, and target application. This premium pricing is justified by the advanced technology, proven clinical efficacy, and the substantial investment required for product development and regulatory approvals.

Margin structures across the value chain typically show high gross margins for manufacturers, often in the range of 60-80%. However, significant investment in R&D, clinical trials, sales, marketing, and post-market surveillance compresses net profit margins. Furthermore, a substantial portion of revenue is often generated through recurring sales of consumables, such as specialized plasma tips, gas cylinders, and disposable accessories, which offer consistent margin streams. These consumables play a crucial role in the overall profitability model for manufacturers in the Medical Cold Plasma Market.

Key cost levers for manufacturers include optimizing the Bill of Materials (BoM) by negotiating with suppliers for components like noble gases and Medical Electronics Market parts, achieving economies of scale in manufacturing, and streamlining production processes. Automation in assembly and quality control can also reduce labor costs. Competitive intensity, particularly from alternative advanced wound care therapies and new entrants offering more cost-effective solutions, exerts continuous pressure on pricing. Additionally, the shift towards value-based healthcare models is compelling manufacturers to demonstrate the long-term cost-effectiveness of cold plasma treatments, not just initial efficacy. This necessitates a clear economic value proposition that highlights reduced hospital stays, lower rates of infection, and improved patient outcomes to sustain premium pricing and maintain healthy profit margins in a rapidly evolving market.

Medical Cold Plasma Segmentation

- 1. Type

- 1.1. Low-Pressure Cold Plasma

- 1.2. Atmospheric Pressure Cold Plasma

- 2. Product Type

- 2.1. Direct Plasma Systems

- 2.2. Indirect (Remote) Plasma Systems

- 3. End-user

- 3.1. Hospitals & Clinics

- 3.2. Ambulatory Surgical Centers

- 3.3. Medical & Biotechnology Research Institutes

- 3.4. Others

- 4. Application

- 4.1. Wound Care & Dermatology

- 4.2. Surface Sterilization & Disinfection

- 4.3. Oncology

- 4.4. Dentistry & Oral Care

- 4.5. Infection Control & Sterilization

- 4.6. Others

Medical Cold Plasma Segmentation By Geography

- 1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

- 2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

- 3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

- 4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

- 5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Medical Cold Plasma Regional Market Share

Geographic Coverage of Medical Cold Plasma

Medical Cold Plasma REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 14.35% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Low-Pressure Cold Plasma

- 5.1.2. Atmospheric Pressure Cold Plasma

- 5.2. Market Analysis, Insights and Forecast - by Product Type

- 5.2.1. Direct Plasma Systems

- 5.2.2. Indirect (Remote) Plasma Systems

- 5.3. Market Analysis, Insights and Forecast - by End-user

- 5.3.1. Hospitals & Clinics

- 5.3.2. Ambulatory Surgical Centers

- 5.3.3. Medical & Biotechnology Research Institutes

- 5.3.4. Others

- 5.4. Market Analysis, Insights and Forecast - by Application

- 5.4.1. Wound Care & Dermatology

- 5.4.2. Surface Sterilization & Disinfection

- 5.4.3. Oncology

- 5.4.4. Dentistry & Oral Care

- 5.4.5. Infection Control & Sterilization

- 5.4.6. Others

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. North America

- 5.5.2. South America

- 5.5.3. Europe

- 5.5.4. Middle East & Africa

- 5.5.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Global Medical Cold Plasma Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Low-Pressure Cold Plasma

- 6.1.2. Atmospheric Pressure Cold Plasma

- 6.2. Market Analysis, Insights and Forecast - by Product Type

- 6.2.1. Direct Plasma Systems

- 6.2.2. Indirect (Remote) Plasma Systems

- 6.3. Market Analysis, Insights and Forecast - by End-user

- 6.3.1. Hospitals & Clinics

- 6.3.2. Ambulatory Surgical Centers

- 6.3.3. Medical & Biotechnology Research Institutes

- 6.3.4. Others

- 6.4. Market Analysis, Insights and Forecast - by Application

- 6.4.1. Wound Care & Dermatology

- 6.4.2. Surface Sterilization & Disinfection

- 6.4.3. Oncology

- 6.4.4. Dentistry & Oral Care

- 6.4.5. Infection Control & Sterilization

- 6.4.6. Others

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. North America Medical Cold Plasma Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Low-Pressure Cold Plasma

- 7.1.2. Atmospheric Pressure Cold Plasma

- 7.2. Market Analysis, Insights and Forecast - by Product Type

- 7.2.1. Direct Plasma Systems

- 7.2.2. Indirect (Remote) Plasma Systems

- 7.3. Market Analysis, Insights and Forecast - by End-user

- 7.3.1. Hospitals & Clinics

- 7.3.2. Ambulatory Surgical Centers

- 7.3.3. Medical & Biotechnology Research Institutes

- 7.3.4. Others

- 7.4. Market Analysis, Insights and Forecast - by Application

- 7.4.1. Wound Care & Dermatology

- 7.4.2. Surface Sterilization & Disinfection

- 7.4.3. Oncology

- 7.4.4. Dentistry & Oral Care

- 7.4.5. Infection Control & Sterilization

- 7.4.6. Others

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. South America Medical Cold Plasma Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Low-Pressure Cold Plasma

- 8.1.2. Atmospheric Pressure Cold Plasma

- 8.2. Market Analysis, Insights and Forecast - by Product Type

- 8.2.1. Direct Plasma Systems

- 8.2.2. Indirect (Remote) Plasma Systems

- 8.3. Market Analysis, Insights and Forecast - by End-user

- 8.3.1. Hospitals & Clinics

- 8.3.2. Ambulatory Surgical Centers

- 8.3.3. Medical & Biotechnology Research Institutes

- 8.3.4. Others

- 8.4. Market Analysis, Insights and Forecast - by Application

- 8.4.1. Wound Care & Dermatology

- 8.4.2. Surface Sterilization & Disinfection

- 8.4.3. Oncology

- 8.4.4. Dentistry & Oral Care

- 8.4.5. Infection Control & Sterilization

- 8.4.6. Others

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Europe Medical Cold Plasma Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Low-Pressure Cold Plasma

- 9.1.2. Atmospheric Pressure Cold Plasma

- 9.2. Market Analysis, Insights and Forecast - by Product Type

- 9.2.1. Direct Plasma Systems

- 9.2.2. Indirect (Remote) Plasma Systems

- 9.3. Market Analysis, Insights and Forecast - by End-user

- 9.3.1. Hospitals & Clinics

- 9.3.2. Ambulatory Surgical Centers

- 9.3.3. Medical & Biotechnology Research Institutes

- 9.3.4. Others

- 9.4. Market Analysis, Insights and Forecast - by Application

- 9.4.1. Wound Care & Dermatology

- 9.4.2. Surface Sterilization & Disinfection

- 9.4.3. Oncology

- 9.4.4. Dentistry & Oral Care

- 9.4.5. Infection Control & Sterilization

- 9.4.6. Others

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Middle East & Africa Medical Cold Plasma Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Low-Pressure Cold Plasma

- 10.1.2. Atmospheric Pressure Cold Plasma

- 10.2. Market Analysis, Insights and Forecast - by Product Type

- 10.2.1. Direct Plasma Systems

- 10.2.2. Indirect (Remote) Plasma Systems

- 10.3. Market Analysis, Insights and Forecast - by End-user

- 10.3.1. Hospitals & Clinics

- 10.3.2. Ambulatory Surgical Centers

- 10.3.3. Medical & Biotechnology Research Institutes

- 10.3.4. Others

- 10.4. Market Analysis, Insights and Forecast - by Application

- 10.4.1. Wound Care & Dermatology

- 10.4.2. Surface Sterilization & Disinfection

- 10.4.3. Oncology

- 10.4.4. Dentistry & Oral Care

- 10.4.5. Infection Control & Sterilization

- 10.4.6. Others

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Asia Pacific Medical Cold Plasma Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Type

- 11.1.1. Low-Pressure Cold Plasma

- 11.1.2. Atmospheric Pressure Cold Plasma

- 11.2. Market Analysis, Insights and Forecast - by Product Type

- 11.2.1. Direct Plasma Systems

- 11.2.2. Indirect (Remote) Plasma Systems

- 11.3. Market Analysis, Insights and Forecast - by End-user

- 11.3.1. Hospitals & Clinics

- 11.3.2. Ambulatory Surgical Centers

- 11.3.3. Medical & Biotechnology Research Institutes

- 11.3.4. Others

- 11.4. Market Analysis, Insights and Forecast - by Application

- 11.4.1. Wound Care & Dermatology

- 11.4.2. Surface Sterilization & Disinfection

- 11.4.3. Oncology

- 11.4.4. Dentistry & Oral Care

- 11.4.5. Infection Control & Sterilization

- 11.4.6. Others

- 11.1. Market Analysis, Insights and Forecast - by Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Apyx Medical Corporation

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 ADTEC Plasma Technology Co. Ltd.

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Neoplas med GmbH

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Terraplasma Medical

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 GD Medical

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Olympus

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 PlasmaDerm

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Adtec Healthcare

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Nova Plasma

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Others

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Apyx Medical Corporation

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Medical Cold Plasma Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Medical Cold Plasma Revenue (billion), by Type 2025 & 2033

- Figure 3: North America Medical Cold Plasma Revenue Share (%), by Type 2025 & 2033

- Figure 4: North America Medical Cold Plasma Revenue (billion), by Product Type 2025 & 2033

- Figure 5: North America Medical Cold Plasma Revenue Share (%), by Product Type 2025 & 2033

- Figure 6: North America Medical Cold Plasma Revenue (billion), by End-user 2025 & 2033

- Figure 7: North America Medical Cold Plasma Revenue Share (%), by End-user 2025 & 2033

- Figure 8: North America Medical Cold Plasma Revenue (billion), by Application 2025 & 2033

- Figure 9: North America Medical Cold Plasma Revenue Share (%), by Application 2025 & 2033

- Figure 10: North America Medical Cold Plasma Revenue (billion), by Country 2025 & 2033

- Figure 11: North America Medical Cold Plasma Revenue Share (%), by Country 2025 & 2033

- Figure 12: South America Medical Cold Plasma Revenue (billion), by Type 2025 & 2033

- Figure 13: South America Medical Cold Plasma Revenue Share (%), by Type 2025 & 2033

- Figure 14: South America Medical Cold Plasma Revenue (billion), by Product Type 2025 & 2033

- Figure 15: South America Medical Cold Plasma Revenue Share (%), by Product Type 2025 & 2033

- Figure 16: South America Medical Cold Plasma Revenue (billion), by End-user 2025 & 2033

- Figure 17: South America Medical Cold Plasma Revenue Share (%), by End-user 2025 & 2033

- Figure 18: South America Medical Cold Plasma Revenue (billion), by Application 2025 & 2033

- Figure 19: South America Medical Cold Plasma Revenue Share (%), by Application 2025 & 2033

- Figure 20: South America Medical Cold Plasma Revenue (billion), by Country 2025 & 2033

- Figure 21: South America Medical Cold Plasma Revenue Share (%), by Country 2025 & 2033

- Figure 22: Europe Medical Cold Plasma Revenue (billion), by Type 2025 & 2033

- Figure 23: Europe Medical Cold Plasma Revenue Share (%), by Type 2025 & 2033

- Figure 24: Europe Medical Cold Plasma Revenue (billion), by Product Type 2025 & 2033

- Figure 25: Europe Medical Cold Plasma Revenue Share (%), by Product Type 2025 & 2033

- Figure 26: Europe Medical Cold Plasma Revenue (billion), by End-user 2025 & 2033

- Figure 27: Europe Medical Cold Plasma Revenue Share (%), by End-user 2025 & 2033

- Figure 28: Europe Medical Cold Plasma Revenue (billion), by Application 2025 & 2033

- Figure 29: Europe Medical Cold Plasma Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Medical Cold Plasma Revenue (billion), by Country 2025 & 2033

- Figure 31: Europe Medical Cold Plasma Revenue Share (%), by Country 2025 & 2033

- Figure 32: Middle East & Africa Medical Cold Plasma Revenue (billion), by Type 2025 & 2033

- Figure 33: Middle East & Africa Medical Cold Plasma Revenue Share (%), by Type 2025 & 2033

- Figure 34: Middle East & Africa Medical Cold Plasma Revenue (billion), by Product Type 2025 & 2033

- Figure 35: Middle East & Africa Medical Cold Plasma Revenue Share (%), by Product Type 2025 & 2033

- Figure 36: Middle East & Africa Medical Cold Plasma Revenue (billion), by End-user 2025 & 2033

- Figure 37: Middle East & Africa Medical Cold Plasma Revenue Share (%), by End-user 2025 & 2033

- Figure 38: Middle East & Africa Medical Cold Plasma Revenue (billion), by Application 2025 & 2033

- Figure 39: Middle East & Africa Medical Cold Plasma Revenue Share (%), by Application 2025 & 2033

- Figure 40: Middle East & Africa Medical Cold Plasma Revenue (billion), by Country 2025 & 2033

- Figure 41: Middle East & Africa Medical Cold Plasma Revenue Share (%), by Country 2025 & 2033

- Figure 42: Asia Pacific Medical Cold Plasma Revenue (billion), by Type 2025 & 2033

- Figure 43: Asia Pacific Medical Cold Plasma Revenue Share (%), by Type 2025 & 2033

- Figure 44: Asia Pacific Medical Cold Plasma Revenue (billion), by Product Type 2025 & 2033

- Figure 45: Asia Pacific Medical Cold Plasma Revenue Share (%), by Product Type 2025 & 2033

- Figure 46: Asia Pacific Medical Cold Plasma Revenue (billion), by End-user 2025 & 2033

- Figure 47: Asia Pacific Medical Cold Plasma Revenue Share (%), by End-user 2025 & 2033

- Figure 48: Asia Pacific Medical Cold Plasma Revenue (billion), by Application 2025 & 2033

- Figure 49: Asia Pacific Medical Cold Plasma Revenue Share (%), by Application 2025 & 2033

- Figure 50: Asia Pacific Medical Cold Plasma Revenue (billion), by Country 2025 & 2033

- Figure 51: Asia Pacific Medical Cold Plasma Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Medical Cold Plasma Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Global Medical Cold Plasma Revenue billion Forecast, by Product Type 2020 & 2033

- Table 3: Global Medical Cold Plasma Revenue billion Forecast, by End-user 2020 & 2033

- Table 4: Global Medical Cold Plasma Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Medical Cold Plasma Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Global Medical Cold Plasma Revenue billion Forecast, by Type 2020 & 2033

- Table 7: Global Medical Cold Plasma Revenue billion Forecast, by Product Type 2020 & 2033

- Table 8: Global Medical Cold Plasma Revenue billion Forecast, by End-user 2020 & 2033

- Table 9: Global Medical Cold Plasma Revenue billion Forecast, by Application 2020 & 2033

- Table 10: Global Medical Cold Plasma Revenue billion Forecast, by Country 2020 & 2033

- Table 11: United States Medical Cold Plasma Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Canada Medical Cold Plasma Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Mexico Medical Cold Plasma Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Global Medical Cold Plasma Revenue billion Forecast, by Type 2020 & 2033

- Table 15: Global Medical Cold Plasma Revenue billion Forecast, by Product Type 2020 & 2033

- Table 16: Global Medical Cold Plasma Revenue billion Forecast, by End-user 2020 & 2033

- Table 17: Global Medical Cold Plasma Revenue billion Forecast, by Application 2020 & 2033

- Table 18: Global Medical Cold Plasma Revenue billion Forecast, by Country 2020 & 2033

- Table 19: Brazil Medical Cold Plasma Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Argentina Medical Cold Plasma Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: Rest of South America Medical Cold Plasma Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Global Medical Cold Plasma Revenue billion Forecast, by Type 2020 & 2033

- Table 23: Global Medical Cold Plasma Revenue billion Forecast, by Product Type 2020 & 2033

- Table 24: Global Medical Cold Plasma Revenue billion Forecast, by End-user 2020 & 2033

- Table 25: Global Medical Cold Plasma Revenue billion Forecast, by Application 2020 & 2033

- Table 26: Global Medical Cold Plasma Revenue billion Forecast, by Country 2020 & 2033

- Table 27: United Kingdom Medical Cold Plasma Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Germany Medical Cold Plasma Revenue (billion) Forecast, by Application 2020 & 2033

- Table 29: France Medical Cold Plasma Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Italy Medical Cold Plasma Revenue (billion) Forecast, by Application 2020 & 2033

- Table 31: Spain Medical Cold Plasma Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Russia Medical Cold Plasma Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: Benelux Medical Cold Plasma Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: Nordics Medical Cold Plasma Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: Rest of Europe Medical Cold Plasma Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Global Medical Cold Plasma Revenue billion Forecast, by Type 2020 & 2033

- Table 37: Global Medical Cold Plasma Revenue billion Forecast, by Product Type 2020 & 2033

- Table 38: Global Medical Cold Plasma Revenue billion Forecast, by End-user 2020 & 2033

- Table 39: Global Medical Cold Plasma Revenue billion Forecast, by Application 2020 & 2033

- Table 40: Global Medical Cold Plasma Revenue billion Forecast, by Country 2020 & 2033

- Table 41: Turkey Medical Cold Plasma Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Israel Medical Cold Plasma Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: GCC Medical Cold Plasma Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: North Africa Medical Cold Plasma Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: South Africa Medical Cold Plasma Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Middle East & Africa Medical Cold Plasma Revenue (billion) Forecast, by Application 2020 & 2033

- Table 47: Global Medical Cold Plasma Revenue billion Forecast, by Type 2020 & 2033

- Table 48: Global Medical Cold Plasma Revenue billion Forecast, by Product Type 2020 & 2033

- Table 49: Global Medical Cold Plasma Revenue billion Forecast, by End-user 2020 & 2033

- Table 50: Global Medical Cold Plasma Revenue billion Forecast, by Application 2020 & 2033

- Table 51: Global Medical Cold Plasma Revenue billion Forecast, by Country 2020 & 2033

- Table 52: China Medical Cold Plasma Revenue (billion) Forecast, by Application 2020 & 2033

- Table 53: India Medical Cold Plasma Revenue (billion) Forecast, by Application 2020 & 2033

- Table 54: Japan Medical Cold Plasma Revenue (billion) Forecast, by Application 2020 & 2033

- Table 55: South Korea Medical Cold Plasma Revenue (billion) Forecast, by Application 2020 & 2033

- Table 56: ASEAN Medical Cold Plasma Revenue (billion) Forecast, by Application 2020 & 2033

- Table 57: Oceania Medical Cold Plasma Revenue (billion) Forecast, by Application 2020 & 2033

- Table 58: Rest of Asia Pacific Medical Cold Plasma Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Medical Cold Plasma?

The projected CAGR is approximately 14.35%.

2. Which companies are prominent players in the Medical Cold Plasma?

Key companies in the market include Apyx Medical Corporation, ADTEC Plasma Technology Co. Ltd., Neoplas med GmbH, Terraplasma Medical, GD Medical, Olympus, PlasmaDerm, Adtec Healthcare, Nova Plasma, Others.

3. What are the main segments of the Medical Cold Plasma?

The market segments include Type, Product Type , End-user, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 3.34 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 5900.00, USD 8850.00, and USD 11800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Medical Cold Plasma," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Medical Cold Plasma report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Medical Cold Plasma?

To stay informed about further developments, trends, and reports in the Medical Cold Plasma, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence