Key Insights

The global Medical Polymer Materials market is poised for significant expansion, projected to reach $25.43 billion by 2025, with a robust Compound Annual Growth Rate (CAGR) of 8%. This growth is propelled by escalating demand for sophisticated medical devices and implantable materials, driven by an aging demographic and the rising incidence of chronic diseases. Innovations in polymer science, yielding enhanced biocompatible, bioabsorbable, and high-performance materials, are also key contributors. Applications in healthcare settings, particularly for bioabsorbable polymers in sutures, scaffolds, and drug delivery systems, and biocompatible polymers for prosthetics, catheters, and surgical instruments, are leading market expansion. The "Others" segment, encompassing specialized medical components, also presents substantial growth prospects.

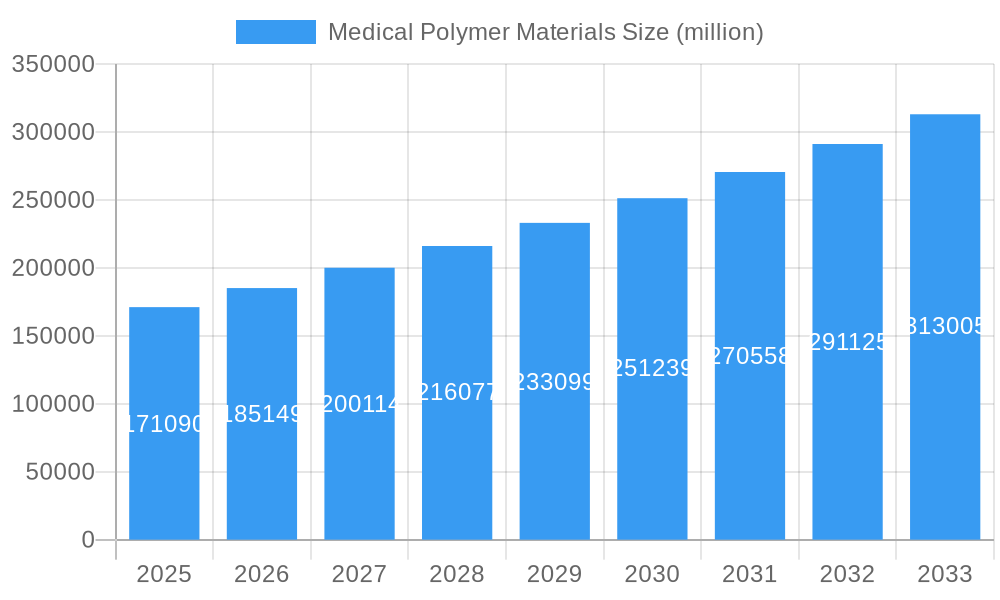

Medical Polymer Materials Market Size (In Billion)

Key market drivers include the advancement of personalized medicine, requiring bespoke medical devices and biomaterials, and the increasing preference for minimally invasive surgeries, which demands advanced polymer components offering superior flexibility, strength, and biocompatibility. While regulatory hurdles and high R&D costs present challenges, strategic initiatives from leading companies, focusing on material innovation, partnerships, and capacity expansion, are expected to mitigate these restraints. Geographically, North America and Europe represent established markets, while the Asia Pacific region is emerging as a critical growth hub, fueled by rising healthcare investments and a rapidly developing medical device industry.

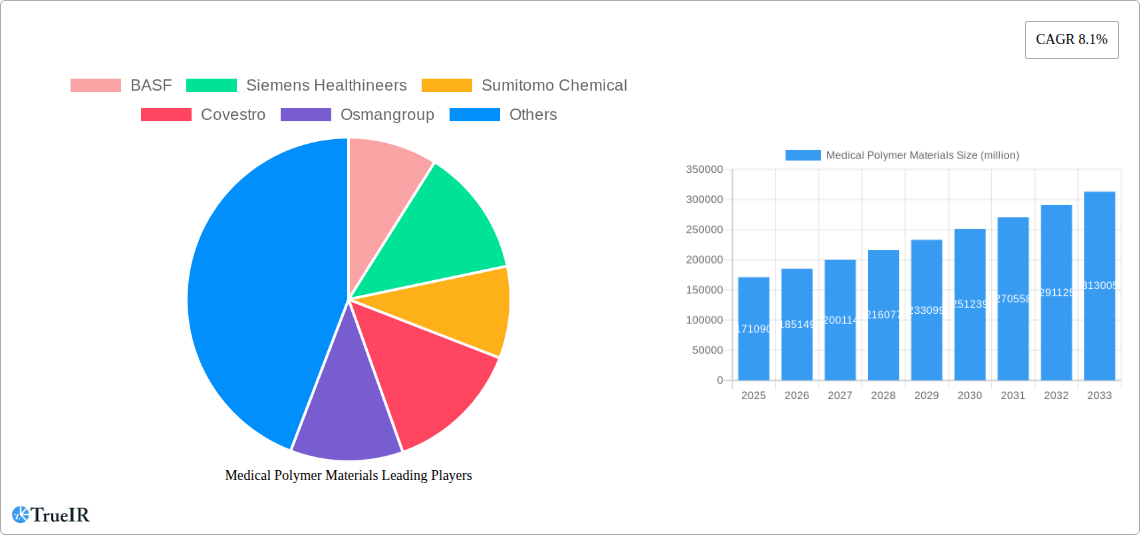

Medical Polymer Materials Company Market Share

Medical Polymer Materials Market Report: Comprehensive Analysis & Future Projections (2019-2033)

This in-depth report delivers a dynamic, SEO-optimized analysis of the global Medical Polymer Materials market, essential for stakeholders seeking to understand market dynamics, identify growth avenues, and navigate competitive landscapes. Leveraging high-volume keywords such as "medical polymers," "biocompatible materials," "bioabsorbable polymers," and "medical device materials," this report is meticulously crafted to enhance search rankings and engage a broad spectrum of industry professionals. The study encompasses a comprehensive historical period (2019–2024), a base year of 2025, and an extensive forecast period extending to 2033, providing actionable insights for strategic decision-making.

Medical Polymer Materials Market Structure & Competitive Landscape

The medical polymer materials market is characterized by a moderate to high concentration, driven by significant R&D investments and stringent regulatory approvals. Key players like BASF, Siemens Healthineers, Sumitomo Chemical, Covestro, and Evonik Industries dominate a substantial portion of the market share, estimated at over 60% of the total market value in the base year 2025. Innovation drivers are primarily centered on the development of advanced biocompatible and bioabsorbable polymers with enhanced mechanical properties, biodegradability profiles, and tailored drug-eluting capabilities. Regulatory impacts, particularly those from the FDA and EMA, play a crucial role in shaping market entry and product development, often requiring extensive testing and validation, which can add millions in development costs but also create barriers to entry for new competitors. Product substitutes, while present in some lower-end applications, are increasingly being displaced by high-performance medical polymers offering superior safety and efficacy. The end-user segmentation points to a strong reliance on the hospital and clinic sectors, which together accounted for approximately 95% of the market demand in the historical period. Mergers and acquisitions (M&A) remain a significant trend, with an estimated volume of over $500 million in M&A deals recorded between 2020 and 2024, aimed at expanding product portfolios and consolidating market presence.

Medical Polymer Materials Market Trends & Opportunities

The global medical polymer materials market is poised for robust growth, projected to expand at a Compound Annual Growth Rate (CAGR) of over 7.5% from 2025 to 2033. This expansion is fueled by a confluence of factors, including an aging global population, a rising prevalence of chronic diseases, and increasing healthcare expenditure worldwide. The market size is estimated to reach over $30 billion by 2025 and is projected to surpass $50 billion by the end of the forecast period. Technological shifts are at the forefront of this growth, with significant advancements in material science leading to the development of novel polymers with superior biocompatibility, biodegradability, and mechanical strength. These advancements are enabling the creation of more sophisticated medical devices, including advanced prosthetics, intricate surgical implants, and minimally invasive surgical tools. Consumer preferences are increasingly shifting towards minimally invasive procedures and personalized medicine, creating a strong demand for specialized medical polymers that can support these trends. For instance, the demand for bioabsorbable polymers for sutures, tissue engineering scaffolds, and drug delivery systems is surging due to their ability to degrade safely within the body, eliminating the need for secondary removal procedures and reducing patient discomfort. The competitive dynamics are intensifying, with established players focusing on R&D and strategic partnerships to maintain their market leadership, while emerging companies are carving out niches by offering innovative solutions for specific medical applications. Market penetration rates for advanced medical polymers in developing economies are expected to rise significantly as healthcare infrastructure improves and access to advanced medical treatments expands. The increasing adoption of 3D printing in the medical industry is also a major opportunity, driving the development of specialized medical-grade filaments and resins for custom implants and prosthetics. Furthermore, the growing emphasis on sustainable and environmentally friendly materials within the healthcare sector presents an opportunity for the development of biodegradable and recyclable medical polymers.

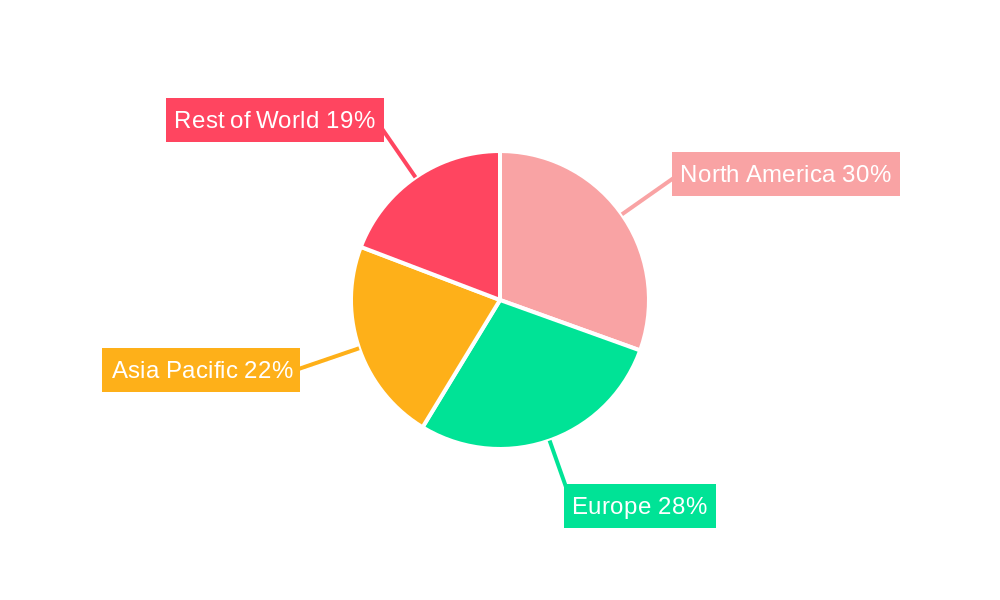

Dominant Markets & Segments in Medical Polymer Materials

The North America region stands as the dominant market for medical polymer materials, driven by its advanced healthcare infrastructure, high per capita healthcare spending, and a strong focus on technological innovation. The United States, in particular, accounts for an estimated 40% of the global market share within this region. Key growth drivers in this market include robust government funding for medical research and development, favorable regulatory policies that support the adoption of new medical technologies, and a high prevalence of age-related diseases and chronic conditions necessitating advanced medical interventions. The Hospital application segment is the largest, representing over 70% of the market demand, attributed to the extensive use of medical polymers in surgical implants, diagnostic equipment, drug delivery systems, and various disposable medical supplies.

Within the Type segmentation, Biocompatible Polymers hold the largest market share, estimated at approximately 65% in 2025. This dominance is due to their critical role in a vast array of medical devices where direct contact with bodily tissues and fluids is required, ensuring minimal adverse reactions. These polymers are indispensable for applications such as catheters, pacemakers, artificial joints, and blood bags.

The Bioabsorbable Polymer segment is experiencing the fastest growth, with a projected CAGR of over 8.5% during the forecast period. This surge is fueled by advancements in tissue engineering, regenerative medicine, and the increasing preference for biodegradable medical implants and sutures. These materials, including polylactic acid (PLA), polyglycolic acid (PGA), and their copolymers, are vital for applications like dissolvable stitches, bone fixation devices, and scaffolds for tissue regeneration, as they naturally break down over time, eliminating the need for removal surgeries. The Clinic segment, while smaller than the hospital segment, is also a significant contributor to market growth, particularly in the areas of outpatient surgical procedures and specialized medical treatments.

Medical Polymer Materials Product Analysis

Product innovation in medical polymer materials is primarily focused on enhancing biocompatibility, biodegradability, and mechanical performance to meet the evolving demands of advanced medical devices. Key advancements include the development of novel polymer composites with improved strength-to-weight ratios for orthopedic implants, and drug-eluting polymers that offer controlled release of therapeutic agents to enhance treatment efficacy and patient outcomes. The competitive advantage for leading manufacturers lies in their ability to develop proprietary formulations and advanced processing techniques that ensure consistent quality, sterilizability, and compliance with stringent regulatory standards. Applications span a wide spectrum, from biodegradable sutures and tissue engineering scaffolds to long-term implantable devices and advanced diagnostic equipment, demonstrating the versatility and critical importance of these materials in modern healthcare.

Key Drivers, Barriers & Challenges in Medical Polymer Materials

Key Drivers: The medical polymer materials market is primarily propelled by the ever-increasing global demand for advanced healthcare solutions, driven by an aging population and a growing prevalence of chronic diseases. Technological advancements in material science are leading to the development of novel polymers with enhanced biocompatibility, biodegradability, and improved mechanical properties, enabling the creation of more sophisticated and safer medical devices. Favorable government initiatives and increasing healthcare expenditure worldwide also play a crucial role in fostering market growth, particularly in emerging economies.

Key Barriers & Challenges: Despite robust growth prospects, the market faces significant challenges. Stringent regulatory frameworks imposed by bodies like the FDA and EMA necessitate extensive and costly validation processes for new materials and medical devices, creating considerable barriers to entry. Supply chain disruptions, geopolitical instabilities, and fluctuations in raw material prices can impact production costs and availability, affecting profit margins. Intense competition among established players and the emergence of new entrants also put pressure on pricing and innovation cycles. The need for continuous R&D investment to keep pace with technological advancements and evolving medical needs represents another substantial challenge, requiring millions in ongoing expenditure.

Growth Drivers in the Medical Polymer Materials Market

The medical polymer materials market's growth is intrinsically linked to the expanding global healthcare sector. Key drivers include the escalating demand for advanced medical devices, fueled by an aging demographic and the rising incidence of chronic diseases such as cardiovascular disorders, diabetes, and orthopedic conditions. Significant investments in research and development by leading companies are continuously yielding novel polymer formulations with superior biocompatibility, biodegradability, and mechanical properties, paving the way for next-generation medical implants, surgical tools, and drug delivery systems. Furthermore, favorable government policies, increasing healthcare expenditure in both developed and developing nations, and the growing adoption of minimally invasive surgical techniques are collectively accelerating market expansion. The rise of personalized medicine and regenerative therapies also presents substantial growth opportunities for specialized medical polymers.

Challenges Impacting Medical Polymer Materials Growth

The medical polymer materials market is not without its hurdles. Foremost among these are the stringent and evolving regulatory landscapes governed by agencies like the FDA and EMA. Obtaining approvals for new materials and their applications is a protracted and expensive process, often requiring millions in testing and documentation. Supply chain vulnerabilities, exacerbated by global events, can lead to material shortages and price volatility, impacting manufacturing timelines and costs. Intense competitive pressures necessitate continuous innovation and cost optimization, while the high cost of raw materials and specialized manufacturing processes can strain profit margins. Furthermore, the need for extensive clinical trials and the development of sustainable material alternatives present ongoing challenges for market participants.

Key Players Shaping the Medical Polymer Materials Market

- BASF

- Siemens Healthineers

- Sumitomo Chemical

- Covestro

- Osmangroup

- Invibio

- PolyOne

- Evonik Industries

- DSM Biomedical

- Raumedic

- Secant Group

- Teleflex Medical

Significant Medical Polymer Materials Industry Milestones

- 2019: Introduction of advanced bioresorbable polymers for enhanced orthopedic fixation devices.

- 2020: Significant increase in demand for biocompatible polymers for use in ventilators and personal protective equipment amidst global health crisis.

- 2021: Launch of novel drug-eluting polymer coatings for cardiovascular stents, improving patient outcomes.

- 2022: Advancements in 3D-printable medical-grade polymers enabling custom implant fabrication.

- 2023: Increased focus on developing sustainable and recyclable medical polymer materials.

- Q1 2024: Strategic acquisition of a specialized bioabsorbable polymer manufacturer by a major chemical company to expand its medical portfolio.

- Q2 2024: Regulatory approval for a new generation of biocompatible polymers designed for long-term implantable electronics.

Future Outlook for Medical Polymer Materials Market

The future outlook for the medical polymer materials market is exceptionally promising, driven by continuous innovation and the expanding needs of the global healthcare industry. Strategic opportunities lie in the burgeoning fields of regenerative medicine, personalized implants, and advanced drug delivery systems, where novel biocompatible and bioabsorbable polymers will play a pivotal role. The increasing adoption of 3D printing in healthcare will further stimulate demand for specialized medical-grade polymers. As regulatory pathways become more streamlined for innovative materials and the focus on sustainable healthcare solutions intensifies, the market is poised for sustained, high-value growth. The forecast period (2025–2033) is expected to witness substantial market expansion, driven by an unwavering commitment to improving patient care through advanced material science.

Medical Polymer Materials Segmentation

-

1. Application

- 1.1. Hospital

- 1.2. Clinic

-

2. Type

- 2.1. Bioabsorbable Polymer

- 2.2. Biocompatible Polymer

- 2.3. Others

Medical Polymer Materials Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Medical Polymer Materials Regional Market Share

Geographic Coverage of Medical Polymer Materials

Medical Polymer Materials REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Hospital

- 5.1.2. Clinic

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Bioabsorbable Polymer

- 5.2.2. Biocompatible Polymer

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Medical Polymer Materials Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Hospital

- 6.1.2. Clinic

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Bioabsorbable Polymer

- 6.2.2. Biocompatible Polymer

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Medical Polymer Materials Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Hospital

- 7.1.2. Clinic

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Bioabsorbable Polymer

- 7.2.2. Biocompatible Polymer

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Medical Polymer Materials Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Hospital

- 8.1.2. Clinic

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Bioabsorbable Polymer

- 8.2.2. Biocompatible Polymer

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Medical Polymer Materials Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Hospital

- 9.1.2. Clinic

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Bioabsorbable Polymer

- 9.2.2. Biocompatible Polymer

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Medical Polymer Materials Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Hospital

- 10.1.2. Clinic

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Bioabsorbable Polymer

- 10.2.2. Biocompatible Polymer

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Medical Polymer Materials Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Hospital

- 11.1.2. Clinic

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Bioabsorbable Polymer

- 11.2.2. Biocompatible Polymer

- 11.2.3. Others

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 BASF

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Siemens Healthineers

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Sumitomo Chemical

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Covestro

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Osmangroup

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Invibio

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 PolyOne

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Evonik Industries

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 DSM Biomedical

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Raumedic

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Secant Group

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Teleflex Medical

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.1 BASF

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Medical Polymer Materials Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Medical Polymer Materials Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Medical Polymer Materials Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Medical Polymer Materials Revenue (billion), by Type 2025 & 2033

- Figure 5: North America Medical Polymer Materials Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Medical Polymer Materials Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Medical Polymer Materials Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Medical Polymer Materials Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Medical Polymer Materials Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Medical Polymer Materials Revenue (billion), by Type 2025 & 2033

- Figure 11: South America Medical Polymer Materials Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Medical Polymer Materials Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Medical Polymer Materials Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Medical Polymer Materials Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Medical Polymer Materials Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Medical Polymer Materials Revenue (billion), by Type 2025 & 2033

- Figure 17: Europe Medical Polymer Materials Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Medical Polymer Materials Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Medical Polymer Materials Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Medical Polymer Materials Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Medical Polymer Materials Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Medical Polymer Materials Revenue (billion), by Type 2025 & 2033

- Figure 23: Middle East & Africa Medical Polymer Materials Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Medical Polymer Materials Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Medical Polymer Materials Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Medical Polymer Materials Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Medical Polymer Materials Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Medical Polymer Materials Revenue (billion), by Type 2025 & 2033

- Figure 29: Asia Pacific Medical Polymer Materials Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Medical Polymer Materials Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Medical Polymer Materials Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Medical Polymer Materials Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Medical Polymer Materials Revenue billion Forecast, by Type 2020 & 2033

- Table 3: Global Medical Polymer Materials Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Medical Polymer Materials Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Medical Polymer Materials Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Global Medical Polymer Materials Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Medical Polymer Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Medical Polymer Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Medical Polymer Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Medical Polymer Materials Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Medical Polymer Materials Revenue billion Forecast, by Type 2020 & 2033

- Table 12: Global Medical Polymer Materials Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Medical Polymer Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Medical Polymer Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Medical Polymer Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Medical Polymer Materials Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Medical Polymer Materials Revenue billion Forecast, by Type 2020 & 2033

- Table 18: Global Medical Polymer Materials Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Medical Polymer Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Medical Polymer Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Medical Polymer Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Medical Polymer Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Medical Polymer Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Medical Polymer Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Medical Polymer Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Medical Polymer Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Medical Polymer Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Medical Polymer Materials Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Medical Polymer Materials Revenue billion Forecast, by Type 2020 & 2033

- Table 30: Global Medical Polymer Materials Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Medical Polymer Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Medical Polymer Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Medical Polymer Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Medical Polymer Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Medical Polymer Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Medical Polymer Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Medical Polymer Materials Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Medical Polymer Materials Revenue billion Forecast, by Type 2020 & 2033

- Table 39: Global Medical Polymer Materials Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Medical Polymer Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Medical Polymer Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Medical Polymer Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Medical Polymer Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Medical Polymer Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Medical Polymer Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Medical Polymer Materials Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Medical Polymer Materials?

The projected CAGR is approximately 8%.

2. Which companies are prominent players in the Medical Polymer Materials?

Key companies in the market include BASF, Siemens Healthineers, Sumitomo Chemical, Covestro, Osmangroup, Invibio, PolyOne, Evonik Industries, DSM Biomedical, Raumedic, Secant Group, Teleflex Medical.

3. What are the main segments of the Medical Polymer Materials?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 25.43 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4250.00, USD 6375.00, and USD 8500.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Medical Polymer Materials," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Medical Polymer Materials report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Medical Polymer Materials?

To stay informed about further developments, trends, and reports in the Medical Polymer Materials, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence