Key Insights

The global Thalassemia Treatment market is projected for robust expansion, exhibiting a Compound Annual Growth Rate (CAGR) of 7.60% and reaching a substantial market size. This growth is primarily fueled by increasing awareness of thalassemia, advancements in treatment modalities like gene therapy and improved supportive care, and a rising prevalence of the genetic blood disorder, particularly in regions with a high carrier rate. Key drivers include the development of novel and less invasive treatment options, government initiatives aimed at early diagnosis and screening programs, and increased healthcare expenditure in emerging economies. The market is segmenting into various treatment types, with blood transfusions and iron chelation therapy remaining cornerstones of management, while folic acid supplements offer supplementary support. Emerging treatments like gene therapy hold significant promise for a curative approach, attracting considerable investment and research. The disease type segmentation is dominated by Beta Thalassemia, which generally presents with more severe symptoms and requires more frequent interventions, followed by Alpha Thalassemia.

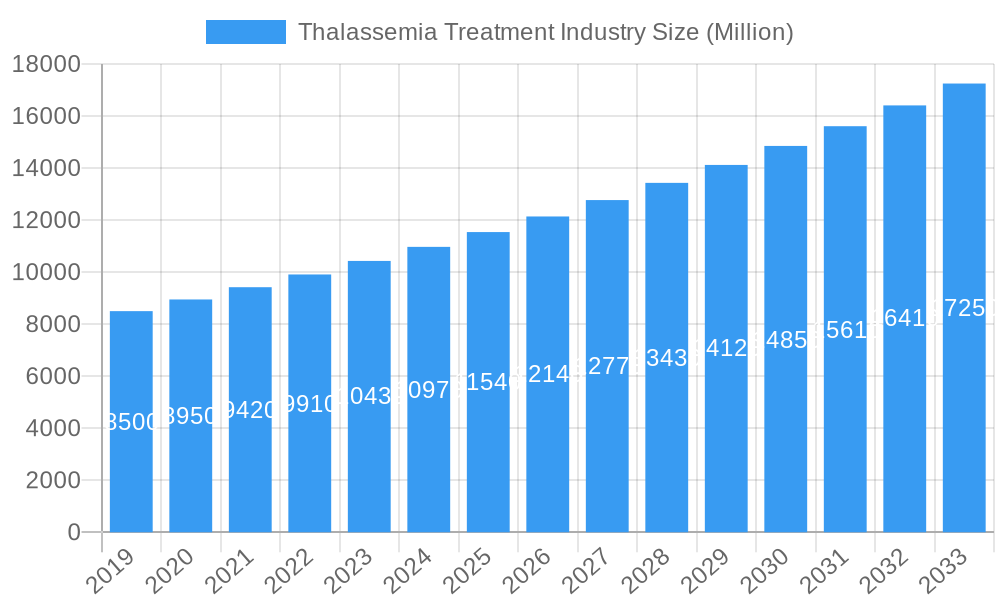

Thalassemia Treatment Industry Market Size (In Billion)

The market's trajectory is further shaped by evolving trends, including a shift towards personalized medicine, focusing on patient-specific genetic profiles to optimize treatment strategies. The integration of digital health solutions for remote patient monitoring and management is also gaining traction. However, restraints such as the high cost of advanced treatments, limited access to specialized care in underdeveloped regions, and the lifelong nature of some therapies pose challenges. The competitive landscape features a mix of established pharmaceutical giants and innovative biopharmaceutical companies, actively engaged in research and development to bring breakthrough therapies to market. Geographical expansion, particularly in the Asia Pacific region, is expected to contribute significantly to market growth due to its large population base and increasing healthcare infrastructure. Hospitals are the primary end-users, owing to the complex and continuous nature of thalassemia management, followed by research institutes focused on developing next-generation treatments.

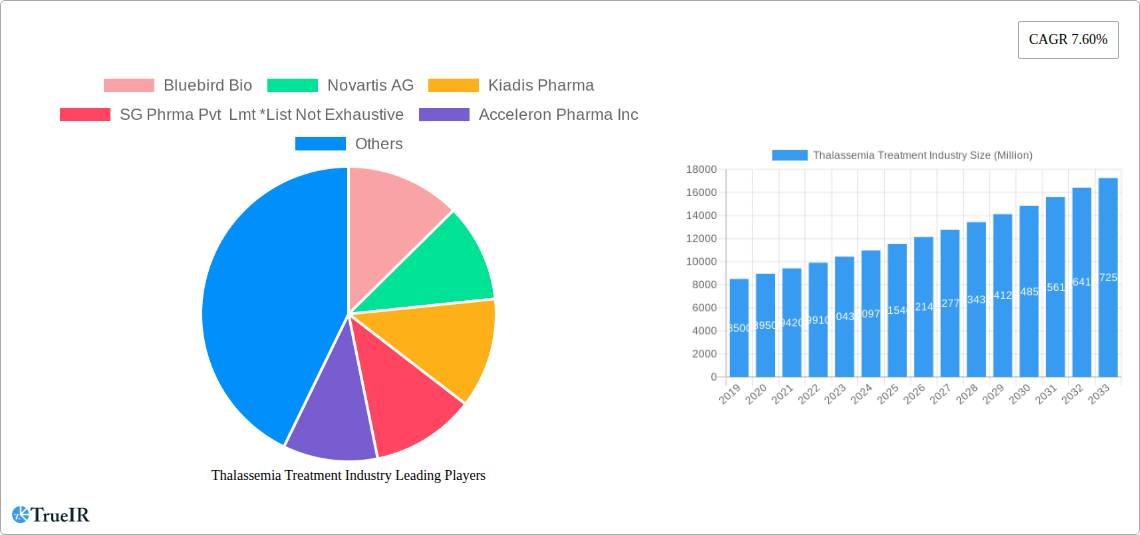

Thalassemia Treatment Industry Company Market Share

This comprehensive Thalassemia Treatment Industry market research report provides in-depth analysis and forecasts for the period of 2019–2033, with a base year of 2025. Leveraging high-volume keywords such as "thalassemia treatment market," "blood disorder therapies," "genetic disorder management," and "hemoglobinopathy solutions," this report is meticulously crafted for optimal SEO performance and to engage a global audience of industry professionals, investors, and healthcare stakeholders.

Thalassemia Treatment Industry Market Structure & Competitive Landscape

The global Thalassemia Treatment Industry is characterized by a moderately concentrated market structure, driven by significant innovation in gene therapy and novel drug development. Key innovation drivers include advanced genetic sequencing technologies, CRISPR-Cas9 advancements, and improved drug delivery mechanisms, leading to more targeted and effective treatments. Regulatory impacts are substantial, with stringent approval processes for novel therapies, particularly impacting market entry for new gene-editing solutions. Product substitutes, while currently limited for severe thalassemia, are emerging with advancements in supportive care and potential curative approaches.

End-user segmentation is dominated by hospitals, accounting for an estimated 70% of market share, followed by research institutes at approximately 25% and others at 5%. Mergers and acquisitions (M&A) activity, while not rampant, is strategic, with larger pharmaceutical companies acquiring promising biotech firms to bolster their gene therapy pipelines. The estimated volume of M&A transactions in the historical period (2019-2024) is approximately 15, with an average deal value in the hundreds of millions of dollars. Concentration ratios are currently estimated around CR4 of 45%, indicating a competitive yet consolidated landscape.

Thalassemia Treatment Industry Market Trends & Opportunities

The Thalassemia Treatment Industry is poised for substantial growth, with an estimated market size projected to reach $15,000 Million by 2033. This robust expansion is fueled by increasing global awareness of thalassemia, advancements in diagnostic tools, and the growing demand for more effective and potentially curative treatment options. The forecast period (2025–2033) anticipates a Compound Annual Growth Rate (CAGR) of approximately 12%. Technological shifts are at the forefront, with a significant move towards gene therapy and gene editing as curative strategies, offering a paradigm shift from traditional symptomatic management. For instance, the development of ex-vivo gene therapy for beta-thalassemia has opened new avenues for patients with severe forms of the disease who are transfusion-dependent.

Consumer preferences are increasingly leaning towards treatments that offer long-term relief or a permanent cure, reducing the lifelong burden of blood transfusions and iron chelation. This evolving preference directly impacts the market penetration rates of innovative therapies. The competitive dynamics are intensifying, with both established pharmaceutical giants and agile biotech startups vying for market share. The market penetration rate for gene therapies, while still nascent, is expected to grow exponentially as regulatory hurdles are overcome and manufacturing scales up. The prevalence of both alpha and beta thalassemia necessitates a broad range of treatment approaches, creating opportunities for diversified product portfolios.

Furthermore, a growing number of clinical trials focused on novel drug targets and therapeutic modalities are promising to unlock new treatment paradigms. The rising incidence of thalassemia in specific geographical regions, coupled with improved healthcare infrastructure, is also a significant growth catalyst. The shift from managing symptoms to addressing the root genetic cause of thalassemia presents a lucrative opportunity for companies investing in research and development of gene-based therapies. The integration of artificial intelligence (AI) in drug discovery and patient stratification is another emerging trend that will optimize treatment outcomes and accelerate market growth. The base year, 2025, represents a pivotal point where emerging therapies are gaining traction, paving the way for accelerated growth in the coming years.

Dominant Markets & Segments in Thalassemia Treatment Industry

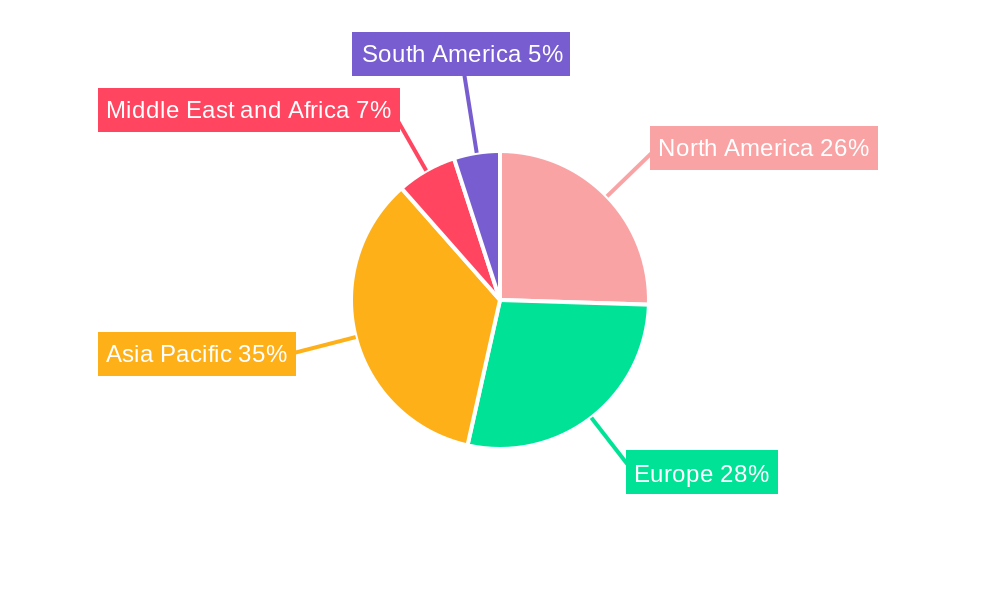

The Thalassemia Treatment Industry exhibits distinct regional dominance, with Asia-Pacific projected to be the leading market due to the high prevalence of thalassemia in countries like India, Pakistan, and Bangladesh. This dominance is further supported by increasing government initiatives and investments in healthcare infrastructure for managing genetic blood disorders.

Dominant Region: Asia-Pacific

- Key Growth Drivers:

- High incidence rates of Beta Thalassemia.

- Increasing government focus on genetic disease management and public health programs.

- Growing disposable income and improved access to advanced healthcare facilities.

- Expansion of diagnostic capabilities and awareness campaigns.

- Detailed Analysis: Countries in South Asia, particularly India, are grappling with a significant burden of thalassemia, driving the demand for both conventional and novel treatments. While healthcare infrastructure is still developing in many parts of the region, there is a clear upward trend in investment and focus on specialized treatment centers. The affordability of treatments remains a critical factor, but the long-term benefits of advanced therapies are gradually being recognized.

Dominant Segment: Beta Thalassemia

- Key Growth Drivers:

- Higher prevalence and severity of Beta Thalassemia compared to Alpha Thalassemia.

- Significant unmet medical needs for effective and curative treatments for transfusion-dependent patients.

- Targeted research and development efforts for Beta Thalassemia gene therapies.

- Detailed Analysis: Beta Thalassemia is the more severe and prevalent form of the disease, particularly in Mediterranean, Middle Eastern, and Asian populations. This has led to concentrated research and development efforts towards gene therapy and bone marrow transplantation, driving innovation and market demand for these advanced interventions.

Dominant Treatment Type: Blood Transfusions & Iron Chelation Therapy

- Key Growth Drivers:

- Established and widely available standard of care for managing symptoms.

- Necessity for lifelong management in severe cases.

- Continued reliance on these therapies while curative options are being developed and adopted.

- Detailed Analysis: Despite the emergence of gene therapies, blood transfusions remain a cornerstone of thalassemia management for millions of patients worldwide, particularly for moderate to severe cases. Iron chelation therapy is crucial to manage iron overload resulting from frequent transfusions. The demand for these supportive treatments remains robust, ensuring their continued market significance in the near to medium term.

Dominant End-User: Hospitals

- Key Growth Drivers:

- Centralized facilities for complex treatments like gene therapy and bone marrow transplants.

- Access to specialized medical professionals and advanced equipment.

- Reimbursement policies and healthcare system integration.

- Detailed Analysis: Hospitals are the primary care providers for thalassemia patients, offering a comprehensive range of services from diagnosis and routine transfusions to complex gene therapies and post-treatment care. Their infrastructure and expertise make them the central hub for all thalassemia treatment modalities.

Thalassemia Treatment Industry Product Analysis

Product innovation in the thalassemia treatment industry is primarily focused on developing curative gene therapies and novel, more targeted iron chelation agents. Gene therapy approaches, such as ex-vivo gene editing and lentiviral vector delivery, aim to correct the genetic defect responsible for the disease, offering a potential one-time cure. Advancements in drug delivery systems for iron chelation are improving patient compliance and reducing side effects. Competitive advantages are being gained by companies demonstrating strong clinical trial data, favorable safety profiles, and scalable manufacturing capabilities for these complex therapies.

Key Drivers, Barriers & Challenges in Thalassemia Treatment Industry

Key Drivers:

- Technological Advancements: Breakthroughs in gene therapy, gene editing (e.g., CRISPR-Cas9), and stem cell transplantation are creating opportunities for curative treatments.

- Increased Global Prevalence: Rising awareness and improved diagnostics are leading to earlier detection and a growing patient pool requiring treatment.

- Government Initiatives & Funding: Growing recognition of thalassemia as a public health concern is leading to increased government support and funding for research and treatment programs.

- Demand for Curative Options: Patients and healthcare providers are actively seeking long-term solutions beyond lifelong management.

Barriers & Challenges:

- High Cost of Novel Therapies: Gene therapies and advanced treatments are extremely expensive, posing significant accessibility and affordability challenges for many patients and healthcare systems.

- Regulatory Hurdles: Stringent approval processes for gene therapies can be time-consuming and complex, delaying market entry.

- Supply Chain Complexities: Manufacturing and distribution of complex biological therapies require specialized infrastructure and stringent quality control.

- Limited Awareness and Infrastructure in Developing Regions: Uneven access to diagnostics and advanced treatment facilities in lower-income countries hinders widespread adoption.

- Potential Long-Term Side Effects: While promising, the long-term safety and efficacy of novel therapies are still being evaluated.

Growth Drivers in the Thalassemia Treatment Industry Market

The Thalassemia Treatment Industry market is experiencing robust growth driven by several key factors. Foremost among these are rapid advancements in gene therapy and gene editing technologies, which offer the potential for definitive cures rather than lifelong management. The increasing global prevalence of thalassemia, coupled with enhanced diagnostic capabilities, leads to earlier detection and a larger patient population seeking effective interventions. Furthermore, growing government initiatives and funding in affected regions are bolstering healthcare infrastructure and research, creating a more conducive environment for market expansion. The persistent unmet need for effective treatments for severe thalassemia cases is a significant demand driver, pushing innovation and investment.

Challenges Impacting Thalassemia Treatment Industry Growth

Despite promising growth prospects, the Thalassemia Treatment Industry faces significant challenges that can impede its expansion. The extremely high cost of emerging gene therapies is a major barrier, limiting accessibility for a large segment of the global patient population and placing immense pressure on healthcare reimbursement systems. Regulatory complexities surrounding novel gene-based treatments can lead to prolonged approval timelines, delaying market entry. Supply chain intricacies for manufacturing and distributing advanced biological therapies require specialized expertise and infrastructure, presenting logistical hurdles. Moreover, disparities in healthcare infrastructure and awareness across different geographical regions contribute to uneven market penetration and treatment accessibility.

Key Players Shaping the Thalassemia Treatment Industry Market

- Bluebird Bio

- Novartis AG

- Kiadis Pharma

- SG Phrma Pvt Lmt

- Acceleron Pharma Inc

- Bellicum Pharmaceuticals

- ApoPharma Inc

- IONIS Pharmaceuticals

- Pfizer Inc

Significant Thalassemia Treatment Industry Industry Milestones

- 2019: Approval of Zynteglo (betibeglogene autotemcel) by Bluebird Bio for transfusion-dependent beta-thalassemia, marking a significant milestone in gene therapy.

- 2020: Novartis AG announces positive interim data from a Phase III clinical trial for a novel gene therapy.

- 2021: Kiadis Pharma is acquired by Sanofi, bolstering its gene therapy pipeline for rare diseases.

- 2022: Regulatory filings submitted for several new iron chelation agents with improved efficacy and safety profiles.

- 2023: Acceleron Pharma Inc. is acquired by Merck & Co., Inc., aiming to integrate its rare disease portfolio, including potential thalassemia treatments.

- 2024: SG Phrma Pvt Lmt expands its manufacturing capabilities for thalassemia treatment generics in emerging markets.

- 2025: Anticipated regulatory review and potential approval of new gene editing therapies showing high efficacy in clinical trials.

- 2026: Expected advancements in personalized medicine approaches for thalassemia treatment, including improved genetic screening and targeted therapies.

Future Outlook for Thalassemia Treatment Industry Market

The future outlook for the Thalassemia Treatment Industry is exceptionally promising, driven by the transformative potential of gene therapy and gene editing. Strategic opportunities lie in developing cost-effective gene therapy solutions, expanding access to advanced treatments in underserved regions, and fostering collaborations between research institutions and pharmaceutical companies. The market is poised for continued innovation in both curative and symptomatic treatments, with a growing emphasis on improving patient quality of life and reducing the lifelong burden of the disease. The increasing prevalence of thalassemia, coupled with advancements in medical technology and a more proactive approach to genetic disorder management, will fuel sustained market growth and define the therapeutic landscape for years to come.

Thalassemia Treatment Industry Segmentation

-

1. Treatment Type

- 1.1. Blood Transfusions

- 1.2. Iron Chelation Therapy

- 1.3. Folic Acid Supplements

- 1.4. Others

-

2. Disease Type

- 2.1. Alpha Thalassemia

- 2.2. Beta Thalassemia

-

3. End-User

- 3.1. Hospitals

- 3.2. Research Institutes

- 3.3. Others

Thalassemia Treatment Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. Europe

- 2.1. Germany

- 2.2. United Kingdom

- 2.3. France

- 2.4. Italy

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Australia

- 3.5. South Korea

- 3.6. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. GCC

- 4.2. South Africa

- 4.3. Rest of Middle East and Africa

-

5. South America

- 5.1. Brazil

- 5.2. Argentina

- 5.3. Rest of South America

Thalassemia Treatment Industry Regional Market Share

Geographic Coverage of Thalassemia Treatment Industry

Thalassemia Treatment Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.60% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Treatment Type

- 5.1.1. Blood Transfusions

- 5.1.2. Iron Chelation Therapy

- 5.1.3. Folic Acid Supplements

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Disease Type

- 5.2.1. Alpha Thalassemia

- 5.2.2. Beta Thalassemia

- 5.3. Market Analysis, Insights and Forecast - by End-User

- 5.3.1. Hospitals

- 5.3.2. Research Institutes

- 5.3.3. Others

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Middle East and Africa

- 5.4.5. South America

- 5.1. Market Analysis, Insights and Forecast - by Treatment Type

- 6. Global Thalassemia Treatment Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Treatment Type

- 6.1.1. Blood Transfusions

- 6.1.2. Iron Chelation Therapy

- 6.1.3. Folic Acid Supplements

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Disease Type

- 6.2.1. Alpha Thalassemia

- 6.2.2. Beta Thalassemia

- 6.3. Market Analysis, Insights and Forecast - by End-User

- 6.3.1. Hospitals

- 6.3.2. Research Institutes

- 6.3.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Treatment Type

- 7. North America Thalassemia Treatment Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Treatment Type

- 7.1.1. Blood Transfusions

- 7.1.2. Iron Chelation Therapy

- 7.1.3. Folic Acid Supplements

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Disease Type

- 7.2.1. Alpha Thalassemia

- 7.2.2. Beta Thalassemia

- 7.3. Market Analysis, Insights and Forecast - by End-User

- 7.3.1. Hospitals

- 7.3.2. Research Institutes

- 7.3.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Treatment Type

- 8. Europe Thalassemia Treatment Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Treatment Type

- 8.1.1. Blood Transfusions

- 8.1.2. Iron Chelation Therapy

- 8.1.3. Folic Acid Supplements

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Disease Type

- 8.2.1. Alpha Thalassemia

- 8.2.2. Beta Thalassemia

- 8.3. Market Analysis, Insights and Forecast - by End-User

- 8.3.1. Hospitals

- 8.3.2. Research Institutes

- 8.3.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Treatment Type

- 9. Asia Pacific Thalassemia Treatment Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Treatment Type

- 9.1.1. Blood Transfusions

- 9.1.2. Iron Chelation Therapy

- 9.1.3. Folic Acid Supplements

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Disease Type

- 9.2.1. Alpha Thalassemia

- 9.2.2. Beta Thalassemia

- 9.3. Market Analysis, Insights and Forecast - by End-User

- 9.3.1. Hospitals

- 9.3.2. Research Institutes

- 9.3.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Treatment Type

- 10. Middle East and Africa Thalassemia Treatment Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Treatment Type

- 10.1.1. Blood Transfusions

- 10.1.2. Iron Chelation Therapy

- 10.1.3. Folic Acid Supplements

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Disease Type

- 10.2.1. Alpha Thalassemia

- 10.2.2. Beta Thalassemia

- 10.3. Market Analysis, Insights and Forecast - by End-User

- 10.3.1. Hospitals

- 10.3.2. Research Institutes

- 10.3.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Treatment Type

- 11. South America Thalassemia Treatment Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Treatment Type

- 11.1.1. Blood Transfusions

- 11.1.2. Iron Chelation Therapy

- 11.1.3. Folic Acid Supplements

- 11.1.4. Others

- 11.2. Market Analysis, Insights and Forecast - by Disease Type

- 11.2.1. Alpha Thalassemia

- 11.2.2. Beta Thalassemia

- 11.3. Market Analysis, Insights and Forecast - by End-User

- 11.3.1. Hospitals

- 11.3.2. Research Institutes

- 11.3.3. Others

- 11.1. Market Analysis, Insights and Forecast - by Treatment Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Bluebird Bio

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Novartis AG

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Kiadis Pharma

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 SG Phrma Pvt Lmt *List Not Exhaustive

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Acceleron Pharma Inc

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Bellicum Pharmaceuticals

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 ApoPharma Inc

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 IONIS Pharmaceuticals

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Pfizer Inc

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.1 Bluebird Bio

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Thalassemia Treatment Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Thalassemia Treatment Industry Revenue (Million), by Treatment Type 2025 & 2033

- Figure 3: North America Thalassemia Treatment Industry Revenue Share (%), by Treatment Type 2025 & 2033

- Figure 4: North America Thalassemia Treatment Industry Revenue (Million), by Disease Type 2025 & 2033

- Figure 5: North America Thalassemia Treatment Industry Revenue Share (%), by Disease Type 2025 & 2033

- Figure 6: North America Thalassemia Treatment Industry Revenue (Million), by End-User 2025 & 2033

- Figure 7: North America Thalassemia Treatment Industry Revenue Share (%), by End-User 2025 & 2033

- Figure 8: North America Thalassemia Treatment Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: North America Thalassemia Treatment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Thalassemia Treatment Industry Revenue (Million), by Treatment Type 2025 & 2033

- Figure 11: Europe Thalassemia Treatment Industry Revenue Share (%), by Treatment Type 2025 & 2033

- Figure 12: Europe Thalassemia Treatment Industry Revenue (Million), by Disease Type 2025 & 2033

- Figure 13: Europe Thalassemia Treatment Industry Revenue Share (%), by Disease Type 2025 & 2033

- Figure 14: Europe Thalassemia Treatment Industry Revenue (Million), by End-User 2025 & 2033

- Figure 15: Europe Thalassemia Treatment Industry Revenue Share (%), by End-User 2025 & 2033

- Figure 16: Europe Thalassemia Treatment Industry Revenue (Million), by Country 2025 & 2033

- Figure 17: Europe Thalassemia Treatment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific Thalassemia Treatment Industry Revenue (Million), by Treatment Type 2025 & 2033

- Figure 19: Asia Pacific Thalassemia Treatment Industry Revenue Share (%), by Treatment Type 2025 & 2033

- Figure 20: Asia Pacific Thalassemia Treatment Industry Revenue (Million), by Disease Type 2025 & 2033

- Figure 21: Asia Pacific Thalassemia Treatment Industry Revenue Share (%), by Disease Type 2025 & 2033

- Figure 22: Asia Pacific Thalassemia Treatment Industry Revenue (Million), by End-User 2025 & 2033

- Figure 23: Asia Pacific Thalassemia Treatment Industry Revenue Share (%), by End-User 2025 & 2033

- Figure 24: Asia Pacific Thalassemia Treatment Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Asia Pacific Thalassemia Treatment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Middle East and Africa Thalassemia Treatment Industry Revenue (Million), by Treatment Type 2025 & 2033

- Figure 27: Middle East and Africa Thalassemia Treatment Industry Revenue Share (%), by Treatment Type 2025 & 2033

- Figure 28: Middle East and Africa Thalassemia Treatment Industry Revenue (Million), by Disease Type 2025 & 2033

- Figure 29: Middle East and Africa Thalassemia Treatment Industry Revenue Share (%), by Disease Type 2025 & 2033

- Figure 30: Middle East and Africa Thalassemia Treatment Industry Revenue (Million), by End-User 2025 & 2033

- Figure 31: Middle East and Africa Thalassemia Treatment Industry Revenue Share (%), by End-User 2025 & 2033

- Figure 32: Middle East and Africa Thalassemia Treatment Industry Revenue (Million), by Country 2025 & 2033

- Figure 33: Middle East and Africa Thalassemia Treatment Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: South America Thalassemia Treatment Industry Revenue (Million), by Treatment Type 2025 & 2033

- Figure 35: South America Thalassemia Treatment Industry Revenue Share (%), by Treatment Type 2025 & 2033

- Figure 36: South America Thalassemia Treatment Industry Revenue (Million), by Disease Type 2025 & 2033

- Figure 37: South America Thalassemia Treatment Industry Revenue Share (%), by Disease Type 2025 & 2033

- Figure 38: South America Thalassemia Treatment Industry Revenue (Million), by End-User 2025 & 2033

- Figure 39: South America Thalassemia Treatment Industry Revenue Share (%), by End-User 2025 & 2033

- Figure 40: South America Thalassemia Treatment Industry Revenue (Million), by Country 2025 & 2033

- Figure 41: South America Thalassemia Treatment Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Thalassemia Treatment Industry Revenue Million Forecast, by Treatment Type 2020 & 2033

- Table 2: Global Thalassemia Treatment Industry Revenue Million Forecast, by Disease Type 2020 & 2033

- Table 3: Global Thalassemia Treatment Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 4: Global Thalassemia Treatment Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Global Thalassemia Treatment Industry Revenue Million Forecast, by Treatment Type 2020 & 2033

- Table 6: Global Thalassemia Treatment Industry Revenue Million Forecast, by Disease Type 2020 & 2033

- Table 7: Global Thalassemia Treatment Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 8: Global Thalassemia Treatment Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: United States Thalassemia Treatment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Canada Thalassemia Treatment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Mexico Thalassemia Treatment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Global Thalassemia Treatment Industry Revenue Million Forecast, by Treatment Type 2020 & 2033

- Table 13: Global Thalassemia Treatment Industry Revenue Million Forecast, by Disease Type 2020 & 2033

- Table 14: Global Thalassemia Treatment Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 15: Global Thalassemia Treatment Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 16: Germany Thalassemia Treatment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: United Kingdom Thalassemia Treatment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: France Thalassemia Treatment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: Italy Thalassemia Treatment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Spain Thalassemia Treatment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: Rest of Europe Thalassemia Treatment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Global Thalassemia Treatment Industry Revenue Million Forecast, by Treatment Type 2020 & 2033

- Table 23: Global Thalassemia Treatment Industry Revenue Million Forecast, by Disease Type 2020 & 2033

- Table 24: Global Thalassemia Treatment Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 25: Global Thalassemia Treatment Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 26: China Thalassemia Treatment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: Japan Thalassemia Treatment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: India Thalassemia Treatment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 29: Australia Thalassemia Treatment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: South Korea Thalassemia Treatment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 31: Rest of Asia Pacific Thalassemia Treatment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Global Thalassemia Treatment Industry Revenue Million Forecast, by Treatment Type 2020 & 2033

- Table 33: Global Thalassemia Treatment Industry Revenue Million Forecast, by Disease Type 2020 & 2033

- Table 34: Global Thalassemia Treatment Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 35: Global Thalassemia Treatment Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 36: GCC Thalassemia Treatment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 37: South Africa Thalassemia Treatment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 38: Rest of Middle East and Africa Thalassemia Treatment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 39: Global Thalassemia Treatment Industry Revenue Million Forecast, by Treatment Type 2020 & 2033

- Table 40: Global Thalassemia Treatment Industry Revenue Million Forecast, by Disease Type 2020 & 2033

- Table 41: Global Thalassemia Treatment Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 42: Global Thalassemia Treatment Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 43: Brazil Thalassemia Treatment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 44: Argentina Thalassemia Treatment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 45: Rest of South America Thalassemia Treatment Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Thalassemia Treatment Industry?

The projected CAGR is approximately 7.60%.

2. Which companies are prominent players in the Thalassemia Treatment Industry?

Key companies in the market include Bluebird Bio, Novartis AG, Kiadis Pharma, SG Phrma Pvt Lmt *List Not Exhaustive, Acceleron Pharma Inc, Bellicum Pharmaceuticals, ApoPharma Inc, IONIS Pharmaceuticals, Pfizer Inc.

3. What are the main segments of the Thalassemia Treatment Industry?

The market segments include Treatment Type, Disease Type, End-User.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

; Rising Prevalence of Thalassemia; Increasing Awareness of Thalassemia Treatment.

6. What are the notable trends driving market growth?

Chelation Therapy segment is expected to be the Fastest Growing Segment.

7. Are there any restraints impacting market growth?

; High Cost of Treatment.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Thalassemia Treatment Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Thalassemia Treatment Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Thalassemia Treatment Industry?

To stay informed about further developments, trends, and reports in the Thalassemia Treatment Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence