Key Insights

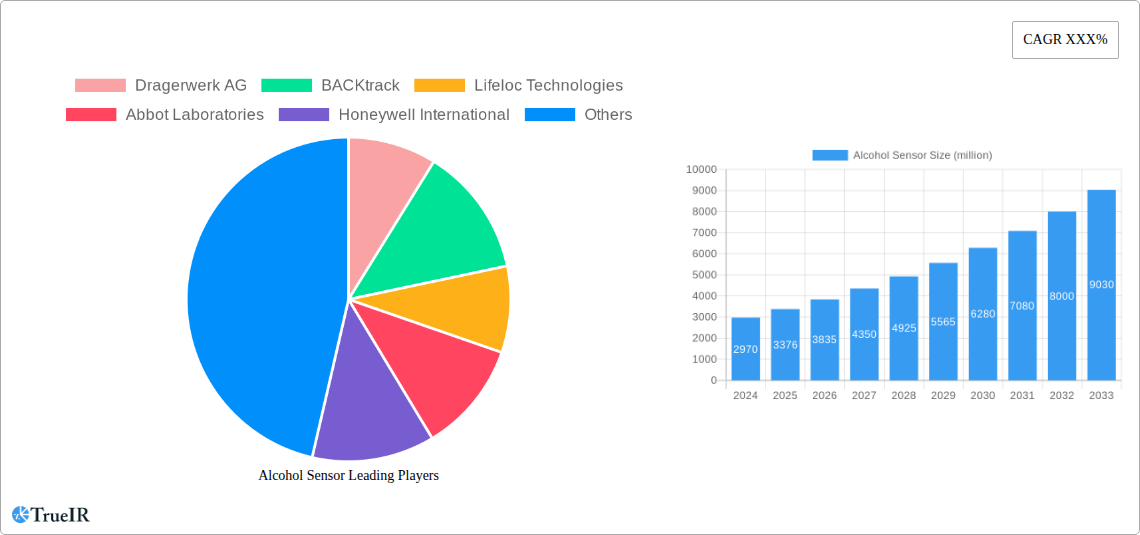

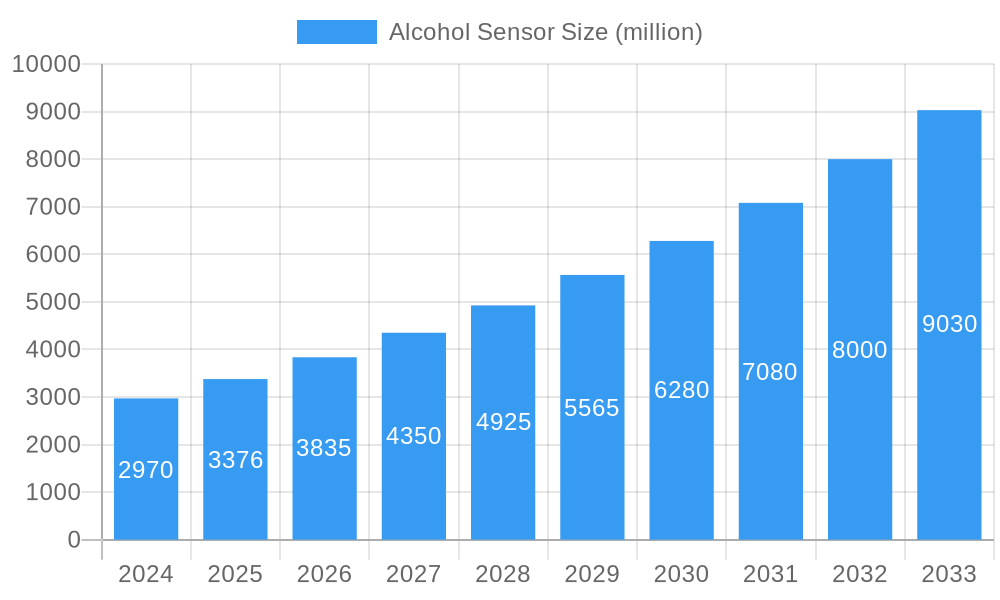

The global Alcohol Sensor market is experiencing robust growth, projected to reach an estimated USD 2.97 billion in 2024, driven by an impressive Compound Annual Growth Rate (CAGR) of 13.7% during the forecast period of 2025-2033. This substantial expansion is primarily fueled by the increasing adoption of alcohol sensors in critical applications such as vehicle controlling systems, including ignition interlocks and driver monitoring, to enhance road safety and reduce alcohol-related incidents. Furthermore, the growing demand for continuous and non-invasive alcohol monitoring in healthcare applications, for patient management and rehabilitation, is another significant growth catalyst. The market is also benefiting from advancements in sensor technologies, particularly in Fuel Cell Technology, which offers higher accuracy and faster response times, and Semiconductor Oxide Sensor Technology, known for its cost-effectiveness and durability.

Alcohol Sensor Market Size (In Billion)

The market's upward trajectory is further supported by the rising awareness and stringent regulatory frameworks globally mandating the use of alcohol detection devices in various sectors. Emerging trends include the integration of sophisticated AI and IoT capabilities into alcohol sensors for real-time data analysis and remote monitoring, expanding their utility beyond traditional applications. While the market enjoys strong growth drivers, potential restraints such as high initial investment costs for advanced technologies and the need for regular calibration and maintenance might present challenges. However, the continuous innovation in miniaturization, power efficiency, and enhanced detection capabilities by key players like Honeywell International, Dragerwerk AG, and Lifeloc Technologies, alongside expanding geographical reach into the Asia Pacific region, is expected to mitigate these constraints and pave the way for sustained market dominance.

Alcohol Sensor Company Market Share

This comprehensive Alcohol Sensor market research report provides an in-depth analysis of the global market, covering historical data, current trends, and future projections. The report leverages high-volume keywords and industry-specific insights to offer valuable intelligence for stakeholders.

Alcohol Sensor Market Structure & Competitive Landscape

The Alcohol Sensor market exhibits a moderate level of concentration, with a few key players dominating a significant share of the market. Innovation drivers are primarily fueled by advancements in sensor technology, including miniaturization, increased accuracy, and lower power consumption. Regulatory impacts, particularly in automotive safety and workplace drug testing, play a crucial role in shaping market dynamics. Product substitutes, such as breathalyzer apps and visual impairment tests, exist but often lack the precision and regulatory acceptance of dedicated alcohol sensors. End-user segmentation reveals strong demand from vehicle manufacturers for integrated alcohol detection systems and from healthcare providers for diagnostic and monitoring applications. Mergers and acquisitions (M&A) activity, with an estimated billion-dollar volume in recent years, indicates a strategic consolidation trend as companies seek to expand their product portfolios and market reach.

- Market Concentration: Moderate, with key players holding substantial market share.

- Innovation Drivers: Technological advancements in sensor accuracy, miniaturization, and power efficiency.

- Regulatory Impacts: Stringent regulations in automotive safety and occupational health.

- Product Substitutes: Breathalyzer apps, visual impairment tests.

- End-User Segmentation: Automotive, Healthcare, Law Enforcement, Personal Use.

- M&A Trends: Growing consolidation for portfolio expansion and market penetration.

Alcohol Sensor Market Trends & Opportunities

The global Alcohol Sensor market is poised for substantial growth, projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 7.5 billion percent from the base year of 2025 through to 2033. This robust expansion is driven by a confluence of factors, including increasing global emphasis on road safety, rising awareness of alcohol-related health issues, and stringent government mandates for alcohol detection in various applications. Technological advancements are continuously refining the performance of alcohol sensors, leading to enhanced accuracy, faster response times, and greater portability. The development of miniaturized and more cost-effective sensors is opening up new avenues for integration into a wider range of devices, from consumer electronics to advanced industrial equipment.

Consumer preferences are shifting towards proactive health monitoring and personalized safety solutions. This translates into a growing demand for user-friendly and reliable alcohol detection devices for personal use, such as portable breathalyzers. In the automotive sector, the push for autonomous driving and advanced driver-assistance systems (ADAS) is accelerating the adoption of alcohol interlock devices and in-cabin alcohol detection systems to prevent impaired driving incidents. This trend is further amplified by evolving legislation in numerous countries mandating such technologies.

The healthcare sector presents a significant opportunity for alcohol sensors, with applications ranging from non-invasive blood alcohol content (BAC) monitoring for patients with alcohol dependency to diagnostic tools for liver function and alcohol-related diseases. The increasing prevalence of chronic diseases and the growing adoption of remote patient monitoring systems will further fuel this demand.

Furthermore, the industrial sector is increasingly adopting alcohol sensors for workplace safety, particularly in industries dealing with hazardous materials or operating heavy machinery. Ensuring employee sobriety is critical for preventing accidents and maintaining productivity. The development of smart sensors that can communicate wirelessly and integrate with existing IoT platforms is creating new opportunities for real-time monitoring and data analytics.

The competitive landscape is characterized by ongoing product innovation and strategic partnerships. Companies are investing heavily in research and development to create next-generation sensors that offer superior performance and address emerging market needs. The market penetration rate for sophisticated alcohol sensors is expected to increase significantly as costs decrease and awareness of their benefits grows across diverse applications. The next decade promises to be a transformative period for the alcohol sensor market, marked by technological breakthroughs, expanding applications, and a steadfast commitment to safety and well-being.

Dominant Markets & Segments in Alcohol Sensor

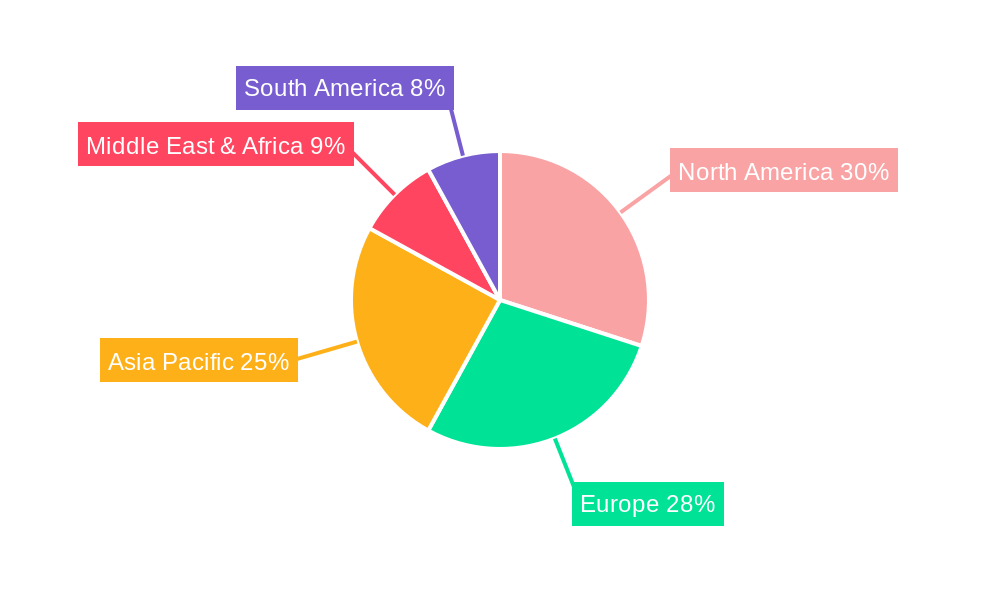

The Alcohol Sensor market demonstrates a clear dominance in specific regions and application segments, driven by a combination of regulatory frameworks, infrastructure development, and societal priorities.

Leading Region: North America currently leads the global alcohol sensor market, largely due to stringent alcohol-related driving laws, robust automotive safety standards, and a high prevalence of alcohol testing in law enforcement and occupational settings. The United States, in particular, has a well-established infrastructure for alcohol interlock programs and workplace screening, which significantly drives demand.

Dominant Application Segment: Vehicle Controlling The Vehicle Controlling application segment is the most prominent driver of the alcohol sensor market. This dominance is underpinned by several key growth factors:

- Mandatory Ignition Interlock Devices: Many jurisdictions worldwide mandate the installation of ignition interlock devices for individuals convicted of DUI offenses. This regulatory requirement creates a consistent and substantial demand for alcohol sensors within the automotive sector.

- Advanced Driver-Assistance Systems (ADAS) & Autonomous Driving: The integration of alcohol detection systems into ADAS and future autonomous vehicles is a significant growth catalyst. Automakers are prioritizing safety, and preventing impaired driving is a critical component of this strategy.

- Fleet Management: Commercial vehicle fleets are increasingly adopting alcohol detection systems to ensure driver sobriety and comply with transportation regulations, enhancing operational safety and efficiency.

- Passenger Vehicle Integration: A growing trend towards proactive safety features in passenger vehicles is leading manufacturers to explore in-cabin alcohol detection systems as a standard safety offering.

Dominant Type Segment: Fuel Cell Technology While Semiconductor Oxide Sensor Technology is also prevalent, Fuel Cell Technology is emerging as a dominant type for high-accuracy and reliable alcohol sensing. Its key advantages contribute to its growing market share:

- High Selectivity and Accuracy: Fuel cell sensors offer superior selectivity to ethanol, minimizing interference from other volatile organic compounds, leading to more accurate readings.

- Low Power Consumption: Their efficiency makes them ideal for battery-powered portable devices and in-vehicle applications where power conservation is crucial.

- Long Lifespan and Stability: Fuel cell sensors generally exhibit longer operational lifespans and greater stability compared to some other sensor types, reducing maintenance costs and replacement frequency.

- Regulatory Acceptance: Their proven accuracy and reliability have led to widespread acceptance by regulatory bodies for evidential breath testing.

The Healthcare Application segment is also experiencing significant growth, driven by the increasing focus on alcohol abuse as a public health concern. This includes applications in addiction monitoring, remote patient care, and diagnostic tools for liver health. The expansion of wearable technology and non-invasive monitoring solutions further bolsters this segment. The development of compact and user-friendly alcohol sensors is crucial for wider adoption in these diverse and impactful applications.

Alcohol Sensor Product Analysis

Recent product innovations in the alcohol sensor market are characterized by advancements in miniaturization, enhanced accuracy, and multi-analyte detection capabilities. Companies are developing fuel cell-based sensors that offer superior specificity and faster response times, crucial for real-time applications like in-vehicle monitoring and personal breathalyzers. Semiconductor oxide sensors are also evolving with improved selectivity and reduced power consumption, making them suitable for a wider array of portable devices. The competitive advantage lies in achieving a balance between cost-effectiveness, accuracy, and ease of use, enabling broader market penetration across automotive safety, healthcare, and personal monitoring sectors.

Key Drivers, Barriers & Challenges in Alcohol Sensor

Growth Drivers: The alcohol sensor market is propelled by an increasing global emphasis on road safety, leading to stringent regulations for alcohol interlock devices and in-vehicle alcohol detection systems. Technological advancements, particularly in fuel cell and semiconductor sensor technologies, are enhancing accuracy, miniaturization, and cost-effectiveness. Growing awareness of alcohol-related health issues and the demand for proactive health monitoring solutions in the healthcare sector also serve as significant growth catalysts. Furthermore, increasing adoption in industrial safety and fleet management contributes to market expansion.

Barriers & Challenges: Regulatory complexities and varying standards across different regions can pose challenges for market penetration. The high initial cost of some advanced sensor technologies can be a restraint for widespread adoption, especially in price-sensitive markets. Supply chain disruptions for key components and the need for calibration and maintenance of sensors can also impact market growth. Intense competition among existing players and emerging market entrants necessitates continuous innovation and competitive pricing strategies.

Growth Drivers in the Alcohol Sensor Market

Key growth drivers in the alcohol sensor market stem from escalating global road safety initiatives, which are mandating the use of alcohol interlock devices and in-vehicle alcohol detection systems. Continuous technological innovation in fuel cell and semiconductor sensor technologies is leading to more accurate, miniaturized, and cost-effective solutions. The increasing public health focus on alcohol abuse, coupled with the growing demand for non-invasive health monitoring devices in the healthcare sector, further fuels market expansion. Additionally, the rising implementation of strict safety protocols in industrial settings and the demand for enhanced driver monitoring in commercial fleets are significant contributors to market growth.

Challenges Impacting Alcohol Sensor Growth

Challenges impacting alcohol sensor growth include navigating diverse and evolving regulatory landscapes across different countries, which can create market access hurdles. The relatively high initial investment cost associated with some advanced sensor technologies can limit their widespread adoption, particularly in developing economies. Disruptions in the global supply chain for critical sensor components can affect production and availability. Furthermore, the ongoing need for regular calibration and maintenance of alcohol sensors adds to the operational costs for end-users. Intense competition also necessitates continuous product development and competitive pricing strategies to maintain market share.

Key Players Shaping the Alcohol Sensor Market

- Dragerwerk AG

- BACKtrack

- Lifeloc Technologies

- Abbot Laboratories

- Honeywell International

- Asahi Kasei

- Alcohol Countermeasure Systems

- AlcoPro

- Giner Labs

- Intoximeters

Significant Alcohol Sensor Industry Milestones

- 2019: Increased focus on stricter DUI enforcement globally, leading to expanded adoption of ignition interlock devices.

- 2020: Advancements in fuel cell technology leading to enhanced accuracy and reduced response times in breathalyzers.

- 2021: Introduction of more compact and portable alcohol sensors for personal and consumer applications.

- 2022: Growing integration of alcohol detection capabilities into advanced driver-assistance systems (ADAS) in passenger vehicles.

- 2023: Increased research into non-invasive alcohol monitoring for healthcare applications, including wearable devices.

- 2024: Collaborations between sensor manufacturers and automotive OEMs to develop next-generation in-cabin alcohol detection systems.

Future Outlook for Alcohol Sensor Market

The future outlook for the Alcohol Sensor market is exceptionally promising, with growth catalysts driven by continued technological innovation and expanding applications. The increasing integration of alcohol detection systems into autonomous vehicles and smart devices will create new revenue streams. Furthermore, the growing emphasis on preventative healthcare and the development of sophisticated diagnostic tools for alcohol-related conditions will further bolster the healthcare segment. Strategic partnerships between technology providers and end-users, coupled with favorable regulatory developments, will accelerate market penetration, positioning the alcohol sensor as an indispensable tool for safety, health, and well-being across diverse industries.

Alcohol Sensor Segmentation

-

1. Application

- 1.1. Vehicle Controlling

- 1.2. Healthcare Application

-

2. Type

- 2.1. Fuel Cell Technology

- 2.2. Semiconductor Oxide Sensor Technology

- 2.3. Others

Alcohol Sensor Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Alcohol Sensor Regional Market Share

Geographic Coverage of Alcohol Sensor

Alcohol Sensor REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 13.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Alcohol Sensor Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Vehicle Controlling

- 5.1.2. Healthcare Application

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Fuel Cell Technology

- 5.2.2. Semiconductor Oxide Sensor Technology

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Alcohol Sensor Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Vehicle Controlling

- 6.1.2. Healthcare Application

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Fuel Cell Technology

- 6.2.2. Semiconductor Oxide Sensor Technology

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Alcohol Sensor Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Vehicle Controlling

- 7.1.2. Healthcare Application

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Fuel Cell Technology

- 7.2.2. Semiconductor Oxide Sensor Technology

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Alcohol Sensor Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Vehicle Controlling

- 8.1.2. Healthcare Application

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Fuel Cell Technology

- 8.2.2. Semiconductor Oxide Sensor Technology

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Alcohol Sensor Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Vehicle Controlling

- 9.1.2. Healthcare Application

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Fuel Cell Technology

- 9.2.2. Semiconductor Oxide Sensor Technology

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Alcohol Sensor Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Vehicle Controlling

- 10.1.2. Healthcare Application

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Fuel Cell Technology

- 10.2.2. Semiconductor Oxide Sensor Technology

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Dragerwerk AG

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 BACKtrack

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Lifeloc Technologies

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Abbot Laboratories

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Honeywell International

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Asahi Kasei

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Alcohol Countermeasure Systems

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 AlcoPro

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Giner Labs

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Intoximeters

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.1 Dragerwerk AG

List of Figures

- Figure 1: Global Alcohol Sensor Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Alcohol Sensor Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Alcohol Sensor Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Alcohol Sensor Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Alcohol Sensor Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Alcohol Sensor Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Alcohol Sensor Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Alcohol Sensor Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Alcohol Sensor Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Alcohol Sensor Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Alcohol Sensor Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Alcohol Sensor Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Alcohol Sensor Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Alcohol Sensor Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Alcohol Sensor Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Alcohol Sensor Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Alcohol Sensor Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Alcohol Sensor Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Alcohol Sensor Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Alcohol Sensor Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Alcohol Sensor Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Alcohol Sensor Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Alcohol Sensor Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Alcohol Sensor Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Alcohol Sensor Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Alcohol Sensor Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Alcohol Sensor Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Alcohol Sensor Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Alcohol Sensor Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Alcohol Sensor Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Alcohol Sensor Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Alcohol Sensor Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Alcohol Sensor Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Alcohol Sensor Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Alcohol Sensor Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Alcohol Sensor Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Alcohol Sensor Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Alcohol Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Alcohol Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Alcohol Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Alcohol Sensor Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Alcohol Sensor Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Alcohol Sensor Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Alcohol Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Alcohol Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Alcohol Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Alcohol Sensor Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Alcohol Sensor Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Alcohol Sensor Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Alcohol Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Alcohol Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Alcohol Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Alcohol Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Alcohol Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Alcohol Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Alcohol Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Alcohol Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Alcohol Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Alcohol Sensor Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Alcohol Sensor Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Alcohol Sensor Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Alcohol Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Alcohol Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Alcohol Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Alcohol Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Alcohol Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Alcohol Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Alcohol Sensor Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Alcohol Sensor Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Alcohol Sensor Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Alcohol Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Alcohol Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Alcohol Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Alcohol Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Alcohol Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Alcohol Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Alcohol Sensor Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Alcohol Sensor?

The projected CAGR is approximately 13.7%.

2. Which companies are prominent players in the Alcohol Sensor?

Key companies in the market include Dragerwerk AG, BACKtrack, Lifeloc Technologies, Abbot Laboratories, Honeywell International, Asahi Kasei, Alcohol Countermeasure Systems, AlcoPro, Giner Labs, Intoximeters.

3. What are the main segments of the Alcohol Sensor?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Alcohol Sensor," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Alcohol Sensor report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Alcohol Sensor?

To stay informed about further developments, trends, and reports in the Alcohol Sensor, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence