Key Insights

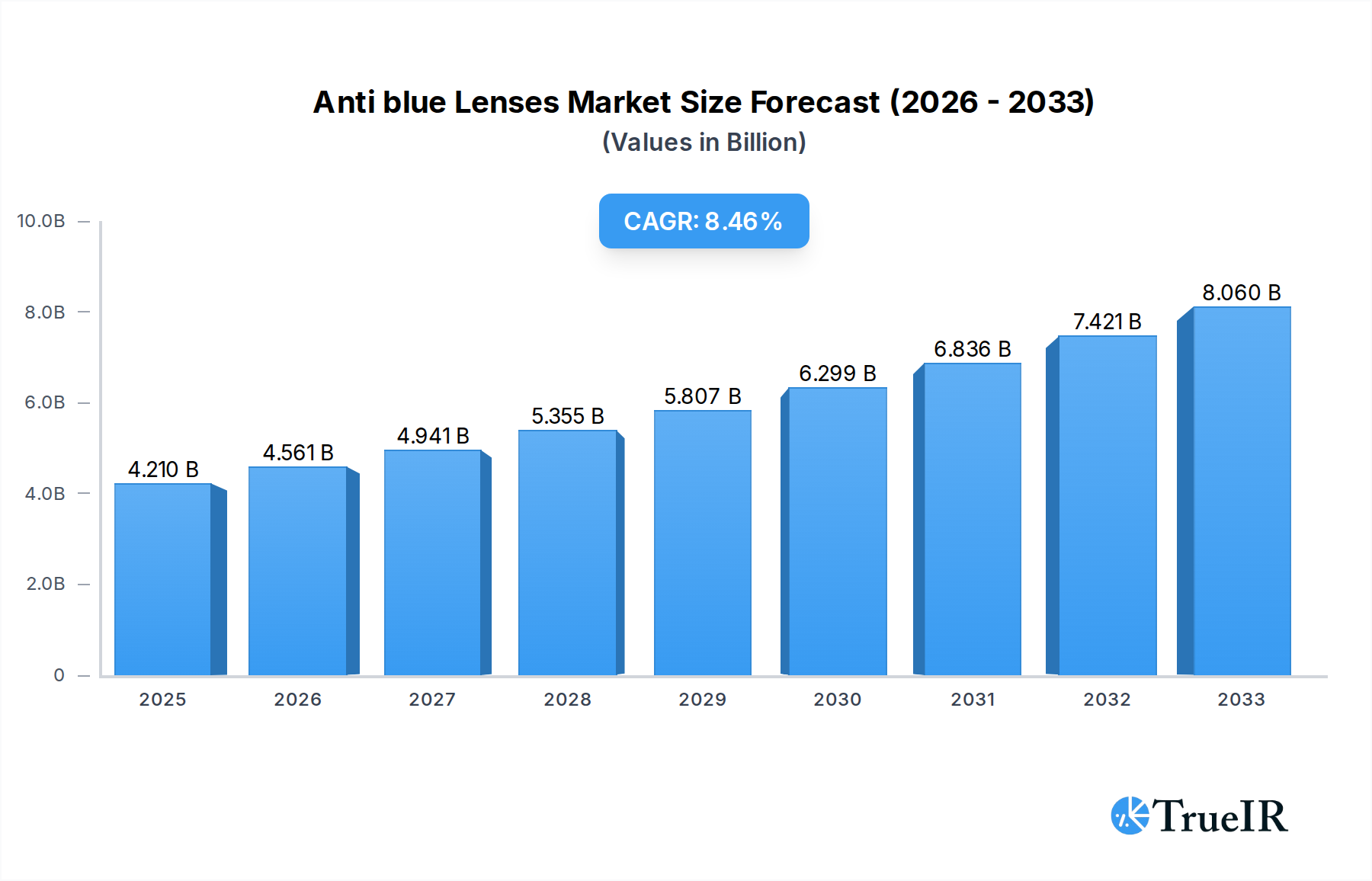

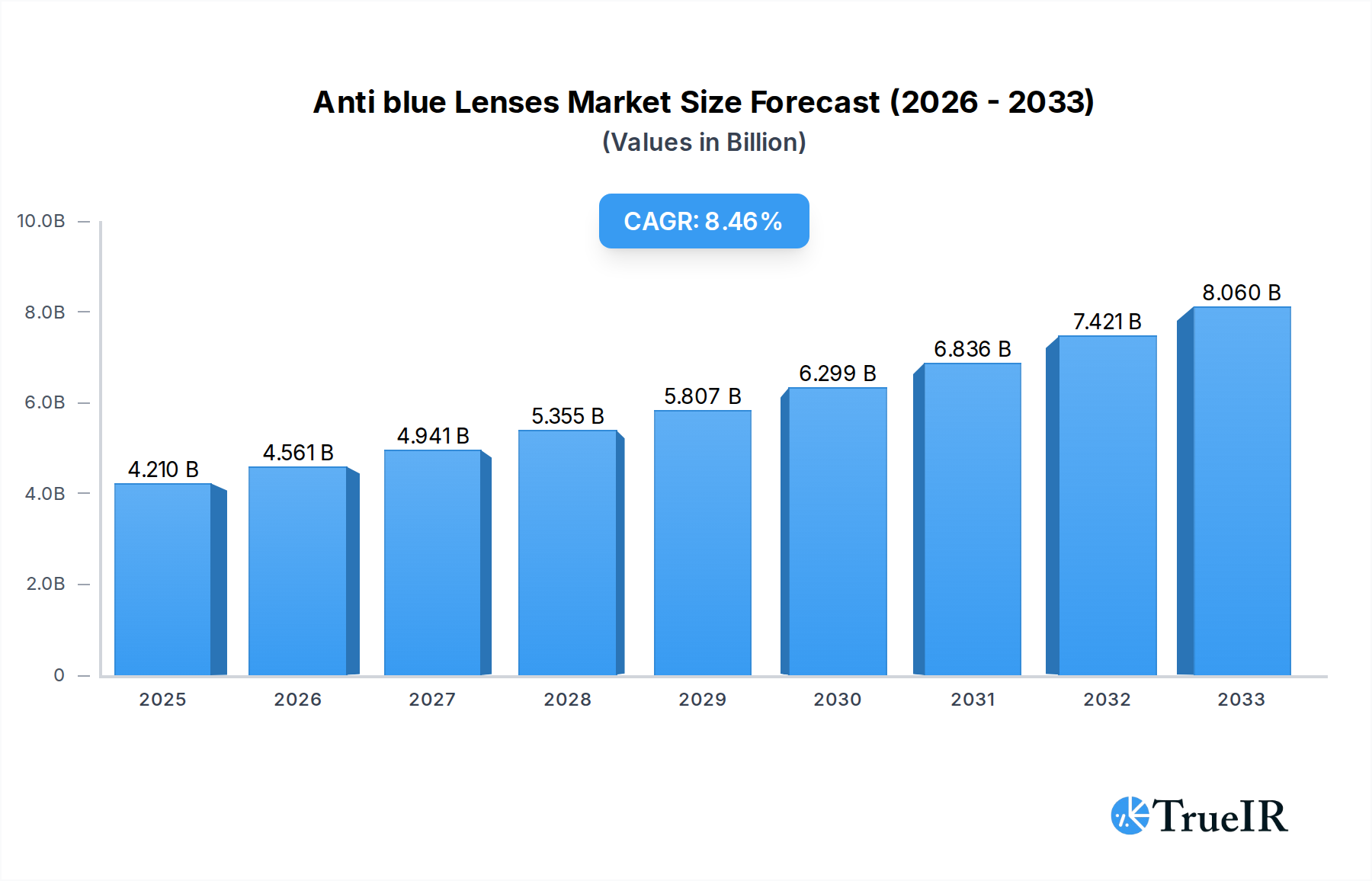

The global anti-blue light lens market is poised for significant expansion, projected to reach an estimated $4.21 billion in 2025. This robust growth is driven by an increasing awareness of the detrimental effects of blue light emitted from digital devices on eye health and sleep patterns. As screen time continues to escalate across all demographics, the demand for protective eyewear is surging. Key market drivers include the growing prevalence of digital eye strain, the rising adoption of smart devices, and a heightened focus on preventative eye care, particularly among younger generations who are digital natives. Furthermore, advancements in lens technology, leading to more effective and aesthetically pleasing blue light filtering solutions, are also fueling market penetration. The CAGR of 8.19% underscores a strong and sustained upward trajectory for the anti-blue light lens market over the forecast period of 2025-2033.

Anti blue Lenses Market Size (In Billion)

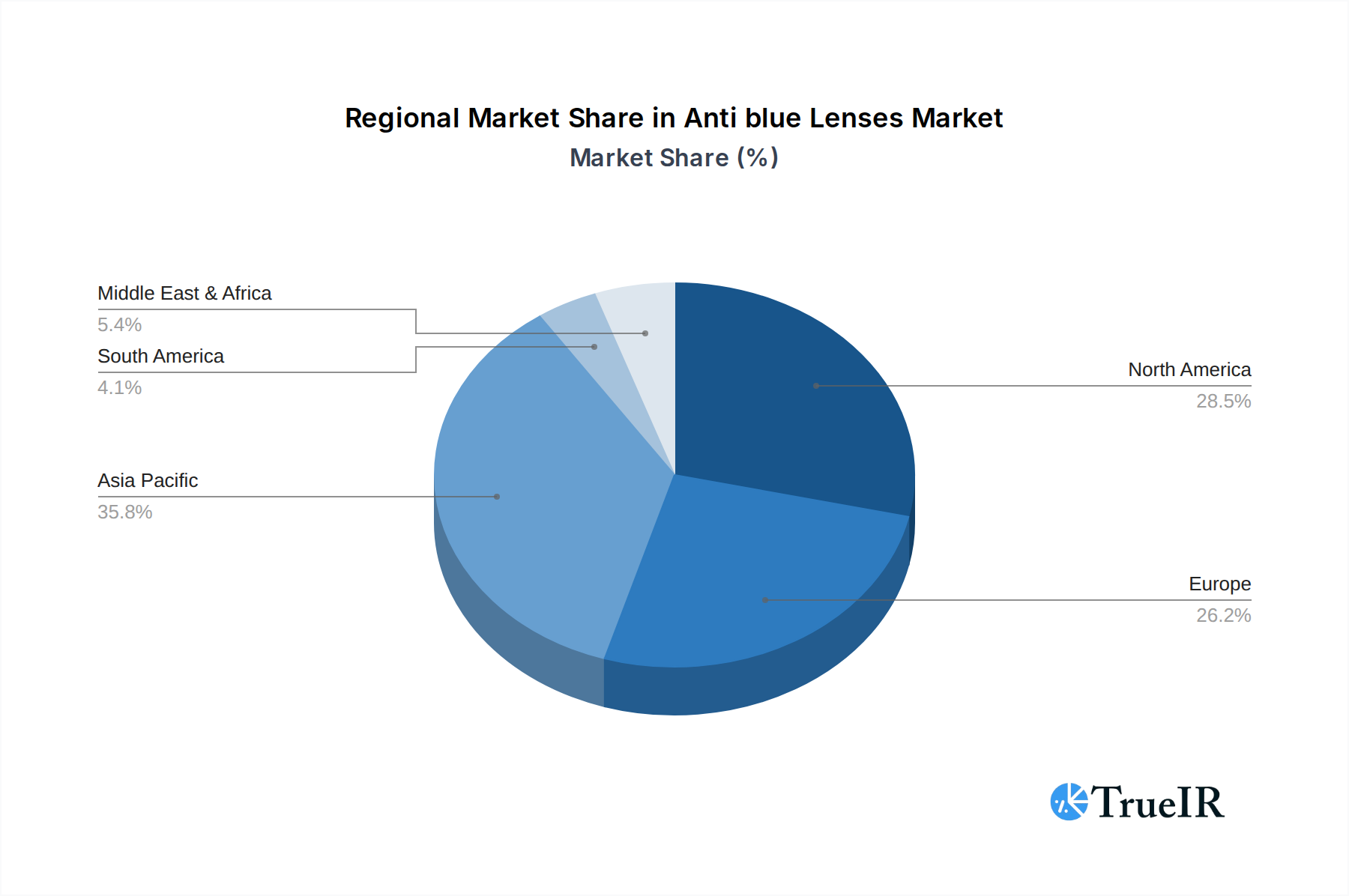

The market's segmentation by application reveals a broad consumer base, encompassing children, teenagers, and adults, all of whom are increasingly exposed to blue light. By type, resin lenses are expected to dominate due to their lightweight, impact-resistant, and customizable nature, while glass lenses and other advanced materials will cater to specific consumer preferences. Geographically, the Asia Pacific region, led by China and India, is anticipated to exhibit the fastest growth due to a large population, increasing disposable incomes, and rapid digital adoption. North America and Europe, with their mature markets and high consumer consciousness regarding eye health, will continue to be significant revenue generators. Challenges such as fluctuating raw material prices and the need for continuous innovation to stay ahead of technological advancements in digital devices will require strategic navigation by market players like ZEISS, HOYA Corporation, and Nikon.

Anti blue Lenses Company Market Share

Here is the SEO-optimized report description for Anti-blue Lenses, structured as requested:

Anti blue Lenses Market Structure & Competitive Landscape

The global anti-blue lenses market is characterized by a moderately concentrated structure, driven by significant investments in research and development and increasing consumer awareness regarding digital eye strain. Key innovation drivers include advancements in lens coating technologies and material science, enabling enhanced blue light filtration without compromising visual clarity or color perception. Regulatory impacts are primarily focused on product safety and performance standards, ensuring effective blue light blocking capabilities. Product substitutes, while present in the form of general UV-blocking lenses or digital eye strain reduction software, offer a less direct solution compared to specialized anti-blue lenses. End-user segmentation reveals a growing demand across Children, Teenagers, and Adults, fueled by pervasive screen time across all age demographics. Mergers and acquisitions (M&A) activity within the industry is moderate, with larger optical giants strategically acquiring smaller, innovative firms to expand their product portfolios and market reach. The concentration ratio in the top five companies is estimated at approximately 70 billion. M&A volumes are projected to reach 5 billion in transactions over the forecast period.

Anti blue Lenses Market Trends & Opportunities

The anti-blue lenses market is experiencing robust growth, projected to reach a market size of 250 billion by 2033, with a Compound Annual Growth Rate (CAGR) of 12.5% during the forecast period of 2025–2033. This expansion is primarily attributed to the escalating prevalence of digital device usage across all age groups, leading to increased instances of digital eye strain, sleep disturbances, and potential long-term retinal damage. Technological shifts are central to this trend, with manufacturers continuously innovating to develop more efficient and aesthetically pleasing anti-blue lens solutions. This includes advancements in multi-layer coatings, embedded blue-light filtering materials, and photochromic anti-blue lenses that adapt to light conditions. Consumer preferences are evolving towards lenses that offer superior blue light protection without compromising optical performance or style. This has led to a demand for lenses that are clear, virtually indistinguishable from standard lenses, and compatible with various prescription strengths and frame styles. Competitive dynamics are intensifying, with established optical leaders investing heavily in marketing and product development to capture market share. Opportunities abound for companies that can offer a balance of advanced technology, competitive pricing, and effective consumer education. The market penetration rate for specialized anti-blue lenses is steadily increasing, estimated to reach 35 billion units by 2033. Emerging trends also include the integration of blue light filtering into smart eyewear and augmented reality devices, opening new avenues for market expansion.

Dominant Markets & Segments in Anti blue Lenses

The global anti-blue lenses market exhibits distinct regional dominance and segment preferences. North America and Asia Pacific are projected to lead market growth, driven by high disposable incomes, widespread adoption of digital technologies, and a growing awareness of eye health. Within Asia Pacific, China is a significant contributor, with a substantial market size of approximately 60 billion, due to the vast population and increasing screen time among both urban and rural demographics. The Adults segment holds the largest market share, accounting for an estimated 70 billion in revenue by 2033. This dominance is fueled by prolonged working hours spent in front of computers and increased leisure time on digital devices. Key growth drivers within this segment include occupational requirements for prolonged screen use and a rising health consciousness.

The Children and Teenagers segments are experiencing the fastest growth, with CAGRs estimated at 15% and 14% respectively. This surge is directly linked to the ubiquitous presence of smartphones, tablets, and gaming consoles in educational settings and daily life, raising parental concerns about the impact of blue light on developing eyes. Government initiatives promoting digital literacy in schools and increasing accessibility to affordable digital devices further bolster this growth.

In terms of lens Types, Resin Lenses are the most dominant, representing a market share of roughly 85 billion by 2033. This preference is driven by their lightweight nature, impact resistance, and versatility in incorporating advanced coatings. Resin lenses are also more conducive to integration with various lens designs, including progressive and bifocal options, catering to a broader consumer base. While Glass Lenses and Other types (e.g., polycarbonate) hold smaller market shares, innovation in these areas continues, particularly in specialized applications or niche markets. The adoption of resin lenses is supported by widespread availability and manufacturing capabilities, making them the preferred choice for mass-market anti-blue lenses.

Anti blue Lenses Product Analysis

Product innovation in anti-blue lenses centers on enhanced blue light filtration efficacy and improved visual comfort. Manufacturers are developing advanced multi-layer anti-reflective coatings and embedding blue-light blocking materials directly into the lens matrix. Competitive advantages lie in achieving superior blue light reduction (e.g., filtering up to 90% of harmful blue light) without causing color distortion or glare. Applications are expanding beyond prescription eyewear to include non-prescription blue light blocking glasses for general use and specialized lenses for gamers and professionals.

Key Drivers, Barriers & Challenges in Anti blue Lenses

Key drivers propelling the anti-blue lenses market include the escalating global screen time across all demographics, heightened consumer awareness of digital eye strain and its associated health risks, and significant advancements in lens technology, such as improved coatings and materials offering better blue light filtration without compromising visual quality. Technological advancements in manufacturing processes are also reducing production costs, making these lenses more accessible.

Challenges impacting growth include the need for greater consumer education on the specific benefits and scientifically proven efficacy of anti-blue lenses, potentially leading to market skepticism. Regulatory hurdles, while generally promoting safety, can add to development costs and time. Supply chain issues for specialized coatings and materials can also pose a restraint. Furthermore, intense competition from numerous brands and the availability of less advanced substitutes present a challenge in capturing market share.

Growth Drivers in the Anti blue Lenses Market

The anti-blue lenses market is propelled by several key growth drivers. The ubiquitous adoption of digital devices, from smartphones to laptops, has created an unprecedented level of daily screen exposure across all age groups, making eye protection a growing concern. This surge in screen time directly correlates with an increased incidence of digital eye strain, sleep cycle disruption, and other vision-related discomforts, fueling demand for effective solutions. Technological innovation in lens manufacturing, particularly in the development of advanced multi-layer coatings and embedded filtering materials, allows for superior blue light absorption without sacrificing optical clarity or aesthetic appeal. Furthermore, growing consumer awareness regarding the potential long-term health impacts of prolonged blue light exposure, such as retinal damage, is a significant catalyst for market growth. Government policies promoting digital literacy and the use of electronic devices in educational institutions also contribute to this expanding market.

Challenges Impacting Anti blue Lenses Growth

Despite robust growth potential, the anti-blue lenses market faces several significant challenges. A primary restraint is the perceived lack of definitive scientific consensus among some consumer segments regarding the necessity and efficacy of blue light filtering, leading to skepticism and lower adoption rates. This necessitates more comprehensive and accessible consumer education campaigns. Regulatory complexities, while ensuring product safety, can also introduce hurdles in terms of product certification and marketing claims, potentially increasing development costs. Supply chain disruptions for specialized raw materials and advanced coatings can impact production timelines and cost-effectiveness. Furthermore, the highly competitive landscape, with numerous market players and the availability of alternative, less specialized eye protection products, exerts pressure on pricing and market differentiation.

Key Players Shaping the Anti blue Lenses Market

- ZEISS

- HOYA Corporation

- Nikon

- Essilor

- Rodenstock

- Tokai

- Chemilens

- Mingyue Optical Lens Co

- WAN XIN

- Seiko Vision

- Shanghai Conant Optical Co

- Akimbo Gaming Co

Significant Anti blue Lenses Industry Milestones

- 2019: Introduction of advanced multi-layer anti-blue coatings offering enhanced blue light blocking without color distortion.

- 2020: Launch of specialized anti-blue lenses targeting the gaming community, emphasizing performance and eye comfort.

- 2021: Increased consumer awareness campaigns highlighting the impact of blue light on sleep patterns and eye health.

- 2022: Development and market introduction of embedded blue-light filtering materials directly within lens polymers.

- 2023: Expansion of anti-blue lens options into non-prescription eyewear and sunglasses segments.

- 2024: Integration of anti-blue filtering technology into smart glasses and augmented reality devices.

Future Outlook for Anti blue Lenses Market

The future outlook for the anti-blue lenses market is exceptionally positive, driven by sustained growth in digital device usage and a deepening understanding of its health implications. Strategic opportunities lie in the continued development of innovative lens technologies that offer a superior balance of efficacy, comfort, and aesthetics. The expanding market penetration into pediatric and geriatric segments, alongside specialized applications for professionals and gamers, presents significant growth catalysts. Furthermore, collaborations between optical manufacturers and technology companies to integrate blue light filtering into next-generation wearable devices will further shape market potential. The focus on personalized lens solutions, tailored to individual needs and screen exposure habits, will also be a key driver of future success.

Anti blue Lenses Segmentation

-

1. Application

- 1.1. Children

- 1.2. Teenagers

- 1.3. Adults

-

2. Types

- 2.1. Resin Lenses

- 2.2. Glass Lenses

- 2.3. Other

Anti blue Lenses Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Anti blue Lenses Regional Market Share

Geographic Coverage of Anti blue Lenses

Anti blue Lenses REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.19% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Anti blue Lenses Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Children

- 5.1.2. Teenagers

- 5.1.3. Adults

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Resin Lenses

- 5.2.2. Glass Lenses

- 5.2.3. Other

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Anti blue Lenses Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Children

- 6.1.2. Teenagers

- 6.1.3. Adults

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Resin Lenses

- 6.2.2. Glass Lenses

- 6.2.3. Other

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Anti blue Lenses Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Children

- 7.1.2. Teenagers

- 7.1.3. Adults

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Resin Lenses

- 7.2.2. Glass Lenses

- 7.2.3. Other

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Anti blue Lenses Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Children

- 8.1.2. Teenagers

- 8.1.3. Adults

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Resin Lenses

- 8.2.2. Glass Lenses

- 8.2.3. Other

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Anti blue Lenses Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Children

- 9.1.2. Teenagers

- 9.1.3. Adults

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Resin Lenses

- 9.2.2. Glass Lenses

- 9.2.3. Other

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Anti blue Lenses Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Children

- 10.1.2. Teenagers

- 10.1.3. Adults

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Resin Lenses

- 10.2.2. Glass Lenses

- 10.2.3. Other

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 ZEISS

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 HOYA Corporation

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Nikon

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Essilor

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Rodenstock

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Tokai

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Chemilens

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Mingyue Optical Lens Co

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 WAN XIN

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Seiko Vision

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Shanghai Conant Optical Co

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Akimbo Gaming Co

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.1 ZEISS

List of Figures

- Figure 1: Global Anti blue Lenses Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Anti blue Lenses Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Anti blue Lenses Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Anti blue Lenses Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Anti blue Lenses Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Anti blue Lenses Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Anti blue Lenses Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Anti blue Lenses Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Anti blue Lenses Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Anti blue Lenses Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Anti blue Lenses Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Anti blue Lenses Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Anti blue Lenses Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Anti blue Lenses Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Anti blue Lenses Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Anti blue Lenses Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Anti blue Lenses Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Anti blue Lenses Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Anti blue Lenses Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Anti blue Lenses Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Anti blue Lenses Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Anti blue Lenses Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Anti blue Lenses Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Anti blue Lenses Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Anti blue Lenses Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Anti blue Lenses Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Anti blue Lenses Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Anti blue Lenses Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Anti blue Lenses Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Anti blue Lenses Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Anti blue Lenses Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Anti blue Lenses Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Anti blue Lenses Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Anti blue Lenses Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Anti blue Lenses Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Anti blue Lenses Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Anti blue Lenses Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Anti blue Lenses Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Anti blue Lenses Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Anti blue Lenses Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Anti blue Lenses Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Anti blue Lenses Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Anti blue Lenses Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Anti blue Lenses Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Anti blue Lenses Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Anti blue Lenses Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Anti blue Lenses Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Anti blue Lenses Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Anti blue Lenses Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Anti blue Lenses Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Anti blue Lenses Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Anti blue Lenses Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Anti blue Lenses Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Anti blue Lenses Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Anti blue Lenses Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Anti blue Lenses Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Anti blue Lenses Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Anti blue Lenses Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Anti blue Lenses Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Anti blue Lenses Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Anti blue Lenses Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Anti blue Lenses Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Anti blue Lenses Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Anti blue Lenses Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Anti blue Lenses Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Anti blue Lenses Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Anti blue Lenses Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Anti blue Lenses Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Anti blue Lenses Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Anti blue Lenses Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Anti blue Lenses Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Anti blue Lenses Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Anti blue Lenses Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Anti blue Lenses Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Anti blue Lenses Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Anti blue Lenses Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Anti blue Lenses Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Anti blue Lenses?

The projected CAGR is approximately 8.19%.

2. Which companies are prominent players in the Anti blue Lenses?

Key companies in the market include ZEISS, HOYA Corporation, Nikon, Essilor, Rodenstock, Tokai, Chemilens, Mingyue Optical Lens Co, WAN XIN, Seiko Vision, Shanghai Conant Optical Co, Akimbo Gaming Co.

3. What are the main segments of the Anti blue Lenses?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Anti blue Lenses," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Anti blue Lenses report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Anti blue Lenses?

To stay informed about further developments, trends, and reports in the Anti blue Lenses, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence