Key Insights

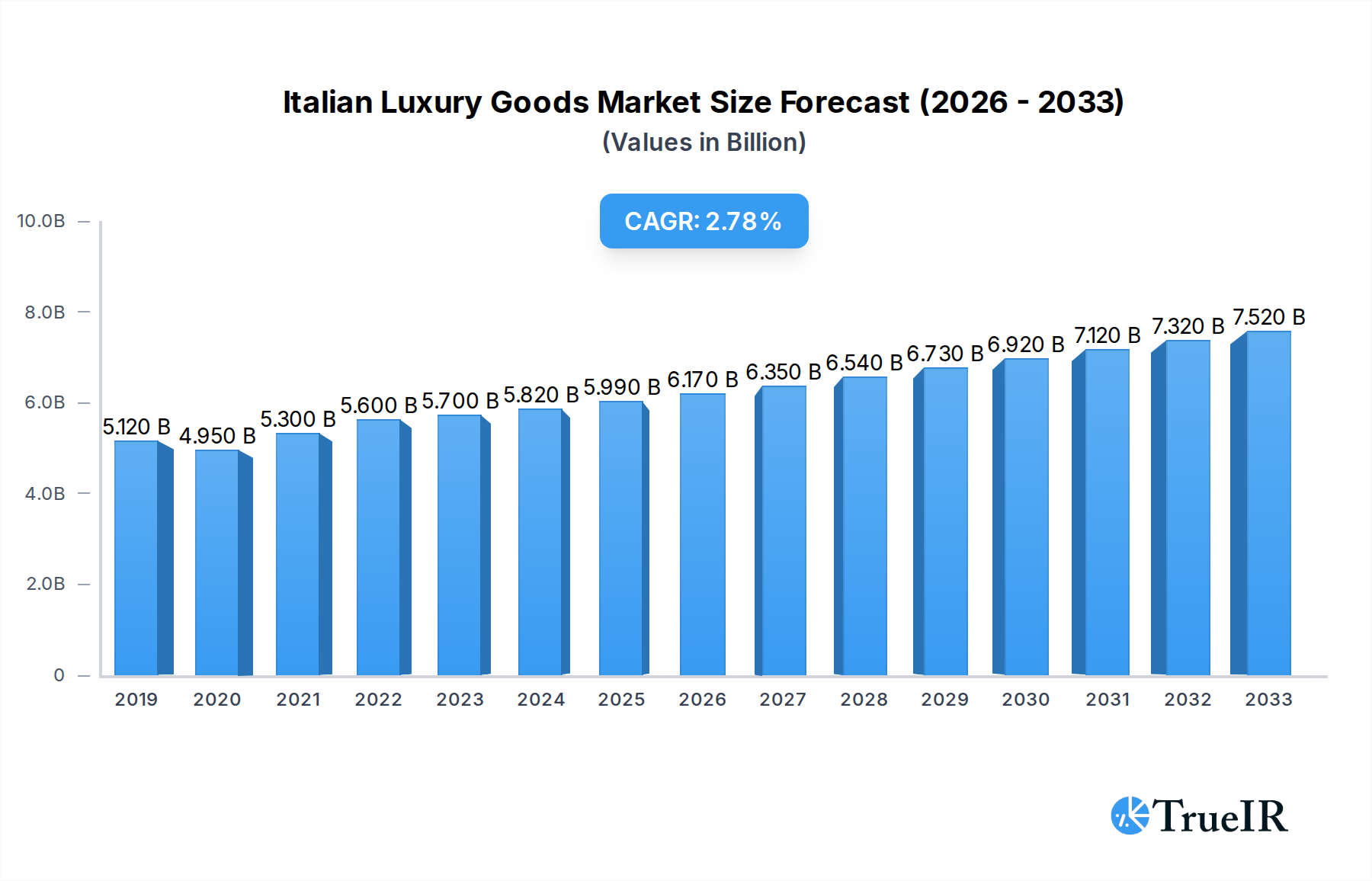

The Italian luxury goods market is poised for steady growth, projected to reach an estimated €5.82 billion in 2024, with a Compound Annual Growth Rate (CAGR) of 3.18% through 2033. This expansion is fueled by robust consumer demand for high-quality, artisanal products and the enduring allure of Italian craftsmanship and heritage. Key growth drivers include the increasing disposable incomes of affluent consumers, particularly among emerging market millennials and Gen Z who are keen on acquiring iconic luxury pieces. Furthermore, strategic brand expansions, innovative marketing campaigns, and a growing online presence are effectively reaching a wider global audience, reinforcing Italy's position as a preeminent destination for luxury fashion, accessories, and lifestyle products. The market's resilience is further bolstered by the continuous demand for timeless elegance and exclusivity, ensuring sustained interest from both established and new luxury patrons.

Italian Luxury Goods Market Market Size (In Billion)

The market's trajectory is influenced by a dynamic interplay of trends and restraints. Emerging trends such as personalization, sustainable luxury, and the integration of digital technologies in retail experiences are shaping consumer preferences and brand strategies. The increasing adoption of e-commerce platforms for luxury goods presents significant opportunities for market penetration and customer engagement. However, the market also faces challenges. Economic uncertainties and fluctuating exchange rates can impact consumer spending power. Intense competition from both established luxury houses and newer, digitally native brands necessitates continuous innovation and adaptation. Furthermore, the reliance on global tourism, which experienced disruptions in recent years, remains a significant factor, though recovery is anticipated. The market's segmentation, encompassing clothing, footwear, bags, jewelry, watches, and other accessories, demonstrates a diverse landscape where each category contributes to the overall market value and growth.

Italian Luxury Goods Market Company Market Share

Italian Luxury Goods Market: Comprehensive Analysis & Future Projections (2019-2033)

This in-depth report provides a granular analysis of the Italian luxury goods market, forecasting its trajectory from 2019 to 2033, with a base year of 2025. Delve into market dynamics, key players, and emerging trends, leveraging high-volume keywords like "Italian luxury market," "luxury fashion," "high-end accessories," and "Italian designer brands" for optimal SEO performance. The report details the market structure, competitive landscape, prevailing trends, dominant segments, product innovations, key drivers, and significant challenges, offering actionable insights for industry stakeholders aiming to capitalize on this vibrant and evolving sector. The Italian luxury goods market is poised for substantial growth, driven by innovation, changing consumer preferences, and strategic investments.

Italian Luxury Goods Market Market Structure & Competitive Landscape

The Italian luxury goods market is characterized by a moderate to high level of concentration, with a few dominant players controlling a significant market share. However, the presence of numerous established heritage brands and agile emerging designers fosters a dynamic competitive environment. Innovation drivers are manifold, encompassing sustainable practices, digitalization, personalized experiences, and the integration of blockchain and NFTs. Regulatory impacts are primarily focused on intellectual property protection, ethical sourcing, and consumer transparency. Product substitutes, while present in the broader consumer goods sector, are largely irrelevant in the high-end luxury segment where brand heritage, craftsmanship, and exclusivity are paramount. End-user segmentation reveals a growing demand from younger, affluent demographics, particularly in emerging economies, alongside traditional high-net-worth individuals. Mergers and acquisitions (M&A) trends indicate strategic consolidations aimed at expanding market reach, acquiring new technologies, and diversifying product portfolios. Quantitative data suggests an M&A volume in the billions of euros over the historical period, with concentration ratios indicating significant market power held by top-tier conglomerates.

- Market Concentration: Dominated by a few large groups, but with a robust ecosystem of smaller, specialized brands.

- Innovation Drivers: Sustainability, digitalization (e-commerce, NFTs), customization, and experiential retail.

- Regulatory Impacts: Focus on IP, ethical sourcing, and anti-counterfeiting measures.

- Product Substitutes: Limited within the core luxury segment due to brand equity and perceived value.

- End-User Segmentation: Increasing influence of Gen Z and Millennials, alongside established affluent consumers.

- M&A Trends: Strategic acquisitions for market expansion, talent acquisition, and technological integration.

Italian Luxury Goods Market Market Trends & Opportunities

The Italian luxury goods market is experiencing robust expansion, driven by a confluence of evolving consumer preferences, technological advancements, and strategic market penetration. The overall market size is projected to grow at a significant compound annual growth rate (CAGR) of approximately 7.5% during the forecast period (2025-2033). This growth is fueled by a rising global middle class with increasing disposable incomes and a burgeoning demand for premium and exclusive products. Technological shifts are profoundly reshaping the market, with a substantial increase in online sales channels accounting for over 30% of market penetration. This digital transformation encompasses enhanced e-commerce platforms, virtual showrooms, augmented reality (AR) try-on experiences, and the burgeoning integration of Non-Fungible Tokens (NFTs) to enhance exclusivity and provenance. Consumer preferences are increasingly gravitating towards sustainability, ethical sourcing, and artisanal craftsmanship. Brands that can authentically communicate their commitment to these values are gaining a competitive edge. Personalized products and bespoke services are also in high demand, offering consumers unique expressions of their individual style and status. Competitive dynamics are intensifying, with both established Italian heritage brands and international luxury powerhouses vying for market share. Opportunities lie in leveraging digital channels for direct-to-consumer (DTC) sales, exploring emerging markets in Asia and the Middle East, and developing innovative product offerings that resonate with the values of younger luxury consumers. The market for luxury watches and high-end jewelry is experiencing a resurgence, driven by investment appeal and status symbolism. Furthermore, the "Other Accessories" segment, encompassing items like luxury stationery, eyewear, and home décor, is witnessing steady growth as consumers seek to extend their luxury lifestyle beyond traditional fashion and accessories. The report estimates the total market value to reach over xx billion euros by 2033.

Dominant Markets & Segments in Italian Luxury Goods Market

The Italian luxury goods market exhibits a clear dominance across several key segments and distribution channels, with significant growth catalysts underpinning their success. Within the Type segmentation, Clothing and Apparel consistently holds the largest market share, estimated to be in the range of 35-40% of the total market value. This dominance is attributed to the enduring appeal of Italian fashion heritage, renowned for its exquisite tailoring, premium fabrics, and timeless designs. Footwear follows closely, with an estimated 20-25% market share, benefiting from the same legacy of craftsmanship and innovation. Bags represent another significant segment, accounting for approximately 15-20% of the market, driven by iconic designs and their role as status symbols. The Jewelry and Watches segments, while individually smaller, collectively contribute a substantial portion, estimated at 15-20%, with a particular emphasis on high-end timepieces and precious jewelry known for their investment value and intricate artistry. The Other Accessories segment, encompassing items like scarves, ties, belts, and eyewear, rounds out the product categories, demonstrating steady growth.

In terms of Distribution Channels, Single-brand Stores remain the most dominant, capturing an estimated 40-45% of the market. These flagship stores offer an immersive brand experience, reinforcing brand identity and exclusivity. Online Stores have witnessed exponential growth, now representing approximately 30-35% of the market. This surge is driven by convenience, wider reach, and the increasing comfort of consumers with purchasing high-value items online. Multi-brand Stores contribute a significant share, estimated at 20-25%, providing curated selections from various luxury brands. Other Distribution Channels, including department stores and travel retail, account for the remaining share.

Key growth drivers for these dominant segments include:

- Infrastructure: Well-developed retail infrastructure in major Italian cities and global fashion capitals, coupled with robust logistics networks supporting international e-commerce.

- Policies: Government support for the luxury sector through initiatives promoting Made in Italy, intellectual property protection, and trade agreements that facilitate exports.

- Brand Heritage & Craftsmanship: The unparalleled reputation of Italian brands for quality, artisanal skills, and historical legacy is a primary driver of consumer demand.

- Digitalization: Investment in sophisticated e-commerce platforms, virtual experiences, and targeted digital marketing strategies to reach a global online audience.

- Consumer Affluence: Sustained growth in global wealth, particularly in emerging economies, has expanded the consumer base for luxury goods.

The market value for clothing and apparel is estimated to be over xx billion euros in 2025, with footwear close behind. The online retail channel is projected to grow at a CAGR of over 10% through 2033, indicating its increasing importance.

Italian Luxury Goods Market Product Analysis

Product innovation in the Italian luxury goods market is a cornerstone of its enduring appeal. Brands are increasingly focusing on integrating cutting-edge technology with traditional craftsmanship. For instance, Prada's foray into NFTs with upcycled fabrics highlights a commitment to sustainability and digital innovation, offering unique digital ownership alongside tangible luxury. Hublot's new Milan store exemplifies sophisticated design and customer experience, blending premium materials like metal, wood, and glass to create an inviting and luxurious retail environment. Fendi's investment in a new shoe factory underscores a strategic focus on enhancing production capabilities and maintaining the "Made in Italy" quality for its footwear. These advancements in product design, material sourcing, and retail experience provide significant competitive advantages, catering to evolving consumer demands for both heritage and modernity. The market fit is enhanced by the ability to deliver exclusive, high-quality products that offer perceived value, longevity, and a distinct brand narrative.

Key Drivers, Barriers & Challenges in Italian Luxury Goods Market

Key Drivers in the Italian Luxury Goods Market:

- Strong Brand Heritage and "Made in Italy" Seal: The intrinsic value associated with Italian craftsmanship, design, and historical legacy continues to be a primary demand driver.

- Growing Global Affluence: Increasing disposable incomes in emerging economies create new consumer segments eager for luxury goods.

- Digital Transformation: The widespread adoption of e-commerce, social media marketing, and digital experiential technologies allows for wider market reach and enhanced customer engagement.

- Sustainability and Ethical Sourcing: A growing consumer consciousness for eco-friendly and ethically produced goods is pushing brands to adopt more sustainable practices, creating a competitive advantage for those who can demonstrably meet these demands.

- Personalization and Exclusivity: Demand for bespoke products, customized services, and limited-edition items drives innovation and customer loyalty.

Barriers and Challenges Impacting Italian Luxury Goods Market Growth:

- Counterfeiting and Intellectual Property Infringement: The pervasive issue of counterfeit luxury goods erodes brand value and profitability, requiring constant vigilance and investment in protective measures, estimated to cost the industry billions annually.

- Supply Chain Volatility and Geopolitical Instability: Disruptions in global supply chains due to political conflicts, trade disputes, or natural disasters can impact raw material sourcing and production timelines, leading to potential revenue losses of billions.

- Intensifying Competition: The market is highly competitive, with both established global luxury conglomerates and agile niche brands vying for consumer attention, demanding continuous innovation and strategic marketing.

- Changing Consumer Demographics and Preferences: Adapting to the evolving tastes and values of younger generations, particularly Gen Z, requires a dynamic approach to product development and marketing strategies.

- Regulatory Compliance: Navigating complex international trade regulations, import/export laws, and varying consumer protection standards across different markets presents ongoing challenges.

Growth Drivers in the Italian Luxury Goods Market Market

The Italian luxury goods market is propelled by several key growth drivers. The enduring appeal of the "Made in Italy" label, synonymous with unparalleled craftsmanship and design excellence, continues to attract discerning consumers globally. Economic growth in emerging markets, particularly in Asia and the Middle East, is expanding the affluent consumer base, eager to invest in premium products. Technological advancements are pivotal; the increasing adoption of e-commerce, augmented reality for virtual try-ons, and the exploration of NFTs for enhanced exclusivity and digital ownership are creating new avenues for sales and brand engagement. The burgeoning consumer demand for sustainable and ethically sourced products is also a significant driver, encouraging brands to invest in eco-friendly materials and transparent production processes. This focus on conscious consumption is reshaping brand narratives and consumer loyalty.

Challenges Impacting Italian Luxury Goods Market Growth

The Italian luxury goods market faces significant challenges that can impede its growth trajectory. The pervasive issue of counterfeiting continues to pose a substantial threat, leading to billions in lost revenue and brand dilution. Global supply chain disruptions, exacerbated by geopolitical tensions and logistical hurdles, can lead to production delays and increased costs, impacting profitability. Intense competition from both established global players and innovative niche brands demands continuous adaptation and investment in marketing and product development. Furthermore, navigating complex and evolving regulatory landscapes across different international markets requires significant resources and expertise. Evolving consumer preferences, particularly among younger demographics, necessitate agile responses in product design, marketing, and brand messaging to maintain relevance and appeal.

Key Players Shaping the Italian Luxury Goods Market Market

- The Estee Lauder Companies Inc

- KERING

- Prada S p A

- Ralph Lauren Corporation

- MAX MARA SRL

- PVH Corp

- TAG Heuer International SA

- L'OREAL

- LVMH Moët Hennessy Louis Vuitton

Significant Italian Luxury Goods Market Industry Milestones

- July 2022: Prada SA unveiled its second Timecapsule NFT collection, featuring a shirt made from upcycled fabric from the Prada archives, incorporating 'Jacquard Animalier' silk brocade, lurex fabric, and a Jacquard Thrush flower sourced from an early 20th-century French archive. This initiative signifies a strong push into digital fashion and sustainable luxury.

- May 2022: Fendi announced an investment to establish a new shoe factory in Fermo, located in Italy's Marche region. This strategic move aims to centralize production and relocate from its existing facility in Porto San Giorgio, enhancing manufacturing capabilities and efficiency.

- February 2022: Hublot, the Swiss luxury watch brand, inaugurated its fourth Italian store in Milan, situated at Via Verri 7. The new boutique spans two floors and features a sophisticated interior design combining metal, wood, and glass, offering an enhanced retail experience for its clientele.

Future Outlook for Italian Luxury Goods Market Market

The future outlook for the Italian luxury goods market remains exceptionally bright, poised for sustained growth driven by strategic innovation and evolving consumer desires. Key growth catalysts include the continued expansion of e-commerce, with a projected market penetration of over 40% by 2033, and the increasing adoption of virtual and augmented reality technologies to enhance online shopping experiences. The growing emphasis on sustainability and ethical sourcing will continue to shape product development and brand messaging, creating opportunities for companies that prioritize these values. Furthermore, the exploration of new technologies like blockchain for provenance tracking and NFTs for digital exclusivity will unlock novel revenue streams and customer engagement models. Emerging markets will continue to be crucial growth engines, demanding tailored strategies to cater to their unique consumer preferences and cultural nuances. The market is expected to witness strategic collaborations and potential mergers and acquisitions as companies seek to consolidate their positions and expand their global reach, ultimately driving the market value to surpass xx billion euros by 2033.

Italian Luxury Goods Market Segmentation

-

1. Type

- 1.1. Clothing and Apparel

- 1.2. Footwear

- 1.3. Bags

- 1.4. Jewelry

- 1.5. Watches

- 1.6. Other Accessories

-

2. Distibution Channel

- 2.1. Single-brand Stores

- 2.2. Multi-brand Stores

- 2.3. Online Stores

- 2.4. Other Distribution Channels

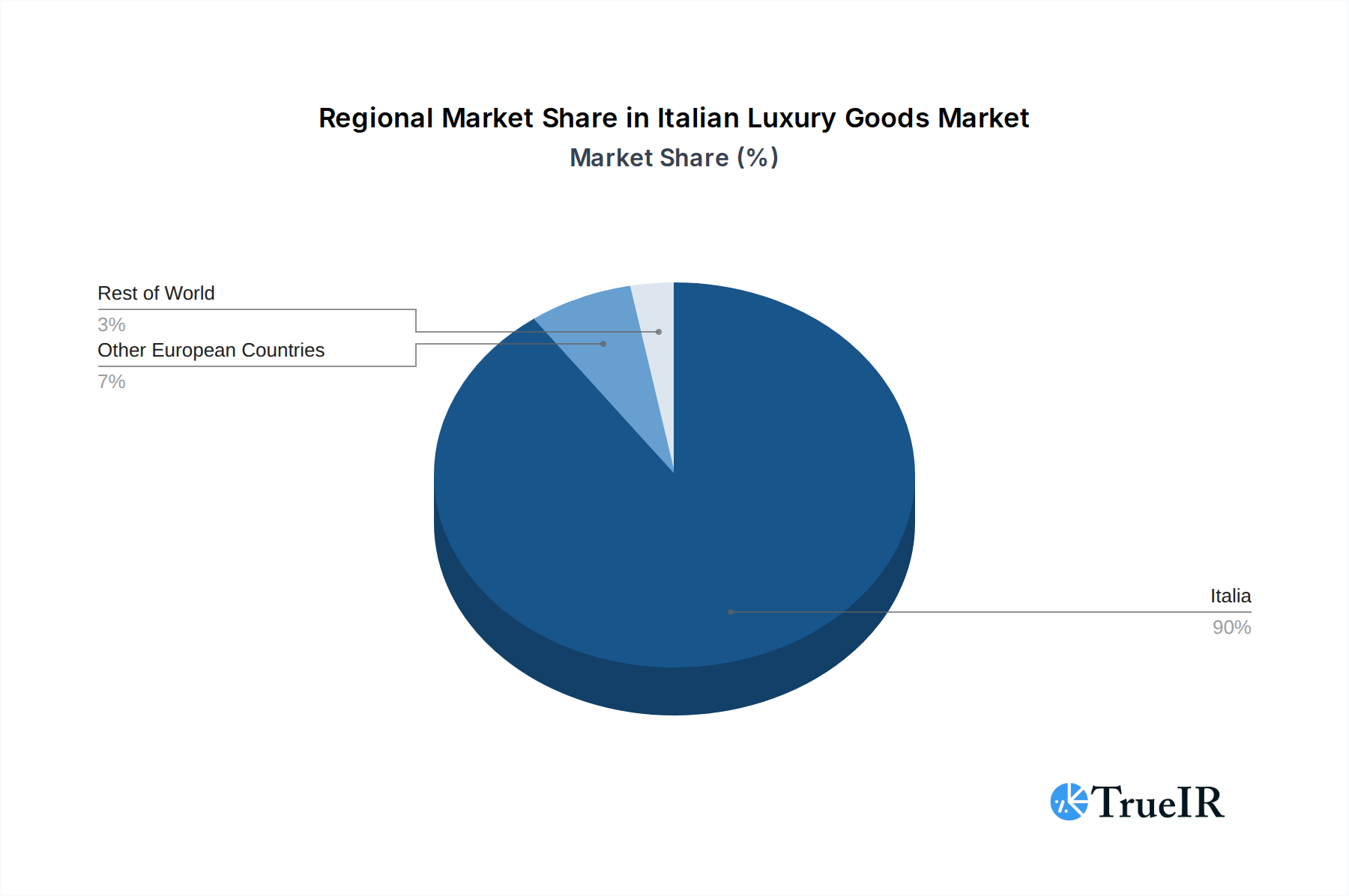

Italian Luxury Goods Market Segmentation By Geography

- 1. Italia

Italian Luxury Goods Market Regional Market Share

Geographic Coverage of Italian Luxury Goods Market

Italian Luxury Goods Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.18% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Clothing and Apparel

- 5.1.2. Footwear

- 5.1.3. Bags

- 5.1.4. Jewelry

- 5.1.5. Watches

- 5.1.6. Other Accessories

- 5.2. Market Analysis, Insights and Forecast - by Distibution Channel

- 5.2.1. Single-brand Stores

- 5.2.2. Multi-brand Stores

- 5.2.3. Online Stores

- 5.2.4. Other Distribution Channels

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Italia

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Italian Luxury Goods Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Clothing and Apparel

- 6.1.2. Footwear

- 6.1.3. Bags

- 6.1.4. Jewelry

- 6.1.5. Watches

- 6.1.6. Other Accessories

- 6.2. Market Analysis, Insights and Forecast - by Distibution Channel

- 6.2.1. Single-brand Stores

- 6.2.2. Multi-brand Stores

- 6.2.3. Online Stores

- 6.2.4. Other Distribution Channels

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 The Estee Lauder Companies Inc

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 KERING

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Prada S p A

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Ralph Lauren Corporation*List Not Exhaustive

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 MAX MARA SRL

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 PVH Corp

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 TAG Heuer International SA

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Ralph Lauren Corporation

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 L'OREAL

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 LVMH Moët Hennessy Louis Vuitton

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 The Estee Lauder Companies Inc

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Italian Luxury Goods Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Italian Luxury Goods Market Share (%) by Company 2025

List of Tables

- Table 1: Italian Luxury Goods Market Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Italian Luxury Goods Market Volume K Units Forecast, by Type 2020 & 2033

- Table 3: Italian Luxury Goods Market Revenue billion Forecast, by Distibution Channel 2020 & 2033

- Table 4: Italian Luxury Goods Market Volume K Units Forecast, by Distibution Channel 2020 & 2033

- Table 5: Italian Luxury Goods Market Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Italian Luxury Goods Market Volume K Units Forecast, by Region 2020 & 2033

- Table 7: Italian Luxury Goods Market Revenue billion Forecast, by Type 2020 & 2033

- Table 8: Italian Luxury Goods Market Volume K Units Forecast, by Type 2020 & 2033

- Table 9: Italian Luxury Goods Market Revenue billion Forecast, by Distibution Channel 2020 & 2033

- Table 10: Italian Luxury Goods Market Volume K Units Forecast, by Distibution Channel 2020 & 2033

- Table 11: Italian Luxury Goods Market Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Italian Luxury Goods Market Volume K Units Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Italian Luxury Goods Market?

The projected CAGR is approximately 3.18%.

2. Which companies are prominent players in the Italian Luxury Goods Market?

Key companies in the market include The Estee Lauder Companies Inc, KERING, Prada S p A, Ralph Lauren Corporation*List Not Exhaustive, MAX MARA SRL, PVH Corp, TAG Heuer International SA, Ralph Lauren Corporation, L'OREAL, LVMH Moët Hennessy Louis Vuitton.

3. What are the main segments of the Italian Luxury Goods Market?

The market segments include Type, Distibution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 5.82 billion as of 2022.

5. What are some drivers contributing to market growth?

Increased Internet Usage and Effortless Shopping Experience; Growing Consumer Inclination Towards Appearance and Latest Fashion.

6. What are the notable trends driving market growth?

Exponentially Growing market of Luxury Leather Goods.

7. Are there any restraints impacting market growth?

Robust Offline Retail Channel Penetration.

8. Can you provide examples of recent developments in the market?

In July 2022, Prada SA unveiled its second Timecapsule NFT collection, a shirt made from upcycled fabric from the Prada archives. The shirt features a 'Jacquard Animalier' silk brocade and lurex fabric in addition to a Jacquard Thrush (flower), which is silk sourced from an early 20th-century French archive.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Units.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Italian Luxury Goods Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Italian Luxury Goods Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Italian Luxury Goods Market?

To stay informed about further developments, trends, and reports in the Italian Luxury Goods Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence