Key Insights

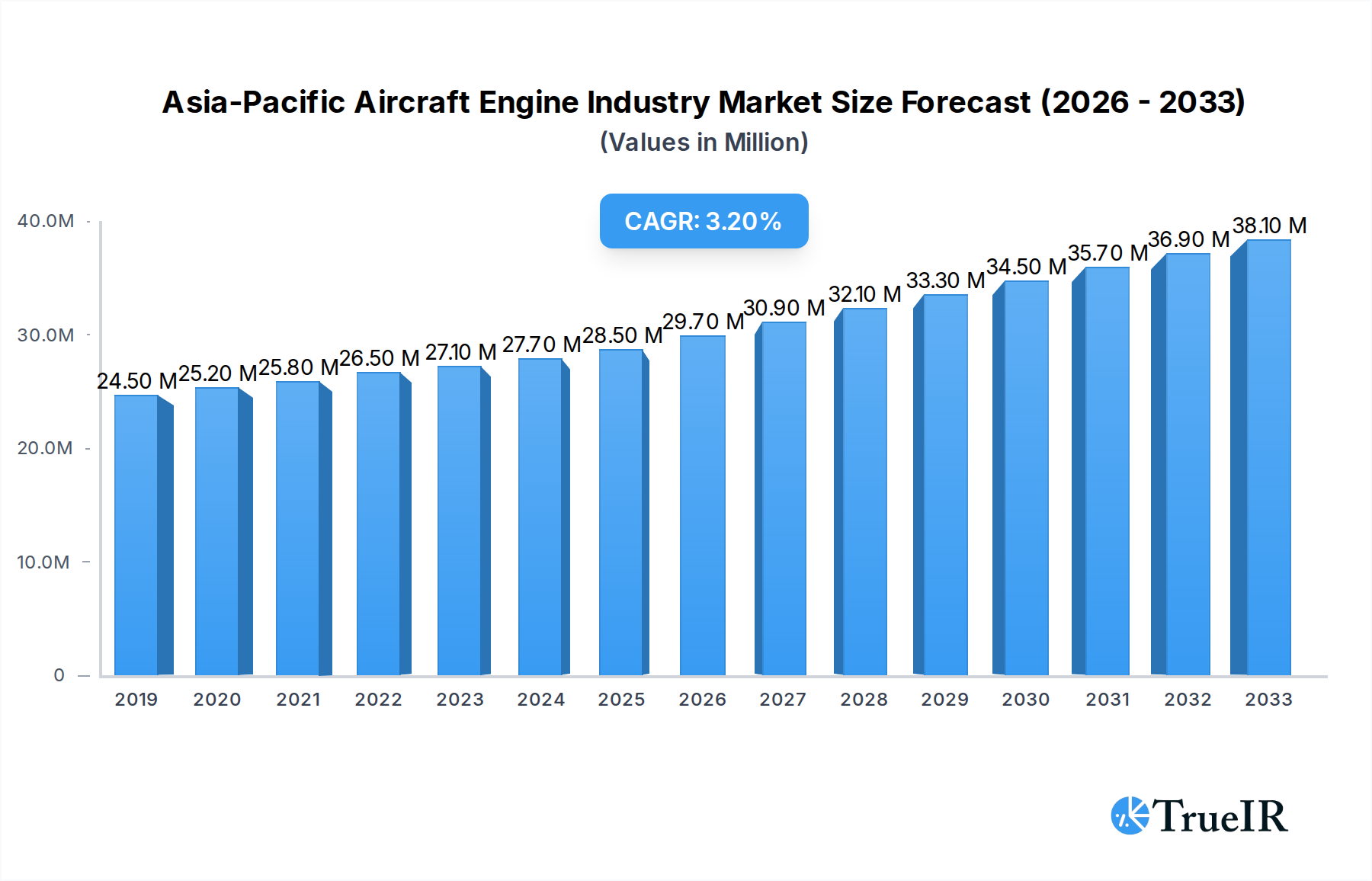

The Asia-Pacific aircraft engine industry is poised for significant expansion, with a current market size of $26.93 million. This growth is fueled by a projected Compound Annual Growth Rate (CAGR) of 4.15% throughout the forecast period of 2025-2033. The sector's trajectory is underpinned by robust demand across its diverse segments, including commercial aviation's increasing passenger and cargo needs, military aviation's ongoing modernization efforts, and the burgeoning general aviation sector. Key drivers include the expanding middle class in emerging economies, leading to a surge in air travel, and substantial government investments in aviation infrastructure and defense. Technological advancements, such as the development of more fuel-efficient and environmentally friendly engine technologies, are also playing a crucial role in shaping market dynamics. The region's strategic importance as a global manufacturing hub further accentuates the growth potential for engine production and maintenance services.

Asia-Pacific Aircraft Engine Industry Market Size (In Million)

Despite this optimistic outlook, the industry faces certain restraints that could temper its growth. These include the high cost of research and development, stringent environmental regulations that necessitate continuous innovation, and geopolitical instabilities that can impact supply chains and demand. However, the industry is actively navigating these challenges through strategic partnerships and a strong focus on sustainable aviation fuel integration and next-generation engine designs. Major players are investing heavily in innovation to meet evolving regulatory standards and consumer preferences for greener air travel. The geographical landscape of the Asia-Pacific region, with its dynamic economies like China and India leading the charge, is expected to contribute significantly to the overall market expansion, driven by a growing fleet size and increasing MRO (Maintenance, Repair, and Overhaul) requirements.

Asia-Pacific Aircraft Engine Industry Company Market Share

This comprehensive report delivers an in-depth analysis of the Asia-Pacific aircraft engine industry, covering market dynamics, competitive landscape, technological advancements, and future growth prospects. Examining the period from 2019 to 2033, with a base year of 2025, this report offers critical insights for stakeholders navigating this rapidly evolving sector. We delve into the intricate interplay of market forces, from dominant players to emerging trends, providing a detailed roadmap for strategic decision-making. This report is essential for industry participants seeking to understand and capitalize on the robust growth potential of the Asia-Pacific aircraft engine market.

Asia-Pacific Aircraft Engine Industry Market Structure & Competitive Landscape

The Asia-Pacific aircraft engine market is characterized by a moderate to high concentration ratio, with a few key global players holding significant market share. Innovation is a primary driver, fueled by substantial R&D investments in fuel efficiency, emissions reduction, and advanced materials. Regulatory frameworks, though varying across nations, are increasingly focused on environmental sustainability and safety standards, influencing product development and market entry. Product substitutes are limited in the high-performance jet engine segment, but advancements in electric and hybrid-electric propulsion systems represent a future threat. End-user segmentation reveals strong demand from Commercial Aviation, followed by Military Aviation, and a growing segment in General Aviation. Mergers & Acquisitions (M&A) activity, while not as frenetic as in some other industries, is strategic, focusing on expanding technological capabilities, market reach, and after-market services. For instance, GE Company's acquisition of CFM International (a joint venture between GE and Safran) has solidified its position. The combined market share of the top three players is estimated to be around 70% in 2025. Investment in new engine technologies is projected to exceed $50 Million annually over the forecast period.

Asia-Pacific Aircraft Engine Industry Market Trends & Opportunities

The Asia-Pacific aircraft engine market is poised for significant expansion, projected to reach a market size exceeding $50,000 Million by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of approximately 6.5% during the forecast period (2025-2033). This growth is underpinned by a resurgence in air travel post-pandemic, coupled with substantial fleet expansion plans by airlines across the region, particularly in China and India. Technological shifts are a defining trend, with a strong emphasis on developing next-generation engines that offer improved fuel efficiency, reduced noise pollution, and lower carbon emissions. Innovations in areas like advanced aerodynamics, lightweight composite materials, and sophisticated control systems are paramount. Consumer preferences are increasingly aligned with sustainability, driving demand for "green" aviation solutions. Competitive dynamics are intensifying, with established global manufacturers vying for market share against emerging regional players and strategic collaborations. The aftermarket services segment, including maintenance, repair, and overhaul (MRO), presents a lucrative opportunity, with an estimated market value of over $15,000 Million by 2033. The increasing integration of digital technologies, such as predictive maintenance and AI-driven diagnostics, further enhances operational efficiency and customer value, creating new avenues for revenue generation. The growing defense procurements in countries like India and South Korea will also significantly contribute to the military aviation engine segment's growth, estimated at a CAGR of 5.8%. The rise of low-cost carriers (LCCs) in the region is also a key driver, demanding cost-effective and reliable engine solutions.

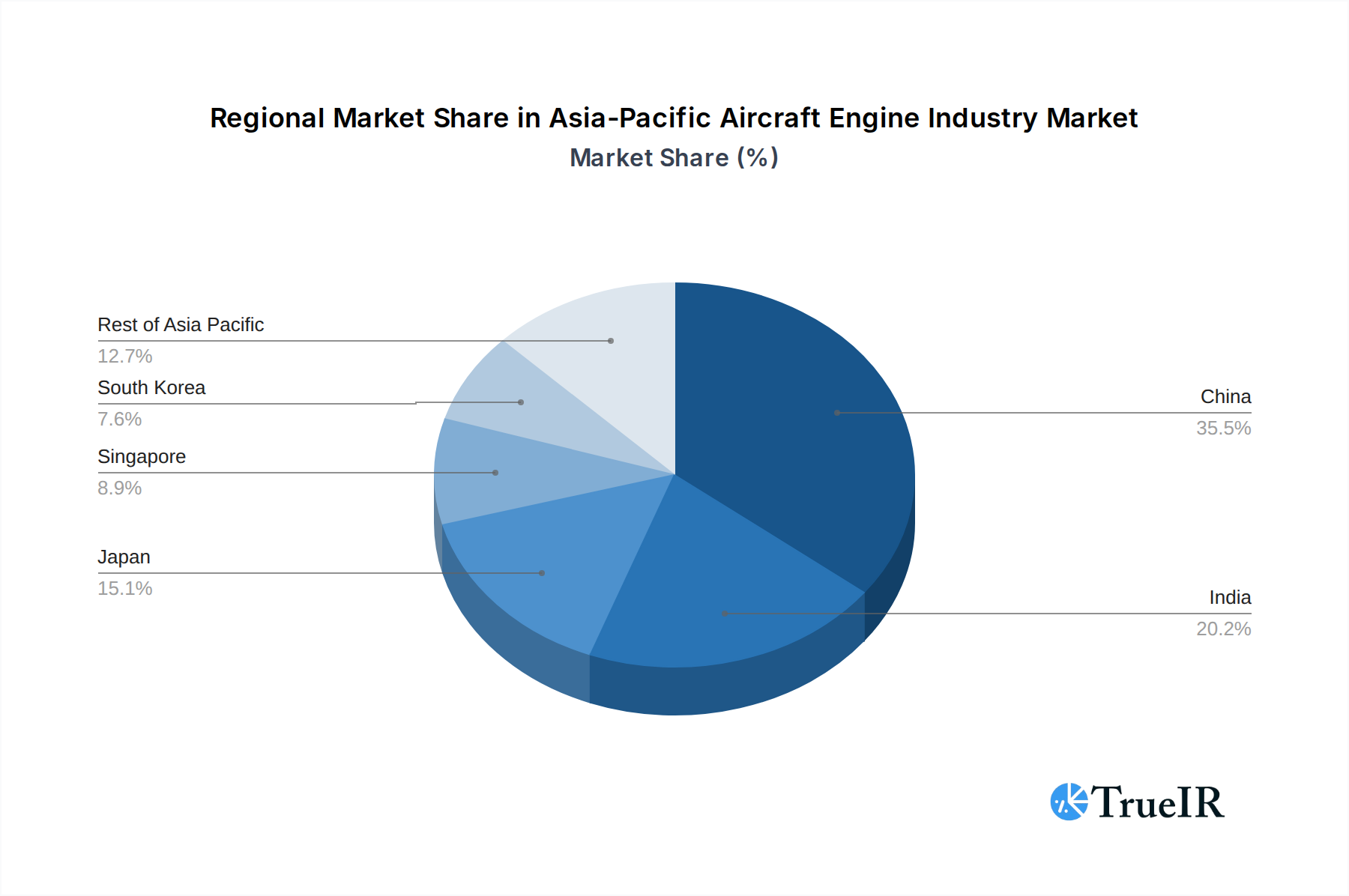

Dominant Markets & Segments in Asia-Pacific Aircraft Engine Industry

China stands out as the dominant market within the Asia-Pacific aircraft engine industry, driven by its massive domestic aviation market and ambitious aerospace manufacturing initiatives. This dominance is fueled by extensive government investment in indigenous aircraft development, such as the COMAC C919, which necessitates a strong domestic engine supply chain. Commercial Aviation is the leading end-user segment, accounting for over 70% of the market share in 2025, propelled by surging passenger traffic and the expansion of airline fleets. The Turbofan engine type is overwhelmingly dominant in this segment, powering the vast majority of commercial aircraft. India's rapidly growing aviation sector and increasing defense modernization efforts position it as the second-fastest-growing market.

Key growth drivers in China include:

- Government Policies: Strong support for domestic aerospace manufacturing and significant R&D funding.

- Infrastructure Development: Expansion of airports and air traffic control systems to accommodate growing air traffic.

- Airline Fleet Expansion: Major airlines ordering hundreds of new aircraft, requiring a commensurate number of engines.

In India, the Military Aviation segment is a significant contributor, with the government prioritizing defense modernization. The Turboprop and Turboshaft engine types find substantial application in this sector, powering various military platforms. Japan’s established aerospace industry, with key players like Ishikawajima Harima Heavy Industries, contributes significantly to the technological advancement and specialized engine manufacturing. Singapore acts as a crucial MRO hub, supporting regional engine maintenance needs. South Korea’s robust defense industry also drives demand for advanced military aircraft engines. The "Rest of Asia-Pacific" region, encompassing Southeast Asian nations and Oceania, presents a fragmented but growing market, with individual countries like Australia and Indonesia showing increasing aviation activity. The increasing demand for regional jets and turboprop aircraft in the less developed parts of the region will boost the Turboprop and Turboshaft segments.

Asia-Pacific Aircraft Engine Industry Product Analysis

The Asia-Pacific aircraft engine industry is witnessing a surge in product innovation centered on enhanced fuel efficiency, reduced emissions, and increased reliability. Turbofan engines, particularly geared turbofans and high-bypass ratio designs, dominate the commercial sector, offering significant fuel savings and lower noise footprints. Advancements in materials science, such as ceramic matrix composites (CMCs) and advanced alloys, enable higher operating temperatures, leading to improved performance. The military segment sees continuous development in combat jet engines, focusing on thrust vectoring and stealth capabilities. Emerging applications include the integration of hybrid-electric and fully electric propulsion systems for smaller aircraft, though widespread adoption is still in its nascent stages. Competitive advantages are derived from superior performance, lower operating costs, and comprehensive after-market support.

Key Drivers, Barriers & Challenges in Asia-Pacific Aircraft Engine Industry

Key Drivers:

- Surging Air Travel Demand: Post-pandemic recovery and growing middle class driving passenger traffic.

- Fleet Modernization & Expansion: Airlines investing in newer, fuel-efficient aircraft.

- Government Support for Aerospace: National initiatives promoting indigenous manufacturing and R&D.

- Technological Advancements: Innovations in engine efficiency, emissions reduction, and materials.

- Defense Spending: Increased military procurement boosting demand for specialized engines.

Barriers & Challenges:

- Supply Chain Disruptions: Geopolitical events and raw material shortages impacting production.

- High R&D Costs: Significant investment required for developing cutting-edge engine technology.

- Stringent Environmental Regulations: Increasing pressure to meet global emissions standards.

- Skilled Workforce Shortage: Demand for highly specialized engineers and technicians.

- Economic Volatility: Fluctuations in global economies can impact airline profitability and aircraft orders.

Growth Drivers in the Asia-Pacific Aircraft Engine Industry Market

The Asia-Pacific aircraft engine industry's growth is predominantly driven by the robust recovery and sustained expansion of air travel across the region. Nations like China and India are witnessing unprecedented increases in passenger numbers, necessitating significant fleet growth and, consequently, engine procurement. Government initiatives promoting domestic aerospace manufacturing, such as India's "Make in India" policy and China's aviation industrial strategy, are fostering local capabilities and attracting investment. Technological advancements, particularly in enhancing fuel efficiency and reducing carbon emissions, are crucial growth catalysts, aligning with global sustainability goals and enabling airlines to optimize operational costs. The increasing defense budgets in several Asia-Pacific countries are also a significant driver, fueling demand for advanced military aircraft engines.

Challenges Impacting Asia-Pacific Aircraft Engine Industry Growth

Despite the strong growth trajectory, the Asia-Pacific aircraft engine industry faces considerable challenges. Global supply chain vulnerabilities, exacerbated by geopolitical tensions and trade disputes, pose a significant risk to timely production and component availability, impacting lead times and costs, potentially by 10-15%. The development of advanced engine technologies requires substantial and sustained R&D investment, which can be a barrier for smaller players. Increasingly stringent environmental regulations worldwide necessitate continuous innovation to meet emissions targets, adding to development costs. The shortage of highly skilled engineers and technicians across the aerospace sector presents a persistent challenge in meeting the growing demand for specialized expertise in design, manufacturing, and MRO.

Key Players Shaping the Asia-Pacific Aircraft Engine Industry Market

- Tata Advanced Systems Limited (Tata Sons Private Limited)

- Safran

- Rolls-Royce pl

- CFM International

- Aero Engine Corporation Of China

- MTU Aero Engines AG

- Ishikawajima Harima Heavy Industries Co Limited

- JSC UEC-Aviadvigatel

- Thompson Aero Seating Limited

- General Electric Company

- Pratt and Whitney (RTX Corporation)

- Hindustan Aeronautics Limited

Significant Asia-Pacific Aircraft Engine Industry Industry Milestones

- February 2023: Air India placed a definitive order for 40 GEnx-1B and 20 GE9X engines and a multi-year TrueChoice engine services agreement with GE Company. This significant order underscored a major commitment to fleet modernization and reliable engine support.

- June 2022: ST Engineering announced that their Commercial Aerospace business signed a five-year agreement with Safran Aircraft Engines, a world-leading aerospace engine manufacturer, for ST Engineering to provide engine maintenance (shop visit) offload for the CFM56-5B and -7B engines. This multi-year agreement was expected to allow ST Engineering and Safran Aircraft Engines to meet the forecasted rise of engine MRO activities as air travel gradually recovered from the pandemic, highlighting the growing importance of the aftermarket services sector.

Future Outlook for Asia-Pacific Aircraft Engine Industry Market

The future outlook for the Asia-Pacific aircraft engine industry is exceptionally robust, propelled by continued strong demand for air travel and ongoing fleet modernization initiatives. Strategic opportunities lie in the development of sustainable aviation fuels (SAFs) compatible engines and further advancements in hybrid-electric and electric propulsion systems for regional and general aviation. The increasing focus on localized manufacturing and MRO capabilities within key Asia-Pacific nations will create new avenues for growth and partnerships. Investments in advanced manufacturing technologies, such as additive manufacturing, are expected to streamline production and reduce costs. The expanding defense sector will continue to fuel demand for sophisticated military-grade engines. Overall, the market is poised for sustained growth, driven by innovation, expanding fleets, and a commitment to environmental sustainability.

Asia-Pacific Aircraft Engine Industry Segmentation

-

1. Engine Type

- 1.1. Turbofan

- 1.2. Turboprop

- 1.3. Turboshaft

- 1.4. Piston

-

2. End User

- 2.1. Commercial Aviation

- 2.2. Military Aviation

- 2.3. General Aviation

-

3. Geography

- 3.1. China

- 3.2. India

- 3.3. Japan

- 3.4. Singapore

- 3.5. South Korea

- 3.6. Rest of Asia-Pacific

Asia-Pacific Aircraft Engine Industry Segmentation By Geography

- 1. China

- 2. India

- 3. Japan

- 4. Singapore

- 5. South Korea

- 6. Rest of Asia Pacific

Asia-Pacific Aircraft Engine Industry Regional Market Share

Geographic Coverage of Asia-Pacific Aircraft Engine Industry

Asia-Pacific Aircraft Engine Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.15% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Engine Type

- 5.1.1. Turbofan

- 5.1.2. Turboprop

- 5.1.3. Turboshaft

- 5.1.4. Piston

- 5.2. Market Analysis, Insights and Forecast - by End User

- 5.2.1. Commercial Aviation

- 5.2.2. Military Aviation

- 5.2.3. General Aviation

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. China

- 5.3.2. India

- 5.3.3. Japan

- 5.3.4. Singapore

- 5.3.5. South Korea

- 5.3.6. Rest of Asia-Pacific

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. China

- 5.4.2. India

- 5.4.3. Japan

- 5.4.4. Singapore

- 5.4.5. South Korea

- 5.4.6. Rest of Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Engine Type

- 6. Asia-Pacific Aircraft Engine Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Engine Type

- 6.1.1. Turbofan

- 6.1.2. Turboprop

- 6.1.3. Turboshaft

- 6.1.4. Piston

- 6.2. Market Analysis, Insights and Forecast - by End User

- 6.2.1. Commercial Aviation

- 6.2.2. Military Aviation

- 6.2.3. General Aviation

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. China

- 6.3.2. India

- 6.3.3. Japan

- 6.3.4. Singapore

- 6.3.5. South Korea

- 6.3.6. Rest of Asia-Pacific

- 6.1. Market Analysis, Insights and Forecast - by Engine Type

- 7. China Asia-Pacific Aircraft Engine Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Engine Type

- 7.1.1. Turbofan

- 7.1.2. Turboprop

- 7.1.3. Turboshaft

- 7.1.4. Piston

- 7.2. Market Analysis, Insights and Forecast - by End User

- 7.2.1. Commercial Aviation

- 7.2.2. Military Aviation

- 7.2.3. General Aviation

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. China

- 7.3.2. India

- 7.3.3. Japan

- 7.3.4. Singapore

- 7.3.5. South Korea

- 7.3.6. Rest of Asia-Pacific

- 7.1. Market Analysis, Insights and Forecast - by Engine Type

- 8. India Asia-Pacific Aircraft Engine Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Engine Type

- 8.1.1. Turbofan

- 8.1.2. Turboprop

- 8.1.3. Turboshaft

- 8.1.4. Piston

- 8.2. Market Analysis, Insights and Forecast - by End User

- 8.2.1. Commercial Aviation

- 8.2.2. Military Aviation

- 8.2.3. General Aviation

- 8.3. Market Analysis, Insights and Forecast - by Geography

- 8.3.1. China

- 8.3.2. India

- 8.3.3. Japan

- 8.3.4. Singapore

- 8.3.5. South Korea

- 8.3.6. Rest of Asia-Pacific

- 8.1. Market Analysis, Insights and Forecast - by Engine Type

- 9. Japan Asia-Pacific Aircraft Engine Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Engine Type

- 9.1.1. Turbofan

- 9.1.2. Turboprop

- 9.1.3. Turboshaft

- 9.1.4. Piston

- 9.2. Market Analysis, Insights and Forecast - by End User

- 9.2.1. Commercial Aviation

- 9.2.2. Military Aviation

- 9.2.3. General Aviation

- 9.3. Market Analysis, Insights and Forecast - by Geography

- 9.3.1. China

- 9.3.2. India

- 9.3.3. Japan

- 9.3.4. Singapore

- 9.3.5. South Korea

- 9.3.6. Rest of Asia-Pacific

- 9.1. Market Analysis, Insights and Forecast - by Engine Type

- 10. Singapore Asia-Pacific Aircraft Engine Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Engine Type

- 10.1.1. Turbofan

- 10.1.2. Turboprop

- 10.1.3. Turboshaft

- 10.1.4. Piston

- 10.2. Market Analysis, Insights and Forecast - by End User

- 10.2.1. Commercial Aviation

- 10.2.2. Military Aviation

- 10.2.3. General Aviation

- 10.3. Market Analysis, Insights and Forecast - by Geography

- 10.3.1. China

- 10.3.2. India

- 10.3.3. Japan

- 10.3.4. Singapore

- 10.3.5. South Korea

- 10.3.6. Rest of Asia-Pacific

- 10.1. Market Analysis, Insights and Forecast - by Engine Type

- 11. South Korea Asia-Pacific Aircraft Engine Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Engine Type

- 11.1.1. Turbofan

- 11.1.2. Turboprop

- 11.1.3. Turboshaft

- 11.1.4. Piston

- 11.2. Market Analysis, Insights and Forecast - by End User

- 11.2.1. Commercial Aviation

- 11.2.2. Military Aviation

- 11.2.3. General Aviation

- 11.3. Market Analysis, Insights and Forecast - by Geography

- 11.3.1. China

- 11.3.2. India

- 11.3.3. Japan

- 11.3.4. Singapore

- 11.3.5. South Korea

- 11.3.6. Rest of Asia-Pacific

- 11.1. Market Analysis, Insights and Forecast - by Engine Type

- 12. Rest of Asia Pacific Asia-Pacific Aircraft Engine Industry Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Engine Type

- 12.1.1. Turbofan

- 12.1.2. Turboprop

- 12.1.3. Turboshaft

- 12.1.4. Piston

- 12.2. Market Analysis, Insights and Forecast - by End User

- 12.2.1. Commercial Aviation

- 12.2.2. Military Aviation

- 12.2.3. General Aviation

- 12.3. Market Analysis, Insights and Forecast - by Geography

- 12.3.1. China

- 12.3.2. India

- 12.3.3. Japan

- 12.3.4. Singapore

- 12.3.5. South Korea

- 12.3.6. Rest of Asia-Pacific

- 12.1. Market Analysis, Insights and Forecast - by Engine Type

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 Tata Advanced Systems Limited (Tata Sons Private Limited)

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 Safran

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 Rolls-Royce pl

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 CFM International

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 Aero Engine Corporation Of China

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 MTU Aero Engines AG

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 Ishikawajima Harima Heavy Industries Co Limited

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 JSC UEC-Aviadvigatel

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.9 Thompson Aero Seating Limited

- 13.1.9.1. Company Overview

- 13.1.9.2. Products

- 13.1.9.3. Company Financials

- 13.1.9.4. SWOT Analysis

- 13.1.10 General Electric Company

- 13.1.10.1. Company Overview

- 13.1.10.2. Products

- 13.1.10.3. Company Financials

- 13.1.10.4. SWOT Analysis

- 13.1.11 Pratt and Whitney (RTX Corporation)

- 13.1.11.1. Company Overview

- 13.1.11.2. Products

- 13.1.11.3. Company Financials

- 13.1.11.4. SWOT Analysis

- 13.1.12 Hindustan Aeronautics Limited

- 13.1.12.1. Company Overview

- 13.1.12.2. Products

- 13.1.12.3. Company Financials

- 13.1.12.4. SWOT Analysis

- 13.1.1 Tata Advanced Systems Limited (Tata Sons Private Limited)

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Asia-Pacific Aircraft Engine Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Asia-Pacific Aircraft Engine Industry Share (%) by Company 2025

List of Tables

- Table 1: Asia-Pacific Aircraft Engine Industry Revenue Million Forecast, by Engine Type 2020 & 2033

- Table 2: Asia-Pacific Aircraft Engine Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 3: Asia-Pacific Aircraft Engine Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 4: Asia-Pacific Aircraft Engine Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Asia-Pacific Aircraft Engine Industry Revenue Million Forecast, by Engine Type 2020 & 2033

- Table 6: Asia-Pacific Aircraft Engine Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 7: Asia-Pacific Aircraft Engine Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 8: Asia-Pacific Aircraft Engine Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: Asia-Pacific Aircraft Engine Industry Revenue Million Forecast, by Engine Type 2020 & 2033

- Table 10: Asia-Pacific Aircraft Engine Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 11: Asia-Pacific Aircraft Engine Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 12: Asia-Pacific Aircraft Engine Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Asia-Pacific Aircraft Engine Industry Revenue Million Forecast, by Engine Type 2020 & 2033

- Table 14: Asia-Pacific Aircraft Engine Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 15: Asia-Pacific Aircraft Engine Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 16: Asia-Pacific Aircraft Engine Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 17: Asia-Pacific Aircraft Engine Industry Revenue Million Forecast, by Engine Type 2020 & 2033

- Table 18: Asia-Pacific Aircraft Engine Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 19: Asia-Pacific Aircraft Engine Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 20: Asia-Pacific Aircraft Engine Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 21: Asia-Pacific Aircraft Engine Industry Revenue Million Forecast, by Engine Type 2020 & 2033

- Table 22: Asia-Pacific Aircraft Engine Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 23: Asia-Pacific Aircraft Engine Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 24: Asia-Pacific Aircraft Engine Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 25: Asia-Pacific Aircraft Engine Industry Revenue Million Forecast, by Engine Type 2020 & 2033

- Table 26: Asia-Pacific Aircraft Engine Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 27: Asia-Pacific Aircraft Engine Industry Revenue Million Forecast, by Geography 2020 & 2033

- Table 28: Asia-Pacific Aircraft Engine Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Asia-Pacific Aircraft Engine Industry?

The projected CAGR is approximately 4.15%.

2. Which companies are prominent players in the Asia-Pacific Aircraft Engine Industry?

Key companies in the market include Tata Advanced Systems Limited (Tata Sons Private Limited), Safran, Rolls-Royce pl, CFM International, Aero Engine Corporation Of China, MTU Aero Engines AG, Ishikawajima Harima Heavy Industries Co Limited, JSC UEC-Aviadvigatel, Thompson Aero Seating Limited, General Electric Company, Pratt and Whitney (RTX Corporation), Hindustan Aeronautics Limited.

3. What are the main segments of the Asia-Pacific Aircraft Engine Industry?

The market segments include Engine Type, End User, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 26.93 Million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Turbofan Engine is expected to Dominate the Market during the Forecasted Period.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

February 2023: Air India placed a definitive order for 40 GEnx-1B and 20 GE9X engines and a multi-year TrueChoice engine services agreement with GE Company.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Asia-Pacific Aircraft Engine Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Asia-Pacific Aircraft Engine Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Asia-Pacific Aircraft Engine Industry?

To stay informed about further developments, trends, and reports in the Asia-Pacific Aircraft Engine Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence