Key Insights

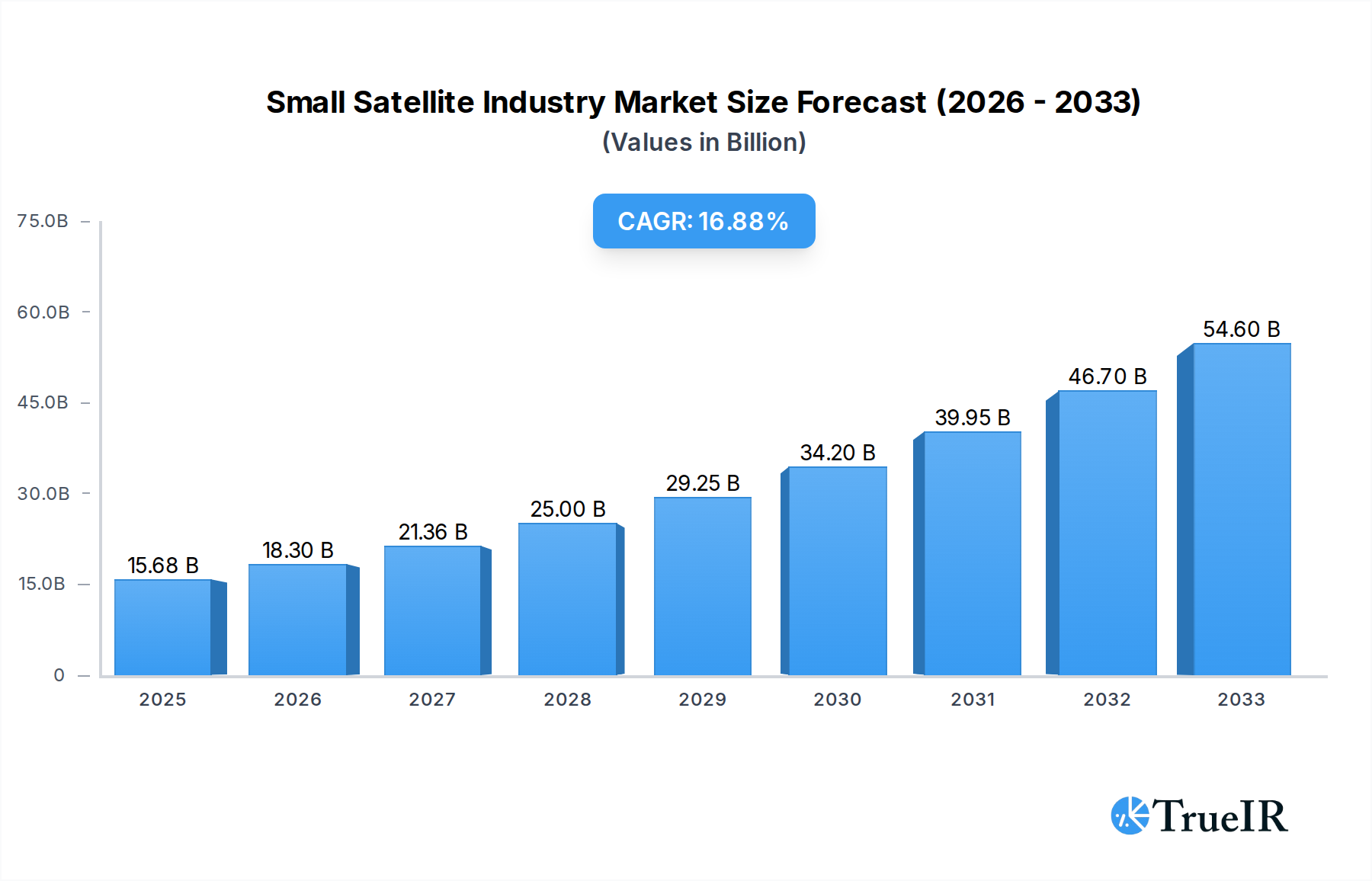

The small satellite market is poised for remarkable expansion, projected to reach USD 15.68 billion in 2025 and grow at a robust CAGR of 16.9% through 2033. This surge is primarily fueled by an escalating demand for cost-effective and agile space solutions across various applications. Communication, particularly for remote and underserved areas, is a major driver, with constellations of small satellites enabling global connectivity. Earth observation is another significant growth catalyst, offering enhanced capabilities for environmental monitoring, disaster management, and resource assessment. The increasing deployment of small satellites in Low Earth Orbit (LEO) is a key trend, facilitating faster data acquisition and reduced latency, which is critical for navigation and real-time applications. The trend towards miniaturization and standardization of satellite components further lowers the barrier to entry, encouraging more players to enter the market. This dynamic landscape is characterized by rapid innovation in propulsion technologies, with electric and gas-based systems gaining traction due to their efficiency and reduced propellant requirements, aligning with the economic and environmental considerations of small satellite missions.

Small Satellite Industry Market Size (In Billion)

The market's rapid growth is supported by substantial investments in space technology and an expanding ecosystem of satellite manufacturers and service providers. Companies like SpaceX, Airbus, and China Aerospace Science and Technology Corporation are at the forefront, developing advanced small satellite platforms and launch capabilities. The increasing participation of commercial entities, alongside military and government agencies, underscores the versatility and growing utility of small satellites. Restraints such as the increasing complexity of regulatory frameworks and the challenges associated with space debris management are being addressed through international cooperation and technological advancements. The market is segmented by orbit class (LEO being dominant), end-user (commercial and military), and propulsion technology, with electric propulsion emerging as a key area of development. Geographically, North America and Asia Pacific are expected to lead market growth, driven by strong governmental initiatives and a burgeoning private space sector.

Small Satellite Industry Company Market Share

This comprehensive report dives deep into the small satellite industry, a rapidly expanding sector projected to reach multi-billion dollar valuations by 2033. Leveraging extensive data from 2019–2024, the analysis meticulously forecasts growth through 2025–2033, with a base year and estimated year of 2025. We provide granular insights into market structure, key trends, dominant segments, product innovations, and the driving forces and challenges shaping this dynamic landscape. Essential for stakeholders seeking to navigate the complexities of small satellite constellations, nano-satellites, and micro-satellites, this report offers actionable intelligence on market penetration rates, technological advancements, and competitive strategies.

Small Satellite Industry Market Structure & Competitive Landscape

The small satellite industry is characterized by a dynamic and evolving market structure, marked by increasing fragmentation yet significant strategic consolidation. Innovation drivers are paramount, fueled by advancements in miniaturization, propulsion systems like electric and gas-based technologies, and the demand for cost-effective satellite communication and earth observation. Regulatory frameworks, while evolving, continue to influence launch capabilities and spectrum allocation. Product substitutes are emerging, particularly in terrestrial communication networks, but the unique capabilities of small satellites in providing global coverage and rapid deployment maintain their competitive edge.

End-user segmentation reveals a strong shift towards commercial applications, driven by a burgeoning demand for data-intensive services and the proliferation of small satellite constellations. The military & government sector also represents a significant and growing segment, leveraging small satellites for intelligence, surveillance, and reconnaissance (ISR). Mergers and acquisitions (M&A) are becoming increasingly prevalent as larger entities seek to integrate small satellite capabilities and smaller, innovative companies aim for scalability. For instance, recent years have witnessed several key acquisitions aimed at bolstering constellations for earth observation and communication. Concentration ratios, while varying across sub-segments, indicate a trend towards larger players consolidating market share in specific application areas.

Small Satellite Industry Market Trends & Opportunities

The global small satellite industry is experiencing an unprecedented surge in growth, projected to expand at a robust Compound Annual Growth Rate (CAGR) of approximately 15-20% over the forecast period of 2025–2033. This expansion is driven by a confluence of factors, including the declining cost of launch services, advancements in satellite technology enabling smaller and more capable payloads, and an insatiable demand for data across various sectors. The market size, which stood at billions in the historical period, is set to multiply significantly, with projections indicating a multi-billion dollar industry by the end of the forecast period.

Technological shifts are at the forefront of this growth. The miniaturization of components has led to the development of nano-satellites and pico-satellites, making space access more democratized. Innovations in electric propulsion and advanced power systems are enhancing satellite lifespan and maneuverability, enabling more complex missions. Furthermore, the rise of Software-Defined Satellites (SDS) allows for in-orbit reconfigurability, increasing mission flexibility and data utility.

Consumer preferences are increasingly leaning towards real-time data delivery and specialized services. This is particularly evident in the earth observation segment, where industries like agriculture, disaster management, and environmental monitoring are leveraging high-resolution imagery and analytics. In the communication sector, the demand for global broadband connectivity, especially in underserved regions, is a major catalyst, driving the deployment of vast small satellite constellations.

Competitive dynamics are intensifying. Established aerospace giants are actively investing in or acquiring small satellite companies to broaden their portfolios, while a new generation of agile startups is disrupting the market with innovative business models and specialized offerings. Companies like Space Exploration Technologies Corp (SpaceX), Planet Labs Inc, and Satellogic are at the forefront of this transformation, deploying large constellations and offering integrated data solutions. Market penetration rates for small satellite services are rapidly increasing across various end-user segments, from commercial enterprises to governmental agencies, signaling a profound shift in how data is acquired and utilized from space. The opportunities lie in catering to niche markets, developing advanced data analytics capabilities, and providing end-to-end space solutions.

Dominant Markets & Segments in Small Satellite Industry

The small satellite industry is witnessing dominant growth across several key markets and segments, driven by specific technological advancements, evolving policy landscapes, and increasing end-user adoption.

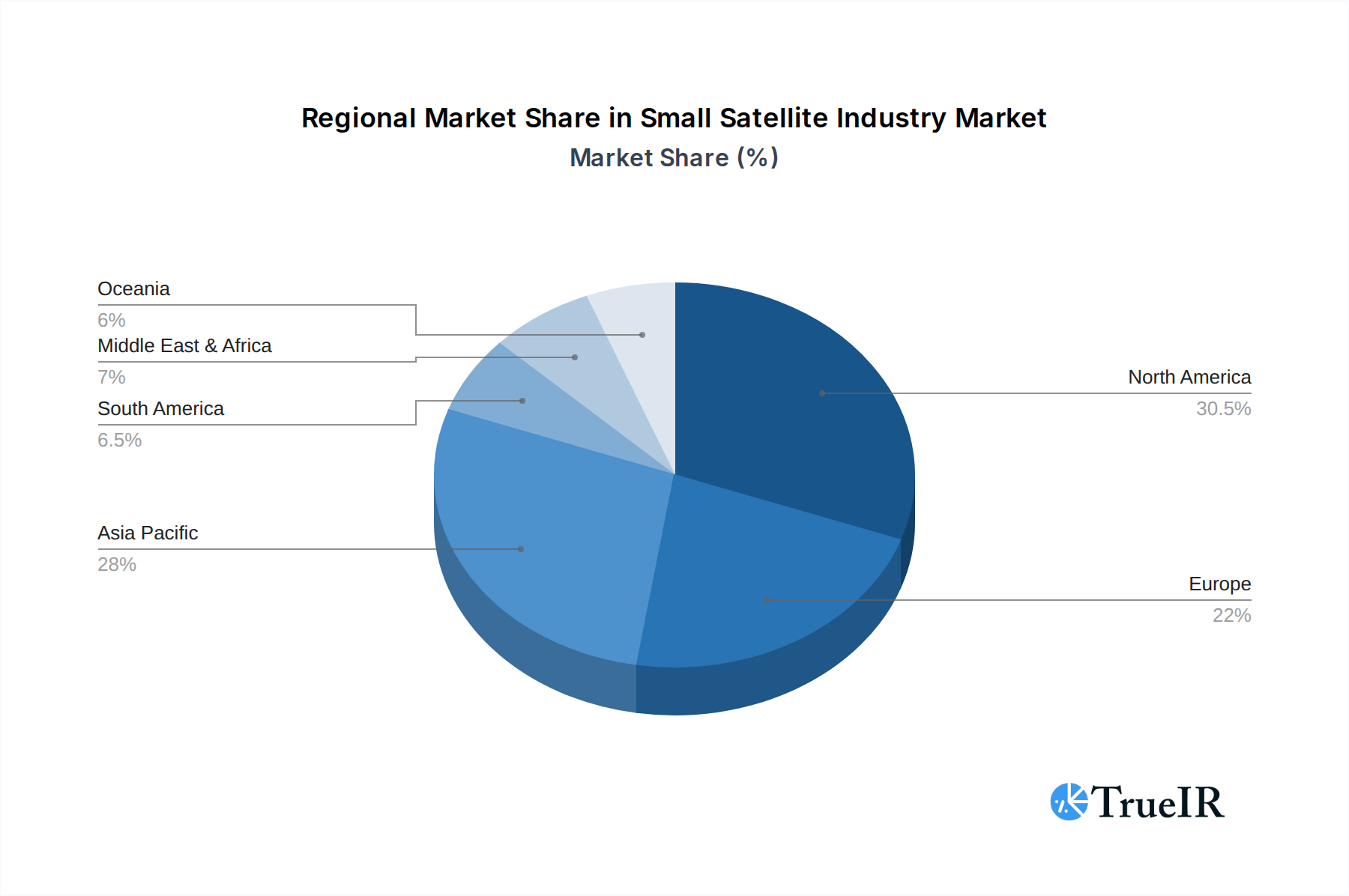

Leading Region: North America currently leads the small satellite market, fueled by robust government investment, a thriving commercial space ecosystem, and pioneering companies. The United States, in particular, benefits from a strong research and development base, a well-established launch infrastructure, and significant demand from both commercial and defense sectors. European countries are also showing substantial growth, with Germany and the UK investing heavily in their domestic space capabilities and research initiatives. Asia-Pacific is emerging as a rapid growth region, particularly China, with its ambitious space programs and increasing commercial ventures.

Application Dominance:

- Earth Observation: This segment is a major growth driver. The demand for high-resolution, frequent imagery for applications such as precision agriculture, environmental monitoring, urban planning, disaster response, and commodity trading is immense. Companies like ICEYE Ltd and Planet Labs Inc are at the forefront, offering sophisticated synthetic-aperture radar (SAR) and optical imaging capabilities.

- Communication: Driven by the need for global broadband, IoT connectivity, and specialized data relay services, the communication segment is experiencing rapid expansion. The deployment of large small satellite constellations by companies like Swarm Technologies Inc and Spire Global Inc is transforming connectivity paradigms.

Orbit Class Dominance:

- Low Earth Orbit (LEO): This orbit class is overwhelmingly dominant for small satellites. LEO offers advantages such as lower launch costs, reduced latency for communication services, and optimal conditions for earth observation due to its proximity to Earth. The vast majority of small satellite constellations are deployed in LEO.

End User Dominance:

- Commercial: The commercial sector is the largest and fastest-growing end-user segment. Businesses across various industries are leveraging small satellite data and services for competitive advantage, operational efficiency, and new revenue streams. This includes sectors like agriculture, logistics, insurance, and telecommunications.

- Military & Government: This segment is a critical consumer of small satellite technology, utilizing them for intelligence, surveillance, reconnaissance (ISR), secure communications, and situational awareness. Government agencies and defense organizations are increasingly adopting small satellites for their cost-effectiveness and rapid deployment capabilities.

Propulsion Tech Trends:

- Electric Propulsion: This technology is gaining significant traction due to its high specific impulse, enabling more efficient orbital maneuvers and station-keeping, thereby extending satellite lifespan and reducing fuel mass. Companies are investing in advanced electric propulsion systems for their small satellite constellations.

- Gas-based Propulsion: Continued use for specific applications requiring simpler and more cost-effective thrust.

The dominance of these segments is further reinforced by favorable policies, ongoing technological innovation in areas like AI-powered data analytics and advanced miniaturization, and substantial investments from both private and public entities.

Small Satellite Industry Product Analysis

Product innovations in the small satellite industry are primarily focused on enhanced miniaturization, increased payload capabilities, and greater operational autonomy. Companies are developing satellites with advanced sensors for higher-resolution earth observation, more efficient communication transponders for global connectivity, and sophisticated software for in-orbit data processing. Competitive advantages are derived from rapid deployment cycles, cost-effectiveness compared to traditional large satellites, and the ability to deploy large constellations for comprehensive coverage. Technological advancements in electric propulsion and advanced power management are extending satellite lifespans and mission capabilities, making them more attractive for a wider range of applications, from scientific research to commercial data services.

Key Drivers, Barriers & Challenges in Small Satellite Industry

Key Drivers: The small satellite industry is propelled by several key factors. Technologically, the miniaturization of components, advancements in digital technologies, and more efficient propulsion systems like electric propulsion are crucial. Economically, declining launch costs, increased venture capital investment, and the demand for cost-effective data solutions are major drivers. Policy-driven factors, such as government initiatives supporting commercial space activities and the increasing utilization of small satellites for national security, also play a significant role.

Key Barriers & Challenges:

- Regulatory Hurdles: Navigating complex and evolving regulations for launch, orbital debris mitigation, and spectrum allocation presents a significant challenge.

- Supply Chain Issues: The reliance on specialized components and potential disruptions in the supply chain can impact production timelines and costs. Quantifiable impacts include potential delays in constellation deployment and increased manufacturing expenses.

- Competitive Pressures: The rapidly growing number of market players intensifies competition, requiring continuous innovation and cost optimization. This can lead to price erosion in certain market segments.

- Orbital Congestion and Debris: The proliferation of satellites raises concerns about orbital congestion and the increasing risk of collisions, demanding robust debris mitigation strategies.

Growth Drivers in the Small Satellite Industry Market

The small satellite industry market is experiencing robust growth driven by several interconnected factors. Technologically, the continuous miniaturization of satellite components, coupled with advancements in electric and gas-based propulsion systems, enables more cost-effective and capable missions. Economically, the significant reduction in launch costs, particularly through reusable rocket technology, has democratized space access. This has spurred a surge in demand for earth observation data, global communication services, and specialized space observation applications, creating new revenue streams. Regulatory support, including favorable licensing processes and government contracts for both commercial and defense purposes, further accelerates market expansion. The increasing adoption by commercial entities for applications ranging from precision agriculture to IoT networks is a major economic catalyst.

Challenges Impacting Small Satellite Industry Growth

Despite its rapid expansion, the small satellite industry faces notable challenges that impact its growth trajectory. Regulatory complexities surrounding orbital slot allocation, spectrum licensing, and international space law can create significant hurdles for deployment and operation. Supply chain issues, particularly for specialized electronic components and advanced materials, can lead to production delays and increased costs. Quantifiable impacts include extended lead times for satellite manufacturing and potential cost overruns. Competitive pressures are intensifying as new players enter the market, leading to potential price wars and margin compression. Furthermore, the growing concern over orbital debris and the need for robust space traffic management systems require significant investment and international cooperation, posing a long-term challenge to sustainable growth.

Key Players Shaping the Small Satellite Industry Market

- Space Exploration Technologies Corp

- German Orbital Systems

- GomSpace ApS

- Swarm Technologies Inc

- SpaceQuest Ltd

- Airbus SE

- Axelspace Corporation

- Astrocast

- China Aerospace Science and Technology Corporation (CASC)

- ICEYE Ltd

- Chang Guang Satellite Technology Co Ltd

- Satellogic

- Thale

- Planet Labs Inc

- Spire Global Inc

Significant Small Satellite Industry Industry Milestones

- June 2022: Falcon 9 launched Globalstar FM15 to low-Earth orbit from Space Launch Complex 40 (SLC-40) at Cape Canaveral Space Force Station in Florida. This launch highlighted the increasing reliability and capacity of commercial launch providers for small satellite missions.

- May 2022: As part of the Transporter-5 mission another five satellites namely ICEYE-X17, -X18, -X19, -X20 and -X24 were launched. This demonstrates the efficiency of rideshare missions and the continued deployment of satellite constellations for Earth observation.

- April 2022: Swarm Technologies 12 'picosatellites' on the Transporter 4 mission for low-data-rate communications network have been launched. This event underscores the growing demand for IoT connectivity solutions enabled by ultra-small satellites.

Future Outlook for Small Satellite Industry Market

The future outlook for the small satellite industry is exceptionally bright, with significant growth catalysts expected to drive further expansion. The increasing demand for real-time data analytics, the continued proliferation of constellations for earth observation and communication, and advancements in on-orbit servicing and in-space manufacturing represent substantial market opportunities. Strategic partnerships between established aerospace companies and innovative startups will likely shape the competitive landscape. Furthermore, the growing integration of AI and machine learning with satellite data processing will unlock new applications and create higher value-added services. The market is poised for continued innovation, leading to more capable, cost-effective, and widespread utilization of small satellites across diverse sectors globally.

Small Satellite Industry Segmentation

-

1. Application

- 1.1. Communication

- 1.2. Earth Observation

- 1.3. Navigation

- 1.4. Space Observation

- 1.5. Others

-

2. Orbit Class

- 2.1. GEO

- 2.2. LEO

- 2.3. MEO

-

3. End User

- 3.1. Commercial

- 3.2. Military & Government

- 3.3. Other

-

4. Propulsion Tech

- 4.1. Electric

- 4.2. Gas based

- 4.3. Liquid Fuel

Small Satellite Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Small Satellite Industry Regional Market Share

Geographic Coverage of Small Satellite Industry

Small Satellite Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Communication

- 5.1.2. Earth Observation

- 5.1.3. Navigation

- 5.1.4. Space Observation

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Orbit Class

- 5.2.1. GEO

- 5.2.2. LEO

- 5.2.3. MEO

- 5.3. Market Analysis, Insights and Forecast - by End User

- 5.3.1. Commercial

- 5.3.2. Military & Government

- 5.3.3. Other

- 5.4. Market Analysis, Insights and Forecast - by Propulsion Tech

- 5.4.1. Electric

- 5.4.2. Gas based

- 5.4.3. Liquid Fuel

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. North America

- 5.5.2. South America

- 5.5.3. Europe

- 5.5.4. Middle East & Africa

- 5.5.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Small Satellite Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Communication

- 6.1.2. Earth Observation

- 6.1.3. Navigation

- 6.1.4. Space Observation

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Orbit Class

- 6.2.1. GEO

- 6.2.2. LEO

- 6.2.3. MEO

- 6.3. Market Analysis, Insights and Forecast - by End User

- 6.3.1. Commercial

- 6.3.2. Military & Government

- 6.3.3. Other

- 6.4. Market Analysis, Insights and Forecast - by Propulsion Tech

- 6.4.1. Electric

- 6.4.2. Gas based

- 6.4.3. Liquid Fuel

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Small Satellite Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Communication

- 7.1.2. Earth Observation

- 7.1.3. Navigation

- 7.1.4. Space Observation

- 7.1.5. Others

- 7.2. Market Analysis, Insights and Forecast - by Orbit Class

- 7.2.1. GEO

- 7.2.2. LEO

- 7.2.3. MEO

- 7.3. Market Analysis, Insights and Forecast - by End User

- 7.3.1. Commercial

- 7.3.2. Military & Government

- 7.3.3. Other

- 7.4. Market Analysis, Insights and Forecast - by Propulsion Tech

- 7.4.1. Electric

- 7.4.2. Gas based

- 7.4.3. Liquid Fuel

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Small Satellite Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Communication

- 8.1.2. Earth Observation

- 8.1.3. Navigation

- 8.1.4. Space Observation

- 8.1.5. Others

- 8.2. Market Analysis, Insights and Forecast - by Orbit Class

- 8.2.1. GEO

- 8.2.2. LEO

- 8.2.3. MEO

- 8.3. Market Analysis, Insights and Forecast - by End User

- 8.3.1. Commercial

- 8.3.2. Military & Government

- 8.3.3. Other

- 8.4. Market Analysis, Insights and Forecast - by Propulsion Tech

- 8.4.1. Electric

- 8.4.2. Gas based

- 8.4.3. Liquid Fuel

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Small Satellite Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Communication

- 9.1.2. Earth Observation

- 9.1.3. Navigation

- 9.1.4. Space Observation

- 9.1.5. Others

- 9.2. Market Analysis, Insights and Forecast - by Orbit Class

- 9.2.1. GEO

- 9.2.2. LEO

- 9.2.3. MEO

- 9.3. Market Analysis, Insights and Forecast - by End User

- 9.3.1. Commercial

- 9.3.2. Military & Government

- 9.3.3. Other

- 9.4. Market Analysis, Insights and Forecast - by Propulsion Tech

- 9.4.1. Electric

- 9.4.2. Gas based

- 9.4.3. Liquid Fuel

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Small Satellite Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Communication

- 10.1.2. Earth Observation

- 10.1.3. Navigation

- 10.1.4. Space Observation

- 10.1.5. Others

- 10.2. Market Analysis, Insights and Forecast - by Orbit Class

- 10.2.1. GEO

- 10.2.2. LEO

- 10.2.3. MEO

- 10.3. Market Analysis, Insights and Forecast - by End User

- 10.3.1. Commercial

- 10.3.2. Military & Government

- 10.3.3. Other

- 10.4. Market Analysis, Insights and Forecast - by Propulsion Tech

- 10.4.1. Electric

- 10.4.2. Gas based

- 10.4.3. Liquid Fuel

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Small Satellite Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Communication

- 11.1.2. Earth Observation

- 11.1.3. Navigation

- 11.1.4. Space Observation

- 11.1.5. Others

- 11.2. Market Analysis, Insights and Forecast - by Orbit Class

- 11.2.1. GEO

- 11.2.2. LEO

- 11.2.3. MEO

- 11.3. Market Analysis, Insights and Forecast - by End User

- 11.3.1. Commercial

- 11.3.2. Military & Government

- 11.3.3. Other

- 11.4. Market Analysis, Insights and Forecast - by Propulsion Tech

- 11.4.1. Electric

- 11.4.2. Gas based

- 11.4.3. Liquid Fuel

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Space Exploration Technologies Corp

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 German Orbital Systems

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 GomSpaceApS

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Swarm Technologies Inc

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 SpaceQuest Ltd

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Airbus SE

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Axelspace Corporation

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Astrocast

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 China Aerospace Science and Technology Corporation (CASC)

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 ICEYE Ltd

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Chang Guang Satellite Technology Co Ltd

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Satellogic

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Thale

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Planet Labs Inc

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Spire Global Inc

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.1 Space Exploration Technologies Corp

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Small Satellite Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Small Satellite Industry Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Small Satellite Industry Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Small Satellite Industry Revenue (billion), by Orbit Class 2025 & 2033

- Figure 5: North America Small Satellite Industry Revenue Share (%), by Orbit Class 2025 & 2033

- Figure 6: North America Small Satellite Industry Revenue (billion), by End User 2025 & 2033

- Figure 7: North America Small Satellite Industry Revenue Share (%), by End User 2025 & 2033

- Figure 8: North America Small Satellite Industry Revenue (billion), by Propulsion Tech 2025 & 2033

- Figure 9: North America Small Satellite Industry Revenue Share (%), by Propulsion Tech 2025 & 2033

- Figure 10: North America Small Satellite Industry Revenue (billion), by Country 2025 & 2033

- Figure 11: North America Small Satellite Industry Revenue Share (%), by Country 2025 & 2033

- Figure 12: South America Small Satellite Industry Revenue (billion), by Application 2025 & 2033

- Figure 13: South America Small Satellite Industry Revenue Share (%), by Application 2025 & 2033

- Figure 14: South America Small Satellite Industry Revenue (billion), by Orbit Class 2025 & 2033

- Figure 15: South America Small Satellite Industry Revenue Share (%), by Orbit Class 2025 & 2033

- Figure 16: South America Small Satellite Industry Revenue (billion), by End User 2025 & 2033

- Figure 17: South America Small Satellite Industry Revenue Share (%), by End User 2025 & 2033

- Figure 18: South America Small Satellite Industry Revenue (billion), by Propulsion Tech 2025 & 2033

- Figure 19: South America Small Satellite Industry Revenue Share (%), by Propulsion Tech 2025 & 2033

- Figure 20: South America Small Satellite Industry Revenue (billion), by Country 2025 & 2033

- Figure 21: South America Small Satellite Industry Revenue Share (%), by Country 2025 & 2033

- Figure 22: Europe Small Satellite Industry Revenue (billion), by Application 2025 & 2033

- Figure 23: Europe Small Satellite Industry Revenue Share (%), by Application 2025 & 2033

- Figure 24: Europe Small Satellite Industry Revenue (billion), by Orbit Class 2025 & 2033

- Figure 25: Europe Small Satellite Industry Revenue Share (%), by Orbit Class 2025 & 2033

- Figure 26: Europe Small Satellite Industry Revenue (billion), by End User 2025 & 2033

- Figure 27: Europe Small Satellite Industry Revenue Share (%), by End User 2025 & 2033

- Figure 28: Europe Small Satellite Industry Revenue (billion), by Propulsion Tech 2025 & 2033

- Figure 29: Europe Small Satellite Industry Revenue Share (%), by Propulsion Tech 2025 & 2033

- Figure 30: Europe Small Satellite Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: Europe Small Satellite Industry Revenue Share (%), by Country 2025 & 2033

- Figure 32: Middle East & Africa Small Satellite Industry Revenue (billion), by Application 2025 & 2033

- Figure 33: Middle East & Africa Small Satellite Industry Revenue Share (%), by Application 2025 & 2033

- Figure 34: Middle East & Africa Small Satellite Industry Revenue (billion), by Orbit Class 2025 & 2033

- Figure 35: Middle East & Africa Small Satellite Industry Revenue Share (%), by Orbit Class 2025 & 2033

- Figure 36: Middle East & Africa Small Satellite Industry Revenue (billion), by End User 2025 & 2033

- Figure 37: Middle East & Africa Small Satellite Industry Revenue Share (%), by End User 2025 & 2033

- Figure 38: Middle East & Africa Small Satellite Industry Revenue (billion), by Propulsion Tech 2025 & 2033

- Figure 39: Middle East & Africa Small Satellite Industry Revenue Share (%), by Propulsion Tech 2025 & 2033

- Figure 40: Middle East & Africa Small Satellite Industry Revenue (billion), by Country 2025 & 2033

- Figure 41: Middle East & Africa Small Satellite Industry Revenue Share (%), by Country 2025 & 2033

- Figure 42: Asia Pacific Small Satellite Industry Revenue (billion), by Application 2025 & 2033

- Figure 43: Asia Pacific Small Satellite Industry Revenue Share (%), by Application 2025 & 2033

- Figure 44: Asia Pacific Small Satellite Industry Revenue (billion), by Orbit Class 2025 & 2033

- Figure 45: Asia Pacific Small Satellite Industry Revenue Share (%), by Orbit Class 2025 & 2033

- Figure 46: Asia Pacific Small Satellite Industry Revenue (billion), by End User 2025 & 2033

- Figure 47: Asia Pacific Small Satellite Industry Revenue Share (%), by End User 2025 & 2033

- Figure 48: Asia Pacific Small Satellite Industry Revenue (billion), by Propulsion Tech 2025 & 2033

- Figure 49: Asia Pacific Small Satellite Industry Revenue Share (%), by Propulsion Tech 2025 & 2033

- Figure 50: Asia Pacific Small Satellite Industry Revenue (billion), by Country 2025 & 2033

- Figure 51: Asia Pacific Small Satellite Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Small Satellite Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Small Satellite Industry Revenue billion Forecast, by Orbit Class 2020 & 2033

- Table 3: Global Small Satellite Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 4: Global Small Satellite Industry Revenue billion Forecast, by Propulsion Tech 2020 & 2033

- Table 5: Global Small Satellite Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Global Small Satellite Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 7: Global Small Satellite Industry Revenue billion Forecast, by Orbit Class 2020 & 2033

- Table 8: Global Small Satellite Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 9: Global Small Satellite Industry Revenue billion Forecast, by Propulsion Tech 2020 & 2033

- Table 10: Global Small Satellite Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 11: United States Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Canada Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Mexico Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Global Small Satellite Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 15: Global Small Satellite Industry Revenue billion Forecast, by Orbit Class 2020 & 2033

- Table 16: Global Small Satellite Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 17: Global Small Satellite Industry Revenue billion Forecast, by Propulsion Tech 2020 & 2033

- Table 18: Global Small Satellite Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 19: Brazil Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Argentina Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: Rest of South America Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Global Small Satellite Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 23: Global Small Satellite Industry Revenue billion Forecast, by Orbit Class 2020 & 2033

- Table 24: Global Small Satellite Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 25: Global Small Satellite Industry Revenue billion Forecast, by Propulsion Tech 2020 & 2033

- Table 26: Global Small Satellite Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 27: United Kingdom Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Germany Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 29: France Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Italy Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 31: Spain Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Russia Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: Benelux Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: Nordics Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: Rest of Europe Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Global Small Satellite Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 37: Global Small Satellite Industry Revenue billion Forecast, by Orbit Class 2020 & 2033

- Table 38: Global Small Satellite Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 39: Global Small Satellite Industry Revenue billion Forecast, by Propulsion Tech 2020 & 2033

- Table 40: Global Small Satellite Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 41: Turkey Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Israel Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: GCC Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: North Africa Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: South Africa Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Middle East & Africa Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 47: Global Small Satellite Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 48: Global Small Satellite Industry Revenue billion Forecast, by Orbit Class 2020 & 2033

- Table 49: Global Small Satellite Industry Revenue billion Forecast, by End User 2020 & 2033

- Table 50: Global Small Satellite Industry Revenue billion Forecast, by Propulsion Tech 2020 & 2033

- Table 51: Global Small Satellite Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 52: China Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 53: India Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 54: Japan Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 55: South Korea Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 56: ASEAN Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 57: Oceania Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 58: Rest of Asia Pacific Small Satellite Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Small Satellite Industry?

The projected CAGR is approximately 11%.

2. Which companies are prominent players in the Small Satellite Industry?

Key companies in the market include Space Exploration Technologies Corp, German Orbital Systems, GomSpaceApS, Swarm Technologies Inc, SpaceQuest Ltd, Airbus SE, Axelspace Corporation, Astrocast, China Aerospace Science and Technology Corporation (CASC), ICEYE Ltd, Chang Guang Satellite Technology Co Ltd, Satellogic, Thale, Planet Labs Inc, Spire Global Inc.

3. What are the main segments of the Small Satellite Industry?

The market segments include Application, Orbit Class, End User, Propulsion Tech.

4. Can you provide details about the market size?

The market size is estimated to be USD 98.28 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

North America may witness significant growth during the forecast period.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

June 2022: Falcon 9 launched Globalstar FM15 to low-Earth orbit from Space Launch Complex 40 (SLC-40) at Cape Canaveral Space Force Station in Florida.May 2022: As part of the Transporter-5 mission another five satellitesnamely ICEYE-X17, -X18, -X19, -X20 and -X24 were launched.April 2022: Swarm Technologies 12 'picosatellites' on the Transporter 4 mission for low-data-rate communications network have been launched.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Small Satellite Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Small Satellite Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Small Satellite Industry?

To stay informed about further developments, trends, and reports in the Small Satellite Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence