Key Insights

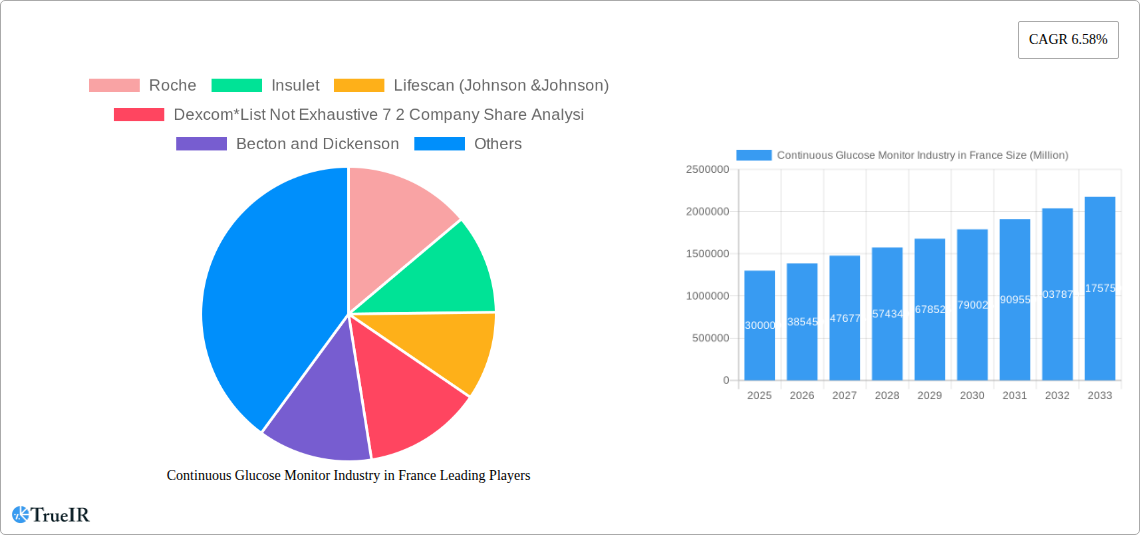

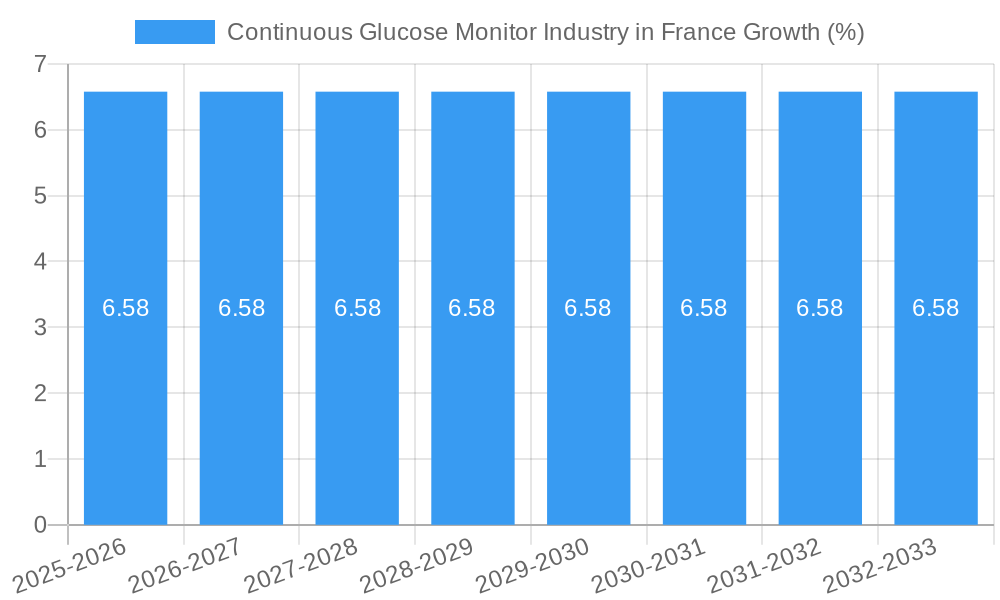

The French Continuous Glucose Monitor (CGM) market is poised for substantial growth, projecting a robust Compound Annual Growth Rate (CAGR) of 6.58% from a base year of 2025 through 2033. This upward trajectory, from an estimated market size of 1.30 million units in 2025, is primarily fueled by increasing awareness of diabetes management, technological advancements in CGMs, and favorable reimbursement policies that are making these devices more accessible to a wider patient population. The market is segmented into monitoring devices, including self-monitoring blood glucose devices like glucometers, test strips, and lancets, alongside advanced continuous blood glucose monitoring systems with sophisticated sensors and durable components. Management devices, such as insulin pumps, syringes, cartridges, and disposable pens, also play a crucial role, indicating a holistic approach to diabetes care.

Key drivers for this market expansion in France include the rising prevalence of diabetes, both Type 1 and Type 2, which necessitates continuous monitoring for effective disease management. The growing adoption of CGMs by healthcare professionals and patients seeking better glycemic control and reduced long-term complications is another significant factor. Technological innovations, leading to smaller, more accurate, and user-friendly CGM devices, are also contributing to market penetration. Furthermore, the increasing focus on preventative healthcare and the digital health revolution are fostering a more proactive approach to chronic disease management. While the market demonstrates strong growth potential, potential restraints might include the initial cost of devices for some segments of the population and the need for continued education and training for both patients and healthcare providers to fully leverage the benefits of CGM technology. The competitive landscape features major players like Roche, Dexcom, and Abbott, driving innovation and market expansion.

Continuous Glucose Monitor Industry in France: Market Dynamics and Forecast 2019-2033

This comprehensive report provides an in-depth analysis of the Continuous Glucose Monitor (CGM) industry in France, covering market structure, competitive landscape, key trends, dominant segments, product analysis, drivers, challenges, and future outlook. Examining data from 2019 to 2033, with a base year of 2025, this report offers critical insights for stakeholders navigating this rapidly evolving healthcare sector.

Continuous Glucose Monitor Industry in France Market Structure & Competitive Landscape

The French Continuous Glucose Monitor (CGM) market exhibits a moderate to high concentration, driven by the significant investments and established presence of global leaders such as Roche, Insulet, Lifescan (Johnson & Johnson), and Dexcom. These companies, alongside Abbott and Medtronic, hold substantial market share, influencing innovation and pricing strategies. The competitive landscape is characterized by a strong emphasis on technological innovation, particularly in sensor accuracy, data connectivity, and user-friendly interfaces. Regulatory impacts, primarily from national health authorities and the European Union, play a crucial role in market access and reimbursement policies, influencing adoption rates for advanced diabetes management devices. Product substitutes include traditional self-monitoring blood glucose (SMBG) devices, though the superior data insights and reduced invasiveness of CGMs are increasingly differentiating them. End-user segmentation centers on individuals with Type 1 and Type 2 diabetes, with a growing segment of pre-diabetes individuals seeking proactive health management. Mergers and acquisitions (M&A) trends are observed as companies seek to expand their product portfolios, gain access to new technologies, or strengthen their market position. For instance, strategic partnerships, like the April 2022 collaboration between CamDiab and Ypsomed, highlight the trend towards integrated diabetes management systems. Quantitative analysis reveals that the top 5 players likely account for over 70% of the market share, with significant investment in R&D from key entities like Dexcom, aiming to enhance sensor longevity and connectivity features.

Continuous Glucose Monitor Industry in France Market Trends & Opportunities

The French Continuous Glucose Monitor (CGM) market is poised for substantial growth, projected to expand significantly over the forecast period (2025-2033). This expansion is fueled by a confluence of factors including rising diabetes prevalence, increasing patient awareness of advanced diabetes management technologies, and favorable reimbursement policies. The market size for CGMs in France is estimated to reach over 5,000 Million by 2025, with a projected Compound Annual Growth Rate (CAGR) of approximately 15% during the forecast period. Technological shifts are a primary driver, with continuous advancements in sensor accuracy, miniaturization, and data analytics transforming the user experience. The integration of AI and machine learning in CGM platforms is enabling more personalized treatment plans and predictive alerts, thereby enhancing glycemic control and reducing the risk of complications. Consumer preferences are increasingly leaning towards non-invasive or minimally invasive devices that offer real-time data, seamless integration with smartphones, and robust reporting capabilities. This shift is evident in the growing demand for advanced CGMs over traditional blood glucose meters. Competitive dynamics are intensifying, with established players and emerging innovators vying for market dominance through product differentiation, strategic partnerships, and expanded market access. For example, the September 2023 announcement regarding Dexcom ONE’s accessibility in France, potentially benefiting an additional half a million individuals with diabetes, signifies a major opportunity to broaden market penetration and improve patient outcomes. Furthermore, the increasing focus on remote patient monitoring and telehealth services provides a fertile ground for CGM adoption, as healthcare providers can remotely track patient glucose levels and intervene proactively. The growing emphasis on preventive healthcare and lifestyle management also presents an opportunity for CGMs to be utilized by a wider population, not just those diagnosed with diabetes. The market penetration rate for CGMs, currently around 20% of the eligible diabetes population, is expected to rise steadily as awareness and affordability increase, presenting a significant untapped market potential.

Dominant Markets & Segments in Continuous Glucose Monitor Industry in France

The Continuous Glucose Monitor (CGM) industry in France is experiencing robust growth across its key segments, with Continuous Blood Glucose Monitoring emerging as the dominant market force. Within this segment, Sensors represent the highest revenue-generating category due to their recurring purchase nature and critical role in CGM functionality. The Durables component, encompassing the transmitter and reader, also contributes significantly to market value as they represent a one-time, albeit higher, initial investment. This segment's dominance is propelled by advancements in sensor technology, leading to improved accuracy, longer wear times, and greater patient comfort. The increasing adoption of real-time CGM systems, which provide continuous data streams, over intermittent scanning systems, further solidifies this segment's lead.

The Management Devices segment also holds substantial importance, particularly the Insulin Pump sub-segment. This includes Insulin Pump Devices, Insulin Pump Reservoirs, and Infusion Sets. The integration of insulin pumps with CGM technology to create Automated Insulin Delivery (AID) systems is a significant growth driver. Partnerships, such as the April 2022 announcement between CamDiab and Ypsomed, which integrates Abbott's FreeStyle Libre 3 sensor with Ypsomed's mylife YpsoPump, underscore the growing trend towards "closed-loop" diabetes management systems. These systems offer a more sophisticated and personalized approach to diabetes care, reducing the burden on patients.

The Self-monitoring Blood Glucose Devices segment, while traditionally dominant, is experiencing a relative decline in growth compared to CGMs, although Test Strips continue to represent a significant market due to the existing installed base of glucometer users. However, the shift towards CGMs is undeniable, driven by their ability to provide a more comprehensive picture of glucose fluctuations and trends.

Key Growth Drivers for Dominant Segments:

- Technological Advancements: Miniaturization, improved accuracy, longer sensor lifespan, and wireless connectivity in CGM sensors and transmitters.

- Integration with Insulin Pumps: The rise of AID systems and artificial pancreas technology enhances the value proposition of both insulin pumps and CGMs.

- Reimbursement Policies: Expanding coverage for CGMs by national health insurance providers in France is a critical factor driving adoption.

- Increased Patient Awareness and Demand: Growing understanding of the benefits of continuous glucose data for proactive diabetes management.

- Supportive Healthcare Infrastructure: A well-established healthcare system capable of supporting the integration and utilization of advanced diabetes technologies.

- Government Initiatives: Public health programs and awareness campaigns promoting diabetes management and early detection.

Continuous Glucose Monitor Industry in France Product Analysis

The French CGM market is characterized by a continuous stream of product innovations aimed at enhancing accuracy, usability, and connectivity. Key advancements include the development of longer-lasting sensors, improved algorithms for predictive alerts, and seamless integration with smartphones and other digital health platforms. Companies are focusing on miniaturizing devices for greater comfort and discretion, while also improving data analytics to provide actionable insights for both patients and healthcare providers. Competitive advantages are being forged through superior sensor accuracy, extended wear times, simplified calibration processes, and robust data management systems that facilitate personalized treatment plans. The emergence of AID systems, which combine CGMs with insulin pumps, represents a significant leap in product development, offering a more automated and effective approach to diabetes management.

Key Drivers, Barriers & Challenges in Continuous Glucose Monitor Industry in France

Key Drivers:

- Technological Innovation: Continuous advancements in sensor accuracy, durability, and connectivity, leading to improved patient outcomes.

- Rising Diabetes Prevalence: An increasing number of individuals diagnosed with diabetes necessitates more effective management tools.

- Government Support and Reimbursement: Favorable policies and expanding insurance coverage for CGMs significantly boost market accessibility.

- Patient Demand for Proactive Management: Growing desire among individuals to actively monitor and control their glucose levels for better health.

- Integration with Digital Health Ecosystems: Seamless connectivity with smartphones and other devices enhances user experience and data utilization.

Key Barriers & Challenges:

- High Cost of Devices: The initial investment for some CGM systems can be a barrier for certain patient populations.

- Reimbursement Complexity: Navigating evolving reimbursement policies and ensuring consistent coverage across different patient profiles.

- User Adoption and Training: Ensuring patients are adequately trained to interpret and act upon CGM data effectively.

- Data Security and Privacy Concerns: Managing and protecting sensitive patient health data.

- Supply Chain Disruptions: Potential for interruptions in the manufacturing and distribution of critical components.

- Competition from Traditional Devices: While declining, the established market for SMBG devices presents ongoing competition.

Growth Drivers in the Continuous Glucose Monitor Industry in France Market

The French Continuous Glucose Monitor (CGM) market is propelled by several key drivers. Technologically, relentless innovation in sensor accuracy, longevity, and reduced invasiveness is making CGMs more appealing. Economic factors, including increasing healthcare expenditure and a growing demand for advanced diabetes management solutions, also contribute significantly. Crucially, government support and evolving reimbursement policies are expanding access to these life-saving devices for a larger patient population. Furthermore, the proactive approach to health management favored by many individuals, coupled with the growing integration of CGMs into digital health ecosystems, creates a synergistic environment for market expansion. For example, the widening coverage for CGMs by French health authorities is a direct catalyst for increased adoption.

Challenges Impacting Continuous Glucose Monitor Industry in France Growth

Despite its promising growth trajectory, the French CGM industry faces significant challenges. Regulatory complexities, while ensuring safety and efficacy, can sometimes slow down the approval and market entry of new technologies. Supply chain issues, particularly in the global electronics and medical device sectors, can lead to material shortages or production delays, impacting device availability. Competitive pressures are also intense, with established players and new entrants constantly vying for market share. The high initial cost of some advanced CGM systems remains a barrier for a segment of the population, and ensuring equitable access requires ongoing efforts in pricing strategies and reimbursement advocacy. Quantifiable impacts of these challenges could include an estimated 5-10% slowdown in market penetration in specific sub-segments if supply chain disruptions persist.

Key Players Shaping the Continuous Glucose Monitor Industry in France Market

- Roche

- Insulet

- Lifescan (Johnson & Johnson)

- Dexcom

- Becton and Dickenson

- Ypsomed

- Abbott

- Novo Nordisk

- Eli Lilly

- Sanofi

- Medtronic

- Tandem

Significant Continuous Glucose Monitor Industry in France Industry Milestones

- September 2023: Dexcom has revealed that their Dexcom ONE system, offering real-time continuous glucose monitoring (CGM), is now accessible in France for individuals with diabetes. This advancement in diabetes technology accessibility is a significant victory for those with diabetes, as it will extend this life-saving technology to an additional half a million individuals with diabetes in France.

- April 2022: CamDiab and Ypsomed announced the partnership to develop and commercialize an integrated automated insulin delivery (AID) system to help lessen the burden of diabetes management for people with diabetes in European countries. The new integrated AID system is designed to connect Abbott's FreeStyle Libre 3 sensor, the world's smallest and most accurate continuous glucose monitoring sensor, to CamDiab's CamAPS FX mobile app, which connects with Ypsomed's mylife YpsoPump creating a smart, automated process to deliver insulin based on real-time glucose data.

Future Outlook for Continuous Glucose Monitor Industry in France Market

The future outlook for the Continuous Glucose Monitor (CGM) industry in France is exceptionally bright, driven by an ongoing wave of technological advancements and increasing patient-centric healthcare approaches. Strategic opportunities lie in the further development of AI-powered predictive analytics within CGM platforms, offering even more personalized insights and proactive interventions for diabetes management. The expansion of integrated diabetes management systems, combining CGMs with advanced insulin delivery devices, will continue to revolutionize patient care. Market potential is substantial as reimbursement policies evolve to encompass broader patient demographics and as awareness campaigns effectively highlight the life-changing benefits of continuous glucose monitoring. The industry is expected to witness sustained growth, driven by innovations that enhance user convenience, accuracy, and affordability, ultimately contributing to improved health outcomes for millions in France.

Continuous Glucose Monitor Industry in France Segmentation

-

1. Monitoring Devices

-

1.1. Self-monitoring Blood Glucose Devices

- 1.1.1. Glucometer Devices

- 1.1.2. Test Strips

- 1.1.3. Lancets

-

1.2. Continuous Blood Glucose Monitoring

- 1.2.1. Sensors

- 1.2.2. Durables

-

1.1. Self-monitoring Blood Glucose Devices

-

2. Management Devices

-

2.1. Insulin Pump

- 2.1.1. Insulin Pump Device

- 2.1.2. Insulin Pump Reservoir

- 2.1.3. Infusion Set

- 2.2. Insulin Syringes

- 2.3. Insulin Cartridges

- 2.4. Disposable Pens

-

2.1. Insulin Pump

Continuous Glucose Monitor Industry in France Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Continuous Glucose Monitor Industry in France REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 6.58% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Number of Preterm and Low-weight Births; Advanced Technology in Fetal and Prenatal Monitoring

- 3.3. Market Restrains

- 3.3.1. Stringent Regulatory Procedures

- 3.4. Market Trends

- 3.4.1. Monitoring Devices Hold Highest Market Share in France Diabetes Care Devices Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Continuous Glucose Monitor Industry in France Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Monitoring Devices

- 5.1.1. Self-monitoring Blood Glucose Devices

- 5.1.1.1. Glucometer Devices

- 5.1.1.2. Test Strips

- 5.1.1.3. Lancets

- 5.1.2. Continuous Blood Glucose Monitoring

- 5.1.2.1. Sensors

- 5.1.2.2. Durables

- 5.1.1. Self-monitoring Blood Glucose Devices

- 5.2. Market Analysis, Insights and Forecast - by Management Devices

- 5.2.1. Insulin Pump

- 5.2.1.1. Insulin Pump Device

- 5.2.1.2. Insulin Pump Reservoir

- 5.2.1.3. Infusion Set

- 5.2.2. Insulin Syringes

- 5.2.3. Insulin Cartridges

- 5.2.4. Disposable Pens

- 5.2.1. Insulin Pump

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Monitoring Devices

- 6. North America Continuous Glucose Monitor Industry in France Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Monitoring Devices

- 6.1.1. Self-monitoring Blood Glucose Devices

- 6.1.1.1. Glucometer Devices

- 6.1.1.2. Test Strips

- 6.1.1.3. Lancets

- 6.1.2. Continuous Blood Glucose Monitoring

- 6.1.2.1. Sensors

- 6.1.2.2. Durables

- 6.1.1. Self-monitoring Blood Glucose Devices

- 6.2. Market Analysis, Insights and Forecast - by Management Devices

- 6.2.1. Insulin Pump

- 6.2.1.1. Insulin Pump Device

- 6.2.1.2. Insulin Pump Reservoir

- 6.2.1.3. Infusion Set

- 6.2.2. Insulin Syringes

- 6.2.3. Insulin Cartridges

- 6.2.4. Disposable Pens

- 6.2.1. Insulin Pump

- 6.1. Market Analysis, Insights and Forecast - by Monitoring Devices

- 7. South America Continuous Glucose Monitor Industry in France Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Monitoring Devices

- 7.1.1. Self-monitoring Blood Glucose Devices

- 7.1.1.1. Glucometer Devices

- 7.1.1.2. Test Strips

- 7.1.1.3. Lancets

- 7.1.2. Continuous Blood Glucose Monitoring

- 7.1.2.1. Sensors

- 7.1.2.2. Durables

- 7.1.1. Self-monitoring Blood Glucose Devices

- 7.2. Market Analysis, Insights and Forecast - by Management Devices

- 7.2.1. Insulin Pump

- 7.2.1.1. Insulin Pump Device

- 7.2.1.2. Insulin Pump Reservoir

- 7.2.1.3. Infusion Set

- 7.2.2. Insulin Syringes

- 7.2.3. Insulin Cartridges

- 7.2.4. Disposable Pens

- 7.2.1. Insulin Pump

- 7.1. Market Analysis, Insights and Forecast - by Monitoring Devices

- 8. Europe Continuous Glucose Monitor Industry in France Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Monitoring Devices

- 8.1.1. Self-monitoring Blood Glucose Devices

- 8.1.1.1. Glucometer Devices

- 8.1.1.2. Test Strips

- 8.1.1.3. Lancets

- 8.1.2. Continuous Blood Glucose Monitoring

- 8.1.2.1. Sensors

- 8.1.2.2. Durables

- 8.1.1. Self-monitoring Blood Glucose Devices

- 8.2. Market Analysis, Insights and Forecast - by Management Devices

- 8.2.1. Insulin Pump

- 8.2.1.1. Insulin Pump Device

- 8.2.1.2. Insulin Pump Reservoir

- 8.2.1.3. Infusion Set

- 8.2.2. Insulin Syringes

- 8.2.3. Insulin Cartridges

- 8.2.4. Disposable Pens

- 8.2.1. Insulin Pump

- 8.1. Market Analysis, Insights and Forecast - by Monitoring Devices

- 9. Middle East & Africa Continuous Glucose Monitor Industry in France Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Monitoring Devices

- 9.1.1. Self-monitoring Blood Glucose Devices

- 9.1.1.1. Glucometer Devices

- 9.1.1.2. Test Strips

- 9.1.1.3. Lancets

- 9.1.2. Continuous Blood Glucose Monitoring

- 9.1.2.1. Sensors

- 9.1.2.2. Durables

- 9.1.1. Self-monitoring Blood Glucose Devices

- 9.2. Market Analysis, Insights and Forecast - by Management Devices

- 9.2.1. Insulin Pump

- 9.2.1.1. Insulin Pump Device

- 9.2.1.2. Insulin Pump Reservoir

- 9.2.1.3. Infusion Set

- 9.2.2. Insulin Syringes

- 9.2.3. Insulin Cartridges

- 9.2.4. Disposable Pens

- 9.2.1. Insulin Pump

- 9.1. Market Analysis, Insights and Forecast - by Monitoring Devices

- 10. Asia Pacific Continuous Glucose Monitor Industry in France Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Monitoring Devices

- 10.1.1. Self-monitoring Blood Glucose Devices

- 10.1.1.1. Glucometer Devices

- 10.1.1.2. Test Strips

- 10.1.1.3. Lancets

- 10.1.2. Continuous Blood Glucose Monitoring

- 10.1.2.1. Sensors

- 10.1.2.2. Durables

- 10.1.1. Self-monitoring Blood Glucose Devices

- 10.2. Market Analysis, Insights and Forecast - by Management Devices

- 10.2.1. Insulin Pump

- 10.2.1.1. Insulin Pump Device

- 10.2.1.2. Insulin Pump Reservoir

- 10.2.1.3. Infusion Set

- 10.2.2. Insulin Syringes

- 10.2.3. Insulin Cartridges

- 10.2.4. Disposable Pens

- 10.2.1. Insulin Pump

- 10.1. Market Analysis, Insights and Forecast - by Monitoring Devices

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 Roche

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Insulet

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Lifescan (Johnson &Johnson)

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Dexcom*List Not Exhaustive 7 2 Company Share Analysi

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Becton and Dickenson

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Ypsomed

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Abbottt

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Novo Nordisk

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Eli Lilly

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Sanofi

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Medtronic

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Tandem

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.1 Roche

List of Figures

- Figure 1: Global Continuous Glucose Monitor Industry in France Revenue Breakdown (Million, %) by Region 2024 & 2032

- Figure 2: France Continuous Glucose Monitor Industry in France Revenue (Million), by Country 2024 & 2032

- Figure 3: France Continuous Glucose Monitor Industry in France Revenue Share (%), by Country 2024 & 2032

- Figure 4: North America Continuous Glucose Monitor Industry in France Revenue (Million), by Monitoring Devices 2024 & 2032

- Figure 5: North America Continuous Glucose Monitor Industry in France Revenue Share (%), by Monitoring Devices 2024 & 2032

- Figure 6: North America Continuous Glucose Monitor Industry in France Revenue (Million), by Management Devices 2024 & 2032

- Figure 7: North America Continuous Glucose Monitor Industry in France Revenue Share (%), by Management Devices 2024 & 2032

- Figure 8: North America Continuous Glucose Monitor Industry in France Revenue (Million), by Country 2024 & 2032

- Figure 9: North America Continuous Glucose Monitor Industry in France Revenue Share (%), by Country 2024 & 2032

- Figure 10: South America Continuous Glucose Monitor Industry in France Revenue (Million), by Monitoring Devices 2024 & 2032

- Figure 11: South America Continuous Glucose Monitor Industry in France Revenue Share (%), by Monitoring Devices 2024 & 2032

- Figure 12: South America Continuous Glucose Monitor Industry in France Revenue (Million), by Management Devices 2024 & 2032

- Figure 13: South America Continuous Glucose Monitor Industry in France Revenue Share (%), by Management Devices 2024 & 2032

- Figure 14: South America Continuous Glucose Monitor Industry in France Revenue (Million), by Country 2024 & 2032

- Figure 15: South America Continuous Glucose Monitor Industry in France Revenue Share (%), by Country 2024 & 2032

- Figure 16: Europe Continuous Glucose Monitor Industry in France Revenue (Million), by Monitoring Devices 2024 & 2032

- Figure 17: Europe Continuous Glucose Monitor Industry in France Revenue Share (%), by Monitoring Devices 2024 & 2032

- Figure 18: Europe Continuous Glucose Monitor Industry in France Revenue (Million), by Management Devices 2024 & 2032

- Figure 19: Europe Continuous Glucose Monitor Industry in France Revenue Share (%), by Management Devices 2024 & 2032

- Figure 20: Europe Continuous Glucose Monitor Industry in France Revenue (Million), by Country 2024 & 2032

- Figure 21: Europe Continuous Glucose Monitor Industry in France Revenue Share (%), by Country 2024 & 2032

- Figure 22: Middle East & Africa Continuous Glucose Monitor Industry in France Revenue (Million), by Monitoring Devices 2024 & 2032

- Figure 23: Middle East & Africa Continuous Glucose Monitor Industry in France Revenue Share (%), by Monitoring Devices 2024 & 2032

- Figure 24: Middle East & Africa Continuous Glucose Monitor Industry in France Revenue (Million), by Management Devices 2024 & 2032

- Figure 25: Middle East & Africa Continuous Glucose Monitor Industry in France Revenue Share (%), by Management Devices 2024 & 2032

- Figure 26: Middle East & Africa Continuous Glucose Monitor Industry in France Revenue (Million), by Country 2024 & 2032

- Figure 27: Middle East & Africa Continuous Glucose Monitor Industry in France Revenue Share (%), by Country 2024 & 2032

- Figure 28: Asia Pacific Continuous Glucose Monitor Industry in France Revenue (Million), by Monitoring Devices 2024 & 2032

- Figure 29: Asia Pacific Continuous Glucose Monitor Industry in France Revenue Share (%), by Monitoring Devices 2024 & 2032

- Figure 30: Asia Pacific Continuous Glucose Monitor Industry in France Revenue (Million), by Management Devices 2024 & 2032

- Figure 31: Asia Pacific Continuous Glucose Monitor Industry in France Revenue Share (%), by Management Devices 2024 & 2032

- Figure 32: Asia Pacific Continuous Glucose Monitor Industry in France Revenue (Million), by Country 2024 & 2032

- Figure 33: Asia Pacific Continuous Glucose Monitor Industry in France Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Continuous Glucose Monitor Industry in France Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Global Continuous Glucose Monitor Industry in France Revenue Million Forecast, by Monitoring Devices 2019 & 2032

- Table 3: Global Continuous Glucose Monitor Industry in France Revenue Million Forecast, by Management Devices 2019 & 2032

- Table 4: Global Continuous Glucose Monitor Industry in France Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Global Continuous Glucose Monitor Industry in France Revenue Million Forecast, by Country 2019 & 2032

- Table 6: Global Continuous Glucose Monitor Industry in France Revenue Million Forecast, by Monitoring Devices 2019 & 2032

- Table 7: Global Continuous Glucose Monitor Industry in France Revenue Million Forecast, by Management Devices 2019 & 2032

- Table 8: Global Continuous Glucose Monitor Industry in France Revenue Million Forecast, by Country 2019 & 2032

- Table 9: United States Continuous Glucose Monitor Industry in France Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Canada Continuous Glucose Monitor Industry in France Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Mexico Continuous Glucose Monitor Industry in France Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Global Continuous Glucose Monitor Industry in France Revenue Million Forecast, by Monitoring Devices 2019 & 2032

- Table 13: Global Continuous Glucose Monitor Industry in France Revenue Million Forecast, by Management Devices 2019 & 2032

- Table 14: Global Continuous Glucose Monitor Industry in France Revenue Million Forecast, by Country 2019 & 2032

- Table 15: Brazil Continuous Glucose Monitor Industry in France Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Argentina Continuous Glucose Monitor Industry in France Revenue (Million) Forecast, by Application 2019 & 2032

- Table 17: Rest of South America Continuous Glucose Monitor Industry in France Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Global Continuous Glucose Monitor Industry in France Revenue Million Forecast, by Monitoring Devices 2019 & 2032

- Table 19: Global Continuous Glucose Monitor Industry in France Revenue Million Forecast, by Management Devices 2019 & 2032

- Table 20: Global Continuous Glucose Monitor Industry in France Revenue Million Forecast, by Country 2019 & 2032

- Table 21: United Kingdom Continuous Glucose Monitor Industry in France Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Germany Continuous Glucose Monitor Industry in France Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: France Continuous Glucose Monitor Industry in France Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: Italy Continuous Glucose Monitor Industry in France Revenue (Million) Forecast, by Application 2019 & 2032

- Table 25: Spain Continuous Glucose Monitor Industry in France Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: Russia Continuous Glucose Monitor Industry in France Revenue (Million) Forecast, by Application 2019 & 2032

- Table 27: Benelux Continuous Glucose Monitor Industry in France Revenue (Million) Forecast, by Application 2019 & 2032

- Table 28: Nordics Continuous Glucose Monitor Industry in France Revenue (Million) Forecast, by Application 2019 & 2032

- Table 29: Rest of Europe Continuous Glucose Monitor Industry in France Revenue (Million) Forecast, by Application 2019 & 2032

- Table 30: Global Continuous Glucose Monitor Industry in France Revenue Million Forecast, by Monitoring Devices 2019 & 2032

- Table 31: Global Continuous Glucose Monitor Industry in France Revenue Million Forecast, by Management Devices 2019 & 2032

- Table 32: Global Continuous Glucose Monitor Industry in France Revenue Million Forecast, by Country 2019 & 2032

- Table 33: Turkey Continuous Glucose Monitor Industry in France Revenue (Million) Forecast, by Application 2019 & 2032

- Table 34: Israel Continuous Glucose Monitor Industry in France Revenue (Million) Forecast, by Application 2019 & 2032

- Table 35: GCC Continuous Glucose Monitor Industry in France Revenue (Million) Forecast, by Application 2019 & 2032

- Table 36: North Africa Continuous Glucose Monitor Industry in France Revenue (Million) Forecast, by Application 2019 & 2032

- Table 37: South Africa Continuous Glucose Monitor Industry in France Revenue (Million) Forecast, by Application 2019 & 2032

- Table 38: Rest of Middle East & Africa Continuous Glucose Monitor Industry in France Revenue (Million) Forecast, by Application 2019 & 2032

- Table 39: Global Continuous Glucose Monitor Industry in France Revenue Million Forecast, by Monitoring Devices 2019 & 2032

- Table 40: Global Continuous Glucose Monitor Industry in France Revenue Million Forecast, by Management Devices 2019 & 2032

- Table 41: Global Continuous Glucose Monitor Industry in France Revenue Million Forecast, by Country 2019 & 2032

- Table 42: China Continuous Glucose Monitor Industry in France Revenue (Million) Forecast, by Application 2019 & 2032

- Table 43: India Continuous Glucose Monitor Industry in France Revenue (Million) Forecast, by Application 2019 & 2032

- Table 44: Japan Continuous Glucose Monitor Industry in France Revenue (Million) Forecast, by Application 2019 & 2032

- Table 45: South Korea Continuous Glucose Monitor Industry in France Revenue (Million) Forecast, by Application 2019 & 2032

- Table 46: ASEAN Continuous Glucose Monitor Industry in France Revenue (Million) Forecast, by Application 2019 & 2032

- Table 47: Oceania Continuous Glucose Monitor Industry in France Revenue (Million) Forecast, by Application 2019 & 2032

- Table 48: Rest of Asia Pacific Continuous Glucose Monitor Industry in France Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Continuous Glucose Monitor Industry in France?

The projected CAGR is approximately 6.58%.

2. Which companies are prominent players in the Continuous Glucose Monitor Industry in France?

Key companies in the market include Roche, Insulet, Lifescan (Johnson &Johnson), Dexcom*List Not Exhaustive 7 2 Company Share Analysi, Becton and Dickenson, Ypsomed, Abbottt, Novo Nordisk, Eli Lilly, Sanofi, Medtronic, Tandem.

3. What are the main segments of the Continuous Glucose Monitor Industry in France?

The market segments include Monitoring Devices, Management Devices.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.30 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Number of Preterm and Low-weight Births; Advanced Technology in Fetal and Prenatal Monitoring.

6. What are the notable trends driving market growth?

Monitoring Devices Hold Highest Market Share in France Diabetes Care Devices Market.

7. Are there any restraints impacting market growth?

Stringent Regulatory Procedures.

8. Can you provide examples of recent developments in the market?

September 2023: Dexcom has revealed that their Dexcom ONE system, which offers real-time continuous glucose monitoring (CGM), is now accessible in France for individuals with diabetes. This advancement in diabetes technology accessibility is a significant victory for those with diabetes, as it will extend this life-saving technology to an additional half a million individuals with diabetes in France.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Continuous Glucose Monitor Industry in France," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Continuous Glucose Monitor Industry in France report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Continuous Glucose Monitor Industry in France?

To stay informed about further developments, trends, and reports in the Continuous Glucose Monitor Industry in France, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence