Key Insights

The European arthroscopy devices market is poised for steady growth, reaching an estimated value of $382.38 million by 2025. This expansion is fueled by an increasing prevalence of orthopedic conditions, particularly among an aging population and a growing number of athletes and physically active individuals. Advances in minimally invasive surgical techniques, driven by the demand for reduced patient recovery times and improved surgical outcomes, are also significant drivers. Key application segments such as knee and hip arthroscopy are expected to lead the market, owing to their high procedural volumes and the continuous development of specialized instrumentation. The market is also witnessing a rise in the adoption of sophisticated visualization systems and radiofrequency devices, enhancing diagnostic accuracy and therapeutic efficacy. Companies are actively investing in research and development to introduce innovative products that offer greater precision, portability, and cost-effectiveness, further stimulating market penetration across Europe.

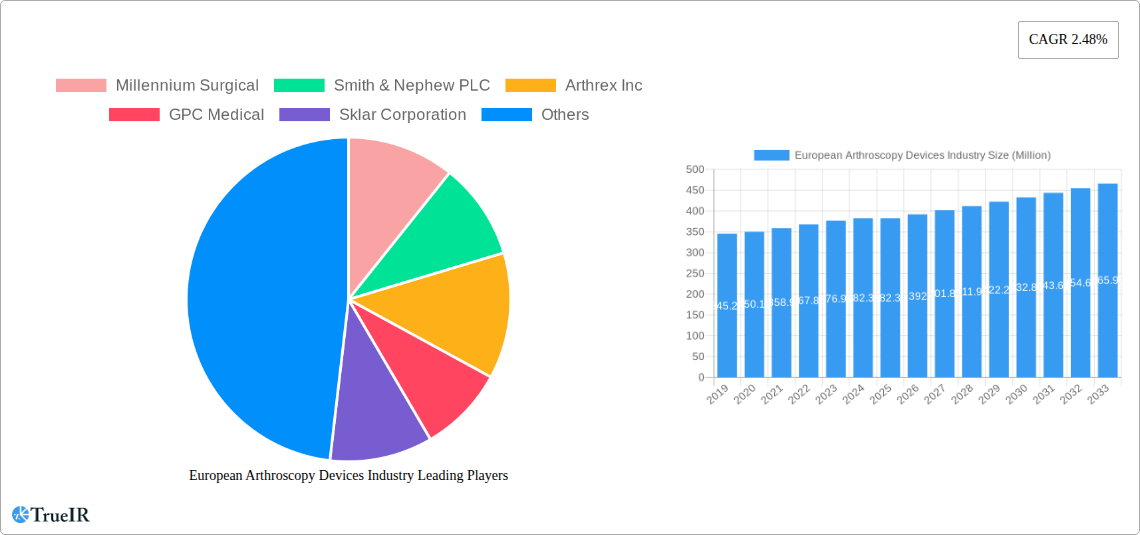

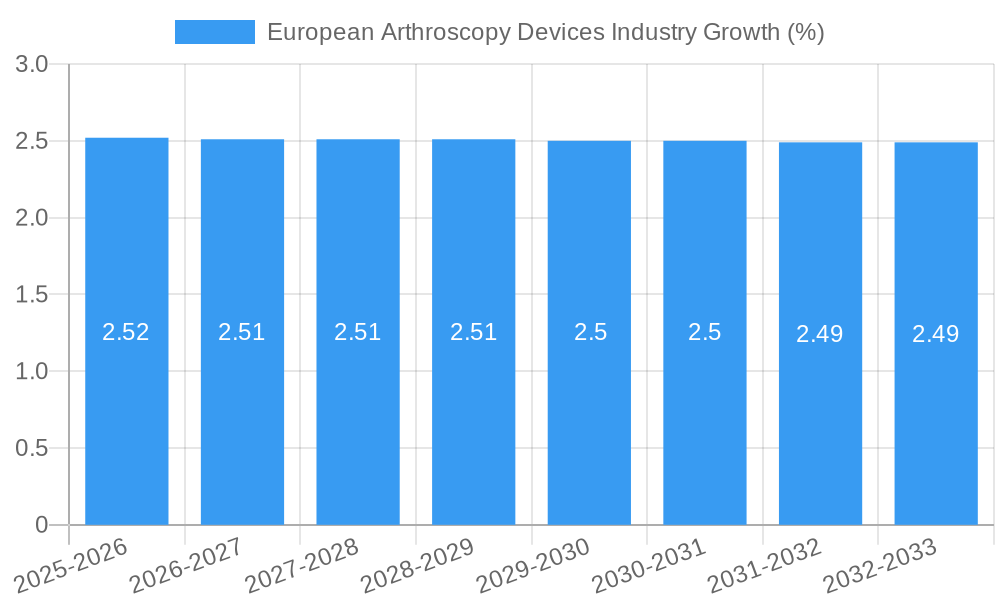

The projected Compound Annual Growth Rate (CAGR) of 2.48% for the European arthroscopy devices market over the forecast period (2025-2033) indicates a robust and sustainable expansion trajectory. This growth is underpinned by several key trends, including the increasing adoption of robotic-assisted arthroscopy and the development of advanced arthroscopic implants designed for enhanced biomechanical performance and faster integration. However, the market is not without its challenges. Restraints such as the high cost of advanced arthroscopy equipment and the limited availability of trained surgeons in certain regions could temper the growth rate. Furthermore, stringent regulatory approvals for new medical devices and the reimbursement landscape for arthroscopic procedures play a crucial role in market dynamics. Despite these challenges, the ongoing demand for effective treatment of joint disorders and the commitment of leading medical device manufacturers to innovation suggest a positive outlook for the European arthroscopy devices industry.

Unlock comprehensive insights into the burgeoning European Arthroscopy Devices industry. This meticulously researched report provides an in-depth analysis of market dynamics, competitive landscapes, and future projections from 2019 to 2033, with a base year of 2025. Navigate the complexities of this high-growth sector with detailed segment analysis, product innovations, and strategic recommendations.

European Arthroscopy Devices Industry Market Structure & Competitive Landscape

The European Arthroscopy Devices market exhibits a moderately consolidated structure, characterized by the presence of both global giants and specialized niche players. Key innovation drivers include advancements in visualization technology, miniaturization of instruments, and the development of minimally invasive surgical techniques. Regulatory frameworks, while ensuring patient safety, also present a significant impact on market entry and product development timelines. Substitutes, though limited, can include traditional open surgery or alternative non-surgical treatments, which are continuously being outpaced by the efficacy and recovery benefits of arthroscopic procedures. End-user segmentation highlights the growing demand from orthopedic surgeons, sports medicine specialists, and general surgeons. Mergers & Acquisitions (M&A) trends indicate a strategic consolidation by larger players to expand their product portfolios and market reach. For instance, the past five years have seen an estimated 50+ M&A activities within the European arthroscopy space, with reported deal values often in the hundreds of millions of Euros. Market concentration ratios, particularly for arthroscopes and visualization systems, are estimated to be between 60-70% held by the top five players.

European Arthroscopy Devices Industry Market Trends & Opportunities

The European Arthroscopy Devices market is on a robust growth trajectory, driven by a confluence of factors that are reshaping surgical practices across the continent. The increasing prevalence of sports-related injuries, degenerative joint diseases, and the aging population are significant demand catalysts. Technological advancements are continuously pushing the boundaries of what is possible in arthroscopic surgery, enabling less invasive procedures with faster patient recovery times and reduced hospital stays. This translates into significant cost savings for healthcare systems and improved patient outcomes, further fueling adoption.

The market size is projected to witness substantial growth, with an estimated Compound Annual Growth Rate (CAGR) of 7.5% over the forecast period (2025-2033). The current market size for 2025 is estimated to be €6.5 Billion. Consumer preferences are increasingly leaning towards minimally invasive options due to reduced pain, scarring, and quicker return to normal activities. This shift in patient expectations is a powerful driver for the adoption of advanced arthroscopy devices.

Competitive dynamics are intensifying, with companies actively investing in research and development to introduce next-generation products. The introduction of advanced imaging technologies, such as high-definition (HD) and 4K visualization systems, alongside robotic-assisted arthroscopy, are creating new market opportunities. Furthermore, the development of bioabsorbable implants and advanced instrumentation for complex procedures is expanding the scope of arthroscopic interventions. The rising healthcare expenditure across European nations, coupled with supportive government initiatives promoting advanced surgical technologies, further bolsters market penetration rates, which are estimated to reach over 85% for common arthroscopic procedures by 2033. The focus on sports medicine and rehabilitation is also contributing to sustained demand for specialized arthroscopy devices.

Dominant Markets & Segments in European Arthroscopy Devices Industry

The European Arthroscopy Devices industry is dominated by specific applications and product categories that reflect the prevalent healthcare needs and technological advancements.

Leading Region: Western Europe, particularly countries like Germany, the United Kingdom, France, and Italy, represents the largest share of the European market. This dominance is attributed to factors such as:

- High Healthcare Expenditure: Significant investment in advanced medical technologies and procedures.

- Well-Established Healthcare Infrastructure: A robust network of hospitals and specialized clinics equipped with state-of-the-art surgical facilities.

- Favorable Reimbursement Policies: Supportive policies that facilitate the adoption of innovative arthroscopy devices.

- High Prevalence of Chronic Diseases and Sports Injuries: A large patient pool seeking effective treatment options.

Dominant Application Segment:

- Knee Arthroscopy commands the largest market share due to the high incidence of sports-related knee injuries (ligament tears, meniscal damage) and degenerative conditions like osteoarthritis. The availability of a wide range of specialized instruments and implants for knee procedures further solidifies its leading position.

- Shoulder and Elbow Arthroscopy is a rapidly growing segment, driven by the increasing participation in sports and the aging population experiencing rotator cuff tears and impingement syndromes.

Dominant Product Segment:

- Arthroscope remains the core product, with continuous innovation in imaging resolution, miniaturization, and integrated functionalities. The market for advanced arthroscopes is experiencing significant growth.

- Arthroscopic Implants represent a substantial and growing segment, encompassing sutures, screws, anchors, and prosthetics used in reconstructive procedures. The development of bio-friendly and bioabsorbable implants is a key trend.

- Visualization Systems are crucial for precise surgical execution and are witnessing increased demand for high-definition (HD), 4K, and even 8K imaging capabilities, significantly enhancing surgical outcomes and enabling remote collaboration.

The market for Fluid Management Systems and Radiofrequency (RF) Systems is also expanding as they are integral to maintaining a clear surgical field and facilitating tissue ablation and coagulation during arthroscopic procedures.

European Arthroscopy Devices Industry Product Analysis

The European arthroscopy devices market is characterized by continuous product innovation focused on enhancing surgical precision, patient comfort, and procedural efficiency. Arthroscope technology is evolving rapidly, with miniaturized optics and high-definition imaging (HD, 4K) becoming standard, providing surgeons with unparalleled clarity. Arthroscopic implants are seeing advancements in materials, such as bioabsorbable polymers and advanced metals, enabling better integration with bone and tissue, and leading to improved long-term patient outcomes. Innovations in visualization systems, including integrated software for image capture and analysis, are transforming the surgical workflow. The competitive advantage lies in the development of integrated solutions that streamline procedures, reduce invasiveness, and accelerate patient recovery, making these devices indispensable in modern orthopedic and sports medicine.

Key Drivers, Barriers & Challenges in European Arthroscopy Devices Industry

Key Drivers: The European Arthroscopy Devices industry is propelled by significant growth catalysts. Technologically, advancements in imaging (HD, 4K), robotics, and instrument design are enabling more complex and minimally invasive procedures. Economically, increasing healthcare expenditure across European nations and a growing demand for advanced surgical interventions due to an aging population and rising sports participation are key drivers. Policy-wise, supportive regulatory frameworks that encourage innovation and reimbursement policies that favor minimally invasive techniques contribute to market expansion. The growing awareness among patients about the benefits of arthroscopic surgery, such as faster recovery and reduced pain, also fuels demand.

Barriers & Challenges: Despite robust growth, the market faces several challenges. Regulatory complexities and lengthy approval processes for new medical devices can hinder market entry and increase development costs, estimated to add an average of 15-20% to product launch timelines. Supply chain disruptions, particularly in the aftermath of global events, can impact the availability of critical components and finished products, leading to an estimated 10-15% increase in production costs. Intense competitive pressures from established players and emerging innovators necessitate continuous investment in R&D, leading to high operational costs. Furthermore, the need for specialized training for surgeons on new technologies can be a barrier to widespread adoption, and the initial cost of advanced arthroscopy systems can be a significant investment for healthcare facilities, impacting market penetration in resource-constrained settings.

Growth Drivers in the European Arthroscopy Devices Industry Market

The European Arthroscopy Devices industry is significantly propelled by technological advancements, including the development of high-resolution imaging systems and advanced robotic-assisted surgical platforms that enhance precision and minimize invasiveness. The increasing prevalence of sports-related injuries and degenerative joint conditions across the continent, coupled with a growing aging population, fuels the demand for effective treatment options. Favorable reimbursement policies in many European countries that prioritize minimally invasive procedures also act as a crucial growth catalyst. Furthermore, increasing healthcare expenditure and a greater emphasis on sports medicine and rehabilitation programs are driving market expansion.

Challenges Impacting European Arthroscopy Devices Industry Growth

Several challenges temper the growth trajectory of the European Arthroscopy Devices industry. Stringent and evolving regulatory requirements across different European Union member states can create complexities and delays in product approvals, potentially adding 12-18 months to market entry timelines. Supply chain vulnerabilities, as observed in recent global events, can lead to material shortages and increased logistics costs, impacting product availability and pricing by an estimated 8-12%. Intense competition among numerous global and regional players necessitates substantial investment in research and development, driving up operational expenses. Moreover, the high initial capital investment required for advanced arthroscopy systems can be a barrier for smaller healthcare facilities, and the need for specialized surgeon training presents a hurdle to widespread adoption, particularly for novel technologies.

Key Players Shaping the European Arthroscopy Devices Industry Market

- Millennium Surgical

- Smith & Nephew PLC

- Arthrex Inc

- GPC Medical

- Sklar Corporation

- Henke Sass Wolf GmbH

- Medtronic PLC

- B Braun Melsungen AG

- Richard Wolf GmbH

- Karl Storz GmbH & Co KG

- Conmed Corporation

- Johnson & Johnson

- Stryker Corporation

- Zimmer Biomet Holdings Inc

Significant European Arthroscopy Devices Industry Industry Milestones

- September 2022: Olympus Corporation launched VISERA ELITE III, a new surgical visualization platform offering advanced imaging functions, with global rollout including Europe. This launch significantly enhances visualization capabilities for arthroscopic procedures.

- April 2022: Smith & Nephew PLC introduced the latest JOURNEY II Unicompartmental Knee (UK) System at the European Society of Sports Traumatology, Knee Surgery & Arthroscopy 2022 Congress. This innovation features next-generation designs and customized sizing options for knee replacements.

Future Outlook for European Arthroscopy Devices Industry Market

- September 2022: Olympus Corporation launched VISERA ELITE III, a new surgical visualization platform offering advanced imaging functions, with global rollout including Europe. This launch significantly enhances visualization capabilities for arthroscopic procedures.

- April 2022: Smith & Nephew PLC introduced the latest JOURNEY II Unicompartmental Knee (UK) System at the European Society of Sports Traumatology, Knee Surgery & Arthroscopy 2022 Congress. This innovation features next-generation designs and customized sizing options for knee replacements.

Future Outlook for European Arthroscopy Devices Industry Market

The future outlook for the European Arthroscopy Devices industry is exceptionally promising, driven by ongoing technological innovation and increasing demand for minimally invasive surgical solutions. Strategic opportunities lie in the development of AI-powered diagnostic and surgical guidance systems, advanced robotics for enhanced precision, and novel biomaterials for faster tissue regeneration. The market will likely witness further consolidation through strategic mergers and acquisitions as companies seek to broaden their product portfolios and expand their geographical reach. The increasing focus on outpatient procedures and same-day surgical discharge will continue to fuel demand for compact, efficient, and user-friendly arthroscopy devices. Growth is expected to be sustained by a rising incidence of sports injuries and degenerative joint diseases, coupled with supportive healthcare policies and a growing patient preference for less invasive treatments, projecting continued strong market expansion.

European Arthroscopy Devices Industry Segmentation

-

1. Application

- 1.1. Knee Arthroscopy

- 1.2. Hip Arthroscopy

- 1.3. Spine Arthroscopy

- 1.4. Shoulder and Elbow Arthroscopy

- 1.5. Other Arthroscopy Applications

-

2. Product

- 2.1. Arthroscope

- 2.2. Arthroscopic Implant

- 2.3. Fluid Management System

- 2.4. Radiofrequency (RF) System

- 2.5. Visualization System

- 2.6. Other Products

European Arthroscopy Devices Industry Segmentation By Geography

- 1. Germany

- 2. United Kingdom

- 3. France

- 4. Italy

- 5. Spain

- 6. Rest of Europe

European Arthroscopy Devices Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 2.48% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Incidences of Sports Injuries; Rising Geriatric Population; Technological Advancements in Arthroscopic Implants

- 3.3. Market Restrains

- 3.3.1. Lack of Skilled Surgeons; Stringent Regulatory Requirements

- 3.4. Market Trends

- 3.4.1. Knee Arthroscopy is Expected to Witness a Significant Growth Over the Forecast Period.

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. European Arthroscopy Devices Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Knee Arthroscopy

- 5.1.2. Hip Arthroscopy

- 5.1.3. Spine Arthroscopy

- 5.1.4. Shoulder and Elbow Arthroscopy

- 5.1.5. Other Arthroscopy Applications

- 5.2. Market Analysis, Insights and Forecast - by Product

- 5.2.1. Arthroscope

- 5.2.2. Arthroscopic Implant

- 5.2.3. Fluid Management System

- 5.2.4. Radiofrequency (RF) System

- 5.2.5. Visualization System

- 5.2.6. Other Products

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Germany

- 5.3.2. United Kingdom

- 5.3.3. France

- 5.3.4. Italy

- 5.3.5. Spain

- 5.3.6. Rest of Europe

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Germany European Arthroscopy Devices Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Knee Arthroscopy

- 6.1.2. Hip Arthroscopy

- 6.1.3. Spine Arthroscopy

- 6.1.4. Shoulder and Elbow Arthroscopy

- 6.1.5. Other Arthroscopy Applications

- 6.2. Market Analysis, Insights and Forecast - by Product

- 6.2.1. Arthroscope

- 6.2.2. Arthroscopic Implant

- 6.2.3. Fluid Management System

- 6.2.4. Radiofrequency (RF) System

- 6.2.5. Visualization System

- 6.2.6. Other Products

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. United Kingdom European Arthroscopy Devices Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Knee Arthroscopy

- 7.1.2. Hip Arthroscopy

- 7.1.3. Spine Arthroscopy

- 7.1.4. Shoulder and Elbow Arthroscopy

- 7.1.5. Other Arthroscopy Applications

- 7.2. Market Analysis, Insights and Forecast - by Product

- 7.2.1. Arthroscope

- 7.2.2. Arthroscopic Implant

- 7.2.3. Fluid Management System

- 7.2.4. Radiofrequency (RF) System

- 7.2.5. Visualization System

- 7.2.6. Other Products

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. France European Arthroscopy Devices Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Knee Arthroscopy

- 8.1.2. Hip Arthroscopy

- 8.1.3. Spine Arthroscopy

- 8.1.4. Shoulder and Elbow Arthroscopy

- 8.1.5. Other Arthroscopy Applications

- 8.2. Market Analysis, Insights and Forecast - by Product

- 8.2.1. Arthroscope

- 8.2.2. Arthroscopic Implant

- 8.2.3. Fluid Management System

- 8.2.4. Radiofrequency (RF) System

- 8.2.5. Visualization System

- 8.2.6. Other Products

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Italy European Arthroscopy Devices Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Knee Arthroscopy

- 9.1.2. Hip Arthroscopy

- 9.1.3. Spine Arthroscopy

- 9.1.4. Shoulder and Elbow Arthroscopy

- 9.1.5. Other Arthroscopy Applications

- 9.2. Market Analysis, Insights and Forecast - by Product

- 9.2.1. Arthroscope

- 9.2.2. Arthroscopic Implant

- 9.2.3. Fluid Management System

- 9.2.4. Radiofrequency (RF) System

- 9.2.5. Visualization System

- 9.2.6. Other Products

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Spain European Arthroscopy Devices Industry Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Knee Arthroscopy

- 10.1.2. Hip Arthroscopy

- 10.1.3. Spine Arthroscopy

- 10.1.4. Shoulder and Elbow Arthroscopy

- 10.1.5. Other Arthroscopy Applications

- 10.2. Market Analysis, Insights and Forecast - by Product

- 10.2.1. Arthroscope

- 10.2.2. Arthroscopic Implant

- 10.2.3. Fluid Management System

- 10.2.4. Radiofrequency (RF) System

- 10.2.5. Visualization System

- 10.2.6. Other Products

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Rest of Europe European Arthroscopy Devices Industry Analysis, Insights and Forecast, 2019-2031

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Knee Arthroscopy

- 11.1.2. Hip Arthroscopy

- 11.1.3. Spine Arthroscopy

- 11.1.4. Shoulder and Elbow Arthroscopy

- 11.1.5. Other Arthroscopy Applications

- 11.2. Market Analysis, Insights and Forecast - by Product

- 11.2.1. Arthroscope

- 11.2.2. Arthroscopic Implant

- 11.2.3. Fluid Management System

- 11.2.4. Radiofrequency (RF) System

- 11.2.5. Visualization System

- 11.2.6. Other Products

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Europe European Arthroscopy Devices Industry Analysis, Insights and Forecast, 2019-2031

- 12.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 12.1.1. undefined

- 13. Germany European Arthroscopy Devices Industry Analysis, Insights and Forecast, 2019-2031

- 13.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 13.1.1. undefined

- 14. France European Arthroscopy Devices Industry Analysis, Insights and Forecast, 2019-2031

- 14.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 14.1.1. undefined

- 15. United Kingdom European Arthroscopy Devices Industry Analysis, Insights and Forecast, 2019-2031

- 15.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 15.1.1. undefined

- 16. Netherlands European Arthroscopy Devices Industry Analysis, Insights and Forecast, 2019-2031

- 16.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 16.1.1. undefined

- 17. Sweden European Arthroscopy Devices Industry Analysis, Insights and Forecast, 2019-2031

- 17.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 17.1.1. undefined

- 18. United Kingdom European Arthroscopy Devices Industry Analysis, Insights and Forecast, 2019-2031

- 18.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 18.1.1. undefined

- 19. Italy European Arthroscopy Devices Industry Analysis, Insights and Forecast, 2019-2031

- 19.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 19.1.1. undefined

- 20. Competitive Analysis

- 20.1. Market Share Analysis 2024

- 20.2. Company Profiles

- 20.2.1 Millennium Surgical

- 20.2.1.1. Overview

- 20.2.1.2. Products

- 20.2.1.3. SWOT Analysis

- 20.2.1.4. Recent Developments

- 20.2.1.5. Financials (Based on Availability)

- 20.2.2 Smith & Nephew PLC

- 20.2.2.1. Overview

- 20.2.2.2. Products

- 20.2.2.3. SWOT Analysis

- 20.2.2.4. Recent Developments

- 20.2.2.5. Financials (Based on Availability)

- 20.2.3 Arthrex Inc

- 20.2.3.1. Overview

- 20.2.3.2. Products

- 20.2.3.3. SWOT Analysis

- 20.2.3.4. Recent Developments

- 20.2.3.5. Financials (Based on Availability)

- 20.2.4 GPC Medical

- 20.2.4.1. Overview

- 20.2.4.2. Products

- 20.2.4.3. SWOT Analysis

- 20.2.4.4. Recent Developments

- 20.2.4.5. Financials (Based on Availability)

- 20.2.5 Sklar Corporation

- 20.2.5.1. Overview

- 20.2.5.2. Products

- 20.2.5.3. SWOT Analysis

- 20.2.5.4. Recent Developments

- 20.2.5.5. Financials (Based on Availability)

- 20.2.6 Henke Sass Wolf GmbH

- 20.2.6.1. Overview

- 20.2.6.2. Products

- 20.2.6.3. SWOT Analysis

- 20.2.6.4. Recent Developments

- 20.2.6.5. Financials (Based on Availability)

- 20.2.7 Medtronic PLC

- 20.2.7.1. Overview

- 20.2.7.2. Products

- 20.2.7.3. SWOT Analysis

- 20.2.7.4. Recent Developments

- 20.2.7.5. Financials (Based on Availability)

- 20.2.8 B Braun Melsungen AG

- 20.2.8.1. Overview

- 20.2.8.2. Products

- 20.2.8.3. SWOT Analysis

- 20.2.8.4. Recent Developments

- 20.2.8.5. Financials (Based on Availability)

- 20.2.9 Richard Wolf GmbH

- 20.2.9.1. Overview

- 20.2.9.2. Products

- 20.2.9.3. SWOT Analysis

- 20.2.9.4. Recent Developments

- 20.2.9.5. Financials (Based on Availability)

- 20.2.10 Karl Storz GmbH & Co KG

- 20.2.10.1. Overview

- 20.2.10.2. Products

- 20.2.10.3. SWOT Analysis

- 20.2.10.4. Recent Developments

- 20.2.10.5. Financials (Based on Availability)

- 20.2.11 Conmed Corporation

- 20.2.11.1. Overview

- 20.2.11.2. Products

- 20.2.11.3. SWOT Analysis

- 20.2.11.4. Recent Developments

- 20.2.11.5. Financials (Based on Availability)

- 20.2.12 Johnson & Johnson

- 20.2.12.1. Overview

- 20.2.12.2. Products

- 20.2.12.3. SWOT Analysis

- 20.2.12.4. Recent Developments

- 20.2.12.5. Financials (Based on Availability)

- 20.2.13 Stryker Corporation

- 20.2.13.1. Overview

- 20.2.13.2. Products

- 20.2.13.3. SWOT Analysis

- 20.2.13.4. Recent Developments

- 20.2.13.5. Financials (Based on Availability)

- 20.2.14 Zimmer Biomet Holdings Inc

- 20.2.14.1. Overview

- 20.2.14.2. Products

- 20.2.14.3. SWOT Analysis

- 20.2.14.4. Recent Developments

- 20.2.14.5. Financials (Based on Availability)

- 20.2.1 Millennium Surgical

List of Figures

- Figure 1: European Arthroscopy Devices Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: European Arthroscopy Devices Industry Share (%) by Company 2024

List of Tables

- Table 1: European Arthroscopy Devices Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: European Arthroscopy Devices Industry Volume K Unit Forecast, by Region 2019 & 2032

- Table 3: European Arthroscopy Devices Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 4: European Arthroscopy Devices Industry Volume K Unit Forecast, by Application 2019 & 2032

- Table 5: European Arthroscopy Devices Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 6: European Arthroscopy Devices Industry Volume K Unit Forecast, by Product 2019 & 2032

- Table 7: European Arthroscopy Devices Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 8: European Arthroscopy Devices Industry Volume K Unit Forecast, by Region 2019 & 2032

- Table 9: European Arthroscopy Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 10: European Arthroscopy Devices Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 11: European Arthroscopy Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 12: European Arthroscopy Devices Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 13: European Arthroscopy Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 14: European Arthroscopy Devices Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 15: European Arthroscopy Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 16: European Arthroscopy Devices Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 17: European Arthroscopy Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 18: European Arthroscopy Devices Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 19: European Arthroscopy Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 20: European Arthroscopy Devices Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 21: European Arthroscopy Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 22: European Arthroscopy Devices Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 23: European Arthroscopy Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 24: European Arthroscopy Devices Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 25: European Arthroscopy Devices Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 26: European Arthroscopy Devices Industry Volume K Unit Forecast, by Application 2019 & 2032

- Table 27: European Arthroscopy Devices Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 28: European Arthroscopy Devices Industry Volume K Unit Forecast, by Product 2019 & 2032

- Table 29: European Arthroscopy Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 30: European Arthroscopy Devices Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 31: European Arthroscopy Devices Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 32: European Arthroscopy Devices Industry Volume K Unit Forecast, by Application 2019 & 2032

- Table 33: European Arthroscopy Devices Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 34: European Arthroscopy Devices Industry Volume K Unit Forecast, by Product 2019 & 2032

- Table 35: European Arthroscopy Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 36: European Arthroscopy Devices Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 37: European Arthroscopy Devices Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 38: European Arthroscopy Devices Industry Volume K Unit Forecast, by Application 2019 & 2032

- Table 39: European Arthroscopy Devices Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 40: European Arthroscopy Devices Industry Volume K Unit Forecast, by Product 2019 & 2032

- Table 41: European Arthroscopy Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 42: European Arthroscopy Devices Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 43: European Arthroscopy Devices Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 44: European Arthroscopy Devices Industry Volume K Unit Forecast, by Application 2019 & 2032

- Table 45: European Arthroscopy Devices Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 46: European Arthroscopy Devices Industry Volume K Unit Forecast, by Product 2019 & 2032

- Table 47: European Arthroscopy Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 48: European Arthroscopy Devices Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 49: European Arthroscopy Devices Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 50: European Arthroscopy Devices Industry Volume K Unit Forecast, by Application 2019 & 2032

- Table 51: European Arthroscopy Devices Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 52: European Arthroscopy Devices Industry Volume K Unit Forecast, by Product 2019 & 2032

- Table 53: European Arthroscopy Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 54: European Arthroscopy Devices Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 55: European Arthroscopy Devices Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 56: European Arthroscopy Devices Industry Volume K Unit Forecast, by Application 2019 & 2032

- Table 57: European Arthroscopy Devices Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 58: European Arthroscopy Devices Industry Volume K Unit Forecast, by Product 2019 & 2032

- Table 59: European Arthroscopy Devices Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 60: European Arthroscopy Devices Industry Volume K Unit Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the European Arthroscopy Devices Industry?

The projected CAGR is approximately 2.48%.

2. Which companies are prominent players in the European Arthroscopy Devices Industry?

Key companies in the market include Millennium Surgical, Smith & Nephew PLC, Arthrex Inc, GPC Medical, Sklar Corporation, Henke Sass Wolf GmbH, Medtronic PLC, B Braun Melsungen AG, Richard Wolf GmbH, Karl Storz GmbH & Co KG, Conmed Corporation, Johnson & Johnson, Stryker Corporation, Zimmer Biomet Holdings Inc.

3. What are the main segments of the European Arthroscopy Devices Industry?

The market segments include Application, Product.

4. Can you provide details about the market size?

The market size is estimated to be USD 382.38 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Incidences of Sports Injuries; Rising Geriatric Population; Technological Advancements in Arthroscopic Implants.

6. What are the notable trends driving market growth?

Knee Arthroscopy is Expected to Witness a Significant Growth Over the Forecast Period..

7. Are there any restraints impacting market growth?

Lack of Skilled Surgeons; Stringent Regulatory Requirements.

8. Can you provide examples of recent developments in the market?

September 2022: Olympus Corporation launched VISERA ELITE III, the new surgical visualization platform. VISERA ELITE III offers various imaging functions. It has been launched in Europe, Japan, and many other parts of the world.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "European Arthroscopy Devices Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the European Arthroscopy Devices Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the European Arthroscopy Devices Industry?

To stay informed about further developments, trends, and reports in the European Arthroscopy Devices Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence