Key Insights

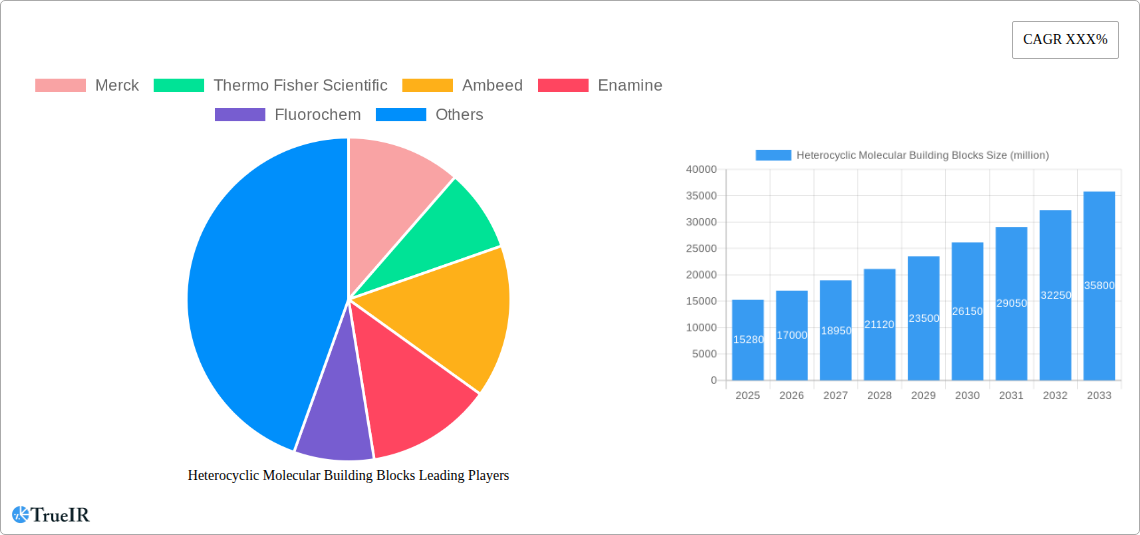

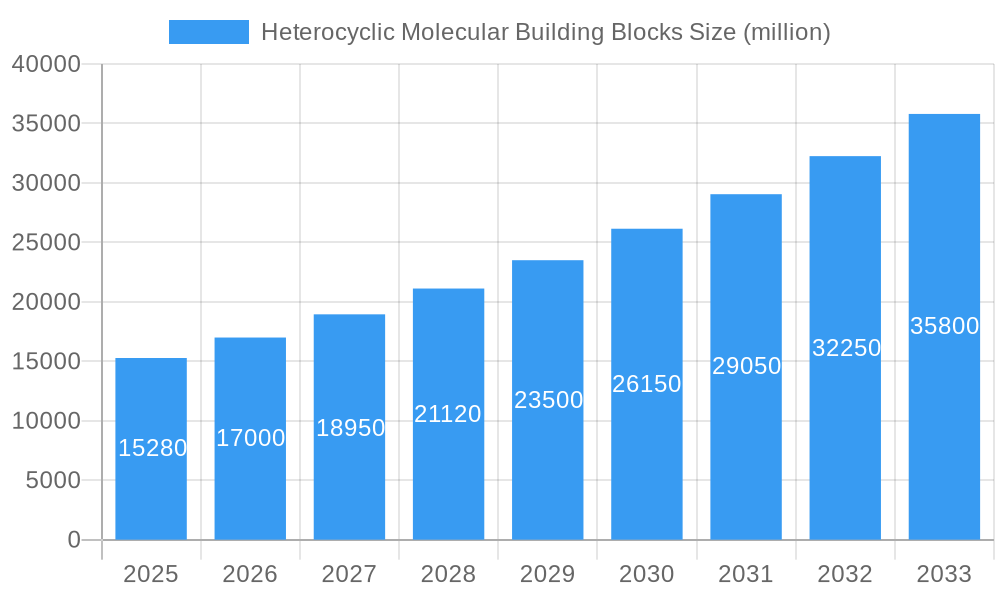

The global market for Heterocyclic Molecular Building Blocks is experiencing robust growth, projected to reach an estimated $15.28 billion in 2025, driven by a compelling CAGR of 11.2% over the forecast period. This expansion is primarily fueled by the increasing demand for innovative drug discovery and development across the pharmaceutical and biotechnology sectors. Specifically, the application segments of "Screening Seedling Compounds," "Modified Lead Compound," and "Optimize Preclinical Candidate Compounds" are witnessing significant traction as researchers explore novel therapeutic targets and accelerate the preclinical pipeline. The development of novel small molecules for drug discovery is a critical component in addressing unmet medical needs, and heterocyclic compounds, with their diverse structural possibilities, are central to this endeavor.

Heterocyclic Molecular Building Blocks Market Size (In Billion)

The market is further propelled by the ongoing advancements in synthetic chemistry and the growing adoption of high-throughput screening technologies. Key trends include a surge in the development of specialized aromatic and non-aromatic heterocyclic molecular building blocks, catering to the intricate requirements of modern drug design. While the market demonstrates strong growth potential, certain restraints, such as the complex regulatory landscape for new drug approvals and the high cost associated with R&D, may pose challenges. Nevertheless, the substantial investment in pharmaceutical R&D, coupled with the growing prevalence of chronic diseases globally, is expected to sustain the upward trajectory of the Heterocyclic Molecular Building Blocks market, with significant opportunities anticipated in regions like Asia Pacific, driven by the burgeoning pharmaceutical industry in China and India.

Heterocyclic Molecular Building Blocks Company Market Share

Here is a dynamic, SEO-optimized report description for Heterocyclic Molecular Building Blocks, designed for immediate use without modification.

Heterocyclic Molecular Building Blocks Market Structure & Competitive Landscape

The global heterocyclic molecular building blocks market, valued at an estimated XX billion in 2025, exhibits a dynamic and evolving competitive landscape. Market concentration is moderately high, with leading players investing significantly in research and development to drive innovation. Key innovation drivers include the increasing demand for novel therapeutics in oncology, infectious diseases, and neurological disorders, fueling the development of more complex and diverse heterocyclic structures. Regulatory impacts, while stringent, also foster innovation by encouraging the development of compliant and high-purity building blocks. Product substitutes, primarily other chemical scaffolds, exist but are often outcompeted by the unique reactivity and biological activity offered by heterocycles. End-user segmentation is dominated by pharmaceutical and biotechnology companies, with smaller contributions from agrochemical and material science sectors. Mergers and acquisitions (M&A) remain a significant trend, with an estimated XX billion in M&A activity observed between 2019 and 2024, as larger entities seek to consolidate their portfolios and gain access to specialized building block libraries. Key companies actively participating in M&A include Merck, Thermo Fisher Scientific, and Enamine, underscoring the strategic importance of these acquisitions for market expansion and technological advancement.

Heterocyclic Molecular Building Blocks Market Trends & Opportunities

The global heterocyclic molecular building blocks market is projected for robust growth, with an estimated market size projected to reach XX billion by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of approximately XX% during the forecast period of 2025–2033. This significant expansion is propelled by a confluence of technological advancements, evolving consumer preferences, and shifting competitive dynamics. The increasing complexity of drug discovery pipelines, particularly in the realm of precision medicine and targeted therapies, necessitates a broader and more sophisticated array of heterocyclic building blocks. Pharmaceutical and biotechnology companies are increasingly relying on these specialized molecules for screening seedling compounds, modifying lead compounds to enhance efficacy and reduce toxicity, optimizing preclinical candidate compounds for improved pharmacokinetic and pharmacodynamic profiles, and ultimately identifying viable clinical candidates. The market penetration of advanced heterocyclic building blocks is steadily rising as researchers gain a deeper understanding of their structure-activity relationships and their ability to confer desirable biological properties.

Technological shifts are playing a pivotal role in shaping market trends. Innovations in synthetic methodologies, including flow chemistry, biocatalysis, and high-throughput synthesis, are enabling the more efficient and cost-effective production of a wider range of heterocyclic scaffolds. This has led to the emergence of novel and complex heterocyclic motifs with previously unattainable functionalities, opening up new avenues for drug discovery. Furthermore, advancements in computational chemistry and AI-driven drug design are accelerating the identification of promising heterocyclic structures, thereby driving demand for their synthesis and availability.

Consumer preferences, primarily driven by the pharmaceutical industry's pursuit of novel and effective treatments for unmet medical needs, are leaning towards building blocks that offer greater structural diversity and specific biological activities. The demand for functionalized heterocycles, chiral building blocks, and those incorporating fluorine or other halogens is on the rise due to their proven ability to enhance drug potency, metabolic stability, and bioavailability.

The competitive landscape is characterized by increasing collaboration and strategic partnerships between building block suppliers and pharmaceutical research organizations. Companies are investing in expanding their product portfolios and developing custom synthesis capabilities to cater to the specific needs of drug discovery programs. The trend towards outsourcing R&D activities also creates opportunities for specialized building block providers to offer integrated services, from library design to custom synthesis. The growing emphasis on sustainable chemistry and green synthesis practices is also influencing market trends, with a growing preference for suppliers who adopt environmentally friendly manufacturing processes.

Dominant Markets & Segments in Heterocyclic Molecular Building Blocks

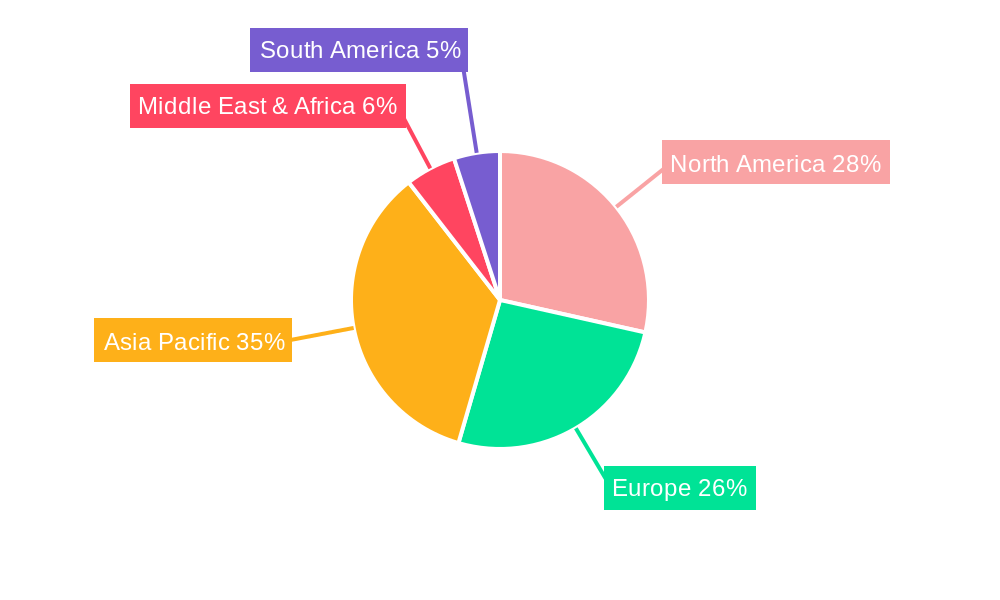

The global heterocyclic molecular building blocks market is characterized by the dominance of certain regions and segments driven by substantial research and development investments, favorable regulatory environments, and robust pharmaceutical and biotechnology industries. North America, particularly the United States, remains a leading region due to its extensive network of research institutions, a high concentration of pharmaceutical giants, and significant government funding for life sciences research. Asia Pacific, spearheaded by China and India, is experiencing rapid growth driven by the expansion of their domestic pharmaceutical industries, increasing contract research organization (CRO) activities, and a growing focus on innovation.

Within the application segment, Screening Seedling Compounds and Modified Lead Compound represent the largest and most rapidly growing categories. This dominance is attributed to the early-stage nature of these applications in the drug discovery pipeline. Pharmaceutical companies constantly require a diverse and extensive library of heterocyclic building blocks to identify novel therapeutic targets and explore initial drug candidates. The ability of heterocyclic structures to interact with a vast array of biological targets makes them indispensable for hit identification and lead generation.

Analyzing the Type segment, Aromatic Heterocyclic Molecular Building Blocks currently hold a larger market share. This is due to their well-established synthetic routes, extensive literature precedent, and broad applicability across various therapeutic areas. Compounds like pyridines, pyrimidines, indoles, and quinolines are foundational in many drug discovery programs. However, the demand for Non-aromatic Heterocyclic Molecular Building Blocks is rapidly gaining momentum. The unique three-dimensional structures and conformational flexibility offered by saturated and partially saturated heterocycles are proving invaluable in overcoming drug resistance, improving target selectivity, and enhancing pharmacokinetic properties.

Key growth drivers contributing to the dominance of specific markets and segments include:

- Infrastructure: Robust research infrastructure, including advanced synthesis laboratories, high-throughput screening facilities, and analytical instrumentation, is crucial for both the development and utilization of heterocyclic building blocks. Regions with well-established R&D ecosystems attract significant investment and foster innovation.

- Policies: Favorable government policies, such as tax incentives for R&D, intellectual property protection, and streamlined regulatory approval processes for new drugs, significantly influence market growth. These policies encourage pharmaceutical companies to invest more heavily in drug discovery, thereby boosting the demand for building blocks.

- Investment in R&D: High levels of investment in pharmaceutical and biotechnology R&D directly translate to increased demand for a diverse range of chemical building blocks. Companies are allocating substantial budgets to explore new therapeutic modalities, which often rely on novel heterocyclic scaffolds.

- Emergence of CROs: The proliferation of Contract Research Organizations (CROs) in regions like Asia Pacific has democratized access to drug discovery services, thereby increasing the overall demand for specialized chemical reagents like heterocyclic building blocks from a wider base of research entities.

The interplay of these factors creates a dynamic market where both established and emerging players have opportunities to capitalize on the growing need for innovative heterocyclic molecular building blocks.

Heterocyclic Molecular Building Blocks Product Analysis

The heterocyclic molecular building blocks market is defined by continuous product innovation, with a focus on developing novel scaffolds with enhanced reactivity, selectivity, and biological activity. Key product innovations include the synthesis of highly functionalized heterocycles, chiral building blocks for stereoselective synthesis, and macrocyclic and spirocyclic systems offering unique three-dimensional architectures. These advancements are driven by the increasing demand for targeted therapies and the need to overcome challenges in drug resistance and off-target effects. The primary applications of these building blocks span the entire drug discovery spectrum, from initial hit identification to the optimization of clinical candidates. Competitive advantages lie in the purity, diversity, and scalability of synthesis, enabling researchers to accelerate their development timelines.

Key Drivers, Barriers & Challenges in Heterocyclic Molecular Building Blocks

The heterocyclic molecular building blocks market is propelled by several key drivers, including the relentless pursuit of novel therapeutics by the pharmaceutical industry to address unmet medical needs, particularly in oncology, neurology, and infectious diseases. Technological advancements in synthetic chemistry, such as flow chemistry and photocatalysis, enable the efficient and cost-effective production of complex heterocyclic structures, expanding their accessibility. Furthermore, the growing trend of outsourcing drug discovery and development activities to CROs fuels demand for specialized building blocks.

However, the market faces significant barriers and challenges. Stringent regulatory requirements for drug development and manufacturing necessitate high-purity and well-characterized building blocks, increasing production costs. Supply chain disruptions, exacerbated by global events, can impact the availability and lead times of raw materials and intermediates, leading to price volatility, estimated at XX% increase in raw material costs during the historical period. Intense competition among established and emerging suppliers leads to price pressures, requiring continuous innovation and cost optimization. The development of complex and novel heterocyclic structures can be time-consuming and resource-intensive, posing a challenge to smaller companies.

Growth Drivers in the Heterocyclic Molecular Building Blocks Market

The growth of the heterocyclic molecular building blocks market is primarily driven by the escalating global demand for novel pharmaceuticals to combat a wide spectrum of diseases. Technological innovations in synthetic methodologies, such as green chemistry approaches and high-throughput synthesis, are making it more efficient and cost-effective to produce a diverse range of heterocyclic scaffolds. Economic factors, including increased R&D expenditure by pharmaceutical companies and government initiatives supporting drug discovery, also play a crucial role. Policy-driven support for biopharmaceutical research and development, coupled with favorable intellectual property protection laws, further stimulates investment and innovation in this sector, creating a fertile ground for the expansion of the building blocks market.

Challenges Impacting Heterocyclic Molecular Building Blocks Growth

Challenges impacting the growth of the heterocyclic molecular building blocks market are multifaceted. Stringent regulatory compliance and quality control standards for pharmaceutical intermediates necessitate significant investment in validation and documentation, adding to production costs, with an estimated XX% increase in compliance-related expenses. Supply chain vulnerabilities, including the reliance on specific raw material suppliers and geopolitical instabilities, can lead to material shortages and price fluctuations, impacting lead times by an average of XX weeks. Intense competition within the market can exert downward pressure on pricing, making it difficult for smaller players to compete without significant differentiation. Furthermore, the intricate synthesis pathways for novel and complex heterocyclic structures can lead to extended development timelines and higher R&D investment requirements.

Key Players Shaping the Heterocyclic Molecular Building Blocks Market

- Merck

- Thermo Fisher Scientific

- Ambeed

- Enamine

- Fluorochem

- Tokyo Chemical Industry

- Shanghai Haoyuan Chemexpress

- Shanghai Bepharm Science&Technology

- Shanghai Haohong scientific

- PharmaBlock Sciences

- Shanghai Ronghe Medical Technology Development

- LinkChem

- Beijing Jinming Biotechnology

- Shanghai Macklin Biochemical

- Shanghai Xian Ding Biotechnology

- Guangzhou Isun Pharmaceutical

Significant Heterocyclic Molecular Building Blocks Industry Milestones

- 2019: Increased adoption of fragment-based drug discovery (FBDD) techniques, driving demand for diverse small-molecule building blocks.

- 2020: Emergence of novel synthetic methodologies like photoredox catalysis, enabling access to previously inaccessible heterocyclic structures.

- 2021: Expansion of custom synthesis services by key players to cater to specific client needs in complex drug discovery programs.

- 2022: Increased focus on sustainable and green chemistry in the production of building blocks.

- 2023: Significant advancements in AI-driven molecule design, accelerating the identification of promising heterocyclic scaffolds for drug development.

- 2024: Growing emphasis on chiral heterocyclic building blocks for stereoselective drug synthesis.

Future Outlook for Heterocyclic Molecular Building Blocks Market

The future outlook for the heterocyclic molecular building blocks market is exceptionally bright, fueled by continuous advancements in drug discovery and development. The increasing complexity of therapeutic targets and the persistent need for novel treatments for diseases like cancer, Alzheimer's, and emerging infectious agents will drive sustained demand for innovative and diverse heterocyclic scaffolds. Emerging trends such as the integration of AI and machine learning in molecular design will accelerate the identification and synthesis of high-value building blocks, further enhancing market growth. Strategic collaborations between building block suppliers and pharmaceutical companies, alongside a focus on sustainable synthesis practices, will define the competitive landscape, promising substantial market expansion and innovation in the years to come.

Heterocyclic Molecular Building Blocks Segmentation

-

1. Application

- 1.1. Screening Seedling Compounds

- 1.2. Modified Lead Compound

- 1.3. Optimize Preclinical Candidate Compounds

- 1.4. Identify Clinical Candidates

-

2. Type

- 2.1. Aromatic Heterocyclic Molecular Building Blocks

- 2.2. Non-aromatic Heterocyclic Molecular Building Blocks

Heterocyclic Molecular Building Blocks Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Heterocyclic Molecular Building Blocks Regional Market Share

Geographic Coverage of Heterocyclic Molecular Building Blocks

Heterocyclic Molecular Building Blocks REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Heterocyclic Molecular Building Blocks Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Screening Seedling Compounds

- 5.1.2. Modified Lead Compound

- 5.1.3. Optimize Preclinical Candidate Compounds

- 5.1.4. Identify Clinical Candidates

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Aromatic Heterocyclic Molecular Building Blocks

- 5.2.2. Non-aromatic Heterocyclic Molecular Building Blocks

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Heterocyclic Molecular Building Blocks Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Screening Seedling Compounds

- 6.1.2. Modified Lead Compound

- 6.1.3. Optimize Preclinical Candidate Compounds

- 6.1.4. Identify Clinical Candidates

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Aromatic Heterocyclic Molecular Building Blocks

- 6.2.2. Non-aromatic Heterocyclic Molecular Building Blocks

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Heterocyclic Molecular Building Blocks Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Screening Seedling Compounds

- 7.1.2. Modified Lead Compound

- 7.1.3. Optimize Preclinical Candidate Compounds

- 7.1.4. Identify Clinical Candidates

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Aromatic Heterocyclic Molecular Building Blocks

- 7.2.2. Non-aromatic Heterocyclic Molecular Building Blocks

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Heterocyclic Molecular Building Blocks Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Screening Seedling Compounds

- 8.1.2. Modified Lead Compound

- 8.1.3. Optimize Preclinical Candidate Compounds

- 8.1.4. Identify Clinical Candidates

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Aromatic Heterocyclic Molecular Building Blocks

- 8.2.2. Non-aromatic Heterocyclic Molecular Building Blocks

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Heterocyclic Molecular Building Blocks Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Screening Seedling Compounds

- 9.1.2. Modified Lead Compound

- 9.1.3. Optimize Preclinical Candidate Compounds

- 9.1.4. Identify Clinical Candidates

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Aromatic Heterocyclic Molecular Building Blocks

- 9.2.2. Non-aromatic Heterocyclic Molecular Building Blocks

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Heterocyclic Molecular Building Blocks Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Screening Seedling Compounds

- 10.1.2. Modified Lead Compound

- 10.1.3. Optimize Preclinical Candidate Compounds

- 10.1.4. Identify Clinical Candidates

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Aromatic Heterocyclic Molecular Building Blocks

- 10.2.2. Non-aromatic Heterocyclic Molecular Building Blocks

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Merck

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Thermo Fisher Scientific

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Ambeed

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Enamine

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Fluorochem

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Tokyo Chemical Industry

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Shanghai Haoyuan Chemexpress

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Shanghai Bepharm Science&Technology

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Shanghai Haohong scientific

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 PharmaBlock Sciences

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Shanghai Ronghe Medical Technology Development

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 LinkChem

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Beijing Jinming Biotechnology

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Shanghai Macklin Biochemical

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Shanghai Xian Ding Biotechnology

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Guangzhou Isun Pharmaceutical

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.1 Merck

List of Figures

- Figure 1: Global Heterocyclic Molecular Building Blocks Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Heterocyclic Molecular Building Blocks Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Heterocyclic Molecular Building Blocks Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Heterocyclic Molecular Building Blocks Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Heterocyclic Molecular Building Blocks Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Heterocyclic Molecular Building Blocks Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Heterocyclic Molecular Building Blocks Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Heterocyclic Molecular Building Blocks Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Heterocyclic Molecular Building Blocks Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Heterocyclic Molecular Building Blocks Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Heterocyclic Molecular Building Blocks Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Heterocyclic Molecular Building Blocks Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Heterocyclic Molecular Building Blocks Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Heterocyclic Molecular Building Blocks Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Heterocyclic Molecular Building Blocks Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Heterocyclic Molecular Building Blocks Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Heterocyclic Molecular Building Blocks Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Heterocyclic Molecular Building Blocks Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Heterocyclic Molecular Building Blocks Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Heterocyclic Molecular Building Blocks Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Heterocyclic Molecular Building Blocks Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Heterocyclic Molecular Building Blocks Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Heterocyclic Molecular Building Blocks Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Heterocyclic Molecular Building Blocks Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Heterocyclic Molecular Building Blocks Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Heterocyclic Molecular Building Blocks Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Heterocyclic Molecular Building Blocks Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Heterocyclic Molecular Building Blocks Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Heterocyclic Molecular Building Blocks Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Heterocyclic Molecular Building Blocks Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Heterocyclic Molecular Building Blocks Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Heterocyclic Molecular Building Blocks Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Heterocyclic Molecular Building Blocks Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Heterocyclic Molecular Building Blocks Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Heterocyclic Molecular Building Blocks Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Heterocyclic Molecular Building Blocks Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Heterocyclic Molecular Building Blocks Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Heterocyclic Molecular Building Blocks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Heterocyclic Molecular Building Blocks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Heterocyclic Molecular Building Blocks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Heterocyclic Molecular Building Blocks Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Heterocyclic Molecular Building Blocks Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Heterocyclic Molecular Building Blocks Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Heterocyclic Molecular Building Blocks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Heterocyclic Molecular Building Blocks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Heterocyclic Molecular Building Blocks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Heterocyclic Molecular Building Blocks Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Heterocyclic Molecular Building Blocks Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Heterocyclic Molecular Building Blocks Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Heterocyclic Molecular Building Blocks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Heterocyclic Molecular Building Blocks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Heterocyclic Molecular Building Blocks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Heterocyclic Molecular Building Blocks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Heterocyclic Molecular Building Blocks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Heterocyclic Molecular Building Blocks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Heterocyclic Molecular Building Blocks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Heterocyclic Molecular Building Blocks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Heterocyclic Molecular Building Blocks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Heterocyclic Molecular Building Blocks Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Heterocyclic Molecular Building Blocks Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Heterocyclic Molecular Building Blocks Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Heterocyclic Molecular Building Blocks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Heterocyclic Molecular Building Blocks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Heterocyclic Molecular Building Blocks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Heterocyclic Molecular Building Blocks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Heterocyclic Molecular Building Blocks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Heterocyclic Molecular Building Blocks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Heterocyclic Molecular Building Blocks Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Heterocyclic Molecular Building Blocks Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Heterocyclic Molecular Building Blocks Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Heterocyclic Molecular Building Blocks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Heterocyclic Molecular Building Blocks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Heterocyclic Molecular Building Blocks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Heterocyclic Molecular Building Blocks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Heterocyclic Molecular Building Blocks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Heterocyclic Molecular Building Blocks Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Heterocyclic Molecular Building Blocks Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Heterocyclic Molecular Building Blocks?

The projected CAGR is approximately 11.2%.

2. Which companies are prominent players in the Heterocyclic Molecular Building Blocks?

Key companies in the market include Merck, Thermo Fisher Scientific, Ambeed, Enamine, Fluorochem, Tokyo Chemical Industry, Shanghai Haoyuan Chemexpress, Shanghai Bepharm Science&Technology, Shanghai Haohong scientific, PharmaBlock Sciences, Shanghai Ronghe Medical Technology Development, LinkChem, Beijing Jinming Biotechnology, Shanghai Macklin Biochemical, Shanghai Xian Ding Biotechnology, Guangzhou Isun Pharmaceutical.

3. What are the main segments of the Heterocyclic Molecular Building Blocks?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Heterocyclic Molecular Building Blocks," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Heterocyclic Molecular Building Blocks report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Heterocyclic Molecular Building Blocks?

To stay informed about further developments, trends, and reports in the Heterocyclic Molecular Building Blocks, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence