Key Insights

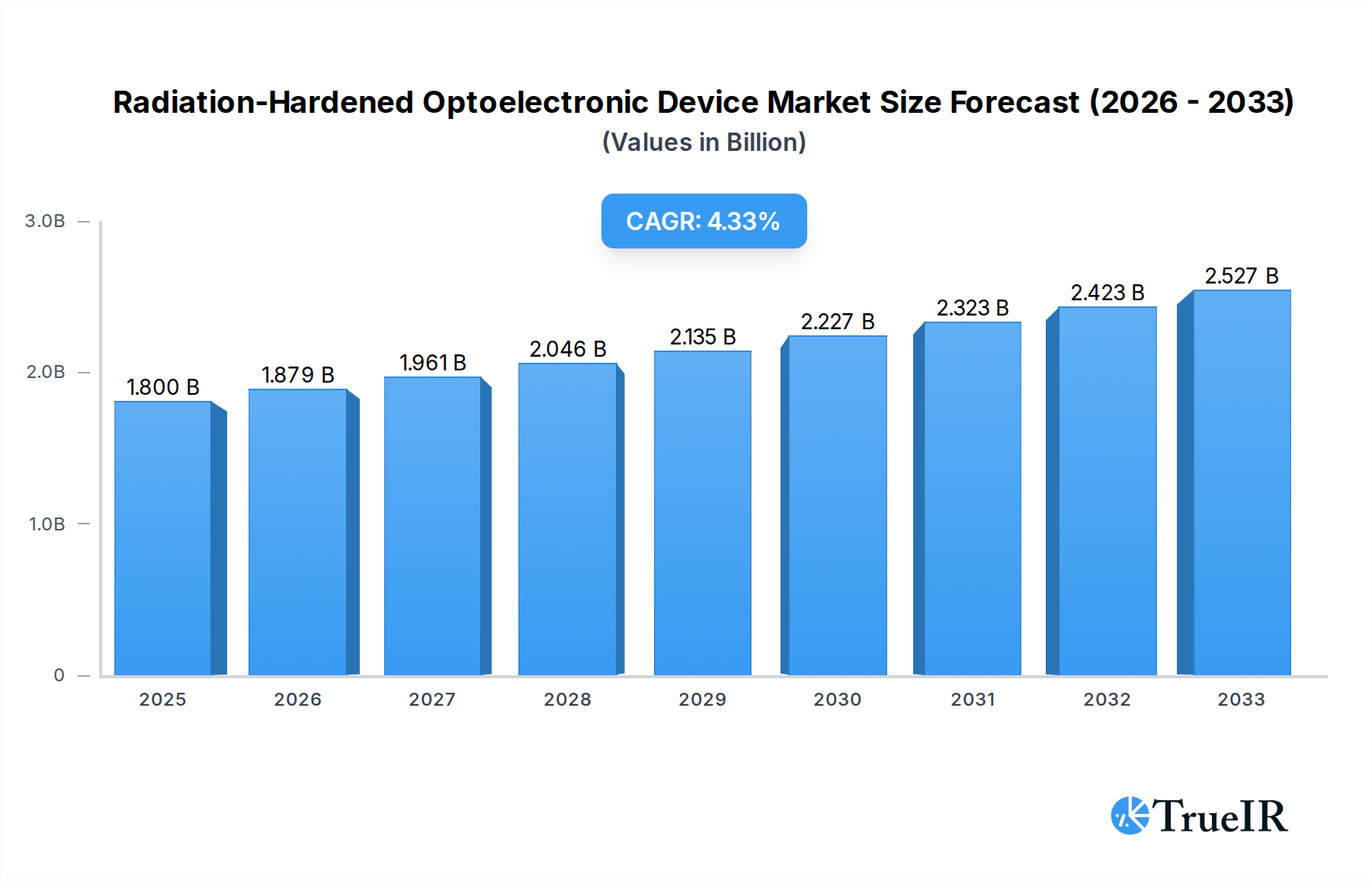

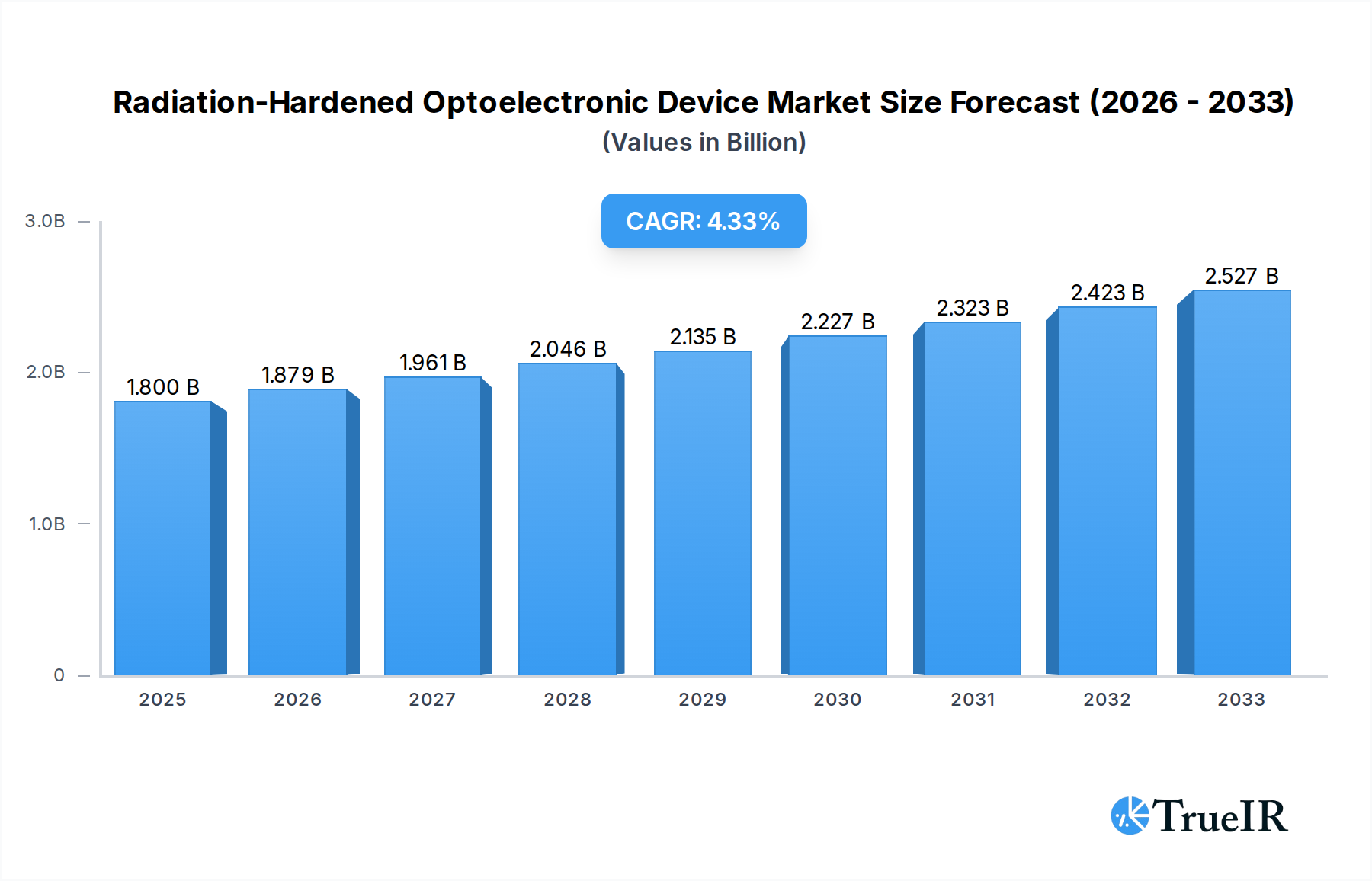

The global Radiation-Hardened Optoelectronic Device market is poised for significant expansion, projected to reach an estimated $1.8 billion in 2025, with a robust Compound Annual Growth Rate (CAGR) of 4.4% through 2033. This growth is underpinned by escalating demand from the space and defense sectors, where the reliability and resilience of electronic components in harsh, radiation-prone environments are paramount. Key drivers include the continuous advancements in satellite technology for communication, Earth observation, and navigation, alongside the increasing deployment of sophisticated defense systems, including guided missiles and airborne platforms that require components immune to radiation-induced failures. The market is also seeing a surge in the development of specialized optoelectronic devices that offer superior performance and longevity in extreme conditions.

Radiation-Hardened Optoelectronic Device Market Size (In Billion)

The market is segmented into key types, including diodes and fiber optics, each catering to distinct applications within the radiation-hardened landscape. While diodes are crucial for sensing and signal processing, fiber optics are increasingly vital for high-speed data transmission in environments where electromagnetic interference is a concern. Restraints such as the high cost of research, development, and manufacturing of specialized radiation-hardened components, coupled with stringent qualification processes, present challenges. However, ongoing technological innovations and strategic collaborations among leading companies like BAE Systems, Infineon Technologies AG, and STMicroelectronics are expected to mitigate these hurdles. Emerging trends point towards miniaturization, increased power efficiency, and the integration of AI-driven functionalities into these devices, further solidifying their critical role in future technological advancements.

Radiation-Hardened Optoelectronic Device Company Market Share

Here is a dynamic, SEO-optimized report description for Radiation-Hardened Optoelectronic Devices, incorporating your specifications:

Unlock the Future of High-Reliability Optoelectronics: Comprehensive Market Analysis Report

Gain unparalleled insights into the rapidly evolving Radiation-Hardened Optoelectronic Device market with our definitive report. This in-depth analysis, covering the Study Period 2019–2033, provides a critical roadmap for stakeholders navigating the Space and Defense sectors, as well as emerging Other applications. Leveraging billion-dollar market valuations and projecting significant growth, this report is essential for understanding the competitive landscape, key trends, dominant segments, and future opportunities. Discover how innovations in Diodes, Fiber Optics, and other critical optoelectronic components are shaping mission-critical systems.

Radiation-Hardened Optoelectronic Device Market Structure & Competitive Landscape

The global Radiation-Hardened Optoelectronic Device market, valued in the billions, exhibits a moderate concentration with key players investing heavily in innovation and vertical integration to maintain competitive advantages. Innovation drivers are primarily fueled by the escalating demands from the Space and Defense industries for components that can withstand extreme radiation environments. Regulatory impacts, particularly stringent qualification standards for aerospace and military applications, significantly shape market entry and product development strategies. The threat of product substitutes, while present, is largely mitigated by the unique reliability requirements of radiation-hardened components. End-user segmentation reveals a substantial reliance on the Space and Defense sectors, with a burgeoning growth trajectory in Other applications such as nuclear power and advanced scientific research. Mergers and acquisitions (M&A) activity, while not at an all-time high, remains a strategic tool for market consolidation and technology acquisition, with an estimated volume of approximately 2 billion in recent years. The market is characterized by a balanced interplay of established giants and agile niche players, each vying for a larger share of this high-value market.

Radiation-Hardened Optoelectronic Device Market Trends & Opportunities

The Radiation-Hardened Optoelectronic Device market is poised for exponential growth, with an estimated market size projected to reach hundreds of billions by the end of the forecast period, driven by a Compound Annual Growth Rate (CAGR) exceeding 10% from the base year of 2025. This robust expansion is fueled by a confluence of technological shifts, evolving consumer preferences in high-reliability sectors, and intensified competitive dynamics. The increasing sophistication of space exploration missions, including deep space probes and satellite constellations, necessitates optoelectronic devices with unprecedented radiation tolerance. Similarly, advancements in military platforms, such as next-generation fighter jets and unmanned aerial vehicles (UAVs), demand robust and reliable communication and sensing capabilities in harsh environments. Consumer preferences are increasingly skewed towards enhanced system longevity and reduced maintenance costs, making radiation-hardened solutions a compelling choice even in applications where radiation is not the primary concern but an added benefit for overall resilience.

Technological shifts are central to this growth trajectory. Innovations in semiconductor fabrication processes, advanced materials science, and novel device architectures are continuously improving radiation resistance while simultaneously enhancing performance metrics like speed, efficiency, and bandwidth. The integration of advanced packaging techniques further contributes to device reliability and miniaturization, making them suitable for a wider array of applications. Furthermore, the rise of AI and machine learning in defense and aerospace necessitates high-speed data processing and communication, where advanced optoelectronic components play a pivotal role.

Competitive dynamics are intensifying, with companies actively investing in research and development to secure intellectual property and establish technological leadership. Strategic partnerships and collaborations are becoming more prevalent, allowing for the pooling of expertise and resources to address complex technological challenges. The market penetration rates for specialized radiation-hardened optoelectronic devices are steadily increasing across core segments, indicating a growing acceptance and demand for these high-performance components. The sustained investment in space infrastructure, coupled with escalating geopolitical tensions, further bolsters the demand for mission-critical defense electronics, thereby creating significant opportunities for market expansion. The evolution of fiber optics in high-bandwidth communication, especially in space-based networks, represents a particularly strong growth avenue.

Dominant Markets & Segments in Radiation-Hardened Optoelectronic Device

The Space application segment stands as the undisputed leader in the Radiation-Hardened Optoelectronic Device market, representing a significant portion of the billion-dollar valuations. Within this segment, Diodes and Fiber Optics are particularly dominant, driven by the stringent reliability requirements for satellites, space probes, and inter-satellite communication systems. The ongoing expansion of satellite constellations for broadband internet, earth observation, and scientific research, valued in the hundreds of billions, is a primary growth catalyst. Government investments in space programs, both civil and military, continue to be a cornerstone of market dominance.

The Defense segment is the second-largest contributor, with a projected market size in the billions, exhibiting strong growth fueled by modernization initiatives and the need for resilient communication, sensing, and targeting systems in adversarial environments. Key growth drivers include the deployment of advanced radar systems, secure communication networks, and electronic warfare capabilities. National security priorities and defense budgets allocated in the hundreds of billions globally underscore the sustained demand for radiation-hardened optoelectronics in military applications.

The Others application segment, while currently smaller in market share, is demonstrating the most dynamic growth trajectory. This segment encompasses a diverse range of applications including nuclear power plants, particle accelerators, industrial automation in hazardous environments, and medical imaging. As the need for reliable operation in high-radiation environments extends beyond traditional defense and space sectors, the market for radiation-hardened optoelectronics is set to expand significantly, potentially reaching tens of billions by the forecast period's end. Infrastructure development in these niche areas, coupled with increasing awareness of the benefits of radiation tolerance, are key growth drivers.

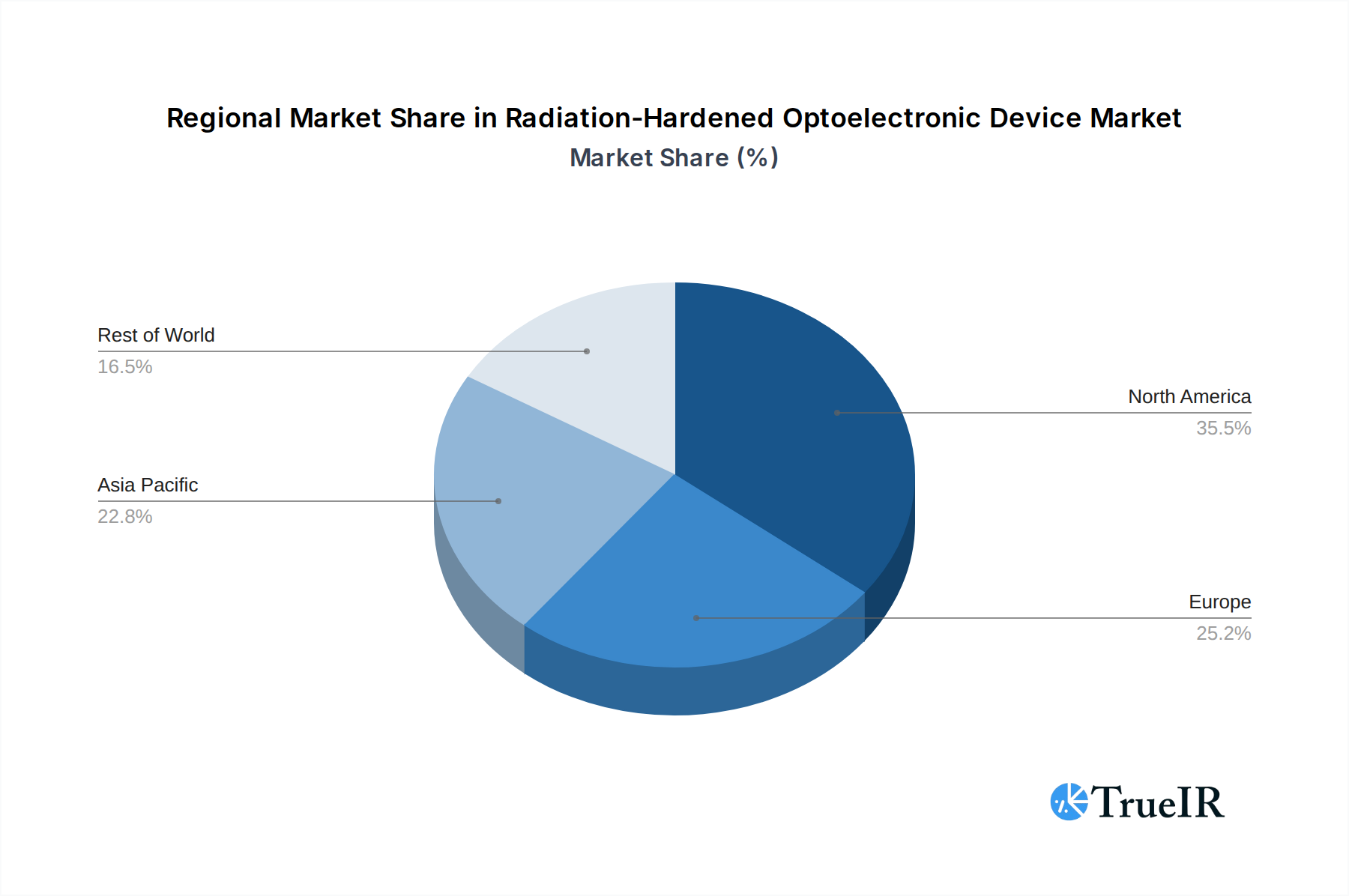

Geographically, North America and Europe currently dominate the market due to established aerospace and defense industries and significant government funding. However, the Asia-Pacific region is emerging as a rapidly growing market, driven by increasing investments in space programs and defense modernization by countries like China and India. This burgeoning demand from emerging economies is projected to contribute billions to the overall market growth in the coming years.

Radiation-Hardened Optoelectronic Device Product Analysis

Radiation-hardened optoelectronic devices represent a pinnacle of engineering resilience, designed to function flawlessly in environments subjected to intense ionizing radiation. Key product innovations focus on enhancing intrinsic radiation tolerance through advanced material selection and device architecture. This includes the development of specialized photodiodes and optocouplers with superior resistance to total ionizing dose (TID) and displacement damage. Fiber optic components, such as radiation-hardened connectors and transceivers, are crucial for reliable data transmission in space and defense applications, supporting bandwidths in the gigabits per second range. Competitive advantages stem from their unparalleled reliability, extended operational lifespan, and reduced failure rates in critical systems, directly impacting mission success and lifecycle costs, which can be in the billions for major programs.

Key Drivers, Barriers & Challenges in Radiation-Hardened Optoelectronic Device

Key Drivers, Barriers & Challenges in Radiation-Hardened Optoelectronic Device

Growth Drivers:

- Escalating Space Exploration & Satellite Deployment: Billions invested in new satellite constellations and deep space missions demand highly reliable optoelectronics.

- Defense Modernization & National Security: The need for resilient communication, sensing, and targeting systems in advanced military platforms fuels demand.

- Technological Advancements in Semiconductor Technology: Improved fabrication processes and materials enhance radiation tolerance and performance.

- Increasing Demand in Emerging Applications: Growth in nuclear power, industrial automation, and medical imaging sectors.

- Government Funding & R&D Investment: Significant public sector investment in aerospace and defense provides a stable demand base.

Challenges Impacting Radiation-Hardened Optoelectronic Device Growth:

- High Development & Qualification Costs: The rigorous testing and certification processes add significant cost, potentially in the hundreds of millions for specific qualifications.

- Complex Supply Chain & Lead Times: Sourcing specialized materials and components can lead to extended production lead times, impacting project timelines.

- Stringent Regulatory Standards & Compliance: Meeting complex and evolving industry-specific standards requires substantial effort and investment.

- Limited Number of Qualified Manufacturers: The specialized nature of the technology restricts the supply base, leading to potential bottlenecks.

- Competition from Commercial Off-the-Shelf (COTS) Components: While not directly comparable in reliability, cost pressures can sometimes drive consideration of less robust solutions.

Growth Drivers in the Radiation-Hardened Optoelectronic Device Market

The radiation-hardened optoelectronic device market is propelled by several key drivers, paramount among them being the aggressive expansion of the global space sector. Billions are being injected into satellite deployment for communication, navigation, and earth observation, creating a relentless demand for components that can endure the harsh conditions of space. Concurrently, national defense initiatives worldwide are undergoing significant modernization, necessitating robust and reliable optoelectronic solutions for advanced military platforms, further contributing billions to market demand. Technological advancements in semiconductor manufacturing and material science are continuously pushing the boundaries of radiation tolerance and performance, making these devices more accessible and effective. Furthermore, a growing awareness of the benefits of radiation hardening in applications like nuclear power and industrial automation is opening up new market avenues, potentially worth billions. Government funding and strategic investments in R&D remain a critical catalyst, providing the financial backbone for innovation and market growth.

Challenges Impacting Radiation-Hardened Optoelectronic Device Growth

Despite the robust growth prospects, the radiation-hardened optoelectronic device market faces significant challenges that could impede its full potential. The development and qualification of these highly specialized components are exceptionally costly, often running into hundreds of millions for comprehensive testing and certification, which can deter smaller players and prolong product development cycles. The supply chain for radiation-hardened materials and manufacturing is intricate and possesses limited capacity, leading to extended lead times that can impact project timelines and increase costs. Adhering to stringent and evolving regulatory standards across different aerospace and defense sectors requires substantial investment and expertise. The limited number of manufacturers capable of producing radiation-hardened devices creates potential bottlenecks and dependency issues. Finally, while not a direct substitute, the lower cost of commercial off-the-shelf (COTS) optoelectronic components can present a challenge in budget-constrained projects, even if they lack the required reliability for mission-critical applications.

Key Players Shaping the Radiation-Hardened Optoelectronic Device Market

- OSI Optoelectronics

- Exail

- SkyWater

- BAE Systems

- Renesas Electronics Corporation

- Infineon Technologies AG

- STMicroelectronics

- Analog Devices

Significant Radiation-Hardened Optoelectronic Device Industry Milestones

- 2019: Launch of next-generation radiation-hardened laser diodes by a leading manufacturer, enhancing data transmission speeds for satellite communications.

- 2020: Major defense contractor announces successful integration of radiation-hardened optocouplers into a new fighter jet program, significantly improving system reliability.

- 2021: Expansion of space-grade fiber optic cable manufacturing capacity by a key industry player to meet burgeoning satellite network demands.

- 2022: Significant breakthroughs in silicon carbide (SiC) based radiation-hardened photodetectors reported, promising higher performance and efficiency.

- 2023: A leading semiconductor foundry announces substantial investment in expanding its radiation-hardened wafer fabrication capabilities, addressing market capacity concerns.

- 2024: Deployment of advanced radiation-hardened optical transceivers in a landmark deep-space exploration mission, validating their long-term reliability.

Future Outlook for Radiation-Hardened Optoelectronic Device Market

The future outlook for the Radiation-Hardened Optoelectronic Device market is exceptionally bright, with sustained growth projected well into the forecast period. Strategic opportunities lie in the increasing demand for higher bandwidth and faster data processing in space-based communication networks and advanced defense systems. The continued miniaturization and integration of optoelectronic components will enable their use in an even wider array of applications, from CubeSats to next-generation military sensors, further expanding the market's reach into the billions. Innovations in materials science and manufacturing processes will drive down costs and improve performance, making radiation-hardened solutions more accessible. The growing emphasis on autonomous systems in both space and defense will also necessitate highly reliable optoelectronic components, acting as a significant growth catalyst and ensuring the market's continued expansion into the hundreds of billions.

Radiation-Hardened Optoelectronic Device Segmentation

-

1. Application

- 1.1. Space

- 1.2. Defense

- 1.3. Others

-

2. Types

- 2.1. Diodes

- 2.2. Fiber Optics

- 2.3. Others

Radiation-Hardened Optoelectronic Device Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Radiation-Hardened Optoelectronic Device Regional Market Share

Geographic Coverage of Radiation-Hardened Optoelectronic Device

Radiation-Hardened Optoelectronic Device REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Radiation-Hardened Optoelectronic Device Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Space

- 5.1.2. Defense

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Diodes

- 5.2.2. Fiber Optics

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Radiation-Hardened Optoelectronic Device Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Space

- 6.1.2. Defense

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Diodes

- 6.2.2. Fiber Optics

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Radiation-Hardened Optoelectronic Device Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Space

- 7.1.2. Defense

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Diodes

- 7.2.2. Fiber Optics

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Radiation-Hardened Optoelectronic Device Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Space

- 8.1.2. Defense

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Diodes

- 8.2.2. Fiber Optics

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Radiation-Hardened Optoelectronic Device Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Space

- 9.1.2. Defense

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Diodes

- 9.2.2. Fiber Optics

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Radiation-Hardened Optoelectronic Device Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Space

- 10.1.2. Defense

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Diodes

- 10.2.2. Fiber Optics

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 OSI Optoelectronics

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Exail

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 SkyWater

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 BAE Systems

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Renesas Electronics Corporation

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Infineon Technologies AG

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 STMicroelectronics

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Analog Devices

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.1 OSI Optoelectronics

List of Figures

- Figure 1: Global Radiation-Hardened Optoelectronic Device Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Radiation-Hardened Optoelectronic Device Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Radiation-Hardened Optoelectronic Device Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Radiation-Hardened Optoelectronic Device Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Radiation-Hardened Optoelectronic Device Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Radiation-Hardened Optoelectronic Device Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Radiation-Hardened Optoelectronic Device Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Radiation-Hardened Optoelectronic Device Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Radiation-Hardened Optoelectronic Device Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Radiation-Hardened Optoelectronic Device Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Radiation-Hardened Optoelectronic Device Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Radiation-Hardened Optoelectronic Device Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Radiation-Hardened Optoelectronic Device Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Radiation-Hardened Optoelectronic Device Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Radiation-Hardened Optoelectronic Device Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Radiation-Hardened Optoelectronic Device Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Radiation-Hardened Optoelectronic Device Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Radiation-Hardened Optoelectronic Device Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Radiation-Hardened Optoelectronic Device Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Radiation-Hardened Optoelectronic Device Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Radiation-Hardened Optoelectronic Device Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Radiation-Hardened Optoelectronic Device Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Radiation-Hardened Optoelectronic Device Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Radiation-Hardened Optoelectronic Device Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Radiation-Hardened Optoelectronic Device Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Radiation-Hardened Optoelectronic Device Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Radiation-Hardened Optoelectronic Device Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Radiation-Hardened Optoelectronic Device Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Radiation-Hardened Optoelectronic Device Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Radiation-Hardened Optoelectronic Device Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Radiation-Hardened Optoelectronic Device Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Radiation-Hardened Optoelectronic Device Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Radiation-Hardened Optoelectronic Device Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Radiation-Hardened Optoelectronic Device Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Radiation-Hardened Optoelectronic Device Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Radiation-Hardened Optoelectronic Device Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Radiation-Hardened Optoelectronic Device Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Radiation-Hardened Optoelectronic Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Radiation-Hardened Optoelectronic Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Radiation-Hardened Optoelectronic Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Radiation-Hardened Optoelectronic Device Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Radiation-Hardened Optoelectronic Device Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Radiation-Hardened Optoelectronic Device Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Radiation-Hardened Optoelectronic Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Radiation-Hardened Optoelectronic Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Radiation-Hardened Optoelectronic Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Radiation-Hardened Optoelectronic Device Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Radiation-Hardened Optoelectronic Device Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Radiation-Hardened Optoelectronic Device Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Radiation-Hardened Optoelectronic Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Radiation-Hardened Optoelectronic Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Radiation-Hardened Optoelectronic Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Radiation-Hardened Optoelectronic Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Radiation-Hardened Optoelectronic Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Radiation-Hardened Optoelectronic Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Radiation-Hardened Optoelectronic Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Radiation-Hardened Optoelectronic Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Radiation-Hardened Optoelectronic Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Radiation-Hardened Optoelectronic Device Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Radiation-Hardened Optoelectronic Device Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Radiation-Hardened Optoelectronic Device Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Radiation-Hardened Optoelectronic Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Radiation-Hardened Optoelectronic Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Radiation-Hardened Optoelectronic Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Radiation-Hardened Optoelectronic Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Radiation-Hardened Optoelectronic Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Radiation-Hardened Optoelectronic Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Radiation-Hardened Optoelectronic Device Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Radiation-Hardened Optoelectronic Device Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Radiation-Hardened Optoelectronic Device Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Radiation-Hardened Optoelectronic Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Radiation-Hardened Optoelectronic Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Radiation-Hardened Optoelectronic Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Radiation-Hardened Optoelectronic Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Radiation-Hardened Optoelectronic Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Radiation-Hardened Optoelectronic Device Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Radiation-Hardened Optoelectronic Device Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Radiation-Hardened Optoelectronic Device?

The projected CAGR is approximately 4.4%.

2. Which companies are prominent players in the Radiation-Hardened Optoelectronic Device?

Key companies in the market include OSI Optoelectronics, Exail, SkyWater, BAE Systems, Renesas Electronics Corporation, Infineon Technologies AG, STMicroelectronics, Analog Devices.

3. What are the main segments of the Radiation-Hardened Optoelectronic Device?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.8 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Radiation-Hardened Optoelectronic Device," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Radiation-Hardened Optoelectronic Device report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Radiation-Hardened Optoelectronic Device?

To stay informed about further developments, trends, and reports in the Radiation-Hardened Optoelectronic Device, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence