Key Insights

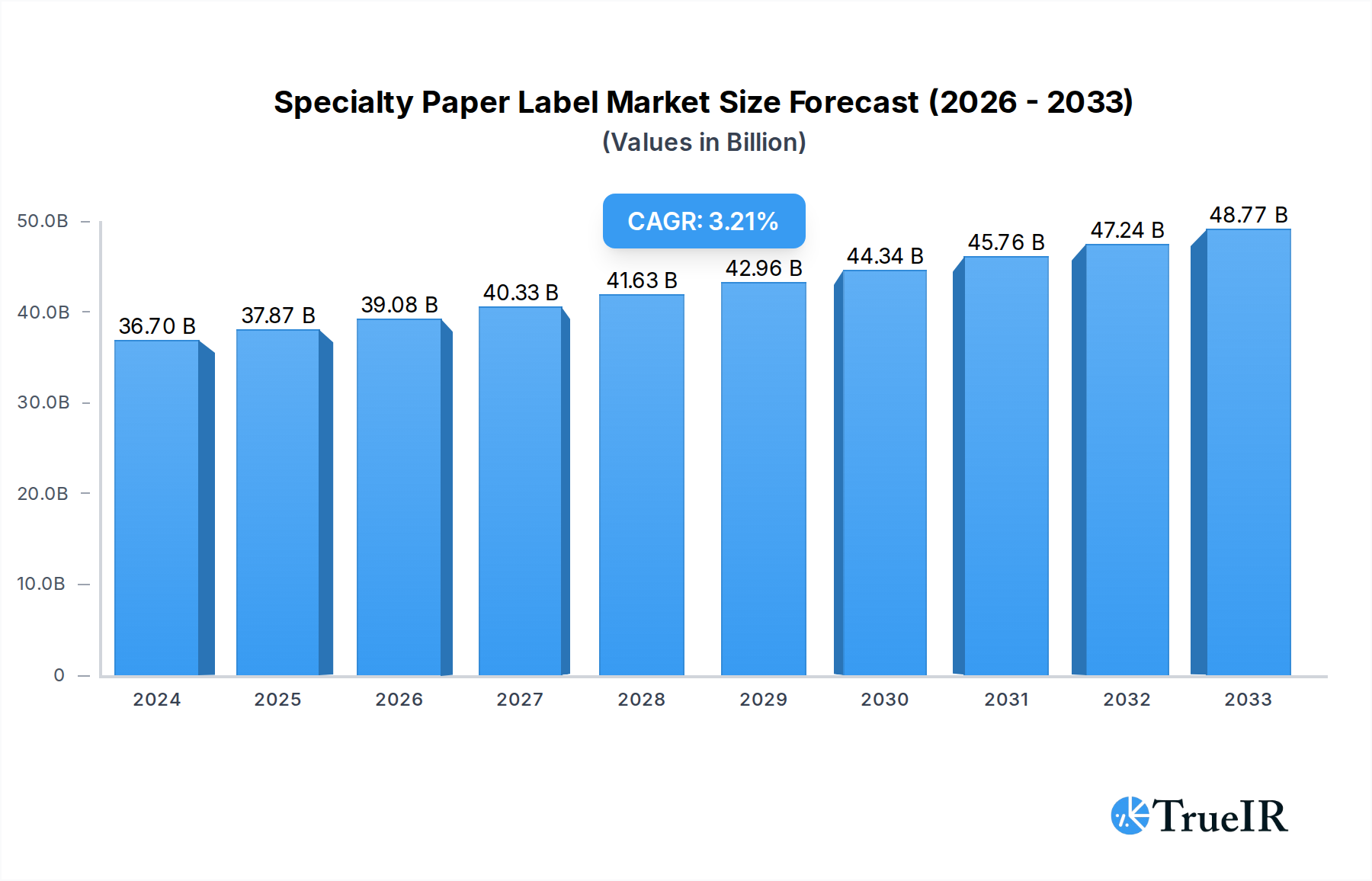

The Specialty Paper Label market is poised for steady expansion, driven by increasing demand across a multitude of industries. In 2024, the market size is estimated at $36.7 billion. This growth is primarily fueled by the escalating need for sophisticated labeling solutions in sectors like pharmaceuticals, where precise identification and tracking are paramount, and the food processing industry, which requires durable, informative, and visually appealing labels. Furthermore, the burgeoning e-commerce landscape significantly contributes to market expansion, as online retailers rely heavily on effective labeling for inventory management, shipping, and brand presentation. The logistics sector's continuous drive for enhanced supply chain visibility and efficiency also acts as a significant impetus for the adoption of advanced specialty paper labels, including those designed for thermal transfer and direct thermal printing technologies.

Specialty Paper Label Market Size (In Billion)

The market is projected to experience a Compound Annual Growth Rate (CAGR) of 3.17% from 2025 to 2033, indicating sustained and robust growth. While the market benefits from strong drivers such as regulatory compliance requirements and consumer demand for product information, it also faces certain restraints. The increasing adoption of digital labeling technologies and the higher cost of some specialty paper materials compared to standard paper labels could present challenges. However, innovations in sustainable and eco-friendly paper label materials are expected to mitigate these concerns and open new avenues for growth. Key players like Zebra Technologies, Avery Dennison, and UPM are actively investing in research and development to offer innovative solutions catering to diverse industry needs, further shaping the market's trajectory.

Specialty Paper Label Company Market Share

Specialty Paper Label Market Structure & Competitive Landscape

The global specialty paper label market exhibits a moderately concentrated structure, with key players like Zebra Technologies, Avery Dennison, and UPM holding significant market share. Innovation remains a critical driver, fueled by advancements in paper coatings, adhesive technologies, and printing capabilities, particularly in direct thermal and thermal transfer segments. Regulatory impacts are most pronounced in the pharmaceutical and food processing industries, where stringent labeling requirements for product safety and traceability influence material selection and compliance. Product substitutes, while present in certain niche applications, are largely overshadowed by the versatility and cost-effectiveness of specialty paper labels for a broad range of uses. End-user segmentation reveals strong demand from the logistics, chemical, and food processing sectors. Mergers and acquisitions (M&A) activity is a notable trend, with private equity firms like Bain Capital actively investing in the sector to consolidate market positions and drive growth. Recent M&A volumes indicate strategic consolidation aimed at expanding product portfolios and geographic reach.

- Market Concentration: Moderate to high, with top players dominating market share.

- Innovation Drivers: Advanced coatings, adhesives, printing technologies (direct thermal, thermal transfer).

- Regulatory Impacts: Significant in pharmaceutical and food processing for safety and traceability.

- Product Substitutes: Limited impact due to broad applicability and cost-effectiveness.

- End-User Segmentation: Strong demand from Logistics, Chemical, and Food Processors.

- M&A Trends: Active consolidation and strategic investments by private equity.

Specialty Paper Label Market Trends & Opportunities

The specialty paper label market is poised for robust growth, projected to expand at a compound annual growth rate (CAGR) of xx% from the base year 2025 through the forecast period of 2033. This upward trajectory is underpinned by several transformative trends. Technologically, the increasing adoption of high-speed digital printing technologies is revolutionizing label production, enabling greater customization, shorter run lengths, and faster turnaround times, thereby catering to the evolving needs of industries like e-commerce and pharmaceuticals. The development of advanced paper substrates with enhanced durability, resistance to extreme temperatures, moisture, and chemicals is further widening the application spectrum for specialty paper labels.

Consumer preferences are increasingly dictating market dynamics, with a growing demand for sustainable and eco-friendly packaging solutions. This has spurred innovation in biodegradable and recyclable specialty paper labels, aligning with global sustainability initiatives. The pharmaceutical industry, in particular, is a significant growth engine, driven by stricter regulatory mandates for drug traceability, patient safety, and anti-counterfeiting measures. The increasing complexity of drug supply chains and the rise of biologics necessitate sophisticated labeling solutions that specialty paper labels are well-equipped to provide.

The logistics and supply chain sector continues to be a major consumer, fueled by the burgeoning e-commerce market and the need for efficient inventory management, shipping, and tracking. Specialty paper labels are crucial for barcodes, QR codes, and serialization, ensuring seamless operations. The food processing industry also presents substantial opportunities, driven by the demand for clear product information, nutritional labeling, and compliance with food safety standards. Furthermore, the "Others" segment, encompassing applications in automotive, electronics, and industrial manufacturing, is showing promising growth as these sectors increasingly rely on specialized labeling for component identification, warning labels, and asset tracking. Competitive dynamics are characterized by ongoing innovation in material science and printing technology, as well as strategic partnerships and acquisitions aimed at expanding market reach and product offerings. The market penetration rate for specialty paper labels is expected to continue its upward climb as businesses recognize their value proposition in enhancing efficiency, compliance, and brand perception.

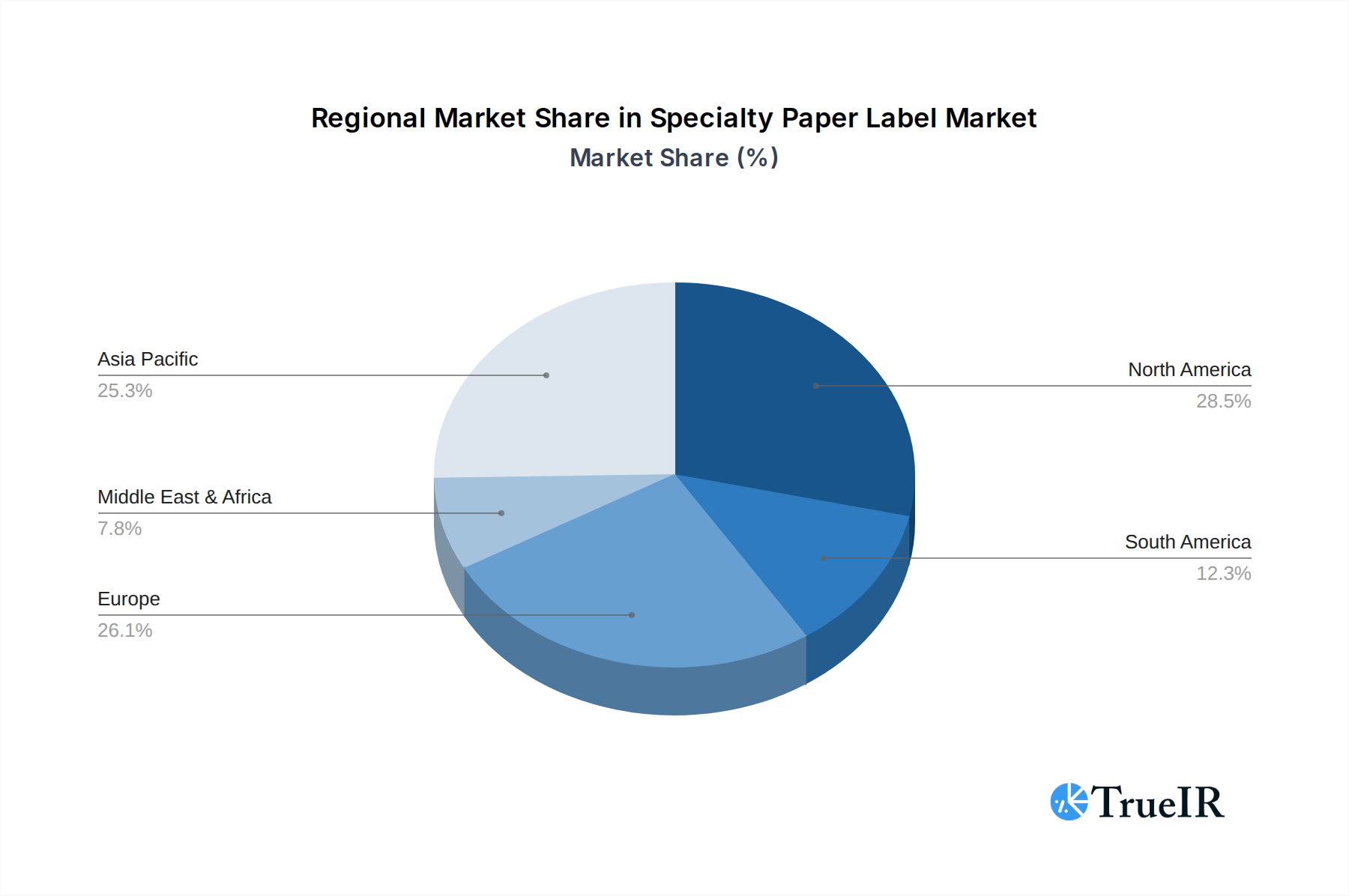

Dominant Markets & Segments in Specialty Paper Label

The global specialty paper label market demonstrates significant regional variations and segment dominance, driven by specific industry needs and economic factors.

Dominant Regions:

- North America: This region holds a commanding position, propelled by a highly developed industrial base, advanced technological adoption, and stringent regulatory frameworks in the pharmaceutical and food processing sectors. The robust logistics infrastructure supporting a thriving e-commerce ecosystem further bolsters demand for specialty paper labels. Key growth drivers include substantial investments in supply chain efficiency and a strong emphasis on product traceability and safety.

- Europe: Europe follows closely, benefiting from a similar focus on regulatory compliance, particularly in the pharmaceutical and chemical industries. The growing awareness and demand for sustainable packaging solutions are also a significant catalyst for the adoption of eco-friendly specialty paper labels. Government initiatives promoting circular economy principles further support this trend.

- Asia Pacific: This region is emerging as a high-growth market, driven by rapid industrialization, expanding manufacturing capabilities, and the accelerating growth of the e-commerce and logistics sectors. Favorable government policies supporting manufacturing and trade, coupled with increasing disposable incomes, are contributing to widespread adoption across various applications.

Dominant Segments:

- Application: Pharmaceutical Industry: This segment is a critical driver of the specialty paper label market. The absolute necessity for tamper-evident, high-durability labels that can withstand sterilization processes, provide detailed patient information, and comply with rigorous serialization and track-and-trace regulations makes specialty paper labels indispensable. Growth is fueled by the increasing complexity of pharmaceutical supply chains and the ongoing battle against counterfeit drugs.

- Application: Food Processors: The food and beverage industry relies heavily on specialty paper labels for nutritional information, ingredient lists, allergen warnings, best-before dates, and branding. The demand for clear, durable, and visually appealing labels that can withstand various environmental conditions, from refrigeration to cooking, drives innovation in this segment. Regulatory requirements for food safety and transparency are paramount.

- Types: Thermal Transfer: Thermal transfer labels are highly favored across multiple industries due to their durability, resistance to fading and abrasion, and ability to produce high-quality, long-lasting prints. Their versatility makes them ideal for barcodes, variable data printing, and product identification in logistics, inventory management, and the pharmaceutical sector. The increasing adoption of advanced thermal transfer printers enhances their efficiency and appeal.

- Types: Direct Thermal: Direct thermal labels are widely used for applications where print permanence is less critical but quick, on-demand printing is essential, such as receipts, shipping labels, and some food product labels. Their cost-effectiveness and ease of use make them popular in retail and logistics. The ongoing improvements in direct thermal paper technology are enhancing their durability and print quality.

Specialty Paper Label Product Analysis

Specialty paper labels are characterized by their innovative product designs and specialized functionalities. Advancements in paper coatings, such as gloss, matte, and textured finishes, alongside the development of high-performance adhesives, enable these labels to adhere securely to diverse surfaces and withstand challenging environmental conditions including extreme temperatures, moisture, and chemical exposure. Key product innovations focus on enhanced durability, printability, and sustainability, catering to specific industry needs such as the pharmaceutical industry's requirement for tamper-evident and scannable labels, or the food processing industry's need for labels resistant to condensation and temperature fluctuations. Their competitive advantage lies in their cost-effectiveness, versatility, and adaptability across a wide array of applications, from direct thermal printing for short-term use to thermal transfer for long-lasting identification.

Key Drivers, Barriers & Challenges in Specialty Paper Label

Key Drivers:

- Technological Advancements: Innovations in paper substrates, adhesives, and printing technologies like digital and thermal transfer printing are expanding application possibilities and enhancing label performance.

- Regulatory Compliance: Strict labeling requirements in industries such as pharmaceuticals and food processing mandate the use of high-quality, traceable, and durable labels.

- E-commerce Boom: The exponential growth of online retail necessitates efficient, scannable, and informative shipping and product labels.

- Sustainability Initiatives: Growing consumer and regulatory pressure for eco-friendly packaging is driving demand for recyclable and biodegradable specialty paper labels.

Barriers & Challenges:

- Supply Chain Disruptions: Global supply chain volatility, including raw material shortages and increased freight costs, can impact the availability and pricing of specialty paper labels.

- Competitive Pressure: Intense competition from alternative labeling materials (e.g., films) and other specialty paper label manufacturers can exert downward pressure on pricing.

- Cost Sensitivity: In some applications, cost remains a significant factor, potentially limiting the adoption of premium specialty paper labels.

- Environmental Concerns: While sustainability is a driver, the production process and disposal of some paper-based labels still present environmental considerations that need to be addressed.

Growth Drivers in the Specialty Paper Label Market

The specialty paper label market is propelled by a confluence of factors. Technological advancements, particularly in digital printing and smart label technologies, are enabling greater customization and functionality. The escalating global demand for e-commerce is a significant growth catalyst, requiring robust and scannable labels for logistics and product identification. Stringent regulatory mandates within the pharmaceutical and food processing sectors, emphasizing product safety, traceability, and anti-counterfeiting, are driving the adoption of high-performance specialty paper labels. Furthermore, a growing consumer consciousness towards sustainability is fueling the demand for eco-friendly, recyclable, and biodegradable paper label solutions, presenting a substantial market opportunity.

Challenges Impacting Specialty Paper Label Growth

The specialty paper label market faces several headwinds that can impede its growth trajectory. Persistent global supply chain disruptions, including raw material availability and rising logistics costs, pose a significant challenge to production and timely delivery. Intense competition from alternative labeling materials, such as plastic films, and price-sensitive markets can limit market share expansion. Regulatory complexities, while often a driver, can also create hurdles if compliance requirements become overly burdensome or expensive to meet for smaller manufacturers. Furthermore, while sustainability is a positive trend, the industry must continually address the environmental impact of paper production and disposal to maintain its eco-friendly appeal.

Key Players Shaping the Specialty Paper Label Market

- Zebra Technologies

- General Data

- Avery Dennison

- UPM

- Mosaico Papers

- Blanklabels

- Twin Rivers

- Sappi

- Domtar

- Panda Paper Roll

- Ahlstrom

- Burgo Group

- Bain Capital

- Chung Hwa Pulp Corporation

Significant Specialty Paper Label Industry Milestones

- 2019: Increased focus on sustainable sourcing and production of specialty papers to meet growing environmental demands.

- 2020: Accelerated adoption of e-commerce drives significant demand for logistics and shipping labels, including specialty paper options.

- 2021: Advancements in digital printing technology enhance customization capabilities for specialty paper labels, catering to niche markets.

- 2022: Heightened regulatory scrutiny in the pharmaceutical sector spurs demand for tamper-evident and serialized specialty paper labels.

- 2023: Several key players announce strategic investments in R&D for biodegradable and compostable specialty paper label materials.

- 2024: Growing awareness of supply chain vulnerabilities leads to increased interest in localized specialty paper label manufacturing and sourcing.

Future Outlook for Specialty Paper Label Market

The future outlook for the specialty paper label market is exceptionally promising, driven by ongoing innovation and expanding application avenues. Strategic opportunities lie in the continued development of advanced, sustainable paper substrates and high-performance adhesives to meet evolving industry needs. The pharmaceutical and food processing sectors will remain strong growth engines, demanding increasingly sophisticated labeling solutions for safety and traceability. The burgeoning e-commerce market will continue to fuel demand for efficient and reliable labeling. Companies that can effectively leverage technological advancements, address sustainability concerns, and navigate supply chain complexities are poised for significant growth and market leadership in the coming years, with an estimated market size of over a billion dollars.

Specialty Paper Label Segmentation

-

1. Application

- 1.1. Chemical

- 1.2. Food Processors

- 1.3. Logistics

- 1.4. Pharmaceutical Industry

- 1.5. Others

-

2. Types

- 2.1. Thermal Transfer

- 2.2. Direct Thermal

Specialty Paper Label Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Specialty Paper Label Regional Market Share

Geographic Coverage of Specialty Paper Label

Specialty Paper Label REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.17% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Specialty Paper Label Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Chemical

- 5.1.2. Food Processors

- 5.1.3. Logistics

- 5.1.4. Pharmaceutical Industry

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Thermal Transfer

- 5.2.2. Direct Thermal

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Specialty Paper Label Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Chemical

- 6.1.2. Food Processors

- 6.1.3. Logistics

- 6.1.4. Pharmaceutical Industry

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Thermal Transfer

- 6.2.2. Direct Thermal

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Specialty Paper Label Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Chemical

- 7.1.2. Food Processors

- 7.1.3. Logistics

- 7.1.4. Pharmaceutical Industry

- 7.1.5. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Thermal Transfer

- 7.2.2. Direct Thermal

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Specialty Paper Label Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Chemical

- 8.1.2. Food Processors

- 8.1.3. Logistics

- 8.1.4. Pharmaceutical Industry

- 8.1.5. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Thermal Transfer

- 8.2.2. Direct Thermal

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Specialty Paper Label Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Chemical

- 9.1.2. Food Processors

- 9.1.3. Logistics

- 9.1.4. Pharmaceutical Industry

- 9.1.5. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Thermal Transfer

- 9.2.2. Direct Thermal

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Specialty Paper Label Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Chemical

- 10.1.2. Food Processors

- 10.1.3. Logistics

- 10.1.4. Pharmaceutical Industry

- 10.1.5. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Thermal Transfer

- 10.2.2. Direct Thermal

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Zebra Technologies

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 General Data

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Avery Dennison

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 UPM

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Mosaico Papers

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Blanklabels

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Twin Rivers

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Sappi

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Domtar

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Panda Paper Roll

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Ahlstrom

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Burgo Group

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Bain Capital

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Chung Hwa Pulp Corporation

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.1 Zebra Technologies

List of Figures

- Figure 1: Global Specialty Paper Label Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Specialty Paper Label Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Specialty Paper Label Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Specialty Paper Label Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Specialty Paper Label Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Specialty Paper Label Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Specialty Paper Label Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Specialty Paper Label Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Specialty Paper Label Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Specialty Paper Label Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Specialty Paper Label Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Specialty Paper Label Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Specialty Paper Label Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Specialty Paper Label Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Specialty Paper Label Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Specialty Paper Label Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Specialty Paper Label Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Specialty Paper Label Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Specialty Paper Label Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Specialty Paper Label Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Specialty Paper Label Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Specialty Paper Label Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Specialty Paper Label Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Specialty Paper Label Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Specialty Paper Label Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Specialty Paper Label Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Specialty Paper Label Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Specialty Paper Label Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Specialty Paper Label Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Specialty Paper Label Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Specialty Paper Label Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Specialty Paper Label Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Specialty Paper Label Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Specialty Paper Label Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Specialty Paper Label Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Specialty Paper Label Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Specialty Paper Label Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Specialty Paper Label Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Specialty Paper Label Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Specialty Paper Label Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Specialty Paper Label Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Specialty Paper Label Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Specialty Paper Label Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Specialty Paper Label Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Specialty Paper Label Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Specialty Paper Label Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Specialty Paper Label Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Specialty Paper Label Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Specialty Paper Label Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Specialty Paper Label Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Specialty Paper Label Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Specialty Paper Label Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Specialty Paper Label Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Specialty Paper Label Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Specialty Paper Label Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Specialty Paper Label Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Specialty Paper Label Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Specialty Paper Label Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Specialty Paper Label Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Specialty Paper Label Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Specialty Paper Label Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Specialty Paper Label Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Specialty Paper Label Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Specialty Paper Label Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Specialty Paper Label Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Specialty Paper Label Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Specialty Paper Label Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Specialty Paper Label Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Specialty Paper Label Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Specialty Paper Label Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Specialty Paper Label Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Specialty Paper Label Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Specialty Paper Label Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Specialty Paper Label Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Specialty Paper Label Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Specialty Paper Label Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Specialty Paper Label Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Specialty Paper Label?

The projected CAGR is approximately 3.17%.

2. Which companies are prominent players in the Specialty Paper Label?

Key companies in the market include Zebra Technologies, General Data, Avery Dennison, UPM, Mosaico Papers, Blanklabels, Twin Rivers, Sappi, Domtar, Panda Paper Roll, Ahlstrom, Burgo Group, Bain Capital, Chung Hwa Pulp Corporation.

3. What are the main segments of the Specialty Paper Label?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Specialty Paper Label," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Specialty Paper Label report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Specialty Paper Label?

To stay informed about further developments, trends, and reports in the Specialty Paper Label, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence