Key Insights

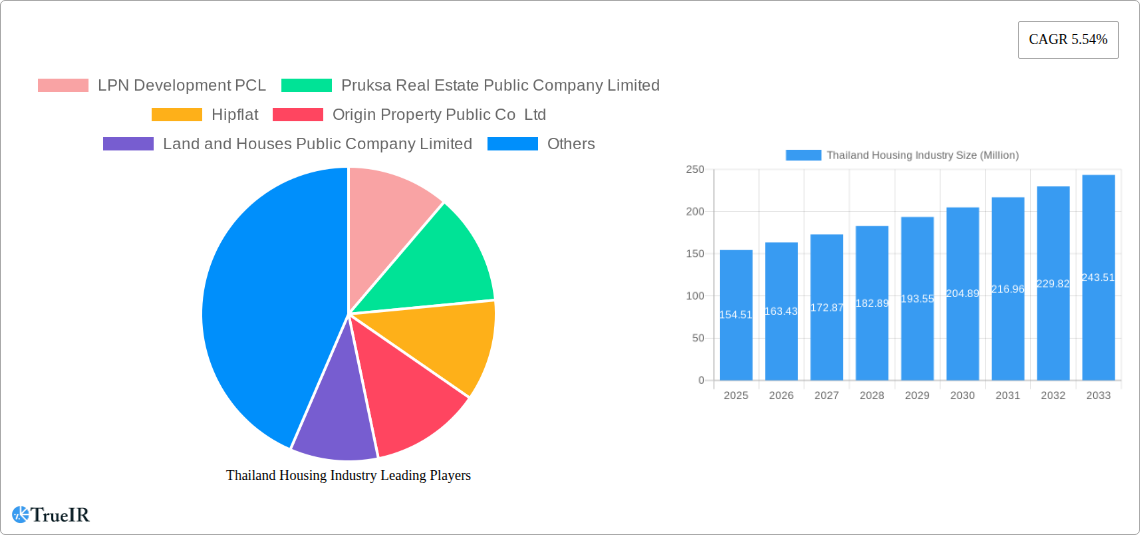

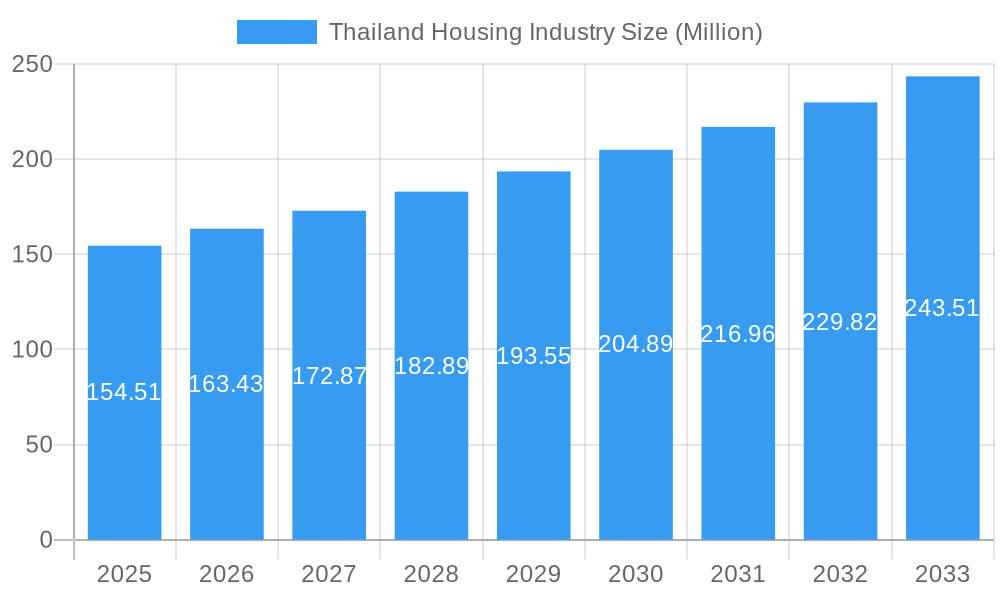

The Thailand Housing Industry is poised for significant expansion, with a current market size estimated at USD 154.51 million and projected to grow at a Compound Annual Growth Rate (CAGR) of 5.54% from 2025 to 2033. This robust growth trajectory is primarily driven by a burgeoning middle class, increasing urbanization, and government initiatives aimed at boosting housing affordability and accessibility. The demand for residential properties, particularly apartments and condominiums, is expected to surge as more people migrate to major urban centers like Bangkok, Chiang Mai, Nonthaburi, and Samut Prakan in pursuit of employment and better living standards. Furthermore, the rising disposable incomes and a growing preference for modern living spaces will continue to fuel the market for landed houses and villas, especially in well-developed suburban areas.

Thailand Housing Industry Market Size (In Million)

Despite the promising outlook, the market is not without its challenges. Rising construction material costs and land acquisition expenses could present a moderate restraint on growth. However, proactive measures by key developers such as LPN Development PCL, Pruksa Real Estate Public Company Limited, and Sansiri Co Ltd, alongside supportive government policies, are expected to mitigate these risks. The industry is also witnessing a significant trend towards sustainable and smart housing solutions, with developers increasingly incorporating eco-friendly designs and smart home technologies to cater to evolving consumer preferences. The competitive landscape is characterized by the presence of established players and emerging companies, all vying for market share by offering diverse housing options and innovative features. This dynamic environment is likely to spur further innovation and customer-centric approaches within the Thailand housing sector.

Thailand Housing Industry Company Market Share

Unlock the Future of Thai Real Estate: A Comprehensive Thailand Housing Industry Market Report (2019-2033)

Dive deep into the dynamic Thailand housing market with this definitive industry report. Covering a comprehensive study period from 2019 to 2033, this analysis provides unparalleled insights into market structure, trends, and future opportunities. Leveraging high-volume keywords such as "Thailand housing market," "real estate Thailand," "condominium market Bangkok," and "property investment Thailand," this report is meticulously designed for optimal SEO performance and maximum industry engagement. Whether you are a developer, investor, policymaker, or industry professional, this report offers the crucial data and strategic foresight needed to navigate and capitalize on the evolving Thai property landscape.

Thailand Housing Industry Market Structure & Competitive Landscape

The Thailand housing industry exhibits a moderately concentrated market structure, with a few dominant players holding significant market share, particularly in the apartments and condominiums segment. Leading companies like LPN Development PCL, Pruksa Real Estate Public Company Limited, Origin Property Public Co Ltd, and Sansiri Public Co Ltd consistently drive innovation and set market benchmarks. The regulatory environment plays a crucial role, with government policies on foreign ownership, mortgage lending, and urban planning directly influencing market dynamics. Product substitutes are limited, primarily existing housing stock and rental options, but innovation in smart home technology and sustainable building practices is increasingly differentiating new developments. End-user segmentation reveals a growing demand from young professionals for urban condominiums and a sustained interest in landed properties for families in suburban areas and key cities like Bangkok, Chiang Mai, Nonthaburi, and Samut Prakan. Merger and acquisition (M&A) trends indicate strategic consolidation, with transaction volumes projected to reach XX Million annually during the forecast period, aimed at expanding market reach and diversifying portfolios. Key M&A drivers include the acquisition of land banks, integration of technology solutions, and the pursuit of economies of scale.

Thailand Housing Industry Market Trends & Opportunities

The Thailand housing industry is poised for sustained growth, driven by a confluence of economic, social, and technological factors. The market size is projected to expand at a Compound Annual Growth Rate (CAGR) of XX% between the base year of 2025 and the forecast period ending in 2033, reaching an estimated market value of XX Billion. This growth is underpinned by a robust post-pandemic economic recovery, increasing disposable incomes, and a growing young population entering the property market. Technological shifts are revolutionizing the industry, with an increased adoption of proptech for virtual property tours, smart home integration, and AI-driven market analysis. Consumer preferences are evolving, with a growing demand for mixed-use developments that offer convenience, lifestyle amenities, and sustainable living. The rise of remote work is also influencing demand for larger living spaces and properties located in more suburban or scenic areas, offering a potential opportunity for developers to tap into these emerging trends. Competitive dynamics are intensifying, pushing companies to focus on differentiation through unique design, integrated services, and enhanced customer experiences. The market penetration rate for new housing units is expected to reach XX% by 2033, indicating significant potential for both established and new market entrants. Opportunities abound in developing affordable housing solutions, catering to the burgeoning middle class, and exploring eco-friendly and sustainable construction methods to align with global environmental consciousness. The tourism sector's recovery also fuels demand for holiday homes and investment properties, particularly in popular tourist destinations.

Dominant Markets & Segments in Thailand Housing Industry

The apartments and condominiums segment unequivocally dominates the Thailand housing industry, driven by rapid urbanization and the lifestyle preferences of a growing urban population. Bangkok stands as the paramount market, commanding a substantial share of national housing development and sales. This dominance is fueled by its status as the economic and administrative capital, attracting a large influx of domestic and international talent, thus creating sustained demand for residential properties. Chiang Mai, with its appeal as a cultural hub and a popular destination for digital nomads and retirees, represents a significant and growing secondary market. Nonthaburi and Samut Prakan, as adjacent metropolitan areas to Bangkok, are experiencing robust growth due to urban sprawl, infrastructure development, and comparatively more affordable land prices, making them attractive for both residential development and homeownership.

Key growth drivers in these dominant markets include:

- Infrastructure Development: Ongoing and planned transportation projects, such as new BTS and MRT lines, significantly enhance accessibility and desirability of various residential locations, particularly in peri-urban areas.

- Government Policies: Initiatives like the Eastern Economic Corridor (EEC) project are stimulating economic activity and population growth in related provinces, indirectly boosting housing demand. Policies promoting foreign investment in real estate also contribute to market vitality.

- Urbanization and Demographic Shifts: The continuous migration from rural to urban centers, coupled with a growing young professional demographic, fuels the demand for apartments and condominiums in prime city locations.

- Economic Growth and Disposable Income: A recovering and growing Thai economy translates into higher disposable incomes, empowering more individuals and families to invest in property.

The dominance of apartments and condominiums in Bangkok is characterized by high-rise developments offering modern amenities and convenient access to commercial centers and public transportation. In contrast, Landed Houses and Villas see strong demand in the suburban fringes of these major cities and in popular provincial tourist destinations, catering to families seeking more space and a quieter lifestyle. The market for landed properties is also influenced by the availability of larger land parcels and the preference for more traditional housing typologies.

Thailand Housing Industry Product Analysis

Thailand's housing industry is witnessing a surge in product innovation, focusing on integrated living solutions and technological advancements. Developers are increasingly offering smart home features, energy-efficient designs, and sustainable materials to meet evolving consumer demands. The competitive advantage lies in creating developments that offer not just a dwelling but a complete lifestyle experience, incorporating co-working spaces, recreational facilities, and green environments. Applications range from urban high-rise condominiums designed for convenience and connectivity to spacious landed villas designed for family comfort and privacy.

Key Drivers, Barriers & Challenges in Thailand Housing Industry

Key Drivers, Barriers & Challenges in Thailand Housing Industry

The Thailand housing industry is propelled by significant growth drivers including a steadily recovering economy, increasing urbanization, and a growing young demographic entering the housing market. Technological advancements in construction and proptech are enhancing efficiency and buyer experience. Government incentives and infrastructure development projects, particularly in and around major cities, further stimulate demand.

Conversely, significant barriers and challenges exist. Regulatory complexities and lengthy approval processes can impede project timelines. Supply chain disruptions and rising material costs can impact profitability. Intense competition among developers, particularly in popular segments, can lead to price pressures. Economic uncertainties and potential interest rate hikes pose risks to affordability and buyer sentiment.

Growth Drivers in the Thailand Housing Industry Market

The Thailand housing industry is experiencing robust growth driven by several key factors. Economic recovery and rising disposable incomes are empowering more individuals to enter the property market. Urbanization and a growing young professional demographic create sustained demand for apartments and condominiums in metropolitan areas. Government infrastructure development projects, such as enhanced public transportation networks, are increasing the attractiveness and accessibility of new residential locations. Furthermore, technological advancements in construction and proptech are improving efficiency and offering innovative living solutions, while evolving consumer preferences for sustainable and community-oriented living are opening new market niches.

Challenges Impacting Thailand Housing Industry Growth

Several challenges are impacting the growth trajectory of the Thailand housing industry. Regulatory hurdles and bureaucratic processes can lead to project delays and increased costs. Fluctuations in construction material prices and potential supply chain disruptions can significantly affect project viability and profitability. Intense competition among a large number of developers, particularly in saturated segments, can lead to margin compression. Economic uncertainties and rising interest rates pose a significant risk to housing affordability and buyer demand. Furthermore, changing consumer preferences and the need for sustainable development require continuous adaptation and investment.

Key Players Shaping the Thailand Housing Industry Market

- LPN Development PCL

- Pruksa Real Estate Public Company Limited

- Hipflat

- Origin Property Public Co Ltd

- Land and Houses Public Company Limited

- Supalai Company Limited

- Property Perfect Public Company Limited

- Sansiri Public Co Ltd

- AP (THAILAND) PUBLIC COMPANY LIMITED

- Ananda Development Public Company Limited

- Quality Houses Public Company Limited

- Magnolia Quality Development Corp Co Ltd

Significant Thailand Housing Industry Industry Milestones

- 2019: Launch of several large-scale mixed-use developments integrating residential, retail, and office spaces, signalling a trend towards comprehensive urban living.

- 2020: Increased adoption of digital sales platforms and virtual property tours due to global pandemic, accelerating proptech integration.

- 2021: Government initiatives to boost the property market through stimulus packages and relaxed loan-to-value ratios for first-time homebuyers.

- 2022: Growing emphasis on sustainable building practices and green certifications in new residential projects.

- 2023: Significant M&A activities as larger developers consolidated portfolios and acquired smaller competitors.

- 2024 (Estimated): Anticipated increase in foreign property investment as travel restrictions eased and economic sentiment improved.

Future Outlook for Thailand Housing Industry Market

The future outlook for the Thailand housing industry remains exceptionally bright, driven by sustained economic growth, ongoing urbanization, and evolving lifestyle demands. Strategic opportunities lie in developing integrated, smart, and sustainable housing solutions that cater to a diverse range of demographics. The market is expected to witness continued innovation in proptech, enhancing customer experience and operational efficiency. Developers focusing on affordable housing, niche segments like co-living, and properties in strategically developing areas are poised for significant success. With a projected CAGR of XX%, the industry presents a compelling landscape for investment and development through 2033.

Thailand Housing Industry Segmentation

-

1. Type

- 1.1. Apartments and Condominiums

- 1.2. Landed Houses and Villas

-

2. Key Cities

- 2.1. Bangkok

- 2.2. Chiang Mais

- 2.3. Nontha Buri

- 2.4. Samut Prakan

Thailand Housing Industry Segmentation By Geography

- 1. Thailand

Thailand Housing Industry Regional Market Share

Geographic Coverage of Thailand Housing Industry

Thailand Housing Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.54% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Apartments and Condominiums

- 5.1.2. Landed Houses and Villas

- 5.2. Market Analysis, Insights and Forecast - by Key Cities

- 5.2.1. Bangkok

- 5.2.2. Chiang Mais

- 5.2.3. Nontha Buri

- 5.2.4. Samut Prakan

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Thailand

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Thailand Housing Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Apartments and Condominiums

- 6.1.2. Landed Houses and Villas

- 6.2. Market Analysis, Insights and Forecast - by Key Cities

- 6.2.1. Bangkok

- 6.2.2. Chiang Mais

- 6.2.3. Nontha Buri

- 6.2.4. Samut Prakan

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 LPN Development PCL

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Pruksa Real Estate Public Company Limited

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Hipflat

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Origin Property Public Co Ltd

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Land and Houses Public Company Limited

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Supalai Company Limited

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Property Perfect Public Company Limited

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Sansiri Public Co Ltd

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 AP (THAILAND) PUBLIC COMPANY LIMITED

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Ananda Development Public Company Limited

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Quality Houses Public Company Limited*List Not Exhaustive

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Magnolia Quality Development Corp Co Ltd

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.1 LPN Development PCL

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Thailand Housing Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Thailand Housing Industry Share (%) by Company 2025

List of Tables

- Table 1: Thailand Housing Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: Thailand Housing Industry Revenue Million Forecast, by Key Cities 2020 & 2033

- Table 3: Thailand Housing Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Thailand Housing Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 5: Thailand Housing Industry Revenue Million Forecast, by Key Cities 2020 & 2033

- Table 6: Thailand Housing Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Thailand Housing Industry?

The projected CAGR is approximately 5.54%.

2. Which companies are prominent players in the Thailand Housing Industry?

Key companies in the market include LPN Development PCL, Pruksa Real Estate Public Company Limited, Hipflat, Origin Property Public Co Ltd, Land and Houses Public Company Limited, Supalai Company Limited, Property Perfect Public Company Limited, Sansiri Public Co Ltd, AP (THAILAND) PUBLIC COMPANY LIMITED, Ananda Development Public Company Limited, Quality Houses Public Company Limited*List Not Exhaustive, Magnolia Quality Development Corp Co Ltd.

3. What are the main segments of the Thailand Housing Industry?

The market segments include Type, Key Cities.

4. Can you provide details about the market size?

The market size is estimated to be USD 154.51 Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Government initiatives and huge investments driving the market4.; Vision 2030 and allied projects driving the market.

6. What are the notable trends driving market growth?

Bangkok and Vicinities Witnessing Growth in the Residential Sector.

7. Are there any restraints impacting market growth?

4.; High construction costs affecting the market4.; Limited land availability affecting the growth of the market.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Thailand Housing Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Thailand Housing Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Thailand Housing Industry?

To stay informed about further developments, trends, and reports in the Thailand Housing Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence