Key Insights

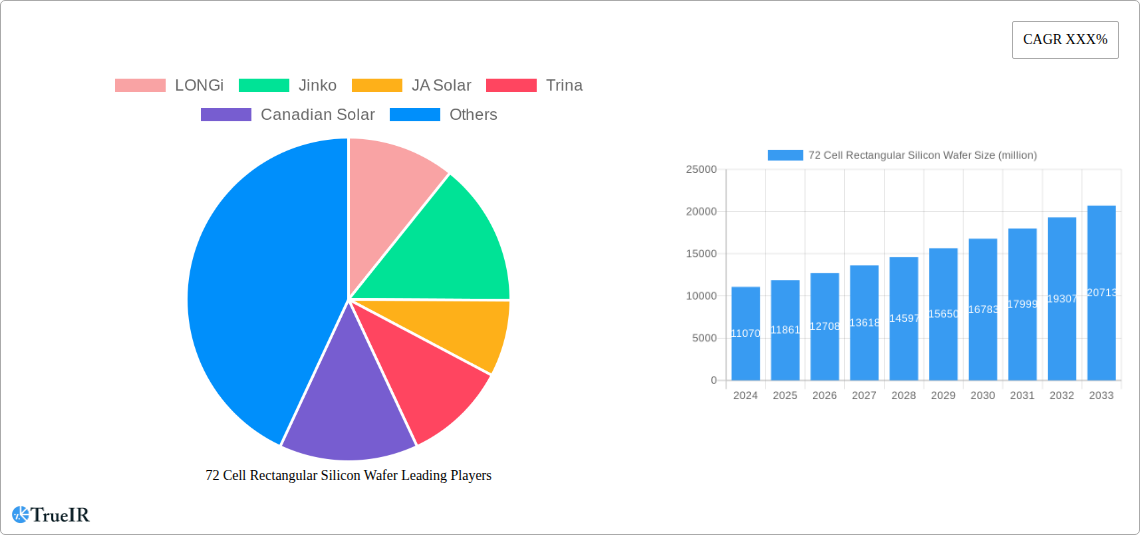

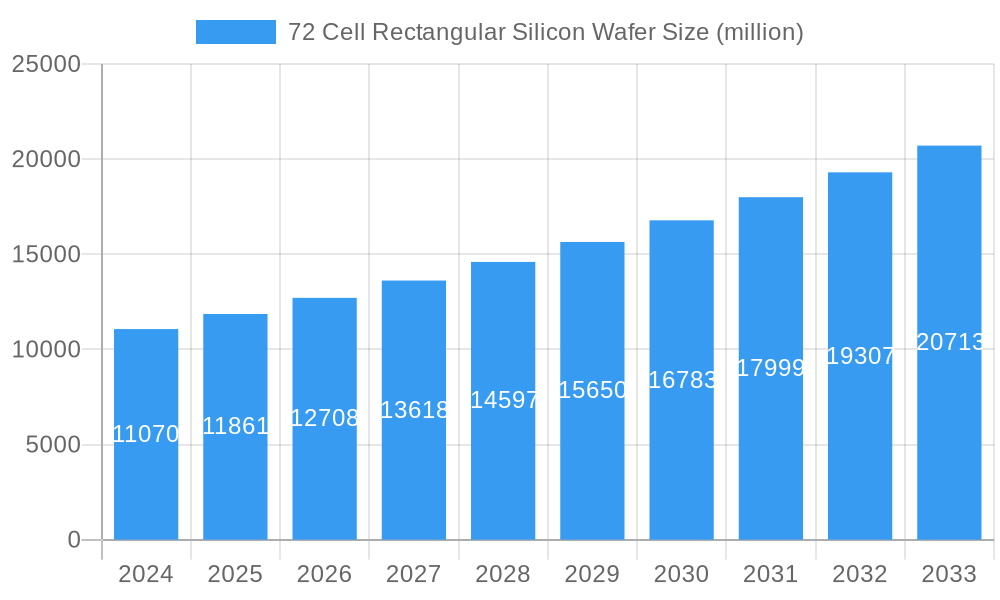

The global market for 72-cell rectangular silicon wafers is experiencing robust growth, driven by the escalating demand for solar energy solutions across residential, industrial, and large-scale power generation sectors. In 2024, the market size is estimated at USD 11.07 billion, poised for significant expansion. The compound annual growth rate (CAGR) is projected at 7.1% over the forecast period of 2025-2033, indicating sustained momentum. Key drivers fueling this growth include supportive government policies, declining solar panel costs, and increasing awareness of environmental sustainability. The transition towards cleaner energy sources is paramount, making silicon wafers a foundational component for renewable energy infrastructure. The prevalence of P-type silicon wafers continues to dominate, though N-type silicon wafers are gaining traction due to their superior efficiency, reflecting an ongoing technological evolution within the industry.

72 Cell Rectangular Silicon Wafer Market Size (In Billion)

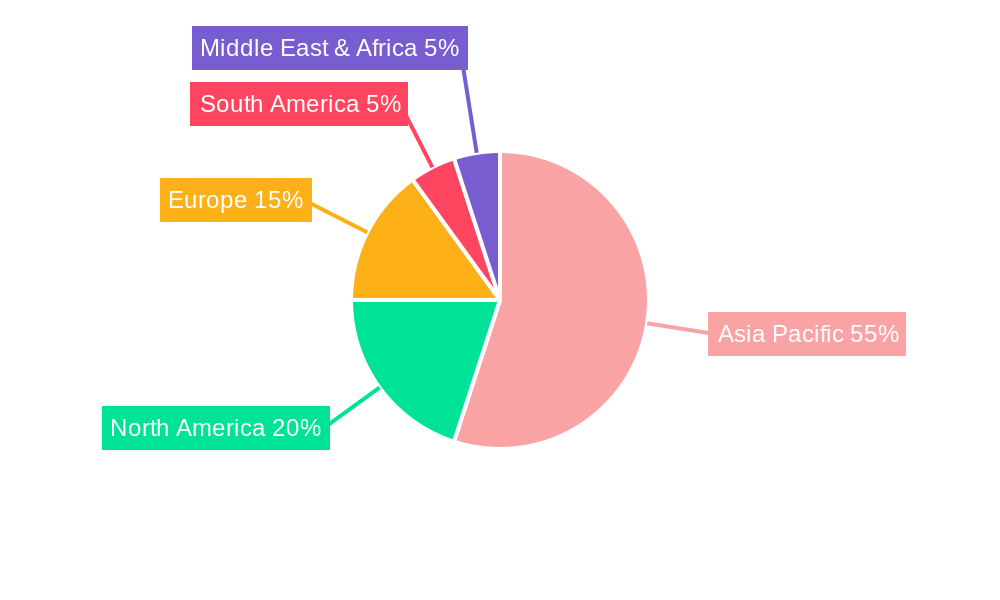

The market landscape is characterized by intense competition and a focus on technological advancements to improve wafer quality and reduce manufacturing costs. Major players like LONGi, Jinko Solar, and JA Solar are at the forefront, investing heavily in research and development to enhance wafer performance and scalability. While the market benefits from strong demand, potential restraints include fluctuations in raw material prices, supply chain disruptions, and evolving trade policies. Nevertheless, the overarching trend towards decarbonization and the critical role of solar power in achieving global energy targets ensure a bright future for the 72-cell rectangular silicon wafer market. Geographically, Asia Pacific, particularly China, is expected to maintain its leadership position due to its extensive manufacturing capabilities and a substantial domestic solar market.

72 Cell Rectangular Silicon Wafer Company Market Share

72 Cell Rectangular Silicon Wafer Market: Comprehensive Industry Analysis and Future Projections (2019-2033)

This comprehensive report delves into the dynamic 72 cell rectangular silicon wafer market, providing an in-depth analysis of its structure, trends, opportunities, and future outlook. Leveraging high-volume keywords and detailed quantitative and qualitative insights, this report is optimized for SEO and designed to engage industry professionals, investors, and stakeholders. The study covers the historical period from 2019 to 2024, with the base year at 2025, and projects significant growth through the forecast period of 2025–2033.

72 Cell Rectangular Silicon Wafer Market Structure & Competitive Landscape

The 72 cell rectangular silicon wafer market exhibits a moderately concentrated structure, with a significant portion of market share held by a few dominant players. Innovation drivers are primarily focused on enhancing wafer purity, reducing manufacturing costs, and improving efficiency to meet the escalating demand for high-performance solar modules. Regulatory impacts, particularly government incentives for renewable energy adoption and stricter environmental standards, are crucial in shaping market dynamics. Product substitutes, such as different wafer sizes and alternative semiconductor materials, pose a limited threat due to the established infrastructure and cost-effectiveness of silicon wafers. End-user segmentation reveals a strong reliance on the solar photovoltaic (PV) industry, with growing adoption across residential, industrial, and large-scale power generation applications. Mergers and acquisitions (M&A) trends are notable, indicating strategic consolidation aimed at achieving economies of scale, expanding production capacity, and securing supply chains. M&A volumes are estimated to be in the billions of dollars over the forecast period. Concentration ratios are projected to remain robust, driven by significant capital investments required for advanced manufacturing facilities.

72 Cell Rectangular Silicon Wafer Market Trends & Opportunities

The global 72 cell rectangular silicon wafer market is poised for substantial growth, driven by the accelerating transition towards renewable energy sources and the increasing affordability of solar power. The market size is projected to expand significantly, with an estimated Compound Annual Growth Rate (CAGR) of over 15% during the forecast period. This growth is fueled by a confluence of factors, including supportive government policies, declining solar panel costs, and rising environmental consciousness worldwide. Technological shifts are playing a pivotal role, with a strong emphasis on advancements in P-type and N-type silicon wafer technologies. N-type wafers, in particular, are gaining traction due to their superior efficiency and lower degradation rates, making them a preferred choice for high-performance solar applications. Consumer preferences are increasingly leaning towards more efficient and aesthetically pleasing solar solutions, which are facilitated by the improved performance characteristics of 72 cell rectangular wafers. Competitive dynamics are characterized by intense price competition and a continuous pursuit of technological innovation among leading manufacturers. The market penetration rate of solar PV systems is expected to climb steadily, further bolstering the demand for silicon wafers. Opportunities abound in emerging markets with ambitious renewable energy targets, as well as in the development of next-generation wafer technologies that offer enhanced power conversion efficiency and reduced material consumption. The continuous decline in manufacturing costs, driven by process optimization and economies of scale, presents a significant market opportunity for widespread solar adoption. The increasing focus on sustainability and circular economy principles is also creating opportunities for wafer recycling and the development of more eco-friendly manufacturing processes, further cementing the market's growth trajectory.

Dominant Markets & Segments in 72 Cell Rectangular Silicon Wafer

The Large Ground Power Stations segment is a dominant force in the 72 cell rectangular silicon wafer market, driven by substantial government investments in renewable energy infrastructure and the pursuit of large-scale decarbonization goals. Countries with ambitious solar energy targets, such as China, the United States, and India, are leading this growth, supported by favorable policies and land availability for utility-scale projects. The Industrial and Commercial Roofs segment is also exhibiting robust expansion, fueled by corporate sustainability initiatives and the economic benefits of on-site solar generation. This segment benefits from increasing awareness of energy independence and reduced operational costs for businesses. While the Residential Roofs segment is a vital component, its growth, though steady, is often more influenced by individual consumer economics and localized incentives.

Regarding wafer type, N-type Silicon Wafer is emerging as a key growth driver. Its superior electrical properties, leading to higher module efficiency and lower light-induced degradation, are making it increasingly attractive for both large-scale and residential applications. This shift is compelling manufacturers to invest heavily in N-type wafer production capabilities. P-type Silicon Wafers, while still commanding a significant market share due to their established cost-effectiveness and mature production processes, are facing increasing competition from their N-type counterparts.

Key growth drivers for market dominance include:

- Government Policies and Incentives: Subsidies, tax credits, and renewable energy mandates are critical in accelerating solar deployment, thus driving wafer demand.

- Infrastructure Development: Investments in grid modernization and energy storage solutions are crucial for integrating large volumes of solar power, further boosting demand for wafers.

- Technological Advancements: Continuous improvements in wafer quality and manufacturing efficiency directly translate to more affordable and higher-performing solar modules.

- Corporate Sustainability Goals: A growing number of corporations are setting ambitious renewable energy targets, driving demand for solar installations and consequently, silicon wafers.

- Cost Competitiveness of Solar PV: The declining levelized cost of electricity (LCOE) from solar power makes it an increasingly competitive energy source, stimulating market expansion.

72 Cell Rectangular Silicon Wafer Product Analysis

The 72 cell rectangular silicon wafer represents a pinnacle of efficiency and cost-effectiveness in solar technology. Innovations are focused on achieving higher purity silicon, reducing wafer thickness without compromising strength, and enhancing surface passivation techniques. These advancements directly translate to improved power conversion efficiency in solar modules, making them more competitive against traditional energy sources. The competitive advantage lies in their optimized size for module manufacturing, enabling higher power output per module and reduced balance-of-system costs. Their widespread adoption across residential, commercial, and utility-scale applications underscores their market fit and technological maturity.

Key Drivers, Barriers & Challenges in 72 Cell Rectangular Silicon Wafer

Key Drivers:

- Global Energy Transition: The urgent need to decarbonize energy systems and combat climate change is the primary driver, propelling the growth of solar PV and, consequently, silicon wafer demand.

- Declining Solar PV Costs: Continuous improvements in manufacturing efficiency and economies of scale have made solar power one of the cheapest forms of electricity generation, spurring adoption.

- Supportive Government Policies: Renewable energy targets, subsidies, and tax incentives worldwide are creating a favorable environment for solar installations.

- Technological Advancements: Innovations in wafer technology, such as N-type silicon, are enhancing solar module efficiency and performance.

Barriers & Challenges:

- Supply Chain Volatility: Geopolitical factors, raw material availability (e.g., polysilicon), and shipping disruptions can impact supply chain stability and increase costs, with potential impacts in the billions of dollars on raw material procurement and logistics.

- Regulatory Hurdles: Navigating diverse international regulations, permitting processes, and trade policies can slow down project development.

- Competitive Pressures: Intense price competition among wafer manufacturers and module assemblers can squeeze profit margins.

- Land Use and Environmental Concerns: Large-scale solar projects can face challenges related to land availability, environmental impact assessments, and public perception.

Growth Drivers in the 72 Cell Rectangular Silicon Wafer Market

The 72 cell rectangular silicon wafer market is experiencing significant growth propelled by the global imperative for clean energy. Technological advancements, particularly in the efficiency and cost-effectiveness of N-type silicon wafers, are major catalysts. Economic drivers include the declining levelized cost of solar electricity, making it increasingly competitive with fossil fuels. Supportive government policies worldwide, including renewable energy mandates and financial incentives, further accelerate market penetration. The increasing corporate commitment to sustainability goals is also a significant growth factor, driving demand for on-site solar generation and Power Purchase Agreements (PPAs).

Challenges Impacting 72 Cell Rectangular Silicon Wafer Growth

The growth of the 72 cell rectangular silicon wafer market is not without its obstacles. Regulatory complexities and trade barriers in different regions can create market access challenges. Supply chain issues, including the availability and price volatility of key raw materials like polysilicon, pose a significant restraint, with potential impacts in the billions of dollars on production costs. Intense competition among manufacturers can lead to price erosion, impacting profitability. Furthermore, the increasing demand for land for large-scale solar farms can lead to land-use conflicts and environmental concerns.

Key Players Shaping the 72 Cell Rectangular Silicon Wafer Market

- LONGi

- Jinko

- JA Solar

- Trina Solar

- Canadian Solar

- Tongwei

- Chint

- Risen Energy

- Huasheng New Energy

- Aixun

- ShinEtsu Chemical

- Sumco

- Global Wafers Co.

- Siltronic AG

- LG Siltron

- SK Siltron

- Soitec

- Wafer Works Corporation

- Okmetic Ltd.

Significant 72 Cell Rectangular Silicon Wafer Industry Milestones

- 2019: Significant advancements in PERC (Passivated Emitter and Rear Cell) technology, improving wafer efficiency.

- 2020: Increased investment in N-type silicon wafer R&D and pilot production lines by major players.

- 2021: Global polysilicon supply chain pressures leading to price hikes, impacting wafer manufacturing costs.

- 2022: Notable increase in M&A activity as companies seek to consolidate and expand capacity in the billions of dollars range.

- 2023: Continued innovation in wafer thinning techniques to reduce silicon consumption and cost.

- 2024: Growing emphasis on sustainability and the circular economy in wafer production processes.

Future Outlook for 72 Cell Rectangular Silicon Wafer Market

The future outlook for the 72 cell rectangular silicon wafer market is exceptionally bright, driven by the unwavering global commitment to renewable energy. Strategic opportunities lie in the expansion of N-type wafer production capacity to meet escalating demand, further technological innovations to enhance efficiency and reduce costs, and the penetration of emerging markets with substantial solar potential. The market is expected to witness continued growth, propelled by ongoing supportive policies, advancements in solar technology, and the increasing economic viability of solar power, with an estimated market value in the hundreds of billions of dollars.

72 Cell Rectangular Silicon Wafer Segmentation

-

1. Application

- 1.1. Residential Roofs

- 1.2. Industrial and Commercial Roofs

- 1.3. Large Ground Power Stations

-

2. Type

- 2.1. P-type Silicon Wafer

- 2.2. N-type Silicon Wafer

72 Cell Rectangular Silicon Wafer Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

72 Cell Rectangular Silicon Wafer Regional Market Share

Geographic Coverage of 72 Cell Rectangular Silicon Wafer

72 Cell Rectangular Silicon Wafer REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global 72 Cell Rectangular Silicon Wafer Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Residential Roofs

- 5.1.2. Industrial and Commercial Roofs

- 5.1.3. Large Ground Power Stations

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. P-type Silicon Wafer

- 5.2.2. N-type Silicon Wafer

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America 72 Cell Rectangular Silicon Wafer Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Residential Roofs

- 6.1.2. Industrial and Commercial Roofs

- 6.1.3. Large Ground Power Stations

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. P-type Silicon Wafer

- 6.2.2. N-type Silicon Wafer

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America 72 Cell Rectangular Silicon Wafer Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Residential Roofs

- 7.1.2. Industrial and Commercial Roofs

- 7.1.3. Large Ground Power Stations

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. P-type Silicon Wafer

- 7.2.2. N-type Silicon Wafer

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe 72 Cell Rectangular Silicon Wafer Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Residential Roofs

- 8.1.2. Industrial and Commercial Roofs

- 8.1.3. Large Ground Power Stations

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. P-type Silicon Wafer

- 8.2.2. N-type Silicon Wafer

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa 72 Cell Rectangular Silicon Wafer Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Residential Roofs

- 9.1.2. Industrial and Commercial Roofs

- 9.1.3. Large Ground Power Stations

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. P-type Silicon Wafer

- 9.2.2. N-type Silicon Wafer

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific 72 Cell Rectangular Silicon Wafer Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Residential Roofs

- 10.1.2. Industrial and Commercial Roofs

- 10.1.3. Large Ground Power Stations

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. P-type Silicon Wafer

- 10.2.2. N-type Silicon Wafer

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 LONGi

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Jinko

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 JA Solar

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Trina

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Canadian Solar

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Tongwei

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Chint

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Risen

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Huasheng

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Aixun

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 ShinEtsu

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Sumco

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Global Wafers Co

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Siltronic AG

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 LG Silrton

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 SK Siltron

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Soitec

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Wafer Works

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 Okmetic

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.1 LONGi

List of Figures

- Figure 1: Global 72 Cell Rectangular Silicon Wafer Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America 72 Cell Rectangular Silicon Wafer Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America 72 Cell Rectangular Silicon Wafer Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America 72 Cell Rectangular Silicon Wafer Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America 72 Cell Rectangular Silicon Wafer Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America 72 Cell Rectangular Silicon Wafer Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America 72 Cell Rectangular Silicon Wafer Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America 72 Cell Rectangular Silicon Wafer Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America 72 Cell Rectangular Silicon Wafer Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America 72 Cell Rectangular Silicon Wafer Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America 72 Cell Rectangular Silicon Wafer Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America 72 Cell Rectangular Silicon Wafer Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America 72 Cell Rectangular Silicon Wafer Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe 72 Cell Rectangular Silicon Wafer Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe 72 Cell Rectangular Silicon Wafer Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe 72 Cell Rectangular Silicon Wafer Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe 72 Cell Rectangular Silicon Wafer Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe 72 Cell Rectangular Silicon Wafer Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe 72 Cell Rectangular Silicon Wafer Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa 72 Cell Rectangular Silicon Wafer Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa 72 Cell Rectangular Silicon Wafer Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa 72 Cell Rectangular Silicon Wafer Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa 72 Cell Rectangular Silicon Wafer Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa 72 Cell Rectangular Silicon Wafer Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa 72 Cell Rectangular Silicon Wafer Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific 72 Cell Rectangular Silicon Wafer Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific 72 Cell Rectangular Silicon Wafer Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific 72 Cell Rectangular Silicon Wafer Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific 72 Cell Rectangular Silicon Wafer Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific 72 Cell Rectangular Silicon Wafer Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific 72 Cell Rectangular Silicon Wafer Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global 72 Cell Rectangular Silicon Wafer Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global 72 Cell Rectangular Silicon Wafer Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global 72 Cell Rectangular Silicon Wafer Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global 72 Cell Rectangular Silicon Wafer Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global 72 Cell Rectangular Silicon Wafer Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global 72 Cell Rectangular Silicon Wafer Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States 72 Cell Rectangular Silicon Wafer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada 72 Cell Rectangular Silicon Wafer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico 72 Cell Rectangular Silicon Wafer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global 72 Cell Rectangular Silicon Wafer Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global 72 Cell Rectangular Silicon Wafer Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global 72 Cell Rectangular Silicon Wafer Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil 72 Cell Rectangular Silicon Wafer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina 72 Cell Rectangular Silicon Wafer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America 72 Cell Rectangular Silicon Wafer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global 72 Cell Rectangular Silicon Wafer Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global 72 Cell Rectangular Silicon Wafer Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global 72 Cell Rectangular Silicon Wafer Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom 72 Cell Rectangular Silicon Wafer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany 72 Cell Rectangular Silicon Wafer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France 72 Cell Rectangular Silicon Wafer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy 72 Cell Rectangular Silicon Wafer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain 72 Cell Rectangular Silicon Wafer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia 72 Cell Rectangular Silicon Wafer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux 72 Cell Rectangular Silicon Wafer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics 72 Cell Rectangular Silicon Wafer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe 72 Cell Rectangular Silicon Wafer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global 72 Cell Rectangular Silicon Wafer Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global 72 Cell Rectangular Silicon Wafer Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global 72 Cell Rectangular Silicon Wafer Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey 72 Cell Rectangular Silicon Wafer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel 72 Cell Rectangular Silicon Wafer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC 72 Cell Rectangular Silicon Wafer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa 72 Cell Rectangular Silicon Wafer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa 72 Cell Rectangular Silicon Wafer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa 72 Cell Rectangular Silicon Wafer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global 72 Cell Rectangular Silicon Wafer Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global 72 Cell Rectangular Silicon Wafer Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global 72 Cell Rectangular Silicon Wafer Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China 72 Cell Rectangular Silicon Wafer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India 72 Cell Rectangular Silicon Wafer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan 72 Cell Rectangular Silicon Wafer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea 72 Cell Rectangular Silicon Wafer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN 72 Cell Rectangular Silicon Wafer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania 72 Cell Rectangular Silicon Wafer Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific 72 Cell Rectangular Silicon Wafer Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the 72 Cell Rectangular Silicon Wafer?

The projected CAGR is approximately 7.1%.

2. Which companies are prominent players in the 72 Cell Rectangular Silicon Wafer?

Key companies in the market include LONGi, Jinko, JA Solar, Trina, Canadian Solar, Tongwei, Chint, Risen, Huasheng, Aixun, ShinEtsu, Sumco, Global Wafers Co, Siltronic AG, LG Silrton, SK Siltron, Soitec, Wafer Works, Okmetic.

3. What are the main segments of the 72 Cell Rectangular Silicon Wafer?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4250.00, USD 6375.00, and USD 8500.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "72 Cell Rectangular Silicon Wafer," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the 72 Cell Rectangular Silicon Wafer report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the 72 Cell Rectangular Silicon Wafer?

To stay informed about further developments, trends, and reports in the 72 Cell Rectangular Silicon Wafer, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence