Key Insights

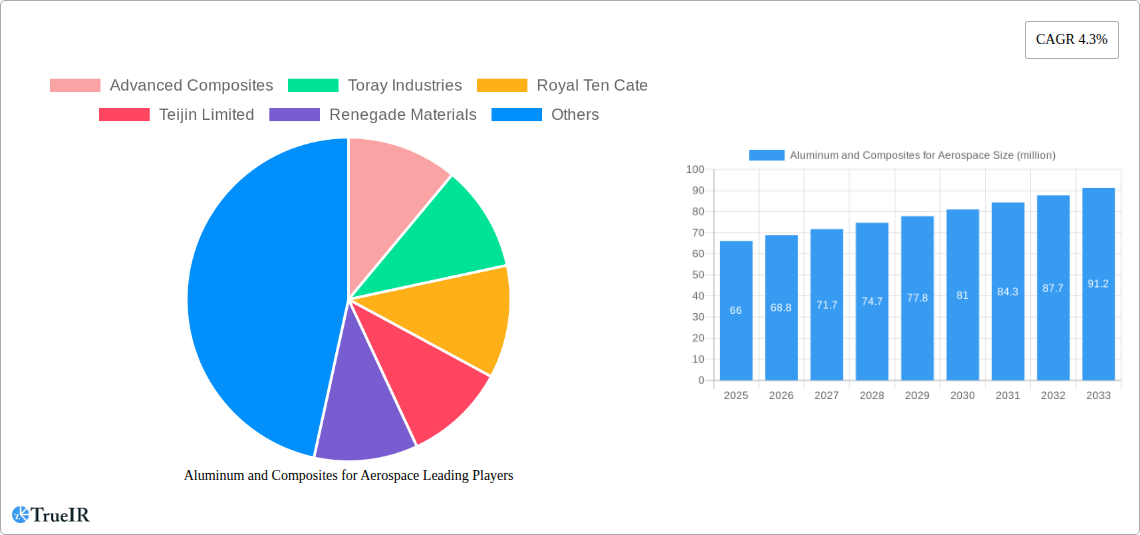

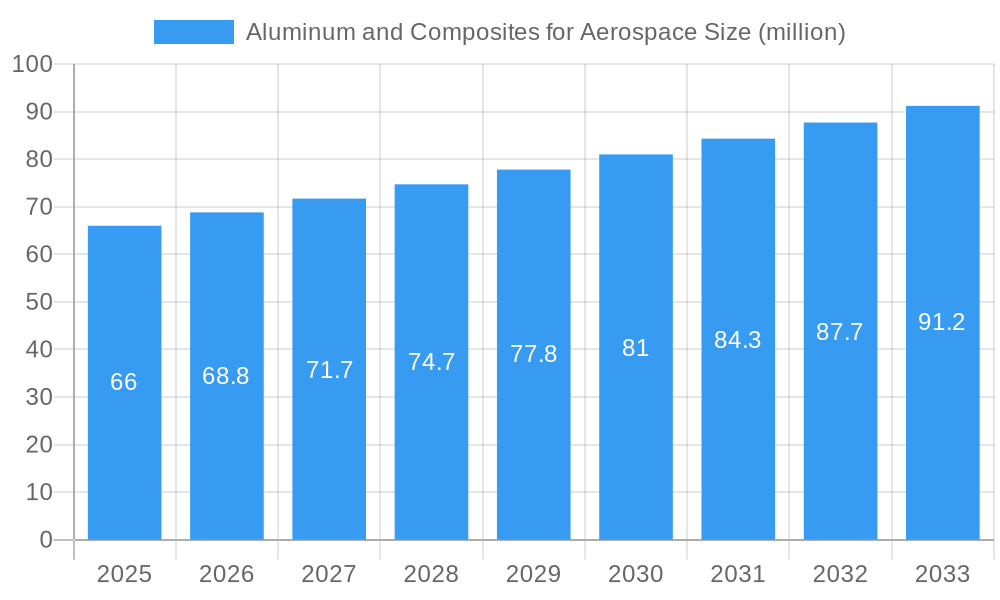

The global market for Aluminum and Composites for Aerospace is poised for significant expansion, driven by the burgeoning demand for lighter, stronger, and more fuel-efficient aircraft. The market size for aluminum and composites in the aerospace sector is estimated at $66 million in 2025, projected to grow at a Compound Annual Growth Rate (CAGR) of 4.3% through 2033. This growth is primarily fueled by continuous advancements in composite material technology, offering superior strength-to-weight ratios compared to traditional aluminum alloys. The increasing production of both commercial and military aircraft, coupled with the evolving requirements for enhanced performance and reduced operational costs, are key market drivers. The aerospace industry's commitment to sustainability also plays a crucial role, as lightweight materials contribute directly to lower fuel consumption and reduced emissions. Furthermore, the ongoing research and development in new material formulations and manufacturing processes are expected to unlock new applications and further propel market adoption.

Aluminum and Composites for Aerospace Market Size (In Million)

The market is segmented into applications including Commercial Aircraft, Military Aircraft, and Helicopters, with the Commercial Aircraft segment expected to dominate due to the sustained global demand for air travel and fleet modernization. In terms of material types, both Aluminum and Composites hold significant shares, with composites gaining increasing traction due to their advantageous properties. Key market players are heavily investing in research and development to innovate next-generation materials and manufacturing techniques. Despite the positive outlook, certain restraints such as the high initial cost of advanced composite materials and the stringent certification processes in the aerospace industry may pose challenges. However, the long-term growth trajectory remains robust, supported by technological innovations and the unwavering demand from the global aviation sector for cutting-edge materials that ensure safety, performance, and economic viability.

Aluminum and Composites for Aerospace Company Market Share

Here is a dynamic, SEO-optimized report description for Aluminum and Composites for Aerospace, designed for immediate use and maximum impact:

Aluminum and Composites for Aerospace Market Structure & Competitive Landscape

The global Aluminum and Composites for Aerospace market is characterized by a moderately concentrated structure, driven by significant capital investments, stringent quality control, and continuous technological innovation. Key players like Toray Industries, Advanced Composites, Solvay S, and HEXEL Works dominate with substantial market share, leveraging their extensive R&D capabilities and established supply chains. Innovation drivers are primarily focused on weight reduction for enhanced fuel efficiency and increased payload capacity, directly impacting the commercial aircraft and military aircraft segments. Regulatory impacts from bodies like the FAA and EASA significantly influence material certifications and manufacturing processes, creating high barriers to entry. Product substitutes, while present, struggle to match the performance-to-weight ratios of advanced composites and specialized aerospace-grade aluminum alloys. End-user segmentation reveals a strong reliance on OEMs for both commercial and defense aviation, with helicopter manufacturers also representing a vital segment. Mergers and acquisitions (M&A) activity remains a significant trend, with an estimated XX million in transaction values observed historically, aimed at consolidating market share, acquiring proprietary technologies, and expanding geographical reach. For instance, acquisitions of specialized composite manufacturers by larger material suppliers are common to enhance their integrated offerings.

- Market Concentration: Moderately concentrated, with top 5 players holding approximately 60-70% market share.

- Innovation Drivers: Fuel efficiency, weight reduction, enhanced performance, advanced manufacturing techniques.

- Regulatory Impact: Stringent certification processes, safety standards, environmental regulations.

- Product Substitutes: High-strength steel, titanium (limited application due to weight/cost), advanced polymers.

- End-User Segmentation: Commercial Aircraft OEMs, Military Aircraft OEMs, Helicopter Manufacturers.

- M&A Trends: Consolidation, technology acquisition, market expansion (XX million historical transaction volume).

Aluminum and Composites for Aerospace Market Trends & Opportunities

The Aluminum and Composites for Aerospace market is experiencing robust growth, projected to reach an impressive XX billion by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of XX% from the base year 2025. This expansion is fundamentally fueled by the insatiable demand for lighter, stronger, and more fuel-efficient aircraft across all segments. The commercial aircraft sector, driven by increasing global air travel and the need to replace aging fleets with next-generation, eco-friendlier models, is a primary growth engine. The continuous development of advanced composite materials, such as carbon fiber reinforced polymers (CFRPs), and the evolution of high-performance aerospace aluminum alloys are at the forefront of technological shifts. These advancements enable the production of airframes, wings, and critical components with significantly improved structural integrity and reduced overall aircraft weight, translating directly into substantial operational cost savings for airlines.

Consumer preferences, manifested through airline demands for lower operating expenses and reduced environmental impact, are pushing OEMs to adopt lighter materials. This creates a significant market penetration opportunity for suppliers of cutting-edge aluminum alloys and composite materials. The competitive dynamics within the market are intensifying, with established giants like Toray Industries, Advanced Composites, and Solvay S investing heavily in R&D to maintain their leadership, while emerging players like Renegade Materials are carving out niches with specialized offerings. The market penetration rate for composites in primary aircraft structures has steadily increased, now accounting for over XX% in many new commercial aircraft designs.

Furthermore, the military aircraft segment is witnessing a surge in demand for advanced materials to support the development of stealthier, more agile, and higher-performance combat and transport aircraft. Composites offer exceptional strength-to-weight ratios and radar-absorbent properties, making them indispensable for modern defense applications. Helicopter manufacturers are also increasingly incorporating composite rotor blades and airframes to enhance performance, reduce vibration, and improve fuel efficiency. The growing emphasis on sustainability and circular economy principles within the aerospace industry presents a significant opportunity for the development and adoption of recyclable composite materials and advanced aluminum recycling initiatives.

The forecast period (2025–2033) is expected to witness accelerated adoption of these materials, driven by ambitious aircraft development programs and ongoing technological advancements. The market is ripe with opportunities for companies that can offer innovative material solutions, cost-effective manufacturing processes, and a strong commitment to sustainability and performance. The trend towards larger, more fuel-efficient commercial aircraft, such as the next-generation narrow-body and wide-body jets, will continue to be a major driver for increased material consumption.

Dominant Markets & Segments in Aluminum and Composites for Aerospace

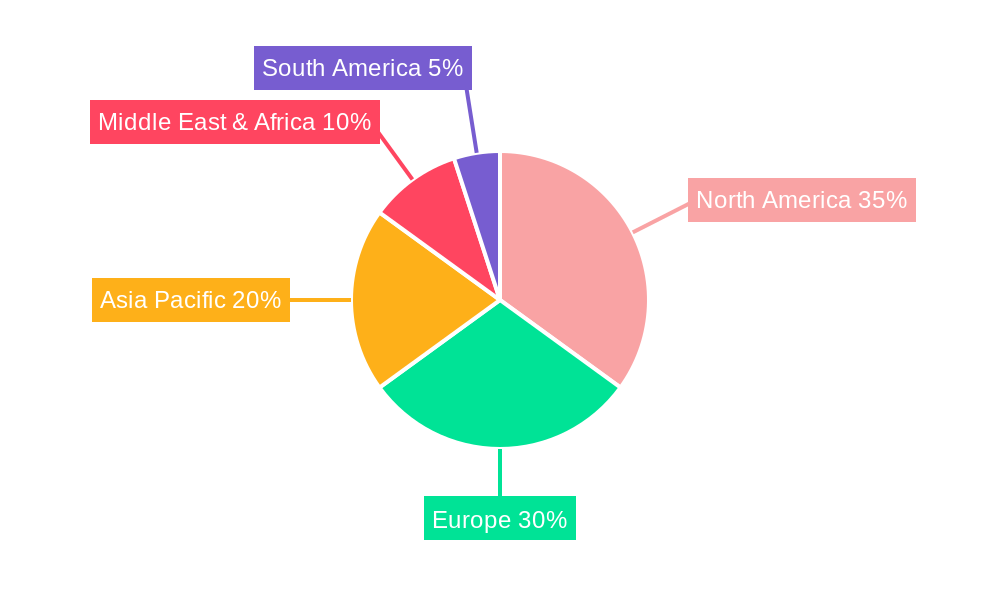

The Aluminum and Composites for Aerospace market is experiencing dominance in specific regions and segments, largely dictated by the presence of major aerospace manufacturing hubs and the specific demands of each application. North America, with its colossal defense industry and a substantial commercial aircraft manufacturing base, stands out as the leading region, accounting for an estimated XX% of the global market share. The United States, in particular, drives this dominance through leading aerospace giants and extensive government investment in aviation research and development. Europe, home to Airbus and a significant network of component suppliers, follows closely, holding approximately XX% of the market.

Within the Application segmentation, Commercial Aircraft represent the largest and most influential segment, projected to account for over XX% of the market value during the forecast period. This is a direct consequence of the ever-growing global demand for air travel, necessitating the continuous production and upgrade of commercial fleets. The drive for fuel efficiency and reduced emissions in commercial aviation makes lightweight aluminum alloys and advanced composites indispensable.

The Types of materials also play a critical role in market dominance. While aluminum has a long-standing legacy in aerospace due to its cost-effectiveness and well-established manufacturing processes, advanced composites are rapidly gaining ground and are projected to witness a higher CAGR of XX% compared to aluminum's XX% during the forecast period. Composites are increasingly preferred for primary structures, fuselage sections, and wings due to their superior strength-to-weight ratios, enabling significant weight reduction and consequently, fuel savings.

The Military Aircraft segment, while smaller in volume compared to commercial aviation, is a high-value segment characterized by the adoption of the most advanced materials. The need for enhanced performance, survivability, and stealth capabilities in defense applications drives the demand for sophisticated composite materials and specialized aluminum alloys. Helicopter manufacturing, although a niche segment, also contributes significantly, particularly in the development of lighter and more agile rotor systems and airframes.

Key growth drivers for market dominance include:

- Infrastructure Development: Expansion of airports and air traffic control systems globally, supporting increased flight operations and aircraft demand.

- Government Policies: Robust defense spending in major economies, coupled with mandates for fuel efficiency and emissions reduction in civil aviation, directly influences material selection.

- Technological Advancements: Continuous innovation in material science leading to lighter, stronger, and more durable aluminum alloys and composite materials.

- OEM Procurement Strategies: Long-term contracts and partnerships between material suppliers and major aircraft manufacturers.

Aluminum and Composites for Aerospace Product Analysis

The aerospace industry's relentless pursuit of enhanced performance and efficiency is driving significant product innovations in both aluminum and composite materials. Advanced aerospace aluminum alloys, such as Al-Li alloys, offer superior strength-to-weight ratios and improved fatigue resistance compared to conventional alloys, making them ideal for fuselage structures and wing components. Composite materials, particularly carbon fiber reinforced polymers (CFRPs), are revolutionizing aircraft design, enabling the creation of complex aerodynamic shapes, integral structures, and significantly lighter airframes. These materials offer exceptional strength, stiffness, and corrosion resistance, leading to substantial weight savings and improved fuel efficiency. Competitive advantages stem from tailored material properties for specific applications, superior performance under extreme conditions, and the potential for reduced manufacturing complexity and assembly time.

Key Drivers, Barriers & Challenges in Aluminum and Composites for Aerospace

The Aluminum and Composites for Aerospace market is propelled by several key drivers. Technological advancements in material science, leading to lighter, stronger, and more durable aluminum alloys and composite materials, are paramount. The increasing global demand for air travel fuels the need for new aircraft, thereby driving material consumption. Government initiatives promoting fuel efficiency and reduced emissions in aviation create a strong incentive for adopting these advanced materials.

Conversely, significant barriers and challenges exist. The high cost of advanced composite materials and the specialized manufacturing processes required present a substantial economic hurdle. Stringent regulatory approval processes for new materials and designs are time-consuming and expensive. Supply chain disruptions, geopolitical instability, and the availability of skilled labor for advanced manufacturing also pose significant challenges. Competitive pressures from established players and the constant need for innovation to stay ahead further complicate the landscape.

Key Drivers:

- Technological Innovation: Development of lightweight, high-strength materials.

- Demand for Fuel Efficiency: Regulatory and economic pressure to reduce emissions.

- Growth in Air Travel: Increased aircraft production and fleet expansion.

- Military Modernization Programs: Demand for advanced materials in defense applications.

Challenges and Restraints:

- High Material and Manufacturing Costs: Particularly for advanced composites.

- Stringent Regulatory Hurdles: Certification processes for new materials.

- Supply Chain Volatility: Geopolitical risks and raw material availability.

- Skilled Workforce Shortage: Need for specialized manufacturing expertise.

- Recycling and Sustainability Concerns: Developing end-of-life solutions for composite materials.

Growth Drivers in the Aluminum and Composites for Aerospace Market

The growth of the Aluminum and Composites for Aerospace market is primarily fueled by technological advancements in material science, enabling the development of ever-lighter, stronger, and more durable materials. The increasing global air travel demand necessitates the production of new aircraft and the replacement of older, less fuel-efficient fleets, directly translating into higher material consumption. Furthermore, stringent environmental regulations and a growing emphasis on sustainability are pushing manufacturers to adopt advanced composites and optimized aluminum alloys to achieve greater fuel efficiency and reduced carbon emissions. Government initiatives, including defense modernization programs and investments in aerospace R&D, also significantly contribute to market expansion.

Challenges Impacting Aluminum and Composites for Aerospace Growth

Several critical challenges impact the growth of the Aluminum and Composites for Aerospace market. The high cost associated with advanced composite materials and their complex manufacturing processes remains a significant barrier. Stringent and lengthy regulatory approval processes for new materials and aircraft designs add to development timelines and expenses. Supply chain vulnerabilities, exacerbated by geopolitical uncertainties and the availability of key raw materials, can lead to production delays and cost overruns. Furthermore, the aerospace industry faces a shortage of skilled labor capable of handling advanced composite manufacturing and intricate aluminum processing, hindering widespread adoption. Competitive pressures and the need for continuous innovation to maintain market share also present ongoing challenges.

Key Players Shaping the Aluminum and Composites for Aerospace Market

- Advanced Composites

- Toray Industries

- Royal Ten Cate

- Teijin Limited

- Renegade Materials

- Owens Corning

- Materion Corp

- HEXEL Works

- Solvay S

- Kaiser Aluminum

- Novelis

- AMSpec

- Constellium

- Smiths Metal Centers

Significant Aluminum and Composites for Aerospace Industry Milestones

- 2019: Launch of a new generation of Al-Li alloys offering XX% weight reduction for commercial aircraft primary structures.

- 2020: Toray Industries announces a XX million investment in expanding its advanced composite manufacturing capacity to meet growing demand.

- 2021: Solvay S introduces a novel high-temperature composite resin system for next-generation jet engines.

- 2022: HEXEL Works acquires a specialized composite repair solutions provider, enhancing its aftermarket services.

- 2023: Renegade Materials receives FAA certification for its advanced aluminum-lithium alloy for military aircraft applications.

- 2024: Teijin Limited partners with a major aircraft OEM to develop recyclable composite materials for a new eco-friendly aircraft program.

Future Outlook for Aluminum and Composites for Aerospace Market

The future outlook for the Aluminum and Composites for Aerospace market is exceptionally promising, driven by sustained demand for fuel-efficient aircraft and advancements in material technology. Strategic opportunities lie in the continued development of sustainable and recyclable composite materials, addressing growing environmental concerns. The increasing adoption of automation and artificial intelligence in manufacturing processes will further enhance efficiency and reduce costs. Market potential is significant as next-generation aircraft programs across commercial, military, and helicopter segments increasingly rely on lightweight, high-performance materials to achieve ambitious performance and sustainability goals. Companies that can offer innovative solutions, robust supply chains, and a commitment to eco-friendly practices will be well-positioned for substantial growth in the coming years.

Aluminum and Composites for Aerospace Segmentation

-

1. Application

- 1.1. Commercial Aircraft

- 1.2. Military Aircraft

- 1.3. Helicopter

-

2. Types

- 2.1. Aluminum

- 2.2. Composites

Aluminum and Composites for Aerospace Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Aluminum and Composites for Aerospace Regional Market Share

Geographic Coverage of Aluminum and Composites for Aerospace

Aluminum and Composites for Aerospace REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Aluminum and Composites for Aerospace Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Commercial Aircraft

- 5.1.2. Military Aircraft

- 5.1.3. Helicopter

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Aluminum

- 5.2.2. Composites

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Aluminum and Composites for Aerospace Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Commercial Aircraft

- 6.1.2. Military Aircraft

- 6.1.3. Helicopter

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Aluminum

- 6.2.2. Composites

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Aluminum and Composites for Aerospace Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Commercial Aircraft

- 7.1.2. Military Aircraft

- 7.1.3. Helicopter

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Aluminum

- 7.2.2. Composites

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Aluminum and Composites for Aerospace Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Commercial Aircraft

- 8.1.2. Military Aircraft

- 8.1.3. Helicopter

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Aluminum

- 8.2.2. Composites

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Aluminum and Composites for Aerospace Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Commercial Aircraft

- 9.1.2. Military Aircraft

- 9.1.3. Helicopter

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Aluminum

- 9.2.2. Composites

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Aluminum and Composites for Aerospace Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Commercial Aircraft

- 10.1.2. Military Aircraft

- 10.1.3. Helicopter

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Aluminum

- 10.2.2. Composites

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Advanced Composites

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Toray Industries

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Royal Ten Cate

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Teijin Limited

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Renegade Materials

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Owens Corning

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Materion Corp

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 HEXEL Works

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Solvay S

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Kaiser Aluminum

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Novelis

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 AMSpec

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Constellium

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Smiths Metal Centers

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.1 Advanced Composites

List of Figures

- Figure 1: Global Aluminum and Composites for Aerospace Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Aluminum and Composites for Aerospace Revenue (million), by Application 2025 & 2033

- Figure 3: North America Aluminum and Composites for Aerospace Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Aluminum and Composites for Aerospace Revenue (million), by Types 2025 & 2033

- Figure 5: North America Aluminum and Composites for Aerospace Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Aluminum and Composites for Aerospace Revenue (million), by Country 2025 & 2033

- Figure 7: North America Aluminum and Composites for Aerospace Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Aluminum and Composites for Aerospace Revenue (million), by Application 2025 & 2033

- Figure 9: South America Aluminum and Composites for Aerospace Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Aluminum and Composites for Aerospace Revenue (million), by Types 2025 & 2033

- Figure 11: South America Aluminum and Composites for Aerospace Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Aluminum and Composites for Aerospace Revenue (million), by Country 2025 & 2033

- Figure 13: South America Aluminum and Composites for Aerospace Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Aluminum and Composites for Aerospace Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Aluminum and Composites for Aerospace Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Aluminum and Composites for Aerospace Revenue (million), by Types 2025 & 2033

- Figure 17: Europe Aluminum and Composites for Aerospace Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Aluminum and Composites for Aerospace Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Aluminum and Composites for Aerospace Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Aluminum and Composites for Aerospace Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Aluminum and Composites for Aerospace Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Aluminum and Composites for Aerospace Revenue (million), by Types 2025 & 2033

- Figure 23: Middle East & Africa Aluminum and Composites for Aerospace Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Aluminum and Composites for Aerospace Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Aluminum and Composites for Aerospace Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Aluminum and Composites for Aerospace Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Aluminum and Composites for Aerospace Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Aluminum and Composites for Aerospace Revenue (million), by Types 2025 & 2033

- Figure 29: Asia Pacific Aluminum and Composites for Aerospace Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Aluminum and Composites for Aerospace Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Aluminum and Composites for Aerospace Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Aluminum and Composites for Aerospace Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Aluminum and Composites for Aerospace Revenue million Forecast, by Types 2020 & 2033

- Table 3: Global Aluminum and Composites for Aerospace Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Aluminum and Composites for Aerospace Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Aluminum and Composites for Aerospace Revenue million Forecast, by Types 2020 & 2033

- Table 6: Global Aluminum and Composites for Aerospace Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Aluminum and Composites for Aerospace Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Aluminum and Composites for Aerospace Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Aluminum and Composites for Aerospace Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Aluminum and Composites for Aerospace Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Aluminum and Composites for Aerospace Revenue million Forecast, by Types 2020 & 2033

- Table 12: Global Aluminum and Composites for Aerospace Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Aluminum and Composites for Aerospace Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Aluminum and Composites for Aerospace Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Aluminum and Composites for Aerospace Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Aluminum and Composites for Aerospace Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Aluminum and Composites for Aerospace Revenue million Forecast, by Types 2020 & 2033

- Table 18: Global Aluminum and Composites for Aerospace Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Aluminum and Composites for Aerospace Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Aluminum and Composites for Aerospace Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Aluminum and Composites for Aerospace Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Aluminum and Composites for Aerospace Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Aluminum and Composites for Aerospace Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Aluminum and Composites for Aerospace Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Aluminum and Composites for Aerospace Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Aluminum and Composites for Aerospace Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Aluminum and Composites for Aerospace Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Aluminum and Composites for Aerospace Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Aluminum and Composites for Aerospace Revenue million Forecast, by Types 2020 & 2033

- Table 30: Global Aluminum and Composites for Aerospace Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Aluminum and Composites for Aerospace Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Aluminum and Composites for Aerospace Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Aluminum and Composites for Aerospace Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Aluminum and Composites for Aerospace Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Aluminum and Composites for Aerospace Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Aluminum and Composites for Aerospace Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Aluminum and Composites for Aerospace Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Aluminum and Composites for Aerospace Revenue million Forecast, by Types 2020 & 2033

- Table 39: Global Aluminum and Composites for Aerospace Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Aluminum and Composites for Aerospace Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Aluminum and Composites for Aerospace Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Aluminum and Composites for Aerospace Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Aluminum and Composites for Aerospace Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Aluminum and Composites for Aerospace Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Aluminum and Composites for Aerospace Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Aluminum and Composites for Aerospace Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Aluminum and Composites for Aerospace?

The projected CAGR is approximately 4.3%.

2. Which companies are prominent players in the Aluminum and Composites for Aerospace?

Key companies in the market include Advanced Composites, Toray Industries, Royal Ten Cate, Teijin Limited, Renegade Materials, Owens Corning, Materion Corp, HEXEL Works, Solvay S, Kaiser Aluminum, Novelis, AMSpec, Constellium, Smiths Metal Centers.

3. What are the main segments of the Aluminum and Composites for Aerospace?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 66 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Aluminum and Composites for Aerospace," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Aluminum and Composites for Aerospace report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Aluminum and Composites for Aerospace?

To stay informed about further developments, trends, and reports in the Aluminum and Composites for Aerospace, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence