Key Insights

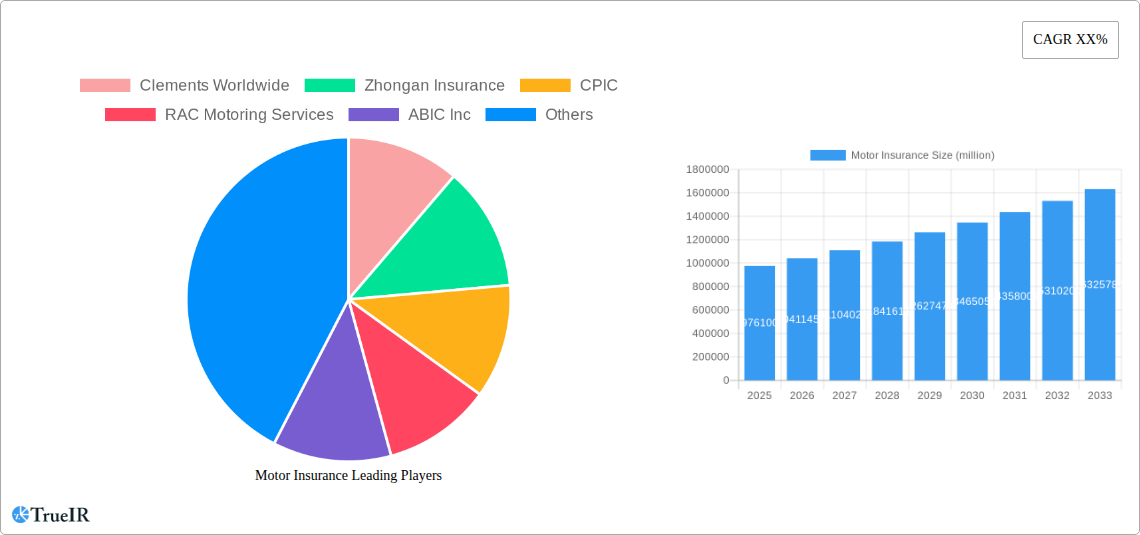

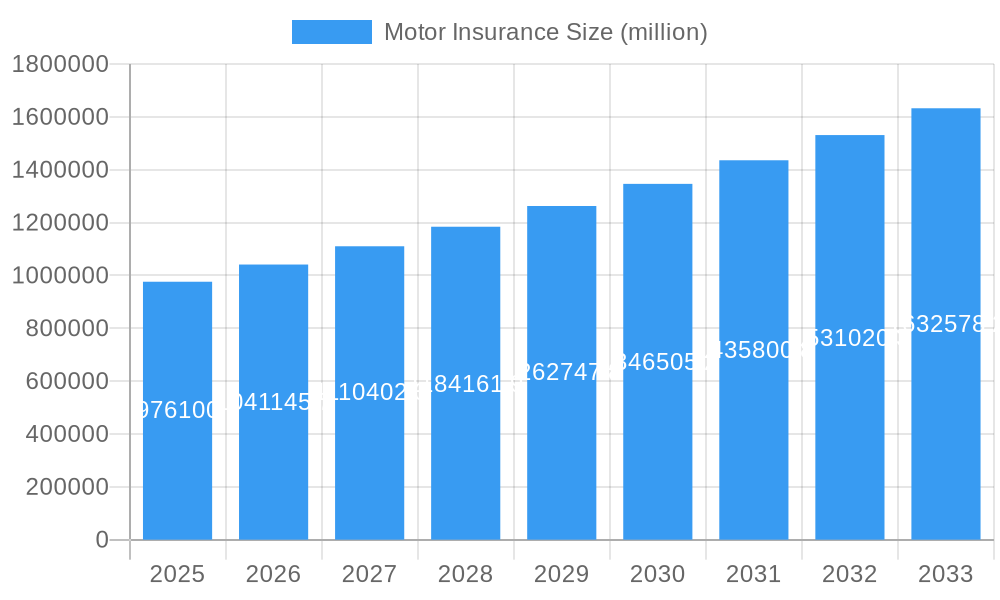

The global Motor Insurance market is poised for significant growth, projected to reach USD 976.1 billion by 2025 with a robust Compound Annual Growth Rate (CAGR) of 6.7% during the forecast period of 2025-2033. This expansion is primarily fueled by a burgeoning global vehicle parc, increasing vehicle complexity, and a rising awareness among consumers regarding the financial protection offered by motor insurance policies. The growing adoption of advanced driver-assistance systems (ADAS) and the surge in electric vehicle (EV) sales are also contributing factors, as these technologies often necessitate specialized and more comprehensive insurance coverage. Furthermore, evolving regulatory landscapes across various regions, mandating certain levels of insurance for vehicle operation, are underpinning this market's upward trajectory. The market is witnessing a dynamic shift, with a growing preference for third-party liability coverage due to its mandatory nature and affordability, while comprehensive insurance is gaining traction among vehicle owners seeking broader protection against damage, theft, and other unforeseen events.

Motor Insurance Market Size (In Billion)

The market's momentum is further amplified by several key trends, including the increasing digitalization of insurance processes, from policy acquisition to claims settlement. Insurers are leveraging advanced analytics and AI to offer personalized policies, streamline operations, and improve customer experiences. The proliferation of telematics and IoT devices in vehicles is enabling usage-based insurance (UBI) models, allowing policyholders to benefit from customized premiums based on their driving behavior. However, the market also faces certain restraints, such as intense competition leading to price wars, increasing frequency and severity of claims due to rising accident rates in certain regions, and the potential for fraud within the insurance ecosystem. Despite these challenges, the overarching growth drivers and the continuous innovation within the motor insurance sector are expected to maintain a strong growth trajectory for the foreseeable future.

Motor Insurance Company Market Share

Motor Insurance Market: Comprehensive Analysis and Future Outlook (2019–2033)

This in-depth report offers a dynamic, SEO-optimized analysis of the global Motor Insurance market, meticulously crafted for industry professionals and decision-makers. Leveraging high-volume keywords and a detailed study period from 2019 to 2033, with a base and estimated year of 2025, this report provides unparalleled insight into market structures, competitive landscapes, emerging trends, and future growth trajectories. We delve into every facet of the motor insurance ecosystem, from product innovation and regional dominance to key drivers and challenges, presenting a comprehensive view of a market poised for significant evolution, projected to reach billions in value.

Motor Insurance Market Structure & Competitive Landscape

The global Motor Insurance market exhibits a dynamic and evolving competitive landscape, characterized by a mix of established global giants and specialized regional players. Market concentration varies significantly across different geographies, with some regions dominated by a few large insurers, while others present a more fragmented picture. Innovation drivers are increasingly focused on technological advancements, including the integration of telematics for personalized pricing, AI-powered claims processing, and enhanced digital customer experiences. Regulatory impacts play a crucial role, with evolving legislation around data privacy, autonomous vehicles, and consumer protection shaping market entry and operational strategies. Product substitutes are emerging, particularly in the form of usage-based insurance (UBI) and pay-as-you-drive (PAYD) models, challenging traditional comprehensive and third-party liability offerings. End-user segmentation is becoming more granular, with insurers tailoring products for specific vehicle types and driver profiles. Merger and acquisition (M&A) trends are expected to continue as companies seek to expand their market share, acquire new technologies, and achieve economies of scale, with an estimated volume of billions in M&A deals anticipated over the forecast period.

- Key aspects of market concentration: Varies by region, with some markets dominated by a few insurers.

- Dominant innovation drivers: Telematics, AI in claims, digital customer engagement.

- Significant regulatory influences: Data privacy laws, autonomous vehicle regulations.

- Emerging product substitutes: Usage-based insurance (UBI), Pay-As-You-Drive (PAYD).

- M&A trend overview: Expected to see billions in deal volumes for market expansion and tech acquisition.

Motor Insurance Market Trends & Opportunities

The Motor Insurance market is projected for substantial growth, with an estimated Compound Annual Growth Rate (CAGR) of XX% over the forecast period. This expansion is fueled by a confluence of technological shifts, evolving consumer preferences, and dynamic competitive forces. The increasing penetration of connected vehicles and the proliferation of advanced driver-assistance systems (ADAS) are creating new opportunities for insurers to gather rich data for risk assessment and personalized pricing, moving beyond traditional demographic factors. The rise of electric vehicles (EVs) and battery cars presents a unique segment with distinct insurance needs, including battery warranty coverage and charging infrastructure protection, opening up new revenue streams. Consumer preferences are shifting towards digital-first experiences, demanding seamless online policy purchase, claims filing, and customer support. Insurers that can deliver intuitive digital platforms and personalized services are poised to gain a significant competitive advantage.

Furthermore, the increasing adoption of autonomous vehicle technology, while still in its nascent stages for widespread public use, necessitates a proactive approach to developing new insurance frameworks. The legal and ethical implications of AI-driven driving require robust insurance solutions that can address liability in novel ways. The competitive dynamics are intensifying, with traditional insurers facing disruption from InsurTech startups and tech giants exploring entry into the insurance space. This competitive pressure is driving innovation in product development and operational efficiency. The global market size is expected to reach billions by 2033, driven by these interconnected trends. Opportunities also lie in underserved markets and niche segments, such as commercial fleets, specialized vehicles like tractors, and the growing demand for motorcycle insurance in emerging economies. The ability to adapt to these evolving trends, embrace new technologies, and cater to changing consumer expectations will be critical for sustained success in the motor insurance sector.

Dominant Markets & Segments in Motor Insurance

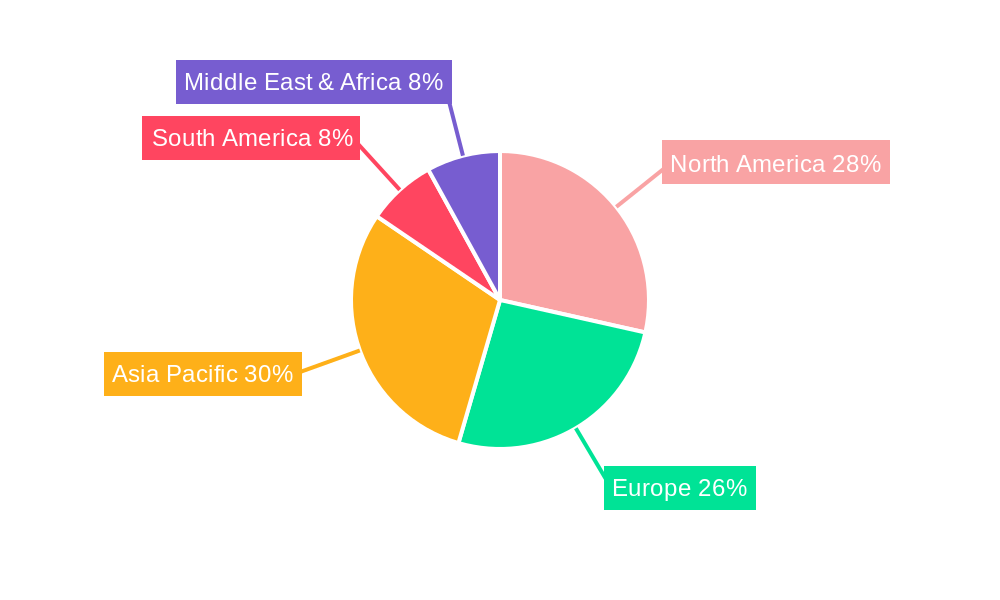

The Motor Insurance market exhibits distinct regional dominance and segment-specific growth patterns. North America and Europe currently lead in terms of market penetration and premium volume, driven by a mature automotive industry, established regulatory frameworks, and high levels of vehicle ownership. However, the Asia-Pacific region is emerging as a significant growth engine, propelled by a rapidly expanding middle class, increasing vehicle sales, and a growing demand for comprehensive insurance coverage. Within this vast market, the Car segment remains the largest and most dominant, accounting for a substantial portion of total premiums. This is attributed to the sheer volume of passenger vehicles on the road worldwide.

The Battery Car segment, while currently smaller, is experiencing exponential growth and represents a critical area of future expansion. Government incentives for EV adoption, coupled with advancements in battery technology and charging infrastructure, are driving this surge. Insurers are actively developing specialized products to cover battery degradation, charging station damage, and the unique risks associated with electric powertrains. The Comprehensive insurance type continues to be the preferred choice for many vehicle owners due to its broad coverage against accidental damage, theft, and natural disasters, contributing significantly to overall market value. However, Third-Party Liability remains a mandatory requirement in many jurisdictions, ensuring a stable and substantial segment.

- Regional Dominance: North America and Europe lead; Asia-Pacific shows high growth.

- Leading Application Segment: Car segment holds the largest market share.

- High-Growth Application Segment: Battery Car segment exhibits rapid expansion due to EV adoption.

- Dominant Insurance Type: Comprehensive coverage is widely preferred.

- Mandatory Insurance Type: Third-Party Liability remains a fundamental segment.

- Key Growth Drivers:

- Infrastructure Development: Expansion of EV charging networks and road infrastructure in emerging markets.

- Policy Support: Government incentives for EV purchases and stricter road safety regulations.

- Technological Advancements: Integration of telematics and AI for enhanced risk assessment and claims processing.

- Consumer Awareness: Increasing understanding of insurance benefits and risk mitigation.

Motor Insurance Product Analysis

Motor insurance products are undergoing significant innovation, driven by technological advancements and evolving market demands. Comprehensive policies are being enhanced with features like roadside assistance, key cover, and new-for-old replacement options, offering greater value to consumers. The application of telematics is revolutionizing car insurance, enabling usage-based pricing models that reward safe driving habits with lower premiums. This data-driven approach also allows for more accurate risk profiling for battery cars, considering charging patterns and driving styles. Third-party liability insurance remains a cornerstone, but insurers are exploring ways to streamline claims processing and improve customer communication through digital platforms. Competitive advantages are increasingly derived from superior digital customer experience, rapid claims settlement, and the ability to offer tailored solutions for niche segments like tractors and motorcycles.

Key Drivers, Barriers & Challenges in Motor Insurance

Key Drivers: The Motor Insurance market is propelled by several key forces. Technological advancements, particularly the widespread adoption of telematics and AI, are enabling more accurate risk assessment and personalized pricing. Economic growth in emerging markets fuels increased vehicle ownership, thereby expanding the customer base for insurance. Favorable government policies and regulatory frameworks that mandate insurance coverage or promote safety initiatives also act as significant drivers. The growing awareness among consumers about the financial protection offered by motor insurance is another crucial factor.

Key Barriers & Challenges: Despite the positive drivers, the market faces considerable challenges. Stringent regulatory hurdles and compliance requirements can increase operational costs and slow down product innovation. Supply chain disruptions, impacting vehicle production and repair times, can lead to higher claims costs and longer settlement periods. Intense competitive pressures from both established players and new InsurTech entrants lead to price wars and reduced profit margins, with market penetration rates for certain advanced products still in the early stages. Furthermore, the increasing frequency and severity of natural disasters due to climate change pose a growing risk and can strain insurer solvency. The transition to electric vehicles also presents challenges in terms of accurately assessing new risks and developing appropriate pricing models, with initial market penetration for specialized EV insurance still below XX%.

Growth Drivers in the Motor Insurance Market

The motor insurance market's growth is primarily fueled by technological integration, economic expansion, and supportive regulatory environments. The pervasive adoption of telematics and AI is a cornerstone, enabling insurers to leverage vast amounts of data for precise risk segmentation and personalized premium calculation. This data-driven approach fosters innovation in product design and customer engagement. Economic growth, particularly in developing nations, directly correlates with rising vehicle ownership and a subsequent demand for motor insurance. Governments globally are increasingly implementing policies that mandate insurance coverage and promote road safety, further bolstering market expansion. The shift towards electric vehicles and advanced driver-assistance systems also creates new avenues for growth, as insurers develop specialized products and services to cater to these evolving automotive technologies.

Challenges Impacting Motor Insurance Growth

Several significant challenges impede the smooth growth of the motor insurance market. Regulatory complexities and the evolving landscape of data privacy laws pose substantial compliance burdens and can slow down the deployment of innovative digital solutions. Supply chain issues, affecting vehicle manufacturing and parts availability, can lead to extended repair times and increased claims costs. Intense competition among insurers, coupled with the emergence of disruptive InsurTech startups, often leads to aggressive pricing strategies, compressing profit margins and making it difficult for smaller players to compete. The increasing frequency and severity of extreme weather events, driven by climate change, present a substantial underwriting risk, potentially leading to higher claims payouts and impacting overall insurer profitability. The transition to autonomous vehicles also introduces a layer of uncertainty regarding liability and claims management, requiring careful consideration and adaptation.

Key Players Shaping the Motor Insurance Market

- Clements Worldwide

- Zhongan Insurance

- CPIC

- RAC Motoring Services

- ABIC Inc

- Progressive Casualty Insurance Company

- Zurich Insurance Group

- RSA Insurance Group

- Allstate Insurance Company

- NFU Mutual

- State Farm Mutual Automobile Insurance Company

- GEICO

- Chubb Ltd

- Nationwide Mutual Insurance

- Liberty Mutual Insurance

- Assicurazioni Generali

- PICC Property & Casualty

- Allianz SE

- Tesla

- Ping An Insurance(Group)

- PICC

Significant Motor Insurance Industry Milestones

- 2019: Increased adoption of telematics for usage-based insurance (UBI) programs, offering personalized pricing.

- 2020: Surge in digital claims processing due to pandemic-related restrictions, accelerating insurer digital transformation.

- 2021: Growing focus on electric vehicle (EV) insurance offerings, addressing battery-specific risks and charging infrastructure.

- 2022: Expansion of AI and machine learning in underwriting and claims fraud detection, leading to greater efficiency.

- 2023: Introduction of micro-insurance and on-demand insurance products catering to specific usage needs and shorter durations.

- 2024: Significant investments in cybersecurity to protect sensitive customer and vehicle data from evolving threats.

- 2025 (Estimated): Widespread integration of IoT devices in vehicles for enhanced real-time risk monitoring and predictive maintenance alerts.

- 2026 (Projected): Development of early regulatory frameworks for insuring fully autonomous vehicles in select regions.

- 2028 (Projected): Emergence of parametric insurance models triggered by pre-defined events for faster claims payout.

- 2030 (Projected): Mature market for Battery Car insurance with specialized products covering battery lifespan and performance guarantees.

- 2033 (Projected): Pervasive use of blockchain technology for secure and transparent claims processing and policy management.

Future Outlook for Motor Insurance Market

The future outlook for the Motor Insurance market is characterized by sustained growth and significant transformation. Strategic opportunities lie in leveraging advanced analytics and AI to create hyper-personalized insurance products that cater to the unique needs of individual drivers and evolving vehicle technologies. The continued expansion of electric and autonomous vehicles will necessitate innovative insurance solutions, opening up new revenue streams and competitive advantages for agile insurers. A key growth catalyst will be the seamless integration of InsurTech capabilities into traditional insurance models, enhancing customer experience and operational efficiency. Market penetration in emerging economies is expected to rise, driven by increasing vehicle ownership and a growing awareness of insurance benefits. The focus will increasingly shift towards proactive risk management and prevention, moving beyond traditional reactive claims handling.

Motor Insurance Segmentation

-

1. Application

- 1.1. Car

- 1.2. Tram

- 1.3. Battery Car

- 1.4. Motorcycle

- 1.5. Tractor

- 1.6. Other

-

2. Types

- 2.1. Third-party Liability

- 2.2. Comprehensive

Motor Insurance Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Motor Insurance Regional Market Share

Geographic Coverage of Motor Insurance

Motor Insurance REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Motor Insurance Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Car

- 5.1.2. Tram

- 5.1.3. Battery Car

- 5.1.4. Motorcycle

- 5.1.5. Tractor

- 5.1.6. Other

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Third-party Liability

- 5.2.2. Comprehensive

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Motor Insurance Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Car

- 6.1.2. Tram

- 6.1.3. Battery Car

- 6.1.4. Motorcycle

- 6.1.5. Tractor

- 6.1.6. Other

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Third-party Liability

- 6.2.2. Comprehensive

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Motor Insurance Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Car

- 7.1.2. Tram

- 7.1.3. Battery Car

- 7.1.4. Motorcycle

- 7.1.5. Tractor

- 7.1.6. Other

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Third-party Liability

- 7.2.2. Comprehensive

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Motor Insurance Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Car

- 8.1.2. Tram

- 8.1.3. Battery Car

- 8.1.4. Motorcycle

- 8.1.5. Tractor

- 8.1.6. Other

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Third-party Liability

- 8.2.2. Comprehensive

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Motor Insurance Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Car

- 9.1.2. Tram

- 9.1.3. Battery Car

- 9.1.4. Motorcycle

- 9.1.5. Tractor

- 9.1.6. Other

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Third-party Liability

- 9.2.2. Comprehensive

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Motor Insurance Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Car

- 10.1.2. Tram

- 10.1.3. Battery Car

- 10.1.4. Motorcycle

- 10.1.5. Tractor

- 10.1.6. Other

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Third-party Liability

- 10.2.2. Comprehensive

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Clements Worldwide

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Zhongan Insurance

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 CPIC

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 RAC Motoring Services

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 ABIC Inc

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Progressive Casualty Insurance Company

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Zurich Insurance Group

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 RSA Insurance Group

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Allstate Insurance Company

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 NFU Mutual

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 State Farm Mutual Automobile Insurance Company

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 GEICO

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Chubb Ltd

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Nationwide Mutual Insurance

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Liberty Mutual Insurance

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Assicurazioni Generali

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 PICC Property & Casualty

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Allianz SE

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 Tesla

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 Ping An Insurance(Group)

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.21 PICC

- 11.2.21.1. Overview

- 11.2.21.2. Products

- 11.2.21.3. SWOT Analysis

- 11.2.21.4. Recent Developments

- 11.2.21.5. Financials (Based on Availability)

- 11.2.1 Clements Worldwide

List of Figures

- Figure 1: Global Motor Insurance Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Motor Insurance Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Motor Insurance Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Motor Insurance Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Motor Insurance Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Motor Insurance Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Motor Insurance Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Motor Insurance Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Motor Insurance Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Motor Insurance Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Motor Insurance Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Motor Insurance Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Motor Insurance Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Motor Insurance Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Motor Insurance Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Motor Insurance Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Motor Insurance Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Motor Insurance Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Motor Insurance Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Motor Insurance Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Motor Insurance Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Motor Insurance Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Motor Insurance Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Motor Insurance Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Motor Insurance Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Motor Insurance Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Motor Insurance Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Motor Insurance Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Motor Insurance Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Motor Insurance Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Motor Insurance Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Motor Insurance Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Motor Insurance Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Motor Insurance Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Motor Insurance Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Motor Insurance Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Motor Insurance Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Motor Insurance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Motor Insurance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Motor Insurance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Motor Insurance Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Motor Insurance Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Motor Insurance Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Motor Insurance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Motor Insurance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Motor Insurance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Motor Insurance Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Motor Insurance Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Motor Insurance Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Motor Insurance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Motor Insurance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Motor Insurance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Motor Insurance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Motor Insurance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Motor Insurance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Motor Insurance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Motor Insurance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Motor Insurance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Motor Insurance Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Motor Insurance Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Motor Insurance Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Motor Insurance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Motor Insurance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Motor Insurance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Motor Insurance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Motor Insurance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Motor Insurance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Motor Insurance Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Motor Insurance Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Motor Insurance Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Motor Insurance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Motor Insurance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Motor Insurance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Motor Insurance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Motor Insurance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Motor Insurance Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Motor Insurance Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Motor Insurance?

The projected CAGR is approximately 4.5%.

2. Which companies are prominent players in the Motor Insurance?

Key companies in the market include Clements Worldwide, Zhongan Insurance, CPIC, RAC Motoring Services, ABIC Inc, Progressive Casualty Insurance Company, Zurich Insurance Group, RSA Insurance Group, Allstate Insurance Company, NFU Mutual, State Farm Mutual Automobile Insurance Company, GEICO, Chubb Ltd, Nationwide Mutual Insurance, Liberty Mutual Insurance, Assicurazioni Generali, PICC Property & Casualty, Allianz SE, Tesla, Ping An Insurance(Group), PICC.

3. What are the main segments of the Motor Insurance?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4350.00, USD 6525.00, and USD 8700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Motor Insurance," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Motor Insurance report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Motor Insurance?

To stay informed about further developments, trends, and reports in the Motor Insurance, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence