Key Insights

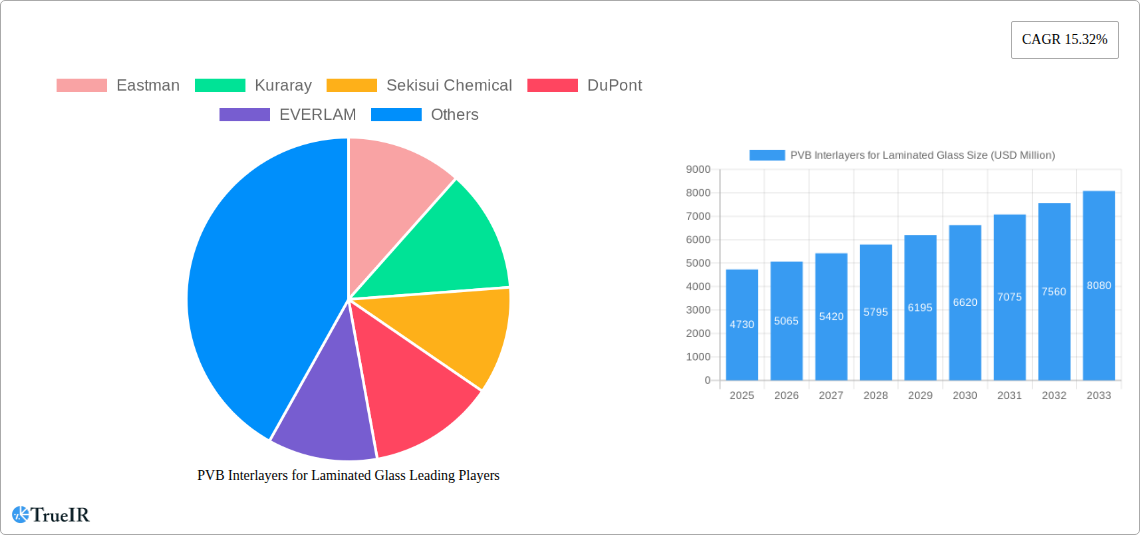

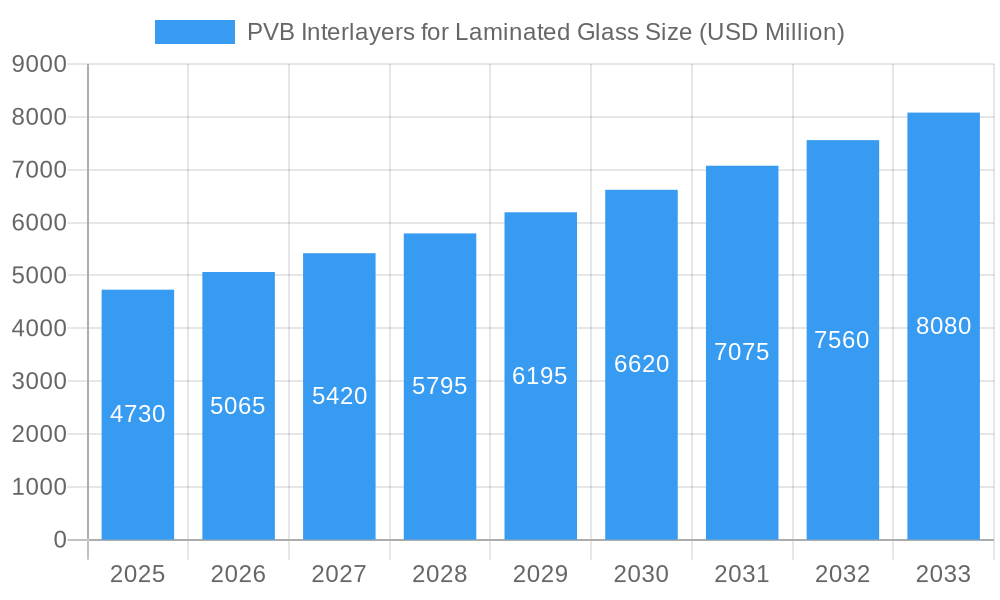

The global PVB Interlayers for Laminated Glass market is poised for significant expansion, projected to reach USD 4.73 billion in 2025, with a robust Compound Annual Growth Rate (CAGR) of 7.12% through 2033. This growth is primarily fueled by the increasing demand for enhanced safety, security, and acoustic insulation in construction and automotive applications. The rising adoption of laminated glass, which utilizes PVB interlayers for its shatter-resistant properties, is a key driver. Furthermore, advancements in PVB interlayer technology, offering improved UV resistance, color options, and specialized functionalities like solar control and privacy, are contributing to market dynamism. The growing global emphasis on energy efficiency and sustainable building practices also benefits the PVB interlayers market, as laminated glass contributes to better thermal performance and reduced energy consumption in buildings.

PVB Interlayers for Laminated Glass Market Size (In Billion)

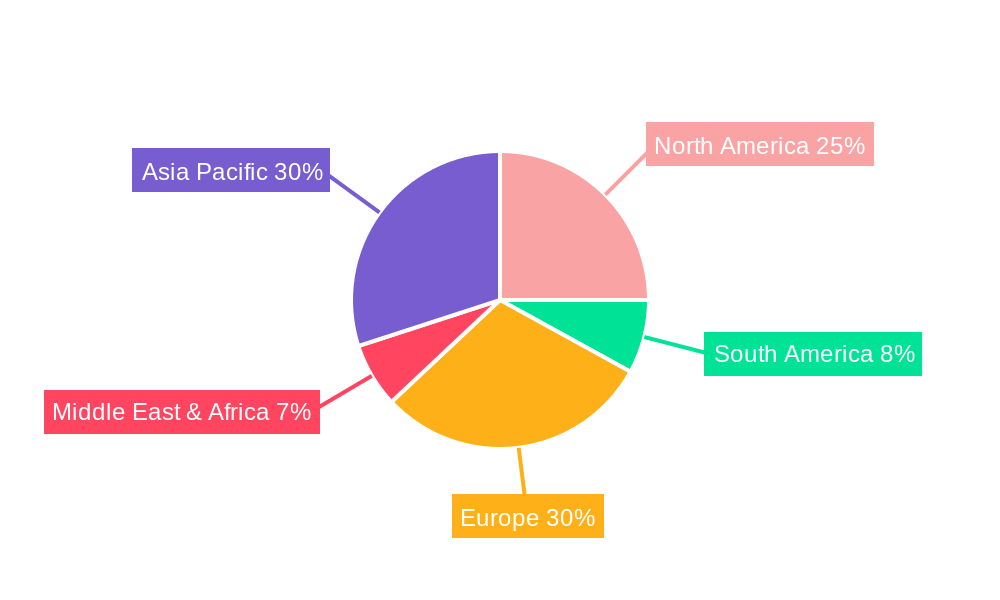

The market's trajectory is further shaped by evolving industry trends such as the development of thinner yet stronger PVB interlayers (e.g., below 0.02 inches) to reduce weight and cost, particularly in the automotive sector, and the increasing use of smart glass technologies incorporating PVB. However, the market faces some restraints, including the fluctuating raw material prices, specifically those linked to petroleum derivatives, and the presence of alternative interlayer materials, though PVB maintains a dominant position due to its performance advantages. Geographically, Asia Pacific is expected to witness the fastest growth, driven by rapid urbanization, infrastructure development, and a burgeoning automotive industry in countries like China and India. North America and Europe remain significant markets, characterized by stringent safety regulations and a mature automotive and construction sector. Key players like Eastman, Kuraray, and DuPont are actively engaged in product innovation and strategic partnerships to capitalize on these market opportunities.

PVB Interlayers for Laminated Glass Company Market Share

Comprehensive PVB Interlayers for Laminated Glass Market Report: Trends, Opportunities, and Competitive Analysis (2019-2033)

This in-depth report provides a comprehensive analysis of the global PVB (Polyvinyl Butyral) interlayers for laminated glass market. Covering the historical period from 2019 to 2024, the base year 2025, and a detailed forecast period extending to 2033, this study leverages a wealth of high-volume keywords to ensure optimal SEO performance and maximum engagement for industry stakeholders. We delve into market dynamics, competitive landscapes, technological advancements, and emerging opportunities within the commercial and residential sectors, examining various product types from below 0.02 inch to above 0.04 inch. Gain critical insights into the forces shaping this billion-dollar industry.

PVB Interlayers for Laminated Glass Market Structure & Competitive Landscape

The global PVB interlayers for laminated glass market is characterized by a moderately concentrated structure, driven by significant technological innovation and stringent regulatory frameworks governing safety and security in building and automotive applications. Key innovation drivers include the demand for enhanced acoustic insulation, UV protection, and increased impact resistance, pushing manufacturers to develop advanced formulations. Regulatory impacts, such as building codes mandating laminated glass for safety glazing and automotive safety standards, play a crucial role in market growth. Product substitutes, while present, are largely confined to niche applications, with PVB remaining the dominant choice for its balance of performance and cost-effectiveness. End-user segmentation clearly favors the Commercial and Residential applications, with the automotive sector also representing a substantial market share. Merger and acquisition (M&A) trends have been steady, consolidating market share among leading players and fostering technological integration. We anticipate the total M&A volume to reach approximately $5 billion over the forecast period, further influencing market concentration. The market concentration ratio for the top three players is estimated to be around 60%, indicating a significant but not entirely consolidated landscape.

PVB Interlayers for Laminated Glass Market Trends & Opportunities

The global PVB interlayers for laminated glass market is projected to experience robust growth, driven by escalating demand for safety, security, and energy-efficient solutions across various end-use industries. The market is anticipated to grow at a Compound Annual Growth Rate (CAGR) of approximately 7.2% from 2025 to 2033, reaching an estimated market size of $18 billion by the end of the forecast period. Technological shifts are at the forefront of this expansion, with ongoing research and development focusing on thinner yet stronger interlayers, improved acoustic performance for noise reduction in urban environments, and enhanced solar control properties for energy efficiency in buildings. Consumer preferences are increasingly leaning towards sustainable and aesthetically pleasing building materials, which aligns well with the advanced functionalities offered by modern PVB interlayers. The integration of PVB into smart glass technologies, offering dynamic tinting and privacy control, represents a significant emerging opportunity. Competitive dynamics are intensifying, with established players continuously investing in R&D and expanding their production capacities to meet global demand. Market penetration rates are expected to climb significantly, particularly in developing economies adopting stricter safety regulations and prioritizing modern architectural designs. The increasing adoption of PVB interlayers in residential renovations and new constructions, driven by rising disposable incomes and a greater emphasis on home safety and comfort, is a key trend. Furthermore, the automotive sector's unwavering focus on occupant safety and lightweighting strategies continues to fuel the demand for advanced PVB solutions that contribute to vehicle structural integrity and fuel efficiency. The growing adoption of architectural glass in the commercial sector, including high-rise buildings and modern office complexes, further bolsters market expansion. The development of specialized PVB interlayers with enhanced fire resistance and self-cleaning properties are also emerging as significant market differentiators and growth catalysts.

Dominant Markets & Segments in PVB Interlayers for Laminated Glass

The Commercial application segment is identified as the dominant market for PVB interlayers for laminated glass, driven by large-scale infrastructure projects, stringent safety regulations in public buildings, and the increasing use of architectural glass in modern commercial spaces. Within this segment, countries with robust construction industries and high safety standards, such as the United States, China, and Germany, exhibit the highest market share. The growth in this segment is significantly fueled by the demand for safety glazing in skylights, facades, and internal partitions, where PVB interlayers provide essential protection against impact and breakage. Policies mandating the use of laminated glass in commercial buildings to enhance security and prevent injuries are crucial growth drivers.

- Commercial Applications: Characterized by large-volume demand, driven by skyscrapers, airports, hospitals, and educational institutions.

- Key Growth Drivers:

- Urbanization and rapid infrastructure development.

- Stricter building codes and safety regulations for public spaces.

- Increasing adoption of energy-efficient and aesthetically pleasing architectural designs.

- Demand for enhanced security and sound insulation in commercial environments.

- Key Growth Drivers:

- Residential Applications: Growing steadily due to increased awareness of home safety, energy efficiency, and demand for premium building materials.

- Key Growth Drivers:

- Rising disposable incomes and home improvement trends.

- Focus on acoustic insulation for quieter living spaces.

- Desire for UV protection in windows and doors.

- Growing adoption of laminated glass in balconies, windows, and doors for enhanced security.

- Key Growth Drivers:

Regarding product types, the 0.03-0.04 Inch thickness segment is currently leading due to its optimal balance of performance, weight, and cost-effectiveness for a wide range of architectural and automotive applications. However, the Below 0.02 Inch segment is experiencing rapid growth, driven by the automotive industry's push for lightweighting and the development of thinner, high-strength PVB interlayers. The 0.02-0.03 Inch and Above 0.04 Inch segments cater to specific high-performance and safety-critical applications, respectively.

PVB Interlayers for Laminated Glass Product Analysis

Innovations in PVB interlayers for laminated glass are continuously expanding their application scope and enhancing performance. Manufacturers are focusing on developing interlayers with superior acoustic dampening capabilities, crucial for urban environments seeking noise reduction. Enhanced UV filtering properties are also a key innovation area, protecting interiors from fading and degradation. Furthermore, advancements in PVB formulations are enabling thinner yet stronger interlayers, contributing to lightweighting in automotive and aerospace applications, while simultaneously improving impact resistance for enhanced safety in architectural glazing. Competitive advantages are derived from differentiated product offerings, such as those with specialized properties like self-cleaning or fire retardancy, and a strong emphasis on consistent quality and supply chain reliability.

Key Drivers, Barriers & Challenges in PVB Interlayers for Laminated Glass

Key Drivers, Barriers & Challenges in PVB Interlayers for Laminated Glass

Key Drivers: The PVB interlayers for laminated glass market is propelled by a confluence of technological, economic, and policy-driven factors.

- Technological Advancement: Continuous innovation in PVB formulations leading to enhanced safety, acoustic, and solar control properties. For instance, the development of low-e PVB interlayers significantly improves energy efficiency in buildings.

- Economic Growth: Rising disposable incomes and increasing urbanization globally are driving construction activities, particularly in residential and commercial sectors. This translates to higher demand for laminated glass.

- Regulatory Mandates: Stringent safety regulations for building materials and automotive safety standards across various regions mandate the use of laminated glass, thereby directly boosting PVB interlayer demand. For example, building codes in many countries require laminated glass for overhead glazing and in schools and hospitals.

Key Barriers & Challenges: Despite robust growth, the market faces several significant challenges that can impact its trajectory.

- Supply Chain Disruptions: Geopolitical events and raw material price volatility can lead to supply chain bottlenecks and increased manufacturing costs. The price of Butyraldehyde, a key raw material, has seen fluctuations of up to 15% in the last two years.

- Regulatory Complexities: Navigating diverse and evolving safety and environmental regulations across different countries can be a complex and costly undertaking for manufacturers.

- Competitive Pressures: The presence of established players and the potential entry of new competitors can lead to price pressures and necessitate continuous investment in R&D to maintain market share.

- Raw Material Availability and Cost: Fluctuations in the availability and cost of key raw materials, such as PVB resin and plasticizers, can impact profit margins and production planning. The cost of PVB resin has seen an average increase of 8% year-on-year.

Growth Drivers in the PVB Interlayers for Laminated Glass Market

The PVB interlayers for laminated glass market is experiencing significant growth driven by several key factors. Technologically, the development of advanced PVB formulations offering superior acoustic insulation, UV blocking, and enhanced impact resistance is creating new market opportunities. Economically, global urbanization and infrastructure development, particularly in emerging economies, are leading to a surge in construction activities requiring safer and more durable building materials. Regulatory mandates, such as stricter building codes for safety glazing and evolving automotive safety standards, are non-negotiable growth catalysts, compelling the widespread adoption of laminated glass. For example, new regulations in Europe requiring enhanced acoustic performance in residential buildings are directly benefiting PVB interlayer manufacturers. The increasing consumer preference for sustainable and energy-efficient solutions is also a major driver, as PVB interlayers contribute to better thermal insulation and reduced reliance on artificial lighting.

Challenges Impacting PVB Interlayers for Laminated Glass Growth

The growth trajectory of the PVB interlayers for laminated glass market is not without its obstacles. Regulatory complexities, with varying standards and compliance requirements across different regions, pose a significant hurdle for global market penetration. Supply chain issues, including the volatility of raw material prices and potential disruptions due to geopolitical factors, can impact production costs and product availability. For instance, disruptions in the supply of key petrochemicals used in PVB production have led to price surges of up to 12% in recent periods. Competitive pressures from established players and the potential emergence of alternative interlayer materials, though currently niche, also necessitate continuous innovation and cost optimization. Furthermore, the increasing focus on sustainability and the circular economy presents a challenge in terms of developing more environmentally friendly production processes and end-of-life management solutions for PVB.

Key Players Shaping the PVB Interlayers for Laminated Glass Market

- Eastman

- Kuraray

- Sekisui Chemical

- DuPont

- EVERLAM

- 3M

- Chang Chun Group

- Kengo

- WMC Glass

Significant PVB Interlayers for Laminated Glass Industry Milestones

- 2019: Introduction of advanced acoustic PVB interlayers by leading manufacturers, enhancing noise reduction capabilities for residential and commercial buildings.

- 2020: Increased focus on developing PVB interlayers with enhanced UV blocking properties to protect interior furnishings and reduce cooling loads in buildings.

- 2021: Growing adoption of thinner PVB interlayers for automotive applications, supporting vehicle lightweighting initiatives and improved fuel efficiency.

- 2022: Expansion of manufacturing capacities by key players to meet the escalating global demand, particularly in Asia-Pacific.

- 2023: Launch of next-generation PVB interlayers with improved self-cleaning and anti-fogging properties for architectural applications.

- 2024: Significant investment in R&D for PVB interlayers capable of integration with smart glass technologies, offering dynamic tinting and privacy control.

Future Outlook for PVB Interlayers for Laminated Glass Market

The future outlook for the PVB interlayers for laminated glass market is exceptionally promising, fueled by a sustained demand for safety, security, and energy-efficient solutions across global construction and automotive sectors. Strategic opportunities lie in the continued innovation of PVB formulations to meet evolving regulatory requirements and consumer preferences, such as enhanced acoustic performance and integrated smart functionalities. The expansion of market penetration in developing economies, coupled with the growing trend of urban revitalization and retrofitting existing buildings, will further propel market growth. The automotive industry's unwavering commitment to lightweighting and occupant safety will continue to drive demand for advanced PVB interlayers. Projections indicate a sustained robust CAGR of approximately 7.2% over the forecast period, with the market size expected to reach $18 billion by 2033, signifying substantial growth potential and a strong market outlook.

PVB Interlayers for Laminated Glass Segmentation

-

1. Application

- 1.1. Commercial

- 1.2. Residential

-

2. Types

- 2.1. Below 0.02 Inch

- 2.2. 0.02-0.03 Inch

- 2.3. 0.03-0.04 Inch

- 2.4. Above 0.04 Inch

PVB Interlayers for Laminated Glass Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

PVB Interlayers for Laminated Glass Regional Market Share

Geographic Coverage of PVB Interlayers for Laminated Glass

PVB Interlayers for Laminated Glass REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.12% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global PVB Interlayers for Laminated Glass Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Commercial

- 5.1.2. Residential

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Below 0.02 Inch

- 5.2.2. 0.02-0.03 Inch

- 5.2.3. 0.03-0.04 Inch

- 5.2.4. Above 0.04 Inch

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America PVB Interlayers for Laminated Glass Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Commercial

- 6.1.2. Residential

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Below 0.02 Inch

- 6.2.2. 0.02-0.03 Inch

- 6.2.3. 0.03-0.04 Inch

- 6.2.4. Above 0.04 Inch

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America PVB Interlayers for Laminated Glass Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Commercial

- 7.1.2. Residential

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Below 0.02 Inch

- 7.2.2. 0.02-0.03 Inch

- 7.2.3. 0.03-0.04 Inch

- 7.2.4. Above 0.04 Inch

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe PVB Interlayers for Laminated Glass Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Commercial

- 8.1.2. Residential

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Below 0.02 Inch

- 8.2.2. 0.02-0.03 Inch

- 8.2.3. 0.03-0.04 Inch

- 8.2.4. Above 0.04 Inch

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa PVB Interlayers for Laminated Glass Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Commercial

- 9.1.2. Residential

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Below 0.02 Inch

- 9.2.2. 0.02-0.03 Inch

- 9.2.3. 0.03-0.04 Inch

- 9.2.4. Above 0.04 Inch

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific PVB Interlayers for Laminated Glass Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Commercial

- 10.1.2. Residential

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Below 0.02 Inch

- 10.2.2. 0.02-0.03 Inch

- 10.2.3. 0.03-0.04 Inch

- 10.2.4. Above 0.04 Inch

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Eastman

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Kuraray

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Sekisui Chemical

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 DuPont

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 EVERLAM

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 3M

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Chang Chun Group

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Kengo

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 WMC Glass

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.1 Eastman

List of Figures

- Figure 1: Global PVB Interlayers for Laminated Glass Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America PVB Interlayers for Laminated Glass Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America PVB Interlayers for Laminated Glass Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America PVB Interlayers for Laminated Glass Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America PVB Interlayers for Laminated Glass Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America PVB Interlayers for Laminated Glass Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America PVB Interlayers for Laminated Glass Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America PVB Interlayers for Laminated Glass Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America PVB Interlayers for Laminated Glass Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America PVB Interlayers for Laminated Glass Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America PVB Interlayers for Laminated Glass Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America PVB Interlayers for Laminated Glass Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America PVB Interlayers for Laminated Glass Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe PVB Interlayers for Laminated Glass Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe PVB Interlayers for Laminated Glass Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe PVB Interlayers for Laminated Glass Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe PVB Interlayers for Laminated Glass Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe PVB Interlayers for Laminated Glass Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe PVB Interlayers for Laminated Glass Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa PVB Interlayers for Laminated Glass Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa PVB Interlayers for Laminated Glass Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa PVB Interlayers for Laminated Glass Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa PVB Interlayers for Laminated Glass Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa PVB Interlayers for Laminated Glass Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa PVB Interlayers for Laminated Glass Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific PVB Interlayers for Laminated Glass Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific PVB Interlayers for Laminated Glass Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific PVB Interlayers for Laminated Glass Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific PVB Interlayers for Laminated Glass Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific PVB Interlayers for Laminated Glass Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific PVB Interlayers for Laminated Glass Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global PVB Interlayers for Laminated Glass Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global PVB Interlayers for Laminated Glass Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global PVB Interlayers for Laminated Glass Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global PVB Interlayers for Laminated Glass Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global PVB Interlayers for Laminated Glass Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global PVB Interlayers for Laminated Glass Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States PVB Interlayers for Laminated Glass Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada PVB Interlayers for Laminated Glass Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico PVB Interlayers for Laminated Glass Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global PVB Interlayers for Laminated Glass Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global PVB Interlayers for Laminated Glass Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global PVB Interlayers for Laminated Glass Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil PVB Interlayers for Laminated Glass Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina PVB Interlayers for Laminated Glass Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America PVB Interlayers for Laminated Glass Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global PVB Interlayers for Laminated Glass Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global PVB Interlayers for Laminated Glass Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global PVB Interlayers for Laminated Glass Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom PVB Interlayers for Laminated Glass Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany PVB Interlayers for Laminated Glass Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France PVB Interlayers for Laminated Glass Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy PVB Interlayers for Laminated Glass Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain PVB Interlayers for Laminated Glass Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia PVB Interlayers for Laminated Glass Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux PVB Interlayers for Laminated Glass Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics PVB Interlayers for Laminated Glass Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe PVB Interlayers for Laminated Glass Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global PVB Interlayers for Laminated Glass Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global PVB Interlayers for Laminated Glass Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global PVB Interlayers for Laminated Glass Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey PVB Interlayers for Laminated Glass Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel PVB Interlayers for Laminated Glass Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC PVB Interlayers for Laminated Glass Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa PVB Interlayers for Laminated Glass Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa PVB Interlayers for Laminated Glass Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa PVB Interlayers for Laminated Glass Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global PVB Interlayers for Laminated Glass Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global PVB Interlayers for Laminated Glass Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global PVB Interlayers for Laminated Glass Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China PVB Interlayers for Laminated Glass Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India PVB Interlayers for Laminated Glass Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan PVB Interlayers for Laminated Glass Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea PVB Interlayers for Laminated Glass Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN PVB Interlayers for Laminated Glass Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania PVB Interlayers for Laminated Glass Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific PVB Interlayers for Laminated Glass Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the PVB Interlayers for Laminated Glass?

The projected CAGR is approximately 7.12%.

2. Which companies are prominent players in the PVB Interlayers for Laminated Glass?

Key companies in the market include Eastman, Kuraray, Sekisui Chemical, DuPont, EVERLAM, 3M, Chang Chun Group, Kengo, WMC Glass.

3. What are the main segments of the PVB Interlayers for Laminated Glass?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "PVB Interlayers for Laminated Glass," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the PVB Interlayers for Laminated Glass report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the PVB Interlayers for Laminated Glass?

To stay informed about further developments, trends, and reports in the PVB Interlayers for Laminated Glass, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence