Key Insights

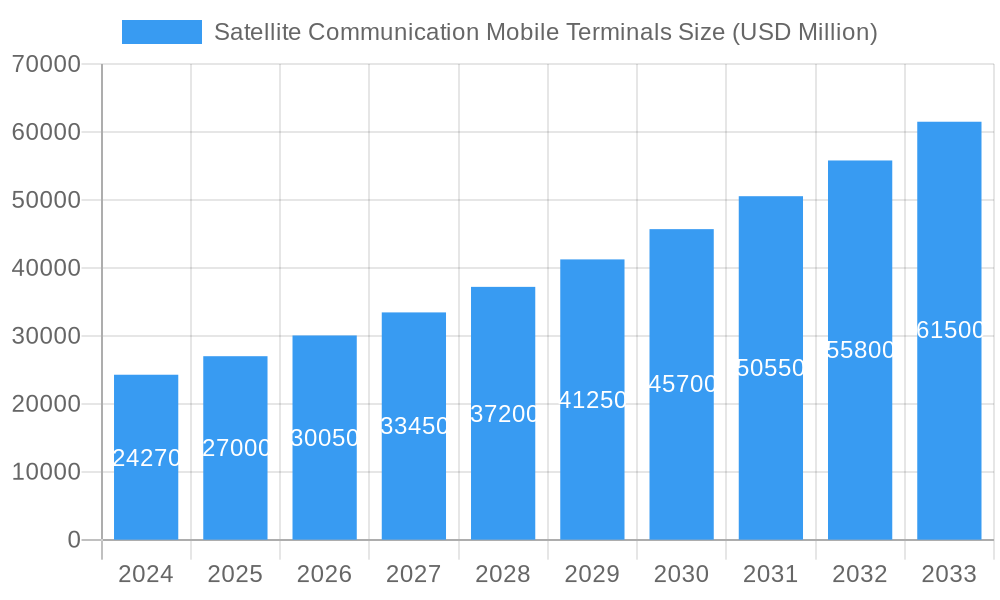

The global Satellite Communication Mobile Terminals market is poised for substantial expansion, projected to reach approximately USD 24.27 billion by 2024. This robust growth is driven by an anticipated Compound Annual Growth Rate (CAGR) of 11.3% from 2025 to 2033, indicating a dynamic and evolving industry. Key factors propelling this surge include the increasing demand for reliable connectivity in remote and underserved areas, the growing adoption of satellite communication solutions by military and defense sectors for enhanced operational capabilities, and the burgeoning need for seamless communication in commercial applications like broadcasting, maritime operations, and aviation. Furthermore, advancements in satellite technology, such as the proliferation of Low Earth Orbit (LEO) satellites and the development of more compact and versatile mobile terminals, are significantly contributing to market momentum. The ongoing digital transformation across various industries necessitates ubiquitous and resilient connectivity, which satellite communication mobile terminals are uniquely positioned to provide.

Satellite Communication Mobile Terminals Market Size (In Billion)

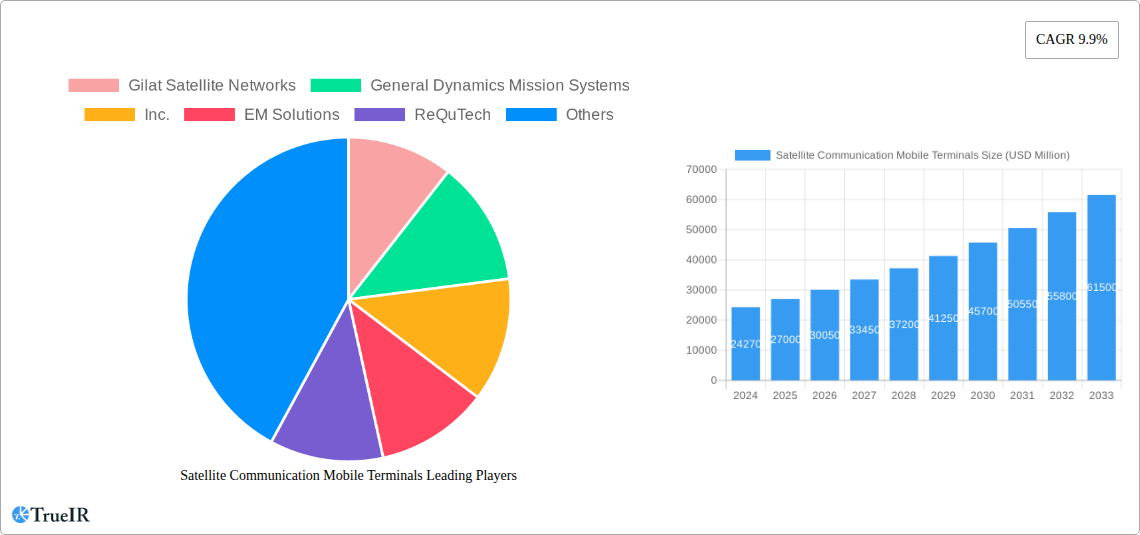

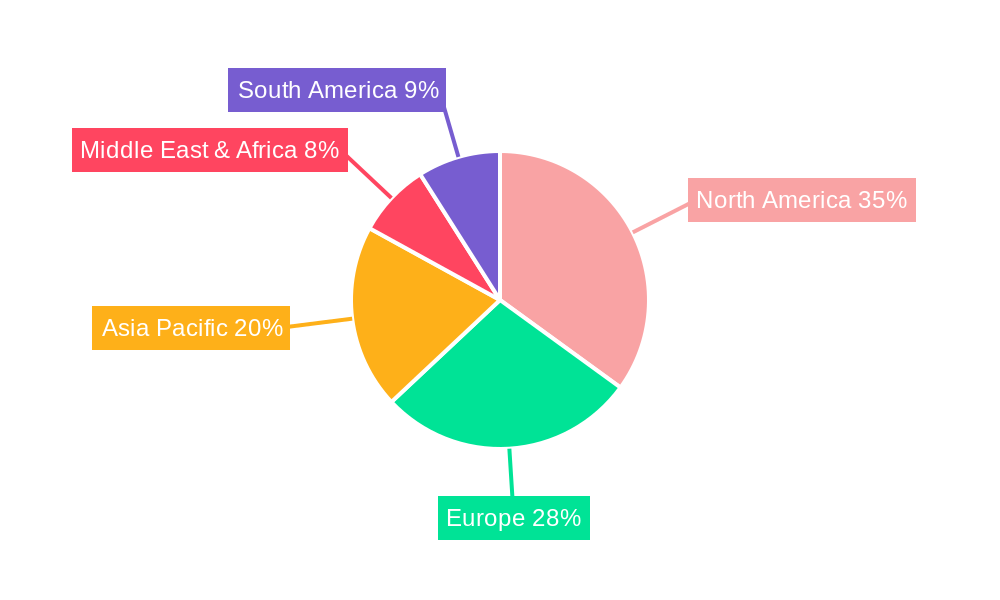

The market segmentation by application highlights the diverse utility of these terminals, with Aerospace, Military, and Commercial sectors emerging as primary growth drivers. The increasing sophistication of security and protection requirements in both governmental and private sectors also fuels demand. In terms of terminal types, Land-based, Maritime, and Aeronautical Satellite Communication Mobile Terminals are all expected to witness steady growth, catering to the specific connectivity needs of each domain. North America and Europe are anticipated to remain dominant regions due to their established technological infrastructure and significant investments in defense and aerospace. However, the Asia Pacific region, particularly China and India, is expected to exhibit the highest growth rates, driven by rapid infrastructure development, increasing internet penetration, and government initiatives promoting digital connectivity. The competitive landscape is characterized by innovation and strategic collaborations among key players like Gilat Satellite Networks, General Dynamics Mission Systems, Inc., and Viasat, Inc., all striving to offer advanced and cost-effective solutions to meet the escalating global demand.

Satellite Communication Mobile Terminals Company Market Share

Here is a dynamic, SEO-optimized report description for Satellite Communication Mobile Terminals, designed for immediate use without modification.

Report Title: Satellite Communication Mobile Terminals Market: Comprehensive Analysis and Future Projections (2019-2033)

Report Description: Unlock critical insights into the global Satellite Communication Mobile Terminals market, projected to reach trillions by 2033. This in-depth report provides a 360-degree view, from market structure and competitive landscape to emerging trends, dominant segments, and future outlook. Covering applications in Aerospace, Military, Commercial, Communication, Security & Protection, News, and Others, alongside types including Land-based, Maritime, and Aeronautical terminals, this research is essential for stakeholders seeking to capitalize on the trillion-dollar opportunities within this rapidly evolving sector. Analyze key players such as Gilat Satellite Networks, General Dynamics Mission Systems, Inc., EM Solutions, ReQuTech, TTI Norte SL, ST Engineering, Viasat, Inc., L3HARRIS, IAI, and Kymeta Corporation, and understand the technological innovations, regulatory impacts, and market drivers shaping the future of mobile satellite communication.

Satellite Communication Mobile Terminals Market Structure & Competitive Landscape

The global Satellite Communication Mobile Terminals market exhibits a moderately concentrated structure, with key players investing heavily in research and development to drive innovation. The innovation drivers are primarily fueled by the increasing demand for high-throughput connectivity in remote and underserved regions, alongside the growing adoption of 5G technologies and the expansion of Low Earth Orbit (LEO) satellite constellations. Regulatory impacts, while varied across regions, are generally leaning towards facilitating satellite broadband deployment, though spectrum allocation and licensing complexities remain a consideration. Product substitutes, such as terrestrial broadband and evolving cellular networks, pose a competitive challenge, but the unique capabilities of mobile satellite terminals in providing ubiquitous connectivity, especially in disaster relief and defense scenarios, maintain their distinct market position. End-user segmentation reveals strong growth in military and commercial applications, driven by national security needs and the increasing reliance on remote operations and mobile workforce connectivity. Mergers and acquisitions (M&A) activity within the industry has been dynamic, with strategic consolidation aimed at expanding product portfolios, geographic reach, and technological capabilities. For instance, over the historical period (2019-2024), an estimated $2 billion in M&A transactions have occurred, reflecting the industry's drive for scale and synergistic growth. The concentration ratio among the top 5 players is estimated to be around 55% in the base year of 2025, indicating significant influence but also room for new entrants and specialized players.

Satellite Communication Mobile Terminals Market Trends & Opportunities

The Satellite Communication Mobile Terminals market is poised for substantial growth, driven by an unprecedented surge in demand for ubiquitous and resilient connectivity solutions across diverse sectors. The market size is projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 12.5% from 2019 to 2033, with the base year of 2025 estimated to see a market value in the trillions. This impressive trajectory is underpinned by several transformative trends. Firstly, the proliferation of Low Earth Orbit (LEO) satellite constellations, such as those by SpaceX's Starlink and OneWeb, is democratizing access to high-speed satellite internet, enabling smaller, more affordable, and high-performance mobile terminals. This technological shift is fundamentally altering consumer preferences, moving towards seamless integration and user-friendly interfaces, even in ruggedized or mobile environments.

The increasing deployment of these LEO constellations directly impacts market penetration rates, which are expected to rise significantly from approximately 15% in 2019 to over 60% by 2033 across key markets. The competitive dynamics are evolving rapidly, with established players like Viasat, Inc. and L3HARRIS focusing on advanced solutions for defense and enterprise, while newer entrants are leveraging LEO to offer more competitive consumer and commercial services.

Opportunities abound in the defense sector, where the need for secure, reliable, and mobile communication for battlefield operations, intelligence gathering, and disaster response is paramount. The commercial sector is witnessing a surge in demand for connectivity in remote mining operations, offshore oil and gas exploration, and global logistics, all of which are facilitated by mobile satellite terminals. Furthermore, the growing importance of emergency services and disaster management communications, especially in regions prone to natural calamities, presents a significant growth avenue. The "Internet of Things" (IoT) enablement through satellite connectivity for remote asset monitoring and control is another burgeoning opportunity. The increasing adoption of flat-panel and electronically steered antennas (ESAs) is also a key trend, offering more compact, robust, and efficient terminal solutions compared to traditional parabolic dishes, further broadening the applicability and appeal of mobile satellite communication. The convergence of satellite and terrestrial networks is also creating new service models and driving innovation in hybrid connectivity solutions.

Dominant Markets & Segments in Satellite Communication Mobile Terminals

The Satellite Communication Mobile Terminals market is characterized by the dominance of specific regions and segments, driven by a confluence of technological advancements, strategic investments, and policy frameworks.

Regionally: North America, particularly the United States, stands as the leading market. This dominance is attributed to:

- Robust Defense Spending: Significant government investment in advanced communication systems for military operations and national security.

- Technological Innovation Hub: Presence of leading satellite technology developers and manufacturers, fostering rapid product development and adoption.

- Extensive Infrastructure Rollout: Early and aggressive deployment of LEO satellite constellations, expanding broadband access across vast geographical areas.

- Favorable Regulatory Environment: Supportive policies encouraging satellite broadband deployment and spectrum utilization.

Europe also represents a significant and growing market, propelled by:

- Growing Commercial Adoption: Increasing use in maritime, aeronautical, and remote enterprise applications.

- European Space Agency (ESA) Initiatives: Funding and support for satellite communication research and development.

- Digitalization Efforts: Government initiatives aimed at bridging digital divides and enhancing connectivity.

Application Segments: The Military segment is a primary growth driver, with an estimated market share exceeding 35% by 2025. Key growth drivers include:

- Enhanced Battlefield Communications: Need for real-time, secure, and resilient data transmission for tactical operations.

- Intelligence, Surveillance, and Reconnaissance (ISR): Demand for uninterrupted data feeds from remote sensing and monitoring platforms.

- Global Deployment Capabilities: Requirement for connectivity across diverse and challenging operational environments worldwide.

- Modernization Programs: Ongoing defense modernization initiatives emphasizing networked warfare and advanced communication technologies.

The Commercial segment is rapidly expanding, driven by the burgeoning need for connectivity in remote industries and enterprise mobility. Growth factors include:

- Remote Operations: Essential for industries like mining, oil and gas, and agriculture operating far from terrestrial infrastructure.

- Mobile Workforce: Providing reliable internet access for remote workers, field service personnel, and transportation fleets.

- Maritime Connectivity: Supporting navigation, crew welfare, and operational efficiency for vessels.

- Aeronautical Connectivity: Enhancing passenger experience and operational efficiency for airlines.

Type Segments: Land-based Satellite Communication Mobile Terminals currently hold the largest market share, accounting for approximately 45% by 2025. This is due to their versatility and widespread use in defense, emergency services, and remote commercial operations.

Maritime Satellite Communication Mobile Terminals are experiencing robust growth, driven by the increasing digitalization of the shipping industry and the need for enhanced crew welfare and operational efficiency.

Aeronautical Satellite Communication Mobile Terminals are also witnessing significant expansion, fueled by the demand for in-flight connectivity for passengers and operational data transmission for airlines.

Satellite Communication Mobile Terminals Product Analysis

Product innovation in Satellite Communication Mobile Terminals is characterized by a relentless pursuit of miniaturization, increased bandwidth, lower power consumption, and enhanced user experience. Companies are developing advanced electronically steered antennas (ESAs) and flat-panel antennas that offer superior portability, rapid deployment, and resistance to harsh environmental conditions. The integration of advanced signal processing and modulation techniques ensures higher data throughput and greater spectral efficiency, crucial for meeting the growing demand for video streaming, real-time data transfer, and cloud-based services in mobile scenarios. Competitive advantages are being forged through the development of terminals that offer seamless switching between satellite constellations, including LEO and GEO, as well as hybrid connectivity solutions that integrate satellite with cellular and Wi-Fi networks. This focus on versatile and resilient connectivity ensures that mobile terminals can maintain uninterrupted communication in a wide range of applications, from critical military operations to remote commercial enterprises.

Key Drivers, Barriers & Challenges in Satellite Communication Mobile Terminals

Key Drivers: The Satellite Communication Mobile Terminals market is propelled by several interconnected factors. Technologically, the launch of new LEO satellite constellations is a monumental driver, offering higher speeds and lower latency at competitive price points. Economic drivers include the ever-increasing demand for connectivity in underserved regions and the growth of remote workforces across industries. Policy-driven factors, such as government initiatives to expand broadband access and support for national security communications, also play a crucial role. For instance, the US government's investment of billions in secure satellite communications for its armed forces is a significant catalyst.

Barriers & Challenges: Despite the strong growth, the market faces several barriers and challenges. Regulatory complexities, including spectrum licensing and international agreements, can hinder rapid deployment and increase operational costs. Supply chain issues, particularly concerning the availability of specialized components for antenna manufacturing and chipsets, can lead to production delays and price volatility, impacting an estimated 10-15% of production timelines. Competitive pressures from rapidly evolving terrestrial technologies, such as 5G expansion, require continuous innovation and cost optimization from satellite terminal manufacturers. Furthermore, the high upfront cost of some advanced terminals can be a restraint for smaller businesses or certain government agencies with limited budgets.

Growth Drivers in the Satellite Communication Mobile Terminals Market

The Satellite Communication Mobile Terminals market is experiencing robust growth fueled by a confluence of powerful factors. Technological advancements, particularly the maturation and expansion of LEO satellite constellations, are dramatically increasing bandwidth and reducing latency, making satellite a viable alternative for high-speed internet. Economically, the global surge in remote work, the expansion of industries in remote locations (e.g., mining, agriculture), and the need for business continuity in the face of natural disasters are creating unprecedented demand for reliable, mobile connectivity solutions. Government initiatives and investments in defense, national security, and rural broadband expansion are also significant catalysts. For example, multi-billion dollar defense modernization programs are driving the adoption of advanced mobile satellite terminals.

Challenges Impacting Satellite Communication Mobile Terminals Growth

Several challenges continue to shape the trajectory of the Satellite Communication Mobile Terminals market. Regulatory complexities remain a significant hurdle, with varying spectrum allocation policies, licensing requirements, and international coordination needs creating potential delays and increased operational expenses across different regions. Supply chain issues, from the sourcing of specialized components to manufacturing capacity, can impact lead times and cost for terminal production, potentially affecting an estimated 10-15% of planned deployments. Intense competitive pressures from the ongoing expansion of terrestrial broadband networks, especially 5G and fiber optics, necessitate continuous innovation and price competitiveness for satellite solutions to maintain market share. Furthermore, the initial capital investment for some advanced mobile satellite terminals can be a barrier for certain segments of the market, demanding effective financing and leasing models.

Key Players Shaping the Satellite Communication Mobile Terminals Market

- Gilat Satellite Networks

- General Dynamics Mission Systems, Inc.

- EM Solutions

- ReQuTech

- TTI Norte SL

- ST Engineering

- Viasat, Inc.

- L3HARRIS

- IAI

- Kymeta Corporation

Significant Satellite Communication Mobile Terminals Industry Milestones

- 2019: Continued expansion and early commercial deployments of LEO constellations by companies like Starlink, signaling a new era of high-throughput mobile satellite services.

- 2020: Increased demand for remote work and connectivity solutions during the COVID-19 pandemic, highlighting the criticality of satellite communication for business continuity and essential services.

- 2021: Major defense contracts awarded for advanced mobile satellite terminals, emphasizing their role in modern military operations and global reach.

- 2022: Introduction of more compact and affordable flat-panel and electronically steered antenna (ESA) terminals, broadening accessibility for commercial and consumer markets.

- 2023: Significant advancements in multi-orbit and multi-constellation terminal technology, enabling seamless transitions between LEO, MEO, and GEO satellites for enhanced reliability.

- 2024: Growing integration of satellite communication with 5G networks, paving the way for hybrid connectivity solutions and expanded IoT applications in remote areas.

Future Outlook for Satellite Communication Mobile Terminals Market

The future outlook for the Satellite Communication Mobile Terminals market is exceptionally bright, characterized by sustained high growth and transformative innovation. The continued expansion of LEO satellite constellations will democratize access to high-speed, low-latency satellite internet, further driving adoption across all segments. Strategic opportunities lie in the burgeoning demand for connected vehicles, the expansion of IoT services in remote environments, and the increasing need for resilient communication in disaster-prone regions. The development of software-defined terminals and integrated multi-orbit solutions will enhance user experience and operational efficiency. With an anticipated market valuation in the trillions by 2033, the sector is poised for continued investment, technological breakthroughs, and a significant impact on global connectivity.

Satellite Communication Mobile Terminals Segmentation

-

1. Application

- 1.1. Aerospace

- 1.2. Military

- 1.3. Commercial

- 1.4. Communication

- 1.5. Security & Protection

- 1.6. News

- 1.7. Others

-

2. Types

- 2.1. Land-based Satellite Communication Mobile Terminals

- 2.2. Maritime Satellite Communication Mobile Terminals

- 2.3. Aeronautical Satellite Communication Mobile Terminals

Satellite Communication Mobile Terminals Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Satellite Communication Mobile Terminals Regional Market Share

Geographic Coverage of Satellite Communication Mobile Terminals

Satellite Communication Mobile Terminals REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Satellite Communication Mobile Terminals Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Aerospace

- 5.1.2. Military

- 5.1.3. Commercial

- 5.1.4. Communication

- 5.1.5. Security & Protection

- 5.1.6. News

- 5.1.7. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Land-based Satellite Communication Mobile Terminals

- 5.2.2. Maritime Satellite Communication Mobile Terminals

- 5.2.3. Aeronautical Satellite Communication Mobile Terminals

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Satellite Communication Mobile Terminals Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Aerospace

- 6.1.2. Military

- 6.1.3. Commercial

- 6.1.4. Communication

- 6.1.5. Security & Protection

- 6.1.6. News

- 6.1.7. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Land-based Satellite Communication Mobile Terminals

- 6.2.2. Maritime Satellite Communication Mobile Terminals

- 6.2.3. Aeronautical Satellite Communication Mobile Terminals

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Satellite Communication Mobile Terminals Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Aerospace

- 7.1.2. Military

- 7.1.3. Commercial

- 7.1.4. Communication

- 7.1.5. Security & Protection

- 7.1.6. News

- 7.1.7. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Land-based Satellite Communication Mobile Terminals

- 7.2.2. Maritime Satellite Communication Mobile Terminals

- 7.2.3. Aeronautical Satellite Communication Mobile Terminals

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Satellite Communication Mobile Terminals Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Aerospace

- 8.1.2. Military

- 8.1.3. Commercial

- 8.1.4. Communication

- 8.1.5. Security & Protection

- 8.1.6. News

- 8.1.7. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Land-based Satellite Communication Mobile Terminals

- 8.2.2. Maritime Satellite Communication Mobile Terminals

- 8.2.3. Aeronautical Satellite Communication Mobile Terminals

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Satellite Communication Mobile Terminals Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Aerospace

- 9.1.2. Military

- 9.1.3. Commercial

- 9.1.4. Communication

- 9.1.5. Security & Protection

- 9.1.6. News

- 9.1.7. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Land-based Satellite Communication Mobile Terminals

- 9.2.2. Maritime Satellite Communication Mobile Terminals

- 9.2.3. Aeronautical Satellite Communication Mobile Terminals

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Satellite Communication Mobile Terminals Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Aerospace

- 10.1.2. Military

- 10.1.3. Commercial

- 10.1.4. Communication

- 10.1.5. Security & Protection

- 10.1.6. News

- 10.1.7. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Land-based Satellite Communication Mobile Terminals

- 10.2.2. Maritime Satellite Communication Mobile Terminals

- 10.2.3. Aeronautical Satellite Communication Mobile Terminals

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Gilat Satellite Networks

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 General Dynamics Mission Systems

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Inc.

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 EM Solutions

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 ReQuTech

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 TTI Norte SL

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 ST Engineering

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Viasat

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Inc.

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 L3HARRIS

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 IAI

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Kymeta Corporation

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.1 Gilat Satellite Networks

List of Figures

- Figure 1: Global Satellite Communication Mobile Terminals Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: Global Satellite Communication Mobile Terminals Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Satellite Communication Mobile Terminals Revenue (undefined), by Application 2025 & 2033

- Figure 4: North America Satellite Communication Mobile Terminals Volume (K), by Application 2025 & 2033

- Figure 5: North America Satellite Communication Mobile Terminals Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Satellite Communication Mobile Terminals Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Satellite Communication Mobile Terminals Revenue (undefined), by Types 2025 & 2033

- Figure 8: North America Satellite Communication Mobile Terminals Volume (K), by Types 2025 & 2033

- Figure 9: North America Satellite Communication Mobile Terminals Revenue Share (%), by Types 2025 & 2033

- Figure 10: North America Satellite Communication Mobile Terminals Volume Share (%), by Types 2025 & 2033

- Figure 11: North America Satellite Communication Mobile Terminals Revenue (undefined), by Country 2025 & 2033

- Figure 12: North America Satellite Communication Mobile Terminals Volume (K), by Country 2025 & 2033

- Figure 13: North America Satellite Communication Mobile Terminals Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Satellite Communication Mobile Terminals Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Satellite Communication Mobile Terminals Revenue (undefined), by Application 2025 & 2033

- Figure 16: South America Satellite Communication Mobile Terminals Volume (K), by Application 2025 & 2033

- Figure 17: South America Satellite Communication Mobile Terminals Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Satellite Communication Mobile Terminals Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Satellite Communication Mobile Terminals Revenue (undefined), by Types 2025 & 2033

- Figure 20: South America Satellite Communication Mobile Terminals Volume (K), by Types 2025 & 2033

- Figure 21: South America Satellite Communication Mobile Terminals Revenue Share (%), by Types 2025 & 2033

- Figure 22: South America Satellite Communication Mobile Terminals Volume Share (%), by Types 2025 & 2033

- Figure 23: South America Satellite Communication Mobile Terminals Revenue (undefined), by Country 2025 & 2033

- Figure 24: South America Satellite Communication Mobile Terminals Volume (K), by Country 2025 & 2033

- Figure 25: South America Satellite Communication Mobile Terminals Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Satellite Communication Mobile Terminals Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Satellite Communication Mobile Terminals Revenue (undefined), by Application 2025 & 2033

- Figure 28: Europe Satellite Communication Mobile Terminals Volume (K), by Application 2025 & 2033

- Figure 29: Europe Satellite Communication Mobile Terminals Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Satellite Communication Mobile Terminals Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Satellite Communication Mobile Terminals Revenue (undefined), by Types 2025 & 2033

- Figure 32: Europe Satellite Communication Mobile Terminals Volume (K), by Types 2025 & 2033

- Figure 33: Europe Satellite Communication Mobile Terminals Revenue Share (%), by Types 2025 & 2033

- Figure 34: Europe Satellite Communication Mobile Terminals Volume Share (%), by Types 2025 & 2033

- Figure 35: Europe Satellite Communication Mobile Terminals Revenue (undefined), by Country 2025 & 2033

- Figure 36: Europe Satellite Communication Mobile Terminals Volume (K), by Country 2025 & 2033

- Figure 37: Europe Satellite Communication Mobile Terminals Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Satellite Communication Mobile Terminals Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Satellite Communication Mobile Terminals Revenue (undefined), by Application 2025 & 2033

- Figure 40: Middle East & Africa Satellite Communication Mobile Terminals Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Satellite Communication Mobile Terminals Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Satellite Communication Mobile Terminals Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Satellite Communication Mobile Terminals Revenue (undefined), by Types 2025 & 2033

- Figure 44: Middle East & Africa Satellite Communication Mobile Terminals Volume (K), by Types 2025 & 2033

- Figure 45: Middle East & Africa Satellite Communication Mobile Terminals Revenue Share (%), by Types 2025 & 2033

- Figure 46: Middle East & Africa Satellite Communication Mobile Terminals Volume Share (%), by Types 2025 & 2033

- Figure 47: Middle East & Africa Satellite Communication Mobile Terminals Revenue (undefined), by Country 2025 & 2033

- Figure 48: Middle East & Africa Satellite Communication Mobile Terminals Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Satellite Communication Mobile Terminals Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Satellite Communication Mobile Terminals Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Satellite Communication Mobile Terminals Revenue (undefined), by Application 2025 & 2033

- Figure 52: Asia Pacific Satellite Communication Mobile Terminals Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Satellite Communication Mobile Terminals Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Satellite Communication Mobile Terminals Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Satellite Communication Mobile Terminals Revenue (undefined), by Types 2025 & 2033

- Figure 56: Asia Pacific Satellite Communication Mobile Terminals Volume (K), by Types 2025 & 2033

- Figure 57: Asia Pacific Satellite Communication Mobile Terminals Revenue Share (%), by Types 2025 & 2033

- Figure 58: Asia Pacific Satellite Communication Mobile Terminals Volume Share (%), by Types 2025 & 2033

- Figure 59: Asia Pacific Satellite Communication Mobile Terminals Revenue (undefined), by Country 2025 & 2033

- Figure 60: Asia Pacific Satellite Communication Mobile Terminals Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Satellite Communication Mobile Terminals Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Satellite Communication Mobile Terminals Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Satellite Communication Mobile Terminals Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Satellite Communication Mobile Terminals Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Satellite Communication Mobile Terminals Revenue undefined Forecast, by Types 2020 & 2033

- Table 4: Global Satellite Communication Mobile Terminals Volume K Forecast, by Types 2020 & 2033

- Table 5: Global Satellite Communication Mobile Terminals Revenue undefined Forecast, by Region 2020 & 2033

- Table 6: Global Satellite Communication Mobile Terminals Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Satellite Communication Mobile Terminals Revenue undefined Forecast, by Application 2020 & 2033

- Table 8: Global Satellite Communication Mobile Terminals Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Satellite Communication Mobile Terminals Revenue undefined Forecast, by Types 2020 & 2033

- Table 10: Global Satellite Communication Mobile Terminals Volume K Forecast, by Types 2020 & 2033

- Table 11: Global Satellite Communication Mobile Terminals Revenue undefined Forecast, by Country 2020 & 2033

- Table 12: Global Satellite Communication Mobile Terminals Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Satellite Communication Mobile Terminals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: United States Satellite Communication Mobile Terminals Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Satellite Communication Mobile Terminals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Canada Satellite Communication Mobile Terminals Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Satellite Communication Mobile Terminals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 18: Mexico Satellite Communication Mobile Terminals Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Satellite Communication Mobile Terminals Revenue undefined Forecast, by Application 2020 & 2033

- Table 20: Global Satellite Communication Mobile Terminals Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Satellite Communication Mobile Terminals Revenue undefined Forecast, by Types 2020 & 2033

- Table 22: Global Satellite Communication Mobile Terminals Volume K Forecast, by Types 2020 & 2033

- Table 23: Global Satellite Communication Mobile Terminals Revenue undefined Forecast, by Country 2020 & 2033

- Table 24: Global Satellite Communication Mobile Terminals Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Satellite Communication Mobile Terminals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Brazil Satellite Communication Mobile Terminals Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Satellite Communication Mobile Terminals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Argentina Satellite Communication Mobile Terminals Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Satellite Communication Mobile Terminals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Satellite Communication Mobile Terminals Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Satellite Communication Mobile Terminals Revenue undefined Forecast, by Application 2020 & 2033

- Table 32: Global Satellite Communication Mobile Terminals Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Satellite Communication Mobile Terminals Revenue undefined Forecast, by Types 2020 & 2033

- Table 34: Global Satellite Communication Mobile Terminals Volume K Forecast, by Types 2020 & 2033

- Table 35: Global Satellite Communication Mobile Terminals Revenue undefined Forecast, by Country 2020 & 2033

- Table 36: Global Satellite Communication Mobile Terminals Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Satellite Communication Mobile Terminals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Satellite Communication Mobile Terminals Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Satellite Communication Mobile Terminals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 40: Germany Satellite Communication Mobile Terminals Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Satellite Communication Mobile Terminals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: France Satellite Communication Mobile Terminals Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Satellite Communication Mobile Terminals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: Italy Satellite Communication Mobile Terminals Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Satellite Communication Mobile Terminals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Spain Satellite Communication Mobile Terminals Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Satellite Communication Mobile Terminals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 48: Russia Satellite Communication Mobile Terminals Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Satellite Communication Mobile Terminals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 50: Benelux Satellite Communication Mobile Terminals Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Satellite Communication Mobile Terminals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 52: Nordics Satellite Communication Mobile Terminals Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Satellite Communication Mobile Terminals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Satellite Communication Mobile Terminals Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Satellite Communication Mobile Terminals Revenue undefined Forecast, by Application 2020 & 2033

- Table 56: Global Satellite Communication Mobile Terminals Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Satellite Communication Mobile Terminals Revenue undefined Forecast, by Types 2020 & 2033

- Table 58: Global Satellite Communication Mobile Terminals Volume K Forecast, by Types 2020 & 2033

- Table 59: Global Satellite Communication Mobile Terminals Revenue undefined Forecast, by Country 2020 & 2033

- Table 60: Global Satellite Communication Mobile Terminals Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Satellite Communication Mobile Terminals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 62: Turkey Satellite Communication Mobile Terminals Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Satellite Communication Mobile Terminals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 64: Israel Satellite Communication Mobile Terminals Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Satellite Communication Mobile Terminals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 66: GCC Satellite Communication Mobile Terminals Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Satellite Communication Mobile Terminals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 68: North Africa Satellite Communication Mobile Terminals Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Satellite Communication Mobile Terminals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 70: South Africa Satellite Communication Mobile Terminals Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Satellite Communication Mobile Terminals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Satellite Communication Mobile Terminals Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Satellite Communication Mobile Terminals Revenue undefined Forecast, by Application 2020 & 2033

- Table 74: Global Satellite Communication Mobile Terminals Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Satellite Communication Mobile Terminals Revenue undefined Forecast, by Types 2020 & 2033

- Table 76: Global Satellite Communication Mobile Terminals Volume K Forecast, by Types 2020 & 2033

- Table 77: Global Satellite Communication Mobile Terminals Revenue undefined Forecast, by Country 2020 & 2033

- Table 78: Global Satellite Communication Mobile Terminals Volume K Forecast, by Country 2020 & 2033

- Table 79: China Satellite Communication Mobile Terminals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 80: China Satellite Communication Mobile Terminals Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Satellite Communication Mobile Terminals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 82: India Satellite Communication Mobile Terminals Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Satellite Communication Mobile Terminals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 84: Japan Satellite Communication Mobile Terminals Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Satellite Communication Mobile Terminals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 86: South Korea Satellite Communication Mobile Terminals Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Satellite Communication Mobile Terminals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Satellite Communication Mobile Terminals Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Satellite Communication Mobile Terminals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 90: Oceania Satellite Communication Mobile Terminals Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Satellite Communication Mobile Terminals Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Satellite Communication Mobile Terminals Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Satellite Communication Mobile Terminals?

The projected CAGR is approximately 11%.

2. Which companies are prominent players in the Satellite Communication Mobile Terminals?

Key companies in the market include Gilat Satellite Networks, General Dynamics Mission Systems, Inc., EM Solutions, ReQuTech, TTI Norte SL, ST Engineering, Viasat, Inc., L3HARRIS, IAI, Kymeta Corporation.

3. What are the main segments of the Satellite Communication Mobile Terminals?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3350.00, USD 5025.00, and USD 6700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Satellite Communication Mobile Terminals," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Satellite Communication Mobile Terminals report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Satellite Communication Mobile Terminals?

To stay informed about further developments, trends, and reports in the Satellite Communication Mobile Terminals, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence