Key Insights

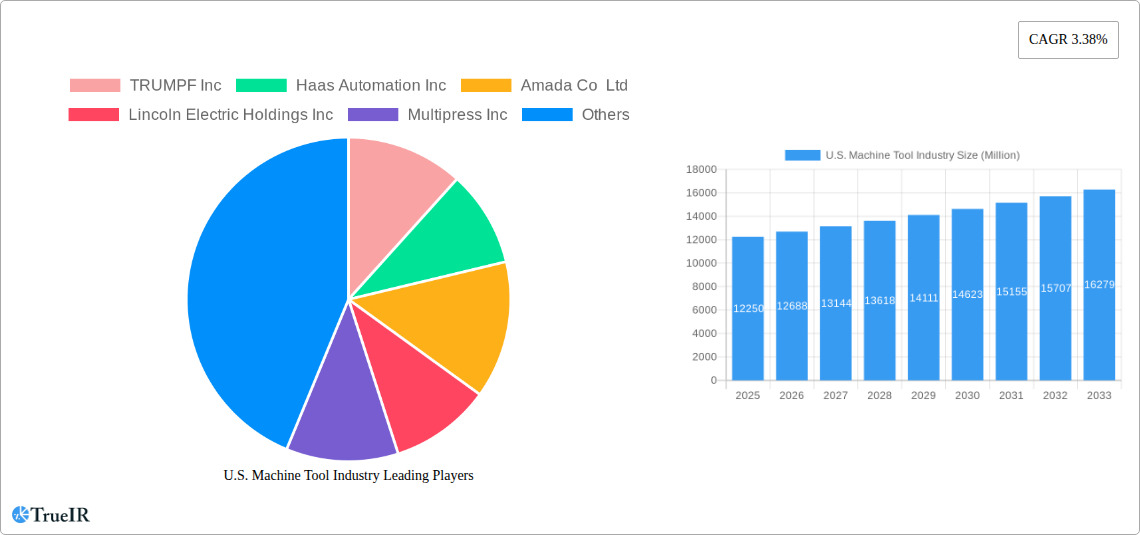

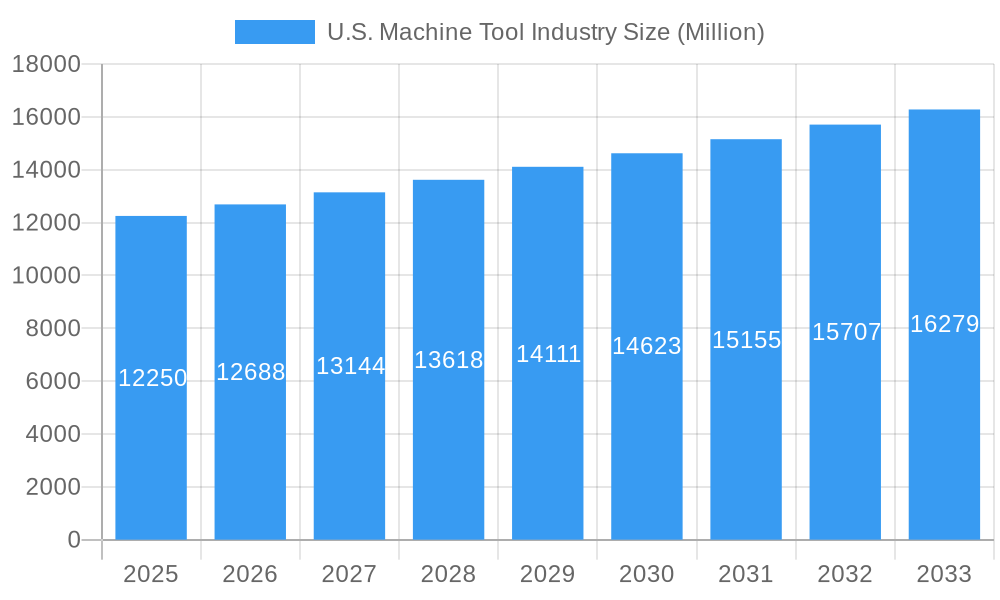

The U.S. machine tool industry, valued at $12.25 billion in 2025, is projected to experience steady growth, driven by a Compound Annual Growth Rate (CAGR) of 3.38% from 2025 to 2033. This expansion is fueled by several key factors. Increased automation across various manufacturing sectors, particularly in automotive, aerospace, and electronics, is a significant driver, demanding sophisticated and high-precision machine tools. Furthermore, reshoring initiatives and a focus on domestic manufacturing capabilities are bolstering demand for domestically produced machine tools. Technological advancements, such as the integration of advanced sensors, AI, and IoT capabilities, are enhancing machine tool performance and efficiency, leading to increased adoption. Government initiatives promoting technological innovation and infrastructure development also contribute positively to market growth. However, challenges exist. Fluctuations in global economic conditions and potential supply chain disruptions can impact industry growth. Moreover, intense competition from international manufacturers necessitates continuous innovation and cost optimization strategies for U.S. companies to maintain their market share. The industry is segmented based on machine type (e.g., milling machines, lathes, grinding machines), application (e.g., automotive, aerospace), and technology (e.g., CNC, conventional). Leading players like TRUMPF, Haas Automation, and Amada are constantly investing in R&D to maintain their competitive edge, further shaping market dynamics.

U.S. Machine Tool Industry Market Size (In Billion)

The forecast period of 2025-2033 anticipates continued growth, although the rate may fluctuate slightly due to macroeconomic factors. Understanding these fluctuations will require careful monitoring of key economic indicators and industry-specific trends. Segment-wise analysis reveals that the CNC machine tool segment holds the largest market share, driven by its flexibility and precision capabilities. Geographical analysis would show a concentration of market activity in key manufacturing hubs across the U.S. The historical period (2019-2024) likely witnessed variations in growth due to factors such as the COVID-19 pandemic, which temporarily disrupted supply chains and reduced manufacturing output. However, the industry's resilience and the ongoing demand for advanced manufacturing solutions suggest a strong recovery and continued expansion in the forecast period.

U.S. Machine Tool Industry Company Market Share

This comprehensive report delivers an in-depth analysis of the U.S. machine tool industry, providing crucial insights for strategic decision-making. Covering the period 2019-2033, with a base year of 2025 and a forecast period of 2025-2033, this report is essential for industry professionals, investors, and researchers seeking to understand the current market dynamics and future growth trajectories. The report incorporates data from the historical period (2019-2024) and offers a robust analysis of key market trends and competitive landscapes.

U.S. Machine Tool Industry Market Structure & Competitive Landscape

The U.S. machine tool industry exhibits a moderately concentrated market structure, with several major players dominating significant segments. The Herfindahl-Hirschman Index (HHI) for 2024 is estimated at xx, indicating a moderately concentrated market. Innovation is a critical driver, with companies continuously investing in advanced technologies like automation, digitalization, and AI-powered solutions to enhance efficiency and precision. Regulatory compliance, particularly concerning environmental and safety standards, exerts a significant influence, shaping manufacturing processes and product design. While some substitution exists through alternative manufacturing methods (e.g., 3D printing), the demand for high-precision machining remains strong across various industries. The industry is segmented by machine type (e.g., milling machines, lathes, grinding machines), application (e.g., automotive, aerospace, medical), and end-user (e.g., OEMs, Tier-1 suppliers). Mergers and acquisitions (M&A) activity has been moderate in recent years, with xx Million in M&A volume recorded in 2024. Key M&A trends involve consolidating market share and acquiring specialized technologies.

- High Concentration in Specific Niches: Certain segments, like high-speed machining centers, show higher concentration due to technological barriers to entry.

- Innovation-Driven Competition: Continuous R&D investments drive competitive advantages and create opportunities for new entrants with innovative technologies.

- Regulatory Compliance: Meeting stringent environmental and safety regulations represents a significant cost and challenge for manufacturers.

- End-User Segmentation: Automotive, aerospace, and medical industries are key end-user segments, each with specific requirements and preferences.

U.S. Machine Tool Industry Market Trends & Opportunities

The U.S. machine tool industry is on a robust growth trajectory, projected to experience a Compound Annual Growth Rate (CAGR) of approximately 6.5% during the forecast period (2025-2033). This expansion is anticipated to elevate the market size to around $25,000 Million by 2033. Several pivotal factors are fueling this surge. The relentless march of technological advancements, particularly in the realms of automation, artificial intelligence (AI), and comprehensive digitalization under the banner of Industry 4.0, is fundamentally reshaping manufacturing operations. These innovations are leading to unprecedented levels of efficiency, precision, and productivity across the board. The escalating adoption of highly sophisticated Computer Numerical Control (CNC) machines, alongside a pronounced demand for highly customized manufacturing solutions, are key catalysts for market expansion. Consumer preferences are increasingly leaning towards machine tools that offer higher precision, faster processing speeds, and enhanced, intuitive automation features. The competitive landscape is characterized by its dynamism, with continuous innovation and strategic alliances playing a crucial role in shaping market trajectories. The penetration rates for cutting-edge technologies such as AI-powered machine learning are experiencing a steady ascent, especially within larger, more established manufacturing facilities. Furthermore, the widespread adoption of digital twin technology and predictive maintenance strategies is significantly bolstering operational efficiency and proactively minimizing costly downtime. The burgeoning emphasis on sustainable manufacturing practices, supported by proactive government initiatives aimed at fostering advanced manufacturing ecosystems, presents substantial and lucrative opportunities for machine tool manufacturers committed to environmentally conscious production. The ongoing trends of reshoring and nearshoring are also contributing significantly to the industry's growth by stimulating increased domestic demand for advanced manufacturing capabilities.

Dominant Markets & Segments in U.S. Machine Tool Industry

The Midwest region currently dominates the U.S. machine tool market, accounting for approximately xx% of total revenue in 2024. This dominance is primarily attributed to the high concentration of manufacturing industries, especially in automotive and aerospace. Within segments, CNC machining centers and advanced milling machines are the leading revenue generators, driven by their versatility and precision.

Key Growth Drivers in the Midwest:

- Established manufacturing base

- Robust automotive and aerospace sectors

- Favorable infrastructure and logistics networks

- State and local government support for manufacturing industries.

Detailed Analysis of Market Dominance: The Midwest's concentration of skilled labor, established supply chains, and proactive government policies supporting advanced manufacturing contribute significantly to its market leadership. This dominance is expected to persist throughout the forecast period, though other regions may experience faster growth rates.

U.S. Machine Tool Industry Product Analysis

The U.S. machine tool industry is characterized by continuous product innovation, with advancements focused on improved precision, automation, and connectivity. Manufacturers are increasingly integrating advanced technologies such as AI, machine learning, and IoT to enhance machine performance, optimize production processes, and improve predictive maintenance capabilities. These innovations are resulting in products with higher efficiency, reduced downtime, and enhanced flexibility, catering to the evolving needs of various industries. The competitive advantage lies in delivering highly customized solutions, integrating advanced technologies, and providing superior after-sales service.

Key Drivers, Barriers & Challenges in U.S. Machine Tool Industry

Key Drivers: The U.S. machine tool industry's growth is primarily propelled by transformative technological advancements, encompassing automation, comprehensive digitalization, and the integration of Artificial Intelligence (AI). The escalating demand from critical end-user sectors, including automotive, aerospace, and medical devices, acts as a significant expansion engine. Government initiatives and dedicated funding programs that champion advanced manufacturing practices are fostering an increasingly favorable operational environment. The strategic imperative of reshoring and nearshoring production is also a substantial contributor, driving up domestic demand for high-quality machine tools.

Challenges: Persistent supply chain disruptions continue to pose a considerable hurdle, impacting the availability of essential components and extending lead times. The escalating costs of raw materials and an ongoing shortage of skilled labor are contributing to increased production expenses. Intense competition from international manufacturers exerts considerable pressure on pricing strategies and overall profit margins. Moreover, stringent environmental regulations necessitate substantial investments in compliance measures and the adoption of more sustainable manufacturing processes.

Growth Drivers in the U.S. Machine Tool Industry Market

The U.S. machine tool industry market's expansion is primarily fueled by a confluence of factors: significant technological advancements in automation, AI, and digitalization; robust and sustained demand emanating from key end-user industries such as automotive, aerospace, and medical manufacturing; proactive government support and incentives for advanced manufacturing adoption; and the strategic economic shifts driven by reshoring and nearshoring initiatives.

Challenges Impacting U.S. Machine Tool Industry Growth

Supply chain disruptions, rising material costs, labor shortages, international competition, and stringent environmental regulations pose significant challenges. These factors can collectively impact profitability and limit growth potential.

Key Players Shaping the U.S. Machine Tool Industry Market

- TRUMPF Inc

- Haas Automation Inc

- Amada Co Ltd

- Lincoln Electric Holdings Inc

- Multipress Inc

- MITUSA Inc

- MC Machinery Systems Inc

- Mate Precision Tooling Inc

- Bystronic Inc

- Laser Mechanisms Inc

- Koike Aronson Inc /Ransome

- FENN Metal Forming Machinery Solutions

- Cincinnati Inc (List Not Exhaustive)

Significant U.S. Machine Tool Industry Milestones

- July 2022: Peterson Tool Company, Inc. acquisition by Sandvik, expanding Sandvik's tooling portfolio.

- June 2022: Doosan Machine Tools rebrands as DN Solutions, signifying a broader focus on complete manufacturing solutions.

Future Outlook for U.S. Machine Tool Industry Market

The U.S. machine tool industry is robustly positioned for sustained and accelerated growth. This positive outlook is predominantly driven by the continuous wave of technological innovation, the widespread integration of advanced automation solutions, and a consistently strong demand from pivotal industrial sectors. Strategic and significant investments in research and development (R&D), coupled with an unwavering commitment to the principles of sustainable manufacturing, will be instrumental in shaping the industry's future trajectory. The market presents a wealth of significant opportunities for forward-thinking companies that demonstrate agility in adapting to evolving technological trends and a deep understanding of dynamic customer needs. The escalating emphasis on comprehensive digitalization and the strategic implementation of Industry 4.0 initiatives will continue to be powerful drivers of market expansion, concurrently unlocking new and exciting avenues for growth and innovation.

U.S. Machine Tool Industry Segmentation

-

1. Type

- 1.1. Metalworking Machines

- 1.2. Parts and Accessories

- 1.3. Installation

- 1.4. Repair

- 1.5. Maintenance

-

2. End User

- 2.1. Automotive

- 2.2. Fabrication and Industrial Machinery Manufacturing

- 2.3. Marine, Aerospace & Defense

- 2.4. Precision Engineering

- 2.5. Other End Users

U.S. Machine Tool Industry Segmentation By Geography

- 1. U.S.

U.S. Machine Tool Industry Regional Market Share

Geographic Coverage of U.S. Machine Tool Industry

U.S. Machine Tool Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.38% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Metalworking Machines

- 5.1.2. Parts and Accessories

- 5.1.3. Installation

- 5.1.4. Repair

- 5.1.5. Maintenance

- 5.2. Market Analysis, Insights and Forecast - by End User

- 5.2.1. Automotive

- 5.2.2. Fabrication and Industrial Machinery Manufacturing

- 5.2.3. Marine, Aerospace & Defense

- 5.2.4. Precision Engineering

- 5.2.5. Other End Users

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. U.S.

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. U.S. Machine Tool Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Metalworking Machines

- 6.1.2. Parts and Accessories

- 6.1.3. Installation

- 6.1.4. Repair

- 6.1.5. Maintenance

- 6.2. Market Analysis, Insights and Forecast - by End User

- 6.2.1. Automotive

- 6.2.2. Fabrication and Industrial Machinery Manufacturing

- 6.2.3. Marine, Aerospace & Defense

- 6.2.4. Precision Engineering

- 6.2.5. Other End Users

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 TRUMPF Inc

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Haas Automation Inc

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Amada Co Ltd

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Lincoln Electric Holdings Inc

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Multipress Inc

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 MITUSA Inc

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 MC Machinery Systems Inc

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Mate Precision Tooling Inc

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Bystronic Inc

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Laser Mechanisms Inc

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Koike Aronson Inc /Ransome

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 FENN Metal Forming Machinery Solutions

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 Cincinnati Inc **List Not Exhaustive

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.1 TRUMPF Inc

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: U.S. Machine Tool Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: U.S. Machine Tool Industry Share (%) by Company 2025

List of Tables

- Table 1: U.S. Machine Tool Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: U.S. Machine Tool Industry Volume Billion Forecast, by Type 2020 & 2033

- Table 3: U.S. Machine Tool Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 4: U.S. Machine Tool Industry Volume Billion Forecast, by End User 2020 & 2033

- Table 5: U.S. Machine Tool Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: U.S. Machine Tool Industry Volume Billion Forecast, by Region 2020 & 2033

- Table 7: U.S. Machine Tool Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 8: U.S. Machine Tool Industry Volume Billion Forecast, by Type 2020 & 2033

- Table 9: U.S. Machine Tool Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 10: U.S. Machine Tool Industry Volume Billion Forecast, by End User 2020 & 2033

- Table 11: U.S. Machine Tool Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 12: U.S. Machine Tool Industry Volume Billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the U.S. Machine Tool Industry?

The projected CAGR is approximately 3.38%.

2. Which companies are prominent players in the U.S. Machine Tool Industry?

Key companies in the market include TRUMPF Inc, Haas Automation Inc, Amada Co Ltd, Lincoln Electric Holdings Inc, Multipress Inc, MITUSA Inc, MC Machinery Systems Inc, Mate Precision Tooling Inc, Bystronic Inc, Laser Mechanisms Inc, Koike Aronson Inc /Ransome, FENN Metal Forming Machinery Solutions, Cincinnati Inc **List Not Exhaustive.

3. What are the main segments of the U.S. Machine Tool Industry?

The market segments include Type, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 12.25 Million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Increasing demand for domestic machine tools driving the market.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

July 2022: Peterson Tool Company, Inc. ("PTC"), a leading provider of machine-specific custom insert tooling solutions, had the previously announced finalized acquisition of its assets by Sandvik. Custom carbide form inserts are part of the product line and are used mainly in the general engineering and automotive industries for high-production turning and grooving applications. The operation will be referred to as Walter's GWS Tool division, which is a part of the Sandvik Manufacturing and Machining Solutions business area.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in Billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "U.S. Machine Tool Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the U.S. Machine Tool Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the U.S. Machine Tool Industry?

To stay informed about further developments, trends, and reports in the U.S. Machine Tool Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence