Key Insights

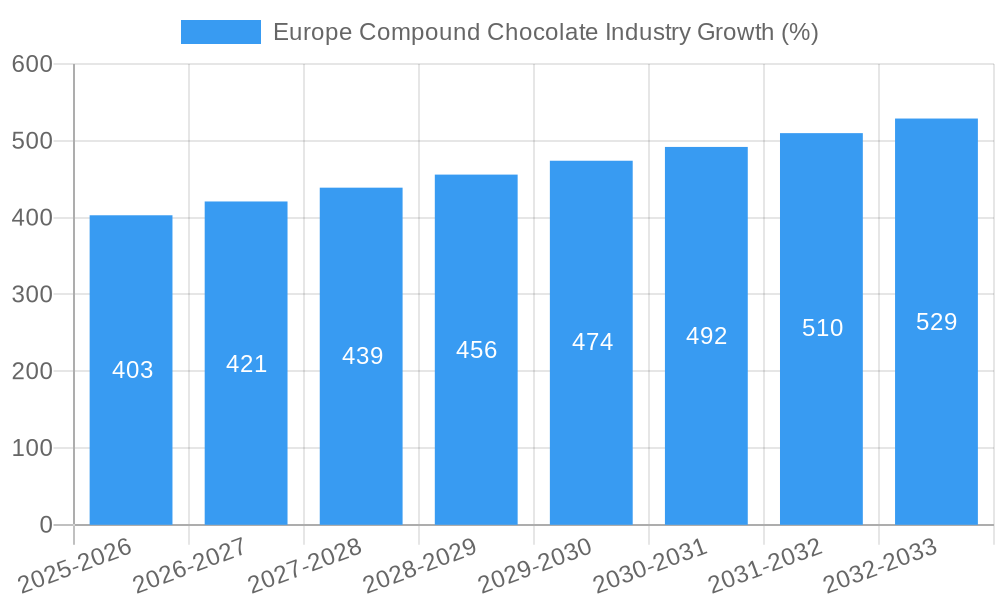

The European compound chocolate market, valued at approximately €X billion in 2025 (assuming a reasonable market size based on global trends and the provided CAGR), is projected to experience steady growth with a Compound Annual Growth Rate (CAGR) of 4.03% from 2025 to 2033. This growth is fueled by several key drivers. The rising popularity of convenient and ready-to-use ingredients within the bakery and confectionery sectors significantly boosts demand for compound chocolate. Furthermore, the increasing consumption of ice cream, frozen desserts, and chocolate-infused beverages fuels market expansion. Consumer preferences for premium and specialized chocolate types, such as dark chocolate, are also contributing to growth within specific segments. The market is segmented by type (dark, milk/white), form (chips, drops, chunks, slabs, coatings, other), and application (bakery, confectionery, ice cream, beverages, cereals, other). While the market shows strong potential, challenges exist. Fluctuations in raw material prices, particularly cocoa beans and dairy products, can impact profitability. Additionally, increasing health consciousness among consumers may lead to a shift towards healthier alternatives, potentially slowing growth in certain segments. Leading companies like Cargill, Barry Callebaut, and Puratos are strategically focusing on product innovation and expansion into new markets to capitalize on emerging opportunities within the European compound chocolate market. Germany, France, Italy, and the UK are key markets within Europe, collectively contributing a significant share of the overall regional market.

The competitive landscape is characterized by both established multinational corporations and smaller regional players. The presence of these diverse players fosters innovation and provides a wide range of product options for consumers. Future growth will hinge on successfully adapting to evolving consumer preferences, managing supply chain complexities, and mitigating the impact of economic factors. The focus on sustainability and ethical sourcing of raw materials is also emerging as a key factor influencing consumer choices and shaping the strategic decisions of companies operating within this dynamic market. The forecast period indicates continued growth, particularly in segments catering to specialized dietary needs and preferences, offering opportunities for both established and emerging players.

Europe Compound Chocolate Industry: A Comprehensive Market Report (2019-2033)

This dynamic report provides a detailed analysis of the Europe compound chocolate industry, offering invaluable insights for businesses, investors, and stakeholders. Leveraging extensive market research and data spanning the period 2019-2033 (base year 2025), this report unveils the industry's structure, competitive dynamics, and future trajectory. The report forecasts a market valued at xx Million by 2033, presenting a compelling growth opportunity for key players.

Europe Compound Chocolate Industry Market Structure & Competitive Landscape

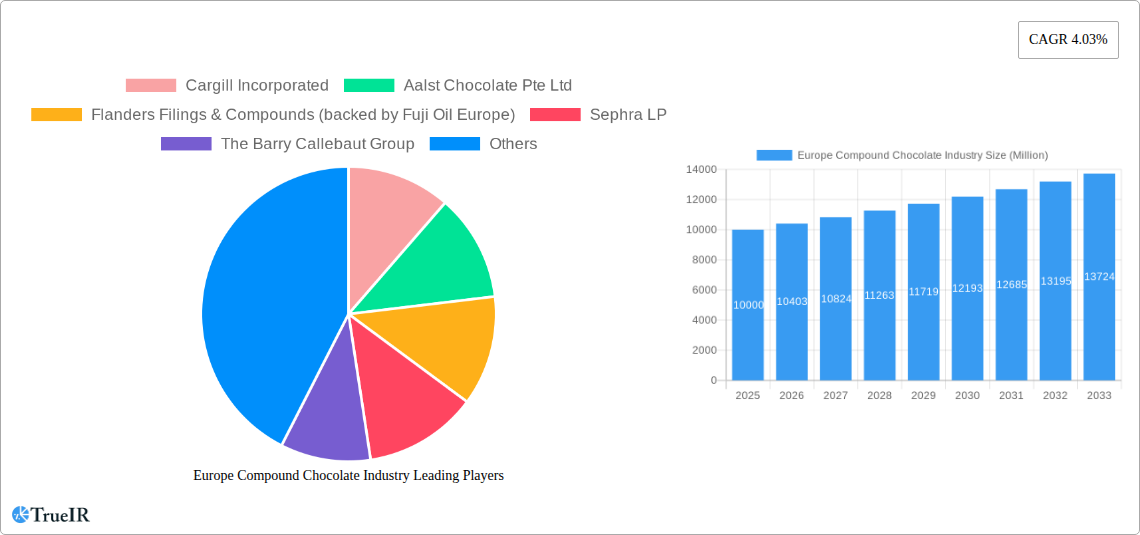

The European compound chocolate market exhibits a moderately concentrated structure, with several multinational giants and regional players vying for market share. Key players, including Cargill Incorporated, Aalst Chocolate Pte Ltd, Flanders Filings & Compounds (backed by Fuji Oil Europe), Sephra LP, The Barry Callebaut Group, Puratos NV, Clasen Quality Chocolate, AAK, and others, constantly innovate to meet evolving consumer demands. The Herfindahl-Hirschman Index (HHI) for the market is estimated at xx, suggesting a moderately competitive landscape.

- Innovation Drivers: Healthier formulations (e.g., reduced sugar, higher cocoa content), sustainable sourcing practices, and novel product formats (e.g., functional chocolates) are driving innovation.

- Regulatory Impacts: EU regulations concerning food labeling, ingredients, and sustainability significantly impact manufacturers' strategies.

- Product Substitutes: Other confectionery items, fruit snacks, and sugar-free alternatives pose some competitive pressure.

- End-User Segmentation: The market is significantly segmented by application, with bakery and confectionery dominating, followed by ice cream, beverages, and cereals.

- M&A Trends: The acquisition of Aalst Chocolate by Fuji Oil Europe in 2021 illustrates the ongoing consolidation in the market. The total value of M&A activities in the sector between 2019 and 2024 is estimated at xx Million.

Europe Compound Chocolate Industry Market Trends & Opportunities

The Europe compound chocolate market is experiencing robust growth, driven by rising disposable incomes, increasing demand for convenient and indulgent food products, and expanding food service sectors. The market size is estimated at xx Million in 2025 and is projected to grow at a Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033). Market penetration rates vary significantly across different product forms and applications. Chocolate chips/drops/chunks dominate, followed by chocolate slabs and coatings. Technological advancements, such as precision chocolate processing and innovative flavor combinations, continue to drive growth. Consumer preferences are shifting towards healthier options with reduced sugar content and increased cocoa solids, creating opportunities for manufacturers to offer premium, functional chocolates. Competitive dynamics are shaped by branding, price points, distribution networks, and innovation, with larger players leveraging their economies of scale.

Dominant Markets & Segments in Europe Compound Chocolate Industry

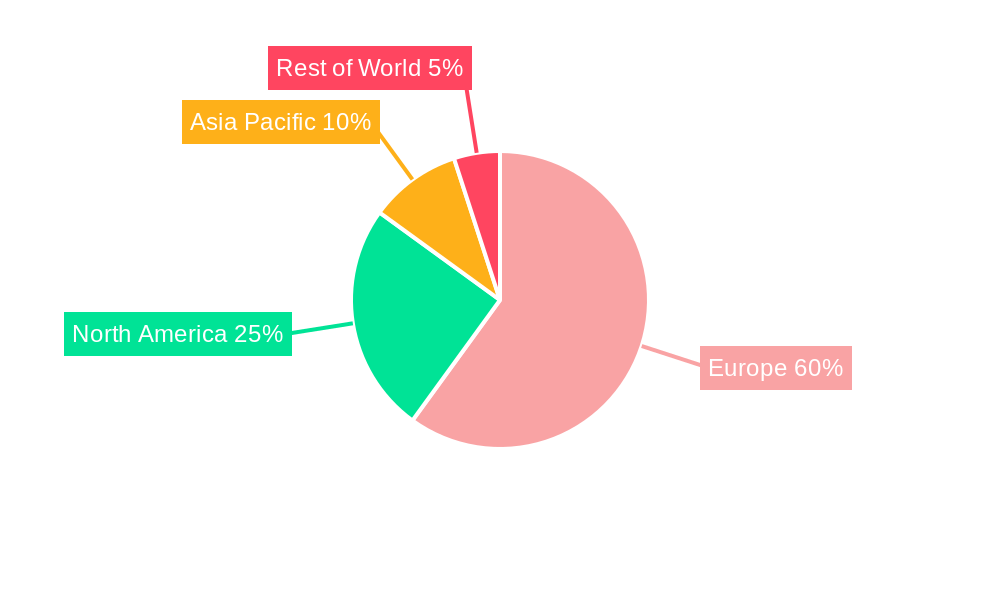

Western Europe represents the dominant market for compound chocolate, with Germany, France, and the UK being the key countries. The substantial confectionery and bakery industries in these nations drive demand.

Key Growth Drivers:

- Well-established food processing and retail infrastructure.

- High per capita chocolate consumption.

- Strong consumer preference for premium and specialized chocolates.

- Favorable regulatory environment promoting innovation and sustainable practices.

Dominant Segments:

- Type: Milk/white chocolate commands the largest market share, followed closely by dark chocolate. Growth in the dark chocolate segment is fueled by health and wellness trends.

- Form: Chocolate chips/drops/chunks are the most popular, favored for their convenience and versatility in various applications.

- Application: The bakery and confectionery sectors are the primary consumers of compound chocolate, accounting for over xx% of total market demand. Growth in the ice cream and frozen dessert segment is expected to be higher in coming years.

The detailed analysis delves into the specific market dynamics of each segment, revealing opportunities and challenges for each.

Europe Compound Chocolate Industry Product Analysis

Product innovation is characterized by a focus on clean-label ingredients, functional benefits (e.g., added fiber, probiotics), and unique flavor profiles. Manufacturers are increasingly leveraging advanced technologies to enhance the texture, taste, and shelf life of compound chocolate. Competitive advantages are derived from superior product quality, cost-effective manufacturing processes, and strong distribution networks. The emphasis on sustainable sourcing practices enhances the brand image and appeals to environmentally conscious consumers.

Key Drivers, Barriers & Challenges in Europe Compound Chocolate Industry

Key Drivers:

Rising disposable incomes, increasing demand for convenient and indulgent foods, expansion of the food service industry, and technological advancements in production are driving market growth. Government initiatives promoting sustainable cocoa sourcing provide further support.

Challenges:

Fluctuations in cocoa prices, stringent food safety and labeling regulations, intense competition, and increasing consumer demand for healthier options present challenges. Supply chain disruptions, especially those related to cocoa bean availability and logistics, may pose further impediments. The impact of these challenges is estimated to reduce the market growth by xx% over the forecast period.

Growth Drivers in the Europe Compound Chocolate Industry Market

The market is propelled by the growing demand for convenient and ready-to-eat products, along with increasing investments in sustainable and ethical sourcing practices. Health and wellness trends also drive the demand for dark chocolate and products with reduced sugar content. Technological advancements in chocolate processing and flavor enhancement contribute to product diversification and improved market offerings.

Challenges Impacting Europe Compound Chocolate Industry Growth

The industry faces challenges including volatile cocoa prices, rising production costs, stringent regulations impacting labeling and ingredient usage, and the growing preference for healthier alternatives. Intense competition from both established players and emerging brands adds to the pressure.

Key Players Shaping the Europe Compound Chocolate Industry Market

- Cargill Incorporated

- Aalst Chocolate Pte Ltd

- Flanders Filings & Compounds (backed by Fuji Oil Europe)

- Sephra LP

- The Barry Callebaut Group

- Puratos NV

- Clasen Quality Chocolate

- AAK

Significant Europe Compound Chocolate Industry Industry Milestones

- 2021: Acquisition of Aalst Chocolate by Fuji Oil Europe, expanding market consolidation.

- Ongoing: Launch of new dark chocolate products with health claims by major manufacturers, targeting the growing health-conscious segment.

- Ongoing: Investments in sustainable cocoa sourcing initiatives by various companies, addressing ethical and environmental concerns.

Future Outlook for Europe Compound Chocolate Industry Market

The Europe compound chocolate market is poised for continued growth driven by the factors previously described. Strategic partnerships, product diversification, and expansion into new markets are key opportunities. The market potential is significant, with further growth expected through innovations in product formats, flavors, and functional properties catering to evolving consumer preferences. The integration of technology and sustainable practices will be crucial for long-term success.

Europe Compound Chocolate Industry Segmentation

-

1. Type

- 1.1. Dark

- 1.2. Milk/White

-

2. Form

- 2.1. Chocolate Chips/Drops/Chunks

- 2.2. Chocolate Slab

- 2.3. Chocolate Coatings

- 2.4. Other Forms

-

3. Application

- 3.1. Bakery

- 3.2. Confectionery

- 3.3. Ice Cream and Frozen Desserts

- 3.4. Beverages

- 3.5. Cereals

- 3.6. Other Applications

Europe Compound Chocolate Industry Segmentation By Geography

-

1. Europe

- 1.1. Germany

- 1.2. United Kingdom

- 1.3. France

- 1.4. Russia

- 1.5. Italy

- 1.6. Spain

- 1.7. Rest of Europe

Europe Compound Chocolate Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 4.03% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Wide Applications and Functionality; Demand For Gluten-Free Products

- 3.3. Market Restrains

- 3.3.1. Easy Availability of Economically Feasible Alternatives

- 3.4. Market Trends

- 3.4.1. Dark Compound Chocolate Becoming the Fastest Growing Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Europe Compound Chocolate Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Dark

- 5.1.2. Milk/White

- 5.2. Market Analysis, Insights and Forecast - by Form

- 5.2.1. Chocolate Chips/Drops/Chunks

- 5.2.2. Chocolate Slab

- 5.2.3. Chocolate Coatings

- 5.2.4. Other Forms

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. Bakery

- 5.3.2. Confectionery

- 5.3.3. Ice Cream and Frozen Desserts

- 5.3.4. Beverages

- 5.3.5. Cereals

- 5.3.6. Other Applications

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Germany Europe Compound Chocolate Industry Analysis, Insights and Forecast, 2019-2031

- 7. France Europe Compound Chocolate Industry Analysis, Insights and Forecast, 2019-2031

- 8. Italy Europe Compound Chocolate Industry Analysis, Insights and Forecast, 2019-2031

- 9. United Kingdom Europe Compound Chocolate Industry Analysis, Insights and Forecast, 2019-2031

- 10. Netherlands Europe Compound Chocolate Industry Analysis, Insights and Forecast, 2019-2031

- 11. Sweden Europe Compound Chocolate Industry Analysis, Insights and Forecast, 2019-2031

- 12. Rest of Europe Europe Compound Chocolate Industry Analysis, Insights and Forecast, 2019-2031

- 13. Competitive Analysis

- 13.1. Market Share Analysis 2024

- 13.2. Company Profiles

- 13.2.1 Cargill Incorporated

- 13.2.1.1. Overview

- 13.2.1.2. Products

- 13.2.1.3. SWOT Analysis

- 13.2.1.4. Recent Developments

- 13.2.1.5. Financials (Based on Availability)

- 13.2.2 Aalst Chocolate Pte Ltd

- 13.2.2.1. Overview

- 13.2.2.2. Products

- 13.2.2.3. SWOT Analysis

- 13.2.2.4. Recent Developments

- 13.2.2.5. Financials (Based on Availability)

- 13.2.3 Flanders Filings & Compounds (backed by Fuji Oil Europe)

- 13.2.3.1. Overview

- 13.2.3.2. Products

- 13.2.3.3. SWOT Analysis

- 13.2.3.4. Recent Developments

- 13.2.3.5. Financials (Based on Availability)

- 13.2.4 Sephra LP

- 13.2.4.1. Overview

- 13.2.4.2. Products

- 13.2.4.3. SWOT Analysis

- 13.2.4.4. Recent Developments

- 13.2.4.5. Financials (Based on Availability)

- 13.2.5 The Barry Callebaut Group

- 13.2.5.1. Overview

- 13.2.5.2. Products

- 13.2.5.3. SWOT Analysis

- 13.2.5.4. Recent Developments

- 13.2.5.5. Financials (Based on Availability)

- 13.2.6 Puratos NV

- 13.2.6.1. Overview

- 13.2.6.2. Products

- 13.2.6.3. SWOT Analysis

- 13.2.6.4. Recent Developments

- 13.2.6.5. Financials (Based on Availability)

- 13.2.7 Clasen Quality Chocolate*List Not Exhaustive

- 13.2.7.1. Overview

- 13.2.7.2. Products

- 13.2.7.3. SWOT Analysis

- 13.2.7.4. Recent Developments

- 13.2.7.5. Financials (Based on Availability)

- 13.2.8 AAK

- 13.2.8.1. Overview

- 13.2.8.2. Products

- 13.2.8.3. SWOT Analysis

- 13.2.8.4. Recent Developments

- 13.2.8.5. Financials (Based on Availability)

- 13.2.1 Cargill Incorporated

List of Figures

- Figure 1: Europe Compound Chocolate Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Europe Compound Chocolate Industry Share (%) by Company 2024

List of Tables

- Table 1: Europe Compound Chocolate Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Europe Compound Chocolate Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 3: Europe Compound Chocolate Industry Revenue Million Forecast, by Form 2019 & 2032

- Table 4: Europe Compound Chocolate Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 5: Europe Compound Chocolate Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 6: Europe Compound Chocolate Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 7: Germany Europe Compound Chocolate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: France Europe Compound Chocolate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Italy Europe Compound Chocolate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: United Kingdom Europe Compound Chocolate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Netherlands Europe Compound Chocolate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Sweden Europe Compound Chocolate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Rest of Europe Europe Compound Chocolate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Europe Compound Chocolate Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 15: Europe Compound Chocolate Industry Revenue Million Forecast, by Form 2019 & 2032

- Table 16: Europe Compound Chocolate Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 17: Europe Compound Chocolate Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 18: Germany Europe Compound Chocolate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: United Kingdom Europe Compound Chocolate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: France Europe Compound Chocolate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: Russia Europe Compound Chocolate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Italy Europe Compound Chocolate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: Spain Europe Compound Chocolate Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: Rest of Europe Europe Compound Chocolate Industry Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Compound Chocolate Industry?

The projected CAGR is approximately 4.03%.

2. Which companies are prominent players in the Europe Compound Chocolate Industry?

Key companies in the market include Cargill Incorporated, Aalst Chocolate Pte Ltd, Flanders Filings & Compounds (backed by Fuji Oil Europe), Sephra LP, The Barry Callebaut Group, Puratos NV, Clasen Quality Chocolate*List Not Exhaustive, AAK.

3. What are the main segments of the Europe Compound Chocolate Industry?

The market segments include Type, Form, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Wide Applications and Functionality; Demand For Gluten-Free Products.

6. What are the notable trends driving market growth?

Dark Compound Chocolate Becoming the Fastest Growing Market.

7. Are there any restraints impacting market growth?

Easy Availability of Economically Feasible Alternatives.

8. Can you provide examples of recent developments in the market?

1. Acquisition of Aalst Chocolate by Fuji Oil Europe in 2021 2. Launch of new dark chocolate products with health claims by leading manufacturers 3. Investment in sustainable cocoa sourcing initiatives by industry players

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Compound Chocolate Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Compound Chocolate Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Compound Chocolate Industry?

To stay informed about further developments, trends, and reports in the Europe Compound Chocolate Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence