Key Insights

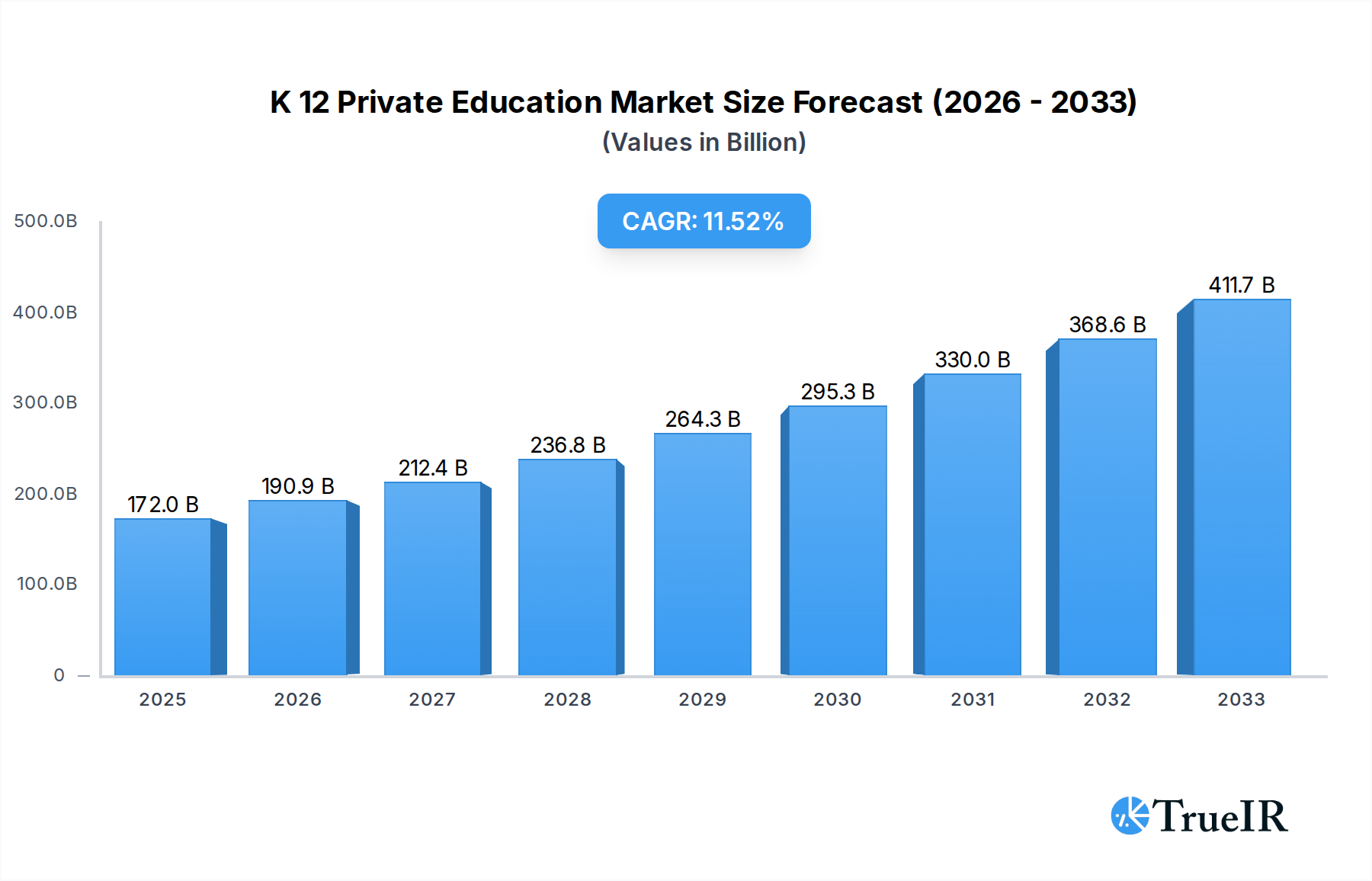

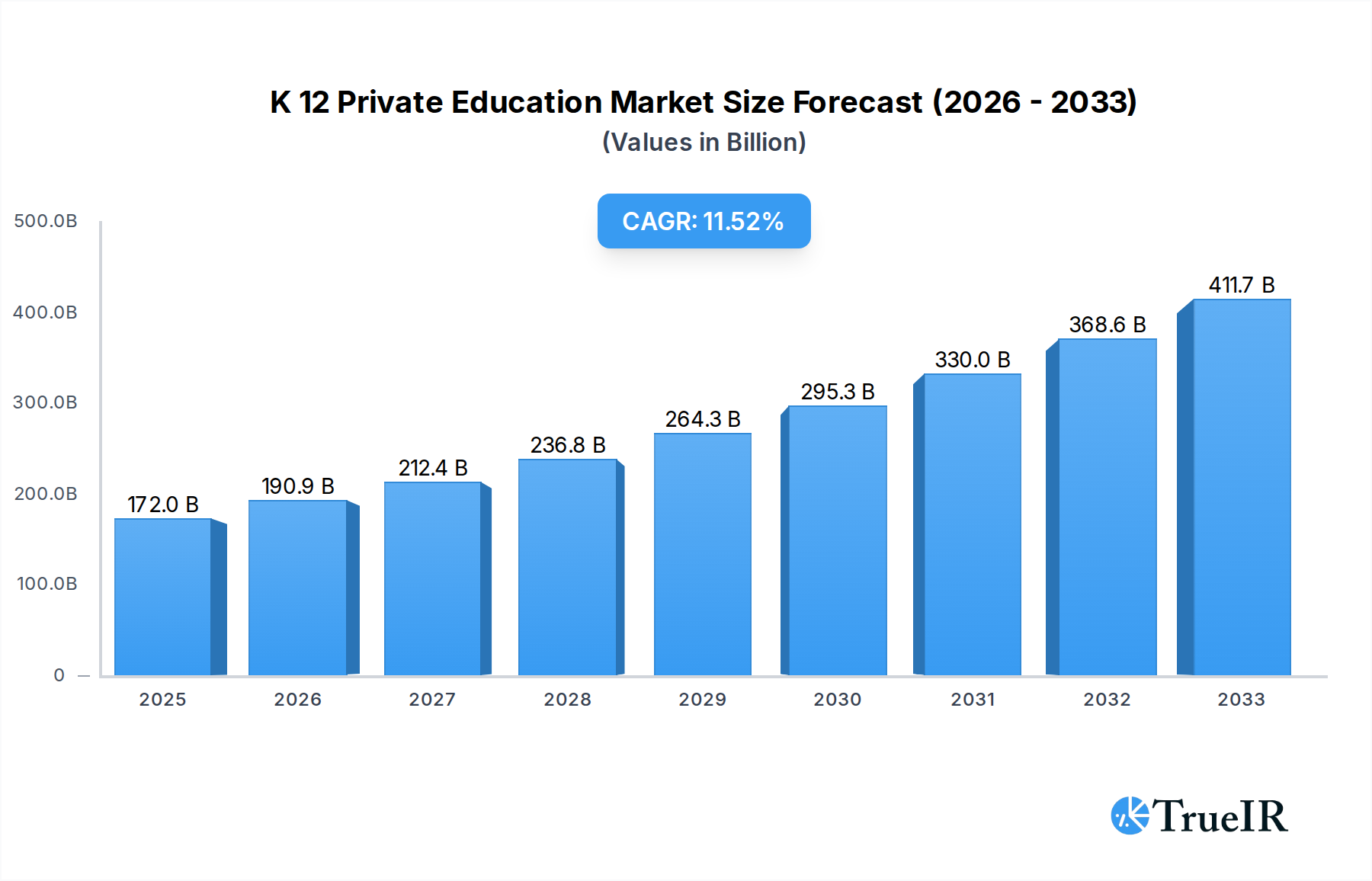

The global K-12 private education market is experiencing robust expansion, projected to reach an estimated USD 172.03 billion in 2025. This significant growth is fueled by an impressive CAGR of 17.47% over the forecast period from 2025 to 2033. A primary driver for this surge is the increasing parental emphasis on high-quality, individualized education that goes beyond traditional public schooling. This includes a growing demand for specialized curricula, advanced learning technologies, and a focus on holistic development, encompassing critical thinking, creativity, and problem-solving skills. The rise of affluent and upwardly mobile populations globally, particularly in emerging economies, is also a key contributor, as these demographics prioritize premium educational opportunities for their children. Furthermore, a perceived inadequacy in public education systems in certain regions, coupled with a desire for safer and more conducive learning environments, propels parents towards private institutions. The market is also being shaped by technological advancements, with online and blended learning models gaining traction, offering greater flexibility and accessibility.

K 12 Private Education Market Size (In Billion)

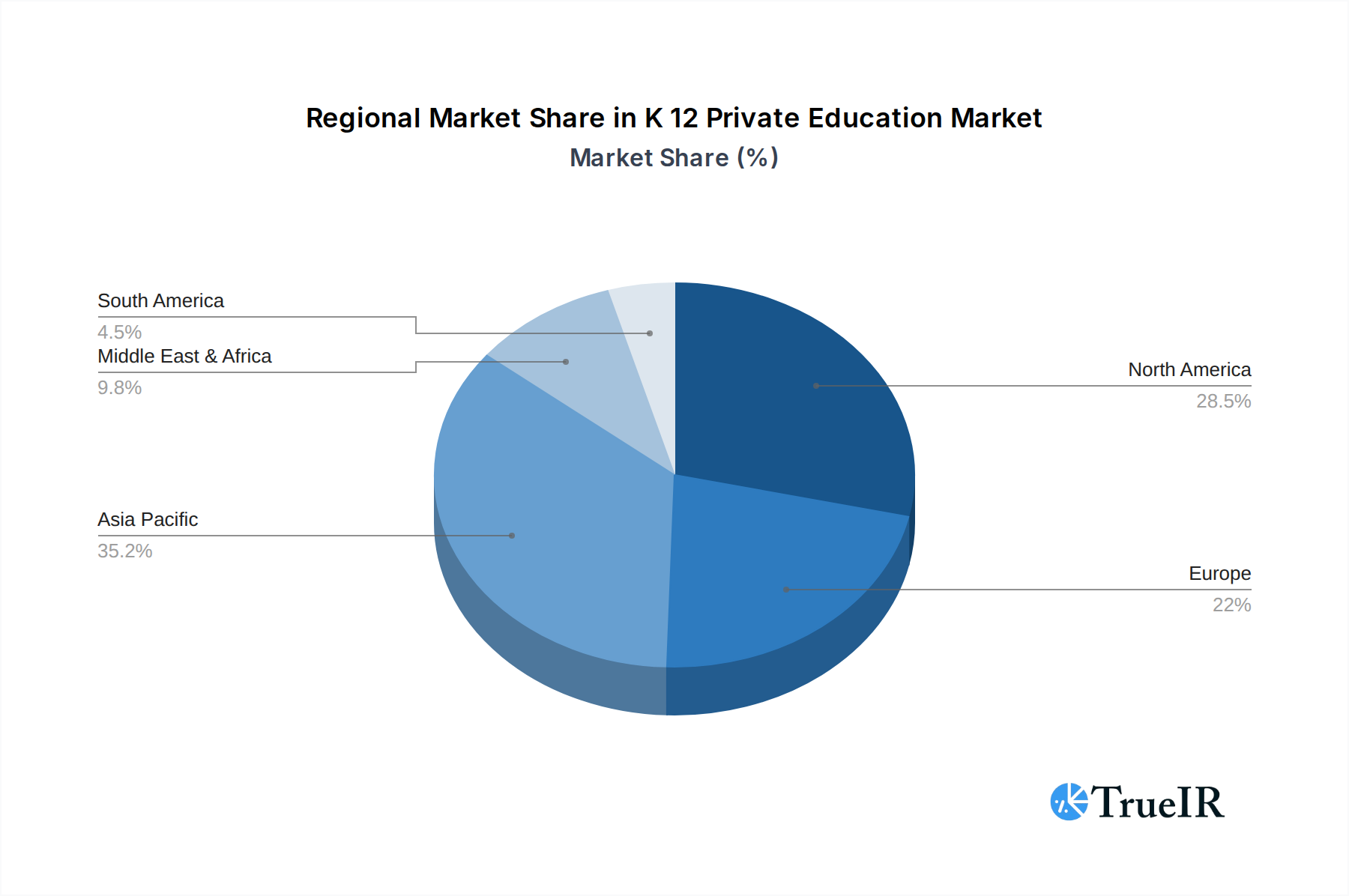

The market segmentation reveals a diverse landscape of offerings. In terms of application, all segments from Pre-Primary to High School education are expected to witness substantial growth as parents invest in their children's educational journey from an early age through to secondary completion. The "Type" segmentation highlights the dynamic shift towards more engaging and effective learning methodologies. While instructor-led training remains a cornerstone, the rapid adoption of computer and web-based training, simulation-based training, and video/audio recordings indicates a strong preference for interactive and modern pedagogical approaches. Textbooks and self-study materials continue to play a role, but their prominence is gradually evolving alongside digital resources. Key companies like Ambow Education, New Oriental Education and Technology, and TAL Education Group are at the forefront, investing in innovation and expanding their reach across various regions, including North America, Europe, and the rapidly growing Asia Pacific market. This competitive landscape, characterized by both established educational providers and emerging EdTech players, will continue to drive market evolution and innovation.

K 12 Private Education Company Market Share

Here is a dynamic, SEO-optimized report description for K 12 Private Education, designed for immediate use without modification.

This comprehensive report provides an in-depth analysis of the global K 12 Private Education market, offering critical insights for industry stakeholders, investors, and educational institutions. Spanning from 2019 to 2033, with a base and estimated year of 2025, this report meticulously dissects market structure, competitive dynamics, emerging trends, and future growth prospects. Leveraging high-volume keywords such as "K 12 private education," "online learning," " edtech," "private schools," "curriculum development," and "educational technology," this report is optimized for maximum search visibility and audience engagement.

K 12 Private Education Market Structure & Competitive Landscape

The K 12 Private Education market exhibits a moderately concentrated structure, with a few dominant players controlling a significant portion of the market share. Innovation is a key driver, fueled by rapid advancements in educational technology (EdTech) and a growing demand for personalized learning experiences. Regulatory frameworks worldwide present a complex yet evolving landscape, influencing curriculum standards, accreditation, and operational compliance. Product substitutes, such as free online resources and public schooling alternatives, continuously challenge market expansion, necessitating differentiation through superior pedagogical approaches and enhanced learning outcomes. End-user segmentation reveals a diverse demand across pre-primary, primary, middle, and high school levels, each with unique educational needs. Mergers and acquisitions (M&A) are an active trend, as larger entities seek to consolidate market presence, acquire innovative technologies, and expand their geographical reach. For instance, M&A volumes are estimated to be in the billions, reflecting strategic consolidations within the industry. Concentration ratios indicate that the top five companies hold approximately xx% of the market share, underscoring the competitive intensity.

- Innovation Drivers: Technological advancements, demand for personalized learning, and pedagogical research.

- Regulatory Impacts: Varied national and international education policies, accreditation standards, and data privacy laws.

- Product Substitutes: Public education, free online learning platforms, homeschooling resources.

- End-User Segmentation: Pre-primary, Primary, Middle School, High School segments with distinct learning requirements.

- M&A Trends: Strategic acquisitions to gain market share, access new technologies, and expand service offerings, with an estimated market value of billions.

K 12 Private Education Market Trends & Opportunities

The global K 12 Private Education market is poised for substantial growth, driven by an escalating demand for high-quality, personalized, and flexible learning solutions. The market size is projected to reach billions by 2033, exhibiting a robust Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025–2033). Technological shifts are fundamentally reshaping the educational landscape, with the proliferation of EdTech solutions, including Artificial Intelligence (AI) in personalized learning, Virtual Reality (VR) for immersive experiences, and advanced Learning Management Systems (LMS). Consumer preferences are increasingly leaning towards blended learning models, digital resources, and a focus on developing 21st-century skills like critical thinking, problem-solving, and digital literacy. The competitive dynamics are intensifying, with both traditional private institutions and new EdTech startups vying for market share. Opportunities abound in emerging economies where access to quality private education is expanding rapidly, and in specialized niches such as STEM education, special needs education, and early childhood development. The increasing adoption of online and hybrid learning models, accelerated by global events, has further democratized access and broadened the market reach for private education providers. The market penetration rate for digital learning tools within private schools is estimated to exceed xx% by 2033.

Dominant Markets & Segments in K 12 Private Education

The K 12 Private Education market's dominance is characterized by a confluence of regional strengths, technological adoption, and specific application segments. Geographically, North America and Asia Pacific are emerging as leading markets due to a strong emphasis on educational excellence, significant investment in EdTech infrastructure, and a growing middle class with the financial capacity for private schooling. Within the Asia Pacific region, countries like China and India are witnessing unprecedented growth in private education, driven by competitive academic pressures and a desire for global standard education.

In terms of Application, the Primary School and Middle School segments are experiencing robust expansion, reflecting the foundational importance of these stages in a child's educational journey and the increasing parental focus on early learning interventions. However, the High School segment is also showing considerable growth, particularly with the rise of international curricula and university preparation programs.

The dominant Type of education delivery is Instructor-led Training, which remains paramount for structured learning and direct student-teacher interaction. Simultaneously, Computer and Web-based Training is experiencing explosive growth, driven by the convenience, flexibility, and accessibility it offers. This includes a wide array of online courses, virtual classrooms, and educational apps. Textbooks and Self-study Material, though evolving, still hold relevance, often integrated with digital platforms. The demand for Video and Audio Recording for supplementary learning and on-demand content is also significant. Simulation-based Training is gaining traction, especially in subjects like science and vocational training, offering practical, hands-on learning experiences in a safe digital environment.

- Leading Region: Asia Pacific, driven by economic growth and rising educational aspirations.

- Key Growth Drivers (Regional): Government initiatives promoting private education, increased disposable income, and a cultural emphasis on academic achievement.

- Dominant Application Segments: Primary School and Middle School, with High School showing strong upward trajectory.

- Key Growth Drivers (Application): Emphasis on foundational learning, preparation for higher education, and personalized learning pathways.

- Dominant Type Segments: Instructor-led Training and Computer and Web-based Training.

- Key Growth Drivers (Type): Demand for flexibility, accessibility, personalized learning experiences, and technological integration in curriculum delivery. The market size for Computer and Web-based Training is projected to reach billions by 2033.

K 12 Private Education Product Analysis

Product innovations in K 12 Private Education are heavily influenced by technological advancements and a drive for enhanced student engagement. AI-powered adaptive learning platforms are revolutionizing personalized instruction, tailoring content and pace to individual student needs. Immersive VR and AR experiences are transforming subjects like science and history, offering unparalleled engagement and comprehension. Gamified learning modules are increasingly integrated to make education more interactive and enjoyable. Competitive advantages are being carved out through comprehensive digital ecosystems that blend curriculum delivery, assessment tools, parent communication portals, and robust analytics for tracking student progress. The market fit is optimized by aligning these products with diverse learning styles and educational standards globally, ensuring scalability and accessibility.

Key Drivers, Barriers & Challenges in K 12 Private Education

The K 12 Private Education market is propelled by several key drivers. Technological innovation, particularly in EdTech, is a primary catalyst, enabling more engaging and personalized learning experiences. Increasing parental awareness of the benefits of private education, including smaller class sizes, specialized curricula, and improved facilities, is a significant economic driver. Favorable government policies and incentives in certain regions also foster growth.

- Technological Advancements: AI, VR, AR, and advanced LMS platforms.

- Parental Demand: Growing emphasis on quality education and individualized attention.

- Economic Factors: Rising disposable incomes and investment in education.

- Policy Support: Government initiatives promoting private educational institutions.

However, the market faces notable barriers and challenges. High operational costs, including infrastructure, technology investment, and qualified faculty, can limit accessibility for some. Stringent and evolving regulatory frameworks across different jurisdictions create compliance hurdles. Intense competition from both established private schools and emerging EdTech providers can lead to price wars and market saturation.

- High Costs: Infrastructure, technology, and faculty expenses.

- Regulatory Hurdles: Varying and complex educational policies and accreditation standards.

- Competitive Pressures: Intense rivalry among private institutions and EdTech players.

- Digital Divide: Unequal access to technology and internet connectivity, impacting the reach of online solutions.

Growth Drivers in the K 12 Private Education Market

The K 12 Private Education market's growth is predominantly fueled by technological advancements and evolving pedagogical approaches. The integration of AI for personalized learning paths and adaptive assessments is a significant driver, catering to individual student needs. The increasing demand for specialized curricula, such as STEM education and international programs, further propels market expansion. Furthermore, favorable economic conditions in many regions, characterized by rising disposable incomes, empower parents to invest more in private schooling, seeking superior educational outcomes for their children. Policy shifts and government support for private education initiatives in select countries also contribute to a positive growth trajectory.

Challenges Impacting K 12 Private Education Growth

Despite robust growth, the K 12 Private Education sector grapples with several challenges. Regulatory complexities and evolving compliance requirements across different countries pose significant hurdles for standardization and scalability. Supply chain issues, particularly concerning the procurement and integration of advanced educational technologies, can lead to delays and increased costs. Competitive pressures are escalating, with both traditional institutions and nimble EdTech startups vying for market share, leading to potential price erosion. Furthermore, the digital divide remains a persistent issue, limiting the reach of online learning solutions to underserved populations and exacerbating educational inequalities. The estimated financial impact of these challenges on market expansion is in the billions.

Key Players Shaping the K 12 Private Education Market

- Ambow Education

- CDEL

- New Oriental Education and Technology

- British International School of Jeddah

- Cengage Learning India Pvt. Ltd.

- Chegg Inc.

- Dhuha International School

- Dubai International Academy

- K12 Inc.

- McGraw-Hill Education

- Nadeen International School

- Vedantu

- Pearson Education Inc.

- Providence Equity Partners LLC

- TAL Education Group

- Next Education India Pvt. Ltd.

- iTutorGroup

- EF Education First

Significant K 12 Private Education Industry Milestones

- 2019: Widespread adoption of blended learning models gains momentum.

- 2020: The COVID-19 pandemic accelerates the adoption of online and remote learning technologies, demonstrating their resilience and effectiveness.

- 2021: Increased investment in EdTech startups focused on AI-driven personalized learning and gamification, with billions invested.

- 2022: Global expansion of international school chains and curriculum providers to meet growing demand.

- 2023: Development and integration of advanced VR/AR educational content for immersive learning experiences.

- 2024: Growing focus on socio-emotional learning (SEL) and mental health support within private educational frameworks.

Future Outlook for K 12 Private Education Market

The future outlook for the K 12 Private Education market is exceptionally promising, driven by continuous technological innovation and an enduring demand for high-quality, customized educational experiences. The continued integration of AI, VR, and AR will revolutionize learning, offering more engaging and effective pedagogical approaches. Blended and hybrid learning models are set to become the norm, providing flexibility and accessibility. Emerging economies present significant growth catalysts, with expanding middle classes prioritizing private education. Strategic collaborations between traditional institutions and EdTech providers will further shape the market, fostering innovation and expanding service offerings. The market is expected to witness sustained growth, reaching billions in value by 2033, fueled by a commitment to lifelong learning and the development of future-ready skills.

K 12 Private Education Segmentation

-

1. Application

- 1.1. Pre-Primary School

- 1.2. Primary School

- 1.3. Middle School

- 1.4. High School

-

2. Type

- 2.1. Instructor-led Training

- 2.2. Computer and Web-based Training

- 2.3. Textbooks and Self-study Material

- 2.4. Video and Audio Recording

- 2.5. Simulation-based Training

- 2.6. Others

K 12 Private Education Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

K 12 Private Education Regional Market Share

Geographic Coverage of K 12 Private Education

K 12 Private Education REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 17.47% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global K 12 Private Education Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Pre-Primary School

- 5.1.2. Primary School

- 5.1.3. Middle School

- 5.1.4. High School

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Instructor-led Training

- 5.2.2. Computer and Web-based Training

- 5.2.3. Textbooks and Self-study Material

- 5.2.4. Video and Audio Recording

- 5.2.5. Simulation-based Training

- 5.2.6. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America K 12 Private Education Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Pre-Primary School

- 6.1.2. Primary School

- 6.1.3. Middle School

- 6.1.4. High School

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Instructor-led Training

- 6.2.2. Computer and Web-based Training

- 6.2.3. Textbooks and Self-study Material

- 6.2.4. Video and Audio Recording

- 6.2.5. Simulation-based Training

- 6.2.6. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America K 12 Private Education Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Pre-Primary School

- 7.1.2. Primary School

- 7.1.3. Middle School

- 7.1.4. High School

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Instructor-led Training

- 7.2.2. Computer and Web-based Training

- 7.2.3. Textbooks and Self-study Material

- 7.2.4. Video and Audio Recording

- 7.2.5. Simulation-based Training

- 7.2.6. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe K 12 Private Education Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Pre-Primary School

- 8.1.2. Primary School

- 8.1.3. Middle School

- 8.1.4. High School

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Instructor-led Training

- 8.2.2. Computer and Web-based Training

- 8.2.3. Textbooks and Self-study Material

- 8.2.4. Video and Audio Recording

- 8.2.5. Simulation-based Training

- 8.2.6. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa K 12 Private Education Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Pre-Primary School

- 9.1.2. Primary School

- 9.1.3. Middle School

- 9.1.4. High School

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Instructor-led Training

- 9.2.2. Computer and Web-based Training

- 9.2.3. Textbooks and Self-study Material

- 9.2.4. Video and Audio Recording

- 9.2.5. Simulation-based Training

- 9.2.6. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific K 12 Private Education Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Pre-Primary School

- 10.1.2. Primary School

- 10.1.3. Middle School

- 10.1.4. High School

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Instructor-led Training

- 10.2.2. Computer and Web-based Training

- 10.2.3. Textbooks and Self-study Material

- 10.2.4. Video and Audio Recording

- 10.2.5. Simulation-based Training

- 10.2.6. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Ambow Education

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 CDEL

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 New Oriental Education and Technology

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 British International School of Jeddah

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Cengage Learning India Pvt. Ltd.

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Chegg Inc.

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Dhuha International School

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Dubai International Academy

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 K12 Inc.

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 McGraw-Hill Education

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Nadeen International School

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Vedantu

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Pearson Education Inc.

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Providence Equity Partners LLC

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 TAL Education Group

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Next Education India Pvt. Ltd.

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 iTutorGroup

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 EF Education First

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.1 Ambow Education

List of Figures

- Figure 1: Global K 12 Private Education Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America K 12 Private Education Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America K 12 Private Education Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America K 12 Private Education Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America K 12 Private Education Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America K 12 Private Education Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America K 12 Private Education Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America K 12 Private Education Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America K 12 Private Education Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America K 12 Private Education Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America K 12 Private Education Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America K 12 Private Education Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America K 12 Private Education Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe K 12 Private Education Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe K 12 Private Education Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe K 12 Private Education Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe K 12 Private Education Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe K 12 Private Education Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe K 12 Private Education Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa K 12 Private Education Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa K 12 Private Education Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa K 12 Private Education Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa K 12 Private Education Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa K 12 Private Education Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa K 12 Private Education Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific K 12 Private Education Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific K 12 Private Education Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific K 12 Private Education Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific K 12 Private Education Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific K 12 Private Education Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific K 12 Private Education Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global K 12 Private Education Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global K 12 Private Education Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global K 12 Private Education Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global K 12 Private Education Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global K 12 Private Education Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global K 12 Private Education Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States K 12 Private Education Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada K 12 Private Education Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico K 12 Private Education Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global K 12 Private Education Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global K 12 Private Education Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global K 12 Private Education Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil K 12 Private Education Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina K 12 Private Education Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America K 12 Private Education Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global K 12 Private Education Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global K 12 Private Education Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global K 12 Private Education Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom K 12 Private Education Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany K 12 Private Education Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France K 12 Private Education Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy K 12 Private Education Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain K 12 Private Education Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia K 12 Private Education Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux K 12 Private Education Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics K 12 Private Education Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe K 12 Private Education Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global K 12 Private Education Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global K 12 Private Education Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global K 12 Private Education Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey K 12 Private Education Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel K 12 Private Education Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC K 12 Private Education Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa K 12 Private Education Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa K 12 Private Education Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa K 12 Private Education Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global K 12 Private Education Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global K 12 Private Education Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global K 12 Private Education Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China K 12 Private Education Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India K 12 Private Education Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan K 12 Private Education Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea K 12 Private Education Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN K 12 Private Education Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania K 12 Private Education Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific K 12 Private Education Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the K 12 Private Education?

The projected CAGR is approximately 17.47%.

2. Which companies are prominent players in the K 12 Private Education?

Key companies in the market include Ambow Education, CDEL, New Oriental Education and Technology, British International School of Jeddah, Cengage Learning India Pvt. Ltd., Chegg Inc., Dhuha International School, Dubai International Academy, K12 Inc., McGraw-Hill Education, Nadeen International School, Vedantu, Pearson Education Inc., Providence Equity Partners LLC, TAL Education Group, Next Education India Pvt. Ltd., iTutorGroup, EF Education First.

3. What are the main segments of the K 12 Private Education?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "K 12 Private Education," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the K 12 Private Education report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the K 12 Private Education?

To stay informed about further developments, trends, and reports in the K 12 Private Education, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence