Key Insights

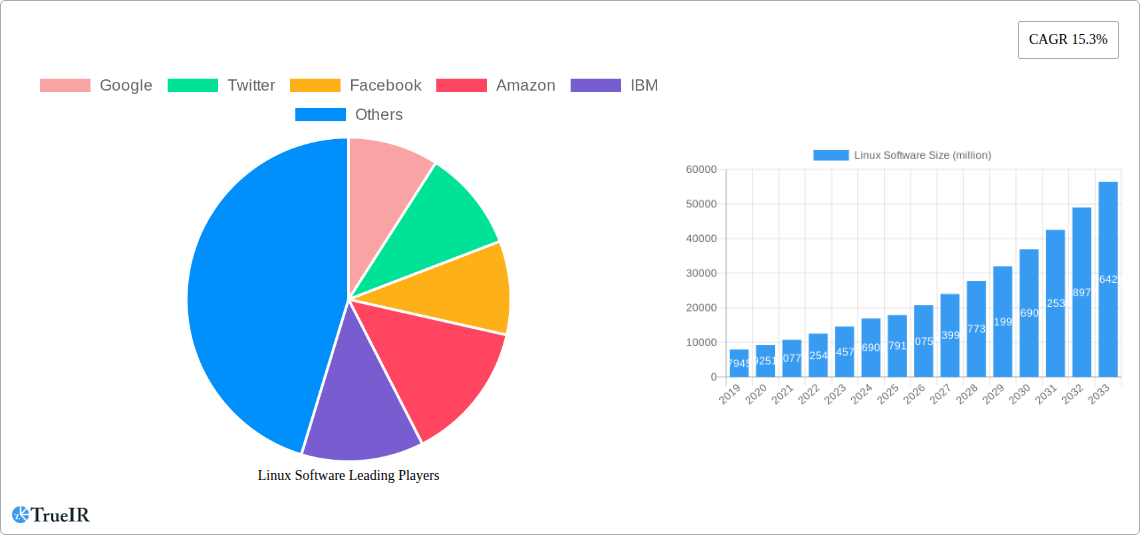

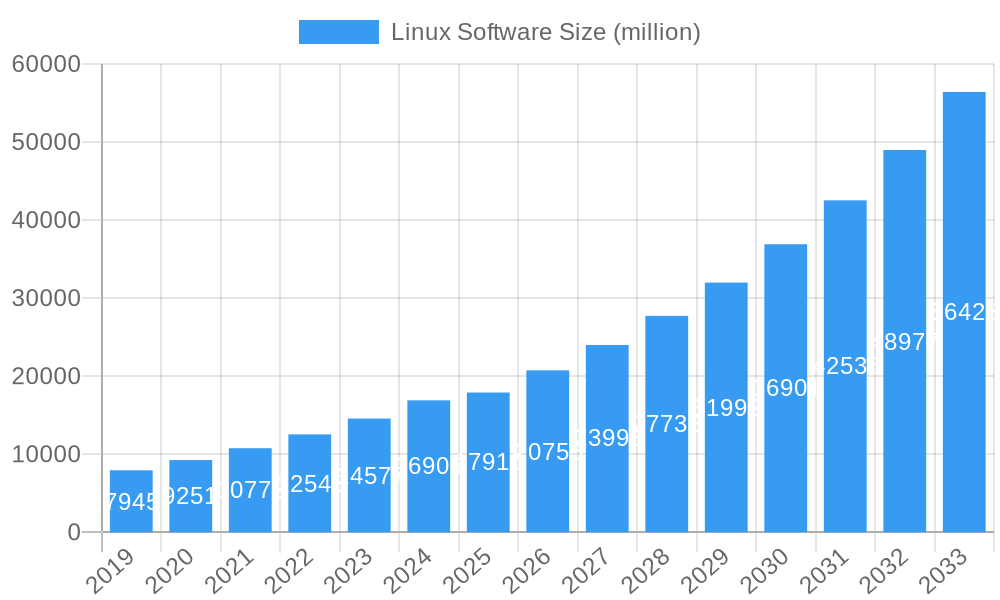

The global Linux Software market is experiencing robust expansion, projected to reach $17910 million by 2025. This impressive growth is underpinned by a CAGR of 15.3% from 2019 to 2033, indicating sustained and dynamic market performance. Key drivers fueling this surge include the escalating demand for open-source solutions across enterprise and government sectors, the increasing adoption of Linux in cloud computing and big data analytics, and its growing presence in the Internet of Things (IoT) ecosystem. The inherent flexibility, cost-effectiveness, and security advantages of Linux software make it a preferred choice for businesses seeking to optimize their IT infrastructure and drive innovation. Emerging trends such as the rise of containerization technologies like Docker and Kubernetes, powered by Linux, and the increasing integration of AI and machine learning with Linux-based platforms, are further accelerating market penetration.

Linux Software Market Size (In Billion)

The Linux Software market's trajectory is further shaped by significant trends in its segmentation. Within applications, both Household and Enterprise segments are showing strong adoption, with Enterprises leading due to critical infrastructure needs and scalability demands. Government adoption is also a substantial contributor, driven by security mandates and cost-efficiency initiatives. In terms of types, while traditional distributions like Debian and Fedora continue to hold significant market share, there's a growing emphasis on specialized or enterprise-grade Linux distributions optimized for specific workloads and cloud environments. Major technology players like Google, Amazon, Microsoft, and Red Hat are actively investing in Linux development and ecosystem expansion, solidifying its position as a foundational technology for modern digital transformation. Despite the overwhelmingly positive outlook, the market may encounter some restraints related to the availability of skilled Linux professionals in certain regions and the initial migration costs for legacy systems, though these are generally outweighed by the long-term benefits and the continuous evolution of support and training resources.

Linux Software Company Market Share

Here is a dynamic, SEO-optimized report description for Linux Software, crafted with high-volume keywords and adhering to all your specifications:

Linux Software Market Structure & Competitive Landscape

This comprehensive analysis delves into the intricate structure and competitive landscape of the global Linux Software market, projecting a market size of over one million dollars for the forecast period. The study meticulously examines market concentration, highlighting the presence of major players like Google, IBM, RedHat, and Oracle, alongside emerging innovators. Key innovation drivers are identified, focusing on the burgeoning demand for cloud-native solutions, containerization technologies, and edge computing. Regulatory impacts are assessed, particularly concerning open-source licensing compliance and data privacy mandates influencing government and enterprise adoption. The report scrutinizes product substitutes, such as proprietary operating systems, and their diminishing market share due to Linux's cost-effectiveness and flexibility. End-user segmentation reveals a significant shift towards enterprise and government sectors, driven by robust security features and scalability. Merger and acquisition (M&A) trends are analyzed, with an estimated xx M&A volumes observed historically, indicating strategic consolidation and expansion within the ecosystem. Concentration ratios are projected to remain moderate, reflecting a healthy competitive environment.

Linux Software Market Trends & Opportunities

The Linux Software market is poised for substantial growth, projected to exceed one million dollars in value over the forecast period. This report provides an in-depth exploration of the critical trends and lucrative opportunities shaping this dynamic sector. We project a Compound Annual Growth Rate (CAGR) of XX%, driven by the pervasive adoption of Linux in cloud infrastructure, big data analytics, and the Internet of Things (IoT). Technological shifts are a primary catalyst, with the increasing prevalence of Kubernetes, Docker, and microservices architectures creating an insatiable demand for robust and adaptable Linux distributions. Consumer preferences are evolving, with a growing inclination towards open-source solutions offering greater control, customization, and cost savings, particularly in household and enterprise segments. Competitive dynamics are intensifying, fostering innovation and driving down costs, making Linux an increasingly attractive alternative to proprietary operating systems. Market penetration rates are expected to reach unprecedented levels, particularly in developing economies where cost-efficiency is paramount. The report meticulously analyzes the interplay of these factors, identifying emerging niches and strategic growth avenues for stakeholders.

Dominant Markets & Segments in Linux Software

This section identifies the dominant regions, countries, and segments within the expansive Linux Software market, projected to reach over one million dollars.

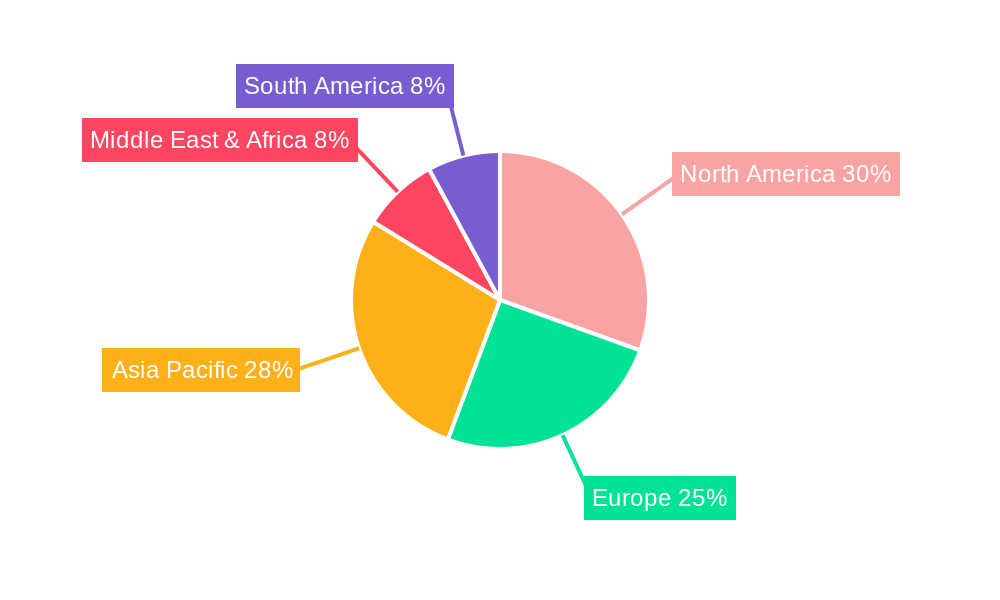

- Leading Regions: North America and Europe currently represent the most significant markets, driven by advanced technological infrastructure, government initiatives promoting open-source adoption, and a high concentration of enterprise users. Asia Pacific is emerging as a rapid growth region, fueled by increasing investments in digital transformation and a burgeoning IT talent pool.

- Dominant Countries: The United States leads in terms of market value and innovation, with a strong presence of key companies like Google, Amazon, and DELL. China and India are exhibiting exceptional growth rates due to their massive populations, expanding digitalization efforts, and government support for open-source technologies.

- Dominant Application Segments:

- Enterprise: This segment commands the largest market share, driven by its critical role in powering data centers, cloud computing, servers, and critical business applications. The demand for high performance, scalability, and security in enterprise environments makes Linux the de facto standard.

- Government: Government adoption is steadily increasing, spurred by mandates for open-source solutions to enhance national cybersecurity, reduce reliance on foreign technology, and promote transparency. Regulations supporting open-source procurement are key growth drivers.

- Household: While a smaller segment, household Linux adoption is growing, particularly among tech-savvy users, developers, and those seeking cost-effective alternatives for personal computing and home servers.

- Others: This encompasses niche applications in embedded systems, telecommunications, automotive, and scientific research, all of which are experiencing significant Linux integration.

- Dominant Type Segments:

- Debian: Renowned for its stability, vast package repository, and strong community support, Debian remains a foundational distribution, widely used in servers and enterprise environments.

- Fedora: As a cutting-edge distribution sponsored by RedHat, Fedora serves as a testing ground for new technologies, influencing enterprise-focused distributions and driving innovation in desktop and developer environments.

- OpenSUSE: Known for its user-friendly interface and robust features, OpenSUSE attracts both desktop users and enterprise deployments, particularly in Europe.

- Others: This category includes a multitude of specialized distributions catering to specific needs, such as Ubuntu (highly popular for desktops and servers), CentOS (historically used for enterprise servers, now moving to alternatives like Rocky Linux and AlmaLinux), and numerous embedded Linux variants.

The dominance in these segments is underpinned by continuous innovation, favorable government policies, and the inherent advantages of Linux in terms of cost, flexibility, and security.

Linux Software Product Analysis

Linux software continues to push the boundaries of technological innovation, offering unparalleled flexibility and performance. Product advancements are centered around enhancing containerization technologies like Docker and Kubernetes, facilitating seamless microservices deployment and scalability. Competitive advantages stem from robust security architectures, extensive customization options, and cost-effectiveness, making distributions like RedHat Enterprise Linux and Ubuntu LTS indispensable for enterprise solutions. The integration of AI and machine learning frameworks onto Linux platforms further solidifies its position as the go-to operating system for cutting-edge research and development.

Key Drivers, Barriers & Challenges in Linux Software

Key Drivers: The Linux Software market is propelled by several significant forces. Technologically, the exponential growth of cloud computing, big data analytics, and the Internet of Things (IoT) creates an insatiable demand for scalable and reliable operating systems. Economically, the cost-effectiveness of Linux, with its open-source nature and minimal licensing fees, makes it highly attractive to businesses of all sizes, particularly small and medium-sized enterprises (SMEs) and startups. Policy-driven factors, such as government initiatives promoting open-source adoption for national security and economic independence, are also crucial.

Barriers & Challenges: Despite its strengths, the market faces challenges. Regulatory hurdles, though often favoring open-source, can sometimes involve complex compliance requirements, especially in highly regulated industries like finance and healthcare. Supply chain issues, while less pronounced for software than hardware, can impact the availability and timely delivery of integrated solutions and specialized support. Competitive pressures from established proprietary operating systems and the constant need for skilled Linux professionals present ongoing challenges.

Growth Drivers in the Linux Software Market

The Linux Software market's growth is significantly driven by technological advancements in cloud computing, artificial intelligence, and the Internet of Things (IoT), creating a demand for robust and scalable operating systems. The inherent cost-effectiveness of Linux, with its open-source model eliminating substantial licensing fees, is a major economic advantage, particularly for startups and SMEs. Furthermore, increasing government mandates and initiatives worldwide encouraging the adoption of open-source software for enhanced national security, reduced vendor lock-in, and digital sovereignty act as powerful policy-driven catalysts.

Challenges Impacting Linux Software Growth

Despite its robust growth, Linux Software faces several impediments. Regulatory complexities, particularly in industries with stringent compliance requirements, can pose adoption barriers. Supply chain disruptions, though less direct for software, can impact the integration of Linux into broader hardware and service ecosystems. Intense competitive pressures from well-entrenched proprietary operating systems and the continuous need to develop and maintain a highly skilled workforce adept at managing and supporting Linux environments present ongoing challenges, potentially impacting the pace of market expansion.

Key Players Shaping the Linux Software Market

- Amazon

- IBM

- Oracle

- Novell

- RedHat

- DELL

- Samsung

- Microsoft

Significant Linux Software Industry Milestones

- 1991: Linus Torvalds announces the initial release of the Linux kernel, laying the foundation for the open-source operating system.

- 1994: Red Hat releases its first commercial Linux distribution, marking a pivotal step towards enterprise adoption.

- 2001: Novell acquires SUSE Linux, strengthening its position in the enterprise Linux market.

- 2003: The creation of the Fedora Project, sponsored by Red Hat, fosters innovation and serves as a testing ground for new technologies.

- 2007: Google announces its acquisition of Android, which is built upon the Linux kernel, significantly expanding its reach into the mobile device market.

- 2014: Docker revolutionizes application deployment with its containerization technology, heavily reliant on Linux kernel features.

- 2015: The rapid growth of Kubernetes, an open-source system for automating deployment, scaling, and management of containerized applications, further solidifies Linux's dominance in cloud-native environments.

- 2017: Amazon Web Services (AWS) launches Amazon Linux 2, a cloud-optimized operating system designed for its platform.

- 2020: IBM completes its acquisition of Red Hat, signaling a massive strategic investment in open-source and hybrid cloud solutions.

- 2022: Microsoft announces enhanced support and integration for the Windows Subsystem for Linux (WSL), bridging the gap between Windows and Linux development environments.

Future Outlook for Linux Software Market

The future of the Linux Software market is exceptionally promising, with growth catalysts including the relentless expansion of cloud infrastructure, the burgeoning Internet of Things (IoT) ecosystem, and the increasing adoption of artificial intelligence and machine learning. Strategic opportunities abound in specialized embedded systems, edge computing solutions, and enhanced cybersecurity offerings. The market's potential is further amplified by government initiatives promoting open-source adoption and the ongoing demand for flexible, cost-effective, and highly customizable operating system solutions across all industry verticals.

Linux Software Segmentation

-

1. Application

- 1.1. Household

- 1.2. Enterprise

- 1.3. Government

- 1.4. Others

-

2. Type

- 2.1. Debian

- 2.2. Fedora

- 2.3. Opensuse

- 2.4. Others

Linux Software Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Linux Software Regional Market Share

Geographic Coverage of Linux Software

Linux Software REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 15.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Linux Software Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Household

- 5.1.2. Enterprise

- 5.1.3. Government

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Debian

- 5.2.2. Fedora

- 5.2.3. Opensuse

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Linux Software Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Household

- 6.1.2. Enterprise

- 6.1.3. Government

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Debian

- 6.2.2. Fedora

- 6.2.3. Opensuse

- 6.2.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Linux Software Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Household

- 7.1.2. Enterprise

- 7.1.3. Government

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Debian

- 7.2.2. Fedora

- 7.2.3. Opensuse

- 7.2.4. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Linux Software Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Household

- 8.1.2. Enterprise

- 8.1.3. Government

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Debian

- 8.2.2. Fedora

- 8.2.3. Opensuse

- 8.2.4. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Linux Software Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Household

- 9.1.2. Enterprise

- 9.1.3. Government

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Debian

- 9.2.2. Fedora

- 9.2.3. Opensuse

- 9.2.4. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Linux Software Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Household

- 10.1.2. Enterprise

- 10.1.3. Government

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Debian

- 10.2.2. Fedora

- 10.2.3. Opensuse

- 10.2.4. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Google

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Twitter

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Facebook

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Amazon

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 IBM

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Oracle

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Novell

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 RedHat

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 DELL

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Samsung

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Microsoft

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.1 Google

List of Figures

- Figure 1: Global Linux Software Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Linux Software Revenue (million), by Application 2025 & 2033

- Figure 3: North America Linux Software Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Linux Software Revenue (million), by Type 2025 & 2033

- Figure 5: North America Linux Software Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Linux Software Revenue (million), by Country 2025 & 2033

- Figure 7: North America Linux Software Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Linux Software Revenue (million), by Application 2025 & 2033

- Figure 9: South America Linux Software Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Linux Software Revenue (million), by Type 2025 & 2033

- Figure 11: South America Linux Software Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Linux Software Revenue (million), by Country 2025 & 2033

- Figure 13: South America Linux Software Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Linux Software Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Linux Software Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Linux Software Revenue (million), by Type 2025 & 2033

- Figure 17: Europe Linux Software Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Linux Software Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Linux Software Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Linux Software Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Linux Software Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Linux Software Revenue (million), by Type 2025 & 2033

- Figure 23: Middle East & Africa Linux Software Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Linux Software Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Linux Software Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Linux Software Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Linux Software Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Linux Software Revenue (million), by Type 2025 & 2033

- Figure 29: Asia Pacific Linux Software Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Linux Software Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Linux Software Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Linux Software Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Linux Software Revenue million Forecast, by Type 2020 & 2033

- Table 3: Global Linux Software Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Linux Software Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Linux Software Revenue million Forecast, by Type 2020 & 2033

- Table 6: Global Linux Software Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Linux Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Linux Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Linux Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Linux Software Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Linux Software Revenue million Forecast, by Type 2020 & 2033

- Table 12: Global Linux Software Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Linux Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Linux Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Linux Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Linux Software Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Linux Software Revenue million Forecast, by Type 2020 & 2033

- Table 18: Global Linux Software Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Linux Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Linux Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Linux Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Linux Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Linux Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Linux Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Linux Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Linux Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Linux Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Linux Software Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Linux Software Revenue million Forecast, by Type 2020 & 2033

- Table 30: Global Linux Software Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Linux Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Linux Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Linux Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Linux Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Linux Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Linux Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Linux Software Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Linux Software Revenue million Forecast, by Type 2020 & 2033

- Table 39: Global Linux Software Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Linux Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Linux Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Linux Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Linux Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Linux Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Linux Software Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Linux Software Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Linux Software?

The projected CAGR is approximately 15.3%.

2. Which companies are prominent players in the Linux Software?

Key companies in the market include Google, Twitter, Facebook, Amazon, IBM, Oracle, Novell, RedHat, DELL, Samsung, Microsoft.

3. What are the main segments of the Linux Software?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 17910 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Linux Software," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Linux Software report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Linux Software?

To stay informed about further developments, trends, and reports in the Linux Software, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence