Key Insights

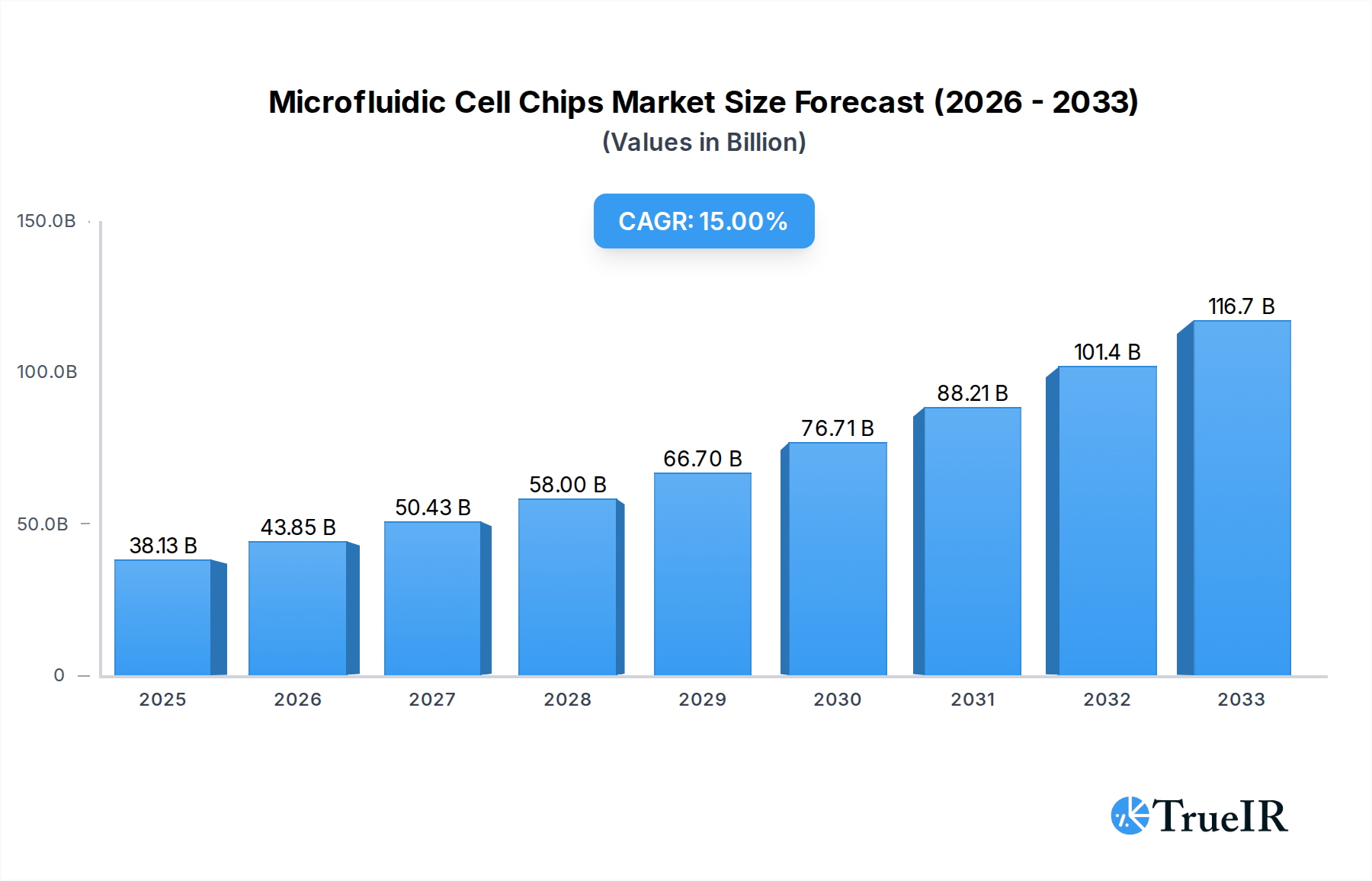

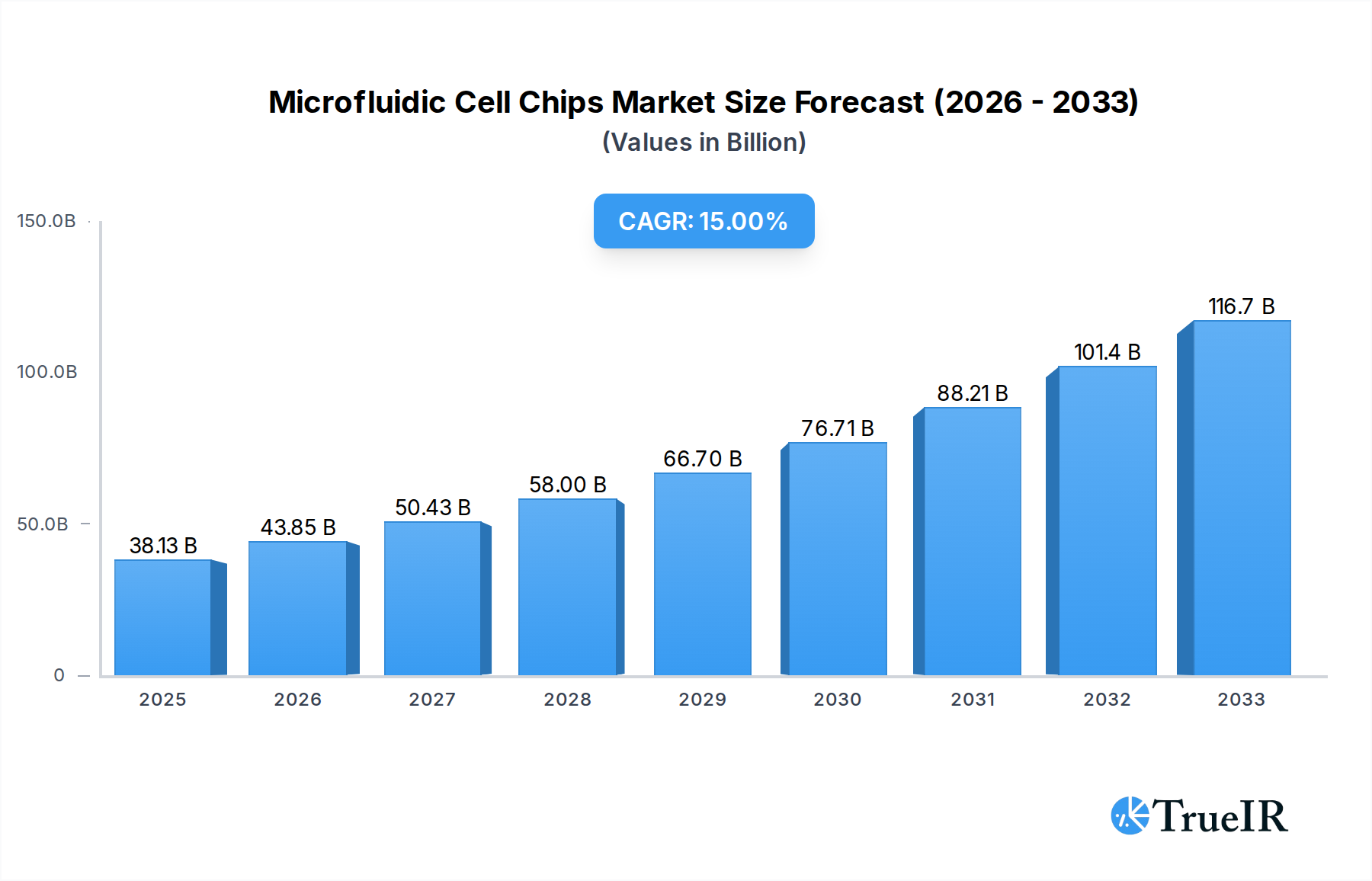

The global Microfluidic Cell Chips market is poised for substantial expansion, projected to reach an estimated $38.13 billion by 2025. This remarkable growth is propelled by a CAGR of 15% over the forecast period, indicating a dynamic and rapidly evolving industry. The increasing adoption of microfluidic cell chips in pharmaceutical research and development, particularly for drug discovery, toxicity testing, and personalized medicine, serves as a primary market driver. These chips enable precise manipulation of small fluid volumes, facilitating high-throughput screening and the creation of more physiologically relevant in-vitro models, thereby reducing the need for animal testing and accelerating the drug development lifecycle. Furthermore, the burgeoning diagnostics sector, driven by the demand for rapid, sensitive, and point-of-care testing solutions for various diseases, is significantly contributing to market growth. The inherent advantages of microfluidics, such as reduced reagent consumption, faster analysis times, and miniaturization, make them ideal for a wide array of diagnostic applications, from infectious disease detection to cancer biomarker analysis.

Microfluidic Cell Chips Market Size (In Billion)

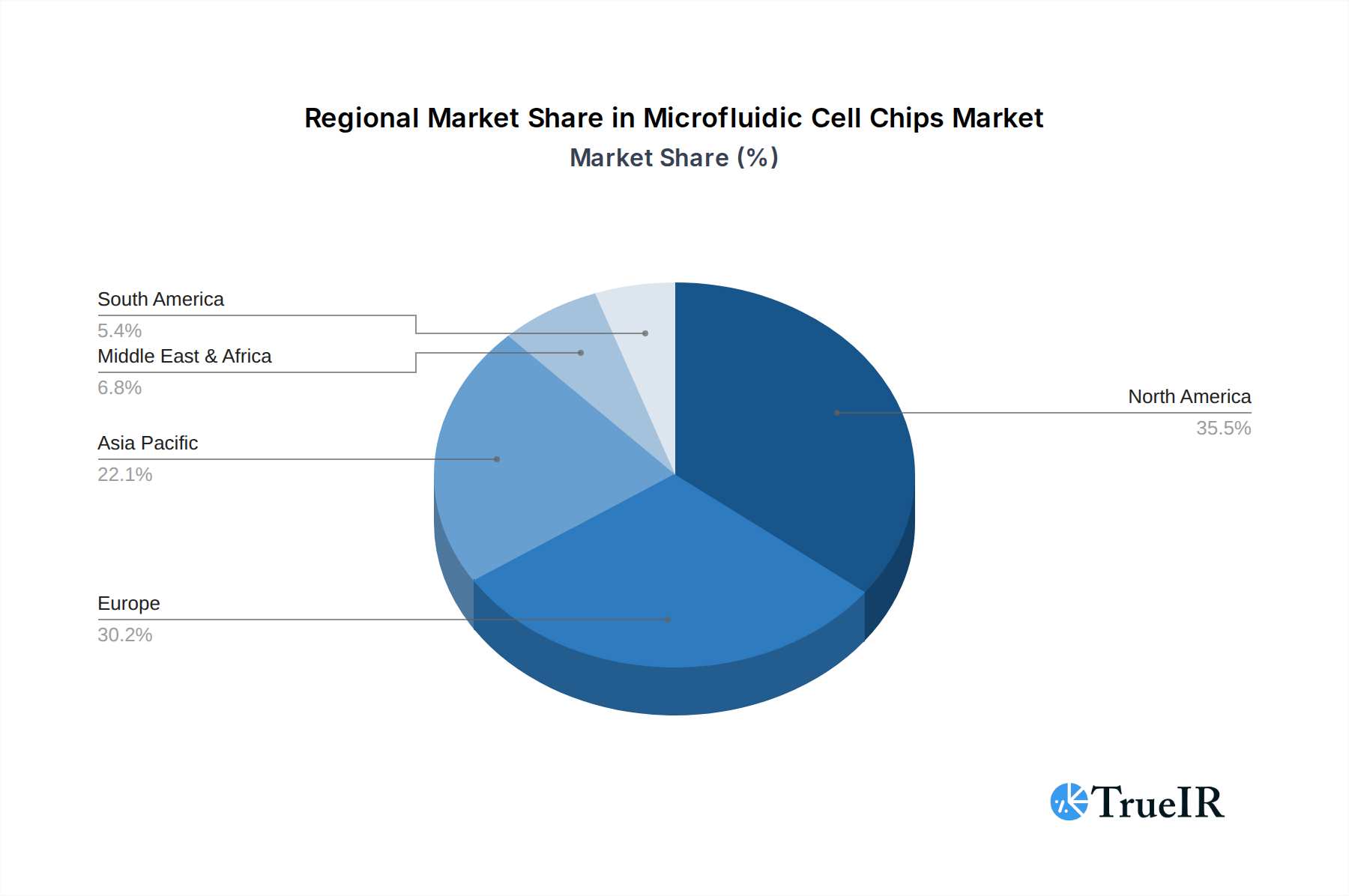

The market is segmented into various applications, including Pharmaceutical, Diagnostic, and Drug Delivery, with polymers, ceramics, and semi-conductors forming the key material types. The pharmaceutical segment is expected to dominate due to the high R&D investments in this sector. Emerging trends such as the integration of artificial intelligence and machine learning with microfluidic platforms for advanced data analysis and predictive modeling, alongside the development of organ-on-a-chip technologies, are expected to further fuel market expansion. However, the market faces certain restraints, including the high initial investment costs associated with setting up microfluidic research facilities and the need for specialized expertise for operation and maintenance. Despite these challenges, the continuous innovation in material science and fabrication techniques, coupled with strategic collaborations among leading companies like Agilent, Fluidigm Corporation, Danaher, and PerkinElmer, is expected to overcome these hurdles and ensure sustained market growth. Geographically, North America and Europe are anticipated to hold significant market shares, driven by robust healthcare infrastructure and substantial R&D funding, with the Asia Pacific region emerging as a key growth hub due to its expanding pharmaceutical industry and increasing investments in biotechnology.

Microfluidic Cell Chips Company Market Share

This in-depth market report offers a definitive analysis of the global Microfluidic Cell Chips market, providing critical insights and actionable intelligence for stakeholders. Covering a study period from 2019 to 2033, with a base and estimated year of 2025, the report delves into the intricate dynamics that will shape this rapidly evolving sector. Leveraging high-volume keywords, this SEO-optimized report is designed to enhance search rankings and engage a broad audience of industry professionals, researchers, and investors.

Microfluidic Cell Chips Market Structure & Competitive Landscape

The global Microfluidic Cell Chips market exhibits a moderately concentrated structure, with a significant portion of the market share held by a select group of established players. Innovation serves as a primary driver, fueled by continuous research and development in miniaturization, high-throughput screening, and cell-based assays. Regulatory impacts, while present, are largely supportive of technological advancement and market expansion in the pharmaceutical and diagnostic sectors. Product substitutes, such as traditional cell culture plates and high-throughput screening platforms, exist but are increasingly being outpaced by the efficiency and precision offered by microfluidic solutions.

End-user segmentation reveals a strong reliance on the pharmaceutical and diagnostic industries, with drug delivery applications also demonstrating substantial growth potential. Mergers and acquisitions (M&A) have been a notable trend, consolidating market expertise and expanding product portfolios. Historical M&A volumes in the past five years are estimated to be in the hundreds of billions. Key industry developments are consistently driving market growth and increasing the competitive intensity among market participants.

- Market Concentration: Moderate, with key players holding significant market share.

- Innovation Drivers: Miniaturization, high-throughput screening, advanced cell assays.

- Regulatory Impacts: Supportive of technological adoption in pharmaceuticals and diagnostics.

- Product Substitutes: Traditional cell culture plates, existing HTS platforms.

- End-User Segmentation: Pharmaceutical, Diagnostic, Drug Delivery.

- M&A Trends: Active, leading to market consolidation and expanded offerings.

Microfluidic Cell Chips Market Trends & Opportunities

The Microfluidic Cell Chips market is experiencing robust growth, projected to expand significantly throughout the forecast period (2025–2033). The estimated market size in 2025 is in the hundreds of billions of dollars, with a compound annual growth rate (CAGR) expected to be in the double digits. This expansion is underpinned by a confluence of technological advancements, evolving consumer preferences, and dynamic competitive landscapes. Technological shifts are at the forefront, with continuous innovation in chip design, materials, and integration capabilities enabling more sophisticated and precise cellular analysis. The advent of organ-on-a-chip technology, powered by advanced microfluidic cell chips, is revolutionizing preclinical drug testing and disease modeling, offering more physiologically relevant insights than traditional 2D cell cultures.

Consumer preferences are increasingly leaning towards high-throughput, cost-effective, and data-rich solutions, directly benefiting the microfluidic cell chip sector. Researchers and pharmaceutical companies are actively seeking methods to accelerate drug discovery and development timelines, reduce animal testing, and improve the accuracy of diagnostic tests. Microfluidic cell chips directly address these needs by enabling miniaturized experiments, reducing reagent consumption, and facilitating the automation of complex biological assays. The market penetration rate for advanced microfluidic cell chip applications is projected to climb steadily as awareness and adoption grow across various research and clinical settings.

Competitive dynamics are characterized by intense innovation and strategic collaborations. Companies are investing heavily in R&D to develop novel chip designs, integrate advanced sensing technologies, and create integrated platforms that offer end-to-end solutions. The increasing demand for personalized medicine and companion diagnostics further fuels the need for microfluidic platforms capable of analyzing individual patient cells with high specificity. Opportunities abound in the development of single-cell analysis platforms, advanced drug screening systems, and point-of-care diagnostic devices. The market is ripe for players who can offer scalable, user-friendly, and cost-effective microfluidic solutions that address the specific pain points of the pharmaceutical, biotechnology, and academic research sectors. The sheer volume of research and development activities globally, estimated to be in the billions of dollars annually, directly translates into a sustained demand for sophisticated microfluidic tools.

Dominant Markets & Segments in Microfluidic Cell Chips

North America is identified as the dominant region in the Microfluidic Cell Chips market, driven by substantial investments in pharmaceutical research and development, a well-established biotechnology ecosystem, and a high adoption rate of cutting-edge technologies. Within North America, the United States leads in market dominance due to the presence of leading research institutions, major pharmaceutical companies, and a robust venture capital landscape that fuels innovation in the life sciences. The pharmaceutical application segment commands the largest market share, owing to the critical role microfluidic cell chips play in drug discovery, preclinical testing, toxicology studies, and personalized medicine development.

Leading Region: North America

- Key Growth Drivers: Extensive R&D funding in pharmaceuticals and biotechnology, presence of leading academic and research institutions, advanced healthcare infrastructure, and significant government support for life science innovation.

- Market Dominance Analysis: The US market is a powerhouse due to its high concentration of pharmaceutical giants, prolific drug discovery pipelines, and a strong focus on advanced diagnostics. The availability of billions in research grants and private investments further propels the adoption of microfluidic technologies.

Dominant Application Segment: Pharmaceutical

- Key Growth Drivers: Need for accelerated drug discovery and development, reduced reliance on animal models, enhanced precision in compound screening, and the growing demand for in-vitro diagnostics for patient stratification.

- Market Dominance Analysis: Microfluidic cell chips enable researchers to perform complex cellular assays with unprecedented efficiency and throughput. The ability to simulate in-vivo environments with organ-on-a-chip models significantly reduces the time and cost associated with traditional drug testing, making it indispensable for pharmaceutical pipelines valued in the billions.

Dominant Type Segment: Polymers

- Key Growth Drivers: Cost-effectiveness, ease of fabrication (e.g., injection molding, 3D printing), biocompatibility, and versatility in chip design.

- Market Dominance Analysis: Polymer-based microfluidic chips, such as those made from PDMS (polydimethylsiloxane) and thermoplastics, offer a balance of performance and affordability. Their widespread use in research and early-stage development, coupled with the ability for rapid prototyping and mass production, solidifies their dominance in a market where billions are invested in research consumables.

The diagnostic segment is also a significant growth area, driven by the demand for faster, more sensitive, and portable diagnostic devices, particularly for infectious diseases, cancer, and genetic testing. Drug delivery applications are emerging, focusing on controlled release mechanisms and personalized drug formulations. While ceramics and semiconductors are utilized for specialized high-performance applications, polymers currently dominate the market due to their manufacturing advantages and cost-effectiveness, particularly in high-volume research applications.

Microfluidic Cell Chips Product Analysis

Product innovations in Microfluidic Cell Chips are centered around enhanced cell manipulation capabilities, integrated sensing technologies, and multiplexed assay formats. These advancements translate into superior performance for applications such as single-cell analysis, high-throughput drug screening, and the creation of complex in-vitro models like organoids and organ-on-a-chip systems. Competitive advantages are gained through improved assay sensitivity, reduced reagent consumption, faster experimental turnaround times, and the ability to generate more physiologically relevant data. The technological sophistication allows for the precise control of cellular environments, mimicking in-vivo conditions with billions of cellular interactions being monitored.

Key Drivers, Barriers & Challenges in Microfluidic Cell Chips

Key Drivers: The Microfluidic Cell Chips market is propelled by a confluence of factors, including the relentless pursuit of precision and efficiency in life science research and diagnostics, the growing imperative for accelerated drug discovery timelines, and the increasing demand for cost-effective alternatives to traditional laboratory methods. Technological advancements in miniaturization and automation are continuously expanding the capabilities of these chips.

- Technological Advancements: Miniaturization, automation, and integration of sensors.

- Economic Factors: Reduced reagent costs, faster experimental cycles, and lower operational expenses.

- Policy-Driven Factors: Government initiatives supporting R&D in life sciences and personalized medicine.

Key Barriers & Challenges: Despite its promising growth, the market faces several restraints. These include the high initial investment required for advanced microfluidic systems, the need for specialized technical expertise for operation and maintenance, and the ongoing challenges in standardizing protocols across different platforms. Regulatory hurdles for new diagnostic applications can also impact market entry.

- Supply Chain Issues: Potential bottlenecks in specialized material sourcing and fabrication.

- Regulatory Hurdles: Evolving compliance requirements for diagnostic and therapeutic applications.

- Competitive Pressures: Intense competition among established and emerging players driving down margins.

Growth Drivers in the Microfluidic Cell Chips Market

Key growth drivers for the Microfluidic Cell Chips market are multifaceted. Technologically, the ongoing miniaturization and integration of advanced functionalities like sensing and imaging are opening new application frontiers. Economically, the significant cost savings in reagents and experimental time, coupled with the ability to perform high-throughput screening with minimal sample volume, make microfluidics an attractive proposition, especially for research projects valued in the billions. Regulatory shifts favoring reduced animal testing and promoting faster drug approval processes further catalyze adoption. The increasing investment in personalized medicine and companion diagnostics, estimated in the hundreds of billions, necessitates the precise cellular analysis capabilities offered by microfluidic chips.

Challenges Impacting Microfluidic Cell Chips Growth

Several challenges can impact the growth trajectory of the Microfluidic Cell Chips market. Regulatory complexities for novel diagnostic and therapeutic applications can lead to lengthy approval processes, despite billions invested in R&D. Supply chain issues related to the consistent availability of specialized materials and components for high-precision chip fabrication can create production bottlenecks. Intense competitive pressures from both established manufacturers and innovative startups necessitate continuous investment in R&D to maintain a competitive edge, potentially impacting profitability margins that can run into the billions. Furthermore, the need for specialized expertise in operating and interpreting data from advanced microfluidic systems can pose a barrier to widespread adoption in some research settings.

Key Players Shaping the Microfluidic Cell Chips Market

- Agilent

- Fluidigm Corporation

- Micralyne, Inc.

- Becton Dickinson

- Danaher

- PerkinElmer

- Bio-Rad Laboratories

- Dolomite

- 908 Devices

- MicroLIQUID

- MicruX Technologies

- Micronit

- Fluigent

Significant Microfluidic Cell Chips Industry Milestones

- 2019: Introduction of advanced organ-on-a-chip systems with enhanced vascularization capabilities.

- 2020: Development of high-throughput microfluidic platforms for rapid COVID-19 diagnostic assay development.

- 2021: Launch of novel microfluidic chips enabling sophisticated single-cell multi-omics analysis.

- 2022: Significant advancements in AI-driven microfluidic control systems for autonomous experiments.

- 2023: Increased commercialization of microfluidic-based liquid biopsy platforms for early cancer detection.

- Early 2024: Introduction of more affordable and user-friendly microfluidic devices for broader academic access.

Future Outlook for Microfluidic Cell Chips Market

The future outlook for the Microfluidic Cell Chips market is exceptionally bright, driven by continued innovation and expanding applications. Strategic opportunities lie in the further development of integrated lab-on-a-chip systems, the expansion of organ-on-a-chip technologies for more complex disease modeling and drug testing, and the increasing demand for point-of-care diagnostic devices. The market potential is immense, fueled by a global push for more efficient, personalized, and cost-effective healthcare solutions, with research and development investments in the billions consistently driving this innovation. The growing emphasis on precision medicine and the need for granular cellular insights will ensure sustained demand for sophisticated microfluidic cell chip technologies.

Microfluidic Cell Chips Segmentation

-

1. Application

- 1.1. Pharmaceutical

- 1.2. Diagnostic

- 1.3. Drug Deliver

-

2. Type

- 2.1. Polymers

- 2.2. Ceramics

- 2.3. Semi-conductors

Microfluidic Cell Chips Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Microfluidic Cell Chips Regional Market Share

Geographic Coverage of Microfluidic Cell Chips

Microfluidic Cell Chips REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 15% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Microfluidic Cell Chips Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Pharmaceutical

- 5.1.2. Diagnostic

- 5.1.3. Drug Deliver

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Polymers

- 5.2.2. Ceramics

- 5.2.3. Semi-conductors

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Microfluidic Cell Chips Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Pharmaceutical

- 6.1.2. Diagnostic

- 6.1.3. Drug Deliver

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Polymers

- 6.2.2. Ceramics

- 6.2.3. Semi-conductors

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Microfluidic Cell Chips Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Pharmaceutical

- 7.1.2. Diagnostic

- 7.1.3. Drug Deliver

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Polymers

- 7.2.2. Ceramics

- 7.2.3. Semi-conductors

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Microfluidic Cell Chips Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Pharmaceutical

- 8.1.2. Diagnostic

- 8.1.3. Drug Deliver

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Polymers

- 8.2.2. Ceramics

- 8.2.3. Semi-conductors

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Microfluidic Cell Chips Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Pharmaceutical

- 9.1.2. Diagnostic

- 9.1.3. Drug Deliver

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Polymers

- 9.2.2. Ceramics

- 9.2.3. Semi-conductors

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Microfluidic Cell Chips Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Pharmaceutical

- 10.1.2. Diagnostic

- 10.1.3. Drug Deliver

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Polymers

- 10.2.2. Ceramics

- 10.2.3. Semi-conductors

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Agilent

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Fluidigm Corporation

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Micralyne Inc

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Becton Dickinson

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Danaher

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 PerkinElmer

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Bio-Rad Laboratories

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Dolomite

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 908 Devices

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 MicroLIQUID

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 MicruX Technologies

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Micronit

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Fluigent

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.1 Agilent

List of Figures

- Figure 1: Global Microfluidic Cell Chips Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Microfluidic Cell Chips Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Microfluidic Cell Chips Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Microfluidic Cell Chips Revenue (undefined), by Type 2025 & 2033

- Figure 5: North America Microfluidic Cell Chips Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Microfluidic Cell Chips Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Microfluidic Cell Chips Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Microfluidic Cell Chips Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Microfluidic Cell Chips Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Microfluidic Cell Chips Revenue (undefined), by Type 2025 & 2033

- Figure 11: South America Microfluidic Cell Chips Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Microfluidic Cell Chips Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Microfluidic Cell Chips Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Microfluidic Cell Chips Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Microfluidic Cell Chips Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Microfluidic Cell Chips Revenue (undefined), by Type 2025 & 2033

- Figure 17: Europe Microfluidic Cell Chips Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Microfluidic Cell Chips Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Microfluidic Cell Chips Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Microfluidic Cell Chips Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Microfluidic Cell Chips Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Microfluidic Cell Chips Revenue (undefined), by Type 2025 & 2033

- Figure 23: Middle East & Africa Microfluidic Cell Chips Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Microfluidic Cell Chips Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Microfluidic Cell Chips Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Microfluidic Cell Chips Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Microfluidic Cell Chips Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Microfluidic Cell Chips Revenue (undefined), by Type 2025 & 2033

- Figure 29: Asia Pacific Microfluidic Cell Chips Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Microfluidic Cell Chips Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Microfluidic Cell Chips Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Microfluidic Cell Chips Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Microfluidic Cell Chips Revenue undefined Forecast, by Type 2020 & 2033

- Table 3: Global Microfluidic Cell Chips Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Microfluidic Cell Chips Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Microfluidic Cell Chips Revenue undefined Forecast, by Type 2020 & 2033

- Table 6: Global Microfluidic Cell Chips Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Microfluidic Cell Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Microfluidic Cell Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Microfluidic Cell Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Microfluidic Cell Chips Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Microfluidic Cell Chips Revenue undefined Forecast, by Type 2020 & 2033

- Table 12: Global Microfluidic Cell Chips Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Microfluidic Cell Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Microfluidic Cell Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Microfluidic Cell Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Microfluidic Cell Chips Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Microfluidic Cell Chips Revenue undefined Forecast, by Type 2020 & 2033

- Table 18: Global Microfluidic Cell Chips Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Microfluidic Cell Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Microfluidic Cell Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Microfluidic Cell Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Microfluidic Cell Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Microfluidic Cell Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Microfluidic Cell Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Microfluidic Cell Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Microfluidic Cell Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Microfluidic Cell Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Microfluidic Cell Chips Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Microfluidic Cell Chips Revenue undefined Forecast, by Type 2020 & 2033

- Table 30: Global Microfluidic Cell Chips Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Microfluidic Cell Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Microfluidic Cell Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Microfluidic Cell Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Microfluidic Cell Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Microfluidic Cell Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Microfluidic Cell Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Microfluidic Cell Chips Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Microfluidic Cell Chips Revenue undefined Forecast, by Type 2020 & 2033

- Table 39: Global Microfluidic Cell Chips Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Microfluidic Cell Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Microfluidic Cell Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Microfluidic Cell Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Microfluidic Cell Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Microfluidic Cell Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Microfluidic Cell Chips Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Microfluidic Cell Chips Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Microfluidic Cell Chips?

The projected CAGR is approximately 15%.

2. Which companies are prominent players in the Microfluidic Cell Chips?

Key companies in the market include Agilent, Fluidigm Corporation, Micralyne, Inc, Becton Dickinson, Danaher, PerkinElmer, Bio-Rad Laboratories, Dolomite, 908 Devices, MicroLIQUID, MicruX Technologies, Micronit, Fluigent.

3. What are the main segments of the Microfluidic Cell Chips?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Microfluidic Cell Chips," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Microfluidic Cell Chips report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Microfluidic Cell Chips?

To stay informed about further developments, trends, and reports in the Microfluidic Cell Chips, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence