Key Insights

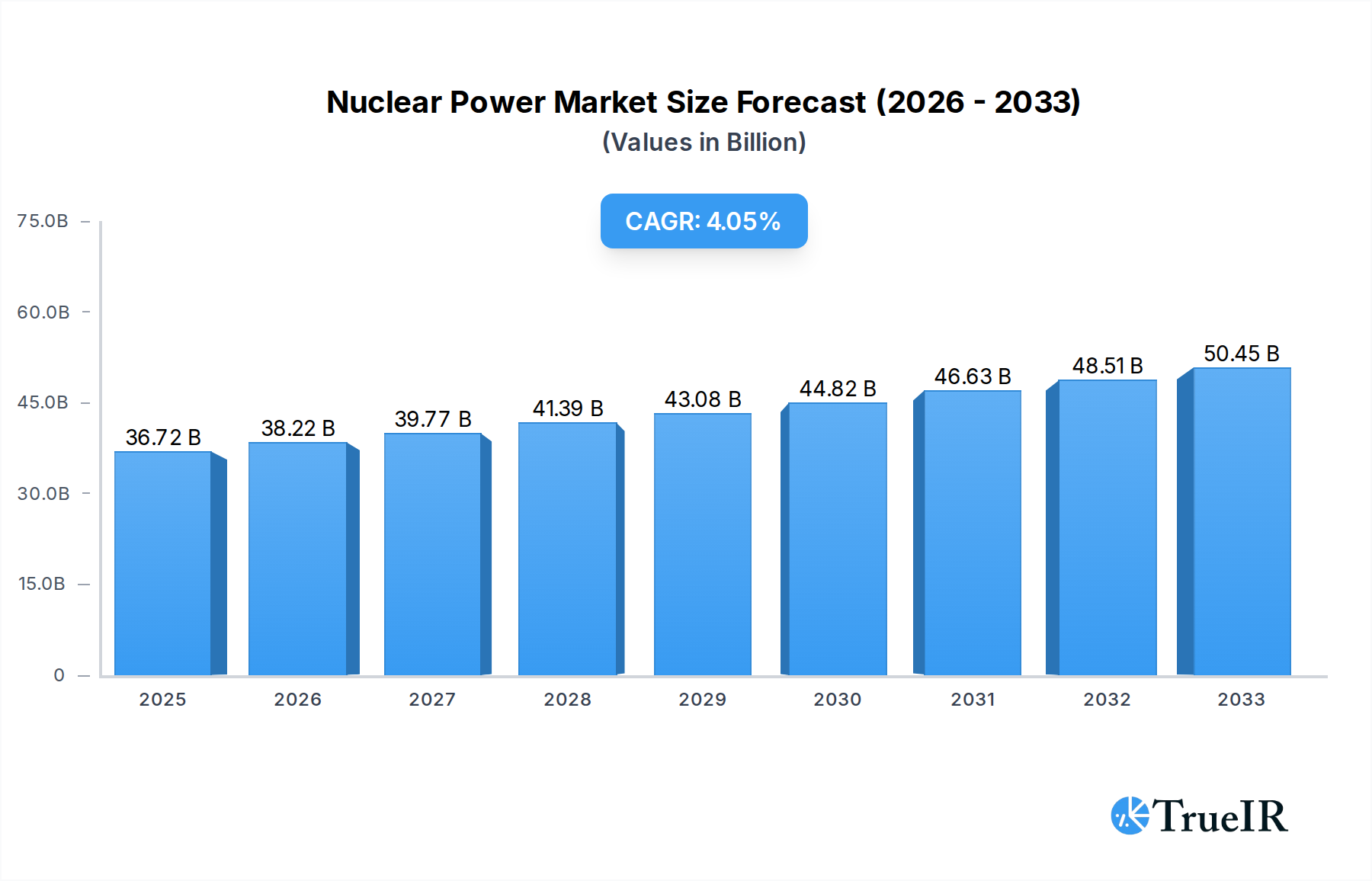

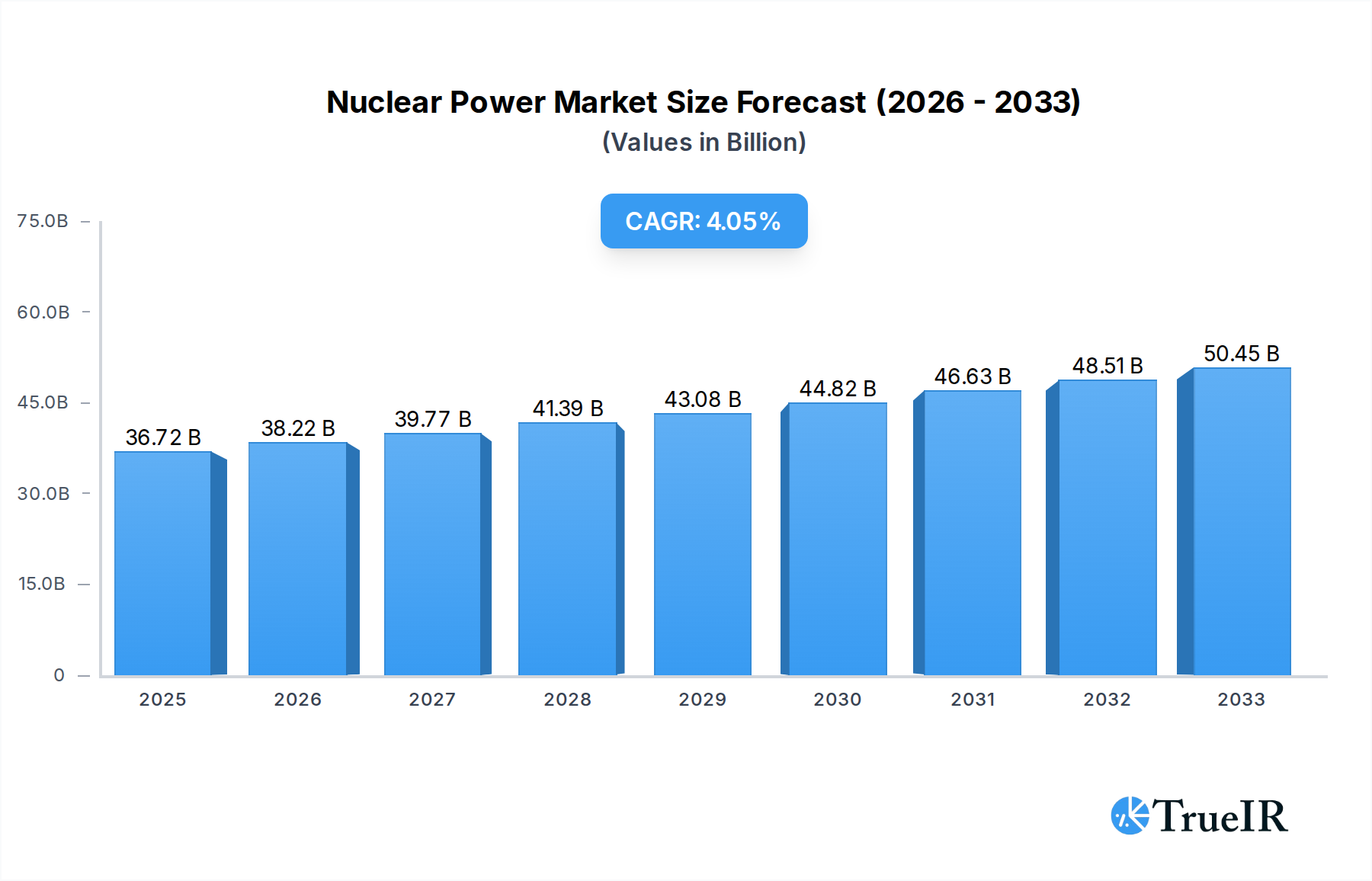

The global Nuclear Power market is poised for robust expansion, projected to reach an estimated $36.72 billion in 2025 and grow at a Compound Annual Growth Rate (CAGR) of 4.1% through 2033. This significant growth is underpinned by a confluence of critical drivers, primarily the escalating global demand for reliable and low-carbon electricity to combat climate change. Governments worldwide are increasingly recognizing nuclear energy as a vital component of their clean energy strategies, offering baseload power capacity that complements intermittent renewable sources like solar and wind. Furthermore, advancements in reactor technology, including small modular reactors (SMRs), are enhancing safety, efficiency, and cost-effectiveness, making nuclear power a more attractive investment. The ongoing need for energy security and diversification, especially in light of geopolitical uncertainties, is also fueling the adoption of nuclear power solutions across various nations.

Nuclear Power Market Size (In Billion)

The market's segmentation reveals key areas of demand. The Electric Power Generation segment dominates, reflecting the primary role of nuclear energy in national power grids. The Industrial sector also presents substantial opportunities, with potential applications in process heat and industrial power. Medical applications, though smaller, are growing due to the increasing use of radioisotopes. The market is diversified by reactor types, with Pressurized Water Reactors (PWRs) holding the largest share due to their established track record and widespread deployment. However, advancements in Boiler Water Reactors (BWRs) and the emerging potential of Gas Cooled Reactors (GCRs) and novel designs are shaping future market dynamics. Major industry players like Westinghouse Electric Company, Orano, and China National Nuclear Cooperation (CNNC) are at the forefront of innovation and deployment, driving market trends and addressing challenges such as waste management and public perception.

Nuclear Power Company Market Share

Nuclear Power Market Report: Powering the Future of Global Energy

This comprehensive nuclear power market report provides an in-depth analysis of the global landscape, encompassing electric power generation, industrial applications, medical uses, and food & agriculture advancements. Dive into the evolving dynamics of Pressurized Water Reactor (PWR), Boiler Water Reactor (BWR), Pressurized Heavy Water Reactor (PHWR), and Gas Cooled Reactor (GCR) technologies. With a robust study period from 2019 to 2033, this report offers unparalleled insights into market trends, opportunities, and the competitive strategies of industry leaders like Westinghouse Electric Company, Orano, and GE Hitachi. Understand the pivotal role of nuclear energy in achieving global decarbonization goals and securing a sustainable energy future.

Nuclear Power Market Structure & Competitive Landscape

The global nuclear power market exhibits a moderately concentrated structure, driven by substantial capital requirements, complex regulatory frameworks, and the need for specialized technological expertise. Key players like Westinghouse Electric Company, Orano, and China National Nuclear Cooperation (CNNC) hold significant market shares, particularly in reactor construction and fuel cycle services. Innovation is a critical driver, with ongoing research and development focused on enhancing reactor safety, improving fuel efficiency, and exploring advanced reactor designs such as Small Modular Reactors (SMRs). Regulatory impacts are profound, with stringent safety standards and licensing procedures influencing project timelines and costs. Product substitutes, primarily renewable energy sources and fossil fuels, present a competitive challenge, though nuclear power's low-carbon, baseload generation capacity remains a distinct advantage. End-user segmentation reveals a dominant reliance on Electric Power Generation, accounting for an estimated billion dollars in revenue annually, with emerging applications in industrial processes and medical isotopes. Mergers and acquisitions (M&A) activity, while not as voluminous as in other energy sectors, are strategic, focusing on consolidating expertise and expanding geographical reach. For instance, the acquisition of smaller specialized firms by larger conglomerates aims to enhance their integrated service offerings, contributing to a consolidation trend to secure project pipelines and manage risks in a sector where project lifecycles span decades. Concentration ratios are estimated to be in the XX% range for the top five players in key segments like reactor manufacturing.

Nuclear Power Market Trends & Opportunities

The global nuclear power market is poised for significant growth, projected to reach an estimated one trillion dollars by 2033, driven by an escalating demand for clean and reliable energy sources. This expansion is underpinned by a compound annual growth rate (CAGR) of approximately XX% during the forecast period (2025-2033). Technological shifts are central to this trend, with a renewed focus on advanced reactor designs, including Small Modular Reactors (SMRs), which offer greater flexibility, reduced construction times, and enhanced safety features. These innovations are crucial for revitalizing existing nuclear fleets and facilitating new deployments in regions seeking to decarbonize their energy mix. Consumer preferences, increasingly aligned with environmental sustainability and energy security, are creating a favorable environment for nuclear power's low-carbon footprint and its ability to provide stable, baseload electricity, irrespective of weather conditions. This contrasts sharply with the intermittency challenges faced by some renewable energy sources. Competitive dynamics are evolving, with established players like GE Hitachi and Mitsubishi Heavy Industries investing heavily in research and development to maintain their technological edge. Simultaneously, emerging market players, particularly from Asia, are rapidly increasing their share, fueled by government support and ambitious energy targets. Opportunities abound in the lifecycle management of nuclear power plants, including decommissioning, waste management, and fuel fabrication, creating a robust ecosystem of related industries. The increasing penetration of electric vehicles and the electrification of industrial processes further bolster the demand for a consistent and abundant electricity supply, a domain where nuclear power excels. Strategic partnerships and collaborative ventures are becoming more prevalent as companies seek to share risks, pool expertise, and navigate the complex regulatory landscapes in different jurisdictions, thereby accelerating the adoption of nuclear technologies globally.

Dominant Markets & Segments in Nuclear Power

The Electric Power Generation segment unequivocally dominates the nuclear power market, representing an estimated one trillion dollars in global revenue. This dominance is driven by nations and regions prioritizing a stable, low-carbon energy supply to meet soaring electricity demands.

Leading Region & Country:

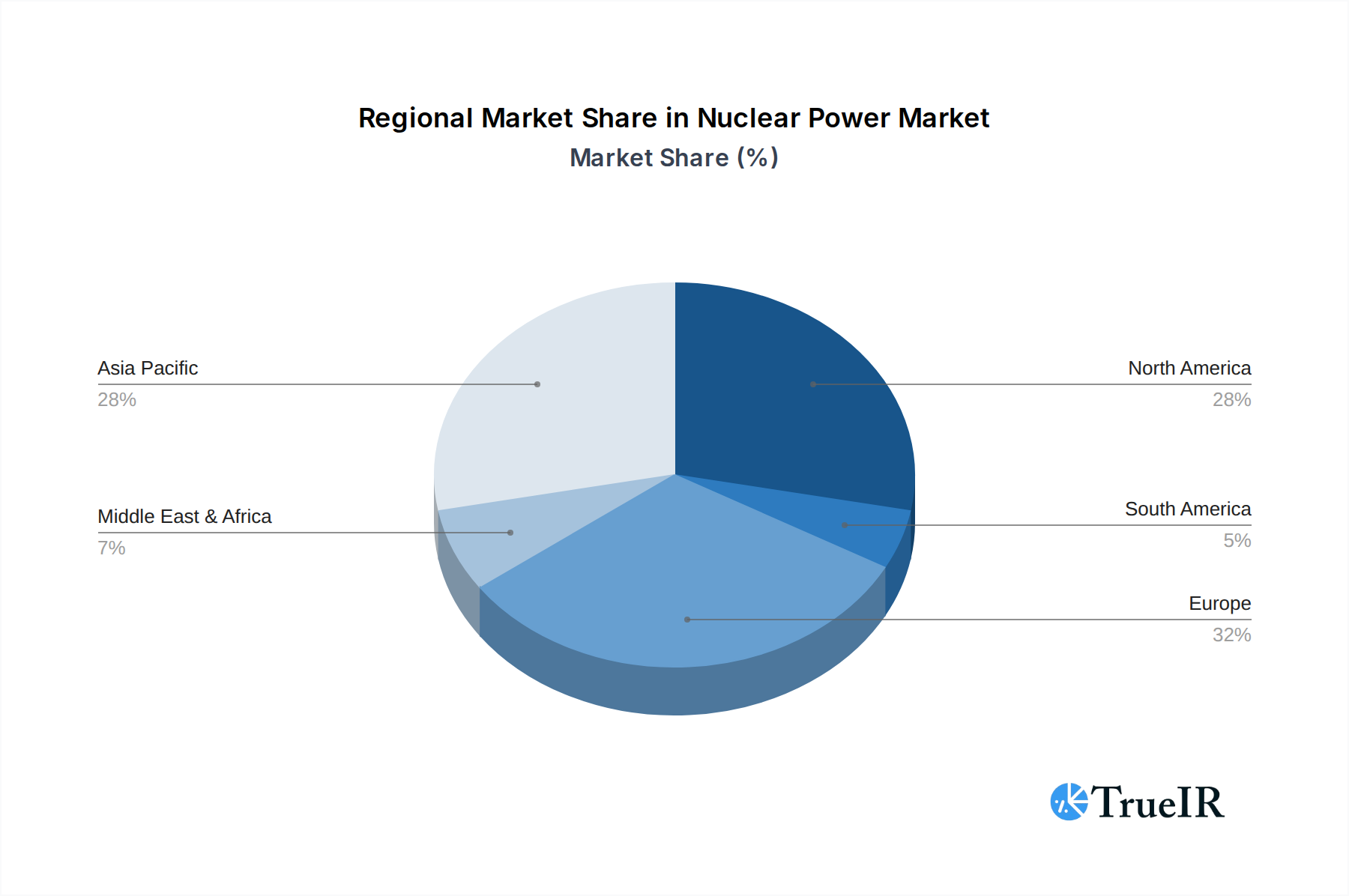

- Asia Pacific, particularly China, is emerging as the most dynamic region for nuclear power growth. China's ambitious energy strategy, aimed at achieving peak carbon emissions before 2030 and carbon neutrality by 2060, has propelled significant investment in new nuclear capacity. The country's ongoing development of large-scale reactors and its commitment to indigenous nuclear technology, spearheaded by entities like the China National Nuclear Cooperation (CNNC), underscore its leading role.

- North America and Europe continue to be significant markets, with a substantial installed base and ongoing efforts to extend the life of existing plants. However, new build projects in these regions often face greater regulatory scrutiny and public perception challenges.

Dominant Application Segment:

- Electric Power Generation: This segment accounts for an overwhelming majority of nuclear power's application. The need for reliable, baseload electricity to power industrial complexes, commercial enterprises, and residential areas makes nuclear power an indispensable component of the global energy mix. Countries are increasingly relying on nuclear power to meet their climate targets and enhance energy independence.

- Industrial Applications: While smaller than power generation, industrial uses of nuclear technology, such as process heat for chemical production or desalination, are gaining traction. This segment offers significant growth potential as industries seek more sustainable and efficient energy solutions.

- Medical Applications: The production of radioisotopes for medical imaging, cancer treatment, and sterilization remains a critical niche for nuclear technology. Demand in this sector is driven by advancements in healthcare and the growing global population.

- Food & Agriculture: Applications in food irradiation for preservation and pest control, as well as in agricultural research, contribute to the diversification of nuclear power's impact, though these segments are relatively smaller in terms of market value.

Dominant Reactor Type:

- Pressurized Water Reactor (PWR): PWRs are the most widely deployed reactor type globally, accounting for an estimated XX% of operational nuclear power capacity. Their proven safety record, operational efficiency, and extensive supply chain make them the preferred choice for new builds and life extensions. Companies like Westinghouse Electric Company are major players in this segment.

- Pressurized Heavy Water Reactor (PHWR): PHWRs, notably Candu reactors developed by Atomic Energy of Canada, are significant in countries like India and Canada, offering advantages in fuel flexibility.

- Boiler Water Reactor (BWR): BWRs, with a notable presence from GE Hitachi, represent another established technology with a substantial operational fleet.

- Gas Cooled Reactor (GCR) & Others: These include advanced reactor designs with evolving potential, such as high-temperature gas-cooled reactors (HTGRs) and future SMR designs, which are attracting significant research and development investment for their enhanced safety and versatility.

Nuclear Power Product Analysis

The nuclear power sector is characterized by continuous product innovation focused on enhancing safety, efficiency, and sustainability. Pressurized Water Reactors (PWRs) remain the most prevalent, offering robust designs and proven operational records, complemented by advancements in fuel enrichment and waste management solutions. Small Modular Reactors (SMRs) represent a significant product innovation, promising reduced construction costs, faster deployment, and enhanced safety profiles, making them attractive for a wider range of applications beyond traditional large-scale power generation. The competitive advantage of these products lies in their ability to provide reliable, carbon-free baseload power, crucial for grid stability and achieving climate objectives. Innovations in fuel cycle technologies, including advanced fuel types and reprocessing, aim to reduce waste volumes and improve resource utilization, further solidifying nuclear power's long-term viability.

Key Drivers, Barriers & Challenges in Nuclear Power

Key Drivers: The primary forces propelling the nuclear power market are the global imperative for decarbonization and the increasing demand for reliable, baseload electricity. Technological advancements, particularly in Small Modular Reactors (SMRs) and enhanced safety features, are making nuclear power more accessible and appealing. Government policies and incentives supporting clean energy, alongside growing energy security concerns, further bolster the sector's growth prospects. For example, numerous countries have set ambitious net-zero targets, with nuclear power identified as a crucial component to achieve these goals, driving investment in new projects and the refurbishment of existing facilities. The estimated market growth driven by these factors is projected to be in the XX% range annually.

Key Barriers & Challenges: Significant challenges impacting nuclear power growth include substantial upfront capital costs and long construction timelines, which can deter investment and lead to cost overruns. Stringent regulatory hurdles and public perception surrounding nuclear safety and waste disposal remain critical barriers. Supply chain complexities and the availability of skilled labor can also pose constraints. For instance, the cost of building a new nuclear power plant can easily run into tens of billions of dollars, and projects can face delays of several years, impacting their economic viability. The long-term management of radioactive waste requires secure and politically acceptable solutions, a persistent challenge for the industry. Competitive pressures from rapidly falling costs of renewable energy sources like solar and wind also present a significant restraint, although nuclear power's baseload capacity is often seen as complementary rather than directly substitutable.

Growth Drivers in the Nuclear Power Market

The nuclear power market is propelled by a confluence of powerful drivers. The global imperative to combat climate change and reduce greenhouse gas emissions is paramount, positioning nuclear power as a vital low-carbon energy source. This is complemented by the escalating demand for reliable, baseload electricity to support economic growth and meet the needs of an increasingly electrified world. Technological innovation is a significant catalyst, with the development and commercialization of Small Modular Reactors (SMRs) offering enhanced safety, cost-effectiveness, and deployment flexibility. Government support, including favorable policies, tax incentives, and long-term energy planning that incorporates nuclear power, further fuels market expansion. Economic factors such as energy security concerns and the desire to diversify energy portfolios away from volatile fossil fuel markets also contribute to the sustained interest in nuclear energy.

Challenges Impacting Nuclear Power Growth

Despite its advantages, nuclear power growth faces considerable challenges. The immense upfront capital investment and lengthy construction periods for traditional large-scale reactors present a significant financial barrier, often requiring substantial government backing or novel financing models. Navigating complex and evolving regulatory frameworks across different jurisdictions is another major hurdle, impacting project timelines and increasing costs. Public perception and concerns regarding nuclear safety, security, and the long-term management of radioactive waste continue to be significant restraints, requiring robust communication and demonstrable safety protocols. Additionally, the supply chain for nuclear components and skilled labor can be constrained, especially for new build projects, potentially leading to delays and cost escalations. Competitive pressures from increasingly affordable renewable energy sources also necessitate a clear demonstration of nuclear power's unique value proposition.

Key Players Shaping the Nuclear Power Market

- Westinghouse Electric Company

- Orano

- Nukem

- NIAEP ASC

- Mitsubishi Heavy Industries

- Larsen and Toubro (L&T)

- KEPCO

- GE Hitachi

- China National Nuclear Cooperation (CNNC)

- CEZ Group

- Bruce Power

- Bharat Heavy Electricals

- Atomic Energy of Canada

Significant Nuclear Power Industry Milestones

- 2019: Launch of the first Small Modular Reactor (SMR) prototype design phase by NuScale Power, signaling a new era of flexible nuclear deployment.

- 2020: China's Taishan 1 becomes the first operational Generation III+ reactor globally to achieve full power output.

- 2021: The UK government announces its intention to build new nuclear power stations, reaffirming its commitment to nuclear energy as a key part of its net-zero strategy.

- 2022: Rolls-Royce secures government funding for its SMR program in the UK, accelerating its development and potential deployment.

- 2023: Several countries, including France and Japan, announce plans to revitalize their nuclear power sectors, emphasizing life extensions and new reactor builds to enhance energy security and climate goals.

- 2024: Continued advancements in fuel reprocessing technologies and waste management solutions are reported by leading research institutions and companies, addressing long-standing challenges in the nuclear fuel cycle.

Future Outlook for Nuclear Power Market

The future outlook for the nuclear power market is characterized by cautious optimism and strategic expansion. The increasing global commitment to decarbonization remains the most significant growth catalyst, positioning nuclear power as an indispensable component of a low-carbon energy future. The anticipated growth in Small Modular Reactors (SMRs) presents a transformative opportunity, promising greater accessibility, enhanced safety, and cost-effectiveness for a wider range of applications. Strategic investments in life extensions for existing plants and the development of new reactor technologies by major players like GE Hitachi and Mitsubishi Heavy Industries will sustain market momentum. Furthermore, the growing emphasis on energy security and independence in various nations is expected to drive renewed interest and investment in nuclear power. The market is poised for steady growth, driven by technological innovation, supportive government policies, and the undeniable need for reliable, carbon-free baseload electricity.

Nuclear Power Segmentation

-

1. Application

- 1.1. Electric Power Generation

- 1.2. Industrial

- 1.3. Medical

- 1.4. Food & Agriculture

- 1.5. Others

-

2. Types

- 2.1. Pressurized Water Reactor (PWR)

- 2.2. Boiler Water Reactor (BWR)

- 2.3. Pressurized Heavy Water Reactor (PHWR)

- 2.4. Gas Cooled Reactor (GCR)

- 2.5. Others

Nuclear Power Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Nuclear Power Regional Market Share

Geographic Coverage of Nuclear Power

Nuclear Power REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Nuclear Power Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Electric Power Generation

- 5.1.2. Industrial

- 5.1.3. Medical

- 5.1.4. Food & Agriculture

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Pressurized Water Reactor (PWR)

- 5.2.2. Boiler Water Reactor (BWR)

- 5.2.3. Pressurized Heavy Water Reactor (PHWR)

- 5.2.4. Gas Cooled Reactor (GCR)

- 5.2.5. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Nuclear Power Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Electric Power Generation

- 6.1.2. Industrial

- 6.1.3. Medical

- 6.1.4. Food & Agriculture

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Pressurized Water Reactor (PWR)

- 6.2.2. Boiler Water Reactor (BWR)

- 6.2.3. Pressurized Heavy Water Reactor (PHWR)

- 6.2.4. Gas Cooled Reactor (GCR)

- 6.2.5. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Nuclear Power Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Electric Power Generation

- 7.1.2. Industrial

- 7.1.3. Medical

- 7.1.4. Food & Agriculture

- 7.1.5. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Pressurized Water Reactor (PWR)

- 7.2.2. Boiler Water Reactor (BWR)

- 7.2.3. Pressurized Heavy Water Reactor (PHWR)

- 7.2.4. Gas Cooled Reactor (GCR)

- 7.2.5. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Nuclear Power Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Electric Power Generation

- 8.1.2. Industrial

- 8.1.3. Medical

- 8.1.4. Food & Agriculture

- 8.1.5. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Pressurized Water Reactor (PWR)

- 8.2.2. Boiler Water Reactor (BWR)

- 8.2.3. Pressurized Heavy Water Reactor (PHWR)

- 8.2.4. Gas Cooled Reactor (GCR)

- 8.2.5. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Nuclear Power Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Electric Power Generation

- 9.1.2. Industrial

- 9.1.3. Medical

- 9.1.4. Food & Agriculture

- 9.1.5. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Pressurized Water Reactor (PWR)

- 9.2.2. Boiler Water Reactor (BWR)

- 9.2.3. Pressurized Heavy Water Reactor (PHWR)

- 9.2.4. Gas Cooled Reactor (GCR)

- 9.2.5. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Nuclear Power Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Electric Power Generation

- 10.1.2. Industrial

- 10.1.3. Medical

- 10.1.4. Food & Agriculture

- 10.1.5. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Pressurized Water Reactor (PWR)

- 10.2.2. Boiler Water Reactor (BWR)

- 10.2.3. Pressurized Heavy Water Reactor (PHWR)

- 10.2.4. Gas Cooled Reactor (GCR)

- 10.2.5. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Westinghouse Electric Company

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Orano

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Nukem

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 NIAEP ASC

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Mitsubishi Heavy Industries

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Larsen and Toubro (L&T)

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 KEPCO

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 GE Hitachi

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 China National Nuclear Cooperation (CNNC)

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 CEZ Group

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Bruce Power

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Bharat Heavy Electricals

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Atomic Energy of Canada

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.1 Westinghouse Electric Company

List of Figures

- Figure 1: Global Nuclear Power Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Nuclear Power Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Nuclear Power Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Nuclear Power Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Nuclear Power Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Nuclear Power Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Nuclear Power Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Nuclear Power Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Nuclear Power Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Nuclear Power Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Nuclear Power Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Nuclear Power Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Nuclear Power Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Nuclear Power Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Nuclear Power Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Nuclear Power Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Nuclear Power Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Nuclear Power Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Nuclear Power Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Nuclear Power Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Nuclear Power Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Nuclear Power Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Nuclear Power Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Nuclear Power Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Nuclear Power Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Nuclear Power Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Nuclear Power Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Nuclear Power Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Nuclear Power Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Nuclear Power Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Nuclear Power Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Nuclear Power Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Nuclear Power Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Nuclear Power Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Nuclear Power Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Nuclear Power Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Nuclear Power Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Nuclear Power Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Nuclear Power Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Nuclear Power Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Nuclear Power Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Nuclear Power Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Nuclear Power Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Nuclear Power Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Nuclear Power Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Nuclear Power Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Nuclear Power Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Nuclear Power Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Nuclear Power Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Nuclear Power Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Nuclear Power Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Nuclear Power Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Nuclear Power Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Nuclear Power Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Nuclear Power Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Nuclear Power Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Nuclear Power Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Nuclear Power Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Nuclear Power Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Nuclear Power Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Nuclear Power Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Nuclear Power Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Nuclear Power Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Nuclear Power Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Nuclear Power Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Nuclear Power Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Nuclear Power Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Nuclear Power Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Nuclear Power Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Nuclear Power Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Nuclear Power Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Nuclear Power Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Nuclear Power Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Nuclear Power Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Nuclear Power Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Nuclear Power Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Nuclear Power Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Nuclear Power?

The projected CAGR is approximately 4.1%.

2. Which companies are prominent players in the Nuclear Power?

Key companies in the market include Westinghouse Electric Company, Orano, Nukem, NIAEP ASC, Mitsubishi Heavy Industries, Larsen and Toubro (L&T), KEPCO, GE Hitachi, China National Nuclear Cooperation (CNNC), CEZ Group, Bruce Power, Bharat Heavy Electricals, Atomic Energy of Canada.

3. What are the main segments of the Nuclear Power?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 36.72 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Nuclear Power," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Nuclear Power report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Nuclear Power?

To stay informed about further developments, trends, and reports in the Nuclear Power, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence