Key Insights

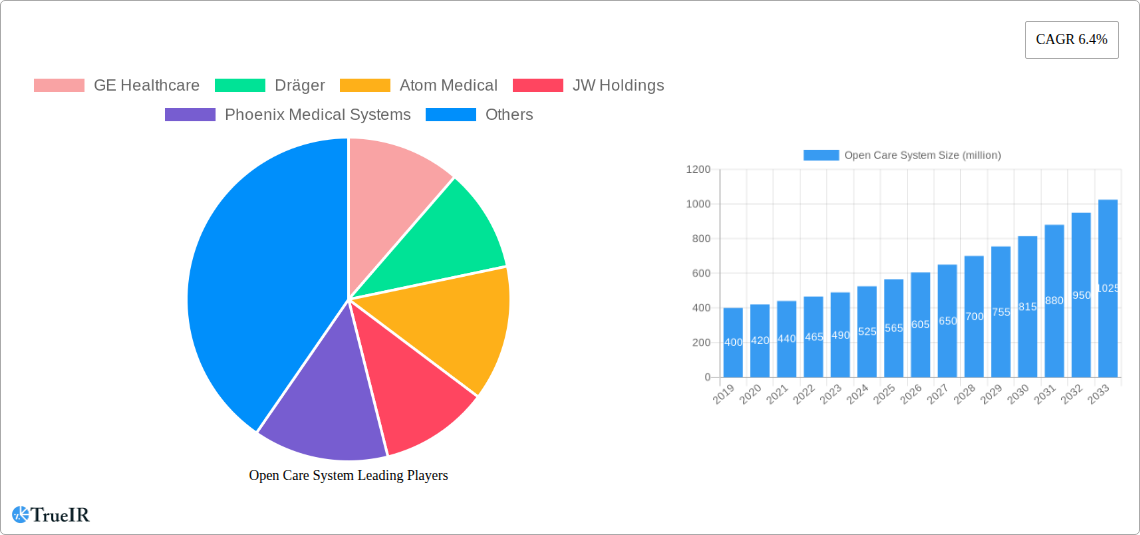

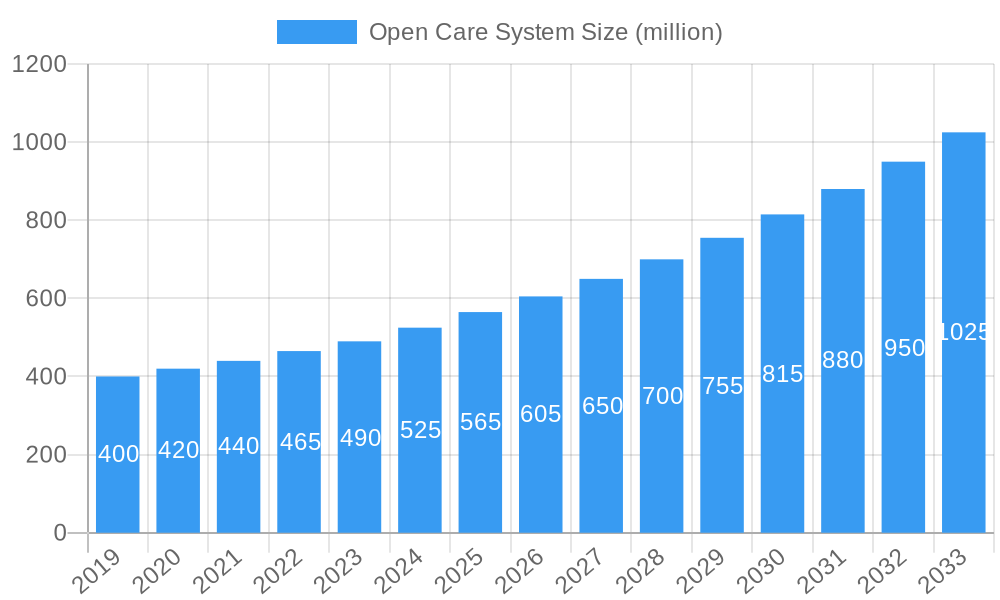

The Open Care System market is projected to experience robust growth, with an estimated market size of $565 million in 2025. Driven by an anticipated Compound Annual Growth Rate (CAGR) of 6.4%, the market is expected to expand significantly over the forecast period of 2025-2033. This expansion is fueled by increasing demand for advanced infant care solutions in both public and private hospital settings. The rising global birth rates, coupled with a greater emphasis on neonatal intensive care units (NICUs) and the need for specialized equipment to manage premature and critically ill newborns, are primary growth drivers. Furthermore, technological advancements leading to the development of more sophisticated and user-friendly open care systems, offering enhanced monitoring and therapeutic capabilities, are contributing to market acceleration. The 'Advanced Type' segment, in particular, is poised for substantial growth as healthcare facilities increasingly invest in cutting-edge technology to improve patient outcomes.

Open Care System Market Size (In Million)

The market is characterized by a diverse range of applications, primarily within Public Hospitals and Private Hospitals, alongside a smaller 'Others' category likely encompassing specialized neonatal clinics and research institutions. The competitive landscape is dynamic, featuring established global players like GE Healthcare and Dräger, alongside emerging regional manufacturers such as Atom Medical and JW Holdings. These companies are focusing on product innovation, strategic partnerships, and expanding their geographical reach to capture market share. While the market exhibits strong growth potential, certain restraints, such as the high initial cost of advanced systems and stringent regulatory requirements for medical devices, may pose challenges. However, the persistent need for effective and accessible neonatal care solutions across various economic regions globally is expected to outweigh these limitations, ensuring a positive market trajectory.

Open Care System Company Market Share

Here is a dynamic, SEO-optimized report description for the Open Care System market, designed for industry engagement and enhanced search rankings, without any placeholder modifications:

Open Care System Market Structure & Competitive Landscape

The global Open Care System market exhibits a moderately concentrated structure, with key players vying for significant market share through strategic product development and market expansion. Innovation drivers are primarily centered around enhancing infant patient outcomes, improving clinician workflow, and ensuring patient safety. Regulatory impacts are substantial, with stringent approvals and certifications required for market entry and product commercialization in major economies, contributing to higher barriers to entry. Product substitutes, while present in the broader infant care segment, offer less comprehensive solutions than integrated open care systems. End-user segmentation by application reveals a strong reliance on public and private hospital settings, with a growing demand from specialized neonatal intensive care units (NICUs). Mergers and acquisitions (M&A) trends are observed as major companies seek to expand their product portfolios, gain access to new technologies, and consolidate their market positions. Over the historical period of 2019–2024, M&A activities involved an estimated xx million in deal value, indicating a dynamic consolidation landscape. Concentration ratios for the top five players are estimated at xx%, highlighting a competitive yet manageable market environment.

Open Care System Market Trends & Opportunities

The global Open Care System market is poised for substantial expansion, projected to grow at a Compound Annual Growth Rate (CAGR) of approximately xx% from 2025 to 2033. This robust growth trajectory is fueled by an increasing global birth rate, a rising incidence of premature births, and a growing awareness of the importance of providing optimal care environments for neonates. Technological shifts are at the forefront, with a pronounced trend towards advanced integrated systems offering enhanced monitoring capabilities, precise temperature regulation, and seamless data integration with hospital information systems. Manufacturers are investing heavily in research and development to introduce next-generation open care systems featuring intelligent alarm management, user-friendly interfaces, and improved ergonomic designs for healthcare professionals. Consumer preferences are leaning towards solutions that offer a holistic approach to infant care, encompassing warmth, monitoring, and treatment within a single, controlled environment. This shift is driving demand for advanced open care systems over basic models. The competitive landscape is characterized by innovation, with companies striving to differentiate themselves through unique technological features and superior clinical outcomes. Market penetration rates are expected to surge as healthcare providers recognize the long-term benefits of investing in high-quality open care solutions, leading to a projected market size exceeding xx million by 2033. The base year of 2025 is critical, with initial market estimates around xx million, setting the stage for this significant upward trend.

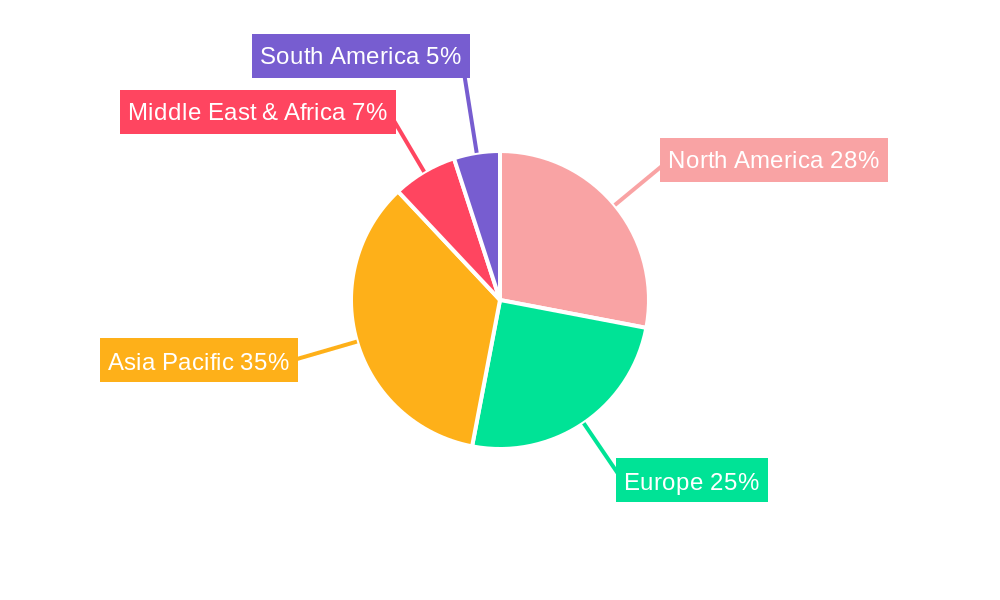

Dominant Markets & Segments in Open Care System

The Open Care System market exhibits distinct dominance across various geographical regions and application segments. Public Hospitals represent a significant application segment, driven by government initiatives aimed at improving neonatal healthcare infrastructure and increasing access to advanced medical technologies in under-served populations. The substantial patient volumes handled by public hospitals globally translate into consistent demand for reliable and efficient open care systems. Growth in this segment is propelled by infrastructure development projects and supportive government policies focused on enhancing maternal and child health.

Private Hospitals, while smaller in number compared to public facilities, represent a lucrative market due to their higher per-patient spending capacity and their emphasis on providing premium healthcare services. These institutions often prioritize the adoption of cutting-edge technologies, including advanced open care systems, to attract discerning clientele and ensure superior patient outcomes. Market dominance in this segment is influenced by factors such as the availability of advanced medical equipment, the presence of highly skilled medical professionals, and a strong focus on patient satisfaction.

In terms of Type, the Advanced Type segment is experiencing more rapid growth. This surge is attributed to increasing awareness of the benefits of sophisticated features like integrated respiratory support, advanced waveform analysis, and enhanced data management capabilities. Healthcare providers are recognizing that the initial higher investment in advanced systems translates into improved clinical efficacy, reduced complication rates, and ultimately, better long-term cost-effectiveness. The Basic/Standard Type segment continues to hold a steady market share, particularly in regions with limited healthcare budgets or for facilities that require foundational open care functionalities without the need for highly specialized features.

Key growth drivers for market dominance across these segments include rising healthcare expenditures, increasing prevalence of neonatal complications requiring specialized care, and the continuous technological evolution of open care systems. The estimated market size for 2025 is projected to be around xx million, with the forecast period of 2025–2033 anticipating a significant upward trend driven by these dominant markets and segments.

Open Care System Product Analysis

Open Care System product innovation is focused on creating integrated, intelligent, and user-centric solutions for neonatal care. Key advancements include enhanced thermal regulation with advanced servo-controlled heating systems, improved patient monitoring through integrated vital sign measurement and waveform display, and simplified user interfaces for intuitive operation by healthcare professionals. Competitive advantages are derived from modular designs allowing for customization, enhanced mobility for patient transport, and seamless data connectivity for electronic health record integration. These technological advancements directly address the critical needs for stable physiological environments and comprehensive patient assessment in the neonatal intensive care unit (NICU).

Key Drivers, Barriers & Challenges in Open Care System

Key Drivers: The Open Care System market is propelled by several key factors, including the increasing global incidence of premature births and low birth weight infants, which necessitates specialized and continuous care. Technological advancements in infant monitoring and life support are also significant drivers, leading to the development of more sophisticated and integrated open care systems. Rising healthcare expenditure, particularly in emerging economies, and government initiatives to improve neonatal healthcare infrastructure further fuel market growth. The growing demand for evidence-based care and improved infant outcomes are also crucial motivators for adopting advanced open care solutions.

Key Barriers & Challenges: Despite robust growth, the market faces several challenges. High initial acquisition costs of advanced open care systems can be a significant barrier, especially for healthcare facilities with limited budgets. Stringent regulatory approvals and compliance requirements across different regions add complexity and time to market entry. Supply chain disruptions, as witnessed in recent global events, can impact manufacturing and delivery timelines. Furthermore, the availability of alternative, less integrated infant care devices and the need for extensive training for healthcare professionals to effectively utilize complex systems pose ongoing challenges. Competitive pressures from established players and emerging manufacturers also necessitate continuous innovation and cost optimization.

Growth Drivers in the Open Care System Market

Several key factors are propelling the growth of the Open Care System market. Technologically, the integration of advanced sensors for precise physiological monitoring, intelligent alarm systems to reduce alarm fatigue, and user-friendly interfaces are enhancing clinical utility and patient safety. Economically, increasing healthcare investments globally, coupled with a rising prevalence of conditions requiring intensive neonatal care like prematurity and low birth weight, are creating substantial demand. Regulatory support and government initiatives aimed at improving maternal and child health outcomes in various countries are also acting as significant growth catalysts. For instance, national newborn screening programs often mandate the availability of advanced care equipment.

Challenges Impacting Open Care System Growth

The Open Care System market confronts several significant challenges that can impact its growth trajectory. Regulatory complexities in obtaining market approvals in different countries can lead to extended launch timelines and increased compliance costs. Supply chain vulnerabilities, including the availability of raw materials and components, pose a risk to consistent production and timely delivery of devices. Fierce competitive pressures from numerous market players, both established and emerging, necessitate continuous innovation and aggressive pricing strategies, potentially impacting profit margins. Moreover, the substantial initial investment required for advanced open care systems can be a barrier for smaller or resource-constrained healthcare facilities, limiting widespread adoption.

Key Players Shaping the Open Care System Market

- GE Healthcare

- Dräger

- Atom Medical

- JW Holdings

- Phoenix Medical Systems

- Médipréma

- Ibis Medical

- ASCO Medical

- Nice Neotech Medical Systems

- Narang Medical

- GPC Medical

- Ningbo David Medical Device

- Suzhou Being Medical Devices

- Zhengzhou Dison Instrument and Meter

Significant Open Care System Industry Milestones

- 2019: Introduction of advanced humidity control features in open care systems, significantly improving patient comfort and reducing insensible water loss.

- 2020: Launch of integrated respiratory support modules, allowing for seamless ventilation management within the open care environment, reducing the need for patient transfers.

- 2021: Development of AI-powered predictive alarm systems to proactively alert clinicians to potential patient deterioration, enhancing patient safety.

- 2022: Increased adoption of antimicrobial surfaces and materials in open care system design to minimize hospital-acquired infections.

- 2023: Enhanced connectivity features enabling real-time data streaming to remote monitoring platforms and electronic health records, improving care coordination.

- 2024: Emergence of highly portable and modular open care systems designed for flexible use across different hospital settings and transport situations.

Future Outlook for Open Care System Market

The future outlook for the Open Care System market is highly promising, driven by continued technological advancements and an unwavering focus on improving neonatal patient outcomes. Strategic opportunities lie in the expansion of integrated diagnostic and therapeutic capabilities within these systems, further enhancing their value proposition. The increasing demand for personalized infant care solutions, coupled with the growing healthcare infrastructure in emerging economies, presents substantial market potential. Companies that prioritize innovation, robust data integration, and user-centric design are well-positioned to capitalize on this evolving market landscape, leading to sustained growth and market penetration through the forecast period of 2025–2033.

Open Care System Segmentation

-

1. Application

- 1.1. Public Hospitals

- 1.2. Private Hospitals

- 1.3. Others

-

2. Type

- 2.1. Basic/Standard Type

- 2.2. Advanced Type

Open Care System Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Open Care System Regional Market Share

Geographic Coverage of Open Care System

Open Care System REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Open Care System Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Public Hospitals

- 5.1.2. Private Hospitals

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Basic/Standard Type

- 5.2.2. Advanced Type

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Open Care System Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Public Hospitals

- 6.1.2. Private Hospitals

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Basic/Standard Type

- 6.2.2. Advanced Type

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Open Care System Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Public Hospitals

- 7.1.2. Private Hospitals

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Basic/Standard Type

- 7.2.2. Advanced Type

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Open Care System Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Public Hospitals

- 8.1.2. Private Hospitals

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Basic/Standard Type

- 8.2.2. Advanced Type

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Open Care System Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Public Hospitals

- 9.1.2. Private Hospitals

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Basic/Standard Type

- 9.2.2. Advanced Type

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Open Care System Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Public Hospitals

- 10.1.2. Private Hospitals

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Basic/Standard Type

- 10.2.2. Advanced Type

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 GE Healthcare

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Dräger

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Atom Medical

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 JW Holdings

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Phoenix Medical Systems

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Médipréma

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Ibis Medical

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 ASCO Medical

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Nice Neotech Medical Systems

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Narang Medical

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 GPC Medical

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Ningbo David Medical Device

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Suzhou Being Medical Devices

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Zhengzhou Dison Instrument and Meter

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.1 GE Healthcare

List of Figures

- Figure 1: Global Open Care System Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: Global Open Care System Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Open Care System Revenue (million), by Application 2025 & 2033

- Figure 4: North America Open Care System Volume (K), by Application 2025 & 2033

- Figure 5: North America Open Care System Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Open Care System Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Open Care System Revenue (million), by Type 2025 & 2033

- Figure 8: North America Open Care System Volume (K), by Type 2025 & 2033

- Figure 9: North America Open Care System Revenue Share (%), by Type 2025 & 2033

- Figure 10: North America Open Care System Volume Share (%), by Type 2025 & 2033

- Figure 11: North America Open Care System Revenue (million), by Country 2025 & 2033

- Figure 12: North America Open Care System Volume (K), by Country 2025 & 2033

- Figure 13: North America Open Care System Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Open Care System Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Open Care System Revenue (million), by Application 2025 & 2033

- Figure 16: South America Open Care System Volume (K), by Application 2025 & 2033

- Figure 17: South America Open Care System Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Open Care System Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Open Care System Revenue (million), by Type 2025 & 2033

- Figure 20: South America Open Care System Volume (K), by Type 2025 & 2033

- Figure 21: South America Open Care System Revenue Share (%), by Type 2025 & 2033

- Figure 22: South America Open Care System Volume Share (%), by Type 2025 & 2033

- Figure 23: South America Open Care System Revenue (million), by Country 2025 & 2033

- Figure 24: South America Open Care System Volume (K), by Country 2025 & 2033

- Figure 25: South America Open Care System Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Open Care System Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Open Care System Revenue (million), by Application 2025 & 2033

- Figure 28: Europe Open Care System Volume (K), by Application 2025 & 2033

- Figure 29: Europe Open Care System Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Open Care System Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Open Care System Revenue (million), by Type 2025 & 2033

- Figure 32: Europe Open Care System Volume (K), by Type 2025 & 2033

- Figure 33: Europe Open Care System Revenue Share (%), by Type 2025 & 2033

- Figure 34: Europe Open Care System Volume Share (%), by Type 2025 & 2033

- Figure 35: Europe Open Care System Revenue (million), by Country 2025 & 2033

- Figure 36: Europe Open Care System Volume (K), by Country 2025 & 2033

- Figure 37: Europe Open Care System Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Open Care System Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Open Care System Revenue (million), by Application 2025 & 2033

- Figure 40: Middle East & Africa Open Care System Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Open Care System Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Open Care System Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Open Care System Revenue (million), by Type 2025 & 2033

- Figure 44: Middle East & Africa Open Care System Volume (K), by Type 2025 & 2033

- Figure 45: Middle East & Africa Open Care System Revenue Share (%), by Type 2025 & 2033

- Figure 46: Middle East & Africa Open Care System Volume Share (%), by Type 2025 & 2033

- Figure 47: Middle East & Africa Open Care System Revenue (million), by Country 2025 & 2033

- Figure 48: Middle East & Africa Open Care System Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Open Care System Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Open Care System Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Open Care System Revenue (million), by Application 2025 & 2033

- Figure 52: Asia Pacific Open Care System Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Open Care System Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Open Care System Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Open Care System Revenue (million), by Type 2025 & 2033

- Figure 56: Asia Pacific Open Care System Volume (K), by Type 2025 & 2033

- Figure 57: Asia Pacific Open Care System Revenue Share (%), by Type 2025 & 2033

- Figure 58: Asia Pacific Open Care System Volume Share (%), by Type 2025 & 2033

- Figure 59: Asia Pacific Open Care System Revenue (million), by Country 2025 & 2033

- Figure 60: Asia Pacific Open Care System Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Open Care System Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Open Care System Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Open Care System Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Open Care System Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Open Care System Revenue million Forecast, by Type 2020 & 2033

- Table 4: Global Open Care System Volume K Forecast, by Type 2020 & 2033

- Table 5: Global Open Care System Revenue million Forecast, by Region 2020 & 2033

- Table 6: Global Open Care System Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Open Care System Revenue million Forecast, by Application 2020 & 2033

- Table 8: Global Open Care System Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Open Care System Revenue million Forecast, by Type 2020 & 2033

- Table 10: Global Open Care System Volume K Forecast, by Type 2020 & 2033

- Table 11: Global Open Care System Revenue million Forecast, by Country 2020 & 2033

- Table 12: Global Open Care System Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Open Care System Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: United States Open Care System Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Open Care System Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Canada Open Care System Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Open Care System Revenue (million) Forecast, by Application 2020 & 2033

- Table 18: Mexico Open Care System Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Open Care System Revenue million Forecast, by Application 2020 & 2033

- Table 20: Global Open Care System Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Open Care System Revenue million Forecast, by Type 2020 & 2033

- Table 22: Global Open Care System Volume K Forecast, by Type 2020 & 2033

- Table 23: Global Open Care System Revenue million Forecast, by Country 2020 & 2033

- Table 24: Global Open Care System Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Open Care System Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Brazil Open Care System Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Open Care System Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Argentina Open Care System Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Open Care System Revenue (million) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Open Care System Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Open Care System Revenue million Forecast, by Application 2020 & 2033

- Table 32: Global Open Care System Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Open Care System Revenue million Forecast, by Type 2020 & 2033

- Table 34: Global Open Care System Volume K Forecast, by Type 2020 & 2033

- Table 35: Global Open Care System Revenue million Forecast, by Country 2020 & 2033

- Table 36: Global Open Care System Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Open Care System Revenue (million) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Open Care System Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Open Care System Revenue (million) Forecast, by Application 2020 & 2033

- Table 40: Germany Open Care System Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Open Care System Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: France Open Care System Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Open Care System Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: Italy Open Care System Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Open Care System Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Spain Open Care System Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Open Care System Revenue (million) Forecast, by Application 2020 & 2033

- Table 48: Russia Open Care System Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Open Care System Revenue (million) Forecast, by Application 2020 & 2033

- Table 50: Benelux Open Care System Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Open Care System Revenue (million) Forecast, by Application 2020 & 2033

- Table 52: Nordics Open Care System Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Open Care System Revenue (million) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Open Care System Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Open Care System Revenue million Forecast, by Application 2020 & 2033

- Table 56: Global Open Care System Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Open Care System Revenue million Forecast, by Type 2020 & 2033

- Table 58: Global Open Care System Volume K Forecast, by Type 2020 & 2033

- Table 59: Global Open Care System Revenue million Forecast, by Country 2020 & 2033

- Table 60: Global Open Care System Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Open Care System Revenue (million) Forecast, by Application 2020 & 2033

- Table 62: Turkey Open Care System Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Open Care System Revenue (million) Forecast, by Application 2020 & 2033

- Table 64: Israel Open Care System Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Open Care System Revenue (million) Forecast, by Application 2020 & 2033

- Table 66: GCC Open Care System Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Open Care System Revenue (million) Forecast, by Application 2020 & 2033

- Table 68: North Africa Open Care System Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Open Care System Revenue (million) Forecast, by Application 2020 & 2033

- Table 70: South Africa Open Care System Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Open Care System Revenue (million) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Open Care System Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Open Care System Revenue million Forecast, by Application 2020 & 2033

- Table 74: Global Open Care System Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Open Care System Revenue million Forecast, by Type 2020 & 2033

- Table 76: Global Open Care System Volume K Forecast, by Type 2020 & 2033

- Table 77: Global Open Care System Revenue million Forecast, by Country 2020 & 2033

- Table 78: Global Open Care System Volume K Forecast, by Country 2020 & 2033

- Table 79: China Open Care System Revenue (million) Forecast, by Application 2020 & 2033

- Table 80: China Open Care System Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Open Care System Revenue (million) Forecast, by Application 2020 & 2033

- Table 82: India Open Care System Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Open Care System Revenue (million) Forecast, by Application 2020 & 2033

- Table 84: Japan Open Care System Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Open Care System Revenue (million) Forecast, by Application 2020 & 2033

- Table 86: South Korea Open Care System Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Open Care System Revenue (million) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Open Care System Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Open Care System Revenue (million) Forecast, by Application 2020 & 2033

- Table 90: Oceania Open Care System Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Open Care System Revenue (million) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Open Care System Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Open Care System?

The projected CAGR is approximately 6.4%.

2. Which companies are prominent players in the Open Care System?

Key companies in the market include GE Healthcare, Dräger, Atom Medical, JW Holdings, Phoenix Medical Systems, Médipréma, Ibis Medical, ASCO Medical, Nice Neotech Medical Systems, Narang Medical, GPC Medical, Ningbo David Medical Device, Suzhou Being Medical Devices, Zhengzhou Dison Instrument and Meter.

3. What are the main segments of the Open Care System?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 565 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Open Care System," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Open Care System report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Open Care System?

To stay informed about further developments, trends, and reports in the Open Care System, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence