Key Insights

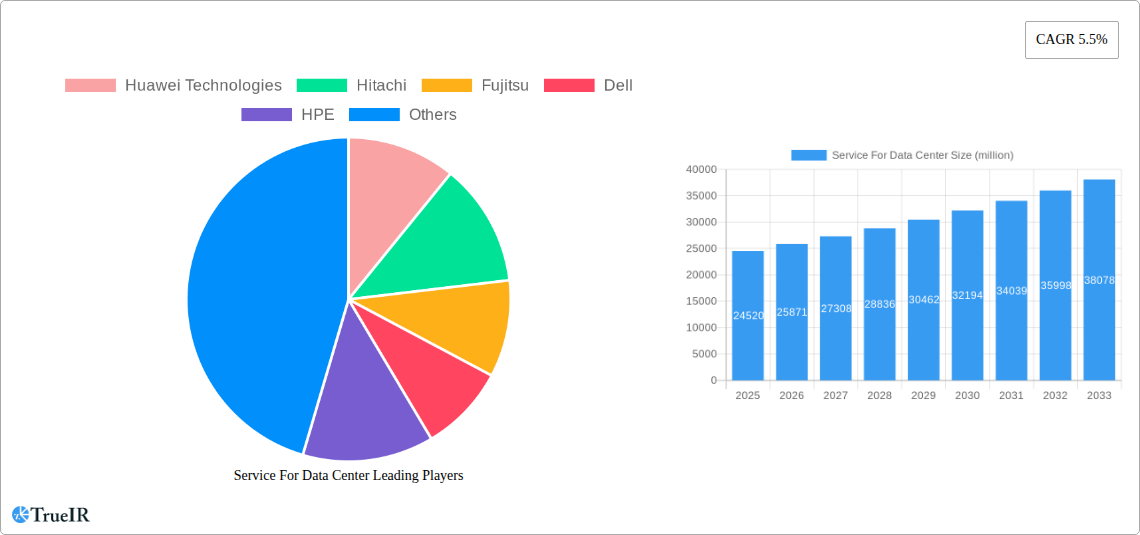

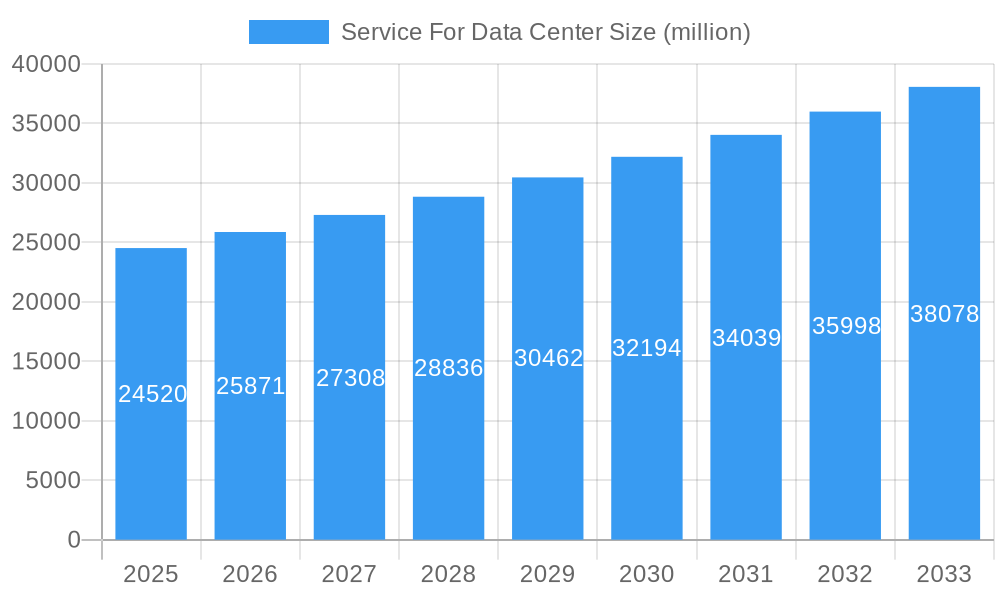

The global market for Data Center Services is poised for significant expansion, with a current market size of approximately 24,520 million in 2025. The sector is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.5% through 2033, indicating robust and sustained demand for comprehensive data center solutions. This growth is primarily fueled by the ever-increasing volume of digital data generated across industries and the escalating need for secure, efficient, and scalable data storage, processing, and management. Key drivers include the digital transformation initiatives across businesses, the widespread adoption of cloud computing, and the burgeoning demand for high-performance computing and AI capabilities. The IT and Telecom industry, Government and Defense, and Healthcare sectors are expected to be major contributors to this market expansion, leveraging advanced data center services for their critical operations and data management needs.

Service For Data Center Market Size (In Billion)

The Service for Data Center market encompasses a broad spectrum of offerings, from initial Design and Consulting to ongoing Support and Maintenance. Installation and Deployment services are experiencing strong demand as organizations build out new facilities or expand existing ones to accommodate evolving technological landscapes. Furthermore, Training and Development services are crucial for ensuring that IT professionals are equipped to manage increasingly complex data center infrastructures. While the market exhibits strong growth, potential restraints could emerge from cybersecurity threats, the significant capital investment required for advanced data center infrastructure, and stringent data privacy regulations. However, ongoing technological advancements, such as edge computing and the increasing focus on sustainability in data center operations, are expected to create new opportunities and further propel the market forward. Leading companies like Huawei Technologies, Hitachi, Fujitsu, Dell, HPE, IBM, and Cisco Systems are actively innovating and expanding their service portfolios to capture a significant share of this dynamic market.

Service For Data Center Company Market Share

Service For Data Center Market Report

This comprehensive report delves into the dynamic global market for Data Center Services, offering deep insights into its structure, competitive landscape, trends, opportunities, and future outlook. Spanning a study period from 2019 to 2033, with a base year of 2025, the report leverages historical data, current estimations, and robust forecasts to provide actionable intelligence for stakeholders. High-volume keywords such as "data center services," "cloud infrastructure," "colocation," "managed services," "IT modernization," "digital transformation," and "enterprise IT solutions" are integrated throughout to maximize SEO visibility and attract a targeted industry audience.

Service For Data Center Market Structure & Competitive Landscape

The Service For Data Center market is characterized by a moderately concentrated structure, with a significant presence of both established multinational corporations and emerging specialized providers. Innovation drivers are predominantly fueled by the escalating demand for cloud computing, big data analytics, artificial intelligence (AI), and the Internet of Things (IoT), necessitating robust and scalable data center infrastructure. Regulatory impacts, particularly concerning data privacy (e.g., GDPR, CCPA) and cybersecurity mandates, play a crucial role in shaping service offerings and compliance requirements. Product substitutes are increasingly sophisticated, with hybrid and multi-cloud strategies offering alternatives to traditional on-premise data center services. End-user segmentation reveals a diverse range of applications, with the IT and Telecom Industry and Government and Defense sectors being major consumers, followed by Healthcare and Manufacturing. Mergers and acquisitions (M&A) remain a key strategic imperative, with an estimated volume of over 50 M&A deals annually, aimed at expanding service portfolios, geographic reach, and technological capabilities. Key players actively engage in M&A to consolidate market share and acquire innovative technologies.

Service For Data Center Market Trends & Opportunities

The global Service For Data Center market is experiencing robust growth, projected to expand from an estimated USD 250,000 million in the base year of 2025 to over USD 500,000 million by the end of the forecast period in 2033. This impressive expansion is driven by a Compound Annual Growth Rate (CAGR) of approximately 10.5%. Technological shifts are fundamentally reshaping the industry, with a pronounced move towards edge computing, hyper-converged infrastructure, and software-defined data centers (SDDCs). These advancements enable greater efficiency, flexibility, and lower latency, catering to the burgeoning needs of real-time data processing. Consumer preferences are increasingly leaning towards comprehensive managed services, allowing organizations to offload complex IT operations and focus on core business objectives. This trend is evident in the rising market penetration rates of cloud-based data center solutions, which are projected to exceed 70% by 2033. Competitive dynamics are intensifying, with providers differentiating themselves through specialized service offerings, enhanced security protocols, and superior customer support. The relentless pursuit of digital transformation across all industries is a primary catalyst, driving demand for scalable, secure, and cost-effective data center solutions. Furthermore, the ongoing evolution of AI and machine learning algorithms necessitates massive data processing capabilities, directly fueling the demand for advanced data center services. The increasing adoption of IoT devices is generating unprecedented volumes of data, requiring sophisticated infrastructure for storage, processing, and analysis. Opportunities abound in niche segments such as hyperscale data centers, sustainable data center solutions, and specialized data center services for emerging technologies like blockchain and quantum computing. The ongoing investment in smart city initiatives and the expansion of 5G networks also present significant growth avenues.

Dominant Markets & Segments in Service For Data Center

The IT and Telecom Industry stands as the dominant segment within the Service For Data Center market, accounting for an estimated 35% of the total market share in 2025. This dominance is driven by the industry's inherent need for scalable, high-performance, and reliable infrastructure to support a vast array of digital services, cloud platforms, and telecommunications networks. The rapid pace of technological innovation and the constant introduction of new services necessitate continuous upgrades and expansion of data center capabilities. Government and Defense sectors represent another significant segment, driven by the critical need for secure, resilient, and compliant data storage and processing for national security, public services, and defense operations. Policies mandating data localization and stringent security standards further bolster demand in this segment.

The Healthcare sector is emerging as a rapidly growing segment, fueled by the digitization of patient records, the adoption of telehealth services, and the increasing use of AI for diagnostics and personalized medicine. Compliance with strict healthcare data regulations (e.g., HIPAA) is a key driver for specialized data center solutions.

Key Growth Drivers:

- Infrastructure Modernization: The ongoing need to upgrade aging data center infrastructure with more efficient and technologically advanced solutions.

- Cloud Adoption: The continuous migration of enterprise workloads to public, private, and hybrid cloud environments.

- Data Growth: The exponential increase in data generation from various sources, including IoT devices, social media, and business operations.

- Regulatory Compliance: Stringent data privacy and security regulations compelling organizations to invest in secure and compliant data center solutions.

- Digital Transformation Initiatives: Widespread adoption of digital technologies across industries, requiring robust IT backbones.

Dominant Segments by Type:

- Support and Maintenance: This segment currently holds the largest market share, estimated at 40%, due to the critical need for continuous operation and upkeep of complex data center environments. Downtime can result in substantial financial losses and reputational damage.

- Installation and Deployment: This segment is projected to witness significant growth, driven by the construction of new data centers and the expansion of existing facilities to meet rising demand.

- Design and Consulting: This segment plays a pivotal role in helping organizations plan, architect, and implement optimal data center strategies, including cloud migration and hybrid IT solutions.

- Training and Development: As data center technologies become more sophisticated, there is an increasing demand for skilled professionals, driving the need for specialized training programs.

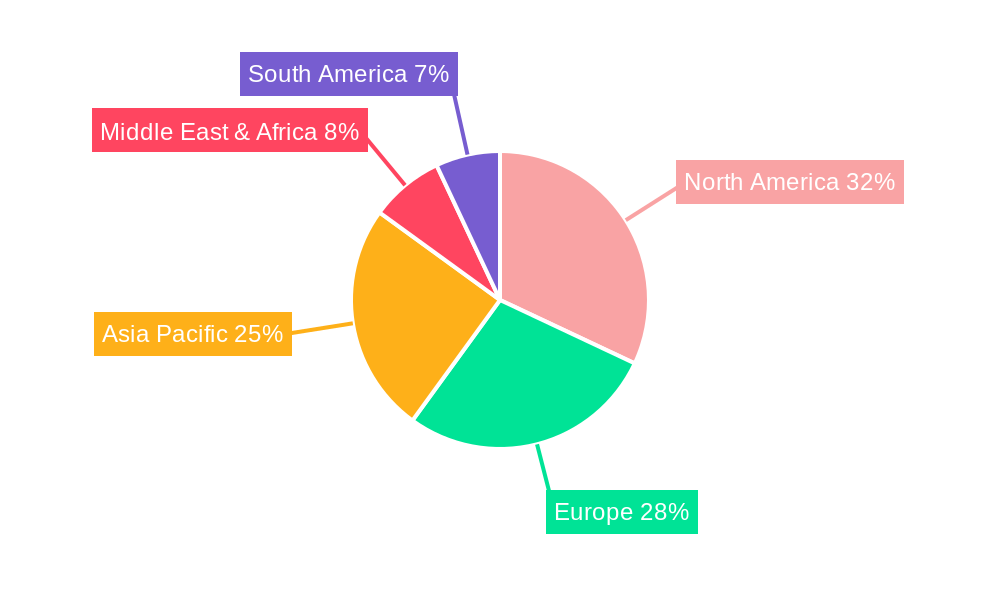

The dominant region for data center services is North America, driven by its mature technology sector, high concentration of hyperscale cloud providers, and significant enterprise adoption of advanced IT solutions. Asia Pacific is projected to be the fastest-growing region, fueled by rapid digitalization, increasing investments in cloud infrastructure, and the growing adoption of technologies like AI and IoT across emerging economies.

Service For Data Center Product Analysis

The Service For Data Center market is characterized by continuous product innovation focused on enhancing efficiency, scalability, and security. Key advancements include the development of modular and pre-fabricated data center solutions for faster deployment, AI-powered infrastructure management tools for predictive maintenance and optimization, and advanced cooling technologies to reduce energy consumption. Software-defined networking (SDN) and storage (SDS) are enabling greater flexibility and agility in data center operations. Competitive advantages are derived from specialized expertise in areas like hyperscale deployment, edge computing solutions, and compliance with stringent industry-specific regulations. The integration of advanced cybersecurity features and the focus on sustainable and green data center practices are becoming critical differentiators in attracting environmentally conscious enterprises.

Key Drivers, Barriers & Challenges in Service For Data Center

Key Drivers, Barriers & Challenges in Service For Data Center

The Service For Data Center market is propelled by several key drivers including the relentless pursuit of digital transformation across industries, the exponential growth of data, and the increasing adoption of cloud computing and AI. Technological advancements in areas like edge computing and hyper-converged infrastructure are enabling greater efficiency and scalability. Government initiatives promoting digitalization and the development of smart cities further contribute to market expansion.

However, significant barriers and challenges persist. High initial capital investment for building and maintaining data centers remains a considerable hurdle. Regulatory complexities, particularly concerning data privacy and cross-border data transfer, add layers of compliance challenges. Cybersecurity threats and the need for robust protection against sophisticated attacks require continuous investment in advanced security solutions. Additionally, the shortage of skilled IT professionals capable of managing complex data center environments poses a significant constraint on growth.

Growth Drivers in the Service For Data Center Market

The growth of the Service For Data Center market is fundamentally driven by the escalating demand for digital transformation initiatives across all sectors. The pervasive adoption of cloud computing, including public, private, and hybrid models, necessitates robust and scalable data center infrastructure. The exponential increase in data generation from IoT devices, big data analytics, and AI applications requires advanced storage, processing, and networking capabilities. Furthermore, governmental policies promoting digitalization and the development of smart infrastructure are creating new avenues for growth. Technological advancements such as edge computing and software-defined data centers are enhancing efficiency and flexibility, making them attractive options for businesses.

Challenges Impacting Service For Data Center Growth

Several challenges are impacting the growth of the Service For Data Center market. The significant initial capital expenditure required for establishing and maintaining data centers presents a substantial financial barrier for many organizations. Evolving regulatory landscapes concerning data privacy, sovereignty, and cybersecurity, such as GDPR and CCPA, introduce complexities in compliance and operations. Supply chain disruptions, particularly for critical hardware components, can lead to project delays and increased costs. Intense competitive pressures from established players and new entrants necessitate continuous innovation and cost optimization. The ongoing shortage of skilled IT professionals capable of managing and securing advanced data center infrastructure also poses a significant impediment to widespread adoption and seamless operation.

Key Players Shaping the Service For Data Center Market

- Huawei Technologies

- Hitachi

- Fujitsu

- Dell

- HPE

- IBM

- Reliance Group

- Capgemini

- HCL Technologies

- Schneider Electric SE

- Cisco Systems

- Vertiv

- Equinix

Significant Service For Data Center Industry Milestones

- 2019: Increased adoption of hybrid cloud strategies by enterprises.

- 2020: Rise in demand for colocation services due to the pandemic-driven remote work surge.

- 2021: Major investments in AI and machine learning infrastructure by hyperscale cloud providers.

- 2022: Growing focus on sustainable data center operations and energy efficiency initiatives.

- 2023: Expansion of edge data center deployments to support 5G networks and IoT applications.

- 2024: Continued M&A activity aimed at consolidating market share and expanding service portfolios.

Future Outlook for Service For Data Center Market

The future outlook for the Service For Data Center market remains exceptionally strong, fueled by the accelerating pace of digital transformation and the ever-increasing demand for data processing and storage. Strategic opportunities lie in the continued expansion of hyperscale data centers, the widespread adoption of edge computing solutions, and the development of specialized data center services for emerging technologies like quantum computing and advanced AI applications. Investments in sustainable data center practices and the implementation of AI-driven operational efficiencies will be key to future success. The market is poised for significant growth, driven by the fundamental shift towards a data-centric economy and the continuous need for robust, secure, and scalable digital infrastructure.

Service For Data Center Segmentation

-

1. Application

- 1.1. IT and Telecom Industry

- 1.2. Government and Defense

- 1.3. Healthcare

- 1.4. Education

- 1.5. Energy

- 1.6. Manufacturing

- 1.7. Other

-

2. Type

- 2.1. Design and Consulting

- 2.2. Installation and Deployment

- 2.3. Training and Development

- 2.4. Support and Maintenance

Service For Data Center Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Service For Data Center Regional Market Share

Geographic Coverage of Service For Data Center

Service For Data Center REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Service For Data Center Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. IT and Telecom Industry

- 5.1.2. Government and Defense

- 5.1.3. Healthcare

- 5.1.4. Education

- 5.1.5. Energy

- 5.1.6. Manufacturing

- 5.1.7. Other

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Design and Consulting

- 5.2.2. Installation and Deployment

- 5.2.3. Training and Development

- 5.2.4. Support and Maintenance

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Service For Data Center Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. IT and Telecom Industry

- 6.1.2. Government and Defense

- 6.1.3. Healthcare

- 6.1.4. Education

- 6.1.5. Energy

- 6.1.6. Manufacturing

- 6.1.7. Other

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Design and Consulting

- 6.2.2. Installation and Deployment

- 6.2.3. Training and Development

- 6.2.4. Support and Maintenance

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Service For Data Center Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. IT and Telecom Industry

- 7.1.2. Government and Defense

- 7.1.3. Healthcare

- 7.1.4. Education

- 7.1.5. Energy

- 7.1.6. Manufacturing

- 7.1.7. Other

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Design and Consulting

- 7.2.2. Installation and Deployment

- 7.2.3. Training and Development

- 7.2.4. Support and Maintenance

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Service For Data Center Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. IT and Telecom Industry

- 8.1.2. Government and Defense

- 8.1.3. Healthcare

- 8.1.4. Education

- 8.1.5. Energy

- 8.1.6. Manufacturing

- 8.1.7. Other

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Design and Consulting

- 8.2.2. Installation and Deployment

- 8.2.3. Training and Development

- 8.2.4. Support and Maintenance

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Service For Data Center Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. IT and Telecom Industry

- 9.1.2. Government and Defense

- 9.1.3. Healthcare

- 9.1.4. Education

- 9.1.5. Energy

- 9.1.6. Manufacturing

- 9.1.7. Other

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Design and Consulting

- 9.2.2. Installation and Deployment

- 9.2.3. Training and Development

- 9.2.4. Support and Maintenance

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Service For Data Center Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. IT and Telecom Industry

- 10.1.2. Government and Defense

- 10.1.3. Healthcare

- 10.1.4. Education

- 10.1.5. Energy

- 10.1.6. Manufacturing

- 10.1.7. Other

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Design and Consulting

- 10.2.2. Installation and Deployment

- 10.2.3. Training and Development

- 10.2.4. Support and Maintenance

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Huawei Technologies

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Hitachi

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Fujitsu

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Dell

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 HPE

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 IBM

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Reliance Group

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Capgemini

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 HCL Technologies

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Schneider Electric SE

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Cisco Systems

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Vertiv

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Equinix

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.1 Huawei Technologies

List of Figures

- Figure 1: Global Service For Data Center Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America Service For Data Center Revenue (million), by Application 2025 & 2033

- Figure 3: North America Service For Data Center Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Service For Data Center Revenue (million), by Type 2025 & 2033

- Figure 5: North America Service For Data Center Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Service For Data Center Revenue (million), by Country 2025 & 2033

- Figure 7: North America Service For Data Center Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Service For Data Center Revenue (million), by Application 2025 & 2033

- Figure 9: South America Service For Data Center Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Service For Data Center Revenue (million), by Type 2025 & 2033

- Figure 11: South America Service For Data Center Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Service For Data Center Revenue (million), by Country 2025 & 2033

- Figure 13: South America Service For Data Center Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Service For Data Center Revenue (million), by Application 2025 & 2033

- Figure 15: Europe Service For Data Center Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Service For Data Center Revenue (million), by Type 2025 & 2033

- Figure 17: Europe Service For Data Center Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Service For Data Center Revenue (million), by Country 2025 & 2033

- Figure 19: Europe Service For Data Center Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Service For Data Center Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa Service For Data Center Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Service For Data Center Revenue (million), by Type 2025 & 2033

- Figure 23: Middle East & Africa Service For Data Center Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Service For Data Center Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa Service For Data Center Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Service For Data Center Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific Service For Data Center Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Service For Data Center Revenue (million), by Type 2025 & 2033

- Figure 29: Asia Pacific Service For Data Center Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Service For Data Center Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific Service For Data Center Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Service For Data Center Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Service For Data Center Revenue million Forecast, by Type 2020 & 2033

- Table 3: Global Service For Data Center Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global Service For Data Center Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global Service For Data Center Revenue million Forecast, by Type 2020 & 2033

- Table 6: Global Service For Data Center Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States Service For Data Center Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada Service For Data Center Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico Service For Data Center Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global Service For Data Center Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global Service For Data Center Revenue million Forecast, by Type 2020 & 2033

- Table 12: Global Service For Data Center Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil Service For Data Center Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina Service For Data Center Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Service For Data Center Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global Service For Data Center Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global Service For Data Center Revenue million Forecast, by Type 2020 & 2033

- Table 18: Global Service For Data Center Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Service For Data Center Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany Service For Data Center Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France Service For Data Center Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy Service For Data Center Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain Service For Data Center Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia Service For Data Center Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux Service For Data Center Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics Service For Data Center Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Service For Data Center Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global Service For Data Center Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global Service For Data Center Revenue million Forecast, by Type 2020 & 2033

- Table 30: Global Service For Data Center Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey Service For Data Center Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel Service For Data Center Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC Service For Data Center Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa Service For Data Center Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa Service For Data Center Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Service For Data Center Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global Service For Data Center Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global Service For Data Center Revenue million Forecast, by Type 2020 & 2033

- Table 39: Global Service For Data Center Revenue million Forecast, by Country 2020 & 2033

- Table 40: China Service For Data Center Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India Service For Data Center Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan Service For Data Center Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea Service For Data Center Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Service For Data Center Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania Service For Data Center Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Service For Data Center Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Service For Data Center?

The projected CAGR is approximately 5.5%.

2. Which companies are prominent players in the Service For Data Center?

Key companies in the market include Huawei Technologies, Hitachi, Fujitsu, Dell, HPE, IBM, Reliance Group, Capgemini, HCL Technologies, Schneider Electric SE, Cisco Systems, Vertiv, Equinix.

3. What are the main segments of the Service For Data Center?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 24520 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4250.00, USD 6375.00, and USD 8500.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Service For Data Center," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Service For Data Center report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Service For Data Center?

To stay informed about further developments, trends, and reports in the Service For Data Center, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence