Key Insights

The African specialty fertilizer market is projected to reach $4.93 billion by 2025, with an anticipated Compound Annual Growth Rate (CAGR) of 6.65% from 2025 to 2033. This growth is propelled by the escalating demand for enhanced crop yields across field crops, horticulture, and turf & ornamental sectors. Specialized fertilizers, tailored for specific crop and soil needs, are central to this trend. The adoption of advanced farming techniques, including fertigation and foliar application, is also improving nutrient uptake and driving market expansion. Government efforts to boost agricultural productivity and food security further support investment in the specialty fertilizer industry. South Africa currently leads the market, with Nigeria and other East African nations showing significant growth potential.

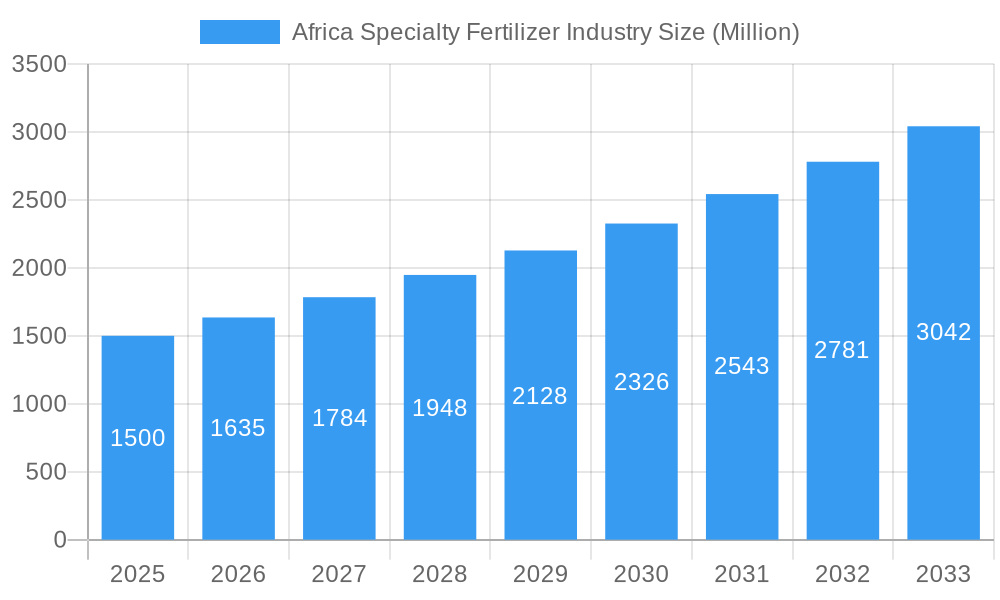

Africa Specialty Fertilizer Industry Market Size (In Billion)

Key challenges for the African specialty fertilizer market include high input costs for raw materials and transportation, potentially limiting access for smallholder farmers. Infrastructural limitations, such as unreliable electricity and poor road networks, can impede efficient distribution. Overcoming these logistical and economic hurdles is vital for market realization. Nevertheless, the long-term outlook is positive, supported by investments in agricultural modernization and increasing food production demands. The growing popularity of controlled-release fertilizers (CRF) and water-soluble fertilizers signals a shift towards precision and sustainable agriculture. Intense competition among key players like Haifa Group, Yara International, and ICL Group is fostering innovation and expanding product offerings.

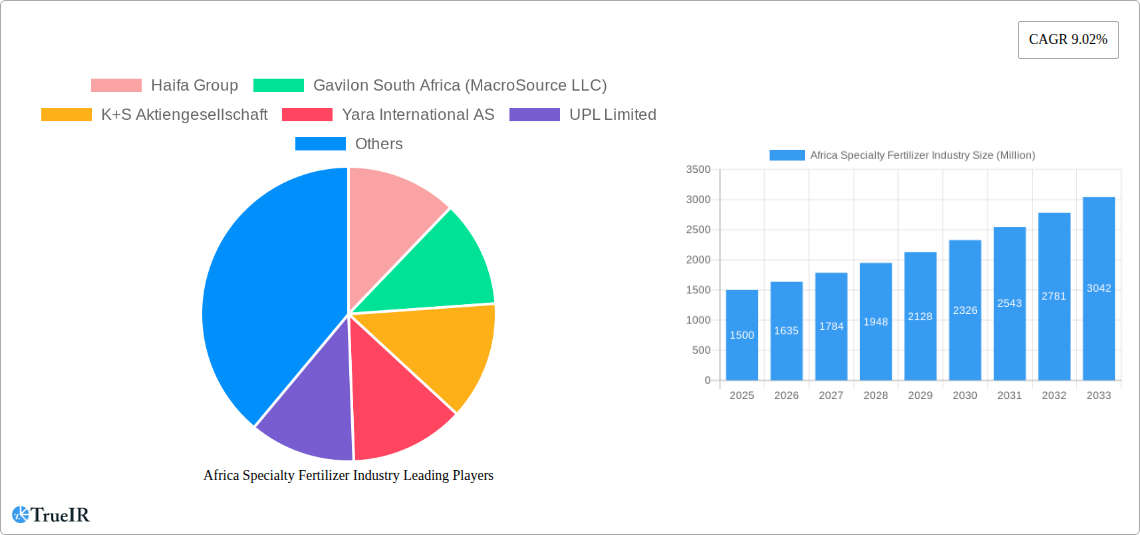

Africa Specialty Fertilizer Industry Company Market Share

Africa Specialty Fertilizer Industry: A Comprehensive Market Report (2019-2033)

This dynamic report provides a detailed analysis of the Africa specialty fertilizer industry, offering invaluable insights for investors, industry professionals, and stakeholders. The study period covers 2019-2033, with a base year of 2025 and a forecast period of 2025-2033. The report leverages extensive market research and data analysis to provide a comprehensive understanding of market size, trends, opportunities, and challenges. This report is crucial for navigating the complexities of this rapidly evolving market and making informed strategic decisions. The market is projected to reach xx Million by 2033, exhibiting a CAGR of xx% during the forecast period.

Africa Specialty Fertilizer Industry Market Structure & Competitive Landscape

The African specialty fertilizer market is characterized by a moderate level of concentration, with key players such as Haifa Group, Gavilon South Africa (MacroSource LLC), K+S Aktiengesellschaft, Yara International AS, UPL Limited, ICL Group Ltd, and Kynoch Fertilizer vying for market share. The market structure is influenced by several factors including:

- Market Concentration: The Herfindahl-Hirschman Index (HHI) for the market is estimated at xx, indicating a moderately concentrated market.

- Innovation Drivers: Demand for high-efficiency fertilizers, coupled with advancements in controlled-release fertilizers (CRFs), water-soluble fertilizers, and liquid fertilizers, are major innovation drivers.

- Regulatory Impacts: Government policies and regulations related to fertilizer use, environmental protection, and food security significantly influence market dynamics. Variations in regulations across different African countries add complexity.

- Product Substitutes: Organic fertilizers and biofertilizers pose a growing competitive threat, particularly among environmentally conscious farmers.

- End-User Segmentation: The market is segmented by crop type (field crops, horticultural crops, turf & ornamental), application mode (fertigation, foliar, soil), and specialty type (CRF, SRF, water-soluble, liquid fertilizer). Field crops currently dominate consumption.

- M&A Trends: Recent mergers and acquisitions, such as K+S's acquisition of a 75% stake in Industrial Commodities Holdings (Pty) Ltd in 2023 and Kynoch's acquisitions of Profert Fertilizer and Sidi Parani in 2019, highlight the ongoing consolidation within the industry. These activities aim to expand market reach, enhance production capabilities, and improve efficiency.

Africa Specialty Fertilizer Industry Market Trends & Opportunities

The Africa specialty fertilizer market is experiencing substantial growth driven by increasing agricultural production, rising demand for high-yielding crops, and government initiatives promoting agricultural modernization. Key trends include:

The market size grew from xx Million in 2019 to xx Million in 2024, demonstrating a robust growth trajectory. Technological advancements, particularly in precision agriculture and controlled-release fertilizer technologies, are transforming farming practices and boosting demand for specialty fertilizers. Consumer preferences are shifting towards environmentally friendly and high-efficiency fertilizers, creating opportunities for sustainable fertilizer solutions. Increased investment in agricultural infrastructure and irrigation systems is fostering further market growth. Intense competition among existing players and the emergence of new entrants are shaping market dynamics. The market penetration rate for specialty fertilizers in key African countries remains relatively low, representing a significant untapped potential. The CAGR for the forecast period (2025-2033) is projected to be xx%, driven by factors such as rising agricultural output, expanding irrigation infrastructure, and governmental support for agricultural development.

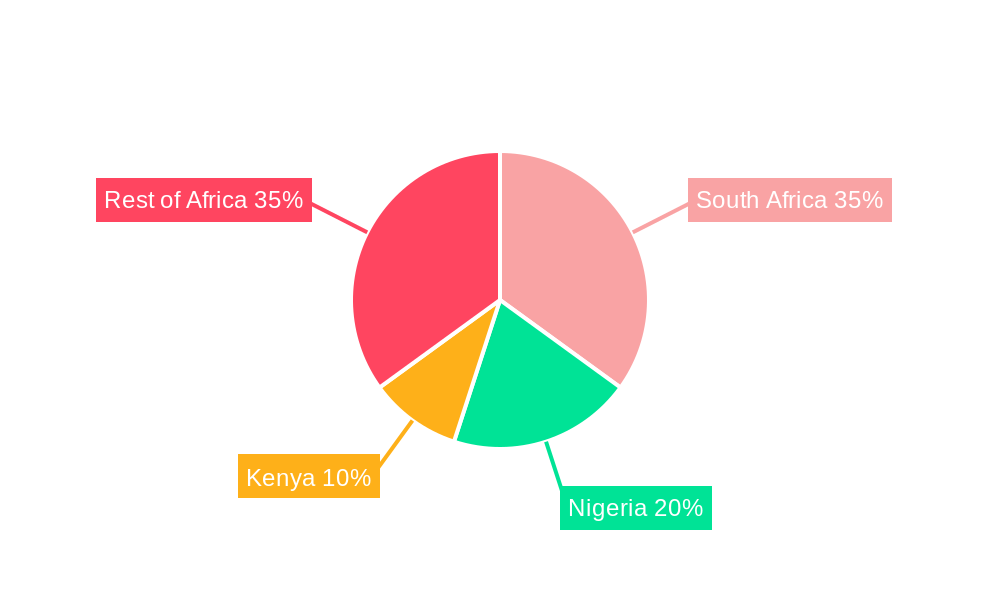

Dominant Markets & Segments in Africa Specialty Fertilizer Industry

South Africa represents the largest national market, followed by Nigeria and the Rest of Africa. Within the segments:

- Leading Region: Southern Africa

- Leading Country: South Africa

- Leading Application Mode: Soil application remains dominant due to established farming practices.

- Leading Crop Type: Field crops constitute the largest segment due to their extensive acreage.

- Leading Specialty Type: CRF fertilizers are gaining traction due to their efficiency and reduced environmental impact.

Key Growth Drivers:

- Increased Agricultural Investments: Government initiatives and private investments in agricultural infrastructure are driving growth.

- Improved Irrigation Systems: Expansion of irrigation networks enhances crop yields and fertilizer demand.

- Favorable Government Policies: Policies promoting agricultural modernization and food security are creating a conducive environment for the fertilizer industry.

- Rising Disposable Incomes: Increasing disposable incomes are leading to higher demand for better-quality produce and hence specialty fertilizers.

The dominance of South Africa is attributed to its relatively advanced agricultural sector, established distribution networks, and supportive government policies. However, Nigeria and other countries in the Rest of Africa present significant growth opportunities due to their large agricultural sectors and potential for expansion.

Africa Specialty Fertilizer Industry Product Analysis

The African specialty fertilizer market showcases a diverse range of products including CRFs, SRFs, water-soluble fertilizers, and liquid fertilizers. Technological advancements focus on improving nutrient use efficiency, reducing environmental impact, and enhancing crop yields. CRFs are becoming increasingly popular due to their ability to release nutrients gradually, maximizing nutrient uptake and minimizing environmental pollution. Water-soluble fertilizers offer the advantage of quick nutrient availability, while liquid fertilizers provide ease of application and improved nutrient uptake. The competitive landscape is shaped by product differentiation, pricing strategies, and brand recognition.

Key Drivers, Barriers & Challenges in Africa Specialty Fertilizer Industry

Key Drivers:

- Growing Agricultural Production: The rising demand for food in Africa is driving agricultural expansion, thereby increasing the need for fertilizers.

- Technological Advancements: Innovations in fertilizer formulations and application technologies improve efficiency and crop yields.

- Government Support: Policies and initiatives aimed at boosting agricultural productivity are creating a supportive environment for the fertilizer industry.

Challenges:

- Infrastructure Deficiencies: Inadequate transportation and storage infrastructure hinder efficient fertilizer distribution, leading to increased costs and reduced accessibility for farmers. This limitation affects approximately xx% of the market.

- High Input Costs: The cost of raw materials, manufacturing, and distribution impacts fertilizer affordability for farmers.

- Climate Change Impacts: Variability in rainfall and extreme weather events affect crop yields and fertilizer use efficiency.

- Counterfeit Products: The prevalence of counterfeit fertilizers undermines quality and poses risks to farmers and the environment.

Growth Drivers in the Africa Specialty Fertilizer Industry Market

The growth of the African specialty fertilizer market is primarily driven by increasing demand for food security, government initiatives promoting agricultural modernization, and improvements in farming techniques. Technological advancements in fertilizer formulations and application methods also play a crucial role. Furthermore, rising disposable incomes contribute to increased demand for better-quality food products.

Challenges Impacting Africa Specialty Fertilizer Industry Growth

Significant challenges include inadequate infrastructure, high input costs (including raw materials and transportation), climate change vulnerability, and the presence of counterfeit products, all of which limit market penetration and profitability. Regulatory complexities and inconsistent policies across different countries further complicate the market landscape.

Key Players Shaping the Africa Specialty Fertilizer Industry Market

- Haifa Group

- Gavilon South Africa (MacroSource LLC)

- K+S Aktiengesellschaft

- Yara International AS

- UPL Limited

- ICL Group Ltd

- Kynoch Fertilizer

Significant Africa Specialty Fertilizer Industry Industry Milestones

- April 2023: K+S acquired a 75% share of Industrial Commodities Holdings (Pty) Ltd's fertilizer business, strengthening its presence in southern and eastern Africa.

- April 2019: Kynoch acquired Profert Fertilizer, expanding its market access and production capacity.

- March 2019: Kynoch acquired Sidi Parani, significantly bolstering its market position in South Africa and across Africa.

Future Outlook for Africa Specialty Fertilizer Industry Market

The African specialty fertilizer market is poised for continued growth, driven by increasing agricultural production, rising demand for high-quality food, and supportive government policies. Strategic investments in infrastructure development, technological innovation, and sustainable farming practices will further unlock market potential. The focus on enhancing nutrient use efficiency and minimizing environmental impacts will shape future product development and market dynamics. The market is expected to experience robust growth, driven by factors such as rising agricultural output and increasing government support.

Africa Specialty Fertilizer Industry Segmentation

- 1. Production Analysis

- 2. Consumption Analysis

- 3. Import Market Analysis (Value & Volume)

- 4. Export Market Analysis (Value & Volume)

- 5. Price Trend Analysis

Africa Specialty Fertilizer Industry Segmentation By Geography

-

1. Africa

- 1.1. Nigeria

- 1.2. South Africa

- 1.3. Egypt

- 1.4. Kenya

- 1.5. Ethiopia

- 1.6. Morocco

- 1.7. Ghana

- 1.8. Algeria

- 1.9. Tanzania

- 1.10. Ivory Coast

Africa Specialty Fertilizer Industry Regional Market Share

Geographic Coverage of Africa Specialty Fertilizer Industry

Africa Specialty Fertilizer Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.65% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Production Analysis

- 5.2. Market Analysis, Insights and Forecast - by Consumption Analysis

- 5.3. Market Analysis, Insights and Forecast - by Import Market Analysis (Value & Volume)

- 5.4. Market Analysis, Insights and Forecast - by Export Market Analysis (Value & Volume)

- 5.5. Market Analysis, Insights and Forecast - by Price Trend Analysis

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. Africa

- 6. Africa Specialty Fertilizer Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Production Analysis

- 6.2. Market Analysis, Insights and Forecast - by Consumption Analysis

- 6.3. Market Analysis, Insights and Forecast - by Import Market Analysis (Value & Volume)

- 6.4. Market Analysis, Insights and Forecast - by Export Market Analysis (Value & Volume)

- 6.5. Market Analysis, Insights and Forecast - by Price Trend Analysis

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Haifa Group

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Gavilon South Africa (MacroSource LLC)

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 K+S Aktiengesellschaft

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Yara International AS

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 UPL Limited

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 ICL Group Ltd

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Kynoch Fertilizer

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.1 Haifa Group

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Africa Specialty Fertilizer Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Africa Specialty Fertilizer Industry Share (%) by Company 2025

List of Tables

- Table 1: Africa Specialty Fertilizer Industry Revenue billion Forecast, by Production Analysis 2020 & 2033

- Table 2: Africa Specialty Fertilizer Industry Revenue billion Forecast, by Consumption Analysis 2020 & 2033

- Table 3: Africa Specialty Fertilizer Industry Revenue billion Forecast, by Import Market Analysis (Value & Volume) 2020 & 2033

- Table 4: Africa Specialty Fertilizer Industry Revenue billion Forecast, by Export Market Analysis (Value & Volume) 2020 & 2033

- Table 5: Africa Specialty Fertilizer Industry Revenue billion Forecast, by Price Trend Analysis 2020 & 2033

- Table 6: Africa Specialty Fertilizer Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 7: Africa Specialty Fertilizer Industry Revenue billion Forecast, by Production Analysis 2020 & 2033

- Table 8: Africa Specialty Fertilizer Industry Revenue billion Forecast, by Consumption Analysis 2020 & 2033

- Table 9: Africa Specialty Fertilizer Industry Revenue billion Forecast, by Import Market Analysis (Value & Volume) 2020 & 2033

- Table 10: Africa Specialty Fertilizer Industry Revenue billion Forecast, by Export Market Analysis (Value & Volume) 2020 & 2033

- Table 11: Africa Specialty Fertilizer Industry Revenue billion Forecast, by Price Trend Analysis 2020 & 2033

- Table 12: Africa Specialty Fertilizer Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Nigeria Africa Specialty Fertilizer Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: South Africa Africa Specialty Fertilizer Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Egypt Africa Specialty Fertilizer Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Kenya Africa Specialty Fertilizer Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 17: Ethiopia Africa Specialty Fertilizer Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Morocco Africa Specialty Fertilizer Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: Ghana Africa Specialty Fertilizer Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Algeria Africa Specialty Fertilizer Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: Tanzania Africa Specialty Fertilizer Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Ivory Coast Africa Specialty Fertilizer Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Africa Specialty Fertilizer Industry?

The projected CAGR is approximately 6.65%.

2. Which companies are prominent players in the Africa Specialty Fertilizer Industry?

Key companies in the market include Haifa Group, Gavilon South Africa (MacroSource LLC), K+S Aktiengesellschaft, Yara International AS, UPL Limited, ICL Group Ltd, Kynoch Fertilizer.

3. What are the main segments of the Africa Specialty Fertilizer Industry?

The market segments include Production Analysis, Consumption Analysis, Import Market Analysis (Value & Volume), Export Market Analysis (Value & Volume), Price Trend Analysis.

4. Can you provide details about the market size?

The market size is estimated to be USD 4.93 billion as of 2022.

5. What are some drivers contributing to market growth?

Need for Custom Product Development; Use of CROs for Regulatory Services.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

Data and Cyber Security Concerns; Lack of Experts and Professionals in this Industry.

8. Can you provide examples of recent developments in the market?

April 2023: K+S acquired a 75% share of the fertilizer business of a South African trading company, Industrial Commodities Holdings (Pty) Ltd (ICH). In addition to expanding the core business, K+S is strengthening its operations in southern and eastern Africa as a result of this acquisition. The newly acquired fertilizer business in the future is to be operated in a joint venture under the name of FertivPty Ltd.April 2019: Kynoch announced Mergers & Acquisitions of Profert Fertilizer a major role player in the granular and liquid fertilizer industry. This transaction will give Kynoch access to new markets and additional production resources, ultimately contributing to their motto of enhancing efficiency through innovation.March 2019: Kynoch Fertilizer, a leading plant nutrient producer and distributor, announced the Mergers & Acquisitions of Sidi Parani to build a substantial position in the fertilizer market in South Africa and Africa.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Africa Specialty Fertilizer Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Africa Specialty Fertilizer Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Africa Specialty Fertilizer Industry?

To stay informed about further developments, trends, and reports in the Africa Specialty Fertilizer Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence