Key Insights

The global forage seeds market is projected to reach $14.6 billion by 2025, driven by a CAGR of 9.8% through 2033. This growth is fueled by rising global demand for livestock products, necessitating improved animal nutrition and pasture management. Key drivers include the adoption of advanced breeding technologies, such as herbicide-tolerant hybrids, offering higher yields, disease resistance, and enhanced nutritional content. The expanding dairy and beef industries, particularly in emerging economies, are creating substantial demand for high-quality forage crops like alfalfa, forage corn, and forage sorghum. Increased farmer awareness of the economic benefits of superior seed varieties for livestock productivity and reduced feed costs is also a significant catalyst. Technological advancements in seed production and genetic research are continuously introducing more resilient and productive forage varieties, stimulating market penetration.

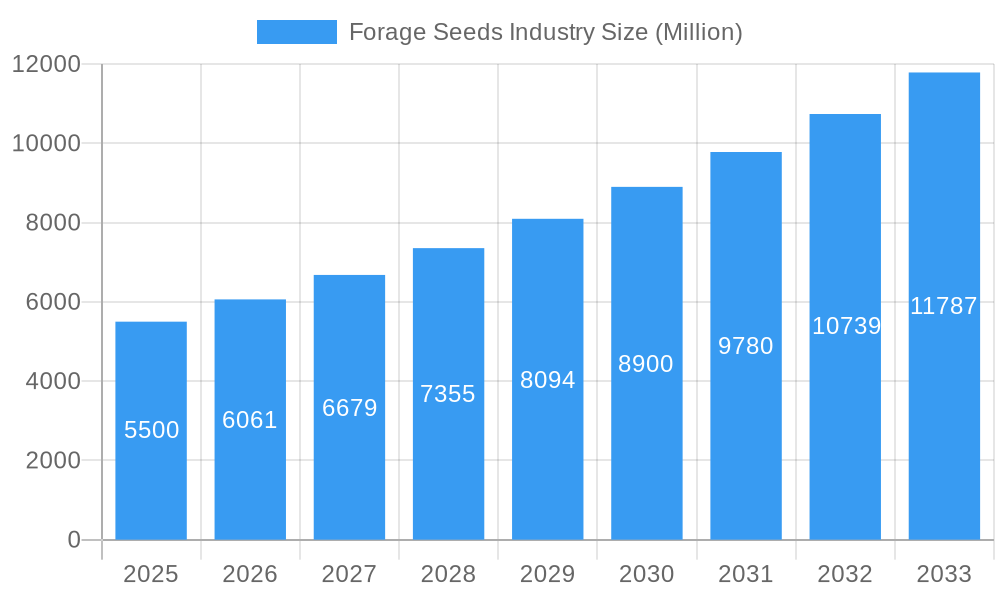

Forage Seeds Industry Market Size (In Billion)

Evolving agricultural practices and a focus on sustainable farming are shaping market trajectory. Innovations in hybrid development, including non-transgenic hybrids and hybrid derivatives, cater to diverse farmer preferences and regulatory environments. Potential restraints include price volatility of conventional feed ingredients, initial investment costs for new seed technologies, and traditional farming methods in certain regions. However, the trend towards precision agriculture and the integration of digital tools in farm management are expected to mitigate these challenges. Key players are investing in R&D to introduce novel forage seed varieties, expand product portfolios, and strengthen global distribution networks.

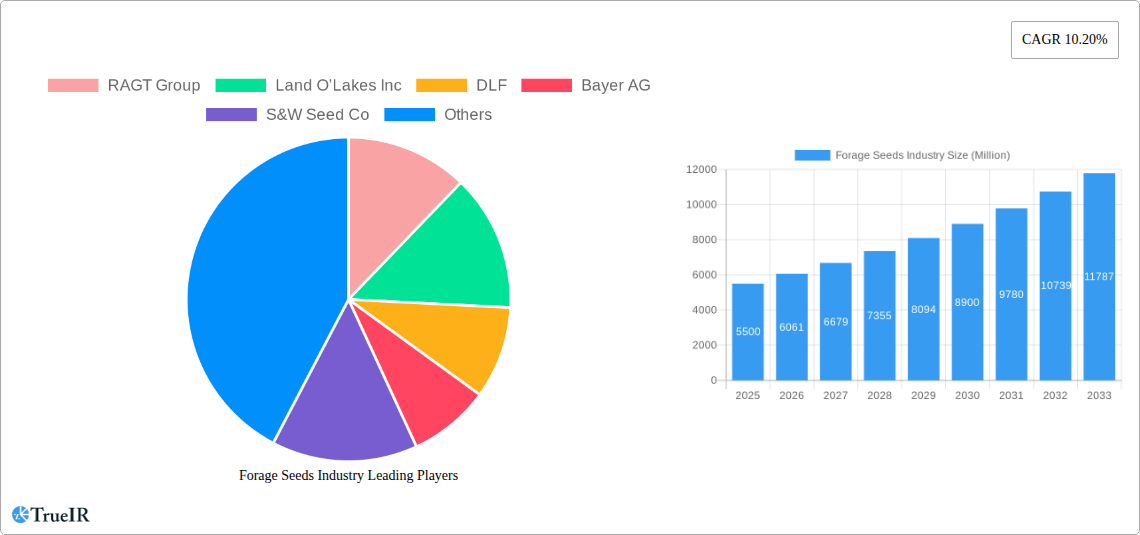

Forage Seeds Industry Company Market Share

This in-depth report provides a dynamic, SEO-optimized analysis of the global forage seeds industry. Leveraging high-volume keywords such as "forage seeds market," "grass seed," "alfalfa seeds," "forage corn," "seed breeding technology," and "agricultural seeds," this report offers critical insights for stakeholders, including farmers, seed manufacturers, distributors, and investors. The study covers a comprehensive period from 2019 to 2033, with a base year of 2025 and a detailed forecast period of 2025–2033, building upon historical data from 2019–2024. Gain a competitive edge with detailed market segmentation, trend analysis, and strategic recommendations.

Forage Seeds Industry Market Structure & Competitive Landscape

The global forage seeds industry is characterized by a moderately concentrated market structure, with a few key players dominating significant market share. The industry's growth is propelled by continuous innovation in breeding technologies, including advancements in hybrid development and the cultivation of high-yield, resilient varieties. Regulatory frameworks surrounding seed production, import/export, and intellectual property rights significantly influence market dynamics, creating both opportunities and barriers for new entrants. Product substitutes, such as alternative feed sources or synthetic feed additives, exert some pressure, but the inherent nutritional and economic benefits of high-quality forage seeds maintain their strong market position. End-user segmentation reveals a strong reliance on the livestock and dairy sectors, with poultry and equine segments also contributing to demand. Mergers and acquisitions (M&A) are a recurring theme, as larger companies seek to consolidate market share, acquire new technologies, and expand their geographical reach. For instance, the acquisition of Watson Group by Barenbrug highlights ongoing consolidation in the grass seed market. This dynamic landscape necessitates continuous strategic adaptation and investment in research and development to maintain a competitive edge. The presence of established players like RAGT Group, Land O’Lakes Inc., DLF, and Bayer AG underscores the competitive intensity, driving innovation and strategic partnerships to capture market share.

Forage Seeds Industry Market Trends & Opportunities

The forage seeds industry is poised for substantial growth, with an estimated market size exceeding $30,000 Million by 2025 and projected to reach $45,000 Million by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of approximately 5.5% during the forecast period. This growth is fueled by several key trends: the increasing global demand for animal protein, necessitating higher livestock productivity, which in turn drives the need for superior quality forage for animal feed. Technological advancements in seed breeding, particularly in developing climate-resilient and high-yield varieties, are a significant market driver. The adoption of advanced breeding techniques, including marker-assisted selection and genetic engineering (where permissible and adopted), allows for the development of forage crops with enhanced nutritional value, disease resistance, and drought tolerance, directly addressing the challenges posed by changing climate patterns. Consumer preferences for sustainably produced animal products also influence the demand for high-quality forage that supports animal health and reduces the environmental footprint of livestock farming.

Furthermore, the expansion of agricultural land, coupled with intensification efforts in existing farming regions, particularly in developing economies, presents significant market penetration opportunities. The growing awareness among farmers regarding the economic benefits of improved forage varieties—such as increased milk production, faster weight gain in livestock, and reduced reliance on expensive supplementary feeds—is a critical factor. Government initiatives promoting sustainable agriculture and animal husbandry practices also contribute to market expansion. The industry is witnessing a shift towards specialized forage solutions tailored to specific regional climates, soil types, and livestock requirements. For example, the development of drought-tolerant varieties like the GT07 phalaris by PGG Wrightson Seeds (DLF) in Australia exemplifies this trend, directly addressing regional climate challenges and market potential.

The global expansion of dairy and beef production, particularly in Asia-Pacific and Latin America, is a major growth catalyst. As these regions experience rising disposable incomes and an increased demand for animal protein, the need for efficient and high-yield forage production intensifies. This creates substantial opportunities for seed companies to introduce advanced forage genetics and tailored solutions. The increasing focus on sustainable agriculture and the reduction of greenhouse gas emissions associated with livestock farming further drive the demand for forage varieties that improve animal digestion and nutrient utilization. Investments in research and development by leading companies are crucial for capitalizing on these trends, with a strong emphasis on developing genetically superior seeds that offer improved performance and environmental benefits. The market penetration rate for advanced forage seeds is expected to rise as farmers recognize the long-term economic advantages and the role of superior forage in achieving sustainable agricultural practices. The ongoing consolidation within the industry, evidenced by strategic acquisitions, indicates a maturing market where innovation and market access are paramount for sustained success.

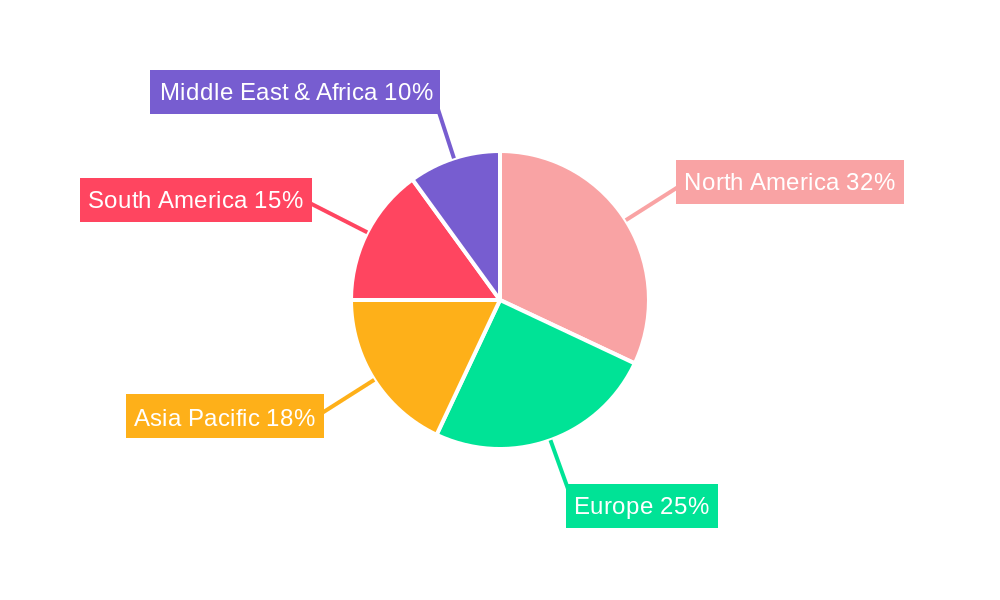

Dominant Markets & Segments in Forage Seeds Industry

The forage seeds industry exhibits distinct regional dominance and segment performance, driven by agricultural practices, economic development, and environmental factors.

Dominant Regions and Countries:

- North America: This region, particularly the United States and Canada, remains a dominant market for forage seeds. Its established dairy and beef industries, coupled with significant investments in agricultural research and development, fuel a consistent demand for high-quality forage crops. The region’s advanced farming techniques and emphasis on productivity make it a key market for innovative seed varieties.

- Europe: European countries, with their strong agricultural sectors and increasing focus on sustainable farming, represent another significant market. The demand for improved forage for dairy herds and beef cattle is robust. Government policies promoting environmental stewardship and efficient land use further support the market.

- Asia-Pacific: This region is emerging as a high-growth market, driven by the expanding livestock populations and increasing demand for animal protein. Countries like China, India, and Australia are witnessing substantial growth in forage seed consumption as agricultural practices modernize. The development of climate-resilient varieties, such as the GT07 phalaris in Australia, is crucial for this region's specific needs.

- Latin America: Similar to Asia-Pacific, Latin America's burgeoning livestock industry, particularly in Brazil and Argentina, is a key driver of forage seed demand. The vast agricultural land available and the increasing adoption of improved farming techniques contribute to market expansion.

Dominant Segments:

- Breeding Technology: Hybrids (Non-Transgenic Hybrids, Herbicide Tolerant Hybrids, Other Traits)

- Non-Transgenic Hybrids: These varieties are highly sought after for their enhanced yield, vigor, and uniformity, offering significant advantages over open-pollinated varieties without the complexities of genetically modified organisms.

- Herbicide Tolerant Hybrids: The development of herbicide-tolerant forage crops allows for more effective weed management, leading to reduced competition for nutrients and water, thus boosting crop yields and quality. This segment is crucial for large-scale agricultural operations.

- Other Traits: Innovations in breeding for traits such as enhanced nutritional content (protein, digestible fiber), disease resistance, pest resistance, and improved palatability are critical growth drivers within the hybrid segment.

- Crop: Alfalfa

- Alfalfa is a cornerstone of the forage industry due to its high protein content, nutritional value, and ability to improve soil fertility. Its adaptability to various climates and its perennial nature make it a valuable crop for sustainable livestock farming. The demand for high-quality alfalfa for dairy cows and beef cattle is consistently strong.

- Crop: Forage Corn

- Forage corn is a vital feed source for livestock, particularly for dairy cows, due to its high energy content. Advancements in breeding have led to varieties with increased yield, starch content, and digestibility, making it a highly efficient feed option.

- Crop: Forage Sorghum

- Forage sorghum is increasingly favored in regions with drier climates or for summer grazing due to its drought tolerance and rapid regrowth capabilities. Its versatility and adaptability make it a critical component of diverse feeding strategies.

- Open Pollinated Varieties & Hybrid Derivatives: While hybrid seeds often lead in performance, open-pollinated varieties and their derivatives continue to hold a significant market share, especially in regions where cost-effectiveness is a primary consideration or for specific niche applications. Breeding efforts continue to improve these varieties, offering a balance of performance and accessibility.

The market dominance in forage seeds is a complex interplay of regional agricultural strengths, technological adoption, and the specific needs of livestock industries. The continuous refinement of breeding technologies and the development of specialized crop varieties are key to capturing market share across these diverse segments.

Forage Seeds Industry Product Analysis

The forage seeds industry is characterized by a continuous stream of product innovations designed to enhance yield, nutritional value, and environmental resilience. Hybrid seed technologies, including non-transgenic, herbicide-tolerant, and other trait-specific varieties, offer significant competitive advantages by providing farmers with crops exhibiting superior performance, disease resistance, and improved adaptability to varied climatic conditions. Alfalfa, forage corn, and forage sorghum remain central, with ongoing breeding efforts focused on increasing protein content, energy density, and digestibility. Innovations extend to developing seeds that require fewer inputs, such as water and fertilizer, aligning with sustainable agricultural practices. The competitive advantage for seed companies lies in their ability to consistently deliver high-performing, reliable, and locally adapted forage solutions that directly address the evolving needs of the global livestock sector.

Key Drivers, Barriers & Challenges in Forage Seeds Industry

Key Drivers:

- Growing Global Demand for Animal Protein: The increasing world population and rising disposable incomes are escalating the demand for meat and dairy products, directly boosting the need for high-quality animal feed, hence forage seeds.

- Technological Advancements in Seed Breeding: Innovations in genetic selection, hybridization, and biotechnology are leading to the development of higher-yielding, more resilient, and nutritionally superior forage varieties, driving adoption.

- Focus on Sustainable Agriculture: The push for environmentally friendly farming practices favors forage varieties that improve soil health, reduce water usage, and require fewer chemical inputs, offering a competitive edge.

- Government Support and Policies: Favorable agricultural policies, subsidies for improved seed adoption, and initiatives promoting livestock productivity can significantly stimulate market growth.

Barriers & Challenges:

- Climate Change and Environmental Uncertainty: Unpredictable weather patterns, including droughts and extreme temperatures, pose a significant risk to crop yields, impacting seed demand and performance, requiring continuous adaptation in breeding programs.

- Regulatory Hurdles and Seed Certification: Stringent regulations regarding seed quality, testing, and certification across different countries can create complexity and increase market entry costs for new products and companies.

- High Research and Development Costs: Developing and bringing new, superior forage seed varieties to market requires substantial and ongoing investment in research, development, and field trials, posing a barrier for smaller players.

- Pest and Disease Outbreaks: The susceptibility of certain forage crops to specific pests and diseases can lead to crop failures, impacting farmer confidence and potentially reducing demand for affected seed types, demanding robust disease resistance traits.

- Price Volatility of Agricultural Commodities: Fluctuations in the prices of grains and other feed inputs can influence farmer purchasing decisions for forage seeds, creating market instability.

Growth Drivers in the Forage Seeds Industry Market

The forage seeds industry's growth is primarily propelled by the surging global demand for animal protein, necessitating enhanced livestock productivity through superior feed. Technological advancements in seed breeding, particularly the development of hybrids with improved yield, nutritional content, and resilience to biotic and abiotic stresses, are pivotal. Government initiatives promoting efficient agriculture, sustainable farming practices, and support for livestock sectors further catalyze market expansion. The increasing adoption of precision agriculture techniques also creates demand for genetically uniform and high-performing seeds. Economic growth in emerging markets is driving the expansion of dairy and beef industries, thereby increasing the consumption of forage seeds.

Challenges Impacting Forage Seeds Industry Growth

Challenges impacting the forage seeds industry include the pervasive effects of climate change, leading to unpredictable weather patterns that threaten crop yields and necessitate continuous adaptation in breeding. Stringent and varied regulatory environments for seed production and trade across different countries can create significant hurdles. High research and development costs associated with creating novel seed varieties represent a substantial financial barrier. Furthermore, the potential for pest and disease outbreaks can disrupt supply chains and negatively impact farmer confidence, demanding robust resistance traits in new seed developments. Fluctuations in the prices of agricultural commodities can also influence farmer investment in high-quality forage seeds.

Key Players Shaping the Forage Seeds Industry Market

- RAGT Group

- Land O’Lakes Inc.

- DLF

- Bayer AG

- S&W Seed Co

- Royal Barenbrug Group

- KWS SAAT SE & Co KGaA

- Advanta Seeds - UPL

- Ampac Seed Company

- Corteva Agriscience

Significant Forage Seeds Industry Industry Milestones

- March 2023: PGG Wrightson Seeds, a subsidiary of DLF, successfully developed the new GT07 phalaris variety. This variety exhibits greater persistence and market potential, particularly under Australia's changing climate conditions. The development of GT07 was made possible through collaboration with CSIRO's breeding program.

- March 2023: Barenbrug entered an agreement to acquire the UK seed specialist Watson Group, which is expected to enable Barenbrug to continue growing in the grass-seed marketplace in the United Kingdom.

- March 2023: DLF expanded its presence in New Zealand by opening a new seed processing and storage facility. This strategic investment aims to enhance seed processing capabilities and improve storage capacity in the country, allowing DLF to better serve the agricultural sector and meet the growing demand for high-quality seeds in New Zealand.

Future Outlook for Forage Seeds Industry Market

The future outlook for the forage seeds industry is robust, driven by increasing global demand for animal protein and a growing emphasis on sustainable agriculture. Continued innovation in breeding technologies, focusing on climate resilience, enhanced nutritional content, and reduced environmental impact, will be key growth catalysts. Strategic partnerships and consolidations are expected to continue, shaping a more competitive landscape. Emerging markets in Asia-Pacific and Latin America present significant opportunities for market penetration. The industry is well-positioned to meet the evolving needs of livestock producers worldwide, offering solutions that enhance productivity, profitability, and environmental stewardship. Investments in research and development for disease resistance and drought tolerance will be critical for sustained growth and market leadership.

Forage Seeds Industry Segmentation

-

1. Breeding Technology

-

1.1. Hybrids

- 1.1.1. Non-Transgenic Hybrids

- 1.1.2. Herbicide Tolerant Hybrids

- 1.1.3. Other Traits

- 1.2. Open Pollinated Varieties & Hybrid Derivatives

-

1.1. Hybrids

-

2. Crop

- 2.1. Alfalfa

- 2.2. Forage Corn

- 2.3. Forage Sorghum

- 2.4. Other Forage Crops

-

3. Breeding Technology

-

3.1. Hybrids

- 3.1.1. Non-Transgenic Hybrids

- 3.1.2. Herbicide Tolerant Hybrids

- 3.1.3. Other Traits

- 3.2. Open Pollinated Varieties & Hybrid Derivatives

-

3.1. Hybrids

-

4. Crop

- 4.1. Alfalfa

- 4.2. Forage Corn

- 4.3. Forage Sorghum

- 4.4. Other Forage Crops

Forage Seeds Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Forage Seeds Industry Regional Market Share

Geographic Coverage of Forage Seeds Industry

Forage Seeds Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Breeding Technology

- 5.1.1. Hybrids

- 5.1.1.1. Non-Transgenic Hybrids

- 5.1.1.2. Herbicide Tolerant Hybrids

- 5.1.1.3. Other Traits

- 5.1.2. Open Pollinated Varieties & Hybrid Derivatives

- 5.1.1. Hybrids

- 5.2. Market Analysis, Insights and Forecast - by Crop

- 5.2.1. Alfalfa

- 5.2.2. Forage Corn

- 5.2.3. Forage Sorghum

- 5.2.4. Other Forage Crops

- 5.3. Market Analysis, Insights and Forecast - by Breeding Technology

- 5.3.1. Hybrids

- 5.3.1.1. Non-Transgenic Hybrids

- 5.3.1.2. Herbicide Tolerant Hybrids

- 5.3.1.3. Other Traits

- 5.3.2. Open Pollinated Varieties & Hybrid Derivatives

- 5.3.1. Hybrids

- 5.4. Market Analysis, Insights and Forecast - by Crop

- 5.4.1. Alfalfa

- 5.4.2. Forage Corn

- 5.4.3. Forage Sorghum

- 5.4.4. Other Forage Crops

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. North America

- 5.5.2. South America

- 5.5.3. Europe

- 5.5.4. Middle East & Africa

- 5.5.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Breeding Technology

- 6. Global Forage Seeds Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Breeding Technology

- 6.1.1. Hybrids

- 6.1.1.1. Non-Transgenic Hybrids

- 6.1.1.2. Herbicide Tolerant Hybrids

- 6.1.1.3. Other Traits

- 6.1.2. Open Pollinated Varieties & Hybrid Derivatives

- 6.1.1. Hybrids

- 6.2. Market Analysis, Insights and Forecast - by Crop

- 6.2.1. Alfalfa

- 6.2.2. Forage Corn

- 6.2.3. Forage Sorghum

- 6.2.4. Other Forage Crops

- 6.3. Market Analysis, Insights and Forecast - by Breeding Technology

- 6.3.1. Hybrids

- 6.3.1.1. Non-Transgenic Hybrids

- 6.3.1.2. Herbicide Tolerant Hybrids

- 6.3.1.3. Other Traits

- 6.3.2. Open Pollinated Varieties & Hybrid Derivatives

- 6.3.1. Hybrids

- 6.4. Market Analysis, Insights and Forecast - by Crop

- 6.4.1. Alfalfa

- 6.4.2. Forage Corn

- 6.4.3. Forage Sorghum

- 6.4.4. Other Forage Crops

- 6.1. Market Analysis, Insights and Forecast - by Breeding Technology

- 7. North America Forage Seeds Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Breeding Technology

- 7.1.1. Hybrids

- 7.1.1.1. Non-Transgenic Hybrids

- 7.1.1.2. Herbicide Tolerant Hybrids

- 7.1.1.3. Other Traits

- 7.1.2. Open Pollinated Varieties & Hybrid Derivatives

- 7.1.1. Hybrids

- 7.2. Market Analysis, Insights and Forecast - by Crop

- 7.2.1. Alfalfa

- 7.2.2. Forage Corn

- 7.2.3. Forage Sorghum

- 7.2.4. Other Forage Crops

- 7.3. Market Analysis, Insights and Forecast - by Breeding Technology

- 7.3.1. Hybrids

- 7.3.1.1. Non-Transgenic Hybrids

- 7.3.1.2. Herbicide Tolerant Hybrids

- 7.3.1.3. Other Traits

- 7.3.2. Open Pollinated Varieties & Hybrid Derivatives

- 7.3.1. Hybrids

- 7.4. Market Analysis, Insights and Forecast - by Crop

- 7.4.1. Alfalfa

- 7.4.2. Forage Corn

- 7.4.3. Forage Sorghum

- 7.4.4. Other Forage Crops

- 7.1. Market Analysis, Insights and Forecast - by Breeding Technology

- 8. South America Forage Seeds Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Breeding Technology

- 8.1.1. Hybrids

- 8.1.1.1. Non-Transgenic Hybrids

- 8.1.1.2. Herbicide Tolerant Hybrids

- 8.1.1.3. Other Traits

- 8.1.2. Open Pollinated Varieties & Hybrid Derivatives

- 8.1.1. Hybrids

- 8.2. Market Analysis, Insights and Forecast - by Crop

- 8.2.1. Alfalfa

- 8.2.2. Forage Corn

- 8.2.3. Forage Sorghum

- 8.2.4. Other Forage Crops

- 8.3. Market Analysis, Insights and Forecast - by Breeding Technology

- 8.3.1. Hybrids

- 8.3.1.1. Non-Transgenic Hybrids

- 8.3.1.2. Herbicide Tolerant Hybrids

- 8.3.1.3. Other Traits

- 8.3.2. Open Pollinated Varieties & Hybrid Derivatives

- 8.3.1. Hybrids

- 8.4. Market Analysis, Insights and Forecast - by Crop

- 8.4.1. Alfalfa

- 8.4.2. Forage Corn

- 8.4.3. Forage Sorghum

- 8.4.4. Other Forage Crops

- 8.1. Market Analysis, Insights and Forecast - by Breeding Technology

- 9. Europe Forage Seeds Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Breeding Technology

- 9.1.1. Hybrids

- 9.1.1.1. Non-Transgenic Hybrids

- 9.1.1.2. Herbicide Tolerant Hybrids

- 9.1.1.3. Other Traits

- 9.1.2. Open Pollinated Varieties & Hybrid Derivatives

- 9.1.1. Hybrids

- 9.2. Market Analysis, Insights and Forecast - by Crop

- 9.2.1. Alfalfa

- 9.2.2. Forage Corn

- 9.2.3. Forage Sorghum

- 9.2.4. Other Forage Crops

- 9.3. Market Analysis, Insights and Forecast - by Breeding Technology

- 9.3.1. Hybrids

- 9.3.1.1. Non-Transgenic Hybrids

- 9.3.1.2. Herbicide Tolerant Hybrids

- 9.3.1.3. Other Traits

- 9.3.2. Open Pollinated Varieties & Hybrid Derivatives

- 9.3.1. Hybrids

- 9.4. Market Analysis, Insights and Forecast - by Crop

- 9.4.1. Alfalfa

- 9.4.2. Forage Corn

- 9.4.3. Forage Sorghum

- 9.4.4. Other Forage Crops

- 9.1. Market Analysis, Insights and Forecast - by Breeding Technology

- 10. Middle East & Africa Forage Seeds Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Breeding Technology

- 10.1.1. Hybrids

- 10.1.1.1. Non-Transgenic Hybrids

- 10.1.1.2. Herbicide Tolerant Hybrids

- 10.1.1.3. Other Traits

- 10.1.2. Open Pollinated Varieties & Hybrid Derivatives

- 10.1.1. Hybrids

- 10.2. Market Analysis, Insights and Forecast - by Crop

- 10.2.1. Alfalfa

- 10.2.2. Forage Corn

- 10.2.3. Forage Sorghum

- 10.2.4. Other Forage Crops

- 10.3. Market Analysis, Insights and Forecast - by Breeding Technology

- 10.3.1. Hybrids

- 10.3.1.1. Non-Transgenic Hybrids

- 10.3.1.2. Herbicide Tolerant Hybrids

- 10.3.1.3. Other Traits

- 10.3.2. Open Pollinated Varieties & Hybrid Derivatives

- 10.3.1. Hybrids

- 10.4. Market Analysis, Insights and Forecast - by Crop

- 10.4.1. Alfalfa

- 10.4.2. Forage Corn

- 10.4.3. Forage Sorghum

- 10.4.4. Other Forage Crops

- 10.1. Market Analysis, Insights and Forecast - by Breeding Technology

- 11. Asia Pacific Forage Seeds Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Breeding Technology

- 11.1.1. Hybrids

- 11.1.1.1. Non-Transgenic Hybrids

- 11.1.1.2. Herbicide Tolerant Hybrids

- 11.1.1.3. Other Traits

- 11.1.2. Open Pollinated Varieties & Hybrid Derivatives

- 11.1.1. Hybrids

- 11.2. Market Analysis, Insights and Forecast - by Crop

- 11.2.1. Alfalfa

- 11.2.2. Forage Corn

- 11.2.3. Forage Sorghum

- 11.2.4. Other Forage Crops

- 11.3. Market Analysis, Insights and Forecast - by Breeding Technology

- 11.3.1. Hybrids

- 11.3.1.1. Non-Transgenic Hybrids

- 11.3.1.2. Herbicide Tolerant Hybrids

- 11.3.1.3. Other Traits

- 11.3.2. Open Pollinated Varieties & Hybrid Derivatives

- 11.3.1. Hybrids

- 11.4. Market Analysis, Insights and Forecast - by Crop

- 11.4.1. Alfalfa

- 11.4.2. Forage Corn

- 11.4.3. Forage Sorghum

- 11.4.4. Other Forage Crops

- 11.1. Market Analysis, Insights and Forecast - by Breeding Technology

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 RAGT Group

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Land O’Lakes Inc

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 DLF

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Bayer AG

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 S&W Seed Co

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Royal Barenbrug Group

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 KWS SAAT SE & Co KGaA

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Advanta Seeds - UPL

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Ampac Seed Company

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Corteva Agriscience

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 RAGT Group

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Forage Seeds Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Forage Seeds Industry Revenue (billion), by Breeding Technology 2025 & 2033

- Figure 3: North America Forage Seeds Industry Revenue Share (%), by Breeding Technology 2025 & 2033

- Figure 4: North America Forage Seeds Industry Revenue (billion), by Crop 2025 & 2033

- Figure 5: North America Forage Seeds Industry Revenue Share (%), by Crop 2025 & 2033

- Figure 6: North America Forage Seeds Industry Revenue (billion), by Breeding Technology 2025 & 2033

- Figure 7: North America Forage Seeds Industry Revenue Share (%), by Breeding Technology 2025 & 2033

- Figure 8: North America Forage Seeds Industry Revenue (billion), by Crop 2025 & 2033

- Figure 9: North America Forage Seeds Industry Revenue Share (%), by Crop 2025 & 2033

- Figure 10: North America Forage Seeds Industry Revenue (billion), by Country 2025 & 2033

- Figure 11: North America Forage Seeds Industry Revenue Share (%), by Country 2025 & 2033

- Figure 12: South America Forage Seeds Industry Revenue (billion), by Breeding Technology 2025 & 2033

- Figure 13: South America Forage Seeds Industry Revenue Share (%), by Breeding Technology 2025 & 2033

- Figure 14: South America Forage Seeds Industry Revenue (billion), by Crop 2025 & 2033

- Figure 15: South America Forage Seeds Industry Revenue Share (%), by Crop 2025 & 2033

- Figure 16: South America Forage Seeds Industry Revenue (billion), by Breeding Technology 2025 & 2033

- Figure 17: South America Forage Seeds Industry Revenue Share (%), by Breeding Technology 2025 & 2033

- Figure 18: South America Forage Seeds Industry Revenue (billion), by Crop 2025 & 2033

- Figure 19: South America Forage Seeds Industry Revenue Share (%), by Crop 2025 & 2033

- Figure 20: South America Forage Seeds Industry Revenue (billion), by Country 2025 & 2033

- Figure 21: South America Forage Seeds Industry Revenue Share (%), by Country 2025 & 2033

- Figure 22: Europe Forage Seeds Industry Revenue (billion), by Breeding Technology 2025 & 2033

- Figure 23: Europe Forage Seeds Industry Revenue Share (%), by Breeding Technology 2025 & 2033

- Figure 24: Europe Forage Seeds Industry Revenue (billion), by Crop 2025 & 2033

- Figure 25: Europe Forage Seeds Industry Revenue Share (%), by Crop 2025 & 2033

- Figure 26: Europe Forage Seeds Industry Revenue (billion), by Breeding Technology 2025 & 2033

- Figure 27: Europe Forage Seeds Industry Revenue Share (%), by Breeding Technology 2025 & 2033

- Figure 28: Europe Forage Seeds Industry Revenue (billion), by Crop 2025 & 2033

- Figure 29: Europe Forage Seeds Industry Revenue Share (%), by Crop 2025 & 2033

- Figure 30: Europe Forage Seeds Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: Europe Forage Seeds Industry Revenue Share (%), by Country 2025 & 2033

- Figure 32: Middle East & Africa Forage Seeds Industry Revenue (billion), by Breeding Technology 2025 & 2033

- Figure 33: Middle East & Africa Forage Seeds Industry Revenue Share (%), by Breeding Technology 2025 & 2033

- Figure 34: Middle East & Africa Forage Seeds Industry Revenue (billion), by Crop 2025 & 2033

- Figure 35: Middle East & Africa Forage Seeds Industry Revenue Share (%), by Crop 2025 & 2033

- Figure 36: Middle East & Africa Forage Seeds Industry Revenue (billion), by Breeding Technology 2025 & 2033

- Figure 37: Middle East & Africa Forage Seeds Industry Revenue Share (%), by Breeding Technology 2025 & 2033

- Figure 38: Middle East & Africa Forage Seeds Industry Revenue (billion), by Crop 2025 & 2033

- Figure 39: Middle East & Africa Forage Seeds Industry Revenue Share (%), by Crop 2025 & 2033

- Figure 40: Middle East & Africa Forage Seeds Industry Revenue (billion), by Country 2025 & 2033

- Figure 41: Middle East & Africa Forage Seeds Industry Revenue Share (%), by Country 2025 & 2033

- Figure 42: Asia Pacific Forage Seeds Industry Revenue (billion), by Breeding Technology 2025 & 2033

- Figure 43: Asia Pacific Forage Seeds Industry Revenue Share (%), by Breeding Technology 2025 & 2033

- Figure 44: Asia Pacific Forage Seeds Industry Revenue (billion), by Crop 2025 & 2033

- Figure 45: Asia Pacific Forage Seeds Industry Revenue Share (%), by Crop 2025 & 2033

- Figure 46: Asia Pacific Forage Seeds Industry Revenue (billion), by Breeding Technology 2025 & 2033

- Figure 47: Asia Pacific Forage Seeds Industry Revenue Share (%), by Breeding Technology 2025 & 2033

- Figure 48: Asia Pacific Forage Seeds Industry Revenue (billion), by Crop 2025 & 2033

- Figure 49: Asia Pacific Forage Seeds Industry Revenue Share (%), by Crop 2025 & 2033

- Figure 50: Asia Pacific Forage Seeds Industry Revenue (billion), by Country 2025 & 2033

- Figure 51: Asia Pacific Forage Seeds Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Forage Seeds Industry Revenue billion Forecast, by Breeding Technology 2020 & 2033

- Table 2: Global Forage Seeds Industry Revenue billion Forecast, by Crop 2020 & 2033

- Table 3: Global Forage Seeds Industry Revenue billion Forecast, by Breeding Technology 2020 & 2033

- Table 4: Global Forage Seeds Industry Revenue billion Forecast, by Crop 2020 & 2033

- Table 5: Global Forage Seeds Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Global Forage Seeds Industry Revenue billion Forecast, by Breeding Technology 2020 & 2033

- Table 7: Global Forage Seeds Industry Revenue billion Forecast, by Crop 2020 & 2033

- Table 8: Global Forage Seeds Industry Revenue billion Forecast, by Breeding Technology 2020 & 2033

- Table 9: Global Forage Seeds Industry Revenue billion Forecast, by Crop 2020 & 2033

- Table 10: Global Forage Seeds Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 11: United States Forage Seeds Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Canada Forage Seeds Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Mexico Forage Seeds Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Global Forage Seeds Industry Revenue billion Forecast, by Breeding Technology 2020 & 2033

- Table 15: Global Forage Seeds Industry Revenue billion Forecast, by Crop 2020 & 2033

- Table 16: Global Forage Seeds Industry Revenue billion Forecast, by Breeding Technology 2020 & 2033

- Table 17: Global Forage Seeds Industry Revenue billion Forecast, by Crop 2020 & 2033

- Table 18: Global Forage Seeds Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 19: Brazil Forage Seeds Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Argentina Forage Seeds Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: Rest of South America Forage Seeds Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Global Forage Seeds Industry Revenue billion Forecast, by Breeding Technology 2020 & 2033

- Table 23: Global Forage Seeds Industry Revenue billion Forecast, by Crop 2020 & 2033

- Table 24: Global Forage Seeds Industry Revenue billion Forecast, by Breeding Technology 2020 & 2033

- Table 25: Global Forage Seeds Industry Revenue billion Forecast, by Crop 2020 & 2033

- Table 26: Global Forage Seeds Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 27: United Kingdom Forage Seeds Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Germany Forage Seeds Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 29: France Forage Seeds Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Italy Forage Seeds Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 31: Spain Forage Seeds Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Russia Forage Seeds Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: Benelux Forage Seeds Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: Nordics Forage Seeds Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: Rest of Europe Forage Seeds Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Global Forage Seeds Industry Revenue billion Forecast, by Breeding Technology 2020 & 2033

- Table 37: Global Forage Seeds Industry Revenue billion Forecast, by Crop 2020 & 2033

- Table 38: Global Forage Seeds Industry Revenue billion Forecast, by Breeding Technology 2020 & 2033

- Table 39: Global Forage Seeds Industry Revenue billion Forecast, by Crop 2020 & 2033

- Table 40: Global Forage Seeds Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 41: Turkey Forage Seeds Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Israel Forage Seeds Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: GCC Forage Seeds Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: North Africa Forage Seeds Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: South Africa Forage Seeds Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Middle East & Africa Forage Seeds Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 47: Global Forage Seeds Industry Revenue billion Forecast, by Breeding Technology 2020 & 2033

- Table 48: Global Forage Seeds Industry Revenue billion Forecast, by Crop 2020 & 2033

- Table 49: Global Forage Seeds Industry Revenue billion Forecast, by Breeding Technology 2020 & 2033

- Table 50: Global Forage Seeds Industry Revenue billion Forecast, by Crop 2020 & 2033

- Table 51: Global Forage Seeds Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 52: China Forage Seeds Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 53: India Forage Seeds Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 54: Japan Forage Seeds Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 55: South Korea Forage Seeds Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 56: ASEAN Forage Seeds Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 57: Oceania Forage Seeds Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 58: Rest of Asia Pacific Forage Seeds Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Forage Seeds Industry?

The projected CAGR is approximately 9.8%.

2. Which companies are prominent players in the Forage Seeds Industry?

Key companies in the market include RAGT Group, Land O’Lakes Inc, DLF, Bayer AG, S&W Seed Co, Royal Barenbrug Group, KWS SAAT SE & Co KGaA, Advanta Seeds - UPL, Ampac Seed Company, Corteva Agriscience.

3. What are the main segments of the Forage Seeds Industry?

The market segments include Breeding Technology, Crop, Breeding Technology, Crop.

4. Can you provide details about the market size?

The market size is estimated to be USD 14.6 billion as of 2022.

5. What are some drivers contributing to market growth?

Demand For Landscaping Maintenance; Adoption of Green Spaces and Green Roofs.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

Shortage of Labor In Landscaping; High Maintenance Cost of Lawn Mowers.

8. Can you provide examples of recent developments in the market?

March 2023: PGG Wrightson Seeds, a subsidiary of DLF, successfully developed the new GT07 phalaris variety. This variety exhibits greater persistence and market potential, particularly under Australia's changing climate conditions. The development of GT07 was made possible through collaboration with CSIRO's breeding program.March 2023: Barenbrug entered an agreement to acquire the UK seed specialist Watson Group, which is expected to enable Barenbrug to continue growing in the grass-seed marketplace in the United Kingdom.March 2023: DLF expanded its presence in New Zealand by opening a new seed processing and storage facility. This strategic investment aims to enhance seed processing capabilities and improve storage capacity in the country, allowing DLF to better serve the agricultural sector and meet the growing demand for high-quality seeds in New Zealand.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Forage Seeds Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Forage Seeds Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Forage Seeds Industry?

To stay informed about further developments, trends, and reports in the Forage Seeds Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence